- Introduction in Microeconomics

Содержание

- 2. STRUCTURE OF THE COURSE 13 Modules Midterm Exam(100) / Final Exam (200) Participation / tests 3

- 3. ECONOMICS IN NEWS 2008 seemed to be the year of economic news. From the worst financial

- 4. SCARCITY Our resources are LIMITED. At any one time, we have only so much land, so

- 5. SCARCITY AND THE FUNDAMENTAL ECONOMIC QUESTIONS What should be produced? How should goods and services be

- 6. OPPORTUNITY COST OPPORTUNITY COST is the value of the best alternative forgone in making any choice.

- 7. Limited resources Unlimited wants Microeconomics

- 8. SUMMARY Economics is a social science that examines how people choose among the alternatives available to

- 9. 10 PRINCIPLES OF ECONOMICS People face trade-offs (between efficiency and equity) The cost of something is

- 10. MACROECONOMICS AND MICROECONOMICS Macroeconomics is the branch of economics that focuses on the impact of choices

- 12. THE ECONOMISTS TOOLKIT In the scientific method, hypotheses are suggested and then tested. A HYPOTHESIS is

- 14. Скачать презентацию

STRUCTURE OF THE COURSE

13 Modules

Midterm Exam(100) / Final Exam (200)

Participation /

STRUCTURE OF THE COURSE

13 Modules

Midterm Exam(100) / Final Exam (200)

Participation /

ECONOMICS IN NEWS

2008 seemed to be the year of economic news.

ECONOMICS IN NEWS

2008 seemed to be the year of economic news.

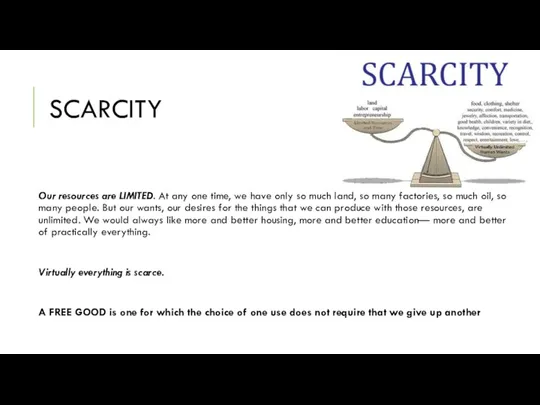

SCARCITY

Our resources are LIMITED. At any one time, we have only

SCARCITY

Our resources are LIMITED. At any one time, we have only

SCARCITY AND THE FUNDAMENTAL ECONOMIC QUESTIONS

What should be produced?

How should

SCARCITY AND THE FUNDAMENTAL ECONOMIC QUESTIONS

What should be produced?

How should

OPPORTUNITY COST

OPPORTUNITY COST is the value of the best alternative

OPPORTUNITY COST

OPPORTUNITY COST is the value of the best alternative

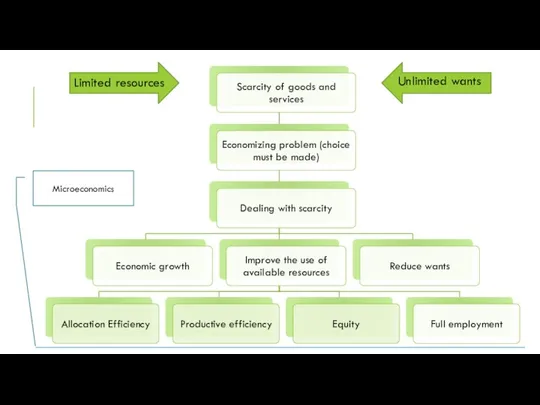

Limited resources

Unlimited wants

Microeconomics

Limited resources

Unlimited wants

Microeconomics

SUMMARY

Economics is a social science that examines how people choose among

SUMMARY

Economics is a social science that examines how people choose among

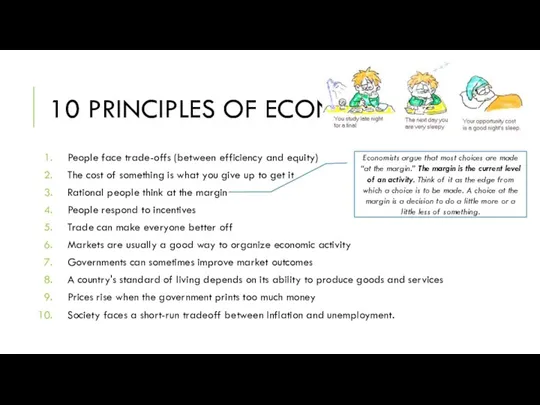

10 PRINCIPLES OF ECONOMICS

People face trade-offs (between efficiency and equity)

The cost

10 PRINCIPLES OF ECONOMICS

People face trade-offs (between efficiency and equity)

The cost

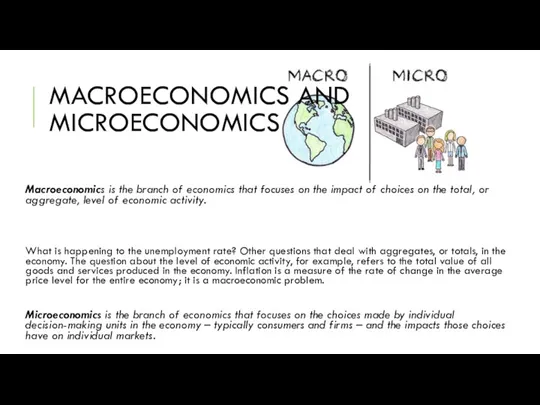

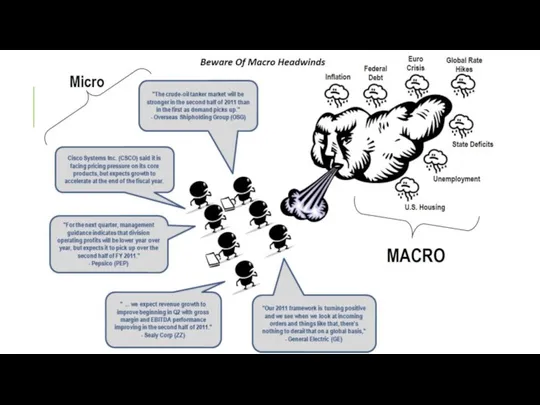

MACROECONOMICS AND MICROECONOMICS

Macroeconomics is the branch of economics that focuses on

MACROECONOMICS AND MICROECONOMICS

Macroeconomics is the branch of economics that focuses on

THE ECONOMISTS TOOLKIT

In the scientific method, hypotheses are suggested and

THE ECONOMISTS TOOLKIT

In the scientific method, hypotheses are suggested and

Основи наукових досліджень і організація науки. Організація наукових досліджень в Китаї

Основи наукових досліджень і організація науки. Організація наукових досліджень в Китаї Инвестирование – основа расширенного воспроизводства

Инвестирование – основа расширенного воспроизводства Балансы в экономике и необходимые условия экономического роста

Балансы в экономике и необходимые условия экономического роста Управление качеством

Управление качеством БЕРЕЖЛИВОЕ ПРОИЗВОДСТВО

БЕРЕЖЛИВОЕ ПРОИЗВОДСТВО Информационно - документационное обеспечение профессиональной деятельности

Информационно - документационное обеспечение профессиональной деятельности Баламалы энергия көздері. (9-сынып)

Баламалы энергия көздері. (9-сынып) Обзор ключевых показателей финансово-экономического развития Российской Федерации в современных условиях

Обзор ключевых показателей финансово-экономического развития Российской Федерации в современных условиях Великие географические открытия. Часть 1

Великие географические открытия. Часть 1 Цикличность экономического развития как закономерность макроэкономики. Безработица и инфляция. Лекция 8

Цикличность экономического развития как закономерность макроэкономики. Безработица и инфляция. Лекция 8 Глобализация и ее противоречия

Глобализация и ее противоречия Демократия. Местное самоуправление в РФ

Демократия. Местное самоуправление в РФ Спеціалізація, кооперування, концентрація та комбінування виробництва підприємств об’єднання

Спеціалізація, кооперування, концентрація та комбінування виробництва підприємств об’єднання Республика Беларусь в системе миро-хозяйственных связей

Республика Беларусь в системе миро-хозяйственных связей Модели циклических закономерностей национальной экономики

Модели циклических закономерностей национальной экономики Тест по теме: Безработица

Тест по теме: Безработица Геополитическое и экономико-географическое положение России (ЭГП)

Геополитическое и экономико-географическое положение России (ЭГП) Náklady a nákladová funkce

Náklady a nákladová funkce Международная сегментация и стратегии проникновения на зарубежные рынки

Международная сегментация и стратегии проникновения на зарубежные рынки Введение в анализ логистической поддержки. Основные термины, определения и сокращения

Введение в анализ логистической поддержки. Основные термины, определения и сокращения Экономика и экономическая наука

Экономика и экономическая наука Теоретические основы ценообразования в рыночной экономике

Теоретические основы ценообразования в рыночной экономике Административно-правовые основы управления отдельными отраслями экономики в Республике Беларусь

Административно-правовые основы управления отдельными отраслями экономики в Республике Беларусь Развитие Осьминской территории. Проблемы, возможности, перспективы

Развитие Осьминской территории. Проблемы, возможности, перспективы Системы, их строение и функционирование

Системы, их строение и функционирование Государственный и муниципальный сектор экономики: основные понятия

Государственный и муниципальный сектор экономики: основные понятия ВВП и его измерение

ВВП и его измерение Ринок в економічній системі суспільства

Ринок в економічній системі суспільства