- Brand B 360 Analysis. Tea market

Содержание

- 2. Сокращения, используемые в презентации в рамках обзора рынка чая TBs/tbgs- teabags (чайные пакетики) LS – leaf

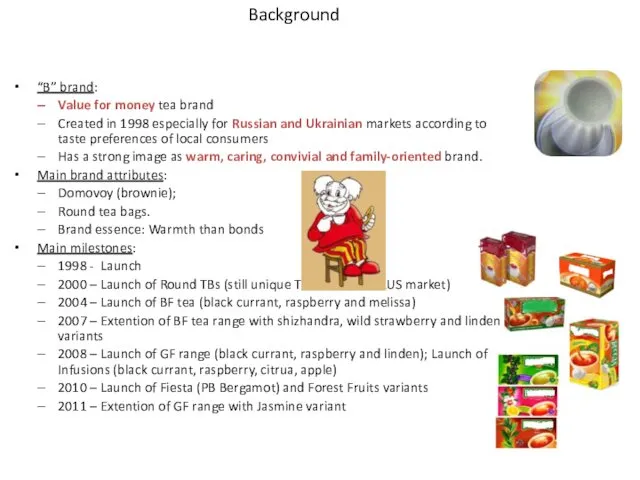

- 3. “B” brand: Value for money tea brand Created in 1998 especially for Russian and Ukrainian markets

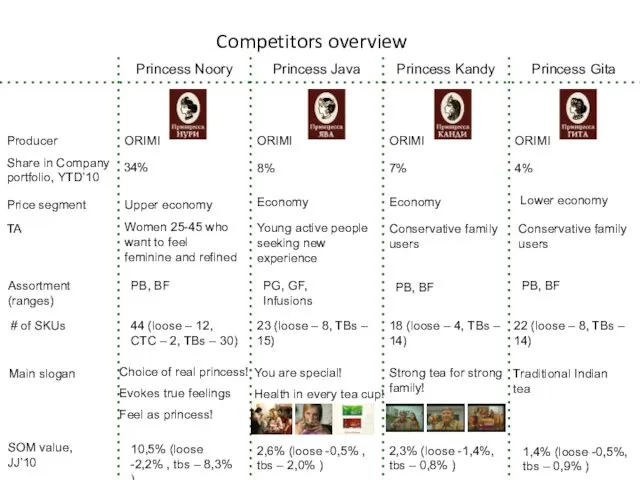

- 4. Competitors overview Princess Noory Princess Java Princess Kandy Princess Gita Producer ORIMI ORIMI ORIMI ORIMI Price

- 5. Competitors overview May tea Bodrost Golden Bowl Lisma Producer Price segment TA Assortment (ranges) Main slogan

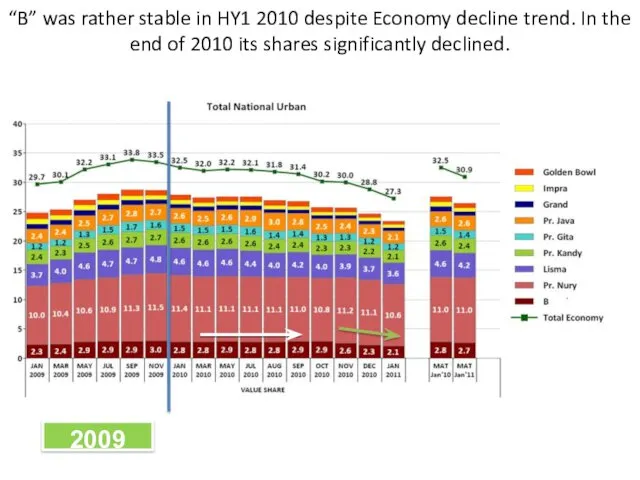

- 6. “B” was rather stable in HY1 2010 despite Economy decline trend. In the end of 2010

- 7. Negative trend was the result of negative trend in both MT and TT. 52% 48% Value

- 8. Tea market development Market growth Market development

- 9. Segment Evolution SOM value

- 10. Tea market development, Sales value & volume, MAT 08 – MAT 10 +5% +5% - Growth

- 11. Tea market development, Sales value & volume, JJ’08 – JJ’10 +33% +20% -3% -1% -5% -6%

- 12. Tea market by price segments In volume sales tea market decline is driven by all the

- 13. Page Tea market by price segments Premium tea holds significantly higher share in Moscow and St.Pete

- 14. Page Tea market by price segments In Hyper/Supermarkets Premium prevails in sales while Economy accounts for

- 15. Page Tea market development: Loose vs TBs At the same time in absolute volume sales all

- 16. Page Tea market development: Loose vs TBs The growth of teabags share comes primarily from the

- 17. Page Tea market development: Loose vs TBs Premium tea prevails in Hyper/Supermarkets and Superettes with slight

- 18. PLACE

- 19. Market vs Economy players split Sales volume, Channels, MAT 08-10 -1% -5% -15% -8% -1% -

- 20. Tea market development : MT vs TT Traditional Trade importance is more or less stable, contributing

- 21. Tea market development : MT vs TT Traditional Trade is still significant for 24 cities and

- 22. Market vs Economy players split Sales volume, Cities, MAT 08-10 +3% - Growth MAT 2010 vs

- 23. Market vs Economy players split Sales volume, City size, MAT 08-10 -3% - Growth MAT 2010

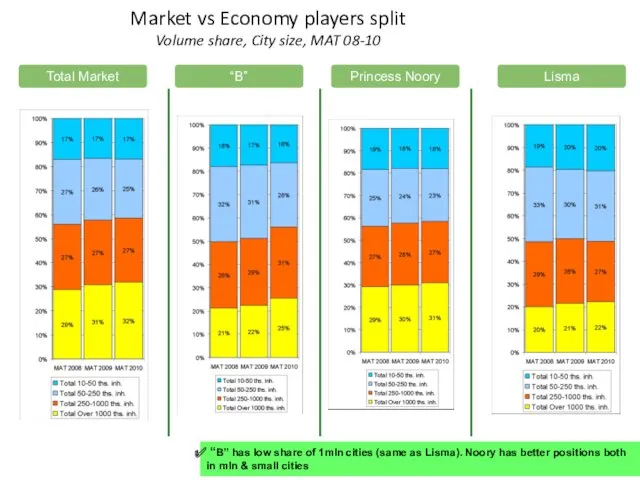

- 24. Market vs Economy players split Volume share, City size, MAT 08-10 “B” has low share of

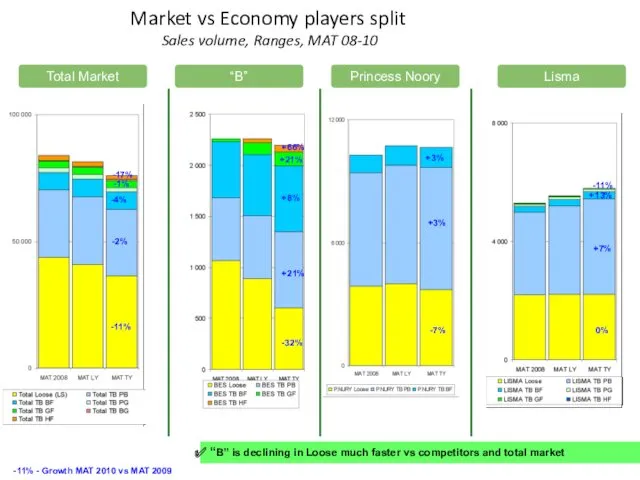

- 25. Market vs Economy players split Sales volume, Ranges, MAT 08-10 -11% - Growth MAT 2010 vs

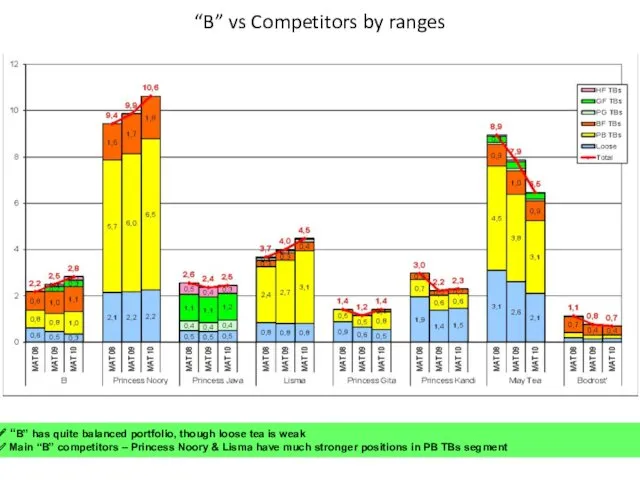

- 26. “B” vs Competitors by ranges “B” has quite balanced portfolio, though loose tea is weak Main

- 27. PRICE

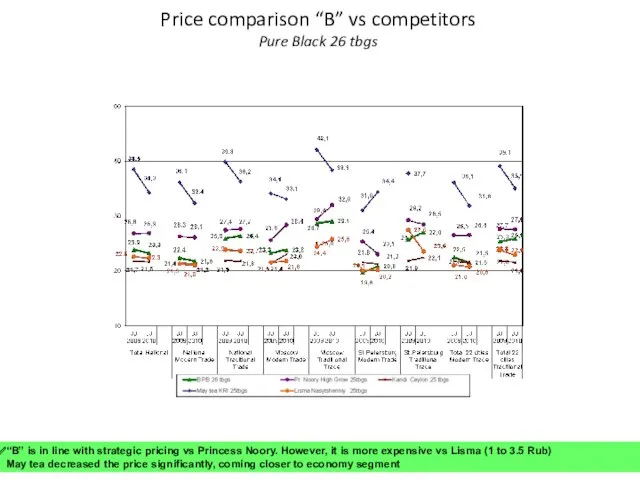

- 28. Price comparison “B” vs competitors Pure Black 26 tbgs “B” is in line with strategic pricing

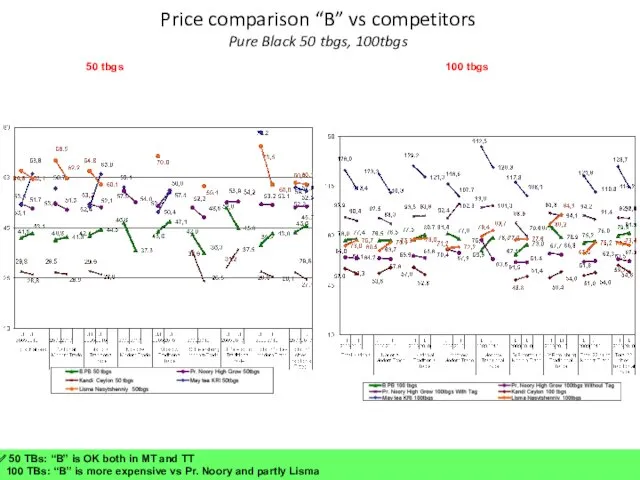

- 29. Price comparison “B” vs competitors Pure Black 50 tbgs, 100tbgs 50 TBs: “B” is OK both

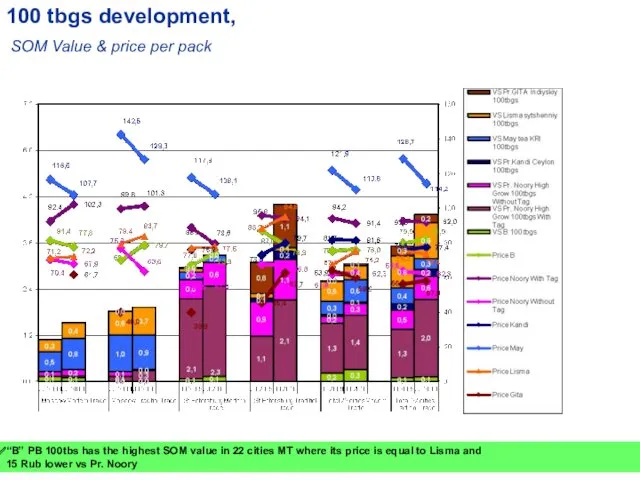

- 30. 100 tbgs development, SOM Value & price per pack “B” PB 100tbs has the highest SOM

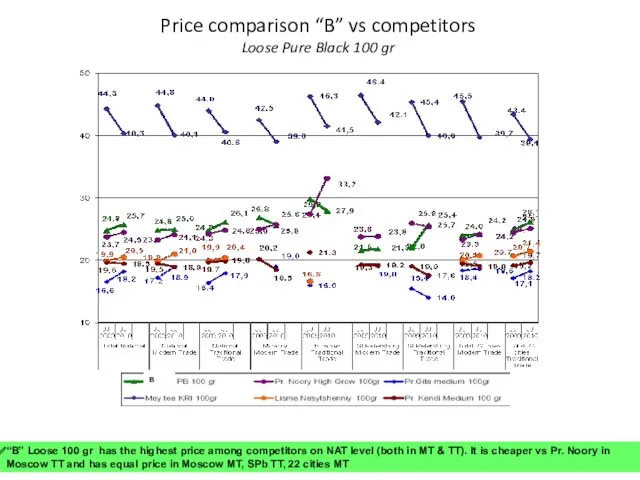

- 31. Price comparison “B” vs competitors Loose Pure Black 100 gr “B” Loose 100 gr has the

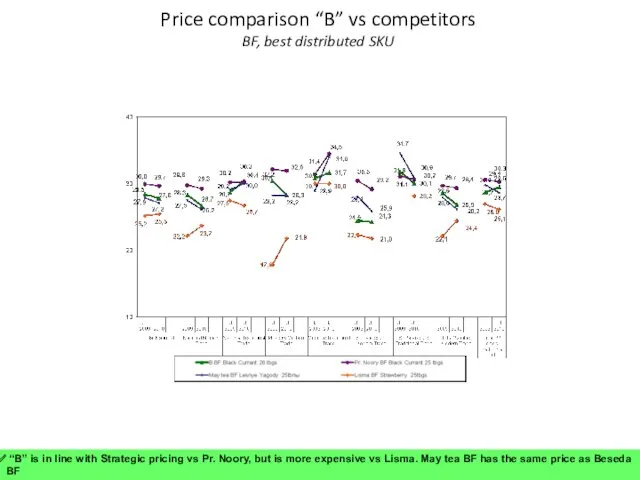

- 32. Price comparison “B” vs competitors BF, best distributed SKU “B” is in line with Strategic pricing

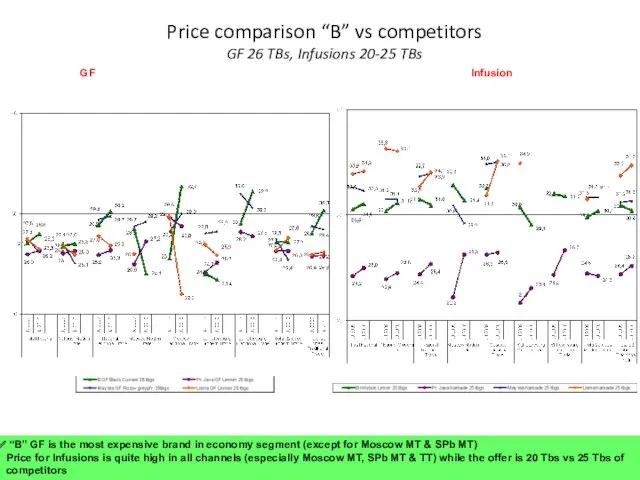

- 33. Price comparison “B” vs competitors GF 26 TBs, Infusions 20-25 TBs “B” GF is the most

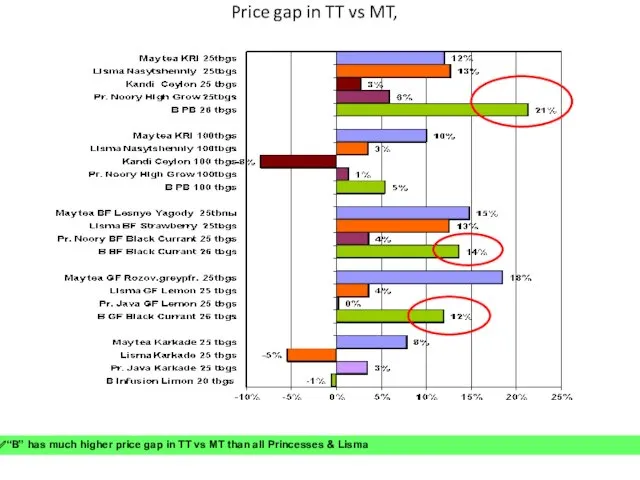

- 34. Price gap in TT vs MT, “B” has much higher price gap in TT vs MT

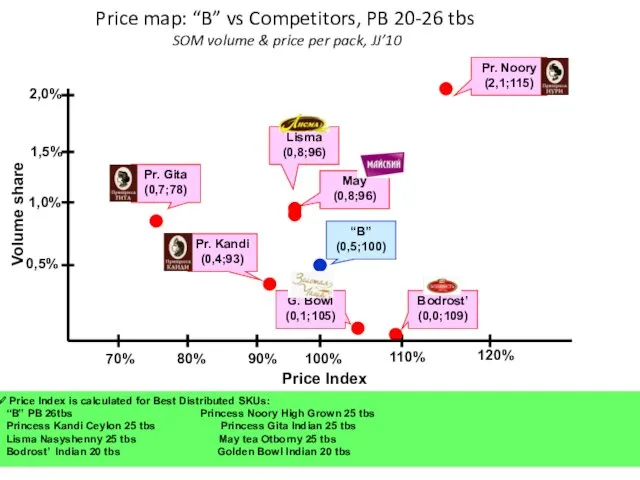

- 35. Price map: “B” vs Competitors, PB 20-26 tbs SOM volume & price per pack, JJ’10 “B”

- 36. Economy brands price development, JJ’09 vs JJ’10 17 18 19 20 21 22 23 24 25

- 37. Consumer Value Index Winter 2009/10: (24/08/09 to 14/02/10) Fair value line Good value More resilient Poor

- 38. PROMOTION

- 39. « L » « B » « BB » Greenfield Tea Ahmad May Tea Princess Nuri

- 40. “B” activities, 2008-2010 TV Launches Promo TV support for promo Fairy Tale 2 160 GRPs 7/04-27/04

- 41. “B” advertising overview, 2006-2009 Over time, “B” shows a consistent and advertising platform Last ads underperform

- 42. Brand Communication Analysis 2009, 30 sec Tested from 14/09/09 to 15/11/09 Correct visibility for the new

- 43. Mean score “B” 2.29 Among total sample Russian average 4.01 Brand Communication Analysis 2009, 30 sec

- 44. PostView TV – “B” ‘Teddy Bears’ Mar-Apr 2010, 15 sec Postview full diagnosis tested from 12/04/10

- 45. (P-ve) (A+ve) (A+ve) (P+ve) (P+ve) (P+ve) (P-ve) (P-ve) (A-ve) (A-ve) (A-ve) (A+ve) Total Russia norm Mean

- 46. PostView TV – “B” ‘Velvet’ May 2010, 15 sec Tested from 07/06/10 to 18/07/10 Hot tea

- 47. (P-ve) (A+ve) (A+ve) (P+ve) (P+ve) (P+ve) (P-ve) (P-ve) (A-ve) (A-ve) (A-ve) (A+ve) Total Russia norm Mean

- 48. “B” communication perception “B” Green Campaign Low spontaneous recall No remarkable character Low purchase intent Positive

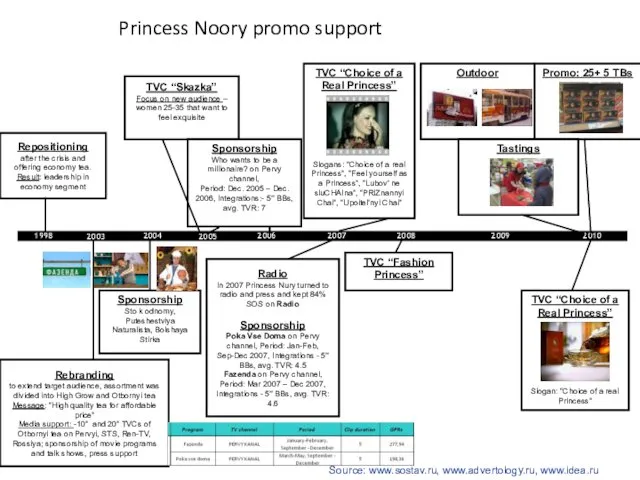

- 49. Princess Noory promo support 1998 2007 2003 2005 2006 2004 2009 2010 Repositioning after the crisis

- 50. “B” sponsorship (Social Mission) Sponsor jingle 10 sec (“B” brand Video) Branded cups on the table

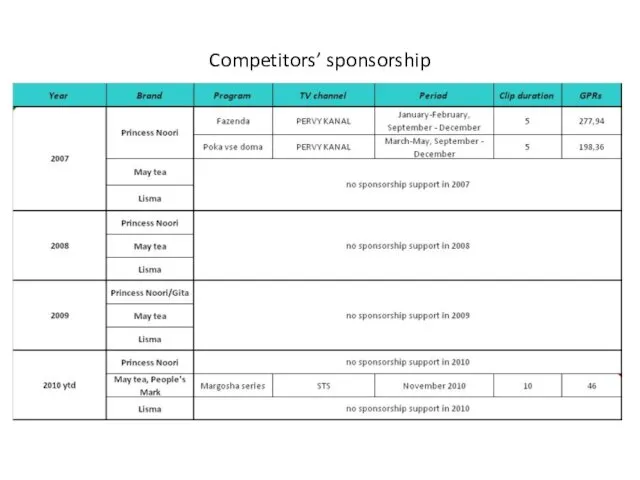

- 51. Competitors’ sponsorship

- 52. Sponsorship: Princess Noory Who wants to be a millionaire? Channel: Pervy Period: Dec. 2005 – Dec.

- 53. Green Rosaria New Indian Summer Fairy Tale Turn on TV Game « B » – Teddy

- 54. Green Indian Summer Fairy Tale Rosaria New «B» – Teddy Bears «B» – Velvet taste Despite

- 55. 49% 16% 11% Awareness Re-purchase intents Trial 31% 8% 4% “B” new product launch summary Indian

- 56. “B” Pure Black 100tbs promo effect SOM Value In MT promo brings good MS growth to

- 57. “B” 100tbs Bears promo “B” PB 100tbs promo has low WSD in several cities and almost

- 58. PRODUCT

- 59. ABC analysis “B” vs competitors, SOM Value “B”

- 60. Assortment structure “B” vs competitors “B” Pr. Noory Pr. Java Pr. Kandi Pr. Gita Lisma May

- 61. “B” vs competitors PB Loose tea tasting results, Q3 2010 “B” Loose has quite good results

- 62. “B” vs competitors PB TBs tasting results, Q3 2010 “B” TBs is inferior to Princess Noory

- 63. PROPOSITION

- 64. Tea category perception GENERAL CATEGORY BENEFITS Tonic/ exhilarant effect Well quenches one’s thirst Health benefits Unites

- 65. Penetration of Tea and “B” by Group Food Innovators Quality Seekers Penny Grabbers Indifferent to Food

- 66. “B” is interesting for… Dieters try to care about their body, need a small support in

- 67. Food Innovators Price-conscious Dieters “B” target audience, Women 30-55 (most valued ones 30-40), with families (3+

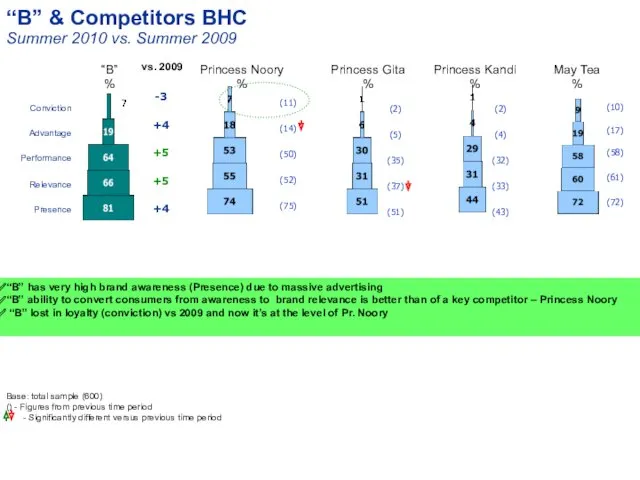

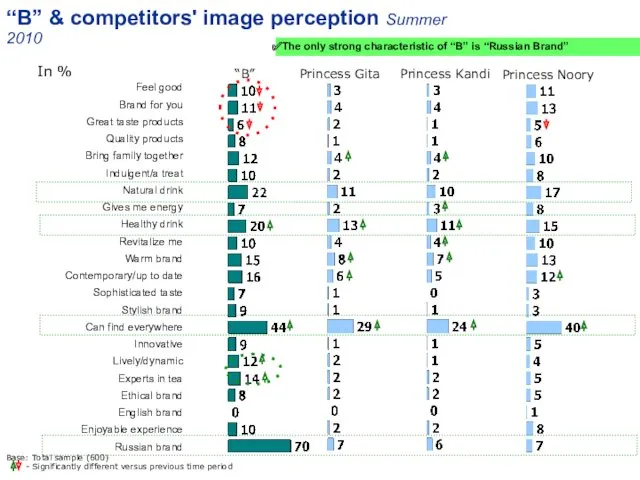

- 68. “B” % Princess Noory % Princess Gita % Base: total sample (600) () - Figures from

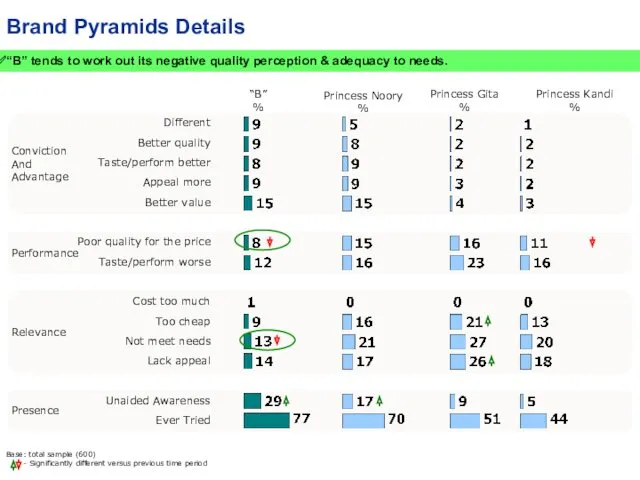

- 69. Better quality Taste/perform better Appeal more Different Better value Cost too much Too cheap Poor quality

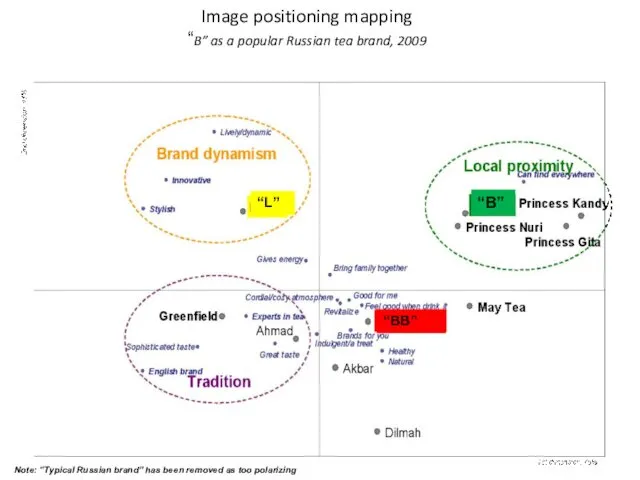

- 70. Image positioning mapping “B” as a popular Russian tea brand, 2009 Note: “Typical Russian brand” has

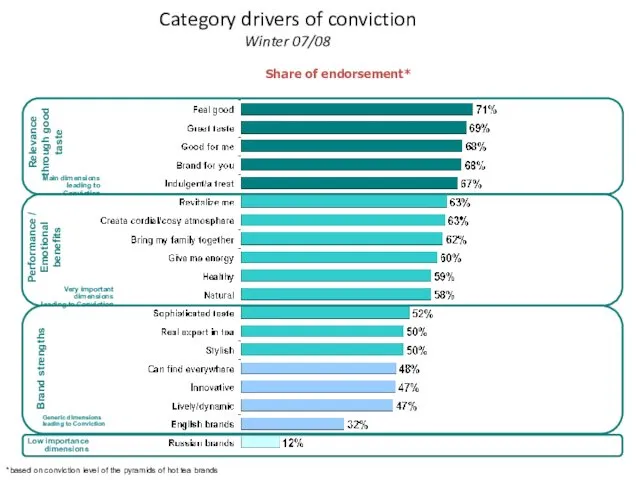

- 71. Category drivers of conviction Winter 07/08 Share of endorsement* Relevance through good taste Performance / Emotional

- 72. Base: Total sample (600) - Significantly different versus previous time period “B” Princess Noory Princess Gita

- 73. “B” Semantic Analysis Conversation Tea party Friends/ friendly Family / Relatives Old man House-spirit Home Sincere

- 74. “B” Brand Perception Ipsos, Sep 2009 Well-known brand with a history Strong and original advertising support

- 75. PACKAGE

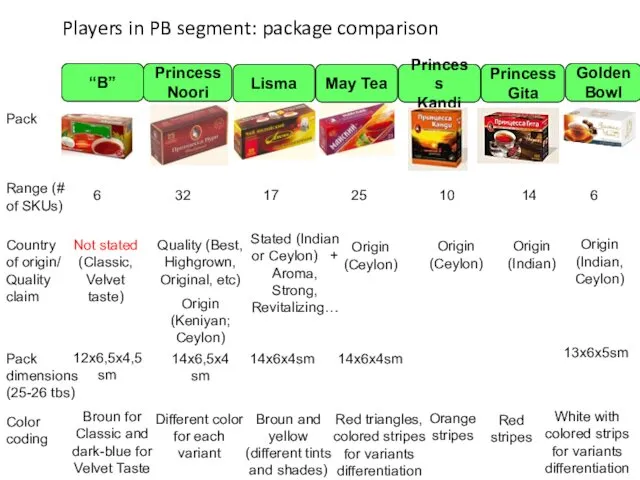

- 76. Players in PB segment: package comparison “B” Princess Noori May Tea Lisma Princess Kandi Princess Gita

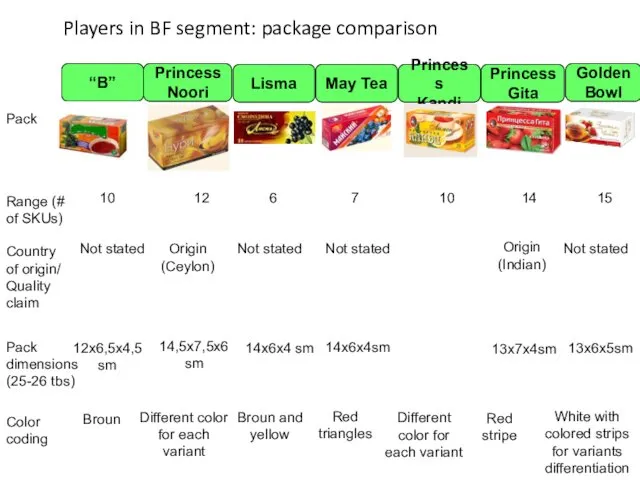

- 77. Players in BF segment: package comparison “B” Princess Noori May Tea Lisma Princess Kandi Princess Gita

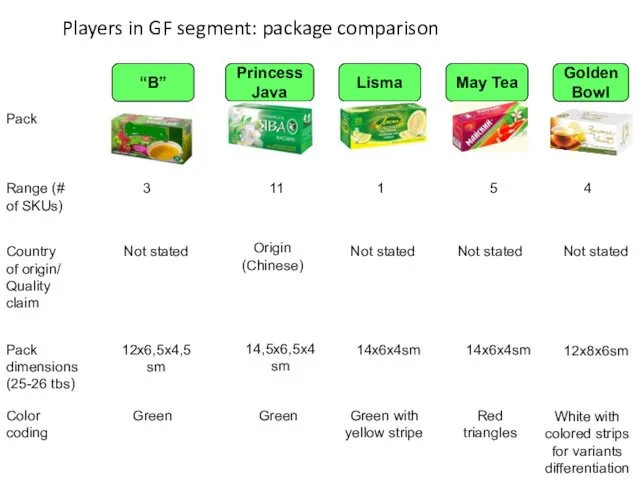

- 78. Players in GF segment: package comparison “B” Princess Java May Tea Lisma Golden Bowl Pack Range

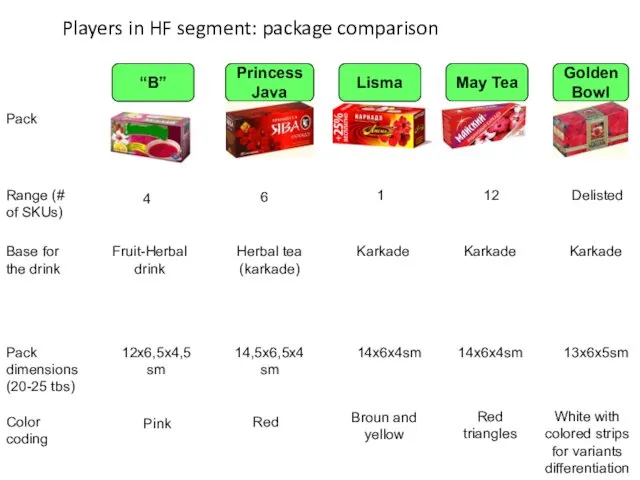

- 79. Players in HF segment: package comparison “B” Princess Java May Tea Lisma Golden Bowl Pack Range

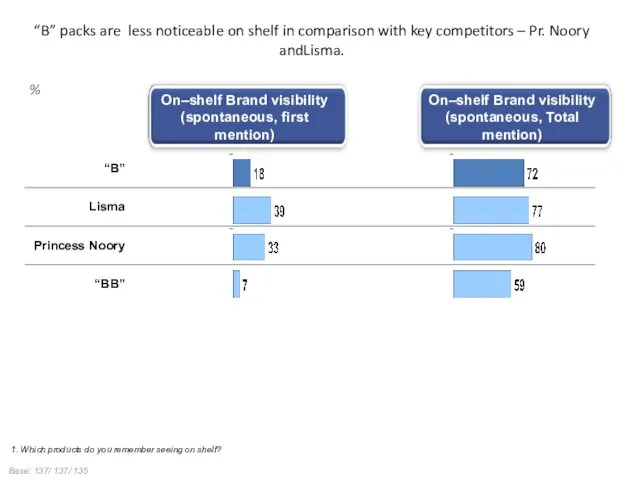

- 80. “B” packs are less noticeable on shelf in comparison with key competitors – Pr. Noory andLisma.

- 82. Скачать презентацию

Сокращения, используемые в презентации

в рамках обзора рынка чая

TBs/tbgs- teabags (чайные пакетики)

LS – leaf

Сокращения, используемые в презентации

в рамках обзора рынка чая

TBs/tbgs- teabags (чайные пакетики)

LS – leaf

“B” brand:

Value for money tea brand

Created in 1998 especially for Russian and Ukrainian

“B” brand:

Value for money tea brand

Created in 1998 especially for Russian and Ukrainian

Competitors overview

Princess Noory

Princess Java

Princess Kandy

Princess Gita

Producer

ORIMI

ORIMI

ORIMI

ORIMI

Price segment

Upper economy

Economy

Economy

Lower economy

TA

Assortment (ranges)

Main slogan

SOM value, JJ’10

10,5%

Competitors overview

Princess Noory

Princess Java

Princess Kandy

Princess Gita

Producer

ORIMI

ORIMI

ORIMI

ORIMI

Price segment

Upper economy

Economy

Economy

Lower economy

TA

Assortment (ranges)

Main slogan

SOM value, JJ’10

10,5%

Competitors overview

May tea

Bodrost

Golden Bowl

Lisma

Producer

Price segment

TA

Assortment (ranges)

Main slogan

SOM value, JJ’10

# of SKUs

All ranges

All ranges

28

Competitors overview

May tea

Bodrost

Golden Bowl

Lisma

Producer

Price segment

TA

Assortment (ranges)

Main slogan

SOM value, JJ’10

# of SKUs

All ranges

All ranges

28

“B” was rather stable in HY1 2010 despite Economy decline trend. In the

“B” was rather stable in HY1 2010 despite Economy decline trend. In the

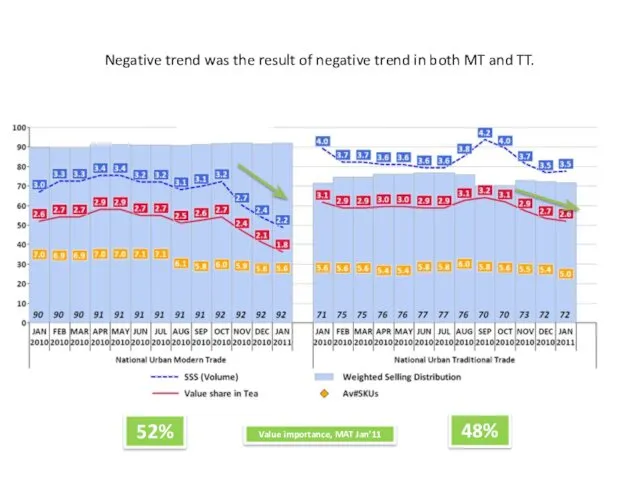

Negative trend was the result of negative trend in both MT and TT.

52%

48%

Value

Negative trend was the result of negative trend in both MT and TT.

52%

48%

Value

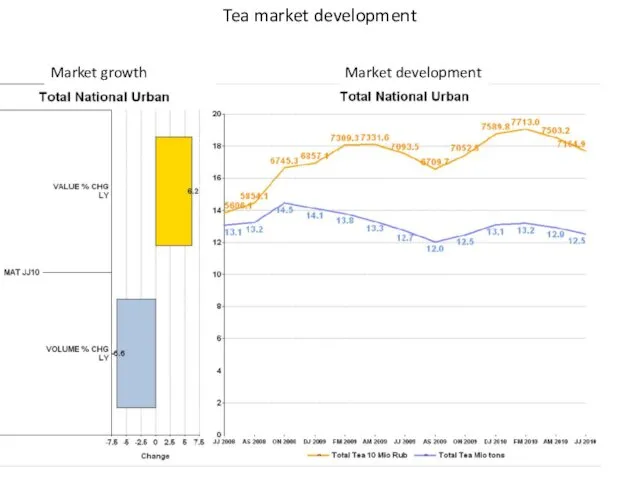

Tea market development

Market growth

Market development

Tea market development

Market growth

Market development

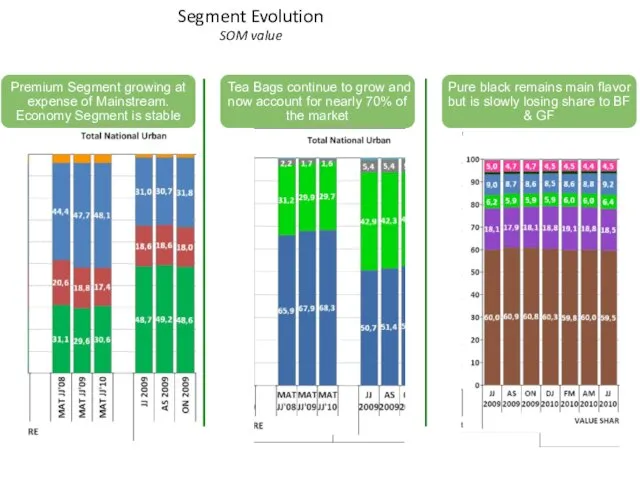

Segment Evolution

SOM value

Segment Evolution

SOM value

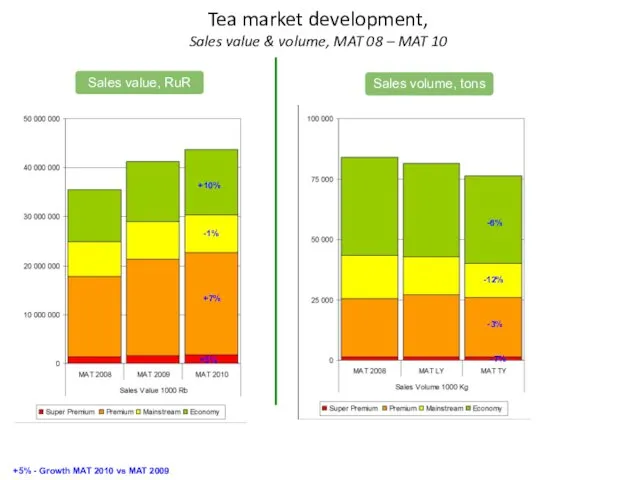

Tea market development,

Sales value & volume, MAT 08 – MAT 10

+5%

+5% - Growth

Tea market development,

Sales value & volume, MAT 08 – MAT 10

+5%

+5% - Growth

Tea market development,

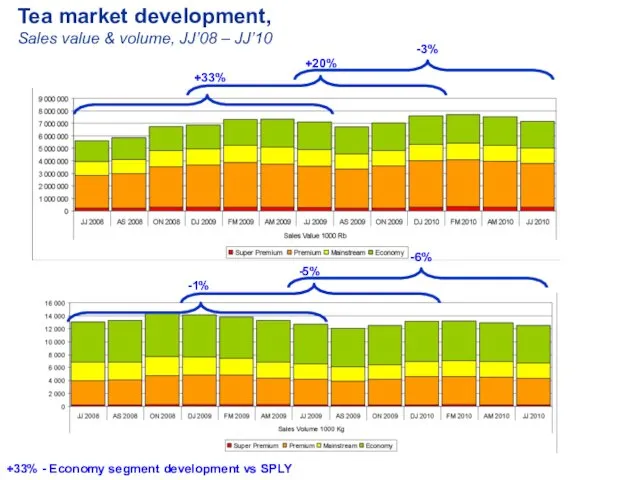

Sales value & volume, JJ’08 – JJ’10

+33%

+20%

-3%

-1%

-5%

-6%

+33% - Economy segment development

Tea market development,

Sales value & volume, JJ’08 – JJ’10

+33%

+20%

-3%

-1%

-5%

-6%

+33% - Economy segment development

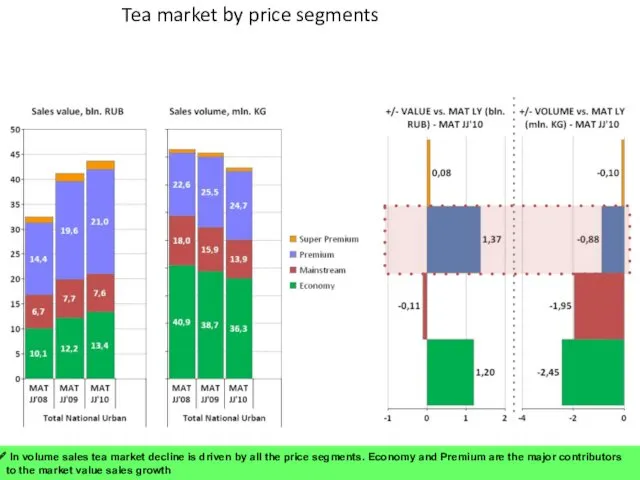

Tea market by price segments

In volume sales tea market decline is driven

Tea market by price segments

In volume sales tea market decline is driven

Page

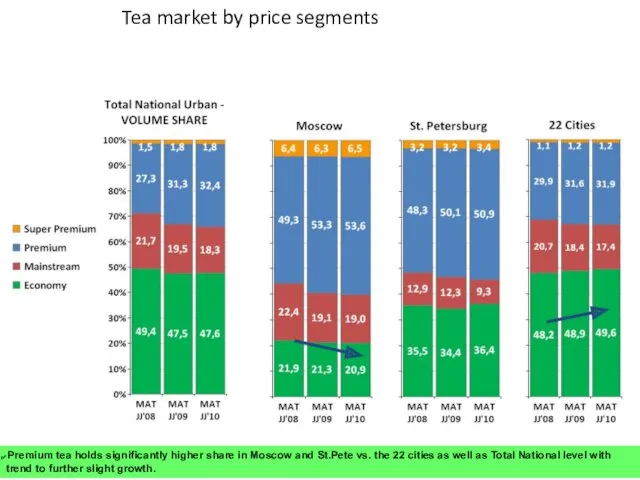

Tea market by price segments

Premium tea holds significantly higher share in

Page

Tea market by price segments

Premium tea holds significantly higher share in

Page

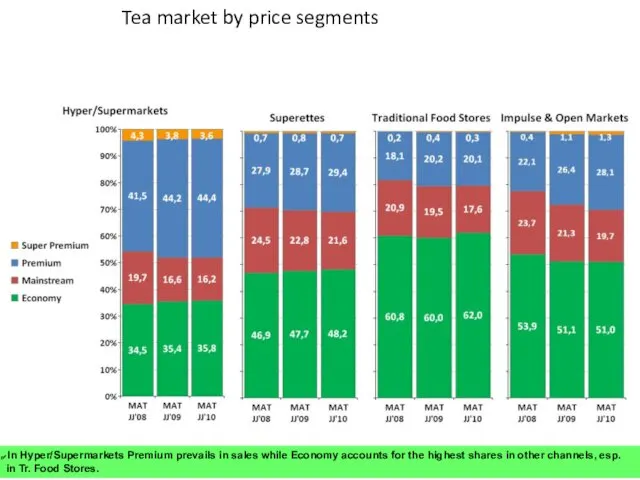

Tea market by price segments

In Hyper/Supermarkets Premium prevails in sales while

Page

Tea market by price segments

In Hyper/Supermarkets Premium prevails in sales while

Page

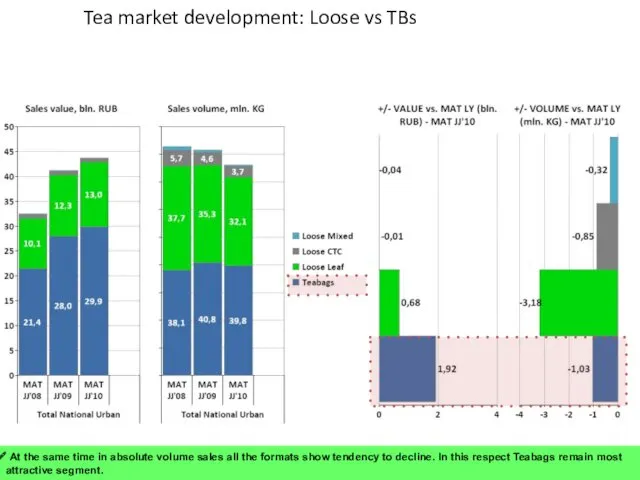

Tea market development: Loose vs TBs

At the same time in absolute

Page

Tea market development: Loose vs TBs

At the same time in absolute

Page

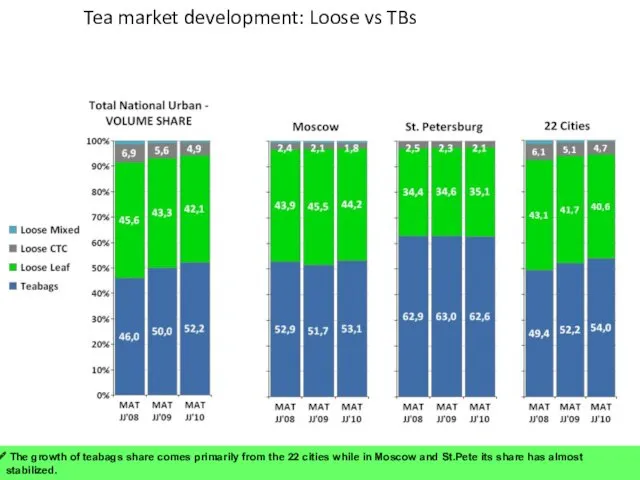

Tea market development: Loose vs TBs

The growth of teabags share comes

Page

Tea market development: Loose vs TBs

The growth of teabags share comes

Page

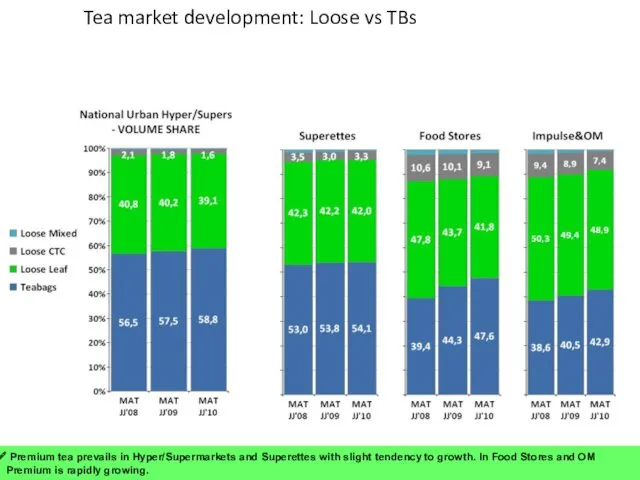

Tea market development: Loose vs TBs

Premium tea prevails in Hyper/Supermarkets and

Page

Tea market development: Loose vs TBs

Premium tea prevails in Hyper/Supermarkets and

PLACE

PLACE

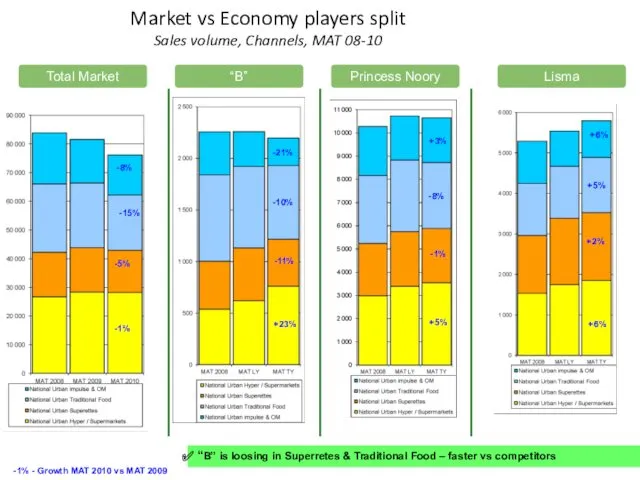

Market vs Economy players split

Sales volume, Channels, MAT 08-10

-1%

-5%

-15%

-8%

-1% - Growth MAT 2010

Market vs Economy players split

Sales volume, Channels, MAT 08-10

-1%

-5%

-15%

-8%

-1% - Growth MAT 2010

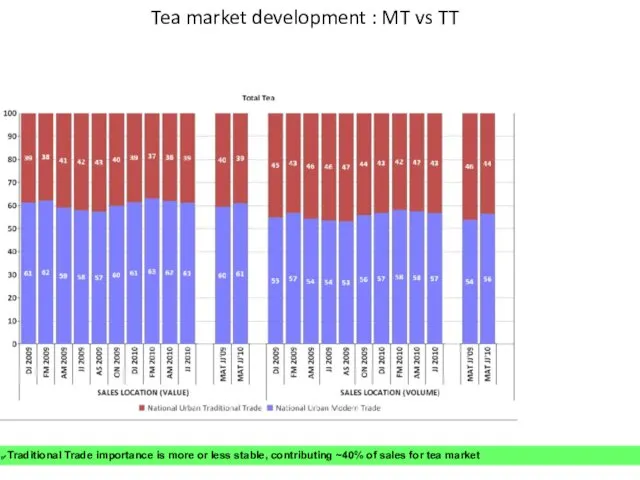

Tea market development : MT vs TT

Traditional Trade importance is more or

Tea market development : MT vs TT

Traditional Trade importance is more or

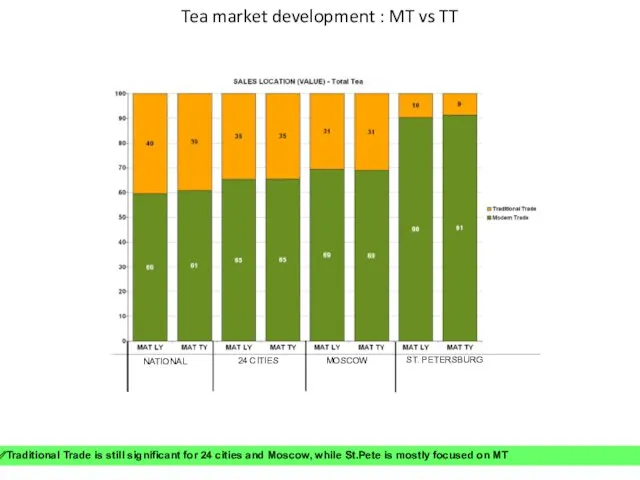

Tea market development : MT vs TT

Traditional Trade is still significant for 24

Tea market development : MT vs TT

Traditional Trade is still significant for 24

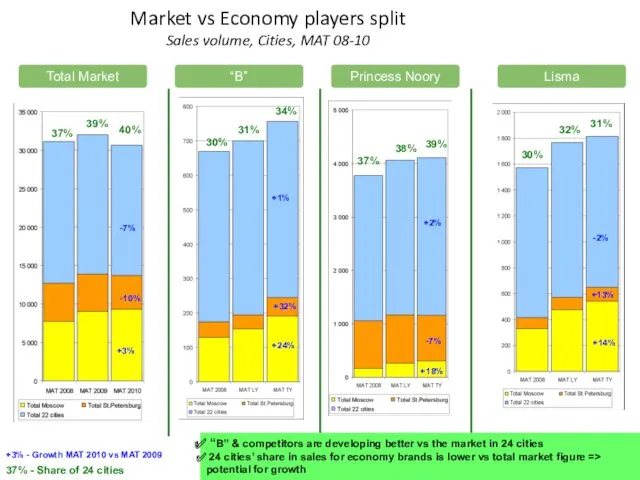

Market vs Economy players split

Sales volume, Cities, MAT 08-10

+3% - Growth MAT 2010

Market vs Economy players split

Sales volume, Cities, MAT 08-10

+3% - Growth MAT 2010

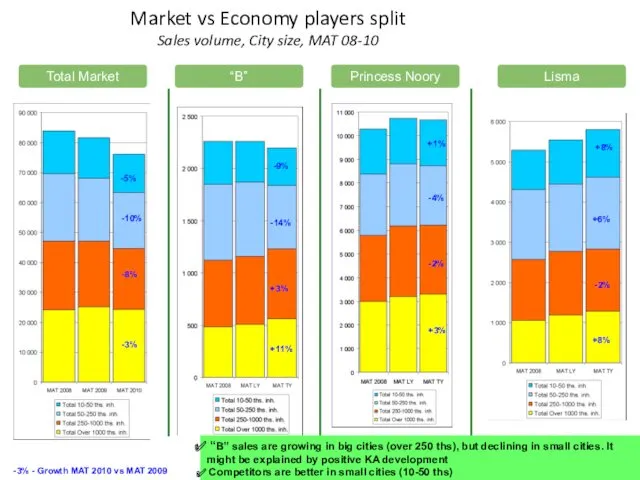

Market vs Economy players split

Sales volume, City size, MAT 08-10

-3% - Growth MAT

Market vs Economy players split

Sales volume, City size, MAT 08-10

-3% - Growth MAT

Market vs Economy players split

Volume share, City size, MAT 08-10

“B” has low

Market vs Economy players split

Volume share, City size, MAT 08-10

“B” has low

Market vs Economy players split

Sales volume, Ranges, MAT 08-10

-11% - Growth MAT

Market vs Economy players split

Sales volume, Ranges, MAT 08-10

-11% - Growth MAT

“B” vs Competitors by ranges

“B” has quite balanced portfolio, though loose tea

“B” vs Competitors by ranges

“B” has quite balanced portfolio, though loose tea

PRICE

PRICE

Price comparison “B” vs competitors

Pure Black 26 tbgs

“B” is in line with strategic

Price comparison “B” vs competitors

Pure Black 26 tbgs

“B” is in line with strategic

Price comparison “B” vs competitors

Pure Black 50 tbgs, 100tbgs

50 TBs: “B” is

Price comparison “B” vs competitors

Pure Black 50 tbgs, 100tbgs

50 TBs: “B” is

100 tbgs development,

SOM Value & price per pack

“B” PB 100tbs has

100 tbgs development,

SOM Value & price per pack

“B” PB 100tbs has

Price comparison “B” vs competitors

Loose Pure Black 100 gr

“B” Loose 100 gr has

Price comparison “B” vs competitors

Loose Pure Black 100 gr

“B” Loose 100 gr has

Price comparison “B” vs competitors

BF, best distributed SKU

“B” is in line with

Price comparison “B” vs competitors

BF, best distributed SKU

“B” is in line with

Price comparison “B” vs competitors

GF 26 TBs, Infusions 20-25 TBs

“B” GF is

Price comparison “B” vs competitors

GF 26 TBs, Infusions 20-25 TBs

“B” GF is

Price gap in TT vs MT,

“B” has much higher price gap in TT

Price gap in TT vs MT,

“B” has much higher price gap in TT

Price map: “B” vs Competitors, PB 20-26 tbs SOM volume & price per

Price map: “B” vs Competitors, PB 20-26 tbs SOM volume & price per

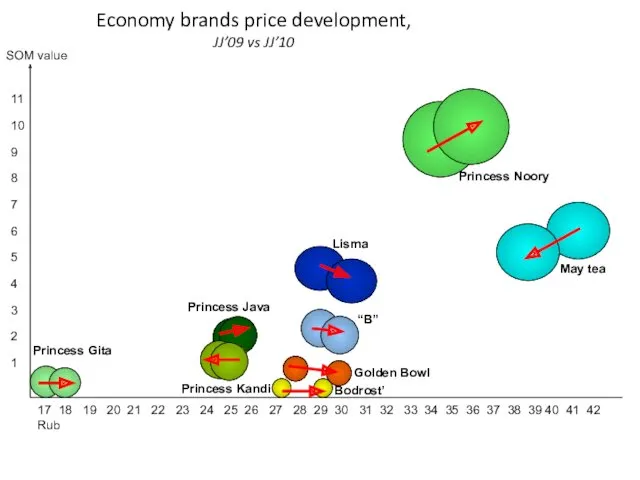

Economy brands price development,

JJ’09 vs JJ’10

17 18 19 20 21 22 23 24

Economy brands price development,

JJ’09 vs JJ’10

17 18 19 20 21 22 23 24

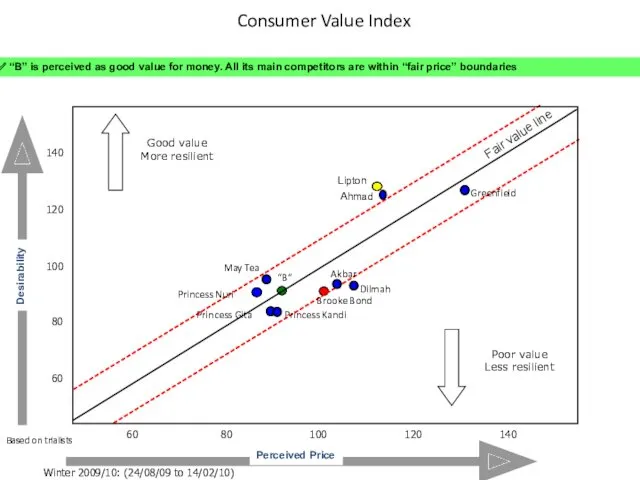

Consumer Value Index

Winter 2009/10: (24/08/09 to 14/02/10)

Fair value line

Good value

More resilient

Poor value

Less resilient

Based

Consumer Value Index

Winter 2009/10: (24/08/09 to 14/02/10)

Fair value line

Good value

More resilient

Poor value

Less resilient

Based

PROMOTION

PROMOTION

« L »

« B »

« BB »

Greenfield Tea

Ahmad

May Tea

Princess Nuri

Akbar

Dilmah

Princess Gita

Princess Kandi

Data period: winter 2009/2010

Total Communication

%

TV

%

Print

%

Outdoor

%

Radio

%

In-store

activity

%

(1186)

Base

Total

sample:

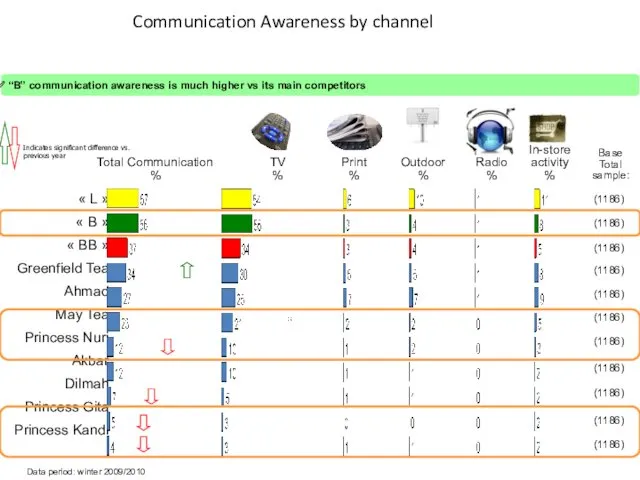

Communication Awareness by

« L »

« B »

« BB »

Greenfield Tea

Ahmad

May Tea

Princess Nuri

Akbar

Dilmah

Princess Gita

Princess Kandi

Data period: winter 2009/2010

Total Communication

%

TV

%

Print

%

Outdoor

%

Radio

%

In-store

activity

%

(1186)

Base

Total

sample:

Communication Awareness by

“B” activities,

2008-2010

TV

Launches

Promo

TV support for promo

Fairy Tale 2

160 GRPs

7/04-27/04

Green

480 GRPs

2/805-08/06

Rosaria

860 GRPs

16/03-03/05

Masterbrand

1099 GRPs

“B” activities,

2008-2010

TV

Launches

Promo

TV support for promo

Fairy Tale 2

160 GRPs

7/04-27/04

Green

480 GRPs

2/805-08/06

Rosaria

860 GRPs

16/03-03/05

Masterbrand

1099 GRPs

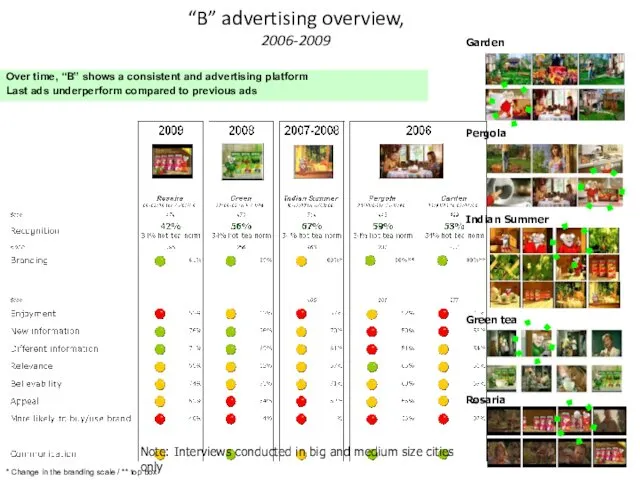

“B” advertising overview,

2006-2009

Over time, “B” shows a consistent and advertising platform

Last ads underperform

“B” advertising overview,

2006-2009

Over time, “B” shows a consistent and advertising platform

Last ads underperform

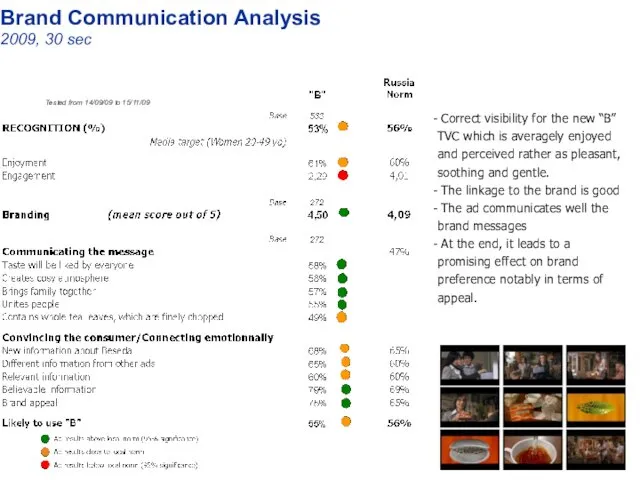

Brand Communication Analysis

2009, 30 sec

Tested from 14/09/09 to 15/11/09

Correct visibility for

Brand Communication Analysis

2009, 30 sec

Tested from 14/09/09 to 15/11/09

Correct visibility for

Mean score

“B” 2.29

Among total sample

Russian average 4.01

Brand Communication Analysis

2009, 30 sec

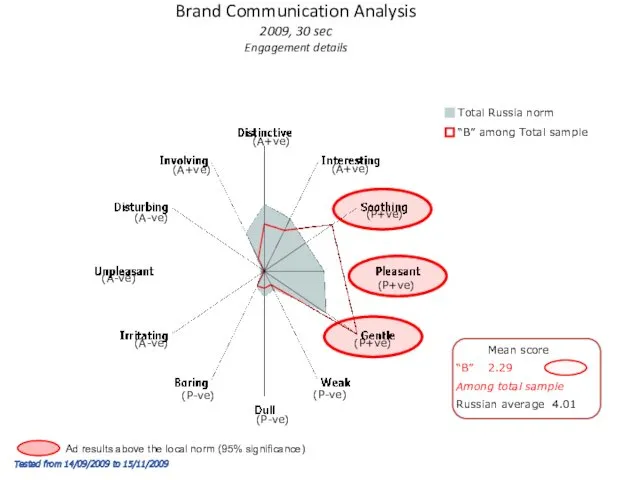

Engagement details

(P-ve)

(A+ve)

(A+ve)

(P+ve)

(P+ve)

(P+ve)

(P-ve)

(P-ve)

(A-ve)

(A-ve)

(A-ve)

(A+ve)

“B” among Total

Mean score

“B” 2.29

Among total sample

Russian average 4.01

Brand Communication Analysis

2009, 30 sec

Engagement details

(P-ve)

(A+ve)

(A+ve)

(P+ve)

(P+ve)

(P+ve)

(P-ve)

(P-ve)

(A-ve)

(A-ve)

(A-ve)

(A+ve)

“B” among Total

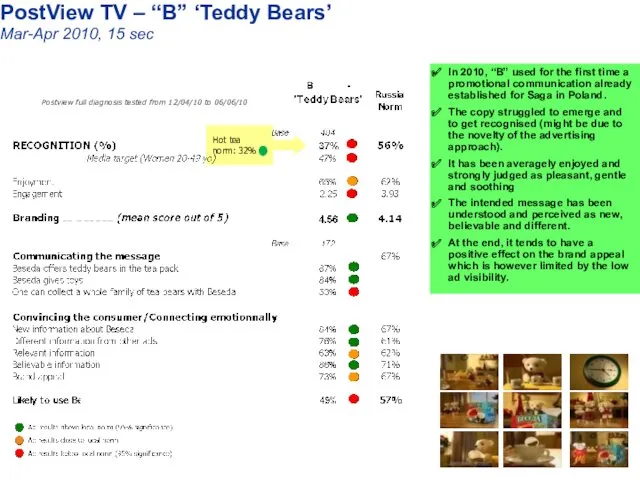

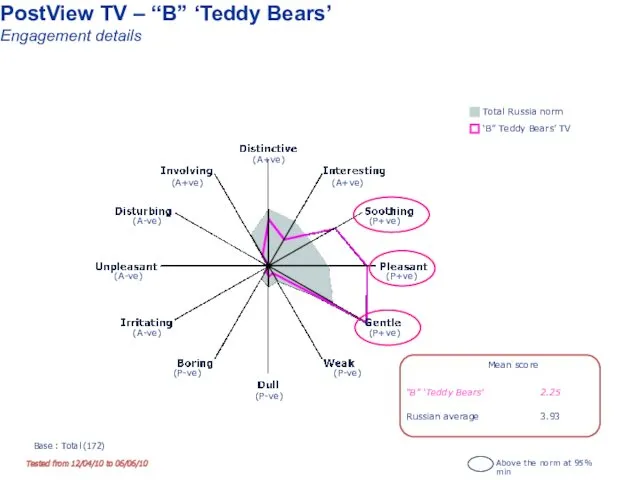

PostView TV – “B” ‘Teddy Bears’

Mar-Apr 2010, 15 sec

Postview full diagnosis tested

PostView TV – “B” ‘Teddy Bears’

Mar-Apr 2010, 15 sec

Postview full diagnosis tested

(P-ve)

(A+ve)

(A+ve)

(P+ve)

(P+ve)

(P+ve)

(P-ve)

(P-ve)

(A-ve)

(A-ve)

(A-ve)

(A+ve)

Total Russia norm

Mean score

“B” ‘Teddy Bears’ 2.25

Russian average 3.93

‘B” Teddy Bears’ TV

Above

(P-ve)

(A+ve)

(A+ve)

(P+ve)

(P+ve)

(P+ve)

(P-ve)

(P-ve)

(A-ve)

(A-ve)

(A-ve)

(A+ve)

Total Russia norm

Mean score

“B” ‘Teddy Bears’ 2.25

Russian average 3.93

‘B” Teddy Bears’ TV

Above

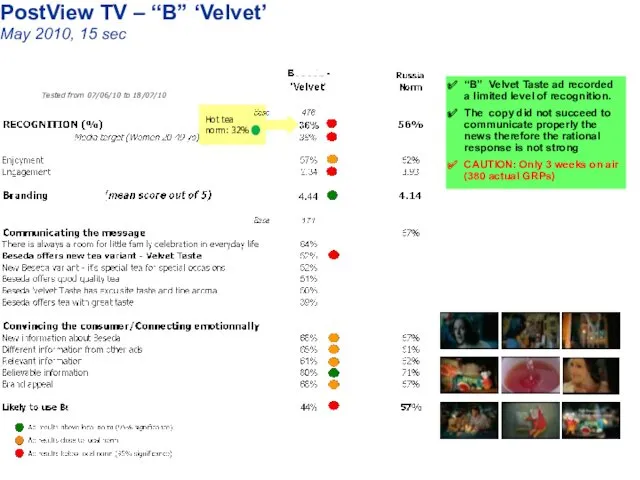

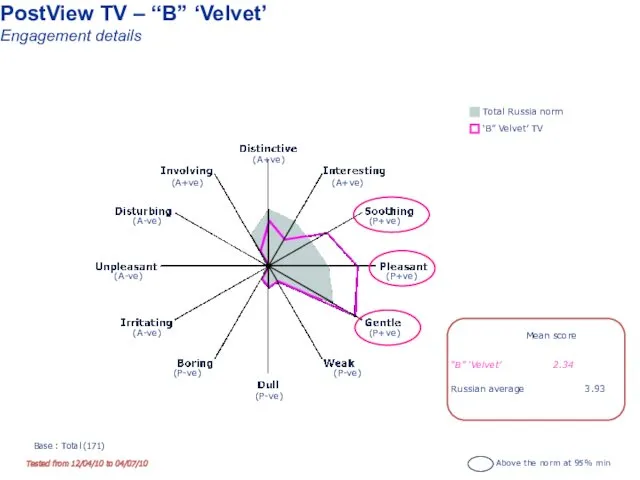

PostView TV – “B” ‘Velvet’

May 2010, 15 sec

Tested from 07/06/10 to 18/07/10

Hot

PostView TV – “B” ‘Velvet’

May 2010, 15 sec

Tested from 07/06/10 to 18/07/10

Hot

(P-ve)

(A+ve)

(A+ve)

(P+ve)

(P+ve)

(P+ve)

(P-ve)

(P-ve)

(A-ve)

(A-ve)

(A-ve)

(A+ve)

Total Russia norm

Mean score

“B” ‘Velvet’ 2.34

Russian average 3.93

‘B” Velvet’ TV

Above the norm

(P-ve)

(A+ve)

(A+ve)

(P+ve)

(P+ve)

(P+ve)

(P-ve)

(P-ve)

(A-ve)

(A-ve)

(A-ve)

(A+ve)

Total Russia norm

Mean score

“B” ‘Velvet’ 2.34

Russian average 3.93

‘B” Velvet’ TV

Above the norm

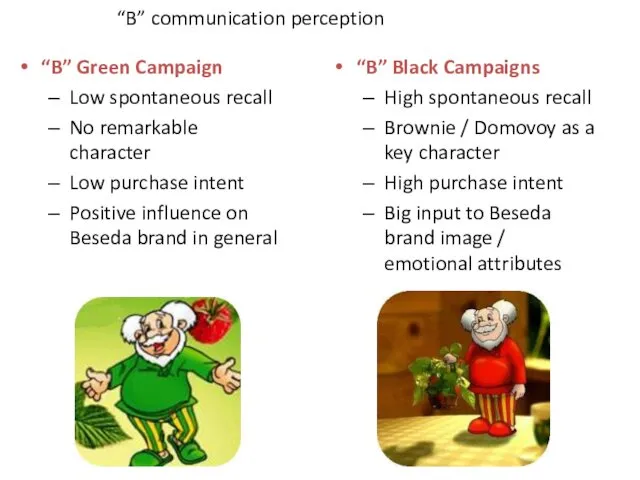

“B” communication perception

“B” Green Campaign

Low spontaneous recall

No remarkable character

Low purchase intent

Positive influence on

“B” communication perception

“B” Green Campaign

Low spontaneous recall

No remarkable character

Low purchase intent

Positive influence on

Princess Noory promo support

1998

2007

2003

2005

2006

2004

2009

2010

Repositioning

after the crisis and offering economy tea.

Result:

Princess Noory promo support

1998

2007

2003

2005

2006

2004

2009

2010

Repositioning

after the crisis and offering economy tea.

Result:

“B” sponsorship (Social Mission)

Sponsor jingle 10 sec (“B” brand Video)

Branded cups on the

“B” sponsorship (Social Mission)

Sponsor jingle 10 sec (“B” brand Video)

Branded cups on the

Competitors’ sponsorship

Competitors’ sponsorship

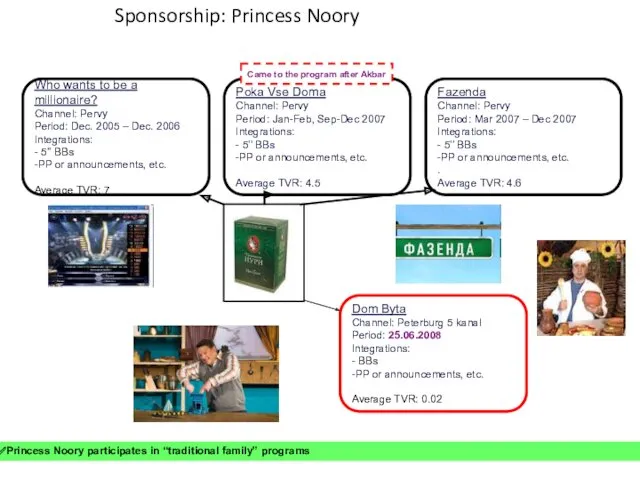

Sponsorship: Princess Noory

Who wants to be a millionaire?

Channel: Pervy

Period: Dec. 2005 – Dec.

Sponsorship: Princess Noory

Who wants to be a millionaire?

Channel: Pervy

Period: Dec. 2005 – Dec.

Green

Rosaria

New

Indian

Summer

Fairy Tale

Turn on TV Game

« B » – Teddy Bears

« B » – Velvet taste

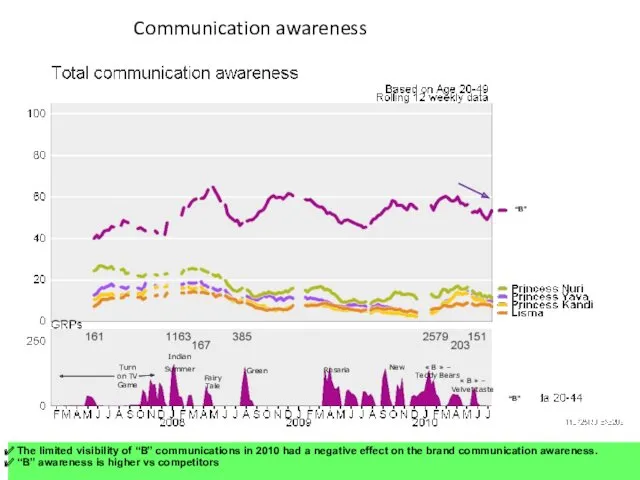

The limited

Green

Rosaria

New

Indian

Summer

Fairy Tale

Turn on TV Game

« B » – Teddy Bears

« B » – Velvet taste

The limited

Green

Indian

Summer

Fairy Tale

Rosaria

New

«B» – Teddy Bears

«B» – Velvet taste

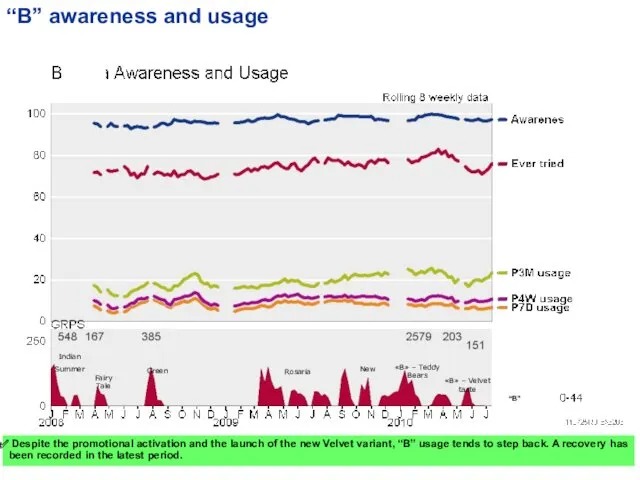

Despite the promotional activation and

Green

Indian

Summer

Fairy Tale

Rosaria

New

«B» – Teddy Bears

«B» – Velvet taste

Despite the promotional activation and

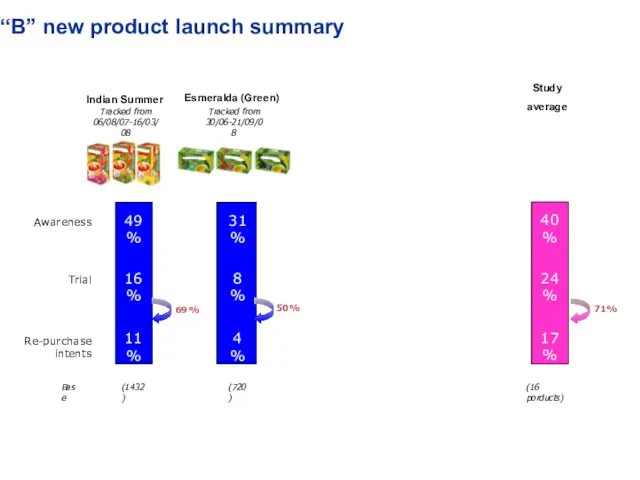

49%

16%

11%

Awareness

Re-purchase intents

Trial

31%

8%

4%

“B” new product launch summary

Indian Summer

Esmeralda (Green)

69%

50%

40%

24%

17%

Study

average

(1432)

(720)

Tracked from

06/08/07-16/03/08

Tracked from

30/06-21/09/08

Base

(16

49%

16%

11%

Awareness

Re-purchase intents

Trial

31%

8%

4%

“B” new product launch summary

Indian Summer

Esmeralda (Green)

69%

50%

40%

24%

17%

Study

average

(1432)

(720)

Tracked from

06/08/07-16/03/08

Tracked from

30/06-21/09/08

Base

(16

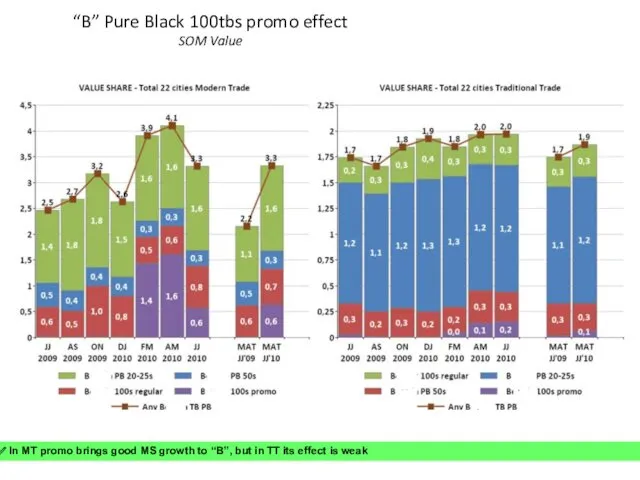

“B” Pure Black 100tbs promo effect

SOM Value

In MT promo brings good MS

“B” Pure Black 100tbs promo effect

SOM Value

In MT promo brings good MS

“B” 100tbs Bears promo

“B” PB 100tbs promo has low WSD in several

“B” 100tbs Bears promo

“B” PB 100tbs promo has low WSD in several

PRODUCT

PRODUCT

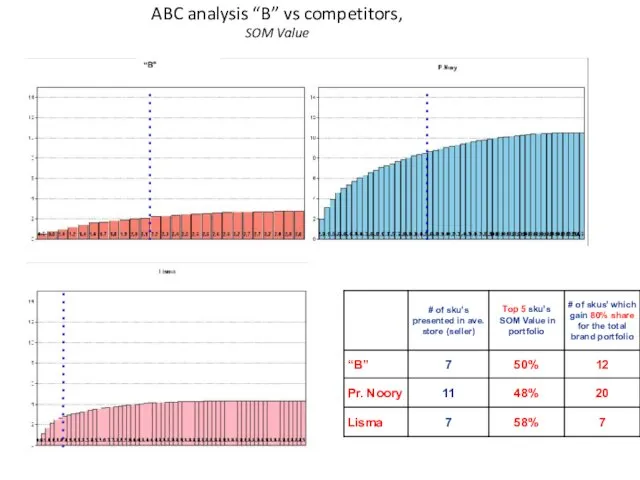

ABC analysis “B” vs competitors,

SOM Value

“B”

ABC analysis “B” vs competitors,

SOM Value

“B”

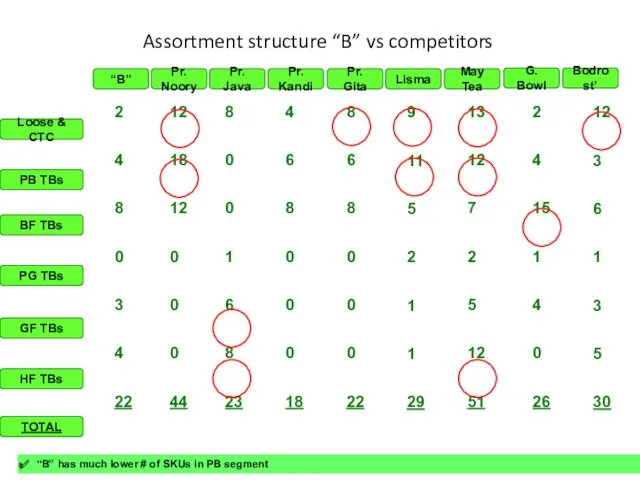

Assortment structure “B” vs competitors

“B”

Pr. Noory

Pr. Java

Pr. Kandi

Pr. Gita

Lisma

May Tea

G. Bowl

Bodrost’

Loose & CTC

PB

Assortment structure “B” vs competitors

“B”

Pr. Noory

Pr. Java

Pr. Kandi

Pr. Gita

Lisma

May Tea

G. Bowl

Bodrost’

Loose & CTC

PB

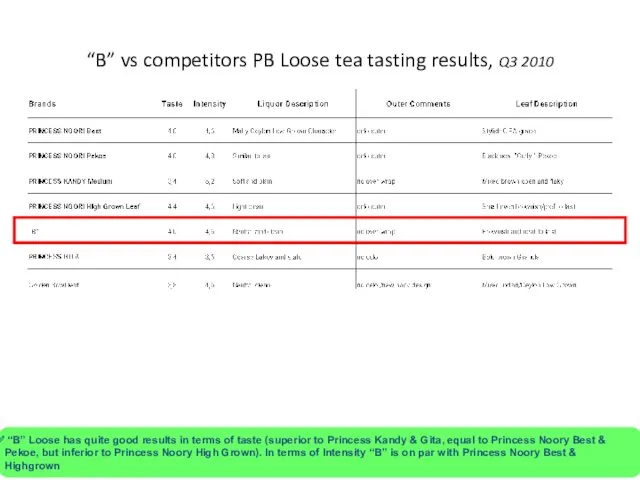

“B” vs competitors PB Loose tea tasting results, Q3 2010

“B” Loose has

“B” vs competitors PB Loose tea tasting results, Q3 2010

“B” Loose has

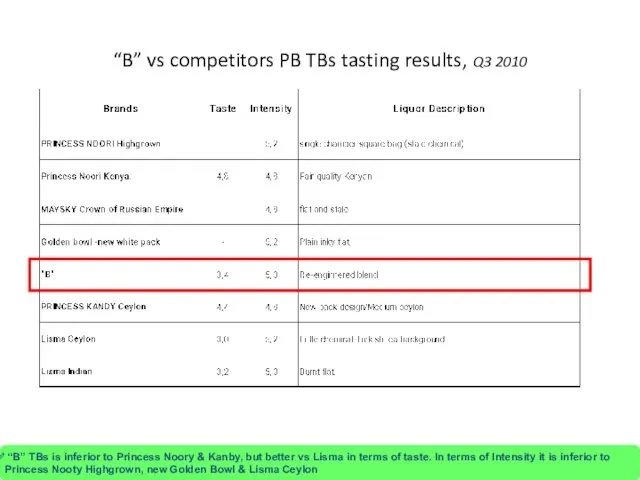

“B” vs competitors PB TBs tasting results, Q3 2010

“B” TBs is inferior

“B” vs competitors PB TBs tasting results, Q3 2010

“B” TBs is inferior

PROPOSITION

PROPOSITION

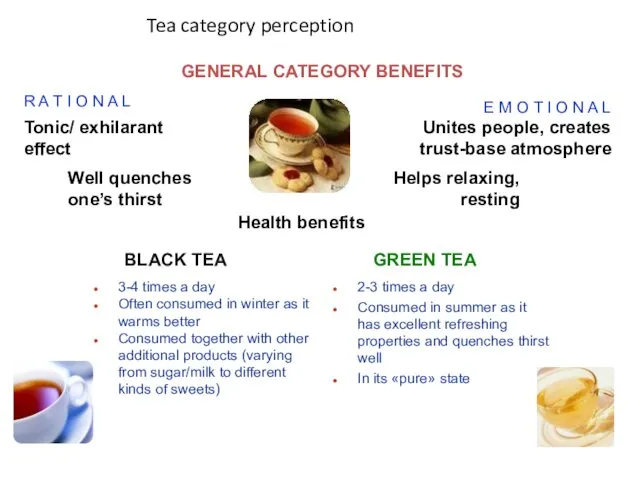

Tea category perception

GENERAL CATEGORY BENEFITS

Tonic/ exhilarant effect

Well quenches one’s thirst

Health benefits

Unites people, creates

Tea category perception

GENERAL CATEGORY BENEFITS

Tonic/ exhilarant effect

Well quenches one’s thirst

Health benefits

Unites people, creates

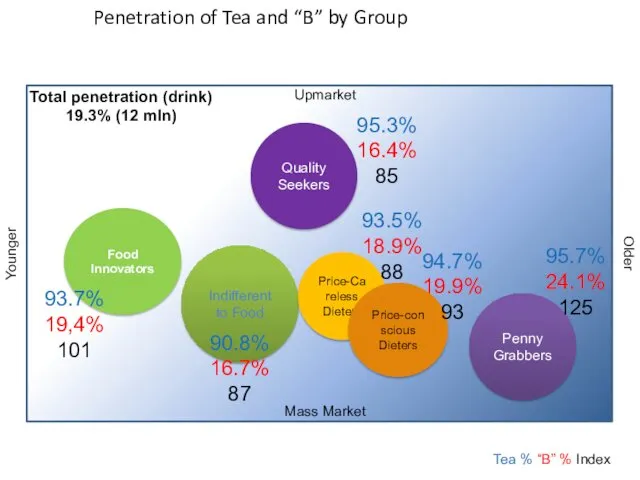

Penetration of Tea and “B” by Group

Food Innovators

Quality Seekers

Penny Grabbers

Indifferent to Food

Mass Market

Upmarket

Older

Younger

Price-Careless

Dieters

Price-conscious

Dieters

95.3%

16.4%

85

93.7%

19,4%

101

90.8%

16.7%

87

Tea

Penetration of Tea and “B” by Group

Food Innovators

Quality Seekers

Penny Grabbers

Indifferent to Food

Mass Market

Upmarket

Older

Younger

Price-Careless

Dieters

Price-conscious

Dieters

95.3%

16.4%

85

93.7%

19,4%

101

90.8%

16.7%

87

Tea

“B” is interesting for…

Dieters try to care about their body, need a small

“B” is interesting for…

Dieters try to care about their body, need a small

Food Innovators

Price-conscious

Dieters

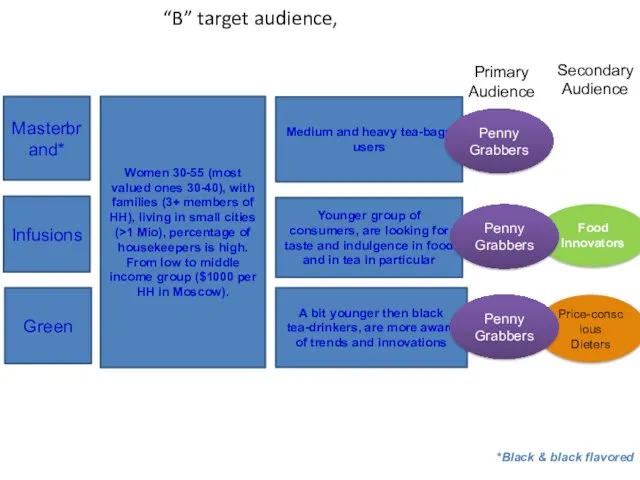

“B” target audience,

Women 30-55 (most valued ones 30-40), with families (3+ members

Food Innovators

Price-conscious

Dieters

“B” target audience,

Women 30-55 (most valued ones 30-40), with families (3+ members

“B”

%

Princess Noory

%

Princess Gita

%

Base: total sample (600)

() - Figures from previous time period

-

“B”

%

Princess Noory

%

Princess Gita

%

Base: total sample (600)

() - Figures from previous time period

-

Better quality

Taste/perform better

Appeal more

Different

Better value

Cost too much

Too cheap

Poor quality for the price

Not meet

Better quality

Taste/perform better

Appeal more

Different

Better value

Cost too much

Too cheap

Poor quality for the price

Not meet

Image positioning mapping

“B” as a popular Russian tea brand, 2009

Note: “Typical Russian

Image positioning mapping

“B” as a popular Russian tea brand, 2009

Note: “Typical Russian

Category drivers of conviction

Winter 07/08

Share of endorsement*

Relevance through good taste

Performance /

Category drivers of conviction

Winter 07/08

Share of endorsement*

Relevance through good taste

Performance /

Base: Total sample (600)

- Significantly different versus previous time period

“B”

Princess Noory

Princess Gita

Princess

Base: Total sample (600)

- Significantly different versus previous time period

“B”

Princess Noory

Princess Gita

Princess

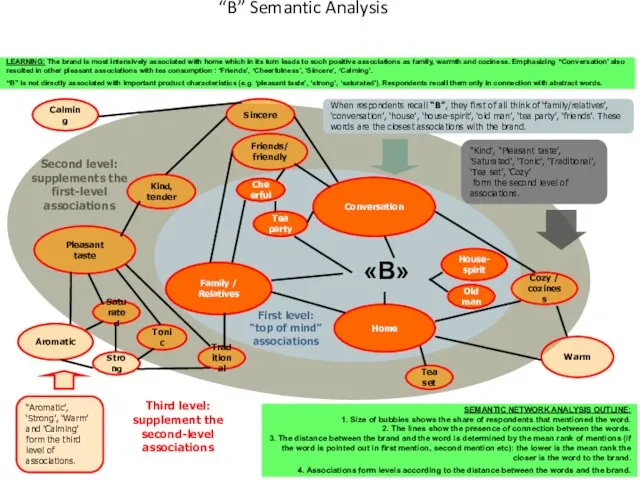

“B” Semantic Analysis

Conversation

Tea party

Friends/ friendly

Family / Relatives

Old man

House-spirit

Home

Sincere

Cozy / coziness

Warm

Kind, tender

Pleasant taste

Traditional

Saturated

Tonic

Tea

set

Aromatic

Strong

When

“B” Semantic Analysis

Conversation

Tea party

Friends/ friendly

Family / Relatives

Old man

House-spirit

Home

Sincere

Cozy / coziness

Warm

Kind, tender

Pleasant taste

Traditional

Saturated

Tonic

Tea

set

Aromatic

Strong

When

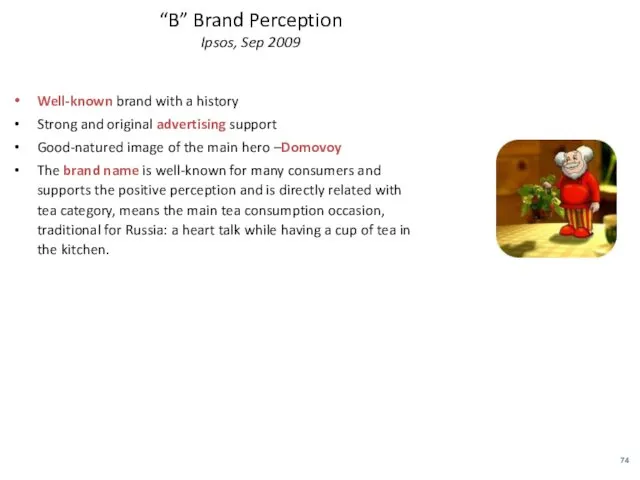

“B” Brand Perception

Ipsos, Sep 2009

Well-known brand with a history

Strong and original advertising support

“B” Brand Perception

Ipsos, Sep 2009

Well-known brand with a history

Strong and original advertising support

PACKAGE

PACKAGE

Players in PB segment: package comparison

“B”

Princess

Noori

May Tea

Lisma

Princess

Kandi

Princess

Gita

Golden

Bowl

Pack

Range (# of

Players in PB segment: package comparison

“B”

Princess

Noori

May Tea

Lisma

Princess

Kandi

Princess

Gita

Golden

Bowl

Pack

Range (# of

Players in BF segment: package comparison

“B”

Princess

Noori

May Tea

Lisma

Princess

Kandi

Princess

Gita

Golden

Bowl

Pack

Range (# of

Players in BF segment: package comparison

“B”

Princess

Noori

May Tea

Lisma

Princess

Kandi

Princess

Gita

Golden

Bowl

Pack

Range (# of

Players in GF segment: package comparison

“B”

Princess

Java

May Tea

Lisma

Golden

Bowl

Pack

Range (# of SKUs)

Country of

Players in GF segment: package comparison

“B”

Princess

Java

May Tea

Lisma

Golden

Bowl

Pack

Range (# of SKUs)

Country of

Players in HF segment: package comparison

“B”

Princess

Java

May Tea

Lisma

Golden

Bowl

Pack

Range (# of SKUs)

Base for

Players in HF segment: package comparison

“B”

Princess

Java

May Tea

Lisma

Golden

Bowl

Pack

Range (# of SKUs)

Base for

“B” packs are less noticeable on shelf in comparison with key competitors –

“B” packs are less noticeable on shelf in comparison with key competitors –

Физико-химические свойства сырья, продукции, реагентов и материалов. (часть 1)

Физико-химические свойства сырья, продукции, реагентов и материалов. (часть 1) Познавательно-исследовательский проект Чудо огород

Познавательно-исследовательский проект Чудо огород Нацистская Германия

Нацистская Германия Инновационные полигоны газоперерабатывающей отрасли НГХК (Нефтегазохимический комплекс)1. Лекция 4

Инновационные полигоны газоперерабатывающей отрасли НГХК (Нефтегазохимический комплекс)1. Лекция 4 Клеточный цикл

Клеточный цикл Движение воздушных масс.Атмосферные фронты.Циклоны и антициклоны 8 класс

Движение воздушных масс.Атмосферные фронты.Циклоны и антициклоны 8 класс Пассивные помехи, ложные цели и ловушки. Тема 8

Пассивные помехи, ложные цели и ловушки. Тема 8 Старостат. Лекция для старост 1 курса Санкт-Петербургского политехнического университета имени Петра Великого

Старостат. Лекция для старост 1 курса Санкт-Петербургского политехнического университета имени Петра Великого Значение бутербродов

Значение бутербродов Глобальные проблемы

Глобальные проблемы Опрессовка

Опрессовка Динамика движения

Динамика движения Балалар және ересектердегі угри ауруы

Балалар және ересектердегі угри ауруы Юрий Алексеевич Гагарин

Юрий Алексеевич Гагарин Процессы физико-химической обработки

Процессы физико-химической обработки Катастрофа Ту-134 в Куйбышеве 20 октября 1986 года

Катастрофа Ту-134 в Куйбышеве 20 октября 1986 года методическая разработка по профилактике дисграфии у дошкольников

методическая разработка по профилактике дисграфии у дошкольников Строение иммунной системы

Строение иммунной системы Теорема Пифагора. Шаржи

Теорема Пифагора. Шаржи Деловая игра для педагогов Гиперактивный ребенок в детском саду

Деловая игра для педагогов Гиперактивный ребенок в детском саду Мультимедийные технологии

Мультимедийные технологии Презентация В гостях у сказки

Презентация В гостях у сказки Слагаемые успеха в бизнесе

Слагаемые успеха в бизнесе Водоснабжение завода по переработке керамических изделий

Водоснабжение завода по переработке керамических изделий Выступление МАОУ24 14.02.22 Гришаткина С.А

Выступление МАОУ24 14.02.22 Гришаткина С.А Символика Приморского края, Надеждинского района и п. Раздольное

Символика Приморского края, Надеждинского района и п. Раздольное Химия в сельском хозяйстве. 9 кл.

Химия в сельском хозяйстве. 9 кл. Психика және сана

Психика және сана