- Primary dealership Ukraine

Содержание

- 2. Introduction After a series of preliminary discussions with the local Banking community, the National bank of

- 3. General set-up and regulatory pre-conditions Dealers: banks registered in Ukraine (including subsidiaries) Maximum number of primary

- 4. The club development in 2009 The selection process procedure: - Should MoF not have managed to

- 5. The general comment of SCO (Jacques Mounier) in support of this activity : - This request

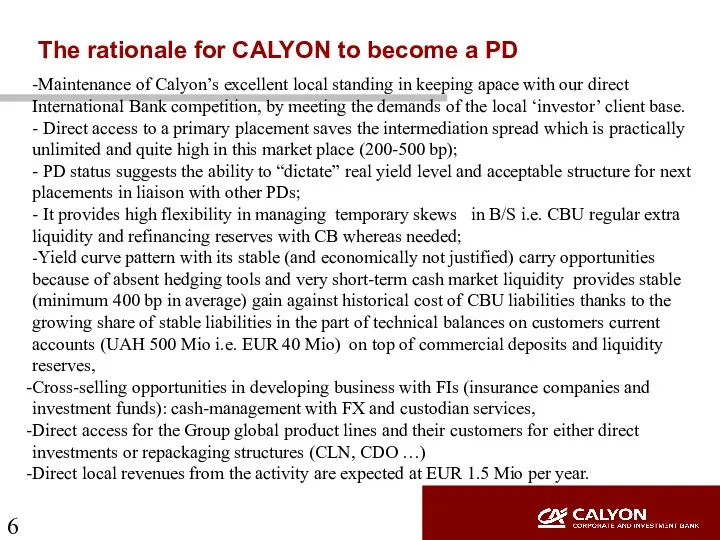

- 6. The rationale for CALYON to become a PD -Maintenance of Calyon’s excellent local standing in keeping

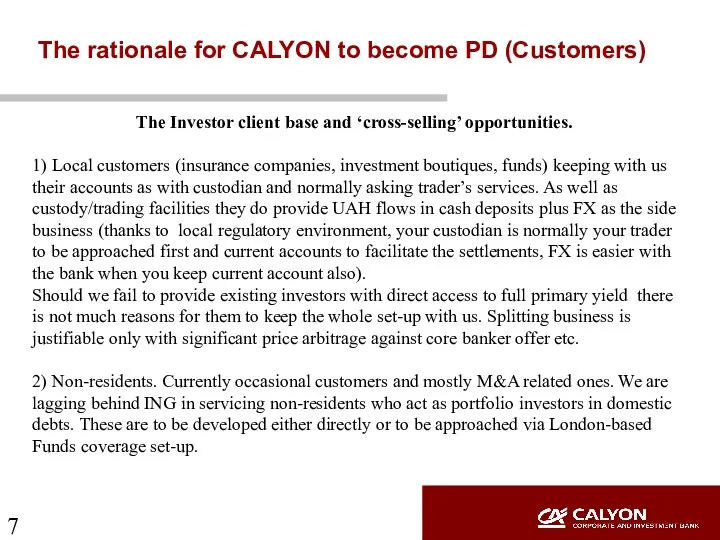

- 7. The rationale for CALYON to become PD (Customers) The Investor client base and ‘cross-selling’ opportunities. 1)

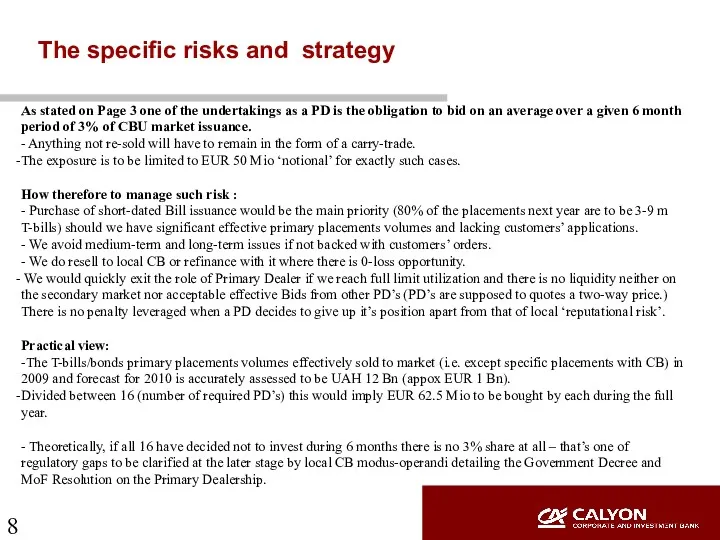

- 8. The specific risks and strategy As stated on Page 3 one of the undertakings as a

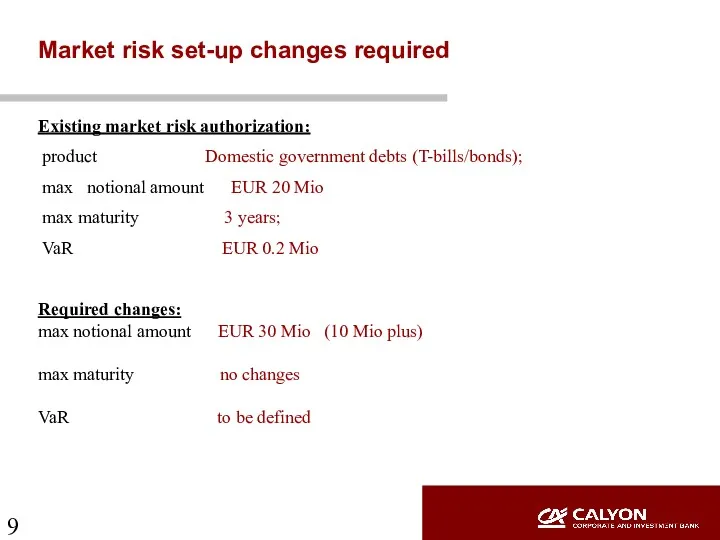

- 9. Market risk set-up changes required Existing market risk authorization: product Domestic government debts (T-bills/bonds); max notional

- 10. H/C and Cost No additional HC is required – requirement of handling the ‘2-way’ quotation as

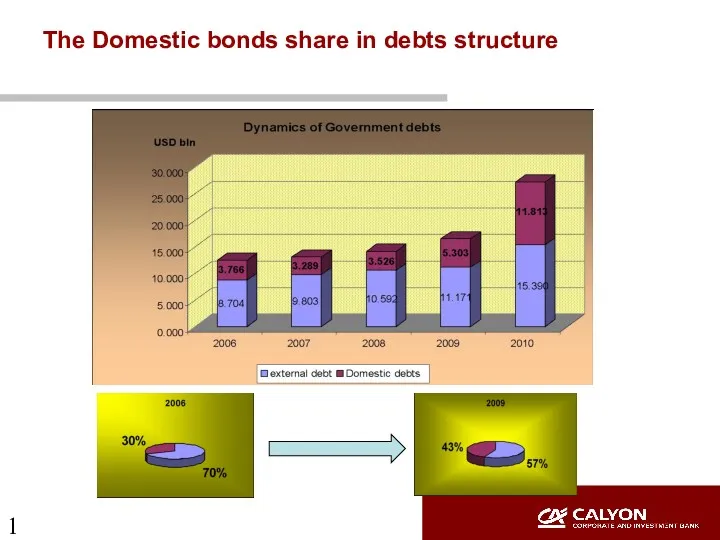

- 11. The Domestic bonds share in debts structure

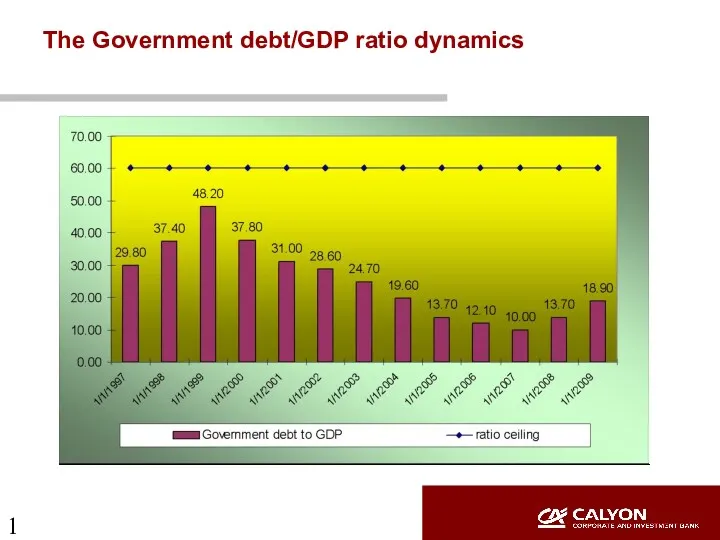

- 12. The Government debt/GDP ratio dynamics

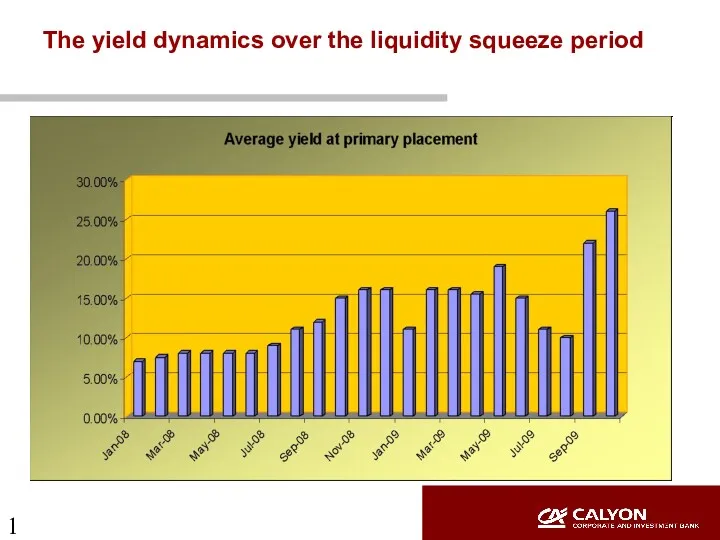

- 13. The yield dynamics over the liquidity squeeze period

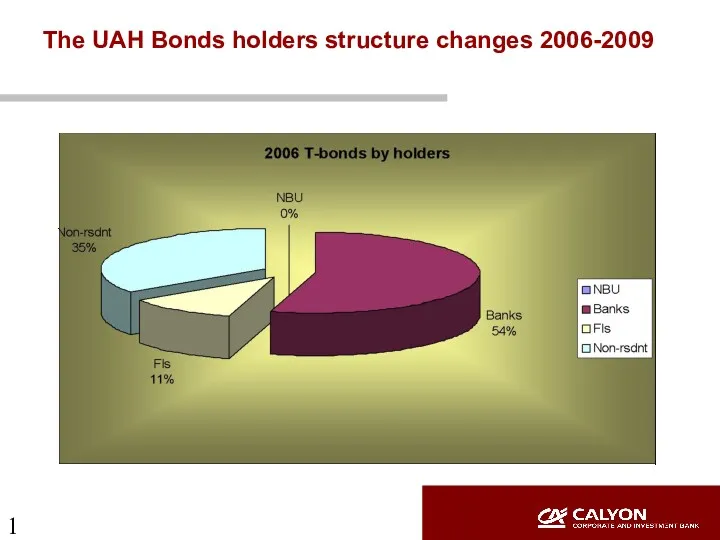

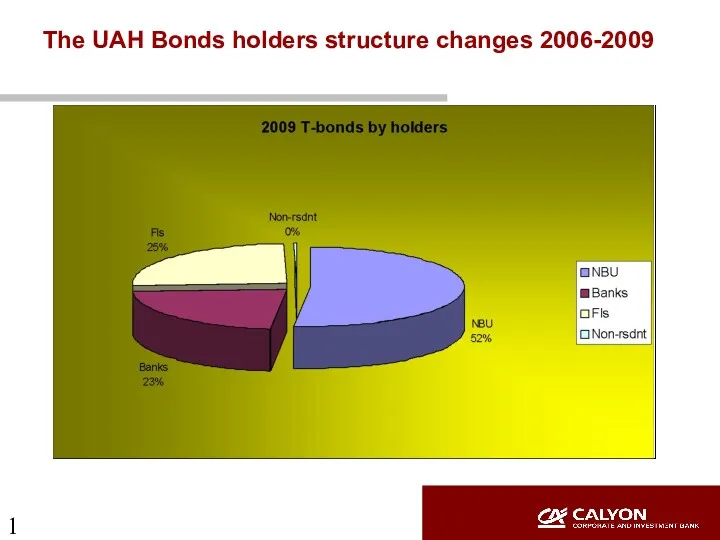

- 14. The UAH Bonds holders structure changes 2006-2009

- 15. The UAH Bonds holders structure changes 2006-2009

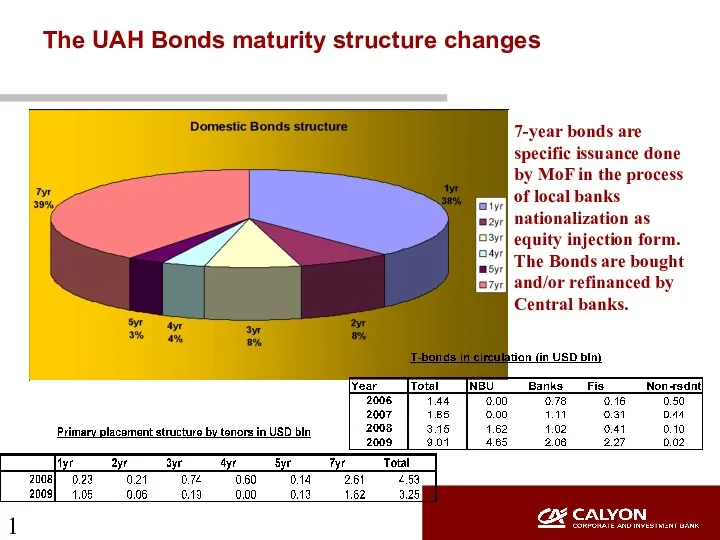

- 16. The UAH Bonds maturity structure changes 7-year bonds are specific issuance done by MoF in the

- 18. Скачать презентацию

Introduction

After a series of preliminary discussions with the local Banking community,

Introduction

After a series of preliminary discussions with the local Banking community,

General set-up and regulatory pre-conditions

Dealers: banks registered in Ukraine (including

General set-up and regulatory pre-conditions

Dealers: banks registered in Ukraine (including

The club development in 2009

The selection process procedure:

- Should MoF not

The club development in 2009

The selection process procedure:

- Should MoF not

The general comment of SCO (Jacques Mounier) in support of this

The general comment of SCO (Jacques Mounier) in support of this

The rationale for CALYON to become a PD

-Maintenance of Calyon’s excellent

The rationale for CALYON to become a PD

-Maintenance of Calyon’s excellent

The rationale for CALYON to become PD (Customers)

The Investor client base

The rationale for CALYON to become PD (Customers)

The Investor client base

The specific risks and strategy

As stated on Page 3 one

The specific risks and strategy

As stated on Page 3 one

Market risk set-up changes required

Existing market risk authorization:

product

Market risk set-up changes required

Existing market risk authorization:

product

H/C and Cost

No additional HC is required – requirement of

H/C and Cost

No additional HC is required – requirement of

The Domestic bonds share in debts structure

The Domestic bonds share in debts structure

The Government debt/GDP ratio dynamics

The Government debt/GDP ratio dynamics

The yield dynamics over the liquidity squeeze period

The yield dynamics over the liquidity squeeze period

The UAH Bonds holders structure changes 2006-2009

The UAH Bonds holders structure changes 2006-2009

The UAH Bonds holders structure changes 2006-2009

The UAH Bonds holders structure changes 2006-2009

The UAH Bonds maturity structure changes

7-year bonds are specific issuance done

The UAH Bonds maturity structure changes

7-year bonds are specific issuance done

Материальные ресурсы предприятия

Материальные ресурсы предприятия Монетарная экономика: предложение денег. Макроэкономика. Тема 7

Монетарная экономика: предложение денег. Макроэкономика. Тема 7 Тест по теме: Безработица

Тест по теме: Безработица Производитель на рынке. Сфера производства

Производитель на рынке. Сфера производства Игра Интеллектуальное сайджу

Игра Интеллектуальное сайджу Квалиметрия, как наука. (Тема 2)

Квалиметрия, как наука. (Тема 2) Оптимизация процесса складирования и отпуска ТМЦ на Главном складе Красноярской дирекции материально-технического обеспечения

Оптимизация процесса складирования и отпуска ТМЦ на Главном складе Красноярской дирекции материально-технического обеспечения Роль государства в экономике

Роль государства в экономике Роль и место России в мировом хозяйстве. Стратегия развития на современном экономическом этапе

Роль и место России в мировом хозяйстве. Стратегия развития на современном экономическом этапе Как устроена мировая экономика. 10 класс

Как устроена мировая экономика. 10 класс Система национальных счетов (СНС)

Система национальных счетов (СНС) Международные аспекты экономической теории

Международные аспекты экономической теории Tacis-методы проведения анализов и изучения рынка

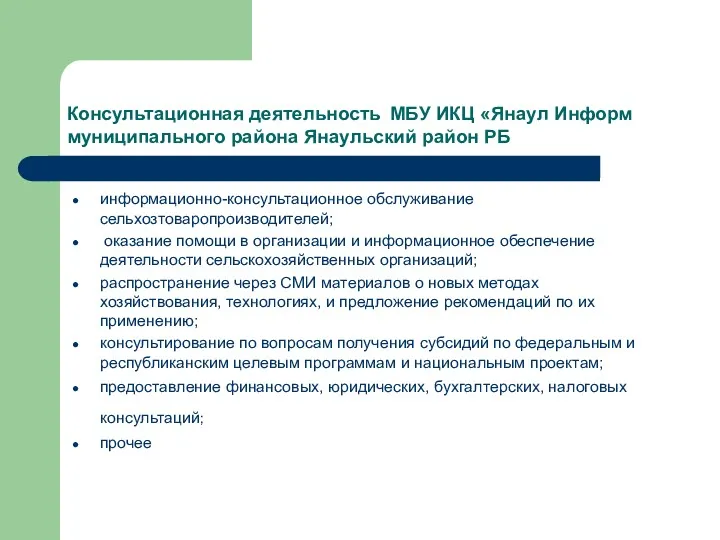

Tacis-методы проведения анализов и изучения рынка Консультационная деятельность МБУ ИКЦ Янаул Информ муниципального района Янаульский район РБ

Консультационная деятельность МБУ ИКЦ Янаул Информ муниципального района Янаульский район РБ Экономика. Сущность экономического цикла и его фазы

Экономика. Сущность экономического цикла и его фазы Макро и микро – экономические анализы

Макро и микро – экономические анализы Разработка рекомендаций по управлению затратами по внедрению системы менеджмента качества на предприятии на примере ООО ШТД

Разработка рекомендаций по управлению затратами по внедрению системы менеджмента качества на предприятии на примере ООО ШТД Тема 8. Теневая ( внелегальная) экономика

Тема 8. Теневая ( внелегальная) экономика Бюджетный процесс в РФ

Бюджетный процесс в РФ Управление человеческими ресурсами

Управление человеческими ресурсами Теоретико-методологические основы государственного регулирования экономики

Теоретико-методологические основы государственного регулирования экономики Методологические подходы в оценке экономической эффективности диагностики оборудования, как инструмент снижения затрат на ТОиР

Методологические подходы в оценке экономической эффективности диагностики оборудования, как инструмент снижения затрат на ТОиР Экономиканы мемлекеттік реттеу әдістемесінің түсінігі және оның негізгі элементтері

Экономиканы мемлекеттік реттеу әдістемесінің түсінігі және оның негізгі элементтері Макроэкономика. Определение выпуска, совокупное предложение и совокупный спрос

Макроэкономика. Определение выпуска, совокупное предложение и совокупный спрос Предмет и методологические принципы макроэкономики. Модель круговых потоков

Предмет и методологические принципы макроэкономики. Модель круговых потоков Земельные ресурсы

Земельные ресурсы Master class. Dº Consumo

Master class. Dº Consumo Виды и характеристики технологий в инновационной деятельности. Лекция 3

Виды и характеристики технологий в инновационной деятельности. Лекция 3