- 00011370_IBMF

Содержание

- 2. South Africa's financial services sector is strong, with numerous of domestic and international institutions offering a

- 3. BANKING SYSTEM National banks have branches across South Africa. Bank branches are generally open from 9am

- 4. CENTRAL BANK South Africa's central bank is the South African Reserve Bank (SARB). The fundamental goal

- 5. According to the SARB's most recent annual report, net investment income climbed by South African R5.8

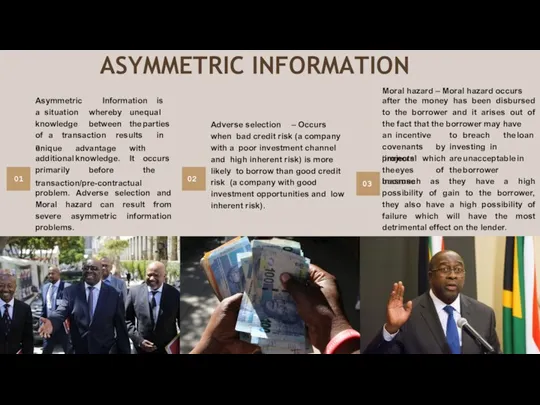

- 6. ASYMMETRIC INFORMATION 01 Asymmetric Information is a situation whereby unequal knowledge between the parties of a

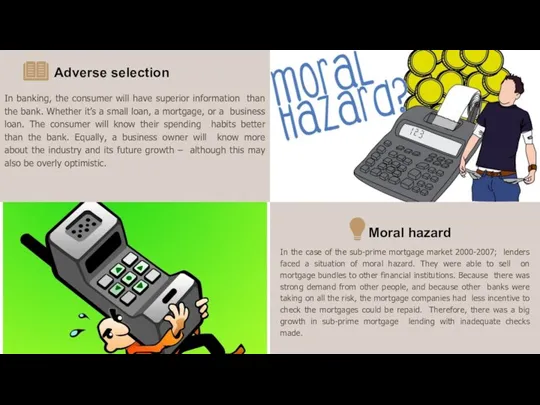

- 7. In banking, the consumer will have superior information than the bank. Whether it’s a small loan,

- 8. Pettinger, T., 2022. Moral Hazard - Economics Help. [online] Economics Help. Available at: [Accessed 14 June

- 10. Скачать презентацию

South Africa's financial services sector is strong, with numerous of domestic

South Africa's financial services sector is strong, with numerous of domestic

BANKING SYSTEM

National banks have branches across South Africa. Bank branches are

BANKING SYSTEM

National banks have branches across South Africa. Bank branches are

CENTRAL BANK

South Africa's central bank is the South African Reserve Bank

CENTRAL BANK

South Africa's central bank is the South African Reserve Bank

According to the SARB's most recent annual report, net investment income

According to the SARB's most recent annual report, net investment income

ASYMMETRIC INFORMATION

01

Asymmetric Information is a situation whereby unequal

knowledge between the parties of a transaction results in a

unique advantage with

additional knowledge. It occurs primarily before the

transaction/pre-contractual

problem. Adverse selection and Moral hazard can

ASYMMETRIC INFORMATION

01

Asymmetric Information is a situation whereby unequal

knowledge between the parties of a transaction results in a

unique advantage with

additional knowledge. It occurs primarily before the

transaction/pre-contractual

problem. Adverse selection and Moral hazard can

In banking, the consumer will have superior information than the bank.

In banking, the consumer will have superior information than the bank.

![Pettinger, T., 2022. Moral Hazard - Economics Help. [online] Economics](/_ipx/f_webp&q_80&fit_contain&s_1440x1080/imagesDir/jpg/341706/slide-7.jpg)

Pettinger, T., 2022. Moral Hazard - Economics Help. [online] Economics Help.

Pettinger, T., 2022. Moral Hazard - Economics Help. [online] Economics Help.

Природные комплексы. Презентация. 6 класс

Природные комплексы. Презентация. 6 класс Хронический гастрит

Хронический гастрит Тип связи в словосочетаниях

Тип связи в словосочетаниях Проект по экспериментальной деятельности Волшебные кристаллы

Проект по экспериментальной деятельности Волшебные кристаллы Непрерывные сигналы. (Лекция 1.4)

Непрерывные сигналы. (Лекция 1.4) Влияние цены на излишек производителей

Влияние цены на излишек производителей Эпоха дворцовых переворотов

Эпоха дворцовых переворотов Науково-методичні засади організації роботи з обдарованими дітьми

Науково-методичні засади організації роботи з обдарованими дітьми Аргентина. Визитная карточка

Аргентина. Визитная карточка Презентация Малая летняя академия

Презентация Малая летняя академия Преимущества и выгода продукции Nature’s Sunshine перед аптечными аналогами

Преимущества и выгода продукции Nature’s Sunshine перед аптечными аналогами Информационные жанры. Как писать заметку

Информационные жанры. Как писать заметку Поздравляем с 23 февраля

Поздравляем с 23 февраля Воспитательный потенциал современной семьи

Воспитательный потенциал современной семьи Площади подобных фигур

Площади подобных фигур Вентиляция помещений

Вентиляция помещений Презентация Шоколад

Презентация Шоколад Международный день охраны памятников и исторических мест

Международный день охраны памятников и исторических мест Симплекс-метод

Симплекс-метод содержание работы по развитию слухового восприятия речи

содержание работы по развитию слухового восприятия речи Внеурочная деятельность Мои первые проекты. тема Декупаж

Внеурочная деятельность Мои первые проекты. тема Декупаж Направления реализации Национальной стратегии по обращению с ТКО и ВМР

Направления реализации Национальной стратегии по обращению с ТКО и ВМР 2.2. Элементарные действия. Алгоритмические структуры [ТРИК]

2.2. Элементарные действия. Алгоритмические структуры [ТРИК] Презентация к занятию по предшкольной подготовке Снеговик - почтовик

Презентация к занятию по предшкольной подготовке Снеговик - почтовик Этнос и этничность в российской этнологии. Признаки этноса – факторы актуализации этничности

Этнос и этничность в российской этнологии. Признаки этноса – факторы актуализации этничности Патофизиология: предмет, задачи, методы

Патофизиология: предмет, задачи, методы Ассортимент курток FW 19-20

Ассортимент курток FW 19-20 Робототехника. Понятие, история и современность

Робототехника. Понятие, история и современность