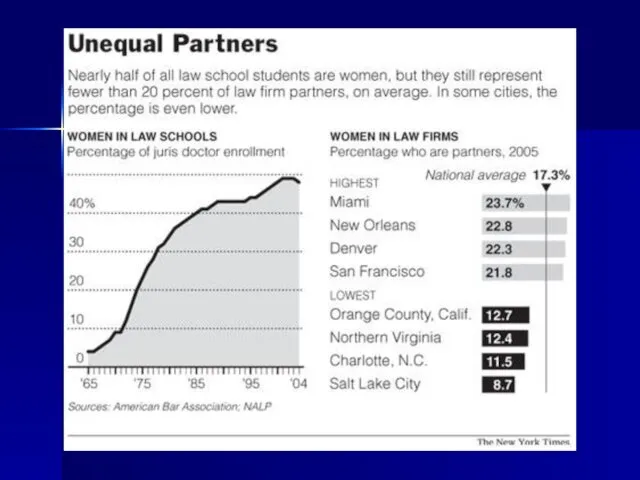

- Public health. Medicare and medicaid. Law and poverty

Содержание

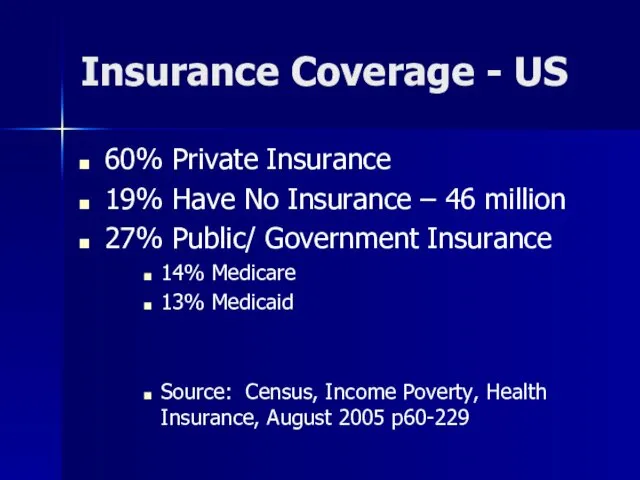

- 3. Insurance Coverage - US 60% Private Insurance 19% Have No Insurance – 46 million 27% Public/

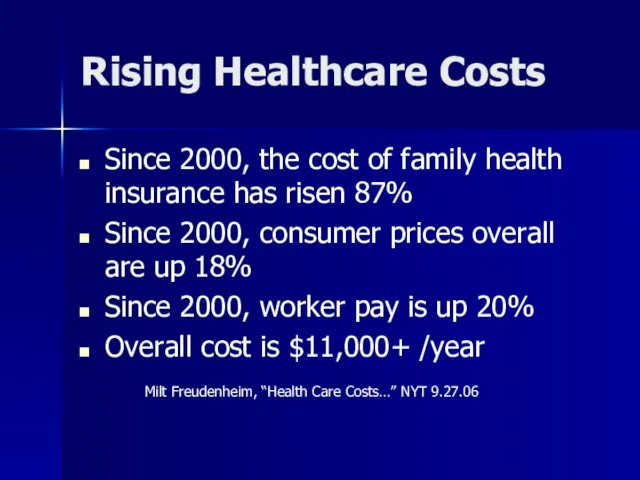

- 4. Rising Healthcare Costs Since 2000, the cost of family health insurance has risen 87% Since 2000,

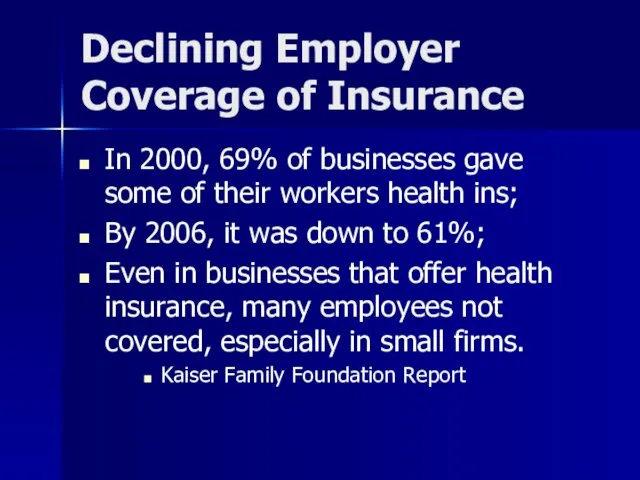

- 5. Declining Employer Coverage of Insurance In 2000, 69% of businesses gave some of their workers health

- 6. Medicare What is it? What kind of law is it? How is a person eligible? What

- 7. What is Medicare? Federal Law Medicare is a nationwide federal health insurance program for the aged

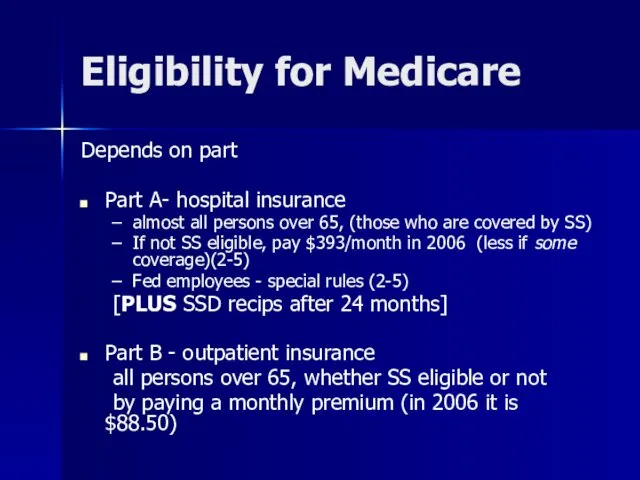

- 8. Eligibility for Medicare Depends on part Part A- hospital insurance almost all persons over 65, (those

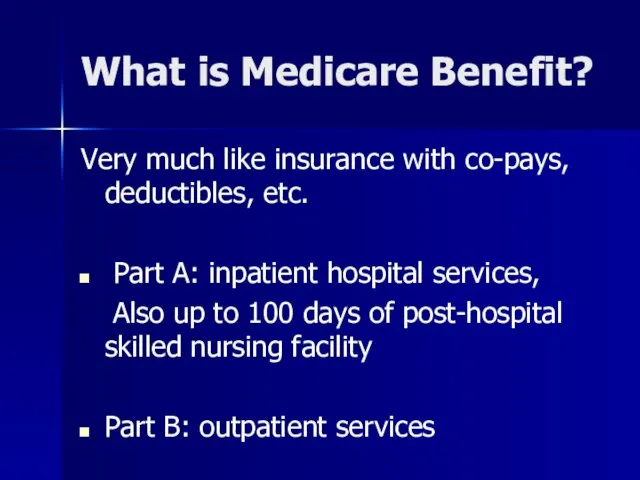

- 10. What is Medicare Benefit? Very much like insurance with co-pays, deductibles, etc. Part A: inpatient hospital

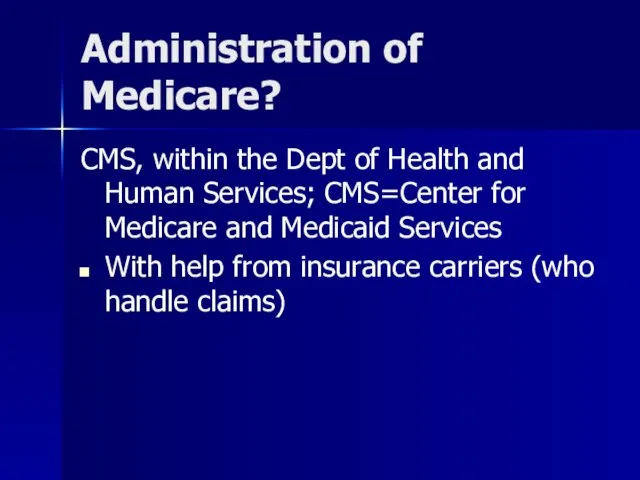

- 11. Administration of Medicare? CMS, within the Dept of Health and Human Services; CMS=Center for Medicare and

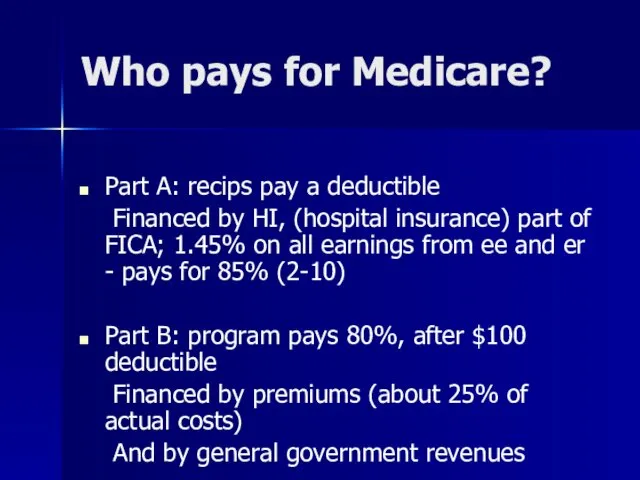

- 12. Who pays for Medicare? Part A: recips pay a deductible Financed by HI, (hospital insurance) part

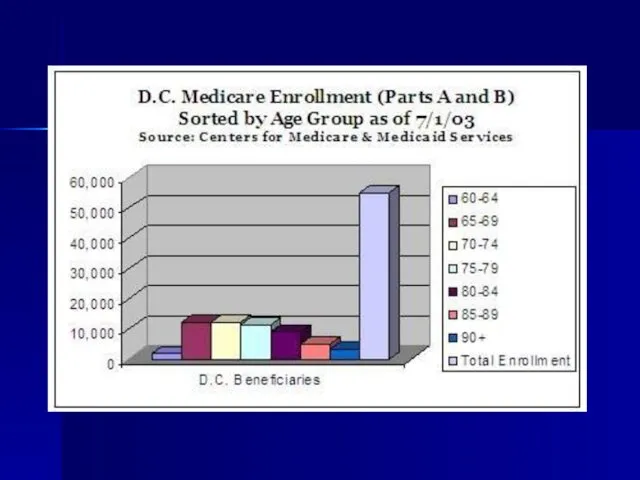

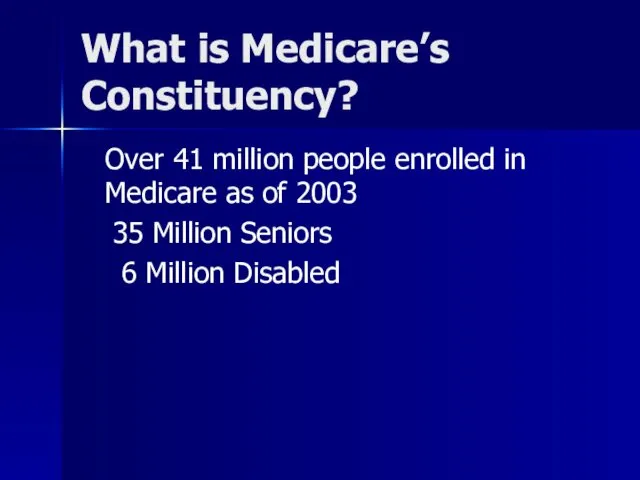

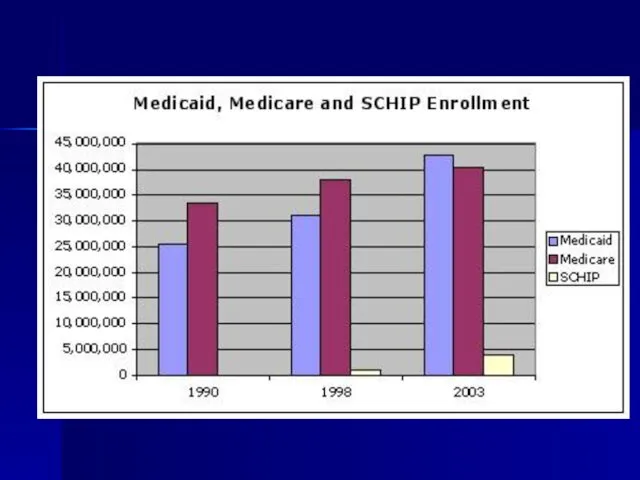

- 13. What is Medicare’s Constituency? Over 41 million people enrolled in Medicare as of 2003 35 Million

- 14. Medicare Coverage

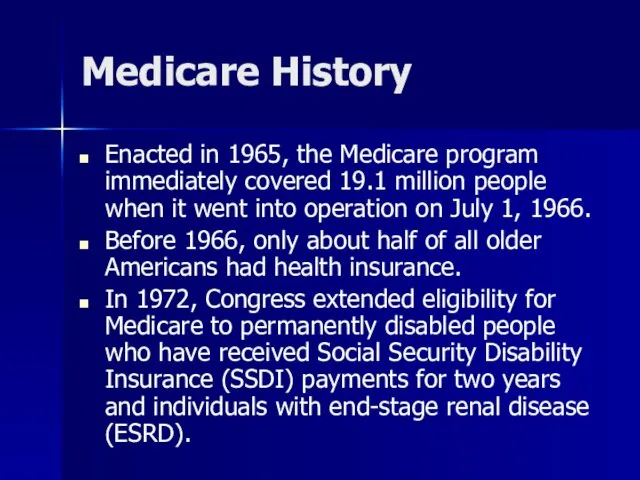

- 15. Medicare History Enacted in 1965, the Medicare program immediately covered 19.1 million people when it went

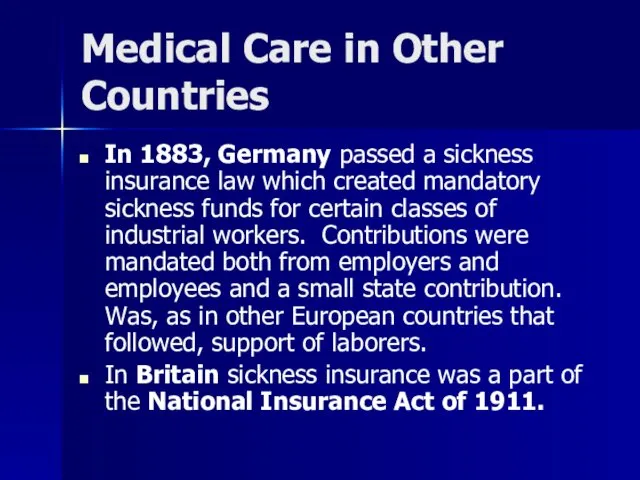

- 16. Medical Care in Other Countries In 1883, Germany passed a sickness insurance law which created mandatory

- 17. Who are collateral beneficiaries?

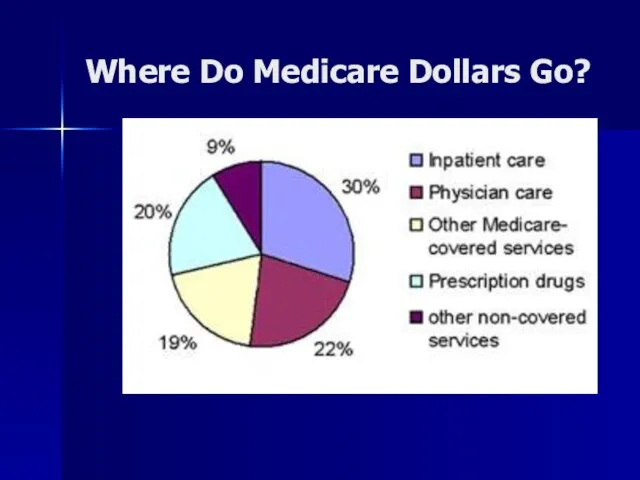

- 18. : Where Do Medicare Dollars Go?

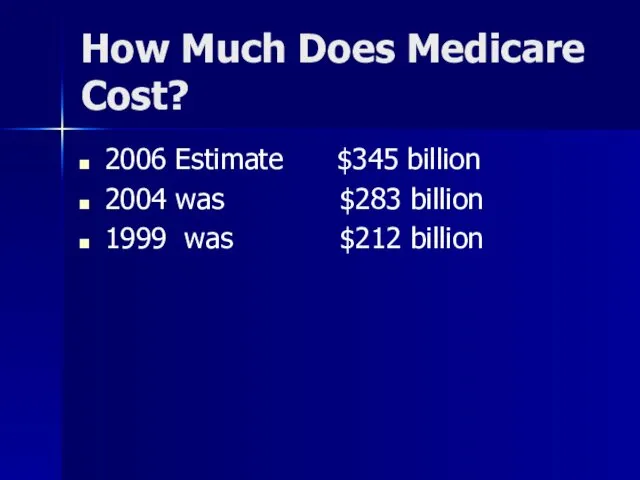

- 19. How Much Does Medicare Cost? 2006 Estimate $345 billion 2004 was $283 billion 1999 was $212

- 21. New Medicare Benefit Prescription Drug Coverage

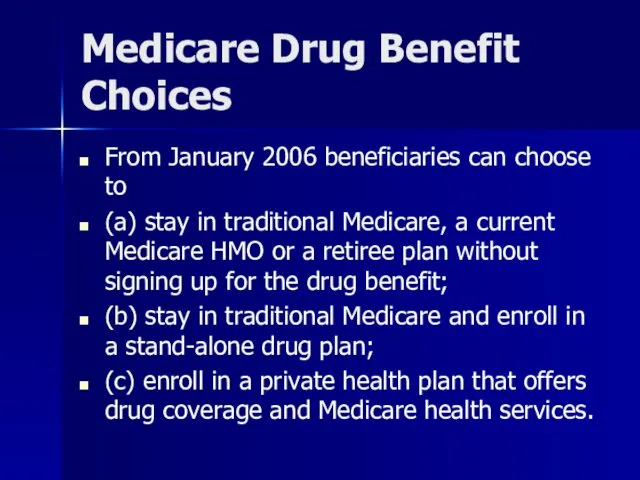

- 22. Medicare Drug Benefit Choices From January 2006 beneficiaries can choose to (a) stay in traditional Medicare,

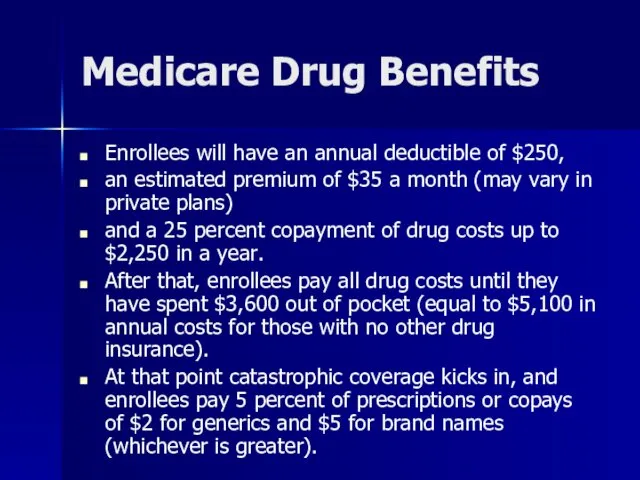

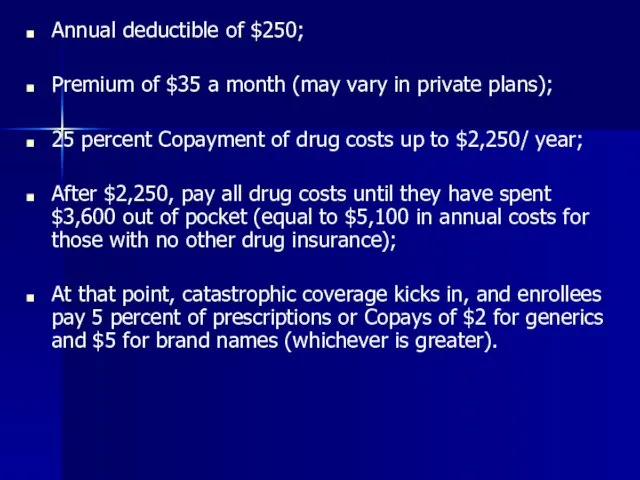

- 23. Medicare Drug Benefits Enrollees will have an annual deductible of $250, an estimated premium of $35

- 25. Annual deductible of $250; Premium of $35 a month (may vary in private plans); 25 percent

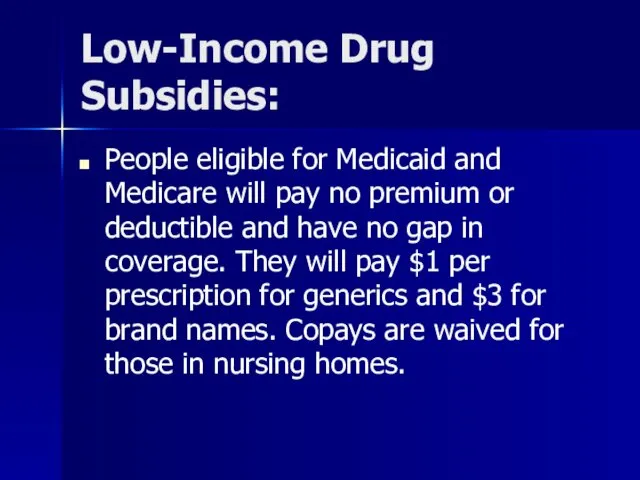

- 26. Low-Income Drug Subsidies: People eligible for Medicaid and Medicare will pay no premium or deductible and

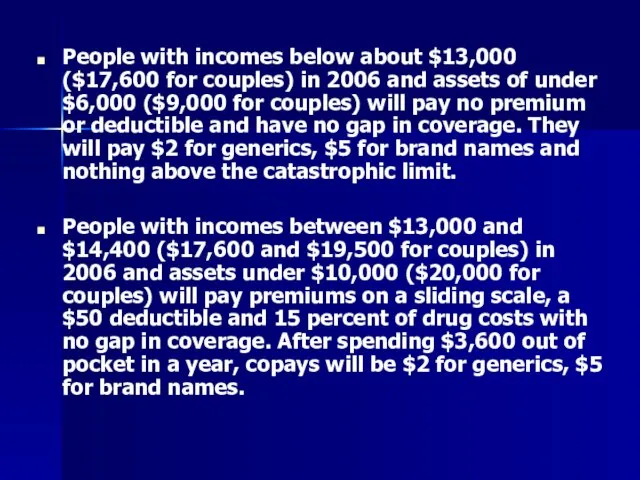

- 27. People with incomes below about $13,000 ($17,600 for couples) in 2006 and assets of under $6,000

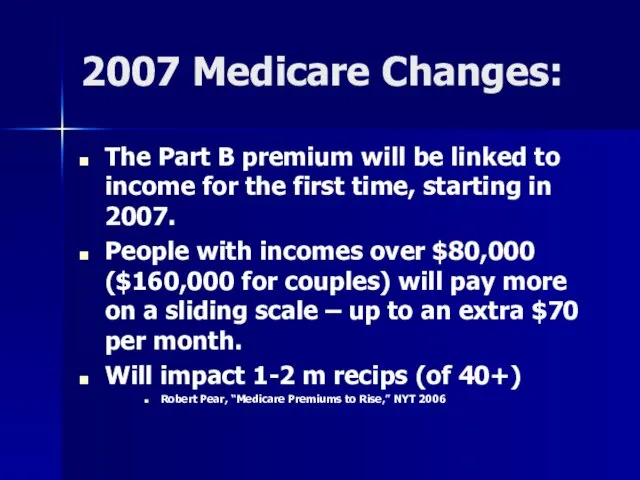

- 29. 2007 Medicare Changes: The Part B premium will be linked to income for the first time,

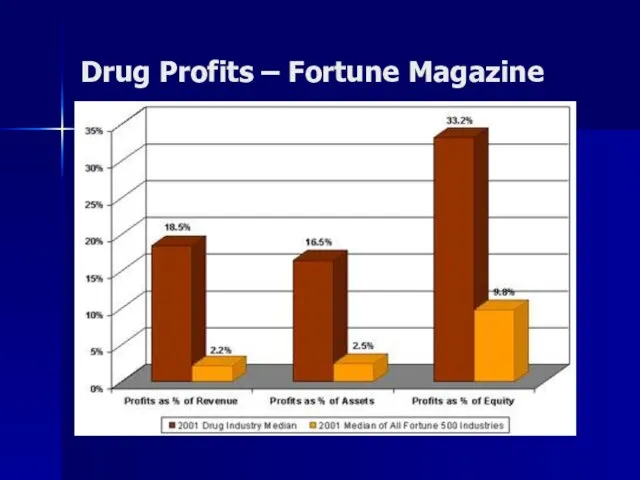

- 30. Drug Profits – Fortune Magazine

- 31. Medicaid What is it? What kind of law is it? How is a person eligible? What

- 32. Medicaid A federal-state program providing medical assistance to low-income persons who are aged, blind, disabled, members

- 33. Medicaid Law Joint Federal and State Law

- 34. Eligibility for Medicaid FINANCIAL REQUIREMENTS: First must be indigent Income and Resources

- 35. Eligibility Medicaid: Mandatory Families Aid to Families with Dependent Children (AFDC); Supplemental Security Income (SSI) recipients;

- 36. What benefit is conferred? MUST OFFER: inpatient outpatient nursing home care MAY OFFER: eyeglasses prescription drugs

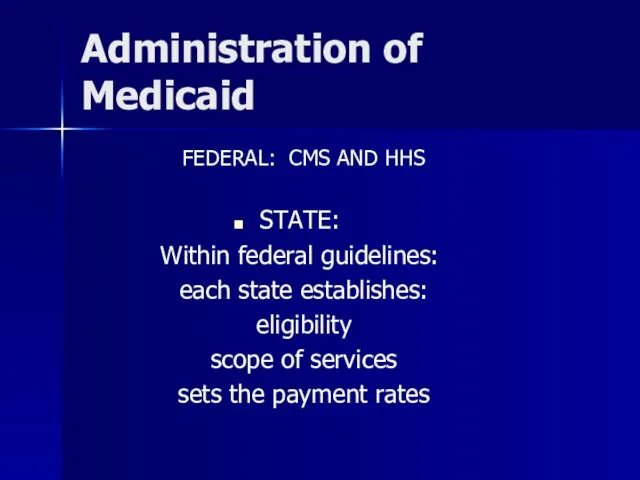

- 37. Administration of Medicaid FEDERAL: CMS AND HHS STATE: Within federal guidelines: each state establishes: eligibility scope

- 38. Medicaid varies considerably among states

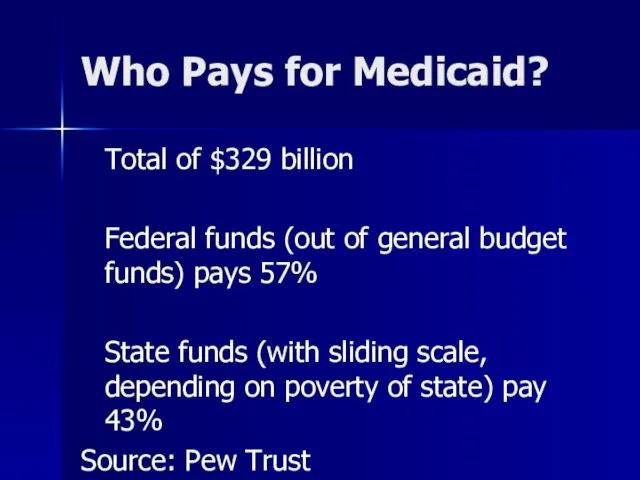

- 39. Who Pays for Medicaid? Total of $329 billion Federal funds (out of general budget funds) pays

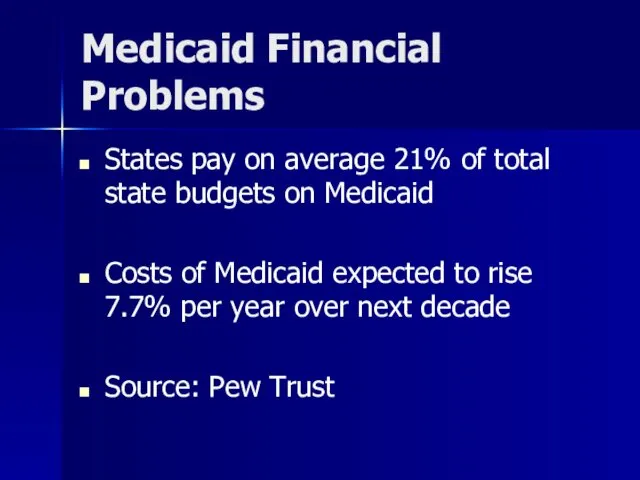

- 40. Medicaid Financial Problems States pay on average 21% of total state budgets on Medicaid Costs of

- 42. Medicaid Constituency 58 million people receive Medicaid – Some receive both Medicare and Medicaid

- 43. Elderly and Medicaid

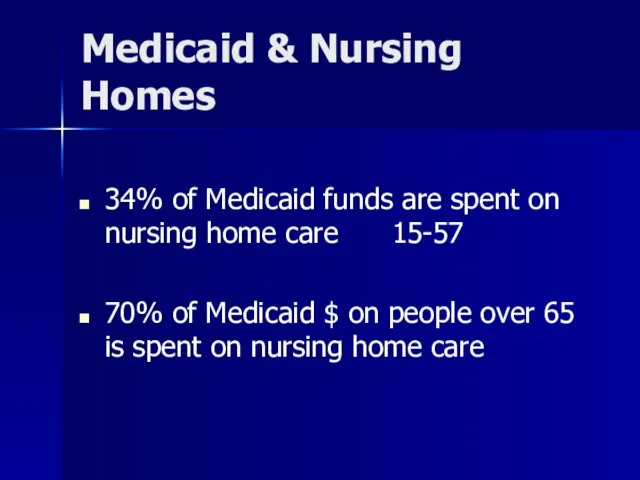

- 44. Medicaid & Nursing Homes 34% of Medicaid funds are spent on nursing home care 15-57 70%

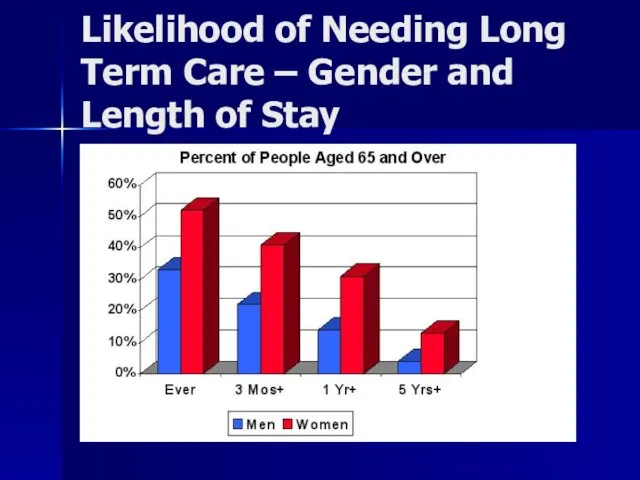

- 45. Likelihood of Needing Long Term Care – Gender and Length of Stay

- 46. Long Term Nursing Care by Age

- 47. Likelihood of Nursing Home The U.S. General Accounting Office reported in 2000 that nearly 40% of

- 48. Medicaid Financial Planning? Medicaid Planning, or the act of shifting assets out of a Medicaid recipient's

- 49. How Poor to Qualify for Medicaid? The government will not pay for nursing home care for

- 50. Policy Issues? Policy Decision to Protect the Assets of Wealthy Seniors? but not the others? Contrast

- 52. Policy Issues Recall History of Law and Poverty, FAMILY RESPONSIBILITY: 3 generation responsibility Tension between: Do

- 53. CHIP CHIP: Children’s Health Insurance Program Structure much like Medicaid Federal / State Partnership States have

- 54. Uninsured in US 46 Million People

- 55. What About Uninsured? Twenty-five percent of all working class families in LA have no health insurance

- 56. Consequences of Lack of Health Insurance (part one) ¨ Uninsured Americans get about half the medical

- 57. Consequences (cont) ¨ Only half of uninsured children visited a physician during 2001, compared with three-quarters

- 58. Consequences (cont) ¨ Tax dollars paid for an estimated 85 percent of the roughly $35 billion

- 59. What Happens When Some of the 46 Million Uninsured Get Sick?

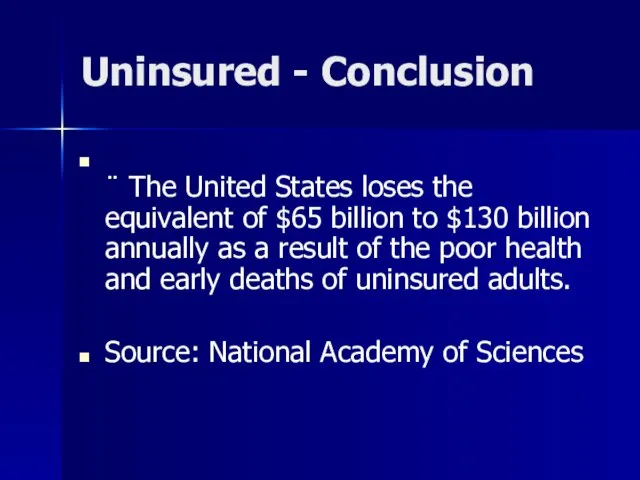

- 60. Uninsured - Conclusion ¨ The United States loses the equivalent of $65 billion to $130 billion

- 62. What Happens When Some of the 46 million Uninsured Get REALLY Sick?

- 64. EMTALA Emergency Medical Treatment and Active Labor Act Anti-Dumping Law, 42 usc 1395dd

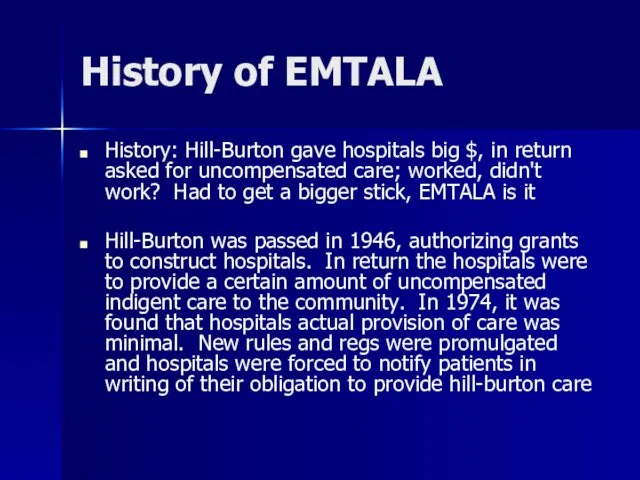

- 66. History of EMTALA History: Hill-Burton gave hospitals big $, in return asked for uncompensated care; worked,

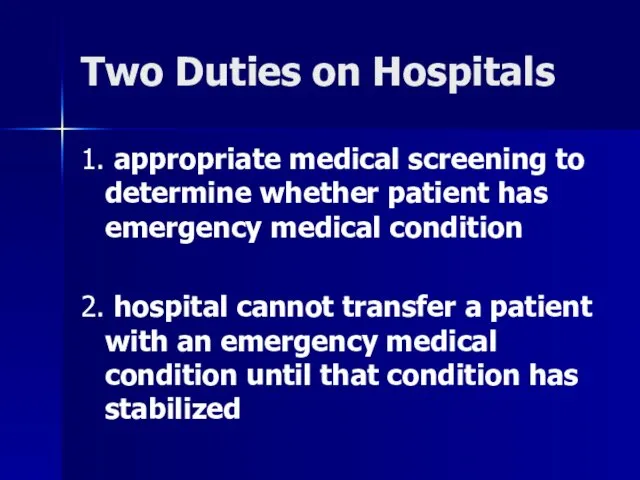

- 67. Two Duties on Hospitals 1. appropriate medical screening to determine whether patient has emergency medical condition

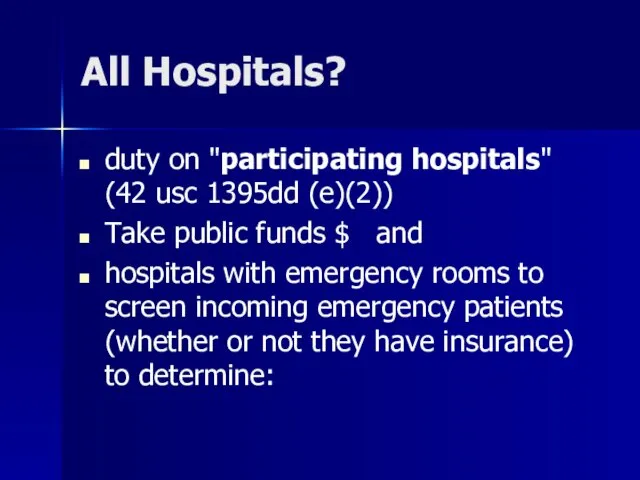

- 68. All Hospitals? duty on "participating hospitals" (42 usc 1395dd (e)(2)) Take public funds $ and hospitals

- 69. What Emergency Conditions Must Hospital Treat? Q: whether they have an emergency medical condition? i. health

- 70. If Emergency Condition If so, must stabilize prior to transfer or discharge transfer is allowed if

- 71. Remedies for EMTALA Violations? if violated, civil penalties, atty fees, personal injuries action, but most importantly

- 72. Actual Logo of Personal Injury Firm of Friedman, Domiano and Smith, Cleveland, Ohio

- 73. Who pays for the uninsured do for healthcare? Who pays for the cost of uncompensated care?

- 74. National Academy of Sciences says: ¨ Tax dollars paid for an estimated 85 percent of the

- 75. We Do Have A National Healthcare System: * Private insurance (premiums subject to market) – citizens

- 76. Public Policy Considerations? Is This The Best System? Is This The Least Expensive System? Does This

- 77. US Healthcare System To be continued….

- 79. Скачать презентацию

Insurance Coverage - US

60% Private Insurance

19% Have No Insurance –

Insurance Coverage - US

60% Private Insurance

19% Have No Insurance –

Rising Healthcare Costs

Since 2000, the cost of family health insurance has

Rising Healthcare Costs

Since 2000, the cost of family health insurance has

Declining Employer Coverage of Insurance

In 2000, 69% of businesses gave some

Declining Employer Coverage of Insurance

In 2000, 69% of businesses gave some

Medicare

What is it?

What kind of law is it?

How is a person

Medicare

What is it?

What kind of law is it?

How is a person

What is Medicare?

Federal Law

Medicare is a nationwide federal health insurance program

What is Medicare?

Federal Law

Medicare is a nationwide federal health insurance program

Eligibility for Medicare

Depends on part

Part A- hospital insurance

almost all persons over

Eligibility for Medicare

Depends on part

Part A- hospital insurance

almost all persons over

What is Medicare Benefit?

Very much like insurance with co-pays, deductibles, etc.

What is Medicare Benefit?

Very much like insurance with co-pays, deductibles, etc.

Administration of Medicare?

CMS, within the Dept of Health and Human Services;

Administration of Medicare?

CMS, within the Dept of Health and Human Services;

Who pays for Medicare?

Part A: recips pay a deductible

Financed by HI,

Who pays for Medicare?

Part A: recips pay a deductible

Financed by HI,

What is Medicare’s Constituency?

Over 41 million people enrolled in Medicare as

What is Medicare’s Constituency?

Over 41 million people enrolled in Medicare as

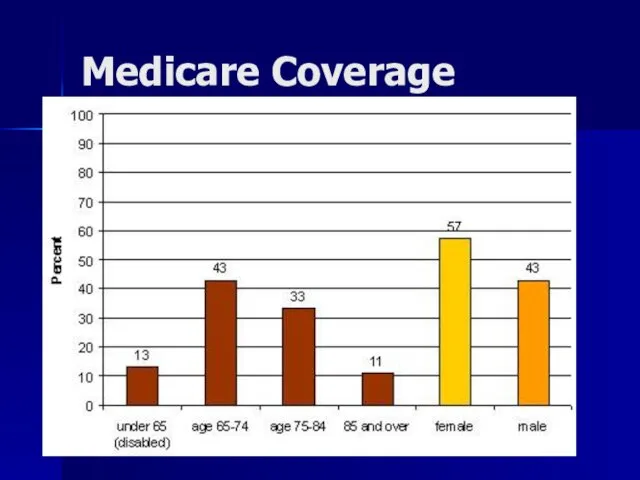

Medicare Coverage

Medicare Coverage

Medicare History

Enacted in 1965, the Medicare program immediately covered 19.1 million

Medicare History

Enacted in 1965, the Medicare program immediately covered 19.1 million

Medical Care in Other Countries

In 1883, Germany passed a sickness insurance

Medical Care in Other Countries

In 1883, Germany passed a sickness insurance

Who are collateral beneficiaries?

Who are collateral beneficiaries?

:

Where Do Medicare Dollars Go?

:

Where Do Medicare Dollars Go?

How Much Does Medicare Cost?

2006 Estimate $345 billion

2004 was $283 billion

1999

How Much Does Medicare Cost?

2006 Estimate $345 billion

2004 was $283 billion

1999

New Medicare Benefit

Prescription Drug Coverage

New Medicare Benefit

Prescription Drug Coverage

Medicare Drug Benefit Choices

From January 2006 beneficiaries can choose to

(a)

Medicare Drug Benefit Choices

From January 2006 beneficiaries can choose to

(a)

Medicare Drug Benefits

Enrollees will have an annual deductible of $250,

an

Medicare Drug Benefits

Enrollees will have an annual deductible of $250,

an

Annual deductible of $250;

Premium of $35 a month (may vary in

Annual deductible of $250;

Premium of $35 a month (may vary in

Low-Income Drug Subsidies:

People eligible for Medicaid and Medicare will pay no

Low-Income Drug Subsidies:

People eligible for Medicaid and Medicare will pay no

People with incomes below about $13,000 ($17,600 for couples) in 2006

People with incomes below about $13,000 ($17,600 for couples) in 2006

2007 Medicare Changes:

The Part B premium will be linked to

2007 Medicare Changes:

The Part B premium will be linked to

Drug Profits – Fortune Magazine

Drug Profits – Fortune Magazine

Medicaid

What is it?

What kind of law is it?

How is a person

Medicaid

What is it?

What kind of law is it?

How is a person

Medicaid

A federal-state program providing medical assistance to low-income persons who are

Medicaid

A federal-state program providing medical assistance to low-income persons who are

Medicaid Law

Joint Federal and State Law

Medicaid Law

Joint Federal and State Law

Eligibility for Medicaid

FINANCIAL REQUIREMENTS:

First must be indigent

Income and

Resources

Eligibility for Medicaid

FINANCIAL REQUIREMENTS:

First must be indigent

Income and

Resources

Eligibility Medicaid: Mandatory

Families Aid to Families with Dependent Children (AFDC);

Supplemental

Eligibility Medicaid: Mandatory

Families Aid to Families with Dependent Children (AFDC);

Supplemental

What benefit is conferred?

MUST OFFER:

inpatient

outpatient

nursing home care

MAY OFFER:

eyeglasses

prescription drugs

What benefit is conferred?

MUST OFFER:

inpatient

outpatient

nursing home care

MAY OFFER:

eyeglasses

prescription drugs

Administration of Medicaid

FEDERAL: CMS AND HHS

STATE:

Within federal guidelines:

each state establishes:

eligibility

scope of

Administration of Medicaid

FEDERAL: CMS AND HHS

STATE:

Within federal guidelines:

each state establishes:

eligibility

scope of

Medicaid varies considerably among states

Medicaid varies considerably among states

Who Pays for Medicaid?

Total of $329 billion

Federal funds (out of general

Who Pays for Medicaid?

Total of $329 billion

Federal funds (out of general

Medicaid Financial Problems

States pay on average 21% of total state budgets

Medicaid Financial Problems

States pay on average 21% of total state budgets

Medicaid Constituency

58 million people receive Medicaid –

Some receive both Medicare

Medicaid Constituency

58 million people receive Medicaid –

Some receive both Medicare

Elderly and Medicaid

Elderly and Medicaid

Medicaid & Nursing Homes

34% of Medicaid funds are spent on nursing

Medicaid & Nursing Homes

34% of Medicaid funds are spent on nursing

Likelihood of Needing Long Term Care – Gender and Length of

Likelihood of Needing Long Term Care – Gender and Length of

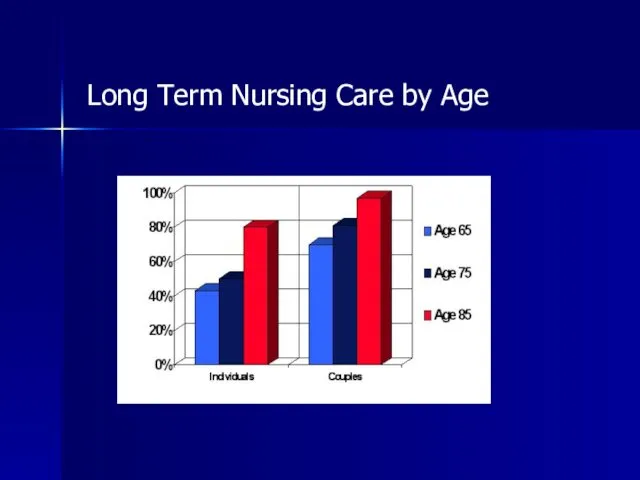

Long Term Nursing Care by Age

Long Term Nursing Care by Age

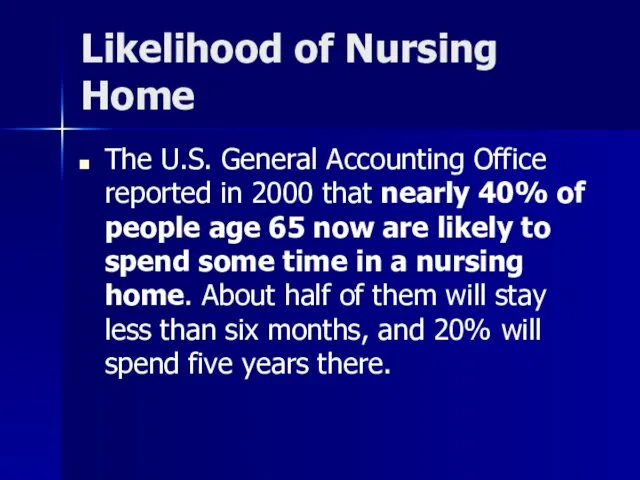

Likelihood of Nursing Home

The U.S. General Accounting Office reported in

Likelihood of Nursing Home

The U.S. General Accounting Office reported in

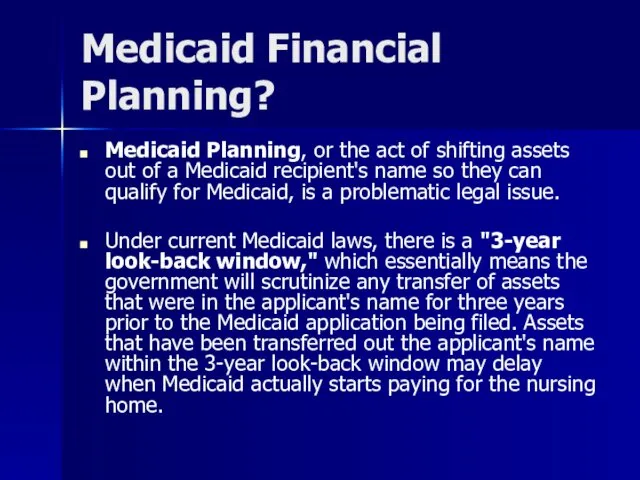

Medicaid Financial Planning?

Medicaid Planning, or the act of shifting assets out

Medicaid Financial Planning?

Medicaid Planning, or the act of shifting assets out

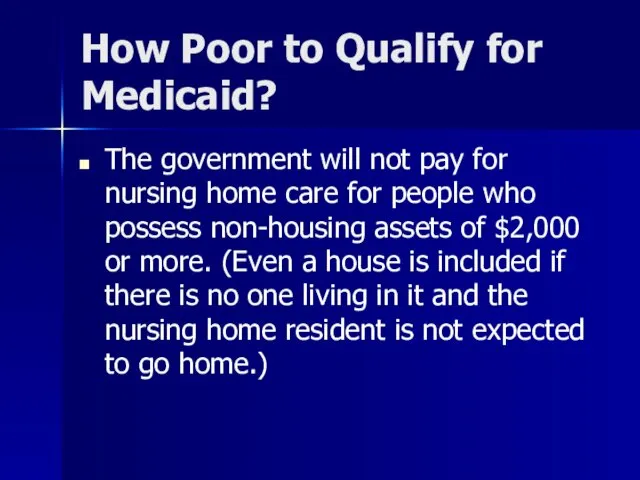

How Poor to Qualify for Medicaid?

The government will not pay for

How Poor to Qualify for Medicaid?

The government will not pay for

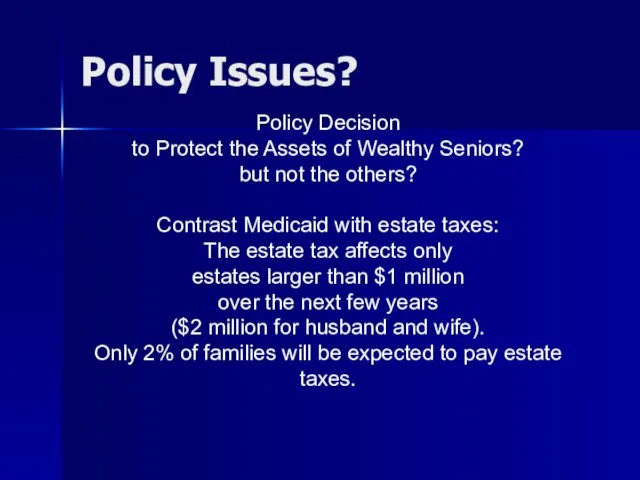

Policy Issues?

Policy Decision

to Protect the Assets of Wealthy Seniors?

but not

Policy Issues?

Policy Decision

to Protect the Assets of Wealthy Seniors?

but not

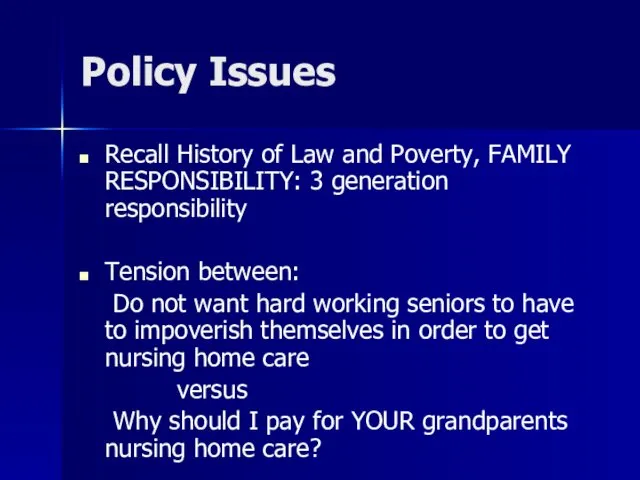

Policy Issues

Recall History of Law and Poverty, FAMILY RESPONSIBILITY: 3 generation

Policy Issues

Recall History of Law and Poverty, FAMILY RESPONSIBILITY: 3 generation

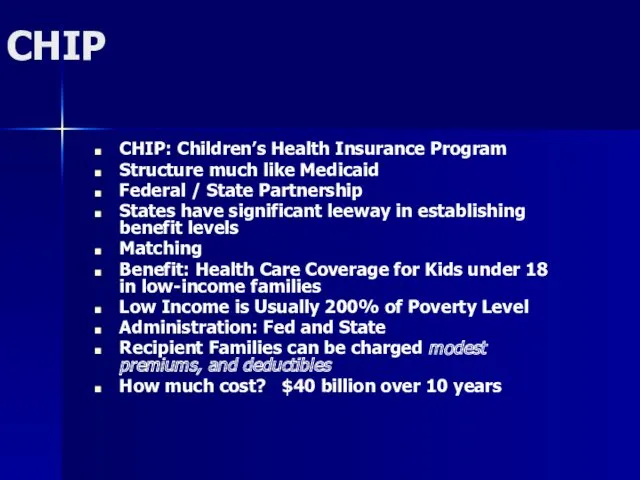

CHIP

CHIP: Children’s Health Insurance Program

Structure much like Medicaid

Federal / State Partnership

States

CHIP

CHIP: Children’s Health Insurance Program

Structure much like Medicaid

Federal / State Partnership

States

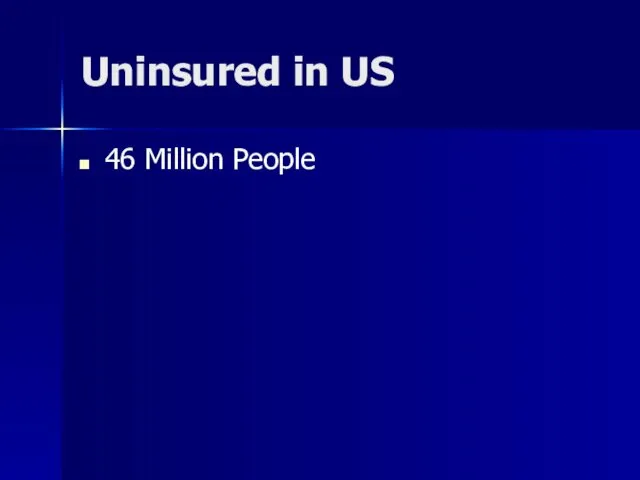

Uninsured in US

46 Million People

Uninsured in US

46 Million People

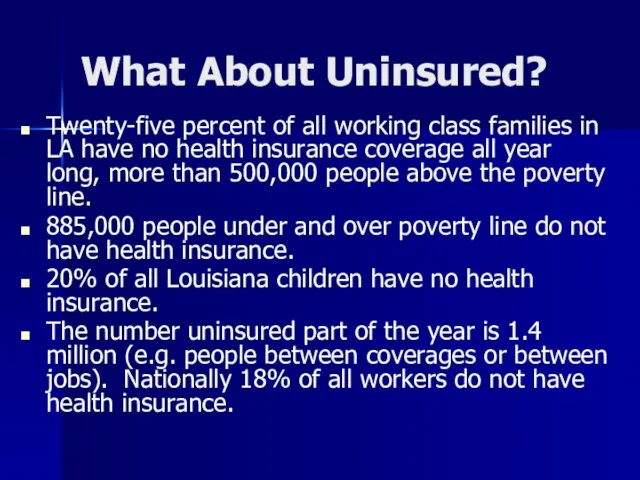

What About Uninsured?

Twenty-five percent of all working class families in LA

What About Uninsured?

Twenty-five percent of all working class families in LA

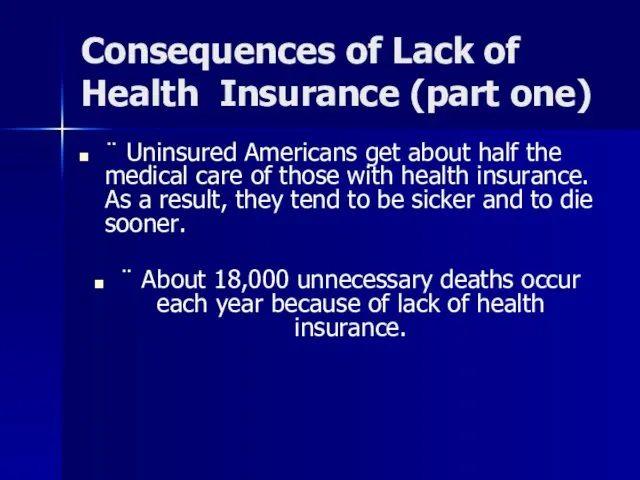

Consequences of Lack of Health Insurance (part one)

¨ Uninsured Americans

Consequences of Lack of Health Insurance (part one)

¨ Uninsured Americans

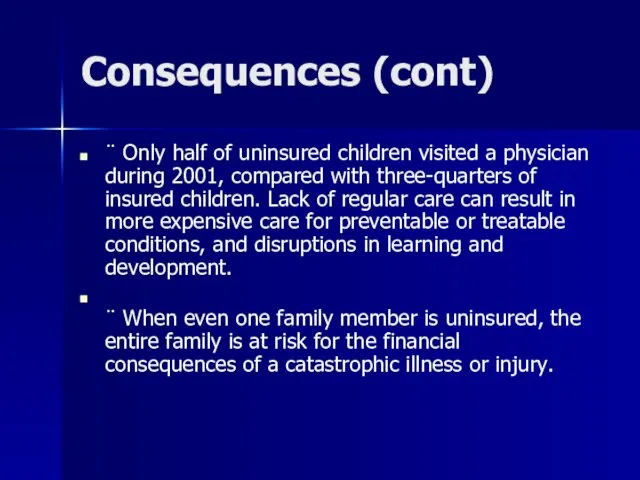

Consequences (cont)

¨ Only half of uninsured children visited a physician during

Consequences (cont)

¨ Only half of uninsured children visited a physician during

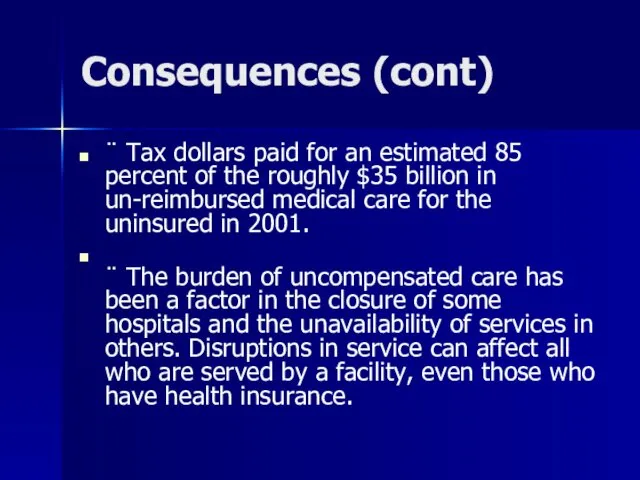

Consequences (cont)

¨ Tax dollars paid for an estimated 85 percent of

Consequences (cont)

¨ Tax dollars paid for an estimated 85 percent of

What Happens When Some of the 46 Million Uninsured Get Sick?

What Happens When Some of the 46 Million Uninsured Get Sick?

Uninsured - Conclusion

¨ The United States loses the equivalent of $65

Uninsured - Conclusion

¨ The United States loses the equivalent of $65

What Happens When Some of the 46 million Uninsured Get REALLY

What Happens When Some of the 46 million Uninsured Get REALLY

EMTALA

Emergency Medical Treatment and Active Labor Act

Anti-Dumping Law, 42 usc

EMTALA

Emergency Medical Treatment and Active Labor Act

Anti-Dumping Law, 42 usc

History of EMTALA

History: Hill-Burton gave hospitals big $, in return asked

History of EMTALA

History: Hill-Burton gave hospitals big $, in return asked

Two Duties on Hospitals

1. appropriate medical screening to determine whether patient

Two Duties on Hospitals

1. appropriate medical screening to determine whether patient

All Hospitals?

duty on "participating hospitals" (42 usc 1395dd (e)(2))

Take public funds

All Hospitals?

duty on "participating hospitals" (42 usc 1395dd (e)(2))

Take public funds

What Emergency Conditions Must Hospital Treat?

Q: whether they have an emergency

What Emergency Conditions Must Hospital Treat?

Q: whether they have an emergency

If Emergency Condition

If so, must stabilize prior to transfer or discharge

transfer

If Emergency Condition

If so, must stabilize prior to transfer or discharge

transfer

Remedies for EMTALA Violations?

if violated, civil penalties, atty fees, personal injuries

Remedies for EMTALA Violations?

if violated, civil penalties, atty fees, personal injuries

Actual Logo of Personal Injury Firm of

Friedman, Domiano and Smith,

Actual Logo of Personal Injury Firm of Friedman, Domiano and Smith,

Who pays for the uninsured do for healthcare?

Who pays for the

Who pays for the uninsured do for healthcare?

Who pays for the

National Academy

of Sciences says:

¨ Tax dollars paid for an estimated

National Academy

of Sciences says:

¨ Tax dollars paid for an estimated

We Do Have A National Healthcare System:

* Private insurance (premiums subject

We Do Have A National Healthcare System:

* Private insurance (premiums subject

Public Policy Considerations?

Is This The Best System?

Is This The Least Expensive

Public Policy Considerations?

Is This The Best System?

Is This The Least Expensive

US Healthcare System

To be continued….

US Healthcare System

To be continued….

Псевдофакичный КМО (Синдром Ирвина-Гасса)

Псевдофакичный КМО (Синдром Ирвина-Гасса) Психология детей с расстройствами эмоционально-волевой сферы и поведения

Психология детей с расстройствами эмоционально-волевой сферы и поведения Хронический пылевой бронхит

Хронический пылевой бронхит Всё, что вы хотели знать про это. Репродуктивное здоровье подростка

Всё, что вы хотели знать про это. Репродуктивное здоровье подростка Ветеринарно-санитарная экспертиза рыб и рыбопродуктов, меры борьбы и профилактика при гельминтозных заболеваниях

Ветеринарно-санитарная экспертиза рыб и рыбопродуктов, меры борьбы и профилактика при гельминтозных заболеваниях Общая фармакология

Общая фармакология Микст-патология у больных хроническим описторхозом. Тактика ведения

Микст-патология у больных хроническим описторхозом. Тактика ведения Эпидемиологическая ситуация заболеваемости корью. Алгоритм расследования побочных эффектов при вакцинации против кори

Эпидемиологическая ситуация заболеваемости корью. Алгоритм расследования побочных эффектов при вакцинации против кори Аномалии размеров, формы и структуры эмали. Этиология. Клиника. Лечение

Аномалии размеров, формы и структуры эмали. Этиология. Клиника. Лечение Двигательная система. АФО двигательного анализатора. Виды нарушение двигательной чувствительности. Методы исследования

Двигательная система. АФО двигательного анализатора. Виды нарушение двигательной чувствительности. Методы исследования Сенсорні області кори. Роль ретикулярної формації. Ноціцепція. Температурна рецепція

Сенсорні області кори. Роль ретикулярної формації. Ноціцепція. Температурна рецепція Эколого-географические особенности и этиологическая структура лептоспироза животных в Среднем Приобье

Эколого-географические особенности и этиологическая структура лептоспироза животных в Среднем Приобье Правильное и здоровое питание ребёнка

Правильное и здоровое питание ребёнка Геморрой. Предрасполагающие факторы

Геморрой. Предрасполагающие факторы Участие медицинской сестры в профилактике инсульта

Участие медицинской сестры в профилактике инсульта Отравления веществами наркотического действия. Клиника, диагностика, лечение

Отравления веществами наркотического действия. Клиника, диагностика, лечение Семиотика и методы диагностики заболеваний, приводящих к формированию пороков сердца. Ревматизм, бактериальный эндокардит

Семиотика и методы диагностики заболеваний, приводящих к формированию пороков сердца. Ревматизм, бактериальный эндокардит Неспецифический язвенный колит

Неспецифический язвенный колит Методы обезболивания. Виды обезболивания. Аппаратура и инструментарий для проведения анестезии

Методы обезболивания. Виды обезболивания. Аппаратура и инструментарий для проведения анестезии Диагностика и лечение синдрома Гудпасчера

Диагностика и лечение синдрома Гудпасчера Внутрибольничные инфекции. Масштаб, проблемы и структура. Инфекционный процесс

Внутрибольничные инфекции. Масштаб, проблемы и структура. Инфекционный процесс Обмен нуклеотидов. Тема 14

Обмен нуклеотидов. Тема 14 Биоритмология (2)

Биоритмология (2) Vitaminele antiinfectioase

Vitaminele antiinfectioase Железодефицитная анемия у детей. Диспансеризация

Железодефицитная анемия у детей. Диспансеризация Адамның жасы мен жынысына байланысты терінің ерекшеліктері

Адамның жасы мен жынысына байланысты терінің ерекшеліктері Методы исследования больных с заболеваниями органов кроветворения

Методы исследования больных с заболеваниями органов кроветворения Реабилитация при эфферентной моторной афазии

Реабилитация при эфферентной моторной афазии