- Products of the past: One Size Fits All

Содержание

- 2. Emergency Access Waiver Active on FIT Retirement Series products currently in 403(b) or 457(b) status and

- 3. Products That Go With the Flow Regularly scheduled contributions for as little as $100 a month

- 4. Customer is at the Heart of FIT Retirement Series Over 10 years to retirement Wants a

- 5. This is Barbara’s FIT MORE Upside potential than a bank product through: Higher caps Indices* Tax-deferred

- 6. This is Wade’s FIT MORE Upside potential through: Higher caps Indices* Tax-deferred growth Income rider with

- 7. Market Potential GLIR with Increasing Income Withdrawal percentage for Single Life Level Option shown above; Joint

- 8. This is Carol’s FIT MORE Upside potential than current interest rates through: 5% immediate interest credit

- 9. This is Frank’s FIT MORE Liquidity and income certainty through: Emergency Access Waiver Income rider, at

- 10. Simple Roll-up GLIR Withdrawal percentage for Single Life Level Option shown above; Joint Life Level Option,

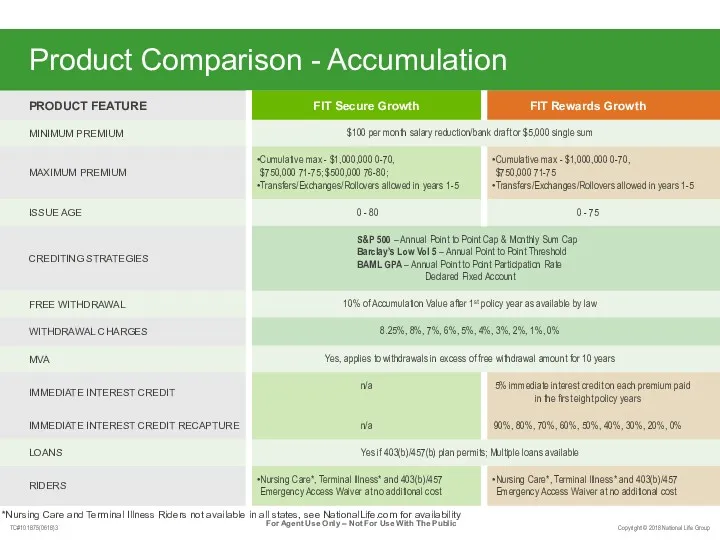

- 11. Product Comparison - Accumulation *Nursing Care and Terminal Illness Riders not available in all states, see

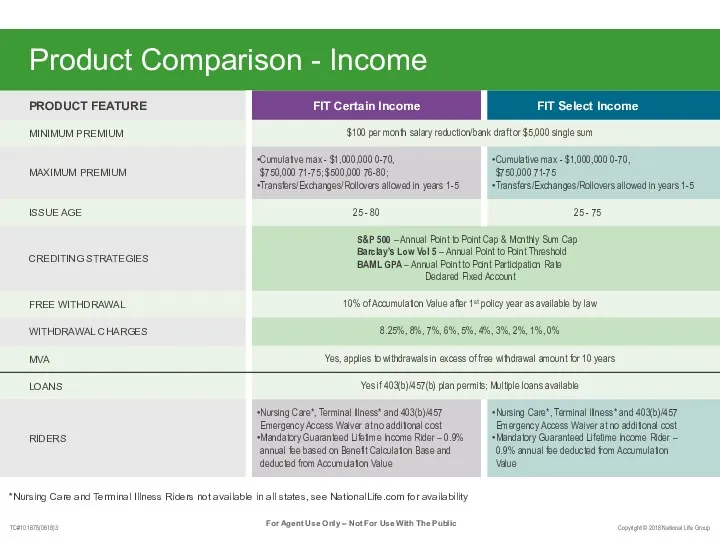

- 12. Product Comparison - Income *Nursing Care and Terminal Illness Riders not available in all states, see

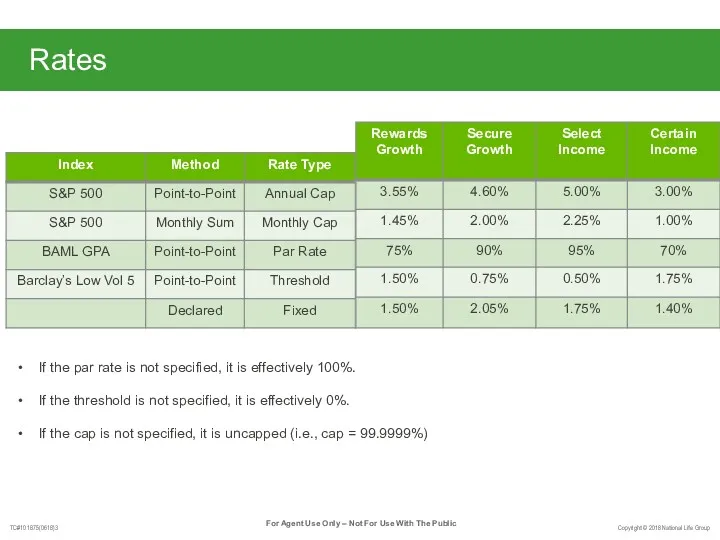

- 13. Rates If the par rate is not specified, it is effectively 100%. If the threshold is

- 15. Скачать презентацию

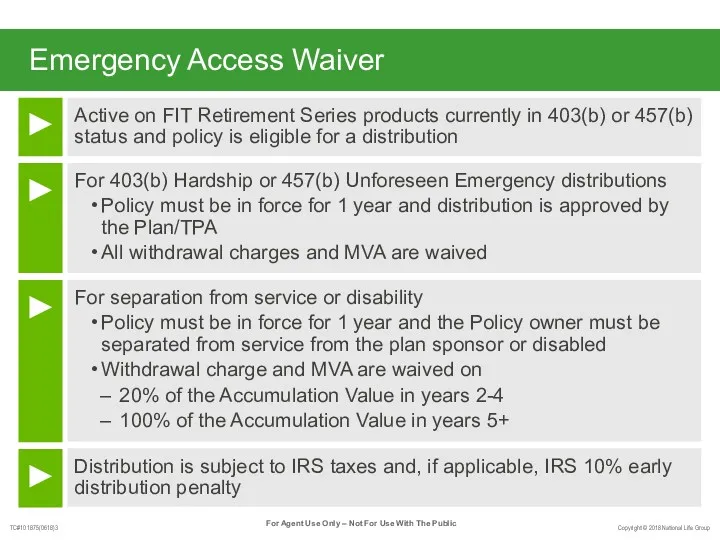

Emergency Access Waiver

Active on FIT Retirement Series products currently in 403(b)

Emergency Access Waiver

Active on FIT Retirement Series products currently in 403(b)

Products That Go With the Flow

Regularly scheduled contributions for as little

Products That Go With the Flow

Regularly scheduled contributions for as little

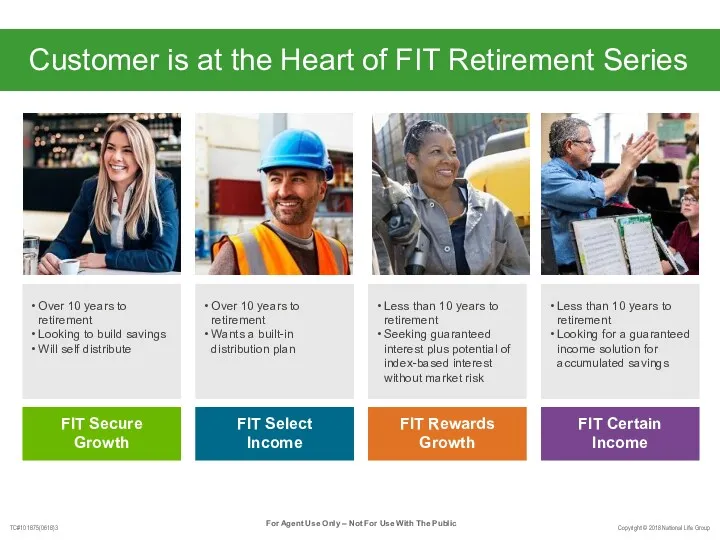

Customer is at the Heart of FIT Retirement Series

Over 10 years

Customer is at the Heart of FIT Retirement Series

Over 10 years

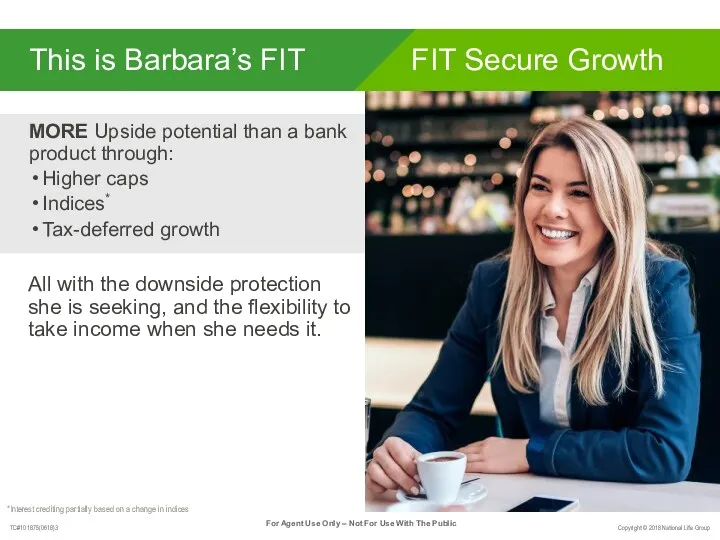

This is Barbara’s FIT

MORE Upside potential than a bank product through:

Higher

This is Barbara’s FIT

MORE Upside potential than a bank product through:

Higher

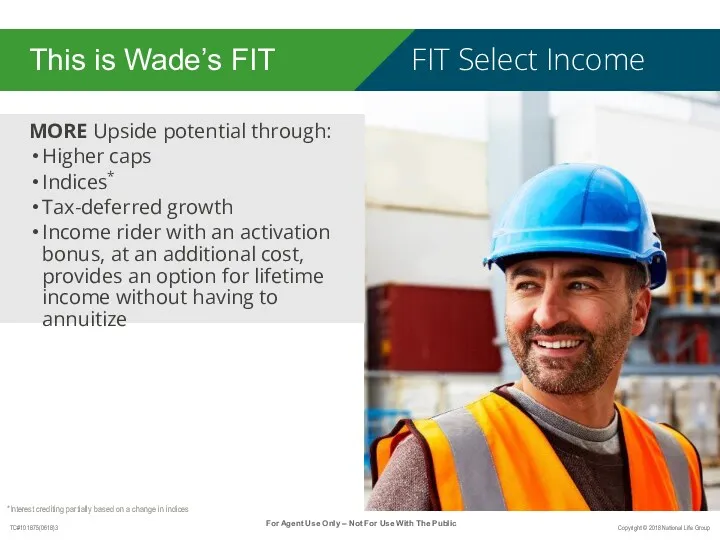

This is Wade’s FIT

MORE Upside potential through:

Higher caps

Indices*

Tax-deferred growth

Income rider with

This is Wade’s FIT

MORE Upside potential through:

Higher caps

Indices*

Tax-deferred growth

Income rider with

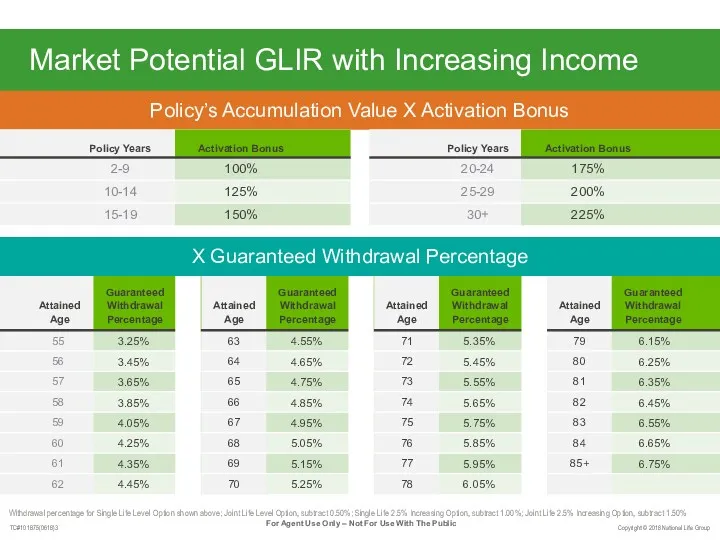

Market Potential GLIR with Increasing Income

Withdrawal percentage for Single Life Level

Market Potential GLIR with Increasing Income

Withdrawal percentage for Single Life Level

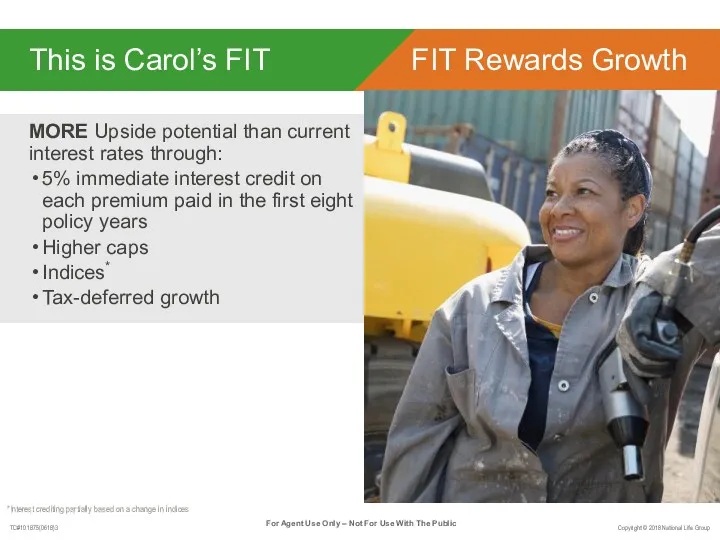

This is Carol’s FIT

MORE Upside potential than current interest rates through:

5%

This is Carol’s FIT

MORE Upside potential than current interest rates through:

5%

This is Frank’s FIT

MORE Liquidity and income certainty through:

Emergency Access Waiver

Income

This is Frank’s FIT

MORE Liquidity and income certainty through:

Emergency Access Waiver

Income

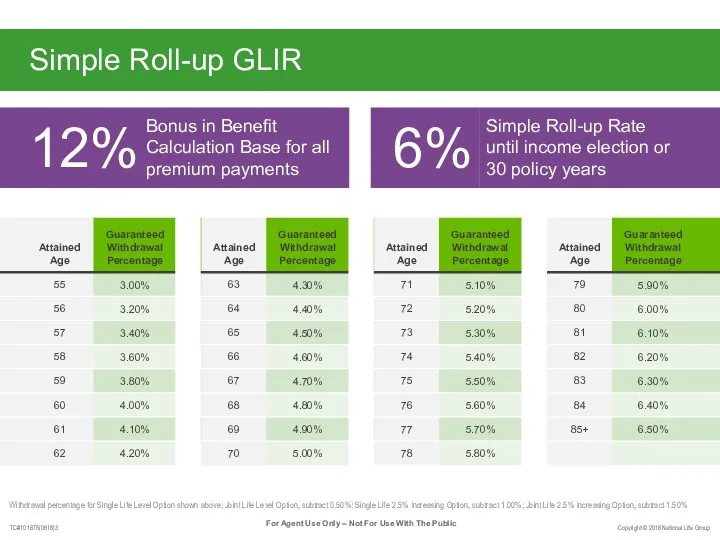

Simple Roll-up GLIR

Withdrawal percentage for Single Life Level Option shown above;

Simple Roll-up GLIR

Withdrawal percentage for Single Life Level Option shown above;

Product Comparison - Accumulation

*Nursing Care and Terminal Illness Riders not available

Product Comparison - Accumulation

*Nursing Care and Terminal Illness Riders not available

Product Comparison - Income

*Nursing Care and Terminal Illness Riders not available

Product Comparison - Income

*Nursing Care and Terminal Illness Riders not available

Rates

If the par rate is not specified, it is effectively 100%.

If

Rates

If the par rate is not specified, it is effectively 100%.

If

Стратегии продвижения товара

Стратегии продвижения товара Электронная коммерция

Электронная коммерция Разработка проекта по продвижению музыкальной группы LaScala

Разработка проекта по продвижению музыкальной группы LaScala Повышение продаж на сайте в несколько кликов

Повышение продаж на сайте в несколько кликов Сеть современных универсальных книжных магазинов Читай-город

Сеть современных универсальных книжных магазинов Читай-город Несколько рецептов для меню аргонавта

Несколько рецептов для меню аргонавта Marketing for Hospitality and Tourism. The Role of Marketing in Strategic Planning. Chapter 3

Marketing for Hospitality and Tourism. The Role of Marketing in Strategic Planning. Chapter 3 Курс тренинг с экономическим эффектом

Курс тренинг с экономическим эффектом Product concepts

Product concepts Каталитическое системы - отопления помещений - очистки воздуха. ООО ЭкоКат

Каталитическое системы - отопления помещений - очистки воздуха. ООО ЭкоКат Характеристики маркетингу. Маркетингові дослідження

Характеристики маркетингу. Маркетингові дослідження Наше новое имя. Бизнес-студия

Наше новое имя. Бизнес-студия Microsoft PowerPoint

Microsoft PowerPoint Semiconductor Chips that Support AI

Semiconductor Chips that Support AI Kaspersky internet security 2017

Kaspersky internet security 2017 Торговый кластер под размещение объектов торговли (48 магазинов)

Торговый кластер под размещение объектов торговли (48 магазинов) Компания Faberon

Компания Faberon Lnternational marketing. Social and cultural environment. (Chapter 4)

Lnternational marketing. Social and cultural environment. (Chapter 4) TCP Optimization

TCP Optimization Не экономьте на бизнесе. Экономьте на связи

Не экономьте на бизнесе. Экономьте на связи Результаты работы по проекту ЕРКЦ в 2015 году и планы на 2016 год

Результаты работы по проекту ЕРКЦ в 2015 году и планы на 2016 год Маркетинг и продажи

Маркетинг и продажи Cost & Sell. CRM sample

Cost & Sell. CRM sample Brief Mika Barni

Brief Mika Barni Как увеличить прибыль своего бизнеса

Как увеличить прибыль своего бизнеса Икона рекламного бизнеса XX века. Coca-Cola

Икона рекламного бизнеса XX века. Coca-Cola Латеральный маркетинг

Латеральный маркетинг The 10 Golden Rules of Customer Service

The 10 Golden Rules of Customer Service