- Entrepreneurship in Russia

Содержание

- 2. Subjects of small and medium-size business in Russia

- 3. Subjects of small business in Russia According to the Federal law of Russian Federation “About small

- 4. Forms of business activities in Russia Sole proprietorship (individual entrepreneur) Legal entity (commercial and non-commercial companies)

- 5. Special features of individual entrepreneur and legal entity.

- 6. Special features of individual entrepreneur and legal entity. Simplified!

- 7. FORMS OF LEGAL ENTITIES WIDELY USED IN RUSSIA

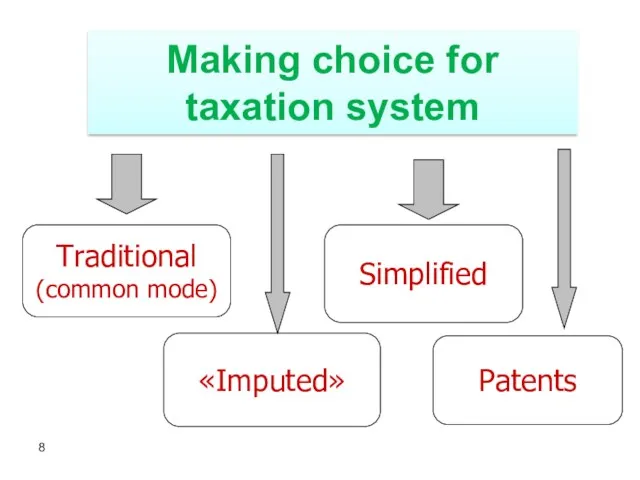

- 8. Making choice for taxation system Patents

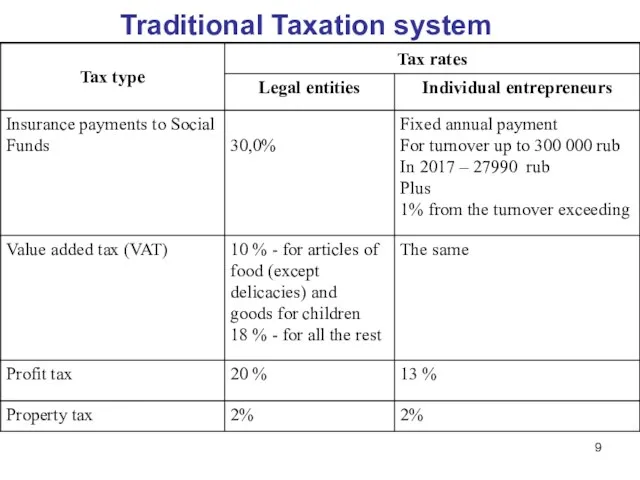

- 9. Traditional Taxation system

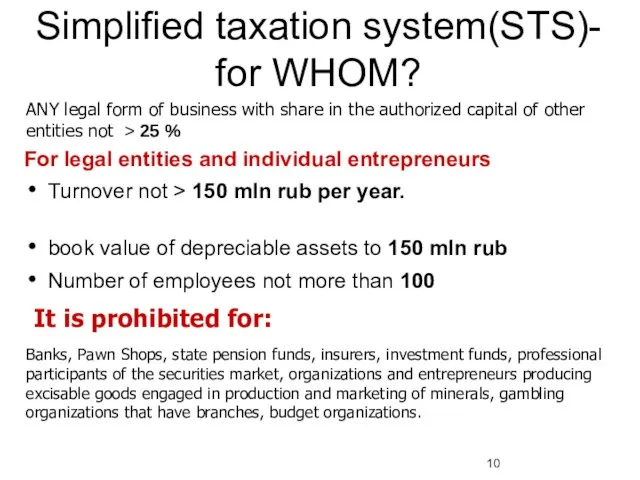

- 10. For legal entities and individual entrepreneurs Turnover not > 150 mln rub per year. book value

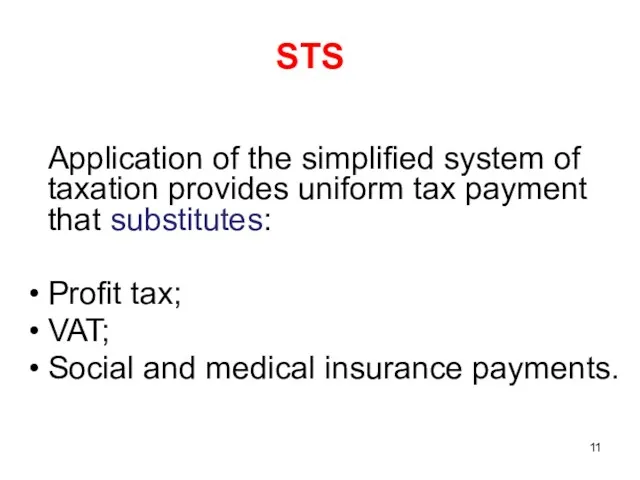

- 11. STS Application of the simplified system of taxation provides uniform tax payment that substitutes: Profit tax;

- 12. STS – how much to PAY? Changes of tax base only once in a year before

- 13. «STS» Pluses and Minuses Main advantages: LESS TAXES POSSIBILITY OF MAKING CHOICE FOR TAXATION BASE SIMPLIFIED

- 14. «Imputed» system: features

- 15. «IMPUTED» - WHO IS PAYING? It differs for the regions in Russia: Retail (sales area not>

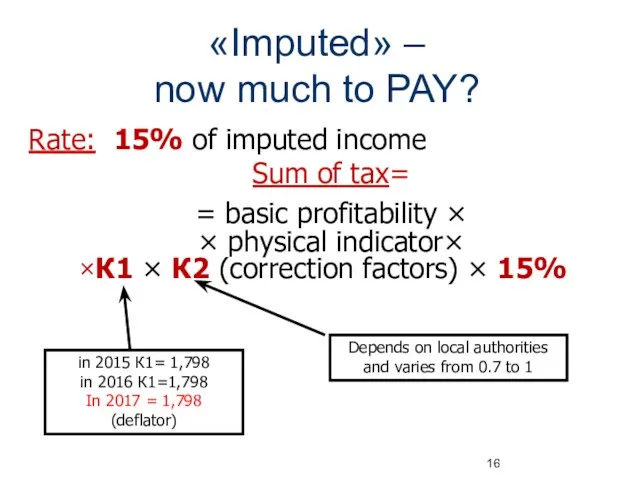

- 16. «Imputed» – now much to PAY? Rate: 15% of imputed income Sum of tax= = basic

- 18. Скачать презентацию

Subjects of small and medium-size business in Russia

Subjects of small and medium-size business in Russia

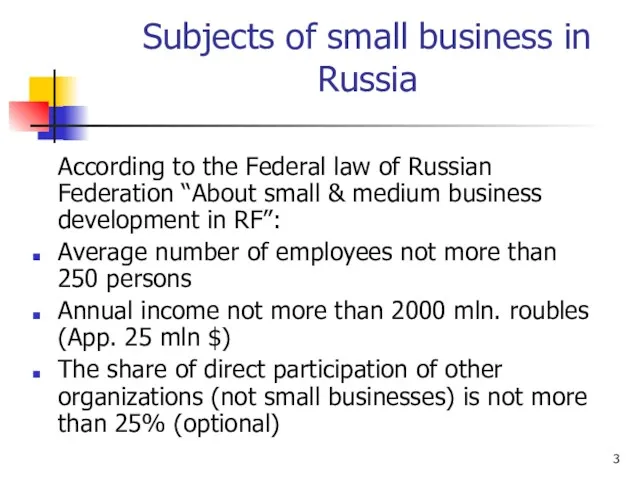

Subjects of small business in Russia

According to the Federal law of

Subjects of small business in Russia

According to the Federal law of

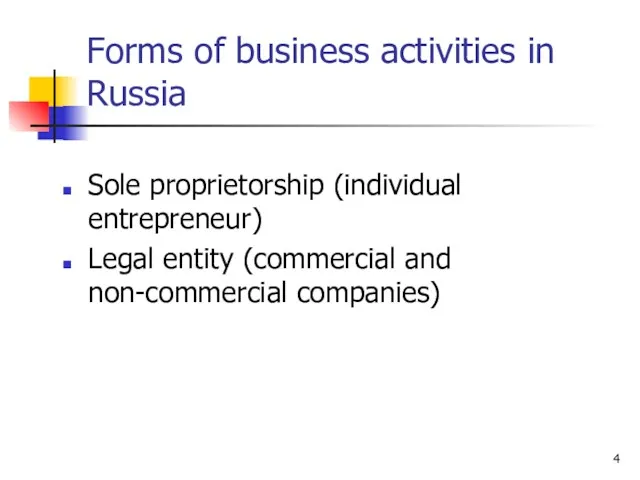

Forms of business activities in Russia

Sole proprietorship (individual entrepreneur)

Legal entity (commercial

Forms of business activities in Russia

Sole proprietorship (individual entrepreneur)

Legal entity (commercial

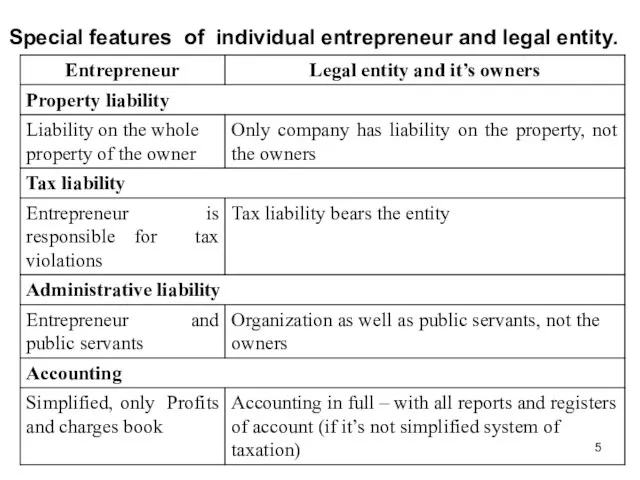

Special features of individual entrepreneur and legal entity.

Special features of individual entrepreneur and legal entity.

Special features of individual entrepreneur and legal entity.

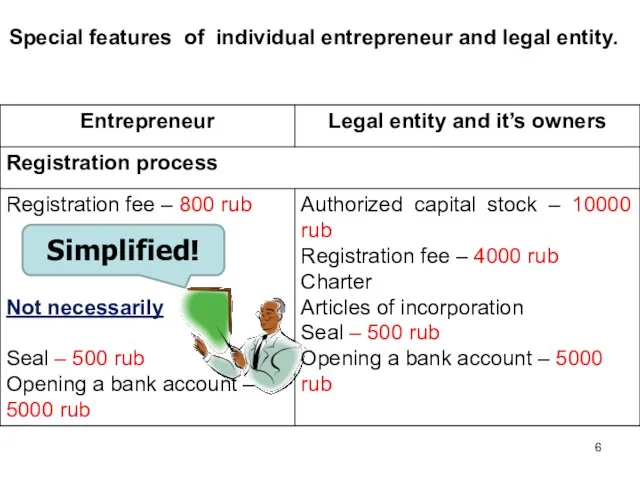

Simplified!

Special features of individual entrepreneur and legal entity.

Simplified!

FORMS OF LEGAL ENTITIES WIDELY USED IN RUSSIA

FORMS OF LEGAL ENTITIES WIDELY USED IN RUSSIA

Making choice for taxation system

Patents

Making choice for taxation system

Patents

Traditional Taxation system

Traditional Taxation system

For legal entities and individual entrepreneurs

Turnover not > 150 mln rub

For legal entities and individual entrepreneurs

Turnover not > 150 mln rub

STS

Application of the simplified system of taxation provides uniform tax payment

STS

Application of the simplified system of taxation provides uniform tax payment

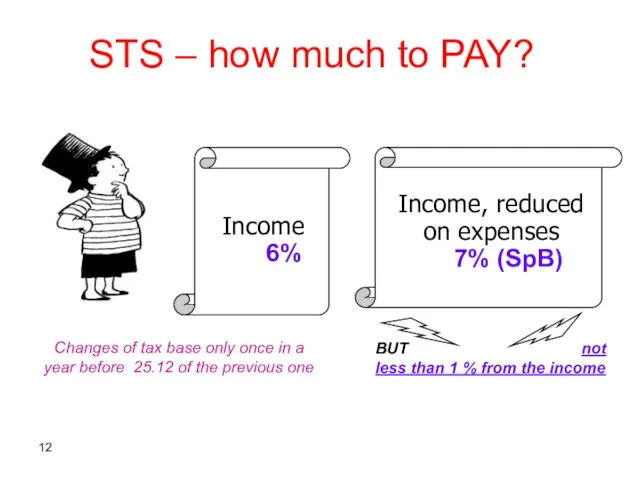

STS – how much to PAY?

Changes of tax base only once

STS – how much to PAY?

Changes of tax base only once

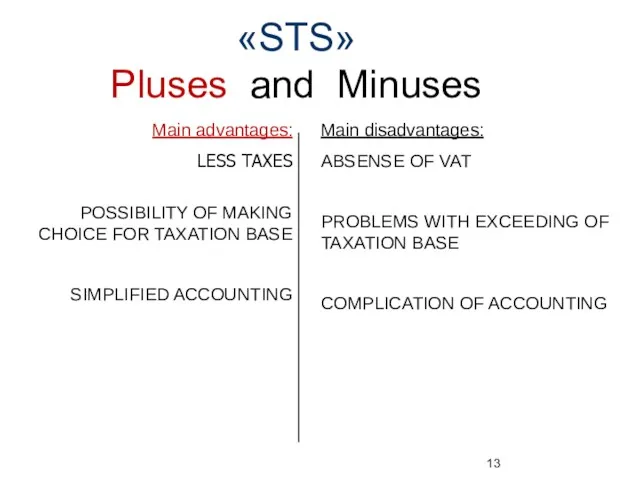

«STS»

Pluses and Minuses

Main advantages:

LESS TAXES

POSSIBILITY OF MAKING CHOICE FOR

«STS»

Pluses and Minuses

Main advantages:

LESS TAXES

POSSIBILITY OF MAKING CHOICE FOR

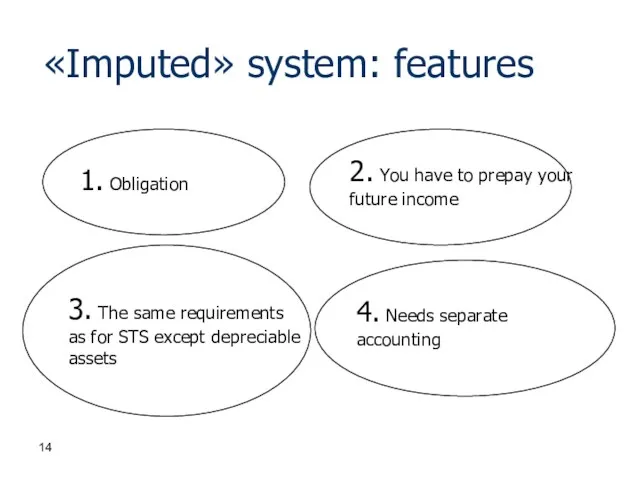

«Imputed» system: features

«Imputed» system: features

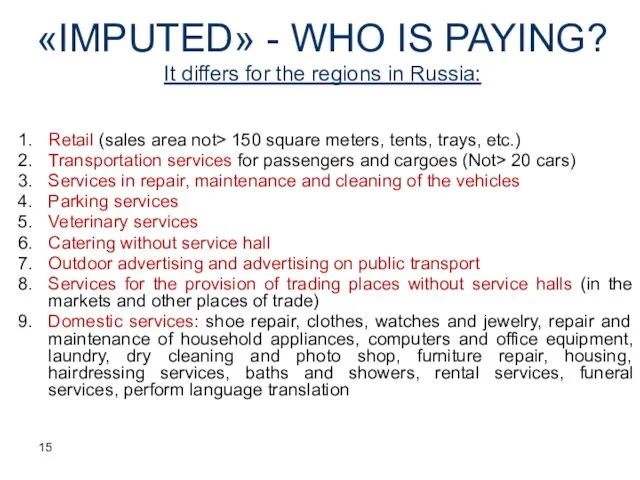

«IMPUTED» - WHO IS PAYING?

It differs for the regions in Russia:

Retail

«IMPUTED» - WHO IS PAYING?

It differs for the regions in Russia:

Retail

«Imputed» –

now much to PAY?

Rate: 15% of imputed income

Sum of

«Imputed» –

now much to PAY?

Rate: 15% of imputed income

Sum of

What are you going to do next weekend

What are you going to do next weekend Пасха в России and Easter in England

Пасха в России and Easter in England Past Simple Questions

Past Simple Questions World Map Infographic

World Map Infographic My family

My family Memory Game 08 (Body parts)

Memory Game 08 (Body parts) French national dishes. Croissant

French national dishes. Croissant Merry Christmas

Merry Christmas Presentation on the topic of personal player

Presentation on the topic of personal player Articles

Articles Articles

Articles Thanksgiving day. День благодарения

Thanksgiving day. День благодарения Some music

Some music The present continuous tense (настоящее продолженное время)

The present continuous tense (настоящее продолженное время) Pulmonary tuberculosis. The Passive Voice. Present and Past Nenses the Pfssive Voice

Pulmonary tuberculosis. The Passive Voice. Present and Past Nenses the Pfssive Voice The monuments of The First World War

The monuments of The First World War Farm Animals Hidden Picture Game

Farm Animals Hidden Picture Game Financial information

Financial information Time. What time is it

Time. What time is it Burger. Pizza

Burger. Pizza Have to, has to

Have to, has to Степени сравнения

Степени сравнения Happu Halloween

Happu Halloween Действия в будущем

Действия в будущем Choose the right modal verb

Choose the right modal verb Paralympic games. One World-One Dream

Paralympic games. One World-One Dream CAMPAIGN. English for the Military

CAMPAIGN. English for the Military Merry Christmas

Merry Christmas