- Securitization and credit crises

Содержание

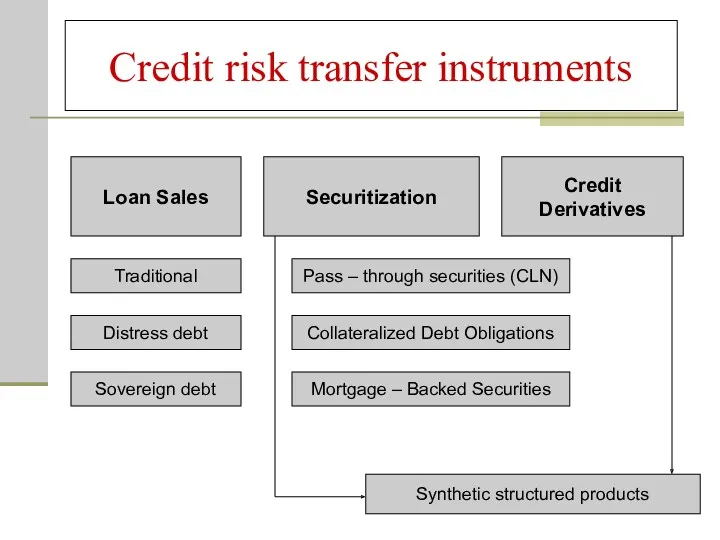

- 2. Credit risk transfer instruments Loan Sales Securitization Credit Derivatives Traditional Distress debt Sovereign debt Pass –

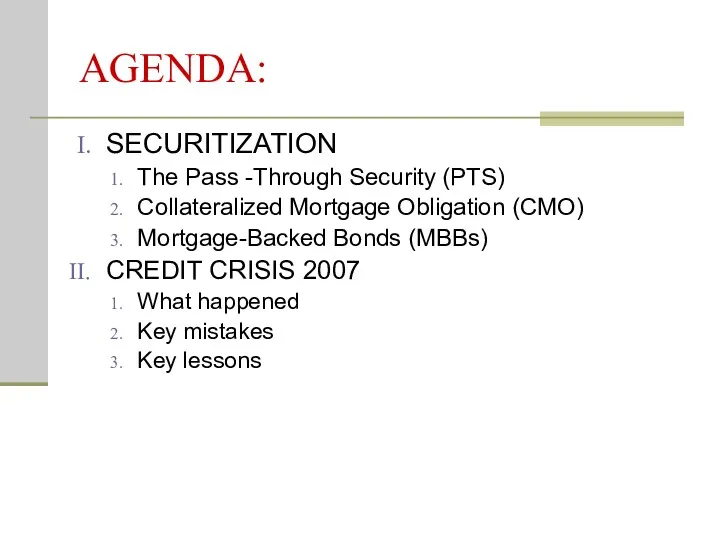

- 3. AGENDA: SECURITIZATION The Pass -Through Security (PTS) Collateralized Mortgage Obligation (CMO) Mortgage-Backed Bonds (MBBs) CREDIT CRISIS

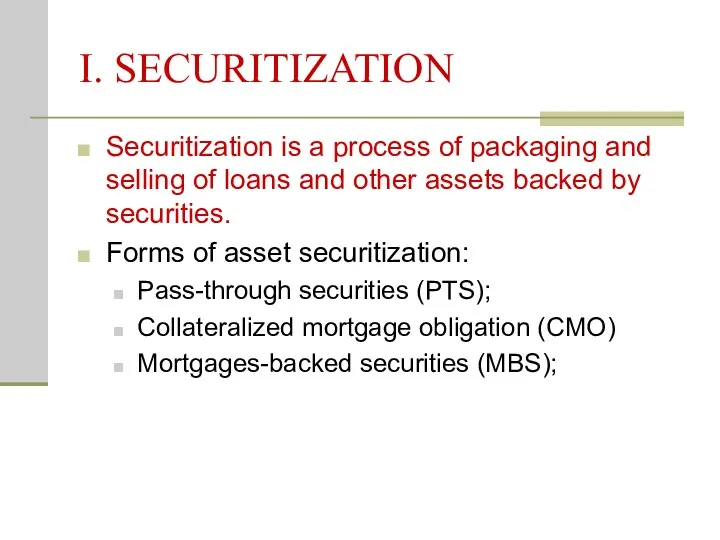

- 4. I. SECURITIZATION Securitization is a process of packaging and selling of loans and other assets backed

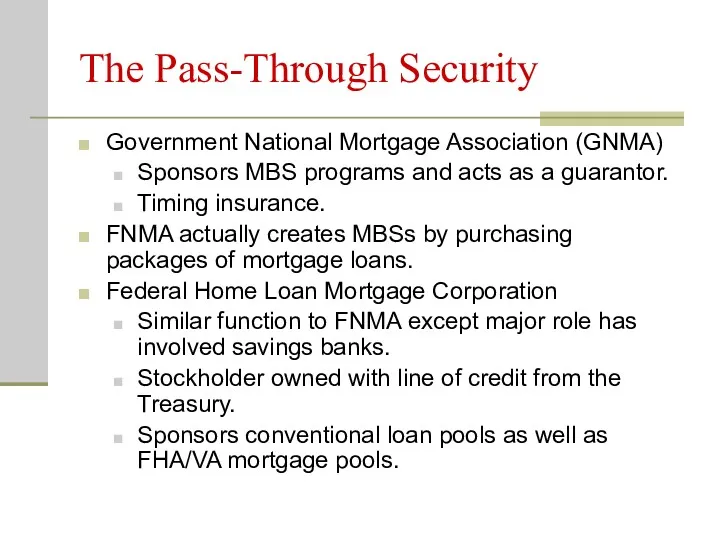

- 5. The Pass-Through Security Government National Mortgage Association (GNMA) Sponsors MBS programs and acts as a guarantor.

- 6. Major Benefits of Securitisation: lower cost of funding due to the enhanced rating stemming from mixed

- 7. Incentives and Mechanics of Pass-Through Security Creation Example: Assume that Bank has 1000 new residential mortgages

- 8. Mechanics of Pass-Through Security Creation Bank pays annual insurance premium to the FDIC. Assume the deposit

- 9. GNMA Pass-Through process: Creation of the Asset backed security (ABS) Mortgage credit insurance Bank Mortgages 2.

- 10. Calculation of a constant monthly payment of borrowers: Size of the pool: PV = $100 000

- 11. Payment schedule Fully amortized mortgages:

- 12. GNMA Pass-Through process The bank aggregates the payments for mortgages and passes funds through to GNMA

- 13. Further Incentives The attractiveness of these bonds to investors. In particular, investors in these bonds are

- 14. Effects of prepayments Prepayment risk is the risk that the loan will be paid off before

- 15. Asset Backed Security (continued)

- 16. The Waterfall Equity Tranche 1st loss 2nd loss, if 1st loss is more than 5% 3d

- 17. Collateralized Mortgage Obligations (ABS CMO) were created to manage the prepayment risk Assets Senior Tranche (80%)

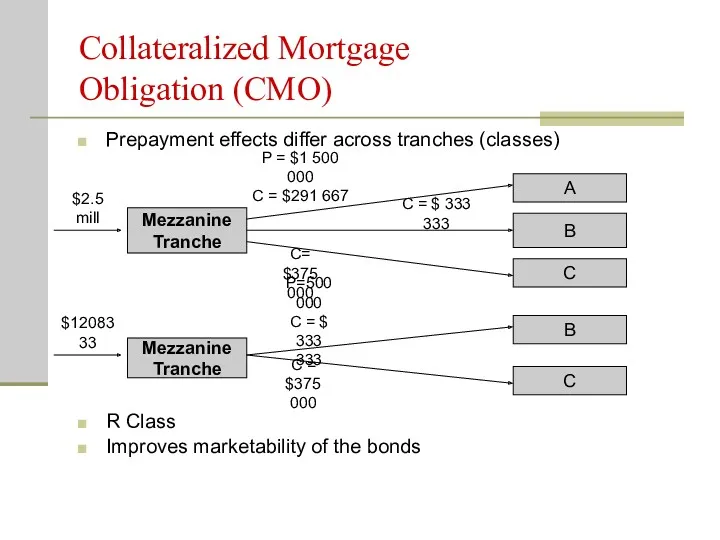

- 18. Collateralized Mortgage Obligation (CMO) Prepayment effects differ across tranches (classes) R Class Improves marketability of the

- 19. Mortgage-Backed Bonds (MBBs) Normally remain on the balance sheet. No direct link between the cash flows

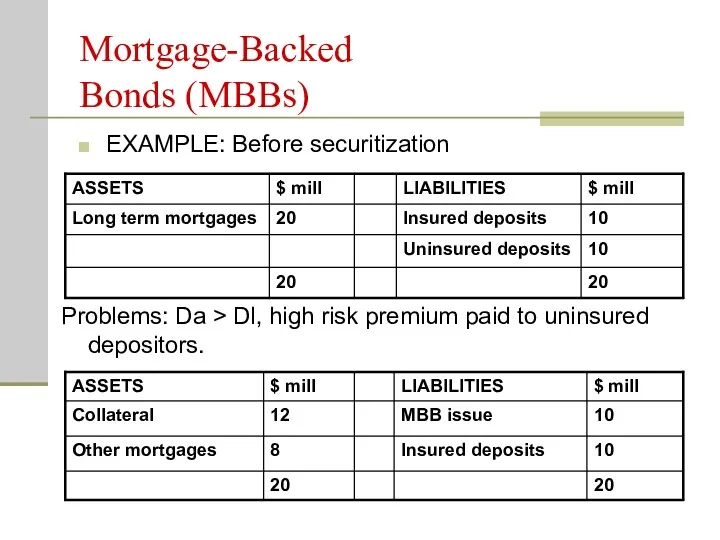

- 20. Mortgage-Backed Bonds (MBBs) EXAMPLE: Before securitization Problems: Da > Dl, high risk premium paid to uninsured

- 21. Mortgage-Backed Bonds (MBBs) Weaknesses: Tied up mortgages on the balance sheet for a long time; Increases

- 22. Securitization of other assets CARDs Various receivables, loans, junk bonds, ARMs. Can all assets be securitized?

- 23. U.S. Real Estate Prices, 1987 to 2009: S&P/Case-Shiller Composite-10 Index Credit Crisis 2007

- 24. What happened… Relaxation of Mortgage standards Starting in 2000, mortgage originators in the US relaxed their

- 25. What happened... Mortgages were packaged in financial products and sold to investors: The most important thing

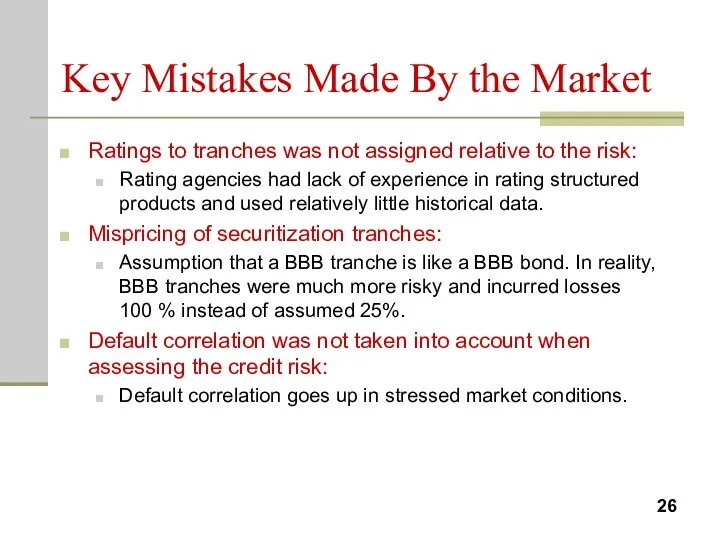

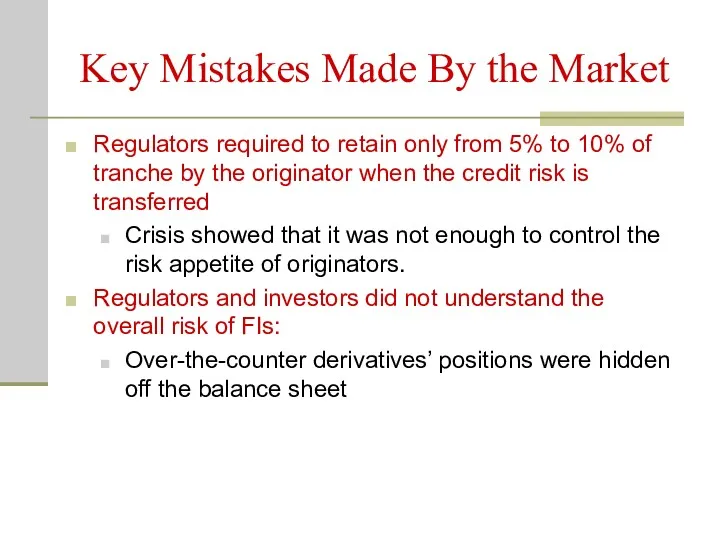

- 26. Key Mistakes Made By the Market Ratings to tranches was not assigned relative to the risk:

- 27. Key Mistakes Made By the Market Regulators required to retain only from 5% to 10% of

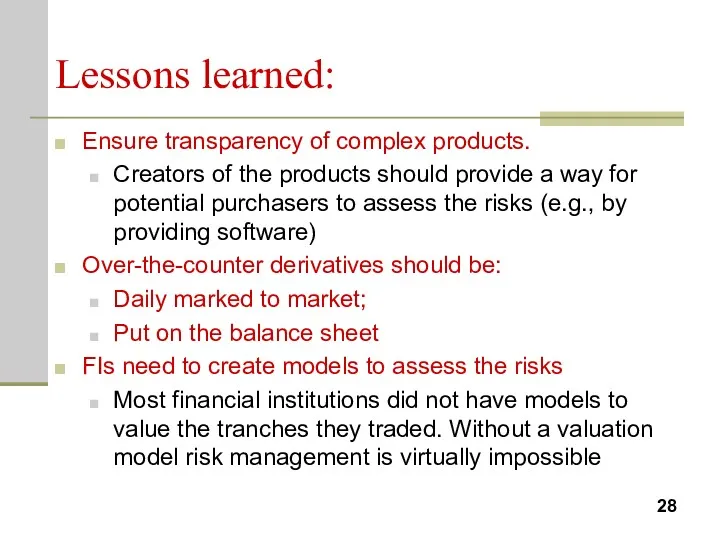

- 28. Lessons learned: Ensure transparency of complex products. Creators of the products should provide a way for

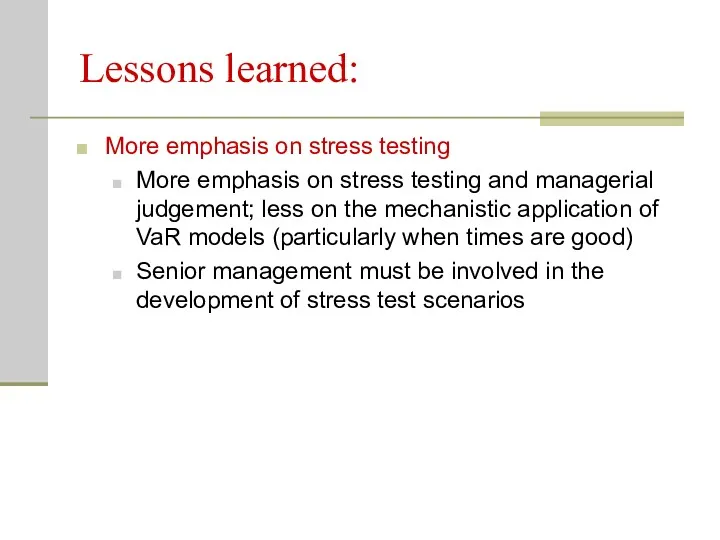

- 29. Lessons learned: More emphasis on stress testing More emphasis on stress testing and managerial judgement; less

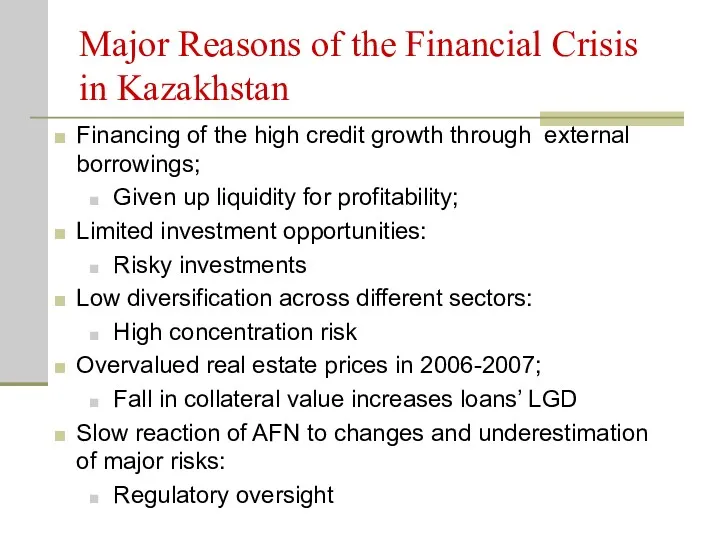

- 30. Major Reasons of the Financial Crisis in Kazakhstan Financing of the high credit growth through external

- 31. Why Financial Crisis in Kazakhstan was not so severe as in developed countries? Proportion of foreign

- 32. Real Estate Price Dynamic in Kazakhstan

- 33. Structural changes in Kazakhstani banking industry since 2008.

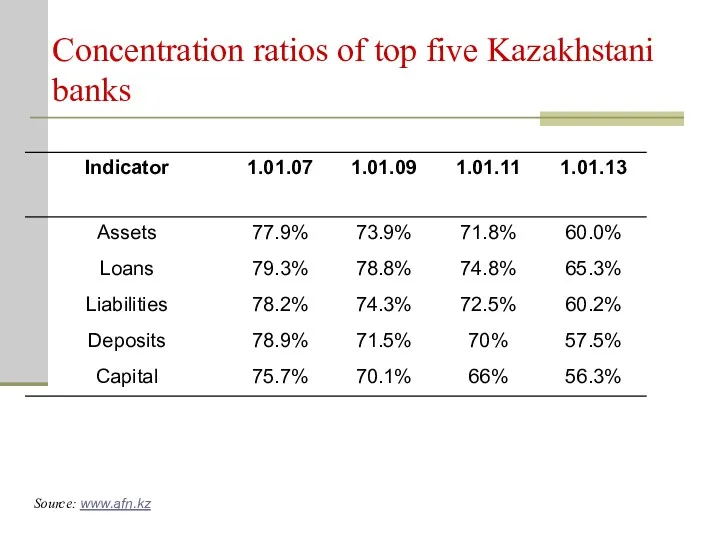

- 34. Concentration ratios of top five Kazakhstani banks Source: www.afn.kz

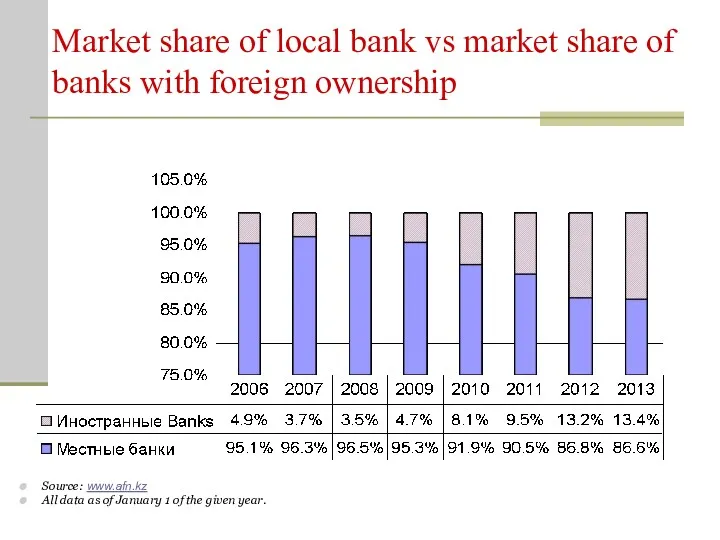

- 35. Market share of local bank vs market share of banks with foreign ownership Source: www.afn.kz All

- 37. Скачать презентацию

Credit risk transfer instruments

Loan Sales

Securitization

Credit Derivatives

Traditional

Distress debt

Sovereign debt

Pass

Credit risk transfer instruments

Loan Sales

Securitization

Credit Derivatives

Traditional

Distress debt

Sovereign debt

Pass

AGENDA:

SECURITIZATION

The Pass -Through Security (PTS)

Collateralized Mortgage Obligation (CMO)

Mortgage-Backed Bonds (MBBs)

CREDIT CRISIS

AGENDA:

SECURITIZATION

The Pass -Through Security (PTS)

Collateralized Mortgage Obligation (CMO)

Mortgage-Backed Bonds (MBBs)

CREDIT CRISIS

I. SECURITIZATION

Securitization is a process of packaging and selling of loans

I. SECURITIZATION

Securitization is a process of packaging and selling of loans

The Pass-Through Security

Government National Mortgage Association (GNMA)

Sponsors MBS programs and acts

The Pass-Through Security

Government National Mortgage Association (GNMA)

Sponsors MBS programs and acts

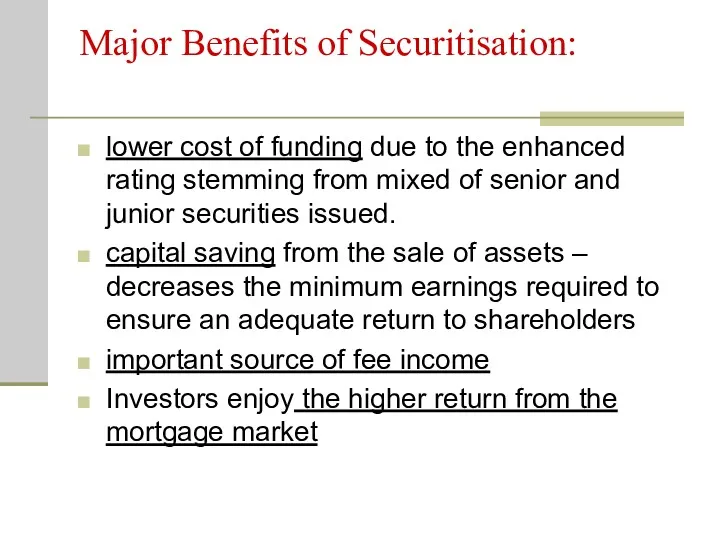

Major Benefits of Securitisation:

lower cost of funding due to the enhanced

Major Benefits of Securitisation:

lower cost of funding due to the enhanced

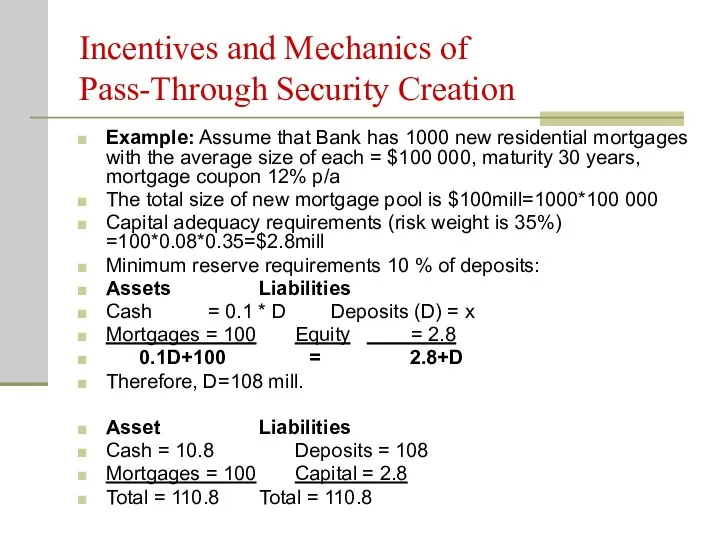

Incentives and Mechanics of

Pass-Through Security Creation

Example: Assume that Bank has

Incentives and Mechanics of

Pass-Through Security Creation

Example: Assume that Bank has

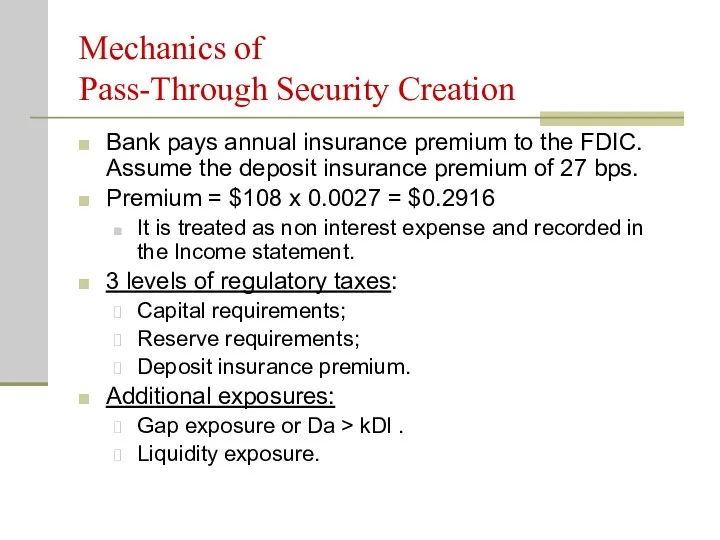

Mechanics of

Pass-Through Security Creation

Bank pays annual insurance premium to the

Mechanics of

Pass-Through Security Creation

Bank pays annual insurance premium to the

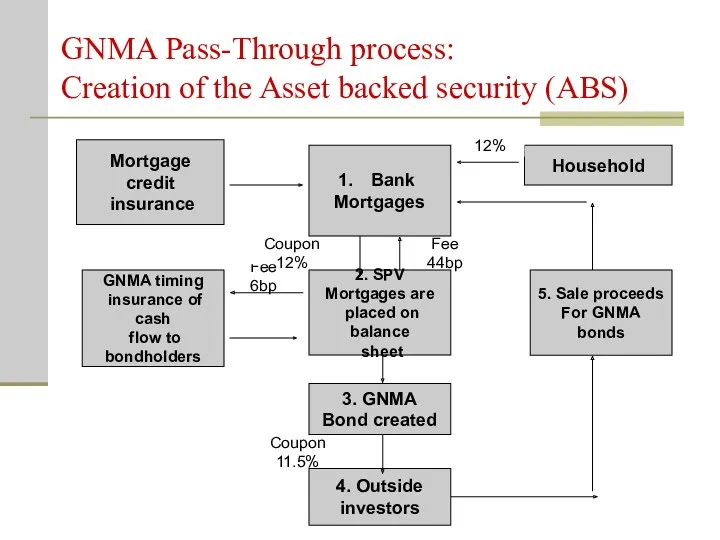

GNMA Pass-Through process:

Creation of the Asset backed security (ABS)

Mortgage credit

insurance

Bank

Mortgages

2.

GNMA Pass-Through process:

Creation of the Asset backed security (ABS)

Mortgage credit

insurance

Bank

Mortgages

2.

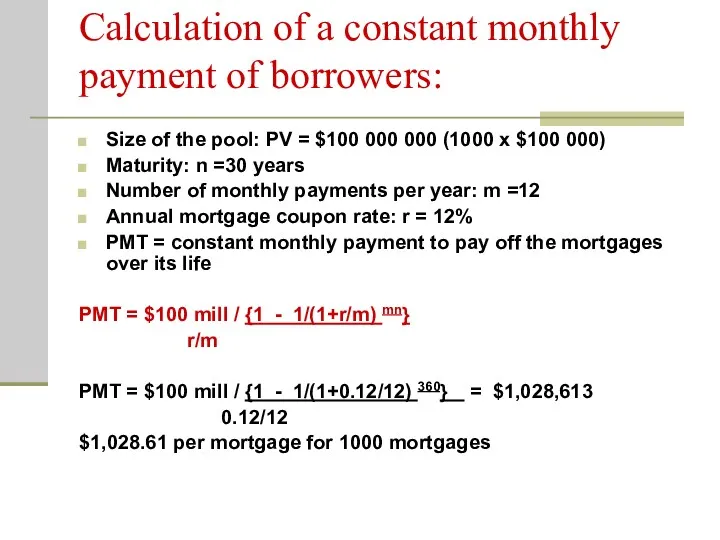

Calculation of a constant monthly payment of borrowers:

Size of the

Calculation of a constant monthly payment of borrowers:

Size of the

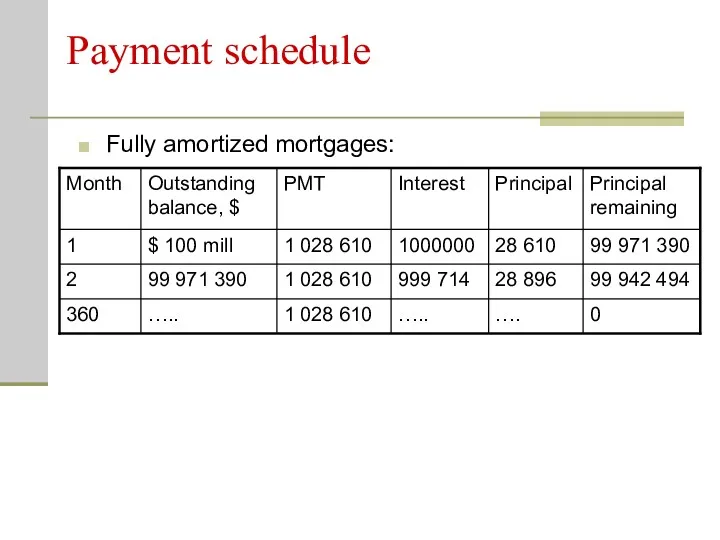

Payment schedule

Fully amortized mortgages:

Payment schedule

Fully amortized mortgages:

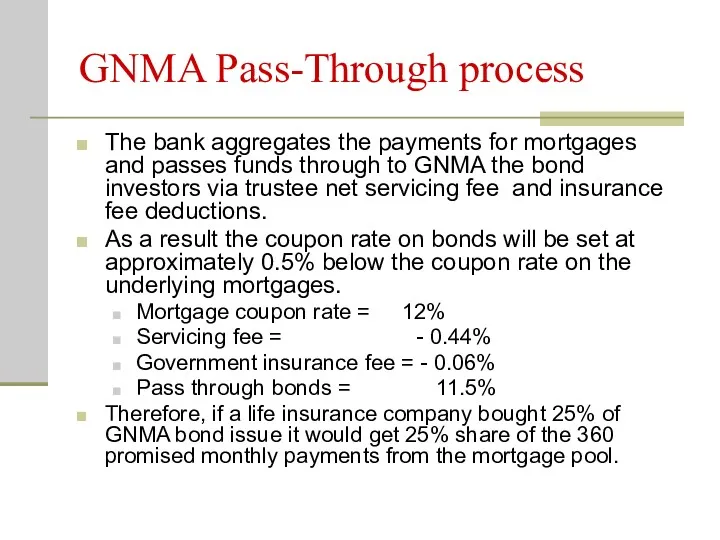

GNMA Pass-Through process

The bank aggregates the payments for mortgages and passes

GNMA Pass-Through process

The bank aggregates the payments for mortgages and passes

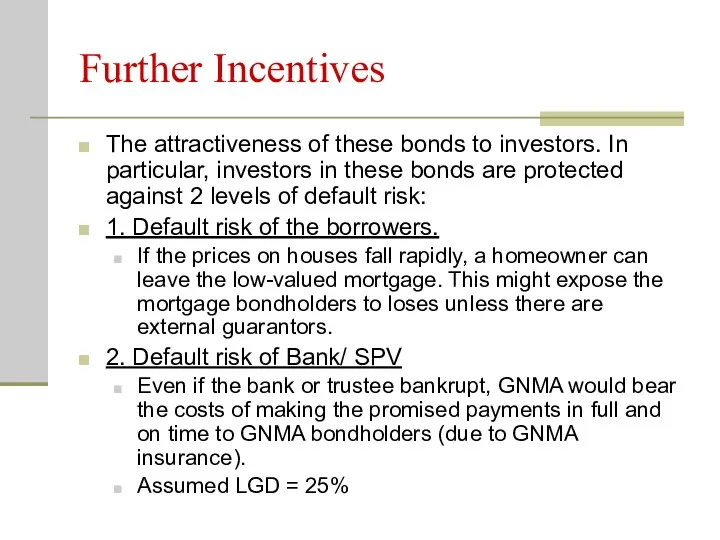

Further Incentives

The attractiveness of these bonds to investors. In particular, investors

Further Incentives

The attractiveness of these bonds to investors. In particular, investors

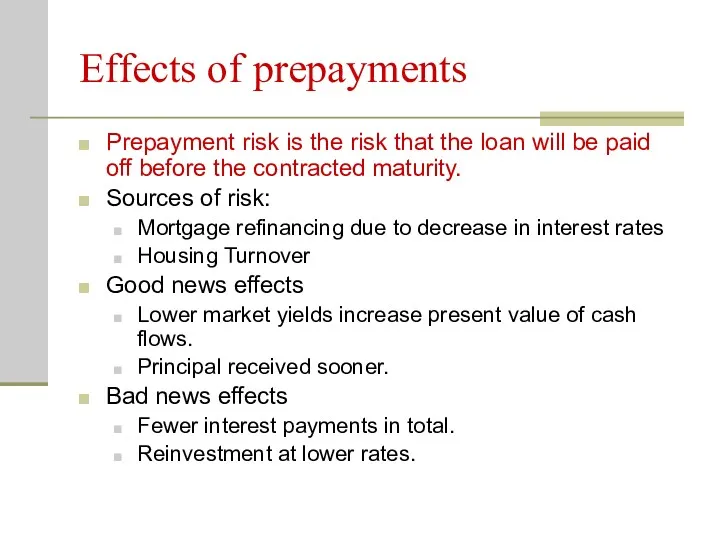

Effects of prepayments

Prepayment risk is the risk that the loan will

Effects of prepayments

Prepayment risk is the risk that the loan will

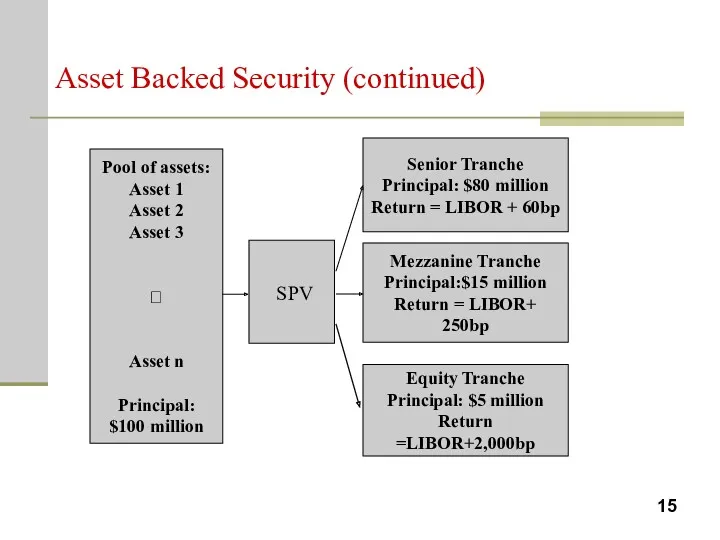

Asset Backed Security (continued)

Asset Backed Security (continued)

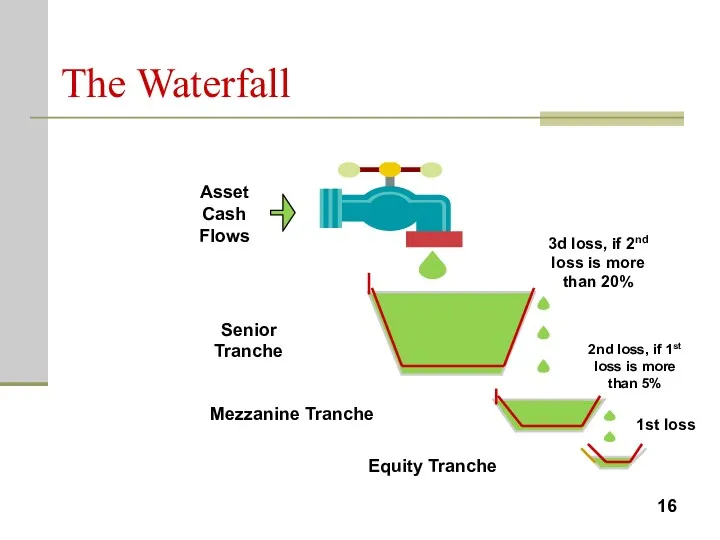

The Waterfall

Equity Tranche

1st loss

2nd loss, if 1st loss is more than

The Waterfall

Equity Tranche

1st loss

2nd loss, if 1st loss is more than

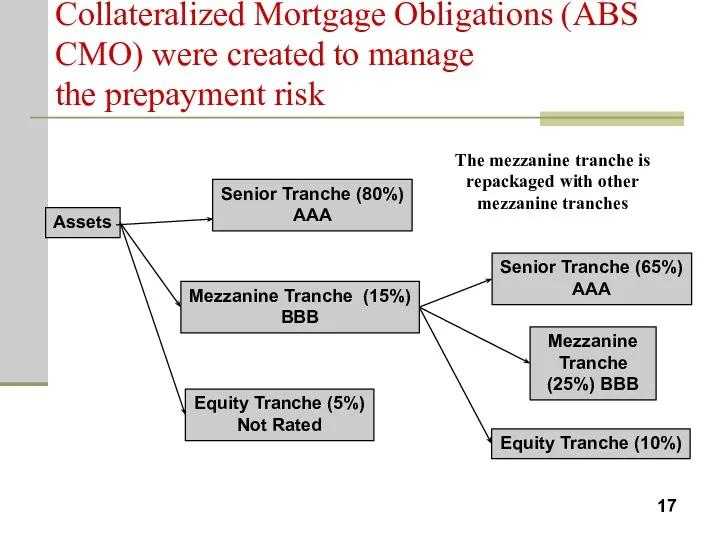

Collateralized Mortgage Obligations (ABS CMO) were created to manage

the prepayment

Collateralized Mortgage Obligations (ABS CMO) were created to manage the prepayment

Collateralized Mortgage

Obligation (CMO)

Prepayment effects differ across tranches (classes)

R Class

Improves marketability

Collateralized Mortgage

Obligation (CMO)

Prepayment effects differ across tranches (classes)

R Class

Improves marketability

Mortgage-Backed

Bonds (MBBs)

Normally remain on the balance sheet.

No direct link between

Mortgage-Backed

Bonds (MBBs)

Normally remain on the balance sheet.

No direct link between

Mortgage-Backed

Bonds (MBBs)

EXAMPLE: Before securitization

Problems: Da > Dl, high risk

Mortgage-Backed

Bonds (MBBs)

EXAMPLE: Before securitization

Problems: Da > Dl, high risk

Mortgage-Backed

Bonds (MBBs)

Weaknesses:

Tied up mortgages on the balance sheet for a

Mortgage-Backed

Bonds (MBBs)

Weaknesses:

Tied up mortgages on the balance sheet for a

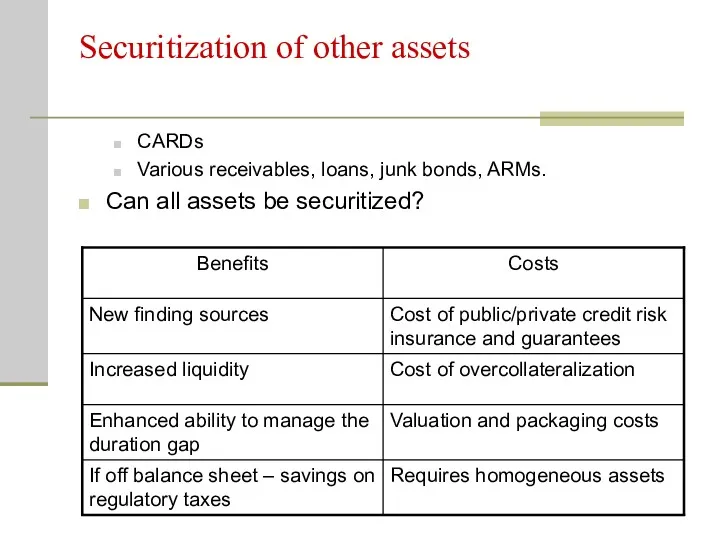

Securitization of other assets

CARDs

Various receivables, loans, junk bonds, ARMs.

Can all assets

Securitization of other assets

CARDs

Various receivables, loans, junk bonds, ARMs.

Can all assets

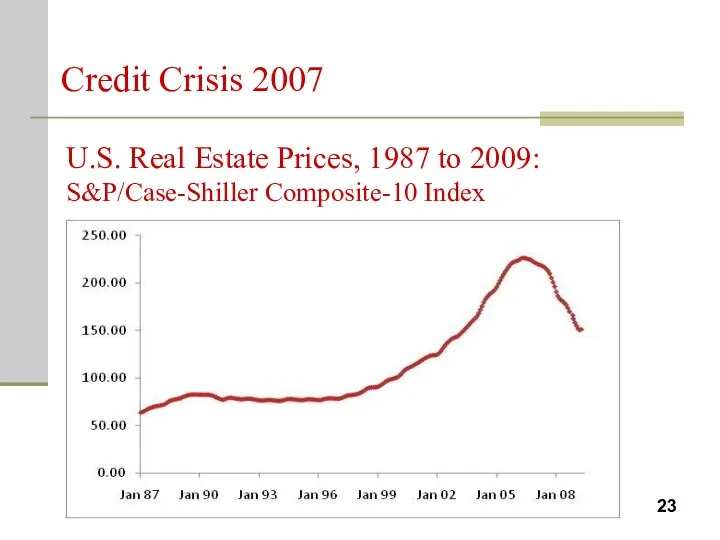

U.S. Real Estate Prices, 1987 to 2009: S&P/Case-Shiller Composite-10 Index

Credit Crisis

U.S. Real Estate Prices, 1987 to 2009: S&P/Case-Shiller Composite-10 Index

Credit Crisis

What happened…

Relaxation of Mortgage standards

Starting in 2000, mortgage originators in the

What happened…

Relaxation of Mortgage standards

Starting in 2000, mortgage originators in the

What happened...

Mortgages were packaged in financial products and sold to investors:

The

What happened...

Mortgages were packaged in financial products and sold to investors:

The

Key Mistakes Made By the Market

Ratings to tranches was not assigned

Key Mistakes Made By the Market

Ratings to tranches was not assigned

Key Mistakes Made By the Market

Regulators required to retain only from

Key Mistakes Made By the Market

Regulators required to retain only from

Lessons learned:

Ensure transparency of complex products.

Creators of the products should

Lessons learned:

Ensure transparency of complex products.

Creators of the products should

Lessons learned:

More emphasis on stress testing

More emphasis on stress testing and

Lessons learned:

More emphasis on stress testing

More emphasis on stress testing and

Major Reasons of the Financial Crisis

in Kazakhstan

Financing of the high

Major Reasons of the Financial Crisis

in Kazakhstan

Financing of the high

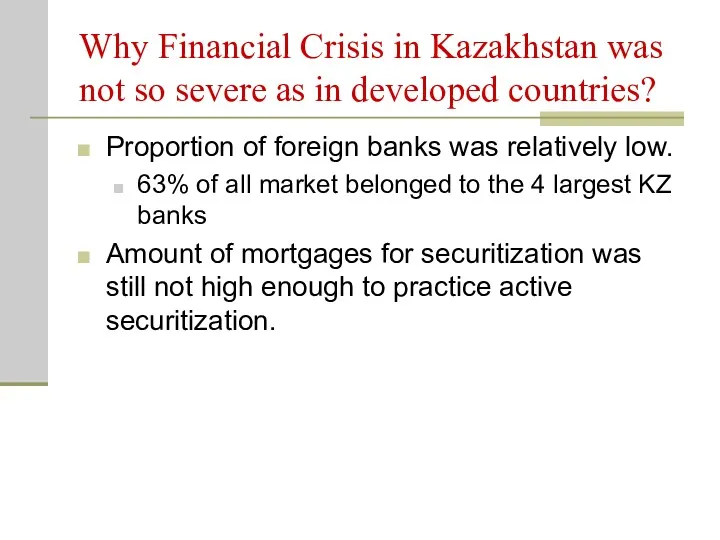

Why Financial Crisis in Kazakhstan was not so severe as in

Why Financial Crisis in Kazakhstan was not so severe as in

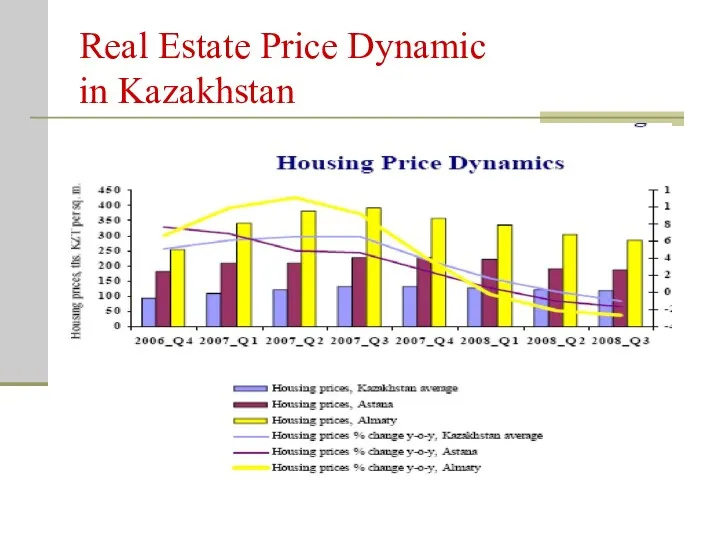

Real Estate Price Dynamic

in Kazakhstan

Real Estate Price Dynamic

in Kazakhstan

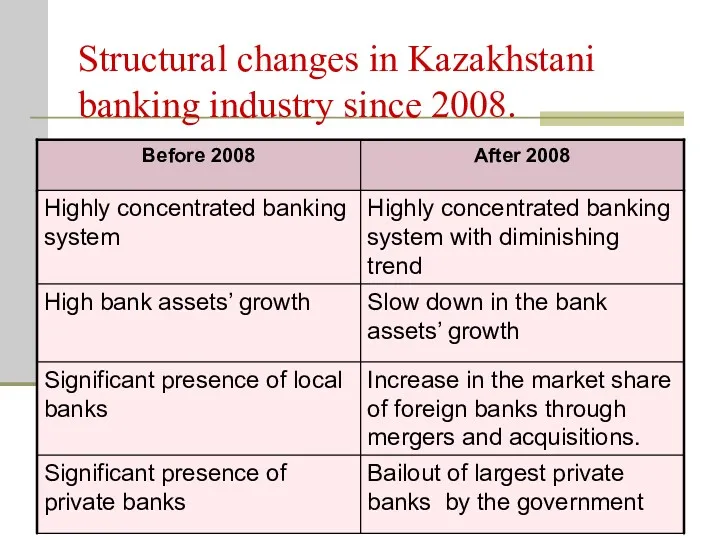

Structural changes in Kazakhstani banking industry since 2008.

Structural changes in Kazakhstani banking industry since 2008.

Concentration ratios of top five Kazakhstani banks

Source: www.afn.kz

Concentration ratios of top five Kazakhstani banks

Source: www.afn.kz

Market share of local bank vs market share of banks with

Market share of local bank vs market share of banks with

Полимеры в нашей жизни

Полимеры в нашей жизни Методы биометрической диагностики зубочелюстных аномалий у детей

Методы биометрической диагностики зубочелюстных аномалий у детей Презентация. Игровые технологии на занятиях в ДОУ.

Презентация. Игровые технологии на занятиях в ДОУ. Психологическая помощь детям и подросткам с отклонениями в развитии. Виды психологической помощи

Психологическая помощь детям и подросткам с отклонениями в развитии. Виды психологической помощи Шаблоны пазлов

Шаблоны пазлов Презентация 8 марта для старшего дошкольного возраста

Презентация 8 марта для старшего дошкольного возраста Проект. Адаптационный клуб В детский сад с улыбкой

Проект. Адаптационный клуб В детский сад с улыбкой Результаты ОГЭ и ЕГЭ по обществознанию. МБОУ СОШ №39 г.Чебоксары ЧР

Результаты ОГЭ и ЕГЭ по обществознанию. МБОУ СОШ №39 г.Чебоксары ЧР С 8 Марта

С 8 Марта Культура СССР в годы Великой Отечественной войны

Культура СССР в годы Великой Отечественной войны Машиностроение

Машиностроение Я хочу знать русский язык

Я хочу знать русский язык Юридическая ответственность и ее задачи. Лекция №7

Юридическая ответственность и ее задачи. Лекция №7 Дыхательная система человека. Эволюция органов дыхания

Дыхательная система человека. Эволюция органов дыхания Summer holidays and activities flashcards

Summer holidays and activities flashcards Параллельный перенос

Параллельный перенос Оценка качества зданий. Показатели качества зданий. Обследование зданий

Оценка качества зданий. Показатели качества зданий. Обследование зданий Clothes (4)

Clothes (4) Это мы

Это мы Простое оштукатуривание стен строительного склада цементным раствором и ремонт облицовки пола керамической метлахской плиткой

Простое оштукатуривание стен строительного склада цементным раствором и ремонт облицовки пола керамической метлахской плиткой Инновационные технологии развития музыкальной культуры старших дошкольников в воспитательном пространстве праздника

Инновационные технологии развития музыкальной культуры старших дошкольников в воспитательном пространстве праздника Интерактивное ТВ

Интерактивное ТВ Шаблон 9 мая. Зима

Шаблон 9 мая. Зима Выступление

Выступление Superheroes. Comparisons

Superheroes. Comparisons США. Интегрированный урок английский язык и география

США. Интегрированный урок английский язык и география Принципы управления А. Файоля и Э. Деминга

Принципы управления А. Файоля и Э. Деминга Тоталитаризм. Отрицательные черты

Тоталитаризм. Отрицательные черты