- The audit

Содержание

- 2. The audit is an entrepreneurial activity on independent check of accounting and financial reporting of organizations

- 3. The audit objective is expression of opinion on reliability of the financial statements of the audited

- 4. The economic substance of the audit is explained by the increased need of users of financial

- 5. Users of financial statements: investors and their representatives; workers and their representatives; the lenders; suppliers and

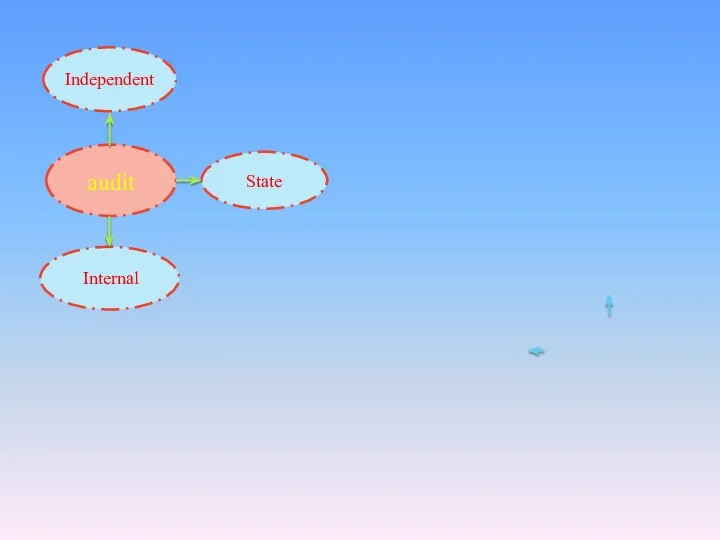

- 6. Classification of audit Классификация аудита

- 7. An examination of the definition of auditing reveals that there are three key aspects of the

- 8. Second, during an examination of financial statements the auditor objectively obtains and evaluates evidence regarding assertions

- 9. Во-вторых, во время рассмотрения финансовой отчетности аудитор получает и оценивает объективно доказательства в отношении утверждений об

- 10. The third and final key aspect of the definition is that auditing involves communicating the results

- 11. Третьим и последним ключевым аспектом определения является то, что аудит предусматривает доведение результатов аудита заинтересованным пользователям.

- 14. Скачать презентацию

The audit is

an entrepreneurial activity on independent check of accounting

The audit is

an entrepreneurial activity on independent check of accounting

The audit objective is

expression of opinion on reliability of the

The audit objective is

expression of opinion on reliability of the

The economic substance of

the audit is explained by the increased

The economic substance of

the audit is explained by the increased

Users of financial statements:

investors and their representatives;

workers and their representatives;

the

Users of financial statements:

investors and their representatives;

workers and their representatives;

the

Classification

of audit

Классификация

аудита

Classification

of audit

Классификация

аудита

An examination of the definition of auditing reveals that there are

An examination of the definition of auditing reveals that there are

Second, during an examination of financial statements the auditor objectively obtains

Second, during an examination of financial statements the auditor objectively obtains

Во-вторых, во время рассмотрения финансовой отчетности аудитор получает и оценивает объективно

Во-вторых, во время рассмотрения финансовой отчетности аудитор получает и оценивает объективно

The third and final key aspect of the definition is that

The third and final key aspect of the definition is that

Третьим и последним ключевым аспектом определения является то, что аудит предусматривает

Третьим и последним ключевым аспектом определения является то, что аудит предусматривает

Traditional Russian kitchen

Traditional Russian kitchen Pronoun. Personal Pronouns

Pronoun. Personal Pronouns Ways to express future tense. My summer holidays plans

Ways to express future tense. My summer holidays plans 10 great days this summer

10 great days this summer Настоящее совершенное

Настоящее совершенное Parrot Peter picked a pack of pickled peppers

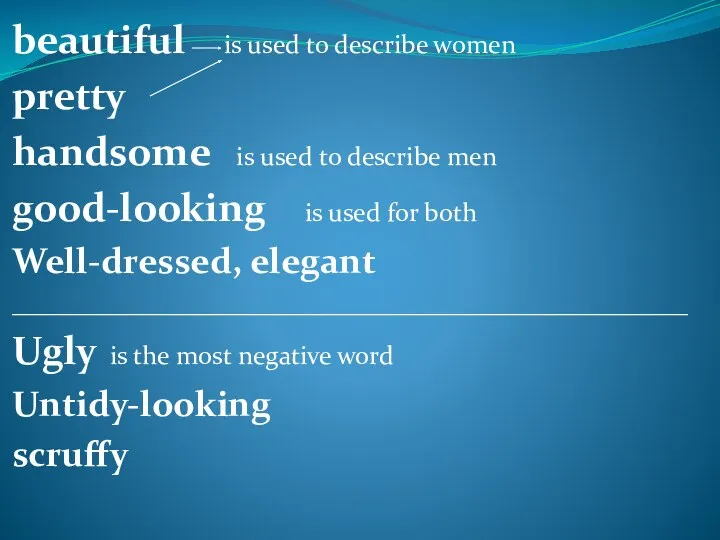

Parrot Peter picked a pack of pickled peppers Appearance. Well - dressed, elegant

Appearance. Well - dressed, elegant Present continuous (progressive). Настоящее продолженное время

Present continuous (progressive). Настоящее продолженное время Let’s repeat relative clauses

Let’s repeat relative clauses How to write case-briefs

How to write case-briefs Singular and plural nouns

Singular and plural nouns Discourse analysis of the concept of ethics of care in the works of N. Noddings and its application in English teaching

Discourse analysis of the concept of ethics of care in the works of N. Noddings and its application in English teaching Opinion Essays. Требования к сочинению

Opinion Essays. Требования к сочинению French fries, recipe at home

French fries, recipe at home Etiquette in England

Etiquette in England My home

My home My favourite sportsman Sergey Vladimirovich Shubenkov

My favourite sportsman Sergey Vladimirovich Shubenkov Instructions for presentation

Instructions for presentation Prepositions

Prepositions Have a look at some beautiful places in my country and complete the conditional sentences with the right verb tense

Have a look at some beautiful places in my country and complete the conditional sentences with the right verb tense Biosphere reserve Askania-Nova

Biosphere reserve Askania-Nova Shops and shopping

Shops and shopping Business culture of Turkey

Business culture of Turkey Medical education in different countries

Medical education in different countries Ilia Efimovich Repin

Ilia Efimovich Repin Customs and traditions of celebrating Christmas in different countries

Customs and traditions of celebrating Christmas in different countries Verbals – non-finite forms of the Verb

Verbals – non-finite forms of the Verb Present simple

Present simple