- Financial Economy

Содержание

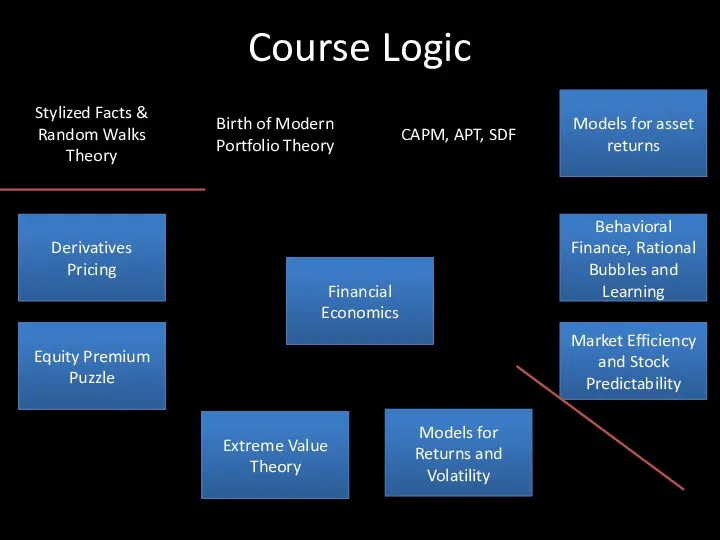

- 2. Course Logic Financial Economics Stylized Facts & Random Walks Theory Birth of Modern Portfolio Theory CAPM,

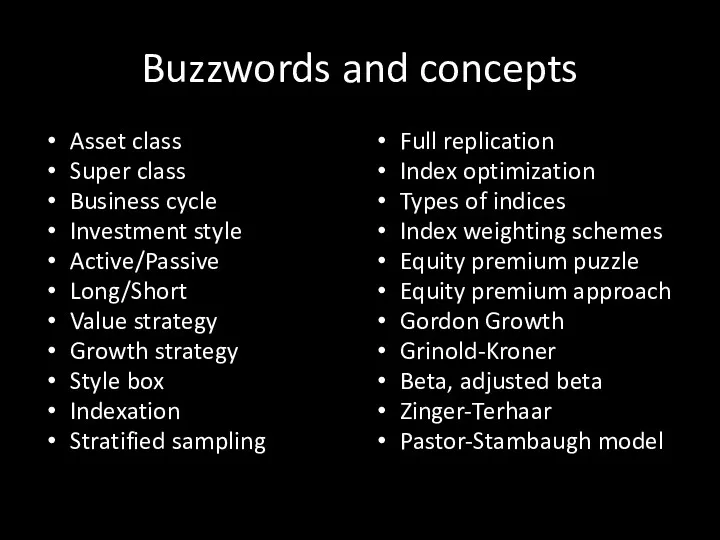

- 3. Buzzwords and concepts Asset class Super class Business cycle Investment style Active/Passive Long/Short Value strategy Growth

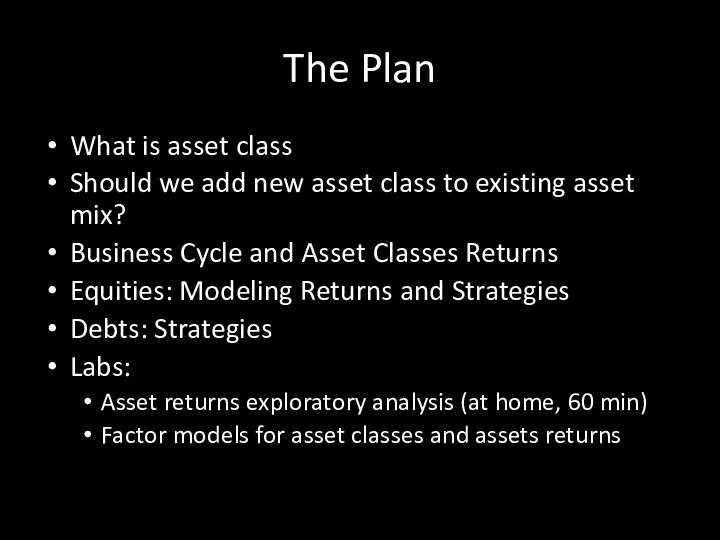

- 4. The Plan What is asset class Should we add new asset class to existing asset mix?

- 5. Asset classes: examples Cash and money market instruments Equities Debts Alternatives Real Estate Commodities Gold Hedge

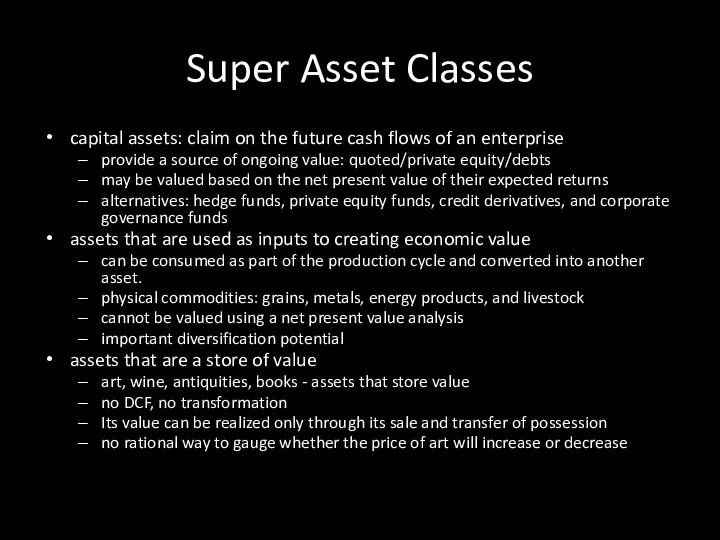

- 6. Super Asset Classes capital assets: claim on the future cash flows of an enterprise provide a

- 7. Bonds and Equities Bonds and equities are dominating as investment assets Equities account for biggest part

- 8. INCLUSION OF NEW ASSET CLASS Part II.1

- 9. Expression for deciding whether to include new asset class in asset mix If this equation holds,

- 10. Tangency portfolio Notice that the tangency portfolio T is optimal in the sense that it has

- 11. ASSET CLASSES AND BUSINESS CYCLE Part II.2

- 12. Attractive Investment Opportunities in Various Business Cycle Stages

- 13. Key variables to watch cycle Confidence: business, consumer GDP Inflation Unemployment Output gap Treasuries spread Central

- 14. EQUITIES: INTRO Part II.3

- 15. Equities generate superior returns in the long run Wealth multipliers for US Assets and Inflation, Dec’1925-Dec’2005

- 16. Equities provide astonishing results in the very long run Wealth multipliers for US Assets and Inflation,

- 17. Exponential growth of $1 Invested in U.S. Stocks and Bonds on Dec. 31, 1870 Sources: Stocks:

- 18. Equity premium puzzle Lack of an explanation generally accepted by economists for the following situation: Much

- 19. US Equity premium using different data sets Source: Equity premium in retrospect, Mehra, Prescott, 2003

- 20. Evolution of the Required Equity Premium (REP) used or recommended in 150 finance and valuation textbooks

- 21. Moving average (last 5 years) of the REP used or recommended in 150 finance and valuation

- 22. The term EP is used to designate 4 different concepts Historical equity premium (HEP): historical differential

- 23. Market Risk Premium for the USA used in 2011 Source: Fernández, 2012

- 24. Are equities really profitable? Survivorship bias: did you know in advance that UK and US would

- 25. Share of equities in market capitalization of investment universe consisting 7 major asset classes Source: Mikaelyan

- 26. Equity Allocations for Institutional Investors Source: Greenwich Associates, 2003. For many investors hierarchy of questions when

- 27. Equities as instrument in PM - inflation hedge — an asset is IH if its returns

- 28. Approaches to Equity Inv. passive management: after costs the return on the average actively managed dollar

- 29. Definitions active return — portfolio's return in excess of the benchmark portfolio active risk — risk

- 30. Returns succesfull active manager will have expected active return of 2+%, but tracking error is likely

- 31. Example The table below shows the active return of an equity portfolio. Calculate the portfolio’s tracking

- 32. Solution

- 33. Passive Equity Investing simple indexing types of indices: price weighted, value weighted, equal weighted major indices

- 34. What makes a good index? It must provide some useful information about the market that is

- 35. Why make an index? considerable research needed, what’s the benefit? some sell-side institutions develop indices as

- 36. Weighting shemes Price-weighted Volume-weighted Cap-weighted / modified cap (MICEX) Free-float weighted Equal (dollar) – weighted /

- 37. Types of indices Broad market Total market Cap range Sector indices Geographic Markets: advanced/emerging/frontier Exchange Concept

- 38. Implementing an indexing strategy Indexed separate or pooled accounts Low cost index mutual funds widely accessible

- 39. 3 methods of indexation full replication Every index security is held with approximately the same weight

- 40. Active Equity Investing equity styles Value vs. Growth vs. Market oriented Style index

- 41. Main types of active strategies Value, value investors are more concerned about buying a stock that

- 42. Value investing buying a stock that is deemed relatively cheap in terms of the purchase price

- 43. P/E ratios as a predictor of twenty-year returns Source: Robert Shiller, Irrational Exhuberance The horizontal axis

- 44. Growth investing value investors are focusing on price; growth investors are focusing on earnings growth rate

- 45. Morningstar Equity Style Box

- 46. Risk/return of Morningstar style indices 2003-2010 Source: Morningstar What’s the sense in Large Core and Value?

- 47. Flaws of indexation Several researchers criticize fundamental indexation on both theoretical and empirical grounds Collared weighting

- 48. Risks of value/growth The main risk for a value investor is the potential for misinterpreting a

- 49. Long/short strategies long-only strategy can capture one overall alpha. in long–short strategy the value added can

- 50. EQUITIES: RETURN MODELS Part II.4

- 51. Models of equity return Historical Estimates premium approach, DCF, Gordon growth, Grinold-Kroner, Singer-Terhaar, Pastor-Stambaugh Barra model

- 52. Historical estimates: geometric mean focus of MVO (Markowiyz, 1952): tradeoff between StdDev and expected return many

- 53. Geometric mean and StdDev

- 54. Example CMA for 5 asset classes Isogeometric mean curves

- 55. DCF You all know it very well, don’t you?

- 56. Historical Premium Approach

- 57. Supply-side premium

- 58. Gordon Model

- 59. Growth rate Expected Real GDP + expected inflation Sometimes: + excess corporate growth (some sectors)

- 60. Grinold-Kroner Model In the United States and other major markets, share repurchases have become an important

- 61. Example

- 62. Case An Australian investor currently holds an A$240 million equity portfolio. He is considering rebalancing the

- 63. Answer

- 64. Singer-Terhaar’s ICAPM “ICAPM minus imperfections” Market Sharpe Ratio? 0.28-0.3

- 65. Case Suppose that an investor predicts that the standard deviation of Canadian bonds will be 7.0

- 66. ICAPM drawbacks the ICAPM assumes perfect markets (markets without any frictional costs, where all assets trade

- 67. Adjustments to ICAPM Most markets lie between the extremes of perfect market integration and complete market

- 68. Segmented ICAPM Because the individual market and the reference market portfolio are identical, ρi,M in equals

- 69. Segmented + Integrated Taking the degree of integration as 0.8 for both Canadian equities and bonds,

- 70. Singer–Terhaar approach Estimate the perfectly integrated and the completely segmented risk premiums for the asset class

- 71. Singer–Terhaar Approach: Case Zimmerman Capital Management (ZCM) is developing a strategic asset allocation for a small

- 72. Case II Exhibit below supplies the standard deviation estimates and gives relevant inputs for other quantities

- 73. Case III Based on the information given, address the following problems: CalculatetheexpectedreturnsonU.S.equities,U.S.fixedincome,non-U.S.equi- ties, non-U.S. fixed income,

- 74. Solution - Integrated Case

- 75. Solution – Segmented Case

- 76. Solution to 1

- 77. Solution to 2 Based on Equation 4-3b with one factor, the covariance between any two assets

- 78. Pastor-Stambaugh the Pastor-Stambaugh model adds a liquidity factor to the Fama-French model. the baseline value for

- 79. Example

- 80. Example contd.

- 81. Adjusted betas when making forecasts of the equity risk premium, some analysts recommend adjusting the beta

- 82. Example

- 83. DEBTS: INTRO AND STRATEGIES Part II.5

- 84. Debts PM Strategies pure bond indexing, enhanced indexing by matching primary risk factors, by small risk

- 85. Pure bond indexing objectives Matching benchmark return Technique matching the portfolio’s characteristics to the benchmark’s risk

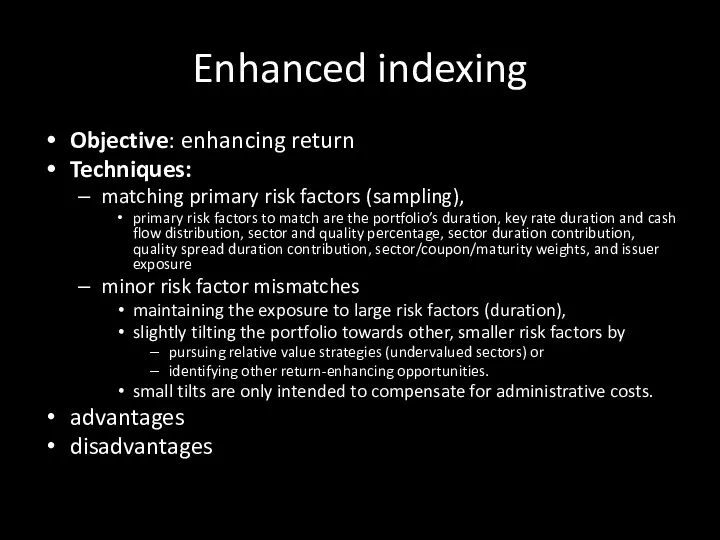

- 86. Enhanced indexing Objective: enhancing return Techniques: matching primary risk factors (sampling), primary risk factors to match

- 87. Other techniques As even perfectly indexed portfolio will still underperform the benchmark by the amount of

- 88. Active Management by Larger Risk Factor Mismatches Objective: earning sufficient return to cover administrative as well

- 89. Full-Blown Active Objectives: outperform at all costs Techniques: tilting, relative value, and duration strategies advantages disadvantages

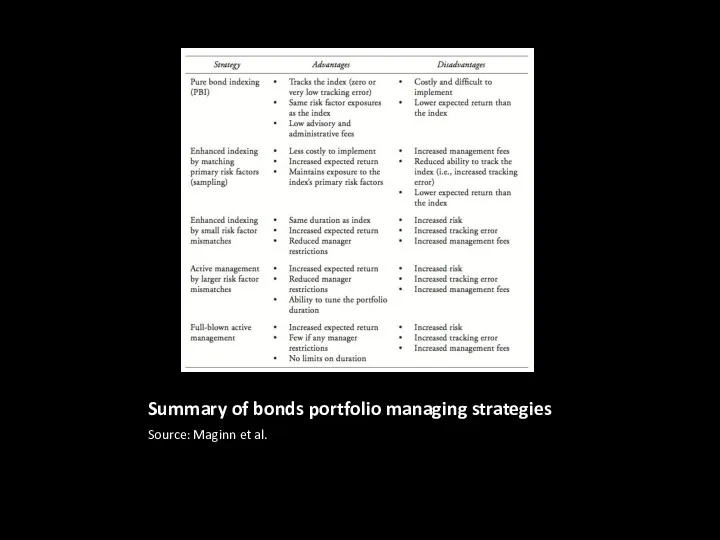

- 90. Summary of bonds portfolio managing strategies Source: Maginn et al.

- 91. Aligning Risk Exposures portfolio and benchmark risk profiles can be measured along several dimensions duration, key

- 93. Скачать презентацию

Course Logic

Financial

Economics

Stylized Facts &

Random Walks Theory

Birth of Modern Portfolio Theory

CAPM,

Course Logic

Financial

Economics

Stylized Facts &

Random Walks Theory

Birth of Modern Portfolio Theory

CAPM,

Buzzwords and concepts

Asset class

Super class

Business cycle

Investment style

Active/Passive

Long/Short

Value strategy

Growth strategy

Style box

Indexation

Stratified sampling

Full

Buzzwords and concepts

Asset class

Super class

Business cycle

Investment style

Active/Passive

Long/Short

Value strategy

Growth strategy

Style box

Indexation

Stratified sampling

Full

The Plan

What is asset class

Should we add new asset class to

The Plan

What is asset class

Should we add new asset class to

Asset classes: examples

Cash and money market instruments

Equities

Debts

Alternatives

Real Estate

Commodities

Gold

Hedge Funds

Private Equity

Asset classes: examples

Cash and money market instruments

Equities

Debts

Alternatives

Real Estate

Commodities

Gold

Hedge Funds

Private Equity

Super Asset Classes

capital assets: claim on the future cash flows of

Super Asset Classes

capital assets: claim on the future cash flows of

Bonds and Equities

Bonds and equities are dominating as investment assets

Equities account

Bonds and Equities

Bonds and equities are dominating as investment assets

Equities account

INCLUSION OF NEW ASSET CLASS

Part II.1

INCLUSION OF NEW ASSET CLASS

Part II.1

Expression for deciding whether to include new asset class in asset

Expression for deciding whether to include new asset class in asset

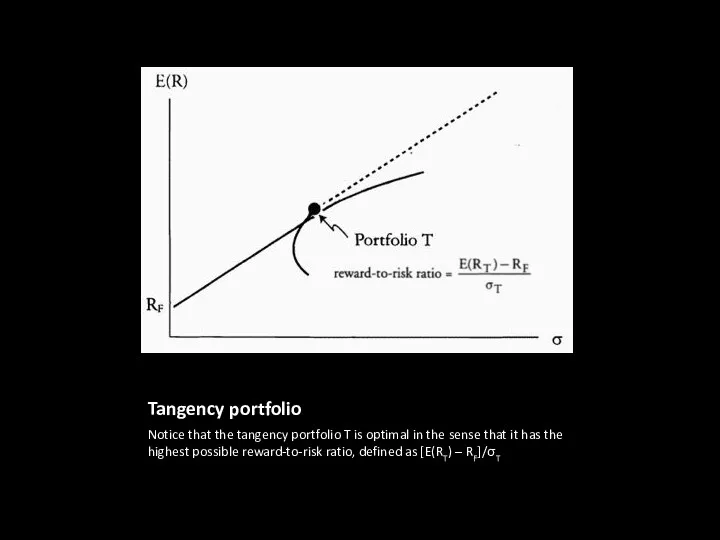

Tangency portfolio

Notice that the tangency portfolio T is optimal in the

Tangency portfolio

Notice that the tangency portfolio T is optimal in the

ASSET CLASSES AND BUSINESS CYCLE

Part II.2

ASSET CLASSES AND BUSINESS CYCLE

Part II.2

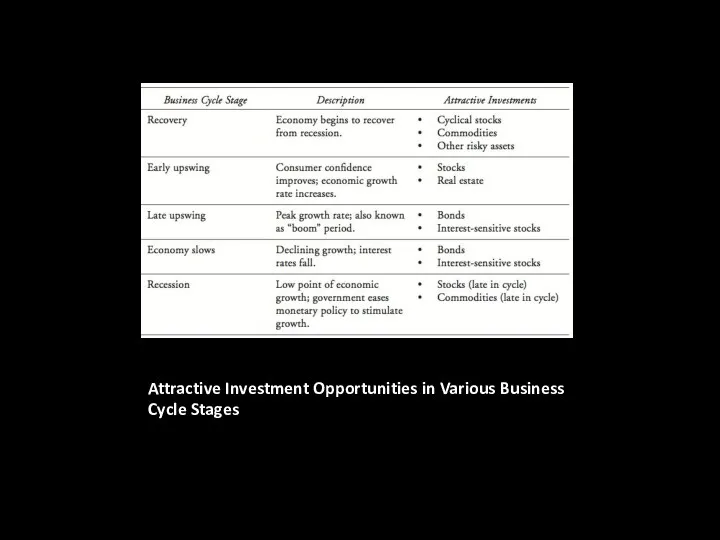

Attractive Investment Opportunities in Various Business Cycle Stages

Attractive Investment Opportunities in Various Business Cycle Stages

Key variables to watch cycle

Confidence: business, consumer

GDP

Inflation

Unemployment

Output gap

Treasuries spread

Central bank policy

Key variables to watch cycle

Confidence: business, consumer

GDP

Inflation

Unemployment

Output gap

Treasuries spread

Central bank policy

EQUITIES: INTRO

Part II.3

EQUITIES: INTRO

Part II.3

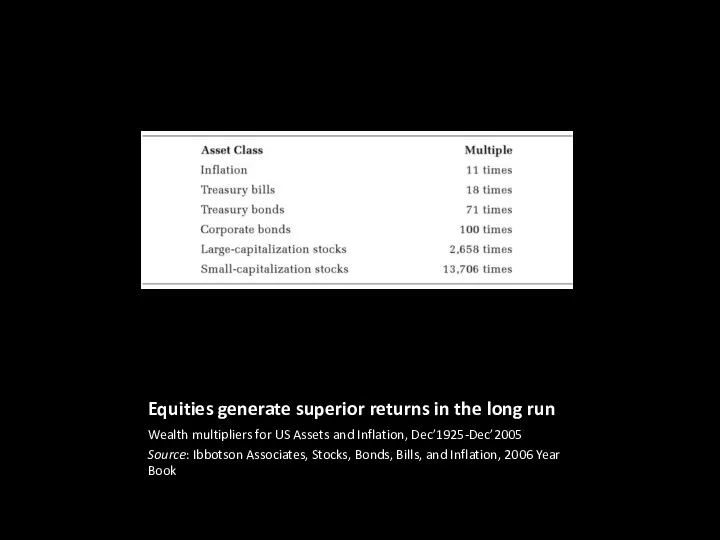

Equities generate superior returns in the long run

Wealth multipliers for US

Equities generate superior returns in the long run

Wealth multipliers for US

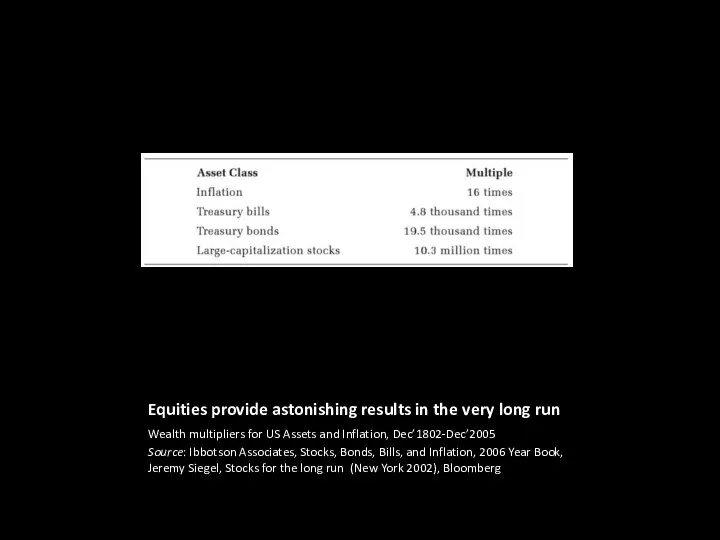

Equities provide astonishing results in the very long run

Wealth multipliers for

Equities provide astonishing results in the very long run

Wealth multipliers for

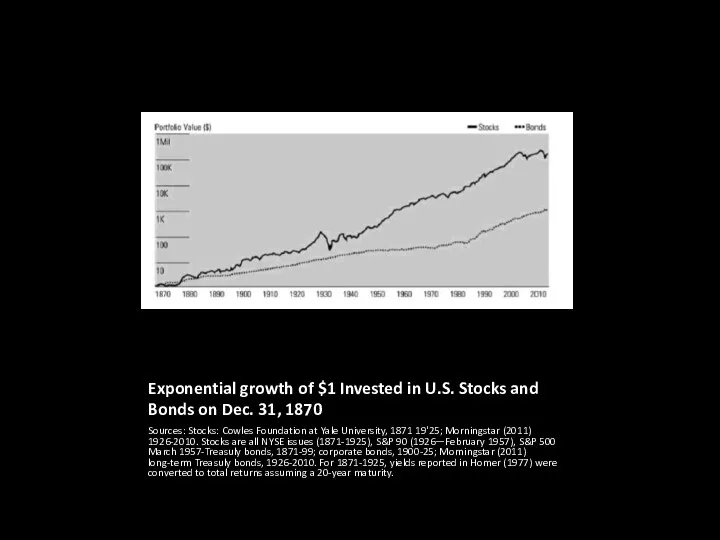

Exponential growth of $1 Invested in U.S. Stocks and Bonds on

Exponential growth of $1 Invested in U.S. Stocks and Bonds on

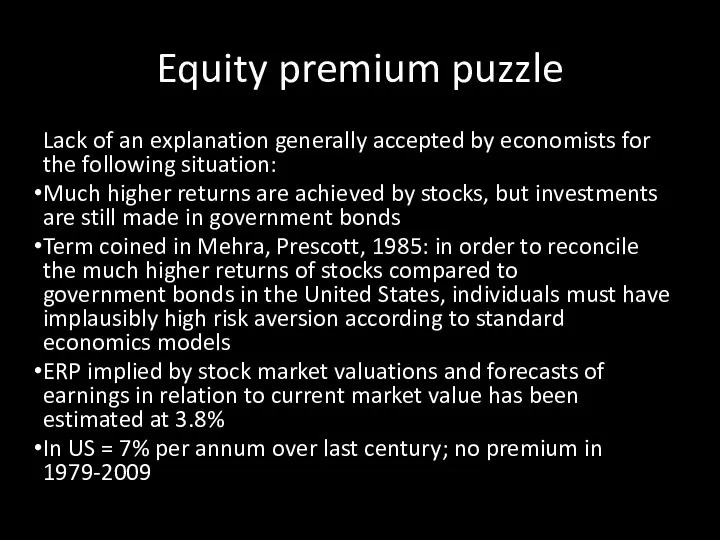

Equity premium puzzle

Lack of an explanation generally accepted by economists for

Equity premium puzzle

Lack of an explanation generally accepted by economists for

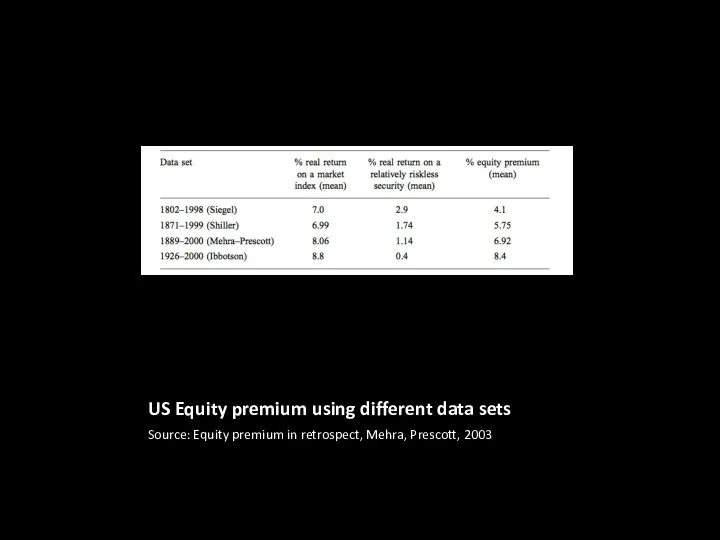

US Equity premium using different data sets

Source: Equity premium in retrospect,

US Equity premium using different data sets

Source: Equity premium in retrospect,

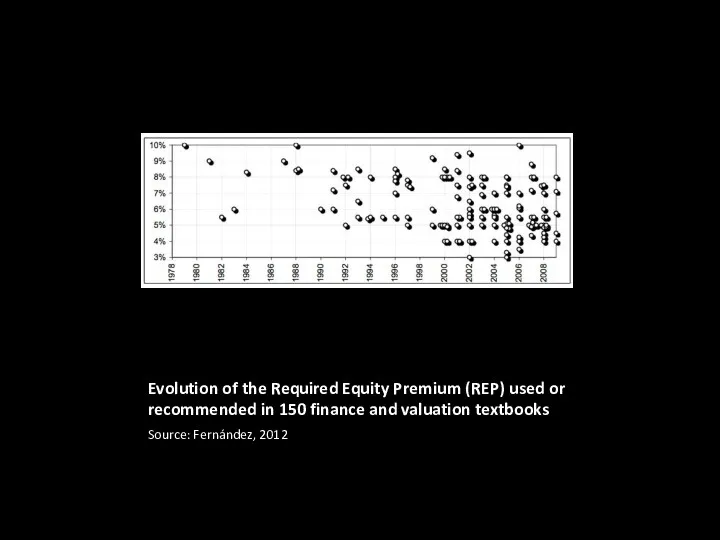

Evolution of the Required Equity Premium (REP) used or recommended in

Evolution of the Required Equity Premium (REP) used or recommended in

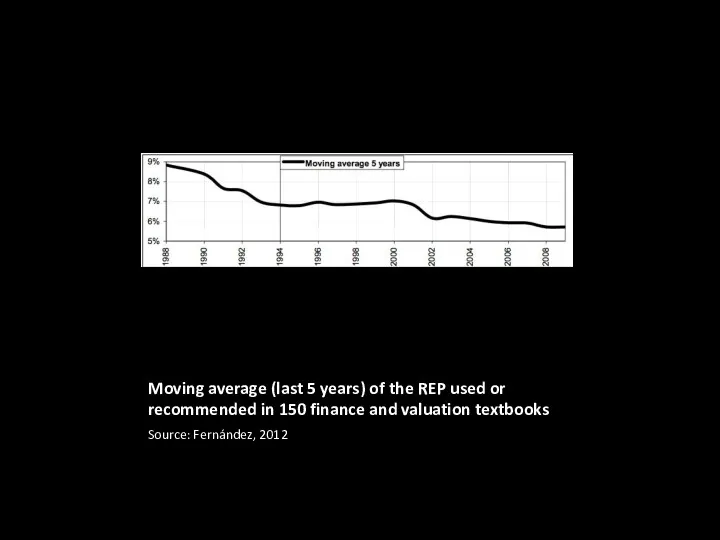

Moving average (last 5 years) of the REP used or recommended

Moving average (last 5 years) of the REP used or recommended

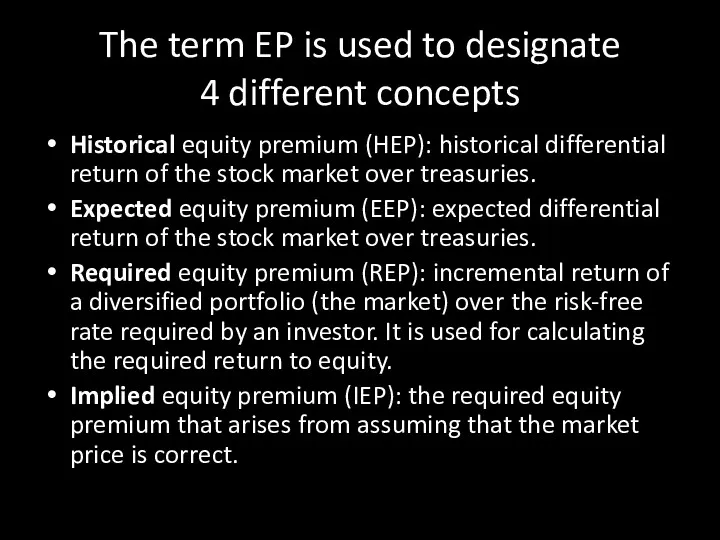

The term EP is used to designate

4 different concepts

Historical

The term EP is used to designate

4 different concepts

Historical

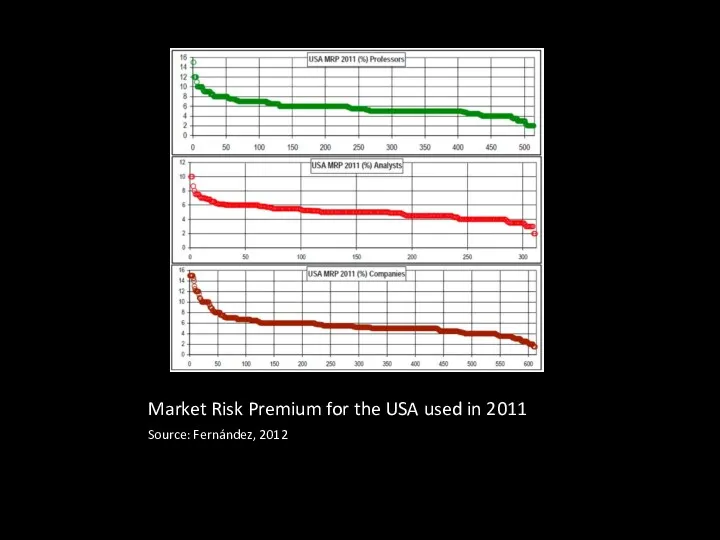

Market Risk Premium for the USA used in 2011

Source: Fernández,

Market Risk Premium for the USA used in 2011

Source: Fernández,

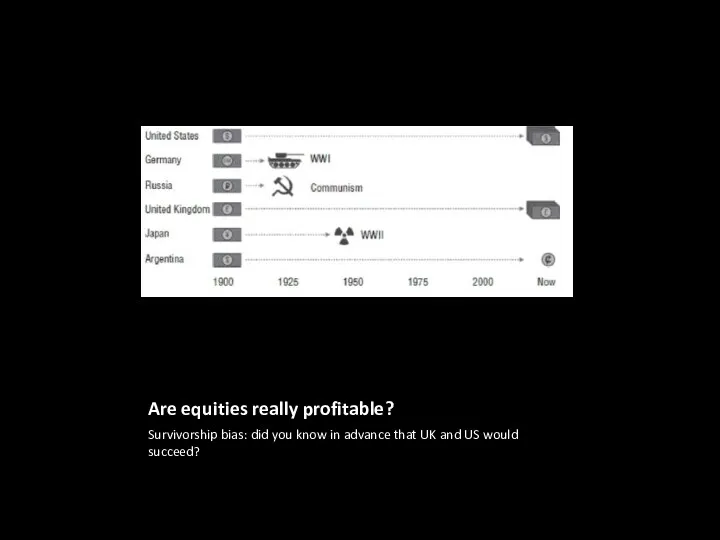

Are equities really profitable?

Survivorship bias: did you know in advance that

Are equities really profitable?

Survivorship bias: did you know in advance that

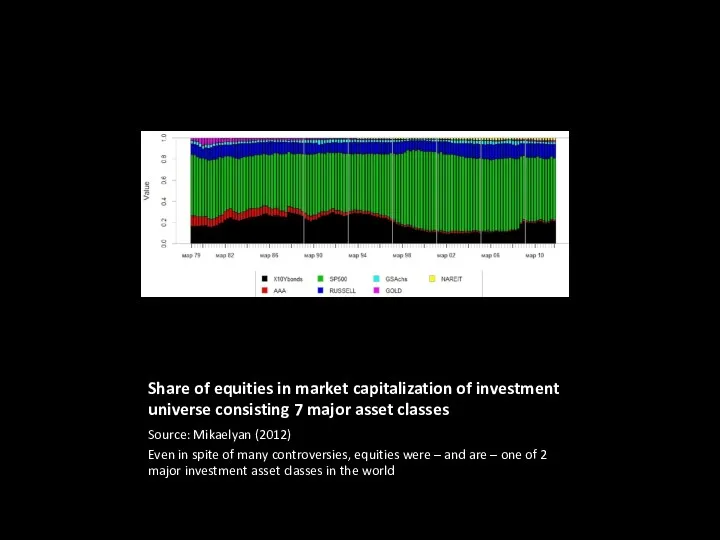

Share of equities in market capitalization of investment universe consisting 7

Share of equities in market capitalization of investment universe consisting 7

Equity Allocations for Institutional Investors

Source: Greenwich Associates, 2003.

For many investors

Equity Allocations for Institutional Investors

Source: Greenwich Associates, 2003.

For many investors

Equities as instrument in PM

- inflation hedge — an asset is

Equities as instrument in PM

- inflation hedge — an asset is

Approaches to Equity Inv.

passive management: after costs the return on the

Approaches to Equity Inv.

passive management: after costs the return on the

Definitions

active return — portfolio's return in excess of the benchmark portfolio

active

Definitions

active return — portfolio's return in excess of the benchmark portfolio

active

Returns

succesfull active manager will have expected active return of 2+%, but

Returns

succesfull active manager will have expected active return of 2+%, but

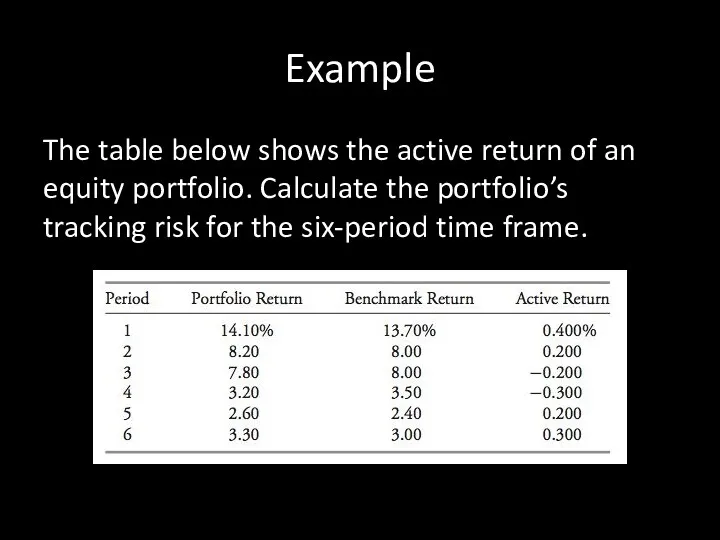

Example

The table below shows the active return of an equity portfolio.

Example

The table below shows the active return of an equity portfolio.

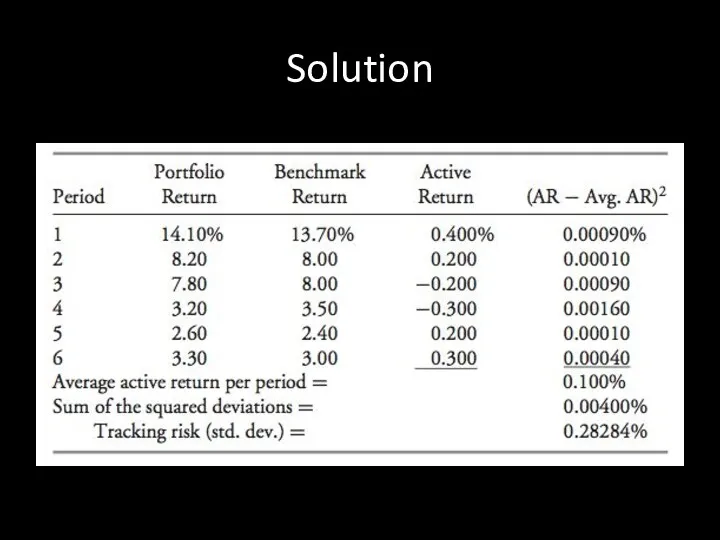

Solution

Solution

Passive Equity Investing

simple indexing

types of indices: price weighted, value weighted, equal

Passive Equity Investing

simple indexing

types of indices: price weighted, value weighted, equal

What makes a good index?

It must provide some useful information about

What makes a good index?

It must provide some useful information about

Why make an index?

considerable research needed, what’s the benefit?

some sell-side institutions

Why make an index?

considerable research needed, what’s the benefit?

some sell-side institutions

Weighting shemes

Price-weighted

Volume-weighted

Cap-weighted / modified cap (MICEX)

Free-float weighted

Equal (dollar) – weighted /

Weighting shemes

Price-weighted

Volume-weighted

Cap-weighted / modified cap (MICEX)

Free-float weighted

Equal (dollar) – weighted /

Types of indices

Broad market

Total market

Cap range

Sector indices

Geographic

Markets: advanced/emerging/frontier

Exchange

Concept based

Style: value/growth/core

Economic sensitivity:

Types of indices

Broad market

Total market

Cap range

Sector indices

Geographic

Markets: advanced/emerging/frontier

Exchange

Concept based

Style: value/growth/core

Economic sensitivity:

Implementing an indexing strategy

Indexed separate or pooled accounts

Low cost

index mutual funds

widely

Implementing an indexing strategy

Indexed separate or pooled accounts

Low cost

index mutual funds

widely

3 methods of indexation

full replication

Every index security is held with approximately

3 methods of indexation

full replication

Every index security is held with approximately

Active Equity Investing

equity styles

Value vs. Growth vs. Market oriented

Style index

Active Equity Investing

equity styles

Value vs. Growth vs. Market oriented

Style index

Main types of active strategies

Value,

value investors are more concerned about

Main types of active strategies

Value,

value investors are more concerned about

Value investing

buying a stock that is deemed relatively cheap in terms

Value investing

buying a stock that is deemed relatively cheap in terms

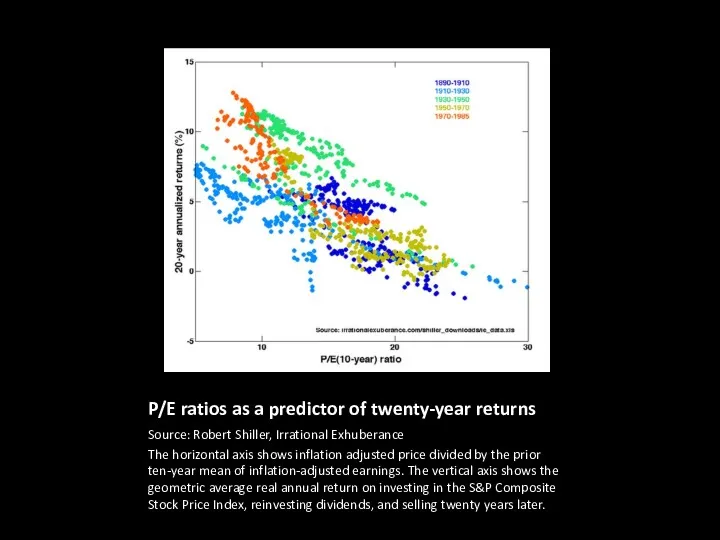

P/E ratios as a predictor of twenty-year returns

Source: Robert Shiller, Irrational

P/E ratios as a predictor of twenty-year returns

Source: Robert Shiller, Irrational

Growth investing

value investors are focusing on price; growth investors are focusing

Growth investing

value investors are focusing on price; growth investors are focusing

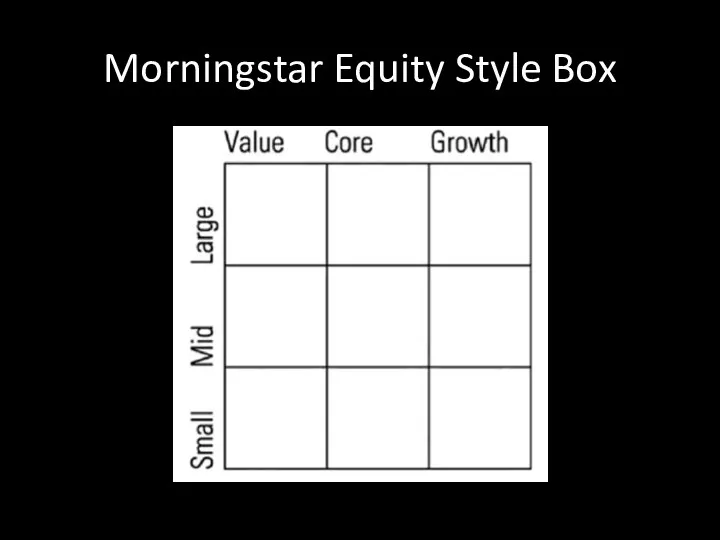

Morningstar Equity Style Box

Morningstar Equity Style Box

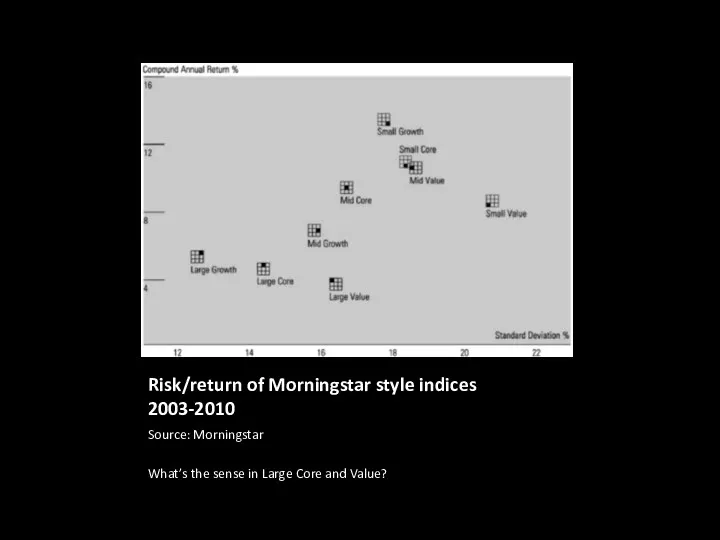

Risk/return of Morningstar style indices 2003-2010

Source: Morningstar

What’s the sense in Large

Risk/return of Morningstar style indices 2003-2010

Source: Morningstar

What’s the sense in Large

Flaws of indexation

Several researchers criticize fundamental indexation on both theoretical and

Flaws of indexation

Several researchers criticize fundamental indexation on both theoretical and

Risks of value/growth

The main risk for a value investor is the

Risks of value/growth

The main risk for a value investor is the

Long/short strategies

long-only strategy can capture one overall alpha.

in long–short strategy

Long/short strategies

long-only strategy can capture one overall alpha.

in long–short strategy

EQUITIES: RETURN MODELS

Part II.4

EQUITIES: RETURN MODELS

Part II.4

Models of equity return

Historical Estimates

premium approach,

DCF,

Gordon growth,

Grinold-Kroner,

Singer-Terhaar,

Models of equity return

Historical Estimates

premium approach,

DCF,

Gordon growth,

Grinold-Kroner,

Singer-Terhaar,

Historical estimates: geometric mean

focus of MVO (Markowiyz, 1952): tradeoff between StdDev

Historical estimates: geometric mean

focus of MVO (Markowiyz, 1952): tradeoff between StdDev

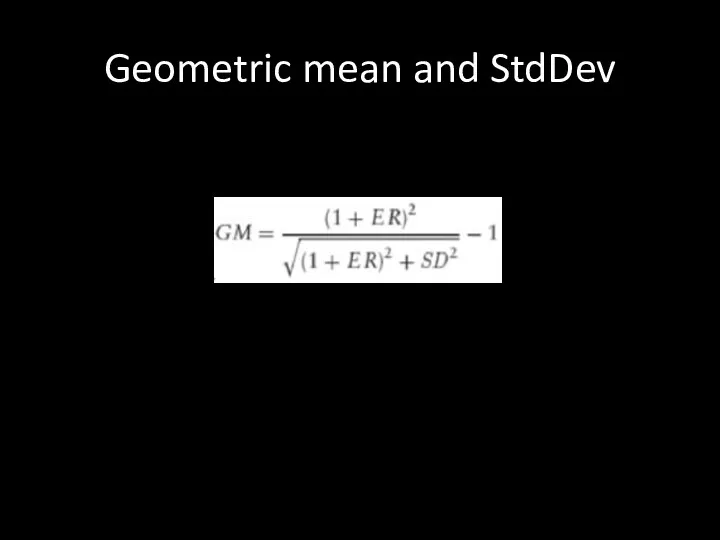

Geometric mean and StdDev

Geometric mean and StdDev

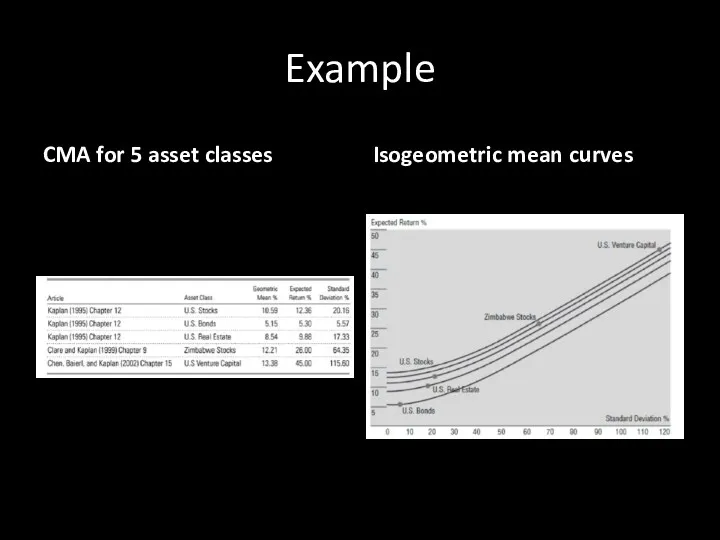

Example

CMA for 5 asset classes

Isogeometric mean curves

Example

CMA for 5 asset classes

Isogeometric mean curves

DCF

You all know it very well, don’t you?

DCF

You all know it very well, don’t you?

Historical Premium Approach

Historical Premium Approach

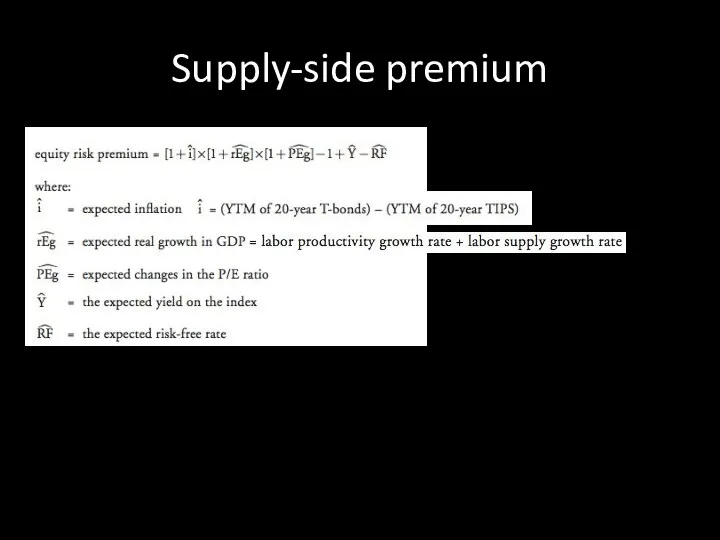

Supply-side premium

Supply-side premium

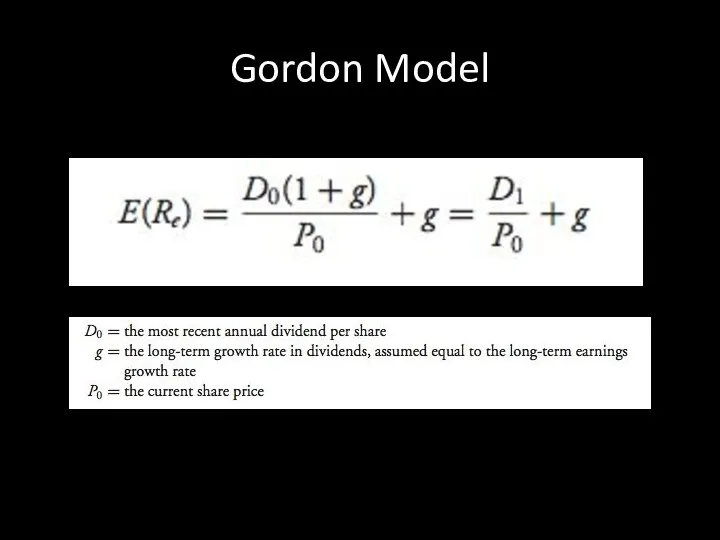

Gordon Model

Gordon Model

Growth rate

Expected Real GDP + expected inflation

Sometimes: + excess corporate growth

Growth rate

Expected Real GDP + expected inflation

Sometimes: + excess corporate growth

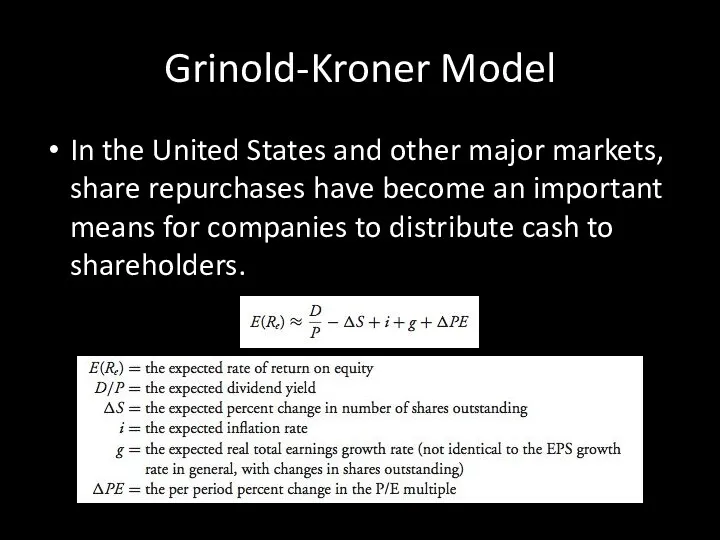

Grinold-Kroner Model

In the United States and other major markets, share repurchases

Grinold-Kroner Model

In the United States and other major markets, share repurchases

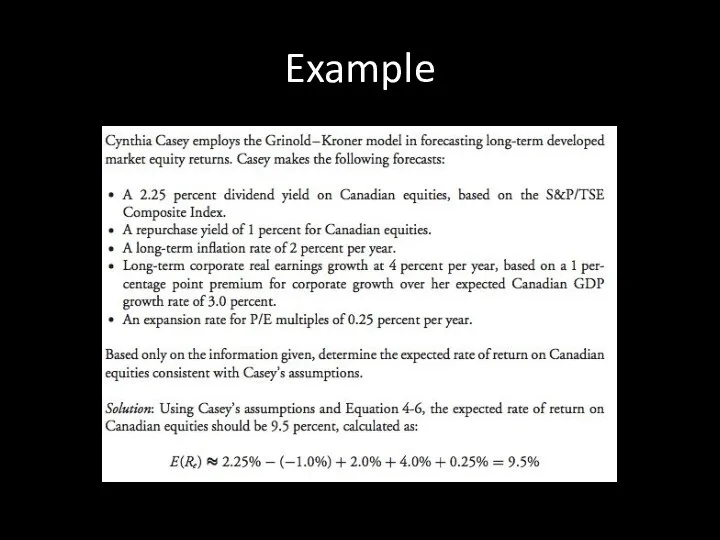

Example

Example

Case

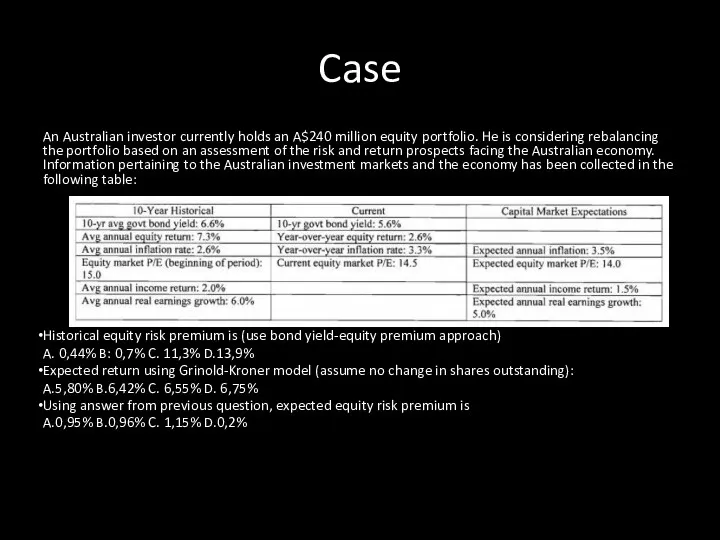

An Australian investor currently holds an A$240 million equity portfolio. He

Case

An Australian investor currently holds an A$240 million equity portfolio. He

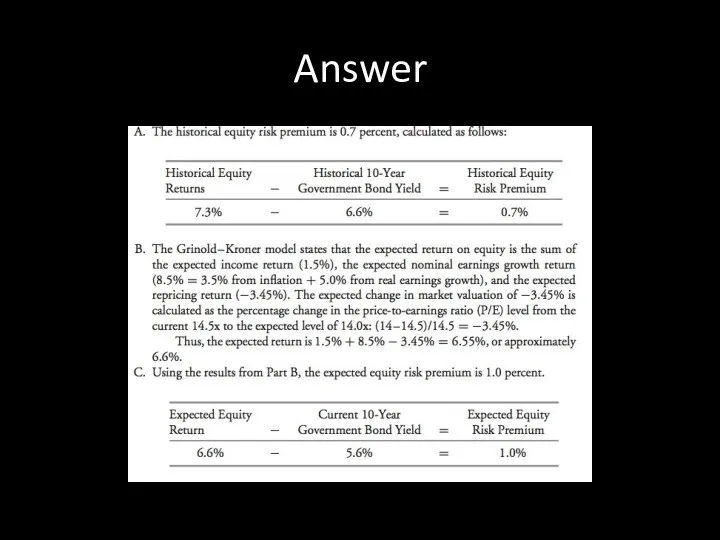

Answer

Answer

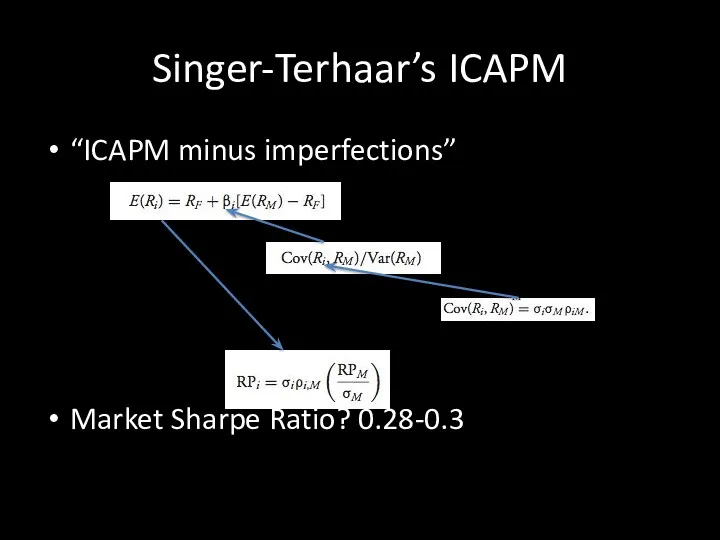

Singer-Terhaar’s ICAPM

“ICAPM minus imperfections”

Market Sharpe Ratio? 0.28-0.3

Singer-Terhaar’s ICAPM

“ICAPM minus imperfections”

Market Sharpe Ratio? 0.28-0.3

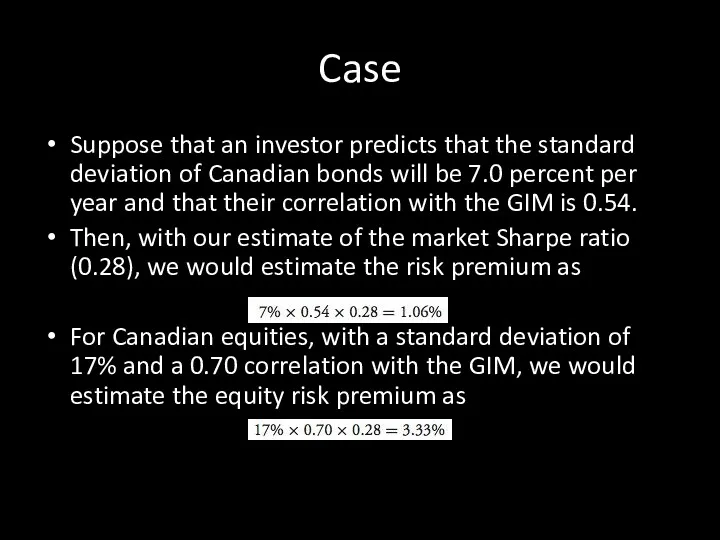

Case

Suppose that an investor predicts that the standard deviation of Canadian

Case

Suppose that an investor predicts that the standard deviation of Canadian

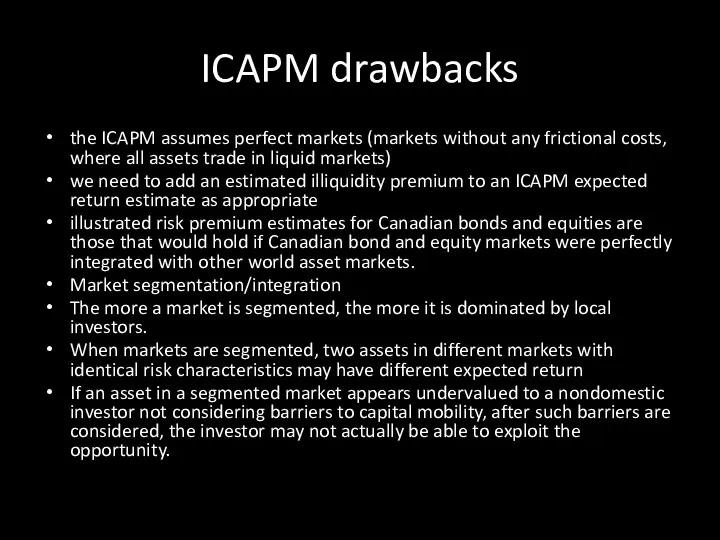

ICAPM drawbacks

the ICAPM assumes perfect markets (markets without any frictional costs,

ICAPM drawbacks

the ICAPM assumes perfect markets (markets without any frictional costs,

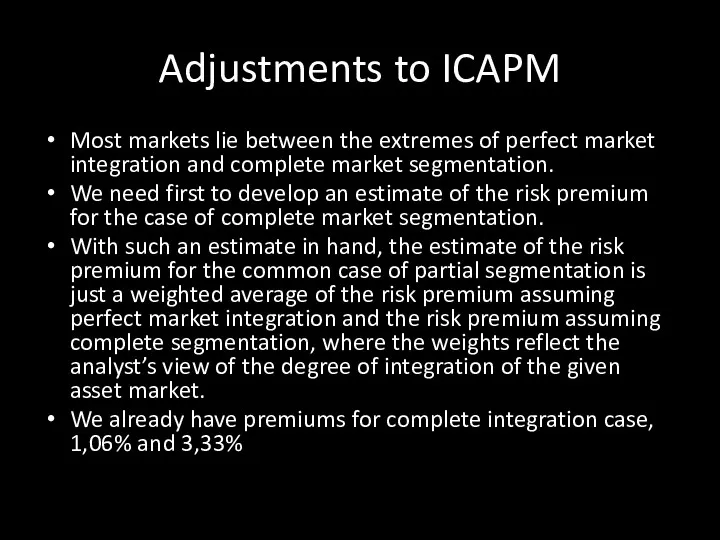

Adjustments to ICAPM

Most markets lie between the extremes of perfect market

Adjustments to ICAPM

Most markets lie between the extremes of perfect market

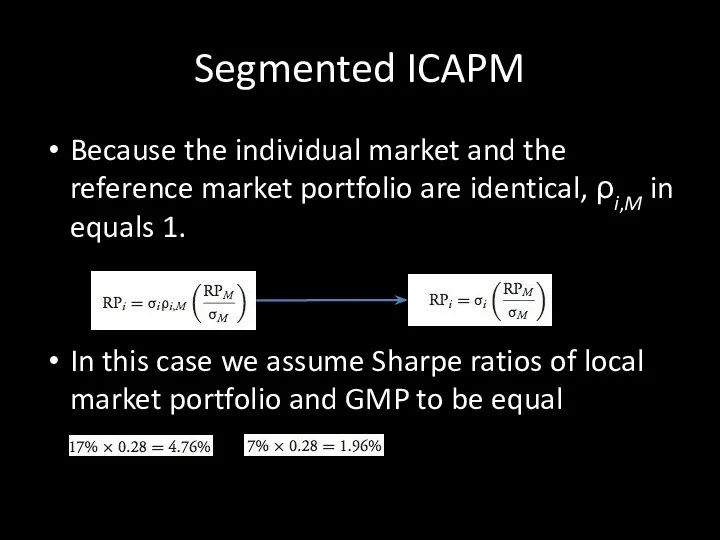

Segmented ICAPM

Because the individual market and the reference market portfolio are

Segmented ICAPM

Because the individual market and the reference market portfolio are

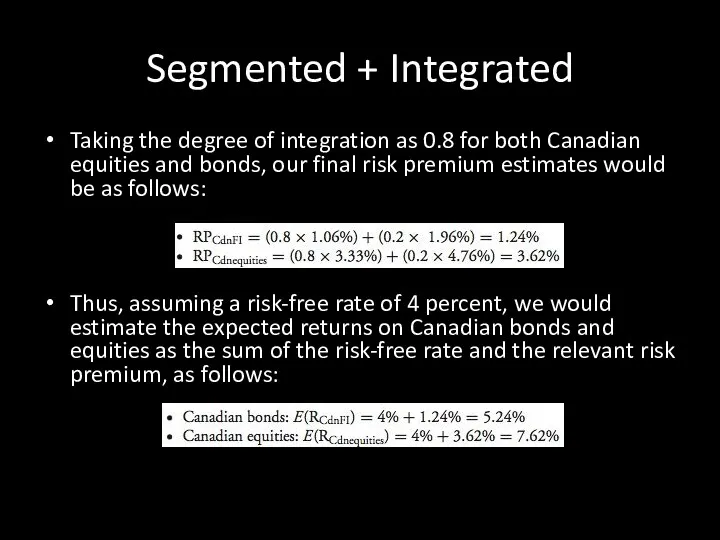

Segmented + Integrated

Taking the degree of integration as 0.8 for both

Segmented + Integrated

Taking the degree of integration as 0.8 for both

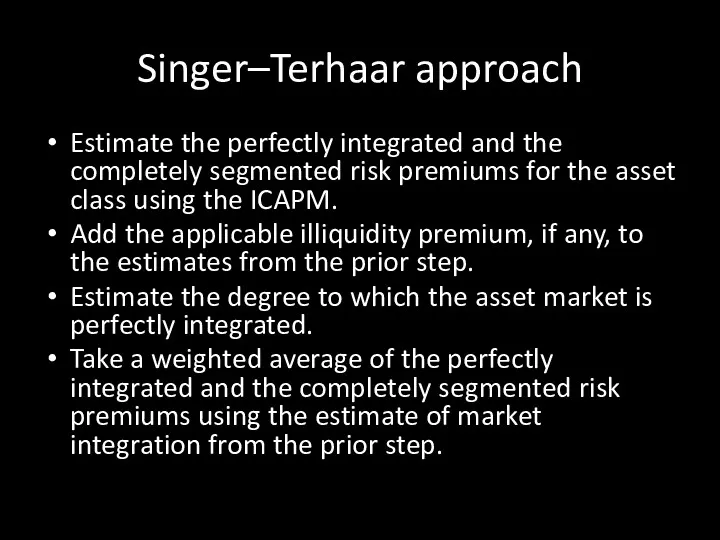

Singer–Terhaar approach

Estimate the perfectly integrated and the completely segmented risk premiums

Singer–Terhaar approach

Estimate the perfectly integrated and the completely segmented risk premiums

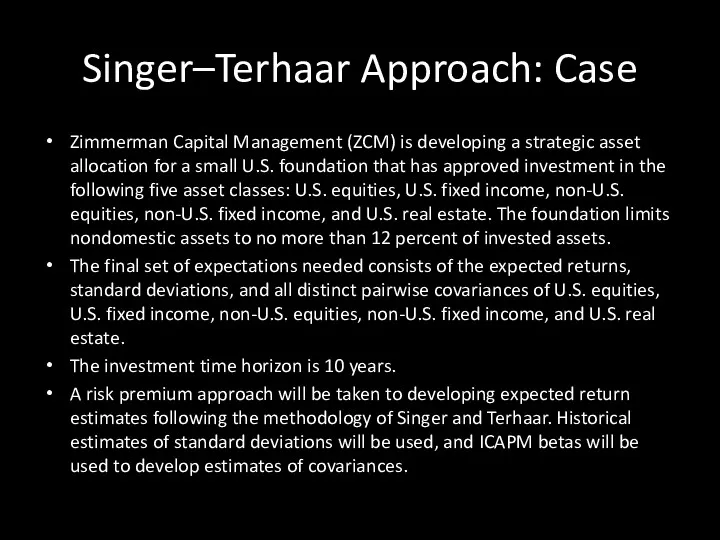

Singer–Terhaar Approach: Case

Zimmerman Capital Management (ZCM) is developing a strategic asset

Singer–Terhaar Approach: Case

Zimmerman Capital Management (ZCM) is developing a strategic asset

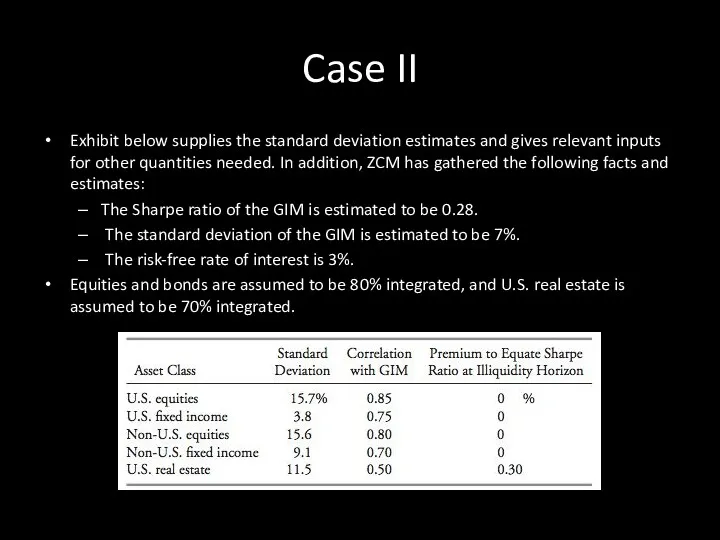

Case II

Exhibit below supplies the standard deviation estimates and gives relevant

Case II

Exhibit below supplies the standard deviation estimates and gives relevant

Case III

Based on the information given, address the following problems:

CalculatetheexpectedreturnsonU.S.equities,U.S.fixedincome,non-U.S.equi-

Case III

Based on the information given, address the following problems:

CalculatetheexpectedreturnsonU.S.equities,U.S.fixedincome,non-U.S.equi-

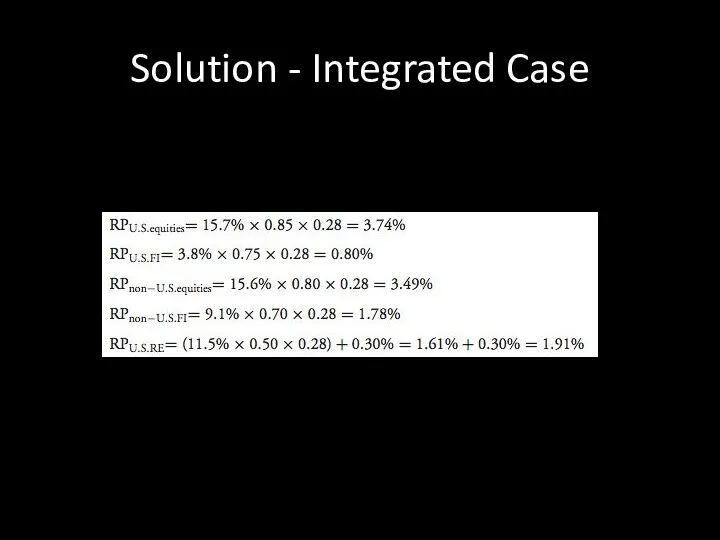

Solution - Integrated Case

Solution - Integrated Case

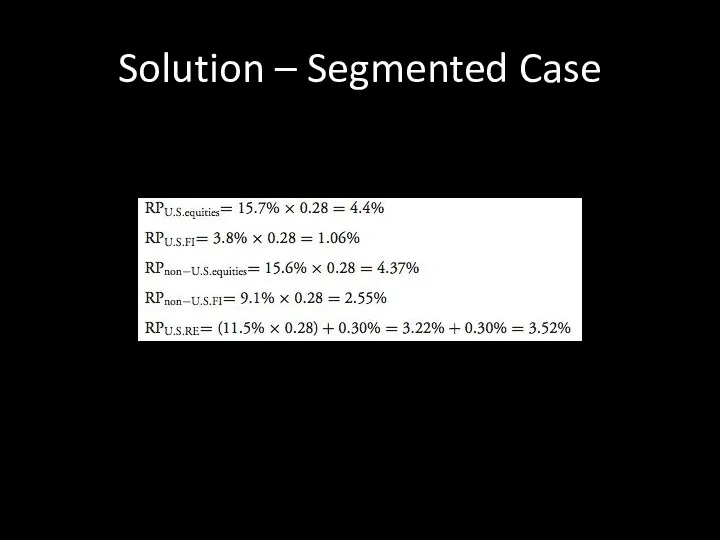

Solution – Segmented Case

Solution – Segmented Case

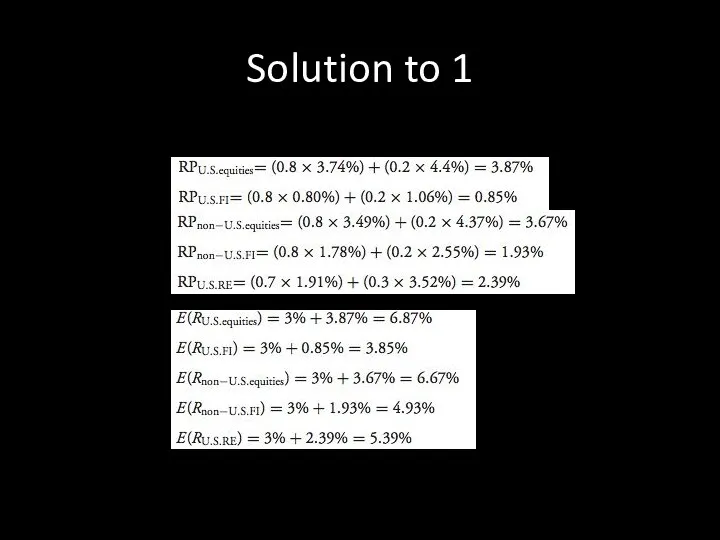

Solution to 1

Solution to 1

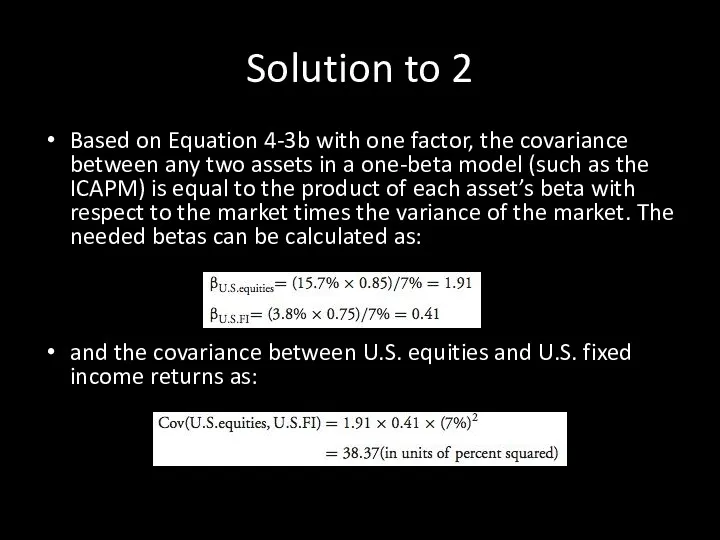

Solution to 2

Based on Equation 4-3b with one factor, the covariance

Solution to 2

Based on Equation 4-3b with one factor, the covariance

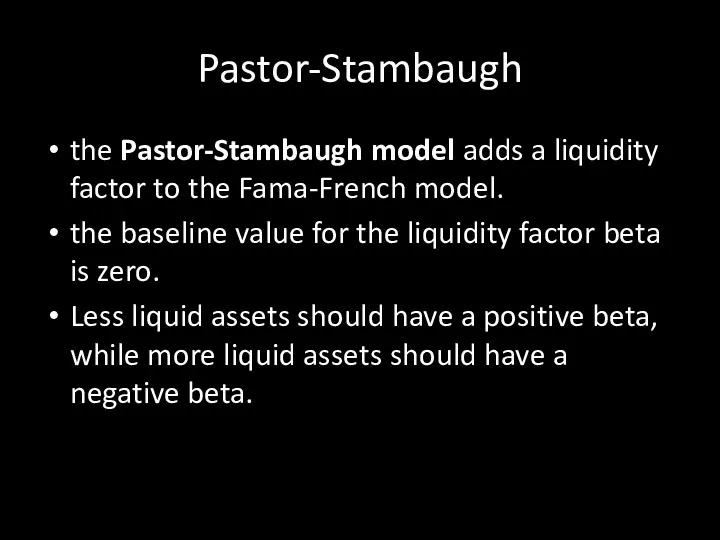

Pastor-Stambaugh

the Pastor-Stambaugh model adds a liquidity factor to the Fama-French model.

Pastor-Stambaugh

the Pastor-Stambaugh model adds a liquidity factor to the Fama-French model.

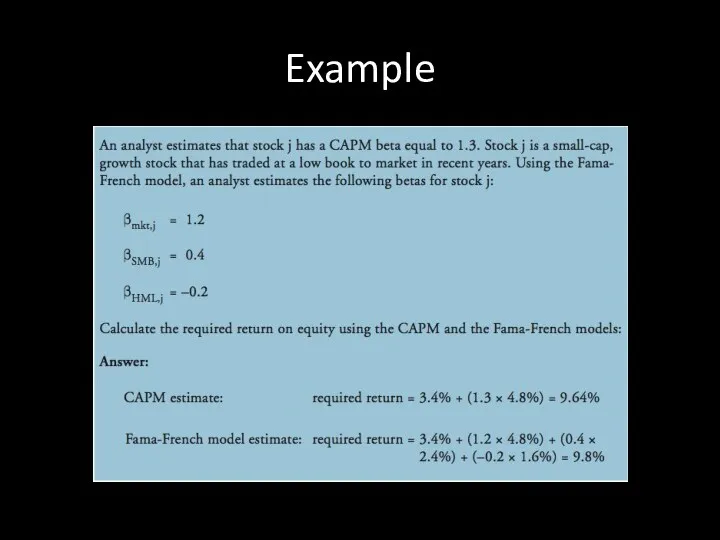

Example

Example

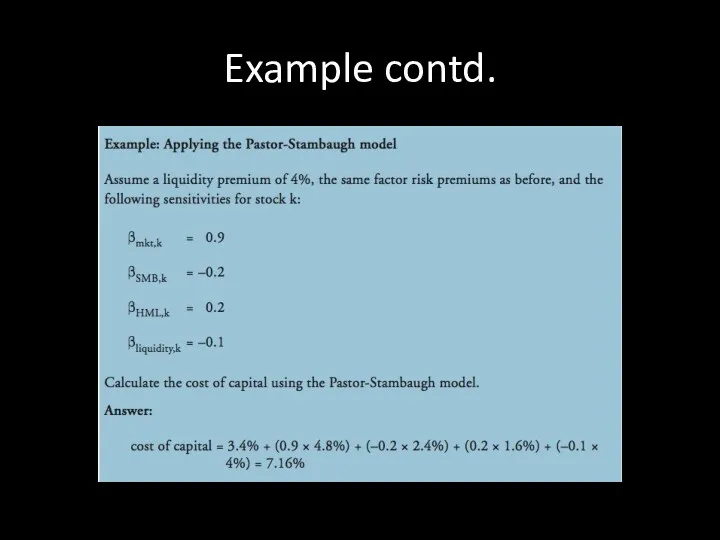

Example contd.

Example contd.

Adjusted betas

when making forecasts of the equity risk premium, some analysts

Adjusted betas

when making forecasts of the equity risk premium, some analysts

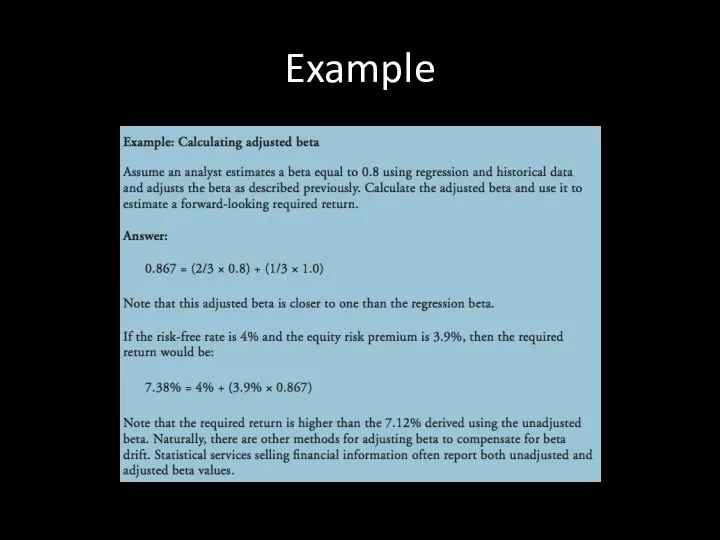

Example

Example

DEBTS: INTRO AND STRATEGIES

Part II.5

DEBTS: INTRO AND STRATEGIES

Part II.5

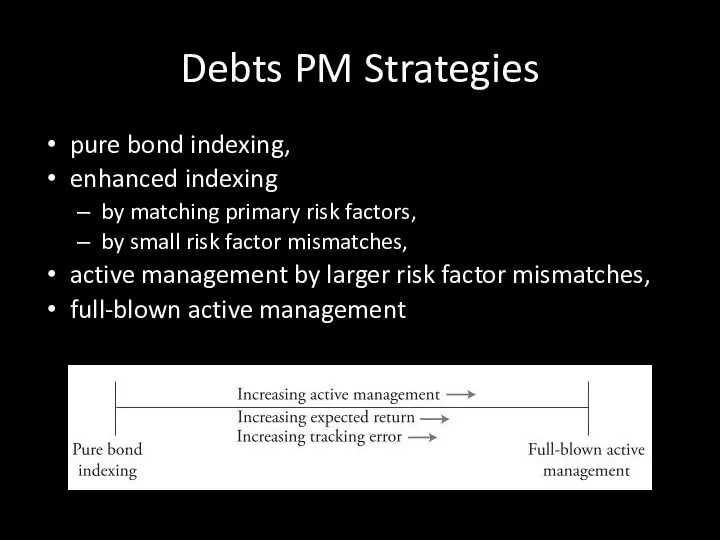

Debts PM Strategies

pure bond indexing,

enhanced indexing

by matching primary risk

Debts PM Strategies

pure bond indexing,

enhanced indexing

by matching primary risk

Pure bond indexing

objectives

Matching benchmark return

Technique

matching the portfolio’s characteristics to the

Pure bond indexing

objectives

Matching benchmark return

Technique

matching the portfolio’s characteristics to the

Enhanced indexing

Objective: enhancing return

Techniques:

matching primary risk factors (sampling),

primary

Enhanced indexing

Objective: enhancing return

Techniques:

matching primary risk factors (sampling),

primary

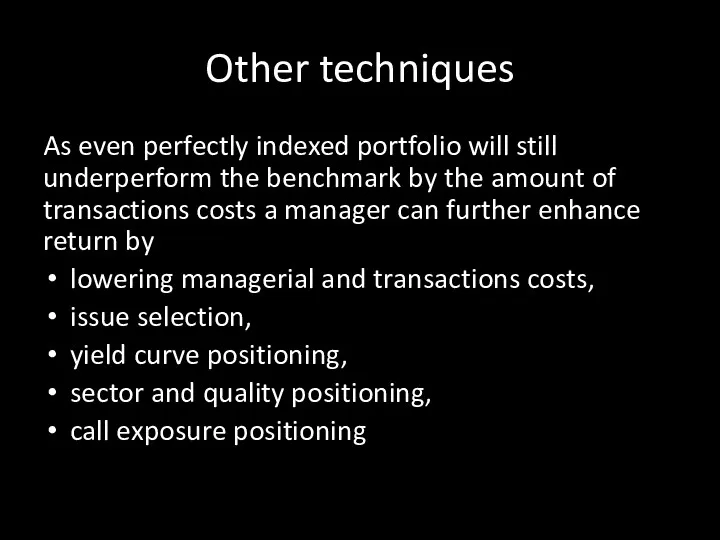

Other techniques

As even perfectly indexed portfolio will still underperform the benchmark

Other techniques

As even perfectly indexed portfolio will still underperform the benchmark

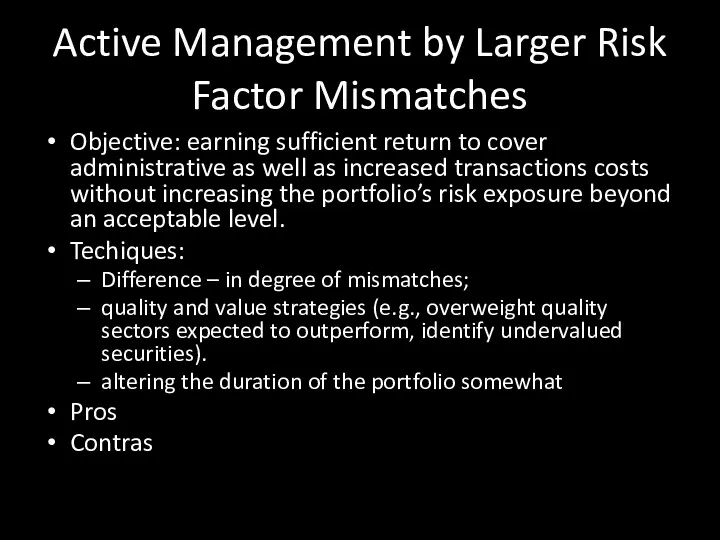

Active Management by Larger Risk Factor Mismatches

Objective: earning sufficient return

Active Management by Larger Risk Factor Mismatches

Objective: earning sufficient return

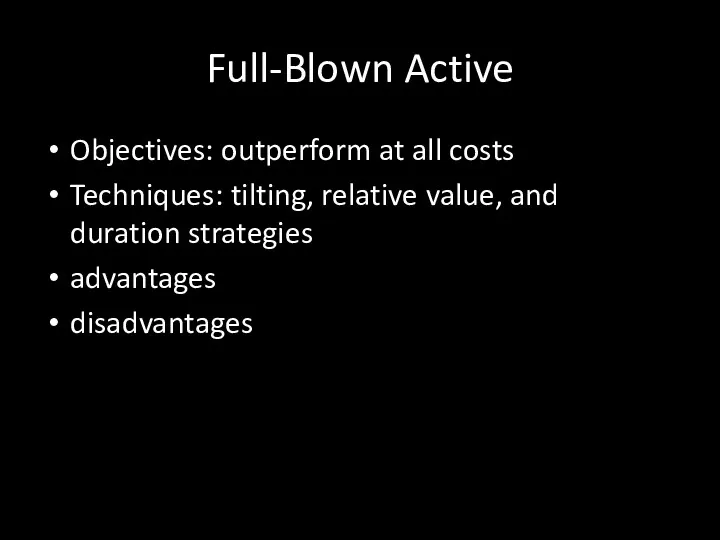

Full-Blown Active

Objectives: outperform at all costs

Techniques: tilting, relative value, and duration

Full-Blown Active

Objectives: outperform at all costs

Techniques: tilting, relative value, and duration

Summary of bonds portfolio managing strategies

Source: Maginn et al.

Summary of bonds portfolio managing strategies

Source: Maginn et al.

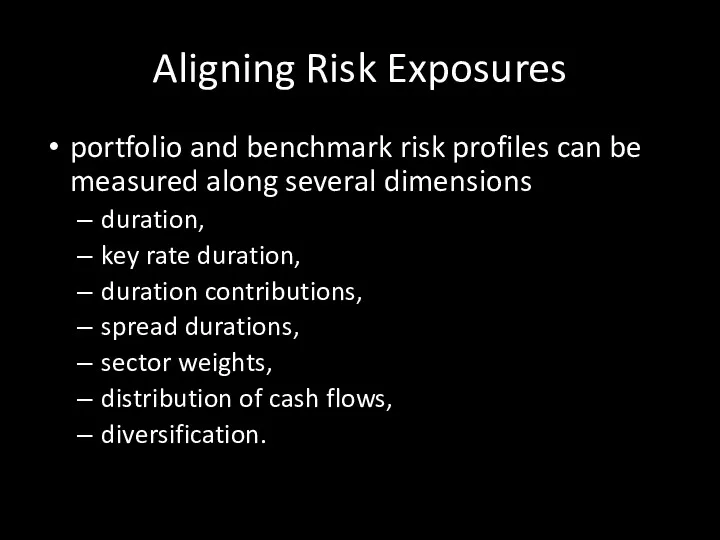

Aligning Risk Exposures

portfolio and benchmark risk profiles can be measured

Aligning Risk Exposures

portfolio and benchmark risk profiles can be measured

Предприятие в условиях рыночной экономики. (Тема 1)

Предприятие в условиях рыночной экономики. (Тема 1) Хозяйство США. Роль США в мировом хозяйстве

Хозяйство США. Роль США в мировом хозяйстве МИГРАЦИОННЫЙ КРИЗИС

МИГРАЦИОННЫЙ КРИЗИС Приоритеты программной стратегии России

Приоритеты программной стратегии России Взаимодействие глобальных проблем

Взаимодействие глобальных проблем Economy of the Arkhangelsk region. Fishing industry

Economy of the Arkhangelsk region. Fishing industry Виды и модели рынка труда

Виды и модели рынка труда Внешнеэкономическая и экономическая безопасность России

Внешнеэкономическая и экономическая безопасность России Экономическое стимулирование природоохранной деятельности (Тема 12)

Экономическое стимулирование природоохранной деятельности (Тема 12) Экономика производителя

Экономика производителя Причины и следствия мирового финансового кризиса 2008 года

Причины и следствия мирового финансового кризиса 2008 года Мировая экономика. (11 класс)

Мировая экономика. (11 класс) Тема 7. Кругооборот і оборот капіталу. Лекція 1. Рух капіталу, його стадії і форми. Функціональні форми капіталу

Тема 7. Кругооборот і оборот капіталу. Лекція 1. Рух капіталу, його стадії і форми. Функціональні форми капіталу Сущность и виды предпринимательства

Сущность и виды предпринимательства Экономический рост и институты

Экономический рост и институты Национальная экономика: цели и результаты развития

Национальная экономика: цели и результаты развития Инновационный процесс: сущность, этапы, модели

Инновационный процесс: сущность, этапы, модели Экономика родного края

Экономика родного края Глобалізація. Види глобалізації

Глобалізація. Види глобалізації Финансовая система и финансовая политика государства

Финансовая система и финансовая политика государства Анализ эффективности инструментов государственного регулирования рынка труда в РФ и ЕС

Анализ эффективности инструментов государственного регулирования рынка труда в РФ и ЕС Внутренняя среда организации

Внутренняя среда организации США в глобальной экономике и роли в странах АТР

США в глобальной экономике и роли в странах АТР Теоритические основы устойчивого развития территорий

Теоритические основы устойчивого развития территорий Генезис основных бизнес-моделей в экономике медиа

Генезис основных бизнес-моделей в экономике медиа Історія розвитку стандартизації у різних країнах світу

Історія розвитку стандартизації у різних країнах світу Мониторинг социально-экономических показателей развития города Тамбова

Мониторинг социально-экономических показателей развития города Тамбова Нұрлы жол – Нұрлы болашаққа бастар жол

Нұрлы жол – Нұрлы болашаққа бастар жол