- European energy transition

Содержание

- 2. Table of contents ▶ Status of natural gas in Europe © World Energy Council 2014 ▶

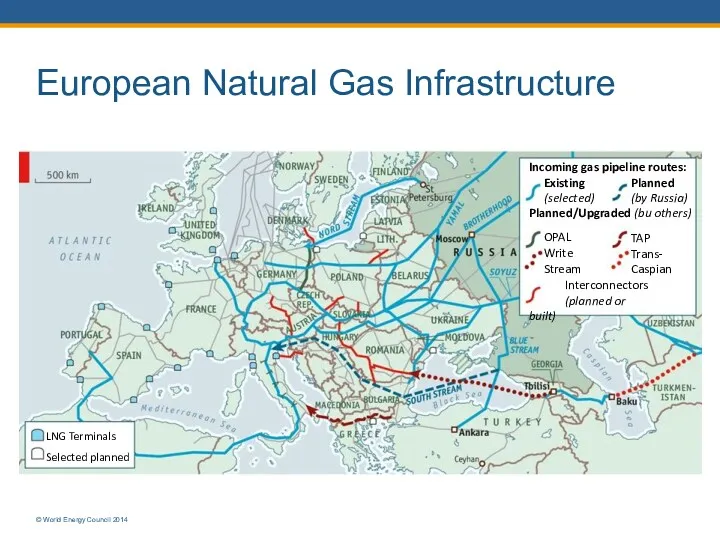

- 3. European Natural Gas Infrastructure © World Energy Council 2014 LNG Terminals Selected planned Incoming gas pipeline

- 4. European Natural Gas Demand/Supply © World Energy Council 2014

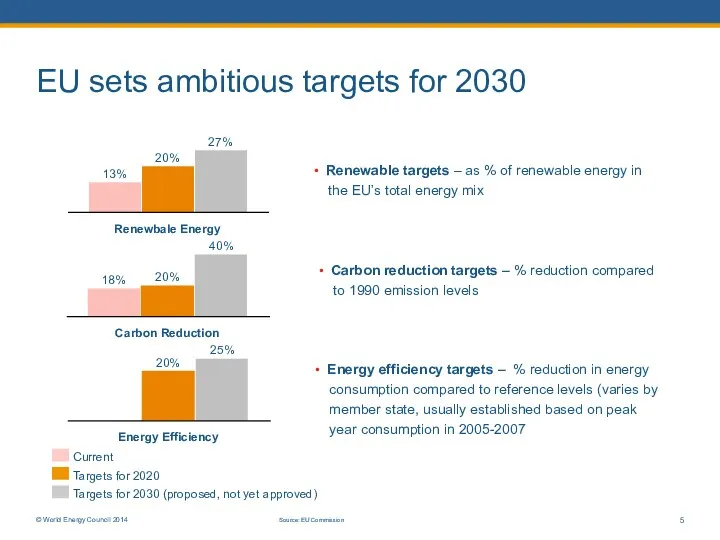

- 5. EU sets ambitious targets for 2030 Renewbale Energy 40% 27% 20% 13% Current Targets for 2020

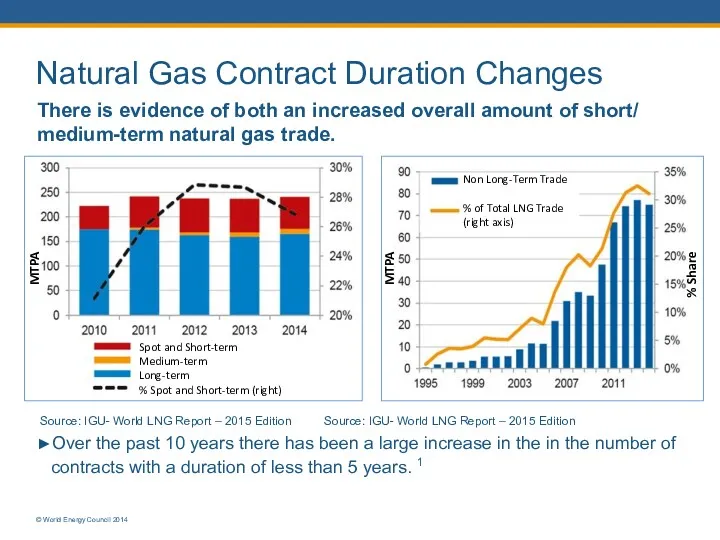

- 6. Natural Gas Contract Duration Changes There is evidence of both an increased overall amount of short/

- 7. Table of contents ▶ Status of natural gas in Europe © World Energy Council 2014 ▶

- 8. Despite the recent turmoil, the outlook for the world economy in 2020 remains unclear © World

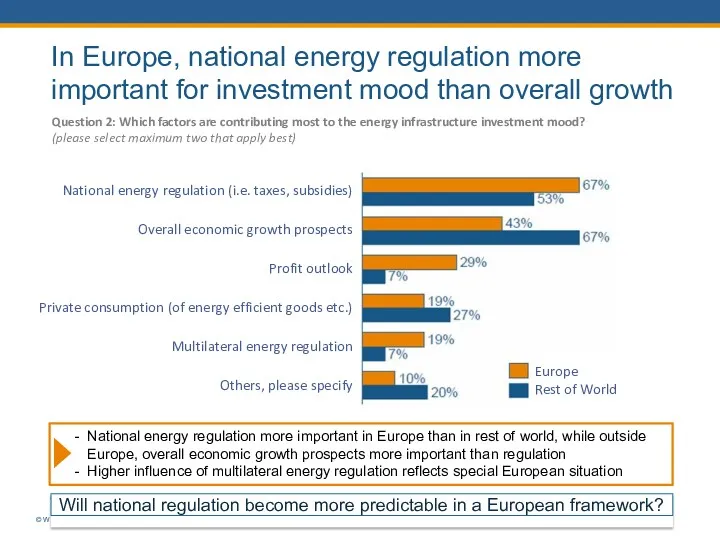

- 9. orld Energy Council 2014 Will national regulation become more predictable in a European framework? © W

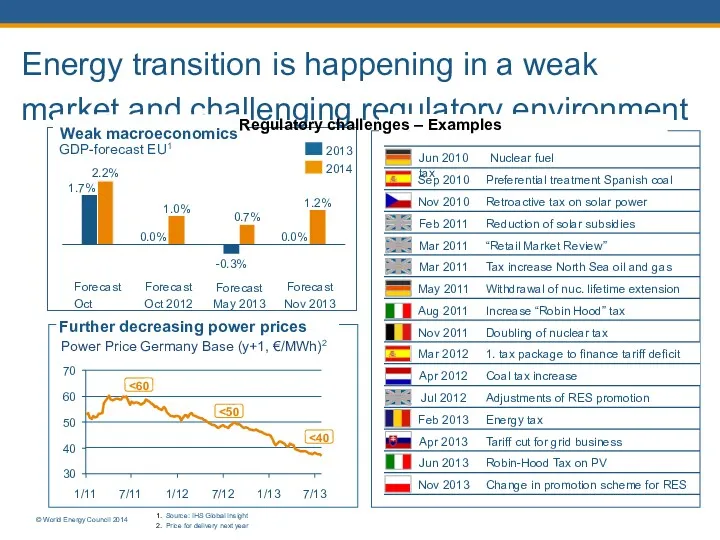

- 10. 10 Energy transition is happening in a weak market and challenging regulatory environment GDP-forecast EU1 2.2%

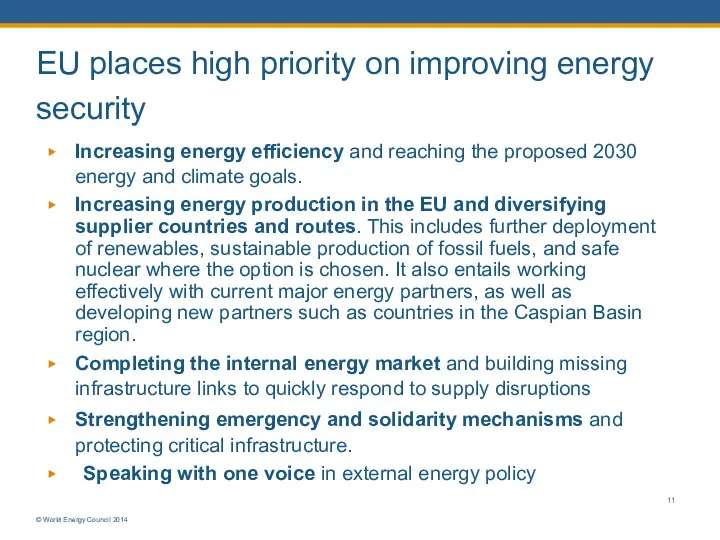

- 11. EU places high priority on improving energy security © World Energy Council 2014 ▶ Increasing energy

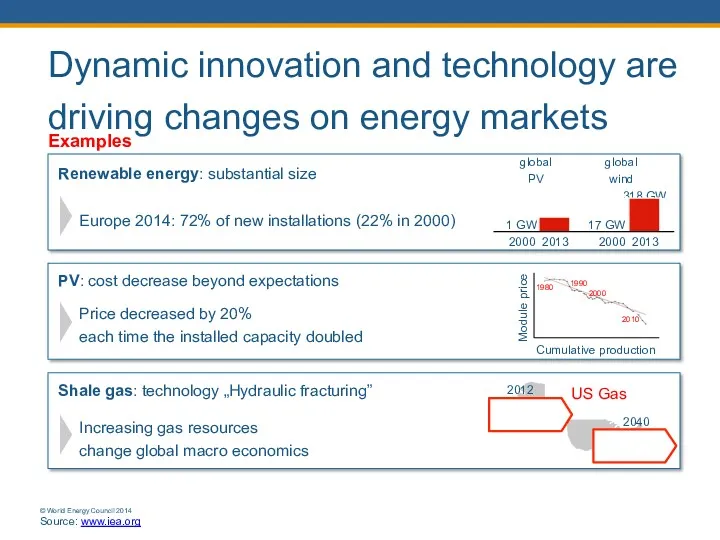

- 12. Dynamic innovation and technology are driving changes on energy markets Examples US Gas 2040 Net exporter

- 13. Table of contents ▶ Status of natural gas in Europe ▶ Forces for change © World

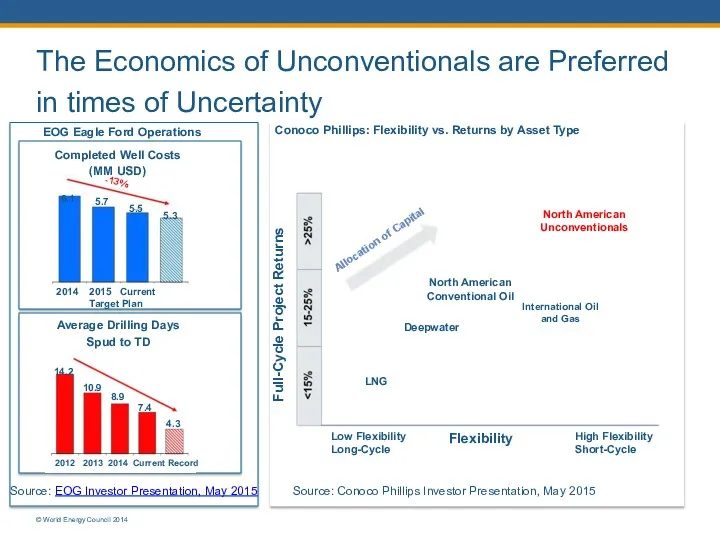

- 14. The Economics of Unconventionals are Preferred in times of Uncertainty Conoco Phillips: Flexibility vs. Returns by

- 16. Скачать презентацию

Table of contents

▶ Status of natural gas in Europe

© World Energy Council

Table of contents

▶ Status of natural gas in Europe

© World Energy Council

European Natural Gas Infrastructure

© World Energy Council 2014

LNG Terminals

Selected planned

Incoming gas

European Natural Gas Infrastructure

© World Energy Council 2014

LNG Terminals

Selected planned

Incoming gas

European Natural Gas Demand/Supply

© World Energy Council 2014

European Natural Gas Demand/Supply

© World Energy Council 2014

EU sets ambitious targets for 2030

Renewbale Energy

40%

27%

20%

13%

Current

Targets for 2020

Targets for 2030

EU sets ambitious targets for 2030

Renewbale Energy

40%

27%

20%

13%

Current

Targets for 2020

Targets for 2030

Natural Gas Contract Duration Changes

There is evidence of both an increased

Natural Gas Contract Duration Changes

There is evidence of both an increased

Table of contents

▶ Status of natural gas in Europe

© World Energy Council

Table of contents

▶ Status of natural gas in Europe

© World Energy Council

Despite the recent turmoil, the outlook for the world economy in

Despite the recent turmoil, the outlook for the world economy in

orld Energy Council 2014

Will national regulation become more predictable in a

orld Energy Council 2014

Will national regulation become more predictable in a

10

Energy transition is happening in a weak market and challenging regulatory environment

GDP-forecast

10

Energy transition is happening in a weak market and challenging regulatory environment

GDP-forecast

EU places high priority on improving energy security

© World Energy Council

EU places high priority on improving energy security

© World Energy Council

Dynamic innovation and technology are driving changes on energy markets

Examples

US Gas

2040

Net

Dynamic innovation and technology are driving changes on energy markets

Examples

US Gas

2040

Net

Table of contents

▶ Status of natural gas in Europe

▶ Forces for change

© World

Table of contents

▶ Status of natural gas in Europe

▶ Forces for change

© World

The Economics of Unconventionals are Preferred in times of Uncertainty

Conoco Phillips:

The Economics of Unconventionals are Preferred in times of Uncertainty

Conoco Phillips:

Презентация Сюжетно-ролевая игра в развитии старших дошкольников

Презентация Сюжетно-ролевая игра в развитии старших дошкольников Теория строение органических соединений

Теория строение органических соединений Приложение 1 к уроку по теме Озёра. Презентация. часть1

Приложение 1 к уроку по теме Озёра. Презентация. часть1 Древние образы в народном искусстве. 5 класс

Древние образы в народном искусстве. 5 класс Сталинградская битва.

Сталинградская битва. Материки и океаны

Материки и океаны Черная металлургия. Производство чугуна и стали. 9 класс

Черная металлургия. Производство чугуна и стали. 9 класс Қатты отындарды газдендіру

Қатты отындарды газдендіру Выявлекние и устранение типовых неисправностей блоков питания

Выявлекние и устранение типовых неисправностей блоков питания Теория к заданию № 16 (ЕГЭ по русскому языку. Версия 2019 года)

Теория к заданию № 16 (ЕГЭ по русскому языку. Версия 2019 года) Самостоятельная двигательная активность детей на прогулке, руководство ею

Самостоятельная двигательная активность детей на прогулке, руководство ею Презентация выступления на педсовете по теме Выявление трудных детей

Презентация выступления на педсовете по теме Выявление трудных детей Родительское собрание Роль книги в развитии интеллектуальных умений ребёнка (Конспект с презентацией)

Родительское собрание Роль книги в развитии интеллектуальных умений ребёнка (Конспект с презентацией) Классный час Я и другие люди. Вежливость.

Классный час Я и другие люди. Вежливость. класс

класс Развертка пирамиды

Развертка пирамиды Общие пути катаболизма. Энергетический обмен

Общие пути катаболизма. Энергетический обмен Презентация к уроку библиотечно-информационной грамотности по теме Структура книги

Презентация к уроку библиотечно-информационной грамотности по теме Структура книги Внеурочная деятельность (кружки)

Внеурочная деятельность (кружки) Деловая игра, как способ развития социальной компетентности у учащихся на уроках географии

Деловая игра, как способ развития социальной компетентности у учащихся на уроках географии Артикуляционная гимнастика для малышей

Артикуляционная гимнастика для малышей Раннее Новое время: от средневекового общества к обществу индустриальному

Раннее Новое время: от средневекового общества к обществу индустриальному Получение негативного изображения

Получение негативного изображения Пеларгония зональная красная

Пеларгония зональная красная Здоровьесберегающие технологии в начальной школе.

Здоровьесберегающие технологии в начальной школе. Презентация Природные зоны Северной Америки

Презентация Природные зоны Северной Америки Органы цветковых растений. Корень

Органы цветковых растений. Корень Система ЦТ SECAM

Система ЦТ SECAM