- Q1 FY2011 Key drivers & Financial highlights

Содержание

- 2. Q1 FY2011 Key drivers Markets International grain prices increase by 35 – 45% (depending on crop)

- 3. Q1 FY2011 Contribution by operating segment Revenue by operating segment (1) Revenue by operating segment includes

- 4. Q1 FY2011 Segmental results Segmental revenue includes intersegment sales, reflected in item “Other and reconciliation” Segmental

- 5. Outlook for FY2011 FY2011 Guidance remains unchanged Revenue of USD 1 300 million EBITDA of USD

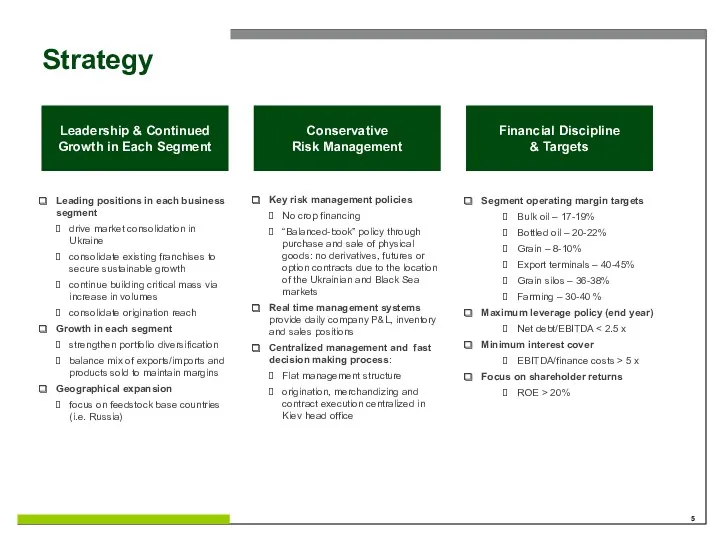

- 6. Strategy Leading positions in each business segment drive market consolidation in Ukraine consolidate existing franchises to

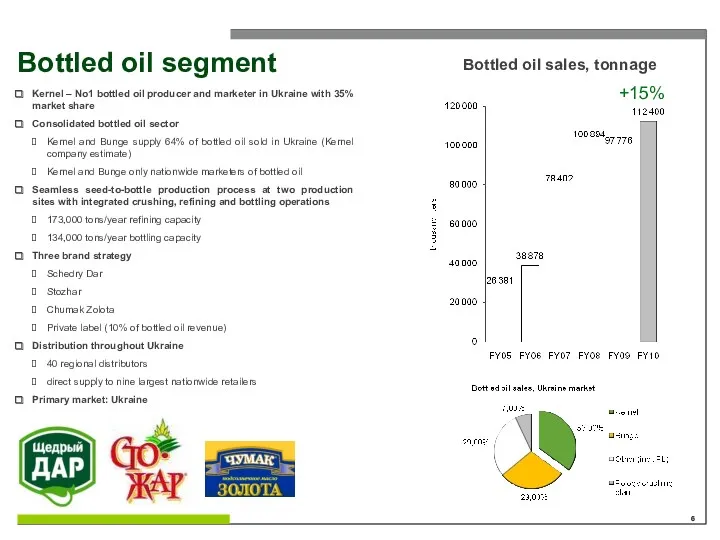

- 7. Bottled oil segment Kernel – No1 bottled oil producer and marketer in Ukraine with 35% market

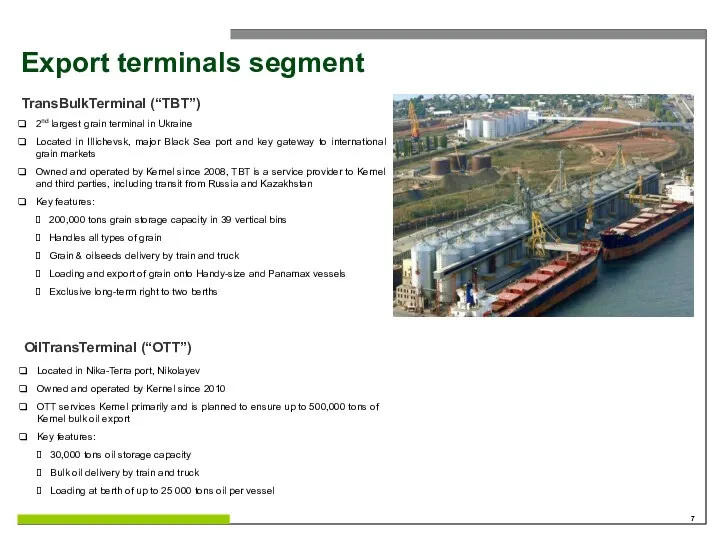

- 8. Export terminals segment 2nd largest grain terminal in Ukraine Located in Illichevsk, major Black Sea port

- 10. Скачать презентацию

Q1 FY2011 Key drivers

Markets

International grain prices increase by 35 –

Q1 FY2011 Key drivers

Markets

International grain prices increase by 35 –

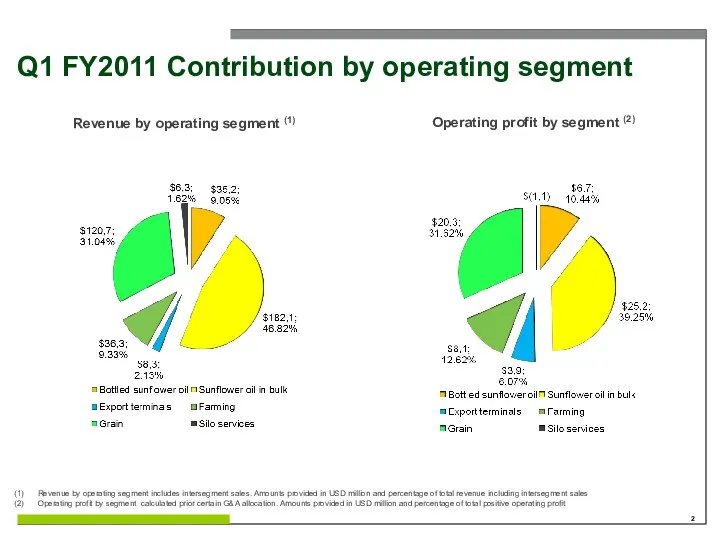

Q1 FY2011 Contribution by operating segment

Revenue by operating segment (1)

Revenue

Q1 FY2011 Contribution by operating segment

Revenue by operating segment (1)

Revenue

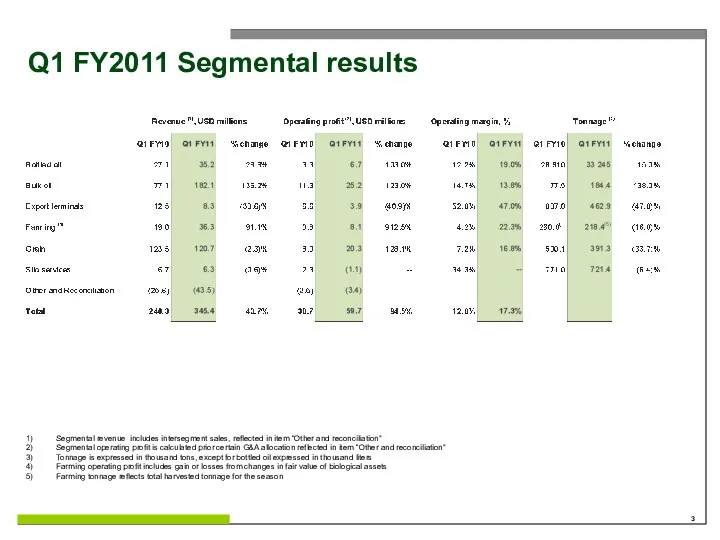

Q1 FY2011 Segmental results

Segmental revenue includes intersegment sales, reflected in item

Q1 FY2011 Segmental results

Segmental revenue includes intersegment sales, reflected in item

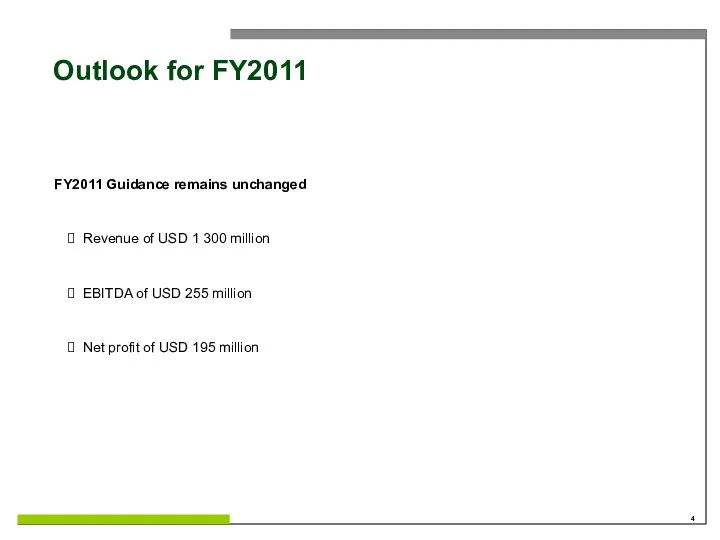

Outlook for FY2011

FY2011 Guidance remains unchanged

Revenue of USD 1 300 million

EBITDA

Outlook for FY2011

FY2011 Guidance remains unchanged

Revenue of USD 1 300 million

EBITDA

Strategy

Leading positions in each business segment

drive market consolidation in Ukraine

consolidate existing

Strategy

Leading positions in each business segment

drive market consolidation in Ukraine

consolidate existing

Bottled oil segment

Kernel – No1 bottled oil producer and marketer in

Bottled oil segment

Kernel – No1 bottled oil producer and marketer in

Export terminals segment

2nd largest grain terminal in Ukraine

Located in Illichevsk, major

Export terminals segment

2nd largest grain terminal in Ukraine

Located in Illichevsk, major

Базовые эмоции

Базовые эмоции Пластилиновая живопись Рыбка в аквариуме

Пластилиновая живопись Рыбка в аквариуме Ян Амос Коменский

Ян Амос Коменский Проект Образование для родителей

Проект Образование для родителей 12 апреля – День космонавтики

12 апреля – День космонавтики Внеклассное мероприятие к 70-летию Великой Победы

Внеклассное мероприятие к 70-летию Великой Победы 70 лет Кемеровской области

70 лет Кемеровской области Презентация Правила дорожного движения

Презентация Правила дорожного движения Памятка по оформлению краткой записи к задачам 1-2 класс

Памятка по оформлению краткой записи к задачам 1-2 класс Презентация Игротека. Звук Л №4

Презентация Игротека. Звук Л №4 Артериалды гипертензия кезінде калийді қолдану тиімділігі

Артериалды гипертензия кезінде калийді қолдану тиімділігі Назови одним словом

Назови одним словом Складнопідрядне речення з підрядними допустовими

Складнопідрядне речення з підрядними допустовими Система технического нормирования и стандартизации Республики Беларусь

Система технического нормирования и стандартизации Республики Беларусь Школа дошколят Звонкие ладошки занятие 2

Школа дошколят Звонкие ладошки занятие 2 Информационные технологии в бухгалтерском учете

Информационные технологии в бухгалтерском учете Ограждение машин и механизмов

Ограждение машин и механизмов Степень окисления элементов

Степень окисления элементов Акустический гнозис. Сенсорные и гностические слуховые расстройства. Исследование слухового гнозиса

Акустический гнозис. Сенсорные и гностические слуховые расстройства. Исследование слухового гнозиса Теплотехнические расчёты изотермических вагонов и контейнеров

Теплотехнические расчёты изотермических вагонов и контейнеров Исторический ликбез. Оливер Кромвель, или Лорд-протектор Англии, Шотландии и Ирландии

Исторический ликбез. Оливер Кромвель, или Лорд-протектор Англии, Шотландии и Ирландии Интернет - викторина Новый год шагает по планете

Интернет - викторина Новый год шагает по планете Понятие, признаки,структура нормы права

Понятие, признаки,структура нормы права Исследование теплового метода неразрушающего контроля качества двухслойных изделий из сплава алюминия с полиамидным покрытием

Исследование теплового метода неразрушающего контроля качества двухслойных изделий из сплава алюминия с полиамидным покрытием Входные устройства при различной связи с антенной

Входные устройства при различной связи с антенной Articles. In this game you have to choose the correct article to complete each sentence

Articles. In this game you have to choose the correct article to complete each sentence Физминутка Веселые смайлики

Физминутка Веселые смайлики Презентация Права ребенка Диск

Презентация Права ребенка Диск