- Strategy and Analysis in Using Net Present Value. Stewart Pharmaceuticals

Содержание

- 2. Chapter Outline 8.1 Decision Trees 8.4 Options

- 3. Stewart Pharmaceuticals The Stewart Pharmaceuticals Corporation is considering investing in developing a drug that cures the

- 4. Stewart Pharmaceuticals NPV of Full-Scale Production following Successful Test Note that the NPV is calculated as

- 5. Stewart Pharmaceuticals NPV of Full-Scale Production following Unsuccessful Test Note that the NPV is calculated as

- 6. Decision Tree for Stewart Pharmaceutical Do not test Test Failure Success Do not invest Invest The

- 7. Stewart Pharmaceutical: Decision to Test Let’s move back to the first stage, where the decision boils

- 8. 8.4 Options One of the fundamental insights of modern finance theory is that options have value.

- 9. Options The Option to Expand Has value if demand turns out to be higher than expected.

- 10. The Option to Expand Imagine a start-up firm, Campusteria, Inc. which plans to open private (for-profit)

- 11. Campusteria pro forma Income Statement We plan to sell 25 meal plans at $200 per month

- 12. The Option to Expand: Valuing a Start-Up Note that while the Campusteria test site has a

- 13. Discounted Cash Flows and Options We can calculate the market value of a project as the

- 14. The Option to Abandon: Example Suppose that we are drilling an oil well. The drilling rig

- 15. The Option to Abandon: Example Traditional NPV analysis would indicate rejection of the project.

- 16. The Option to Abandon: Example The firm has two decisions to make: drill or not, abandon

- 17. The Option to Abandon: Example When we include the value of the option to abandon, the

- 18. Valuation of the Option to Abandon Recall that we can calculate the market value of a

- 20. Скачать презентацию

Chapter Outline

8.1 Decision Trees

8.4 Options

Chapter Outline

8.1 Decision Trees

8.4 Options

Stewart Pharmaceuticals

The Stewart Pharmaceuticals Corporation is considering investing in developing

Stewart Pharmaceuticals

The Stewart Pharmaceuticals Corporation is considering investing in developing

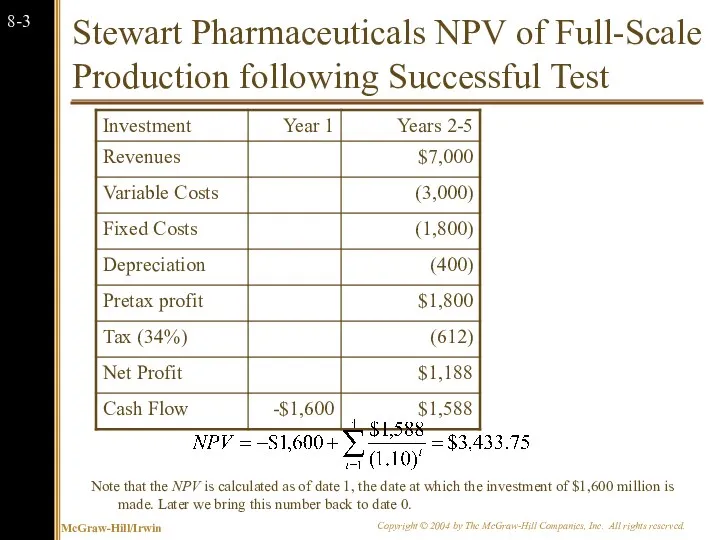

Stewart Pharmaceuticals NPV of Full-Scale Production following Successful Test

Note that the

Stewart Pharmaceuticals NPV of Full-Scale Production following Successful Test

Note that the

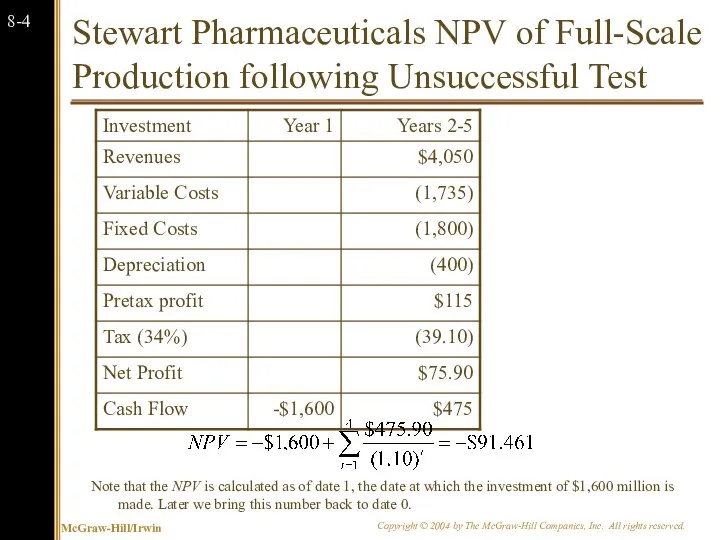

Stewart Pharmaceuticals NPV of Full-Scale Production following Unsuccessful Test

Note that the

Stewart Pharmaceuticals NPV of Full-Scale Production following Unsuccessful Test

Note that the

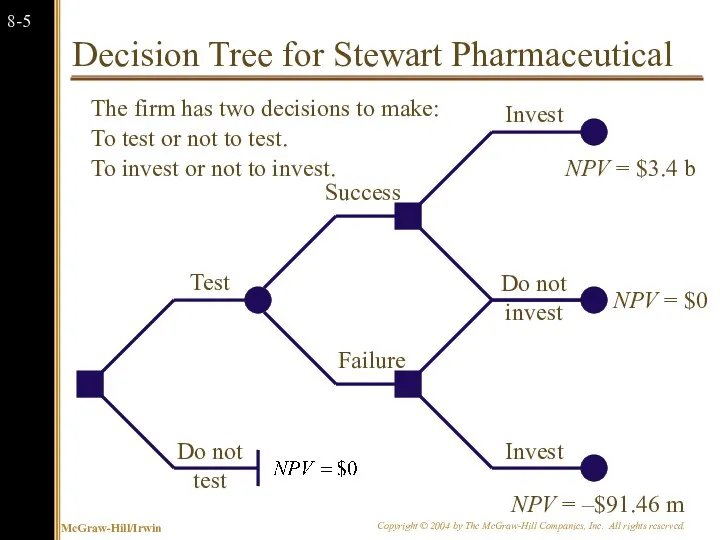

Decision Tree for Stewart Pharmaceutical

Do not test

Test

Failure

Success

Do not invest

Invest

The firm has

Decision Tree for Stewart Pharmaceutical

Do not test

Test

Failure

Success

Do not invest

Invest

The firm has

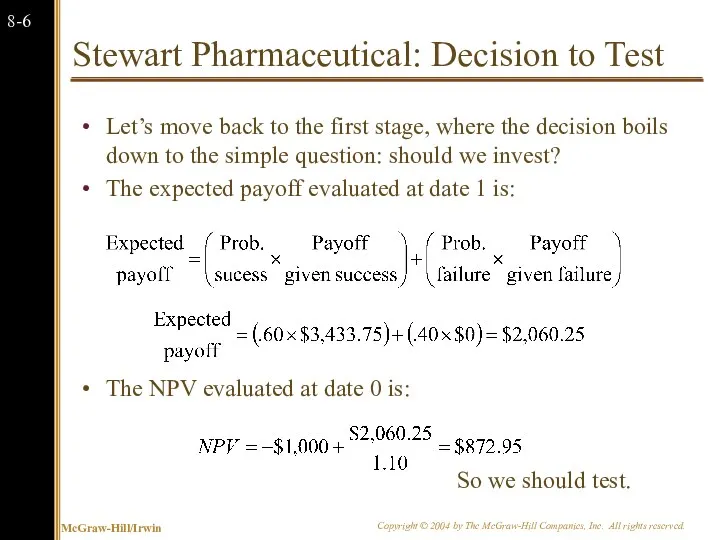

Stewart Pharmaceutical: Decision to Test

Let’s move back to the first stage,

Stewart Pharmaceutical: Decision to Test

Let’s move back to the first stage,

8.4 Options

One of the fundamental insights of modern finance theory is

8.4 Options

One of the fundamental insights of modern finance theory is

Options

The Option to Expand

Has value if demand turns out to be

Options

The Option to Expand

Has value if demand turns out to be

The Option to Expand

Imagine a start-up firm, Campusteria, Inc. which plans

The Option to Expand

Imagine a start-up firm, Campusteria, Inc. which plans

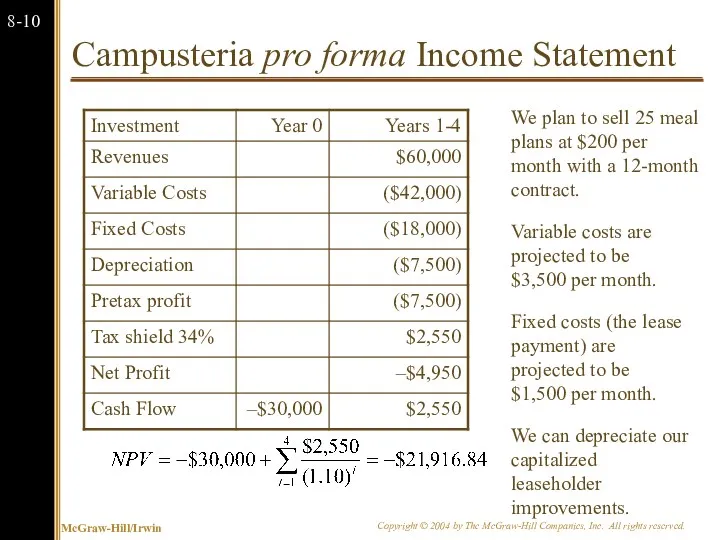

Campusteria pro forma Income Statement

We plan to sell 25 meal plans

Campusteria pro forma Income Statement

We plan to sell 25 meal plans

The Option to Expand: Valuing a Start-Up

Note that while the Campusteria

The Option to Expand: Valuing a Start-Up

Note that while the Campusteria

Discounted Cash Flows and Options

We can calculate the market value of

Discounted Cash Flows and Options

We can calculate the market value of

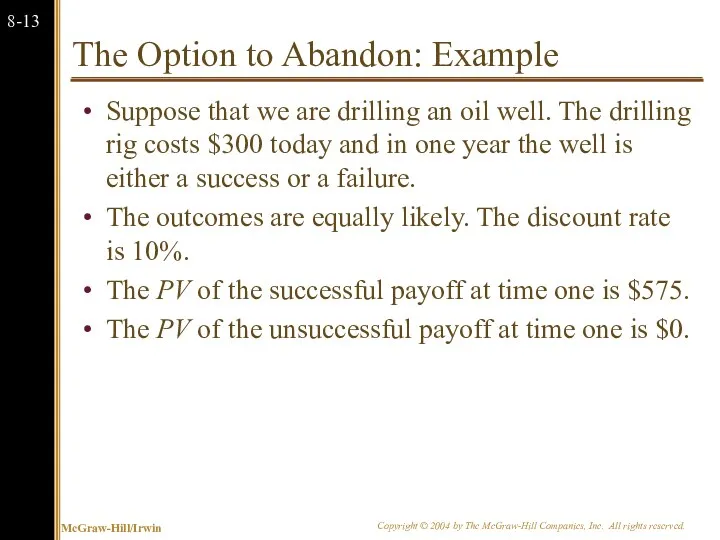

The Option to Abandon: Example

Suppose that we are drilling an oil

The Option to Abandon: Example

Suppose that we are drilling an oil

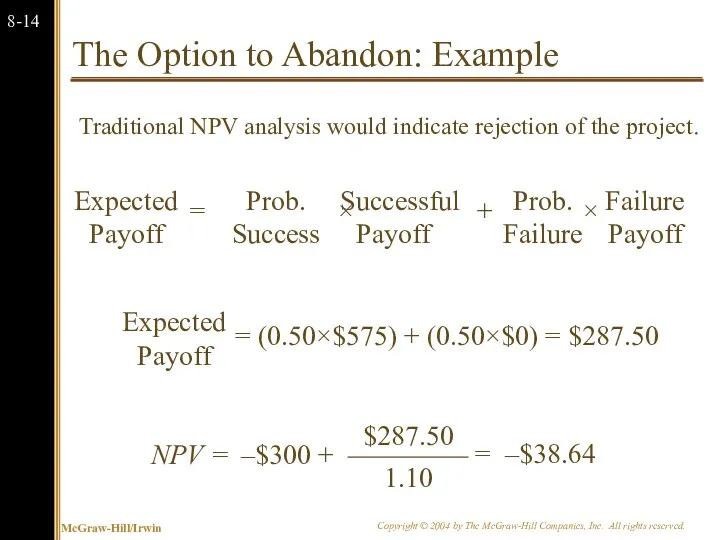

The Option to Abandon: Example

Traditional NPV analysis would indicate rejection

The Option to Abandon: Example

Traditional NPV analysis would indicate rejection

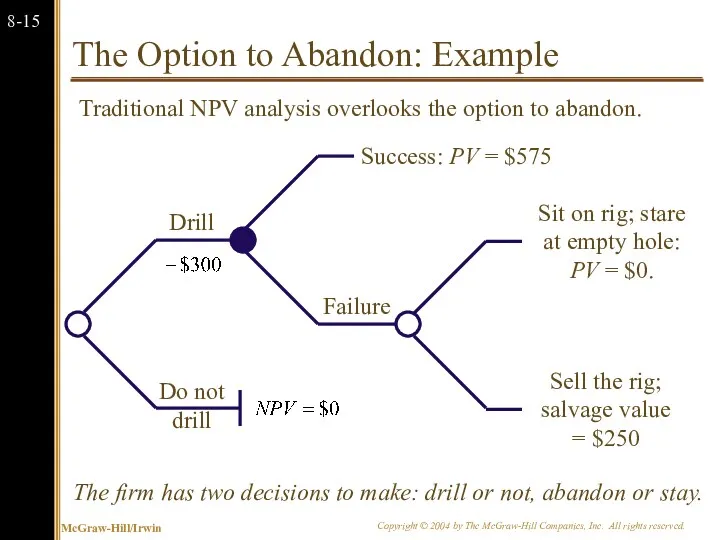

The Option to Abandon: Example

The firm has two decisions to make:

The Option to Abandon: Example

The firm has two decisions to make:

The Option to Abandon: Example

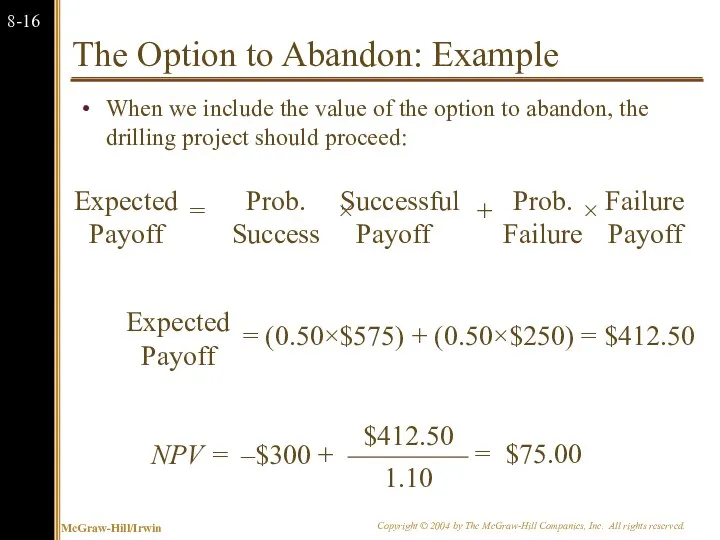

When we include the value of

The Option to Abandon: Example

When we include the value of

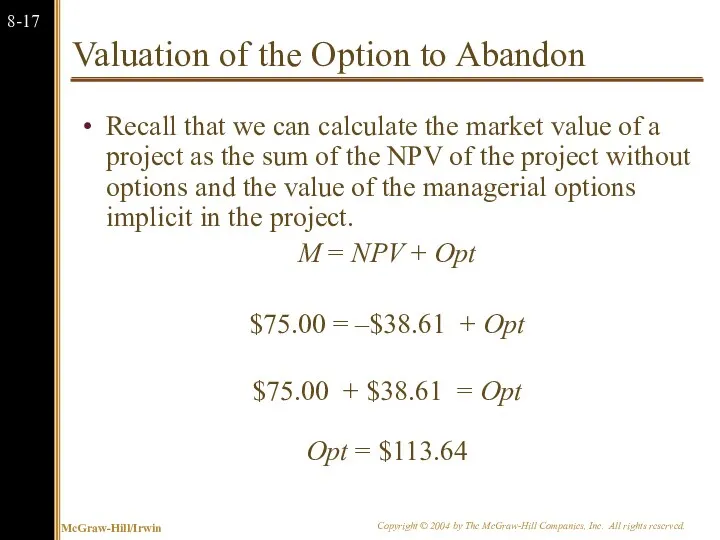

Valuation of the Option to Abandon

Recall that we can calculate the

Valuation of the Option to Abandon

Recall that we can calculate the

Комплексная характеристика предприятия Gloria Jeans

Комплексная характеристика предприятия Gloria Jeans Сбербанк России

Сбербанк России Тарифные планы Билайн

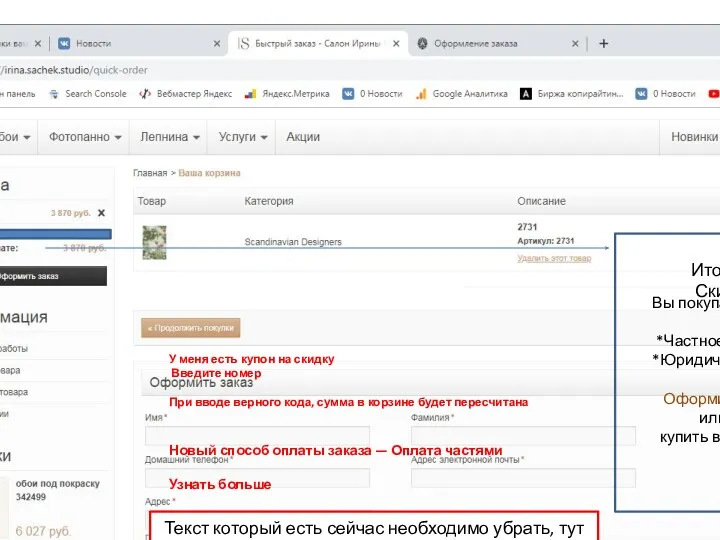

Тарифные планы Билайн Polotno. Простой подход к созданию совершенных свадеб

Polotno. Простой подход к созданию совершенных свадеб Товародвижение и сбыт в маркетинге

Товародвижение и сбыт в маркетинге Продвижение в социальных сетях. Приложение Instagram

Продвижение в социальных сетях. Приложение Instagram P3 Business Analysis

P3 Business Analysis Компания Faberon

Компания Faberon Ошибки при подборе запросов для сайта

Ошибки при подборе запросов для сайта Агентство DDB

Агентство DDB Поставка. Актуальные вопросы заключения, исполнения и расторжения

Поставка. Актуальные вопросы заключения, исполнения и расторжения Использование Интернета в маркетинге

Использование Интернета в маркетинге Правила оформления продажи товара

Правила оформления продажи товара Продажи для менеджера

Продажи для менеджера Передова мережа станцій оренди павербанків

Передова мережа станцій оренди павербанків Производитель кофе Agazzi

Производитель кофе Agazzi USDA Agricultural Marketing Service National Organic Program An Overview

USDA Agricultural Marketing Service National Organic Program An Overview Интернет-магазин одежды

Интернет-магазин одежды Tutorial to advertise Money Leads apps on Adwords

Tutorial to advertise Money Leads apps on Adwords Группа компаний Упаковкин. Упаковочные пленки и емкости из полимеров, одноразовая посуда и расходные материалы

Группа компаний Упаковкин. Упаковочные пленки и емкости из полимеров, одноразовая посуда и расходные материалы Нестандартные упаковочные решения ООО Зеленая территория

Нестандартные упаковочные решения ООО Зеленая территория Риэлтор в социальных сетях

Риэлтор в социальных сетях Омега-3. Онлайн мастер-класс

Омега-3. Онлайн мастер-класс Анализ рыночной ситуации

Анализ рыночной ситуации Гайды для креативов

Гайды для креативов Рекламное агентство Соль

Рекламное агентство Соль Пиар-технологии во внешней политике государства

Пиар-технологии во внешней политике государства Индивидуальный проект. СПА салон

Индивидуальный проект. СПА салон