Financial Statements and Ratio Analysis Cash Flow and Financial Planning. Time Value of Money презентация

- Financial Statements and Ratio Analysis Cash Flow and Financial Planning. Time Value of Money

Содержание

- 2. Learning Goals Review the contents of the stockholders’ report and the procedures for consolidating international financial

- 3. The Stockholders’ Report generally accepted accounting principles (GAAP) The practice and procedure guidelines used to prepare

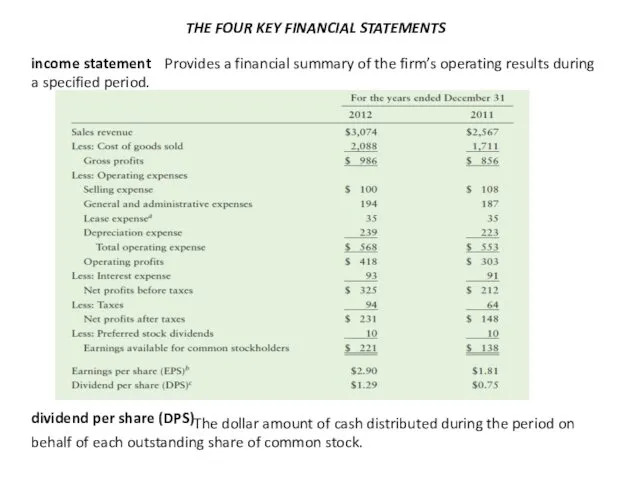

- 4. THE FOUR KEY FINANCIAL STATEMENTS income statement Provides a financial summary of the firm’s operating results

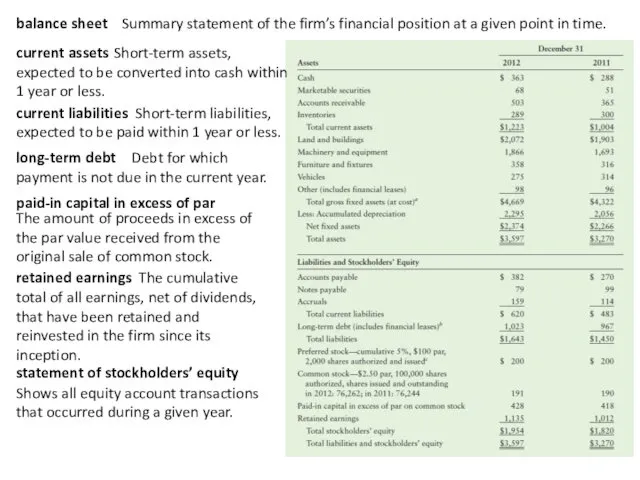

- 5. balance sheet Summary statement of the firm’s financial position at a given point in time. current

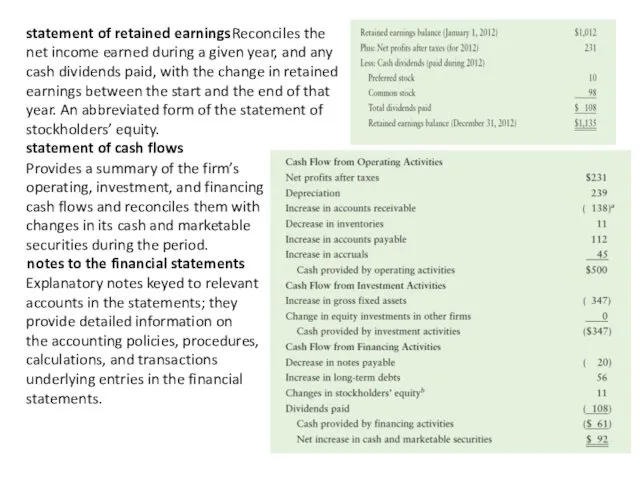

- 6. statement of retained earnings Reconciles the net income earned during a given year, and any cash

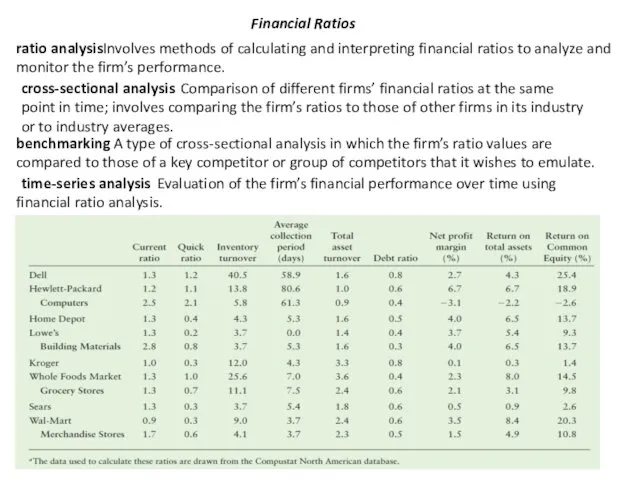

- 7. Financial Ratios ratio analysis Involves methods of calculating and interpreting financial ratios to analyze and monitor

- 8. Liquidity Ratios liquidity A firm’s ability to satisfy its short-term obligations as they come due. current

- 9. debt ratio Measures the proportion of total assets financed by the firm’s creditors. times interest earned

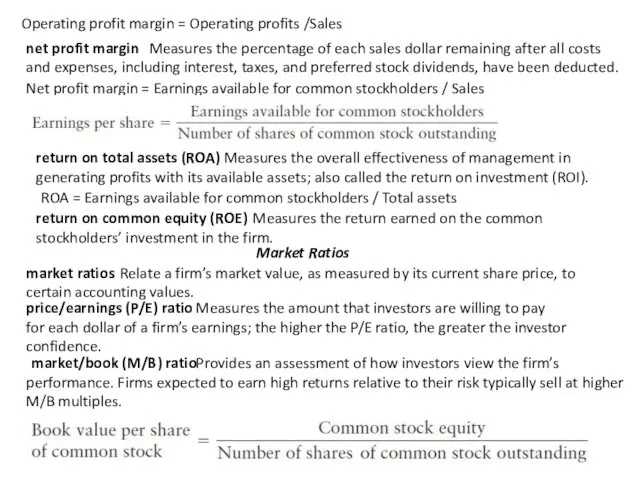

- 10. Operating profit margin = Operating profits /Sales net profit margin Measures the percentage of each sales

- 12. Скачать презентацию

Learning Goals

Review the contents of the stockholders’ report and the procedures

Learning Goals

Review the contents of the stockholders’ report and the procedures

The Stockholders’ Report

generally accepted accounting principles (GAAP)

The practice and procedure

The Stockholders’ Report

generally accepted accounting principles (GAAP)

The practice and procedure

THE FOUR KEY FINANCIAL STATEMENTS

income statement

Provides a financial summary of

THE FOUR KEY FINANCIAL STATEMENTS

income statement

Provides a financial summary of

balance sheet

Summary statement of the firm’s financial position at a

balance sheet

Summary statement of the firm’s financial position at a

statement of retained earnings

Reconciles the net income earned during a

statement of retained earnings

Reconciles the net income earned during a

Financial Ratios

ratio analysis

Involves methods of calculating and interpreting financial ratios

Financial Ratios

ratio analysis

Involves methods of calculating and interpreting financial ratios

Liquidity Ratios

liquidity

A firm’s ability to satisfy its short-term obligations as

Liquidity Ratios

liquidity

A firm’s ability to satisfy its short-term obligations as

debt ratio

Measures the proportion of total assets financed by the

debt ratio

Measures the proportion of total assets financed by the

Operating profit margin = Operating profits /Sales

net profit margin

Measures the

Operating profit margin = Operating profits /Sales

net profit margin

Measures the

Основные свойства функций

Основные свойства функций Всестороннее развитие ребёнка дошкольного возраста родителями дома

Всестороннее развитие ребёнка дошкольного возраста родителями дома Презентация Мой любимый город

Презентация Мой любимый город Работа с возражениями клиентов компании Пивград

Работа с возражениями клиентов компании Пивград Управление изменениями и жизненным циклом организации

Управление изменениями и жизненным циклом организации Вредоносные и антивирусные программы

Вредоносные и антивирусные программы Древнейшая стадия в развитии человечества

Древнейшая стадия в развитии человечества Презентация: Информационно-образовательный Портал Республики Хакасия. Вход для родителей. Диск

Презентация: Информационно-образовательный Портал Республики Хакасия. Вход для родителей. Диск Рак шийки матки

Рак шийки матки Родина - слово большое, большое.

Родина - слово большое, большое. Психолого-педагогическая диагностика развития детей

Психолого-педагогическая диагностика развития детей Поговорим о дружбе

Поговорим о дружбе Проблема создания космического комплекса для исследования короны солнца

Проблема создания космического комплекса для исследования короны солнца Песни с которыми мы победили

Песни с которыми мы победили Упаковочные оборудования для хлебобулочных изделий

Упаковочные оборудования для хлебобулочных изделий Профессии

Профессии Трудовые и непосредственно связанные с ними правоотношения: их элементы, основания возникновения, изменения и прекращения

Трудовые и непосредственно связанные с ними правоотношения: их элементы, основания возникновения, изменения и прекращения психолог - детям

психолог - детям Московское княжество в первой половине 15 в

Московское княжество в первой половине 15 в Психологические проблемы педагогического оценивания

Психологические проблемы педагогического оценивания метапредметные результаты

метапредметные результаты Инвагинация кишечника у детей

Инвагинация кишечника у детей Классификация и значение витаминов

Классификация и значение витаминов [Ю] авазы, Ю, ю хэрефлэре темасына презентация

[Ю] авазы, Ю, ю хэрефлэре темасына презентация игра Космическое путешествие

игра Космическое путешествие Архитектура и скульптура. Россия: 1-я половина 19 века

Архитектура и скульптура. Россия: 1-я половина 19 века Викторина для девочек к 8 марта Собираем букет

Викторина для девочек к 8 марта Собираем букет Интелектуальная ига по математике для 8 класса.

Интелектуальная ига по математике для 8 класса.