- FIT Retirement Series

Содержание

- 2. SecurePlus Gold SecurePlus Paramount 5 SecurePlus Reliance Products of the past: One Size Fits All

- 3. More Upside Upside interest crediting potential through strategies with higher caps More Liquidity A new emergency

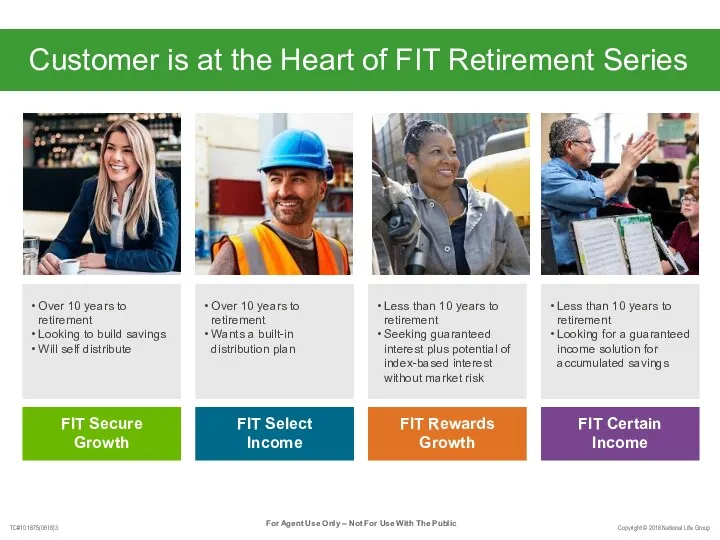

- 4. Customer is at the Heart of FIT Retirement Series Over 10 years to retirement Wants a

- 5. New Product Features

- 6. Emergency Access Waiver Active on FIT Retirement Series products currently in 403(b) or 457(b) status and

- 7. Products That Go With the Flow Regularly scheduled contributions for as little as $100 a month

- 8. Market Value Adjustment (MVA) Reduces our risk - allows us to use higher caps and pars

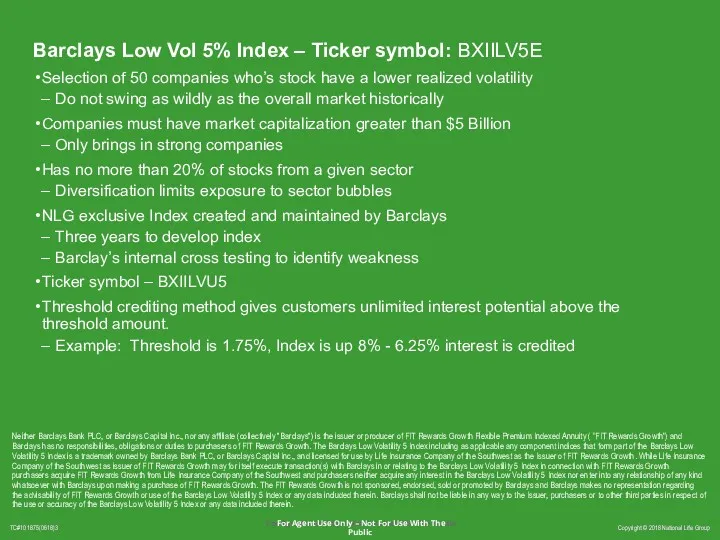

- 9. Barclays Low Vol 5% – Threshold Ticker Symbol – BXIILV5E Bank of America Merrill Lynch GPA

- 10. What is a Volatility Control Index Volatility Control Index Volatility Indexes Market Performance Lower cost, allowing

- 11. Monthly Sum Cap Monthly Cap Tracks the movement of the index on a month-to-month basis Assigns

- 12. FIT Retirement Series: Case Studies

- 13. This is Barbara Barbara has left her old job and wants to continue to build her

- 14. This is Barbara’s FIT MORE Upside potential than a bank product through: Higher caps Indices* Tax-deferred

- 15. This is Wade Wade works for a small company who does not have a 401(k). He

- 16. This is Wade’s FIT MORE Upside potential through: Higher caps Indices* Tax-deferred growth Income rider with

- 17. Market Potential GLIR with Increasing Income Withdrawal percentage for Single Life Level Option shown above; Joint

- 18. GLIR Examples Income calculation example in the 17th policy year at age 67 Multiply by Guarantee

- 19. This is Carol Carol is late saving for her post-career life and is looking to build

- 20. This is Carol’s FIT MORE Upside potential than current interest rates through: 5% immediate interest credit

- 21. This is Frank Frank has diligently saved in his 403(b) and is quickly approaching retirement. He

- 22. This is Frank’s FIT MORE Liquidity and income certainty through: Emergency Access Waiver Income rider, at

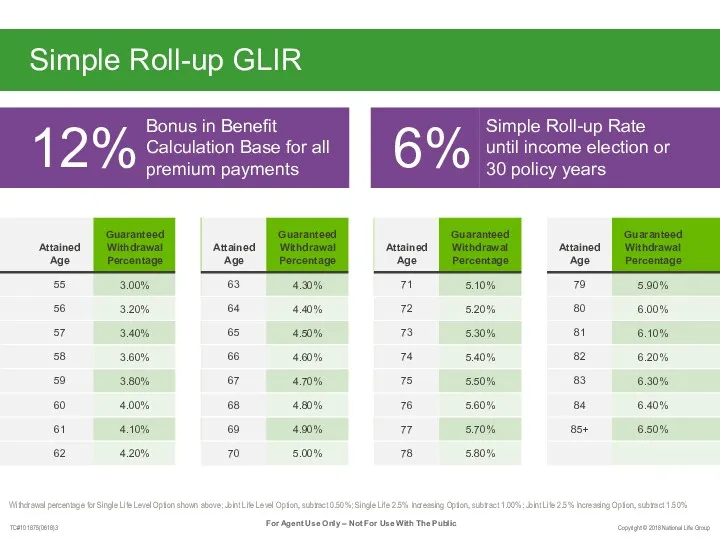

- 23. Simple Roll-up GLIR Withdrawal percentage for Single Life Level Option shown above; Joint Life Level Option,

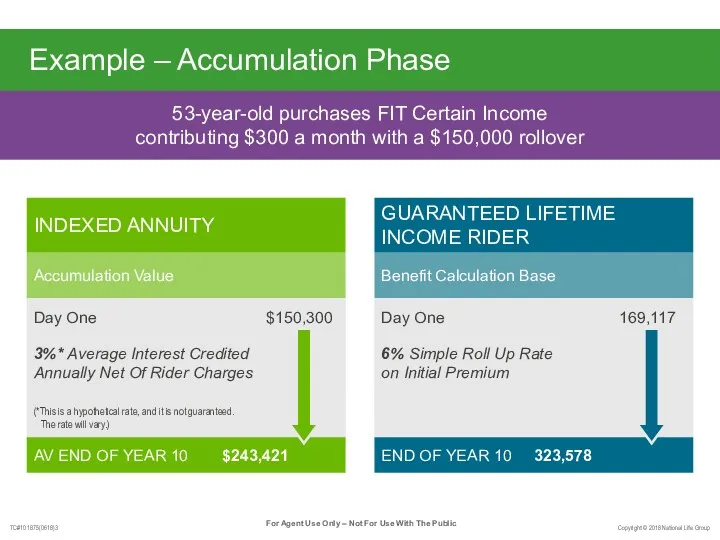

- 24. Example – Accumulation Phase 53-year-old purchases FIT Certain Income contributing $300 a month with a $150,000

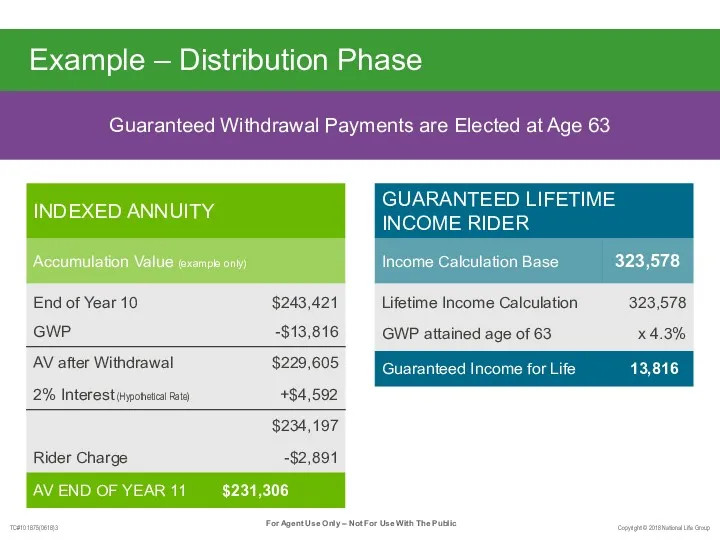

- 25. Guaranteed Withdrawal Payments are Elected at Age 63 Example – Distribution Phase GUARANTEED LIFETIME INCOME RIDER

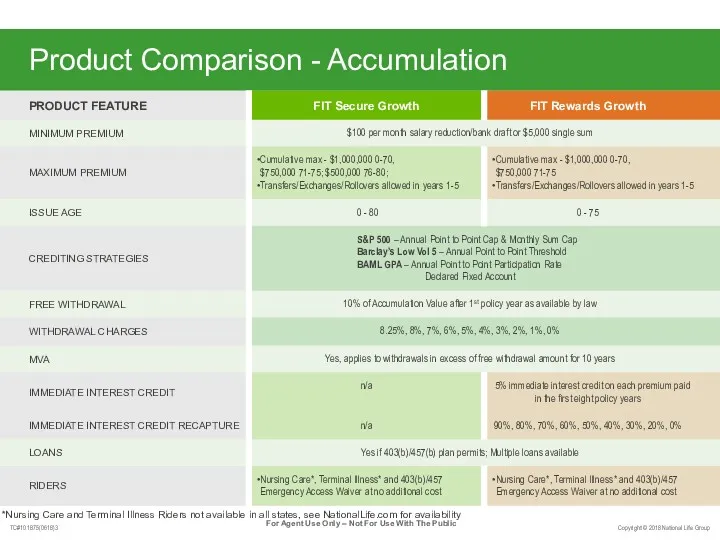

- 26. Product Comparison - Accumulation *Nursing Care and Terminal Illness Riders not available in all states, see

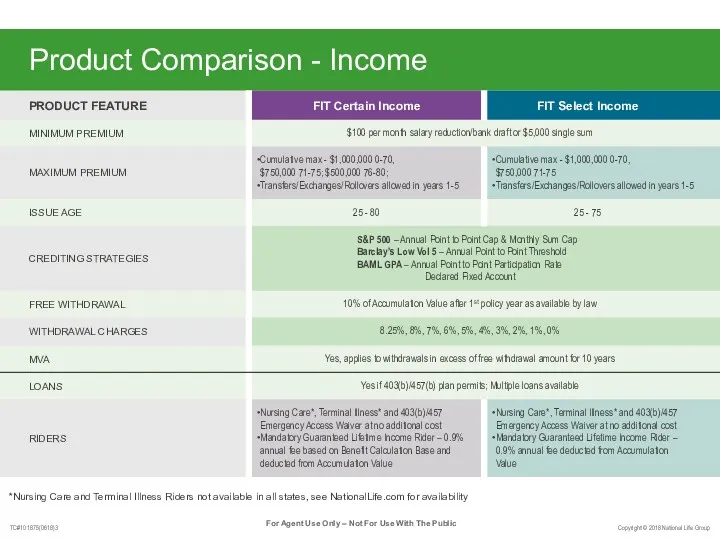

- 27. Product Comparison - Income *Nursing Care and Terminal Illness Riders not available in all states, see

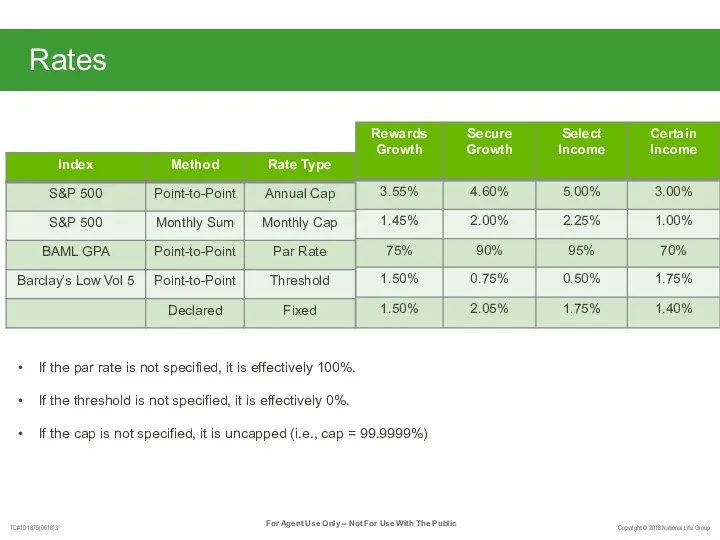

- 28. Rates If the par rate is not specified, it is effectively 100%. If the threshold is

- 29. FIT Retirement Series Illustrations FIT Certain Income and FIT Select Income in Quick Quote on Agent

- 30. Questions?

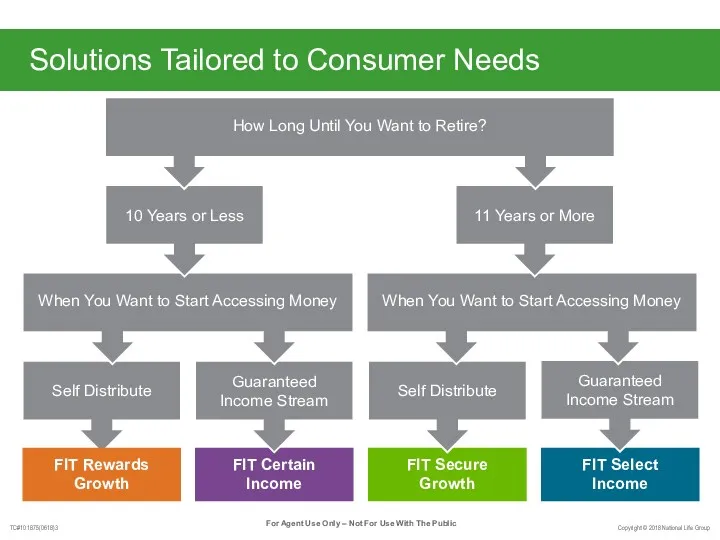

- 31. Solutions Tailored to Consumer Needs Self Distribute FIT Select Income FIT Secure Growth FIT Rewards Growth

- 32. Barclays Low Vol 5% Index – Ticker symbol: BXIILV5E Selection of 50 companies who’s stock have

- 34. Скачать презентацию

SecurePlus Gold

SecurePlus Paramount 5

SecurePlus Reliance

Products of the past:

One Size Fits All

SecurePlus Gold

SecurePlus Paramount 5

SecurePlus Reliance

Products of the past:

One Size Fits All

More Upside

Upside interest crediting potential through strategies with higher caps

More Liquidity

A

More Upside

Upside interest crediting potential through strategies with higher caps

More Liquidity

A

Customer is at the Heart of FIT Retirement Series

Over 10 years

Customer is at the Heart of FIT Retirement Series

Over 10 years

New Product Features

New Product Features

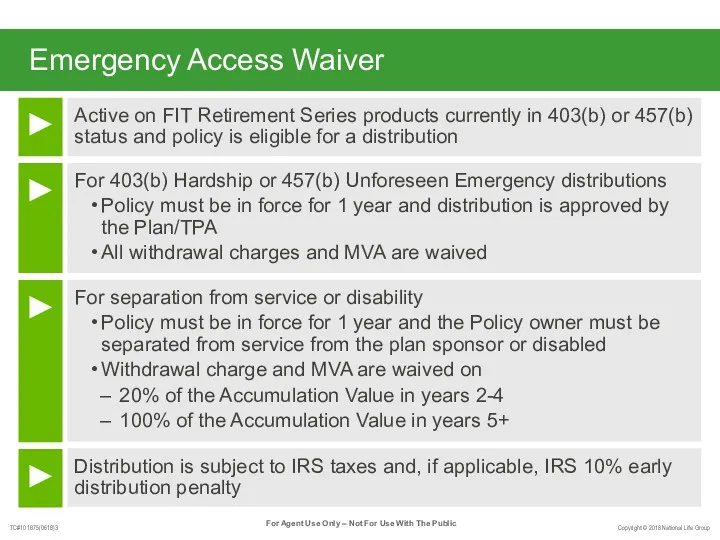

Emergency Access Waiver

Active on FIT Retirement Series products currently in 403(b)

Emergency Access Waiver

Active on FIT Retirement Series products currently in 403(b)

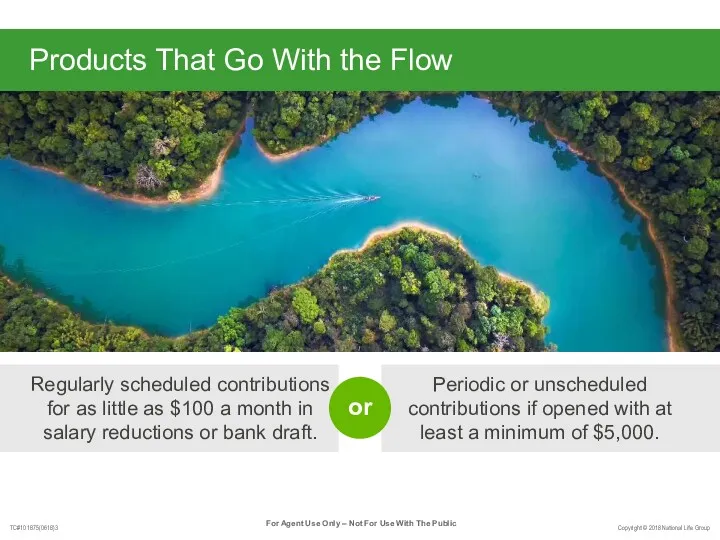

Products That Go With the Flow

Regularly scheduled contributions for as little

Products That Go With the Flow

Regularly scheduled contributions for as little

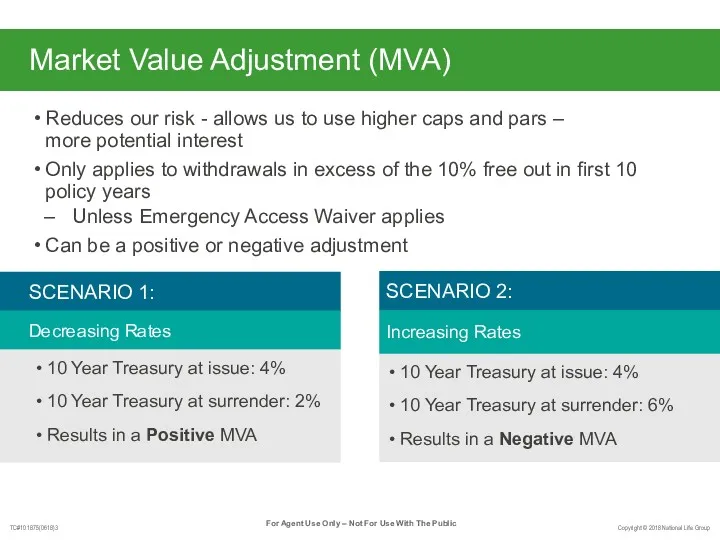

Market Value Adjustment (MVA)

Reduces our risk - allows us to use

Market Value Adjustment (MVA)

Reduces our risk - allows us to use

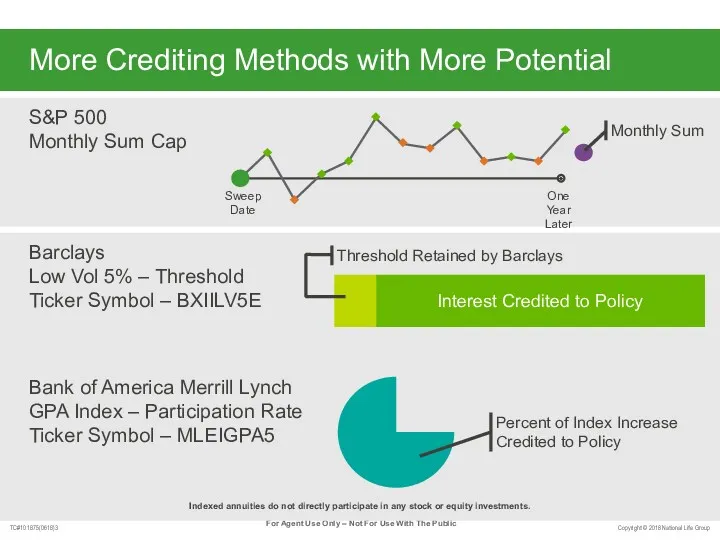

Barclays

Low Vol 5% – Threshold

Ticker Symbol – BXIILV5E

Bank of America Merrill

Barclays

Low Vol 5% – Threshold

Ticker Symbol – BXIILV5E

Bank of America Merrill

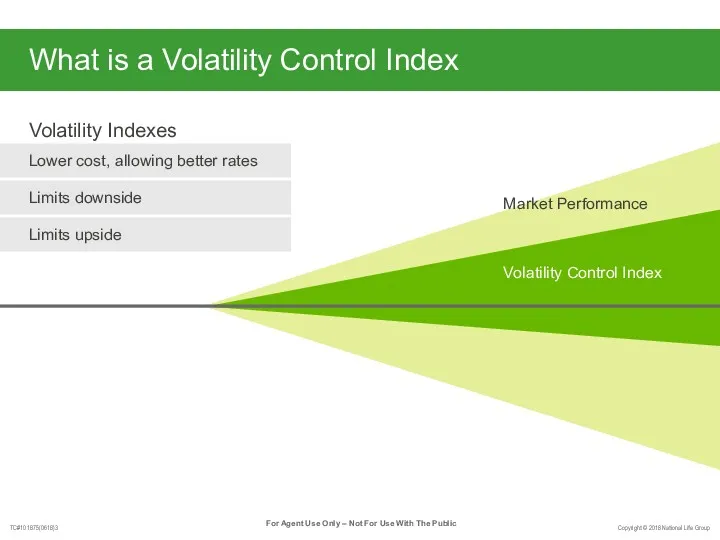

What is a Volatility Control Index

Volatility Control Index

Volatility Indexes

Market Performance

Lower cost,

What is a Volatility Control Index

Volatility Control Index

Volatility Indexes

Market Performance

Lower cost,

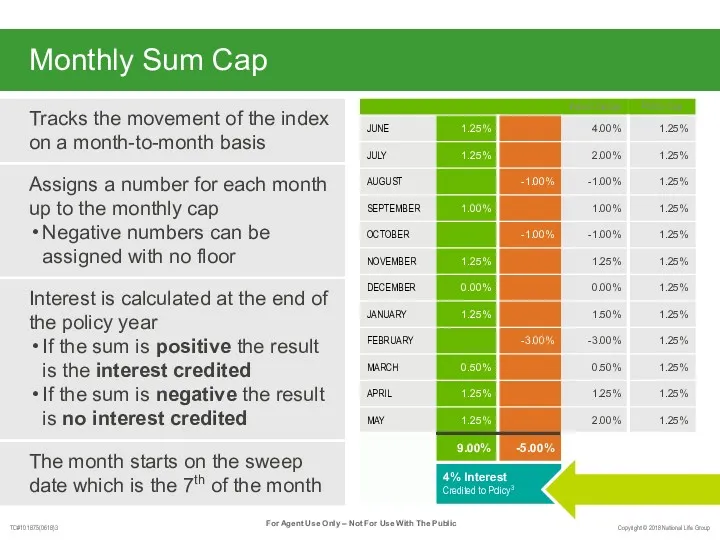

Monthly Sum Cap

Monthly Cap

Tracks the movement of the index on a

Monthly Sum Cap

Monthly Cap

Tracks the movement of the index on a

FIT Retirement Series: Case Studies

FIT Retirement Series: Case Studies

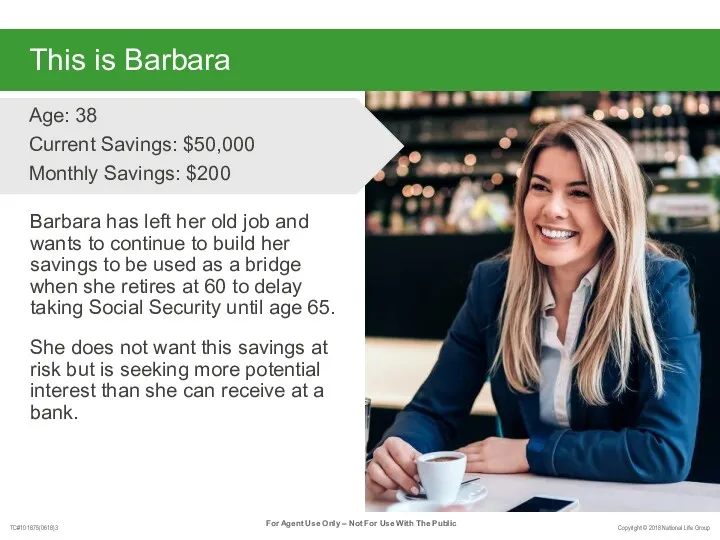

This is Barbara

Barbara has left her old job and wants to

This is Barbara

Barbara has left her old job and wants to

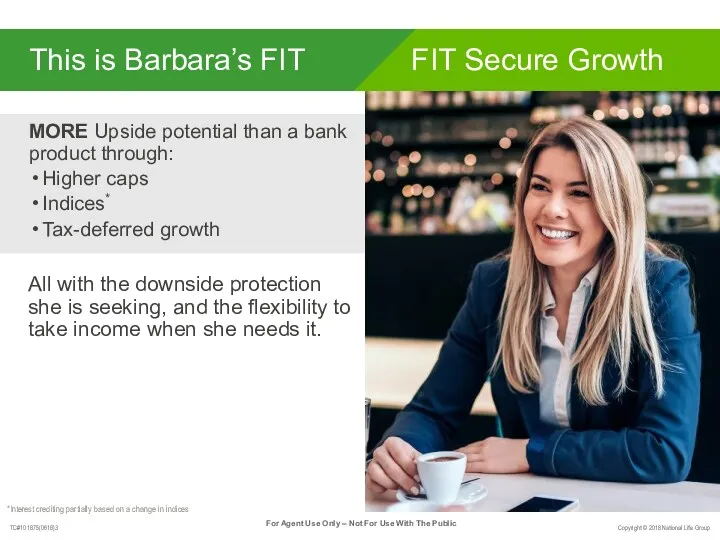

This is Barbara’s FIT

MORE Upside potential than a bank product through:

Higher

This is Barbara’s FIT

MORE Upside potential than a bank product through:

Higher

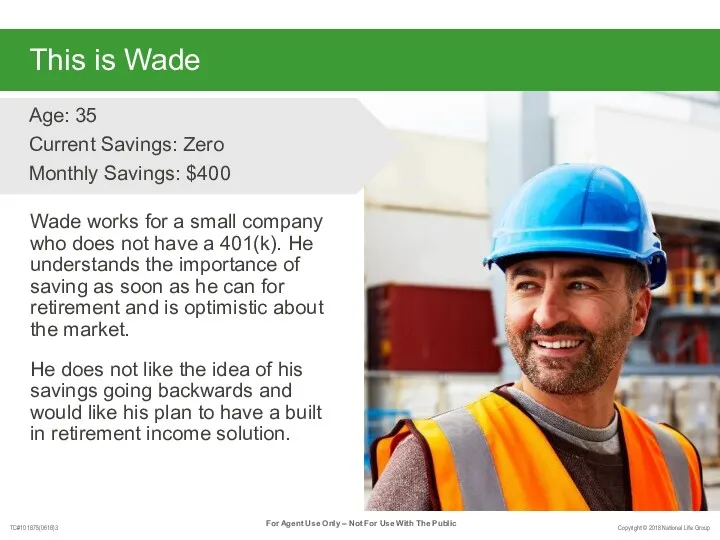

This is Wade

Wade works for a small company who does not

This is Wade

Wade works for a small company who does not

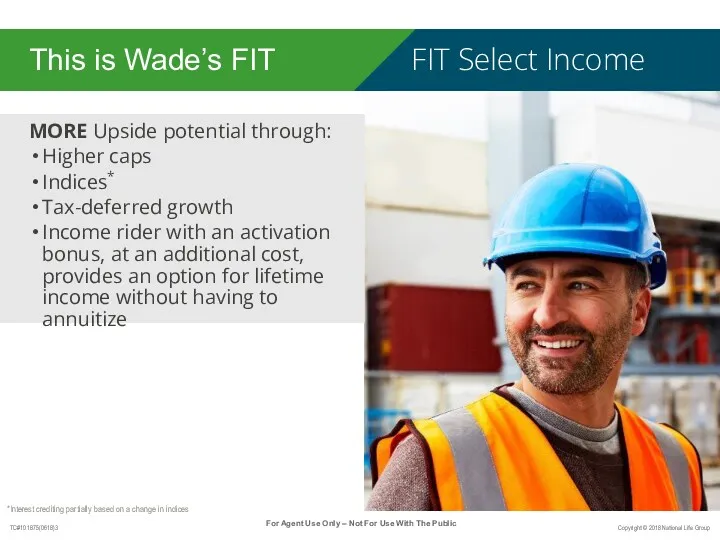

This is Wade’s FIT

MORE Upside potential through:

Higher caps

Indices*

Tax-deferred growth

Income rider with

This is Wade’s FIT

MORE Upside potential through:

Higher caps

Indices*

Tax-deferred growth

Income rider with

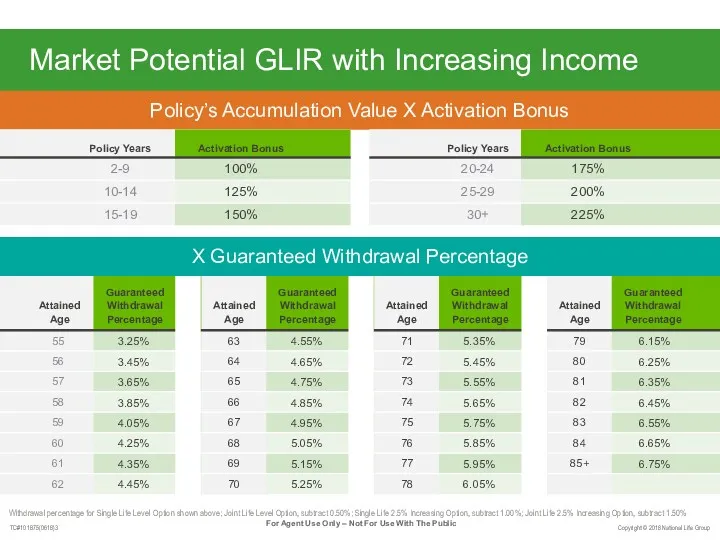

Market Potential GLIR with Increasing Income

Withdrawal percentage for Single Life Level

Market Potential GLIR with Increasing Income

Withdrawal percentage for Single Life Level

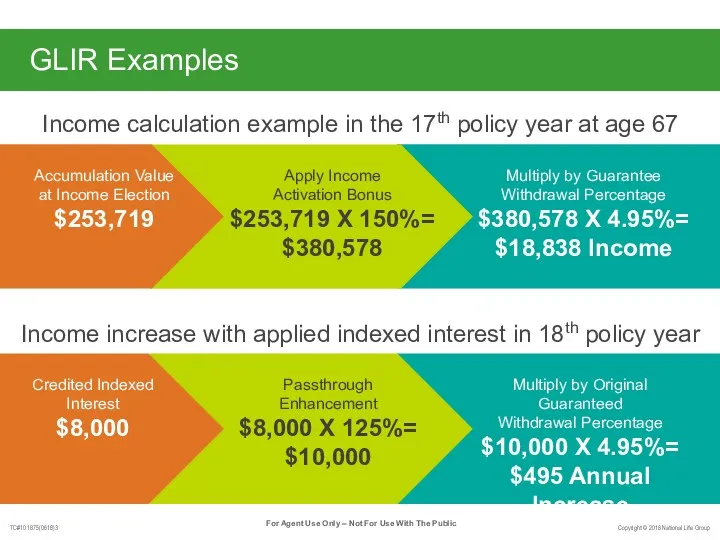

GLIR Examples

Income calculation example in the 17th policy year at age

GLIR Examples

Income calculation example in the 17th policy year at age

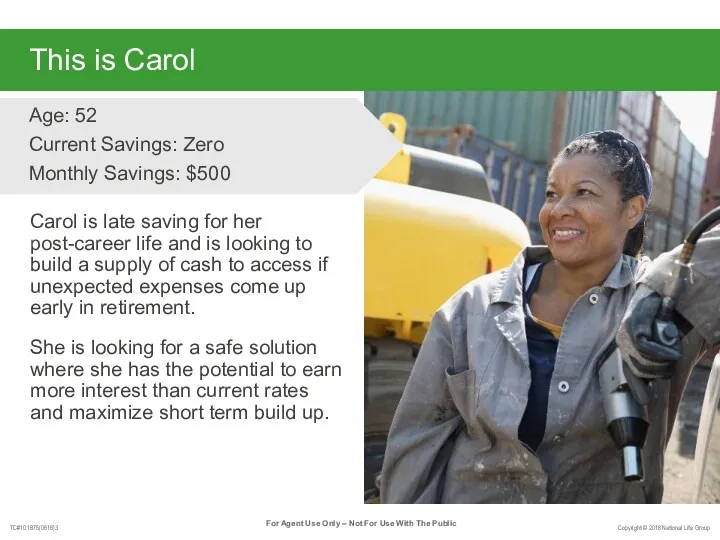

This is Carol

Carol is late saving for her post-career life and

This is Carol

Carol is late saving for her post-career life and

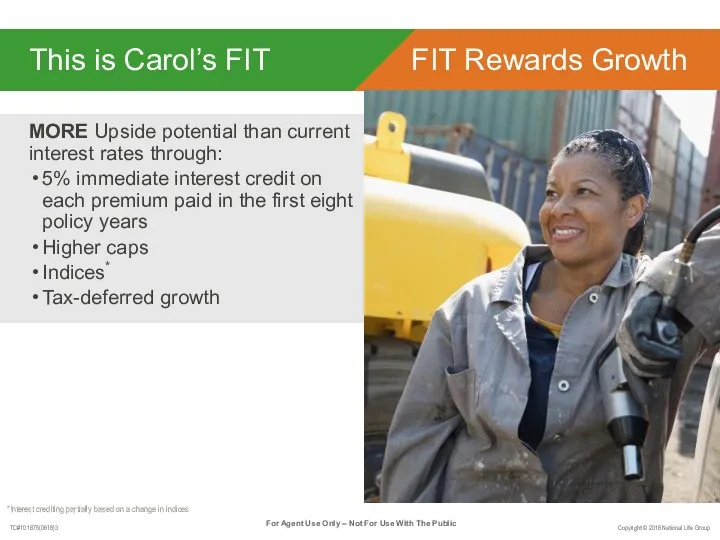

This is Carol’s FIT

MORE Upside potential than current interest rates through:

5%

This is Carol’s FIT

MORE Upside potential than current interest rates through:

5%

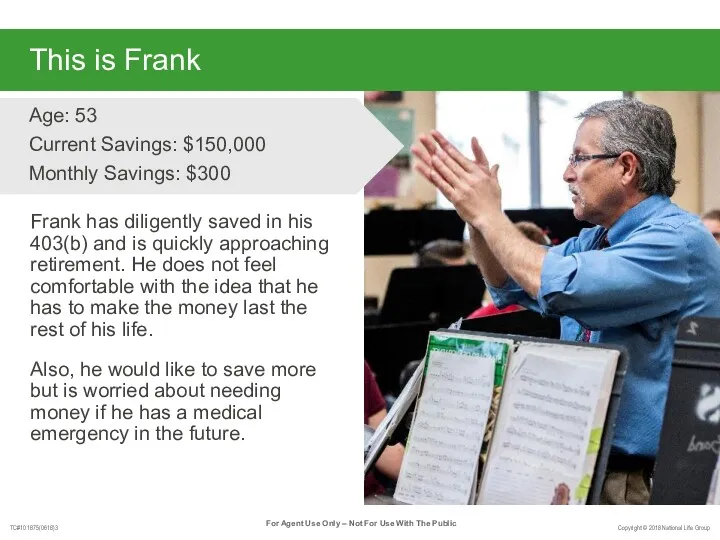

This is Frank

Frank has diligently saved in his 403(b) and is

This is Frank

Frank has diligently saved in his 403(b) and is

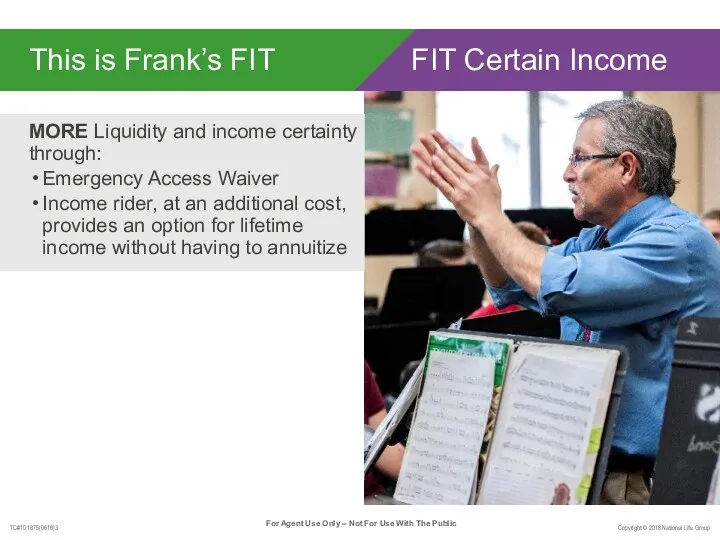

This is Frank’s FIT

MORE Liquidity and income certainty through:

Emergency Access Waiver

Income

This is Frank’s FIT

MORE Liquidity and income certainty through:

Emergency Access Waiver

Income

Simple Roll-up GLIR

Withdrawal percentage for Single Life Level Option shown above;

Simple Roll-up GLIR

Withdrawal percentage for Single Life Level Option shown above;

Example – Accumulation Phase

53-year-old purchases FIT Certain Income

contributing $300 a month

Example – Accumulation Phase

53-year-old purchases FIT Certain Income contributing $300 a month

Guaranteed Withdrawal Payments are Elected at Age 63

Example – Distribution Phase

Guaranteed Withdrawal Payments are Elected at Age 63

Example – Distribution Phase

Product Comparison - Accumulation

*Nursing Care and Terminal Illness Riders not available

Product Comparison - Accumulation

*Nursing Care and Terminal Illness Riders not available

Product Comparison - Income

*Nursing Care and Terminal Illness Riders not available

Product Comparison - Income

*Nursing Care and Terminal Illness Riders not available

Rates

If the par rate is not specified, it is effectively 100%.

If

Rates

If the par rate is not specified, it is effectively 100%.

If

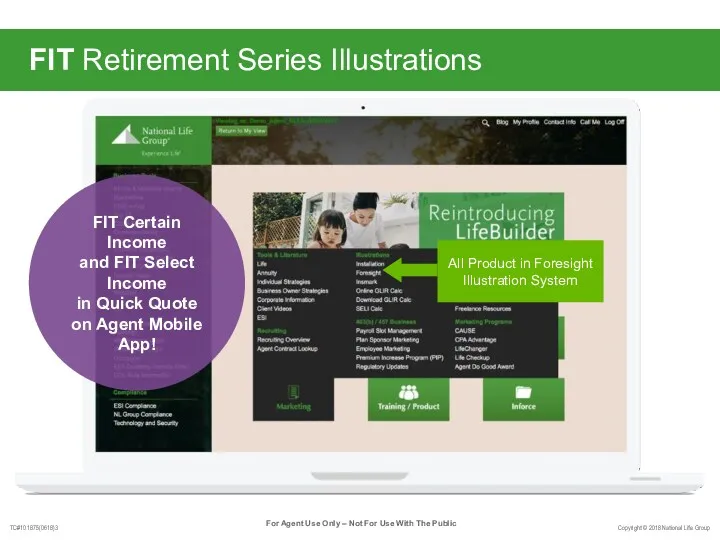

FIT Retirement Series Illustrations

FIT Certain Income

and FIT Select Income

in Quick

FIT Retirement Series Illustrations

FIT Certain Income and FIT Select Income in Quick

Questions?

Questions?

Solutions Tailored to Consumer Needs

Self Distribute

FIT Select Income

FIT Secure Growth

FIT Rewards

Solutions Tailored to Consumer Needs

Self Distribute

FIT Select Income

FIT Secure Growth

FIT Rewards

Barclays Low Vol 5% Index – Ticker symbol: BXIILV5E

Selection of 50

Barclays Low Vol 5% Index – Ticker symbol: BXIILV5E

Selection of 50

Шоу-выставка GLICH

Шоу-выставка GLICH Оценка рыночной стоимости земельного участка

Оценка рыночной стоимости земельного участка Бренды Campbell’s. Адаптация бренда для российского рынка

Бренды Campbell’s. Адаптация бренда для российского рынка Красота в любом возрасте! Сhronolong

Красота в любом возрасте! Сhronolong Интенсив для копирайтеров. Текст О компании

Интенсив для копирайтеров. Текст О компании Привлечение клиентов через рекламу в такси

Привлечение клиентов через рекламу в такси M2M-Мониторинг. Современное решение по управлению М2М-устройствами

M2M-Мониторинг. Современное решение по управлению М2М-устройствами Формула компании. Как продавать дорого и без скидок

Формула компании. Как продавать дорого и без скидок Группы и основные элементы рекламных средств

Группы и основные элементы рекламных средств Продвижение в социальных сетях. Создание и ведение сообщества в ВКонтакте

Продвижение в социальных сетях. Создание и ведение сообщества в ВКонтакте Туристическая компания КОМПАС-ТУР

Туристическая компания КОМПАС-ТУР Best sellers

Best sellers Свойства рекламного текста

Свойства рекламного текста 10 ошибок руководителя в работе с маркетингом

10 ошибок руководителя в работе с маркетингом Otdushi– український виробник креативних товарів

Otdushi– український виробник креативних товарів Гостиницы Канавинского района

Гостиницы Канавинского района Продукция компании Евроснек

Продукция компании Евроснек Ткани нового поколения постельной группы. Вологодский текстильный комбинат

Ткани нового поколения постельной группы. Вологодский текстильный комбинат Коммерческое предложение для застройщиков

Коммерческое предложение для застройщиков Курс тренинг с экономическим эффектом

Курс тренинг с экономическим эффектом Marketing Dissertations

Marketing Dissertations Стартовая коллекция ЛДСП ООО КМДК СОЮЗ-Центр

Стартовая коллекция ЛДСП ООО КМДК СОЮЗ-Центр ИГРА (интернет-магазин) Твой ход

ИГРА (интернет-магазин) Твой ход Профессионалы для профессионалов. Международный Центр Профессионального Клининга

Профессионалы для профессионалов. Международный Центр Профессионального Клининга Современная французская аптека

Современная французская аптека Стажировки в зарубежных ИТ компаниях

Стажировки в зарубежных ИТ компаниях Сдается 2-х комнатная квартира. Авиационная 13

Сдается 2-х комнатная квартира. Авиационная 13 Виды гостиниц и гостиничных комплексов. Классификация гостиниц 2

Виды гостиниц и гостиничных комплексов. Классификация гостиниц 2