- Cost management. Accounting and control

Содержание

- 2. Basic Cost Management Concepts CHAPTER 2

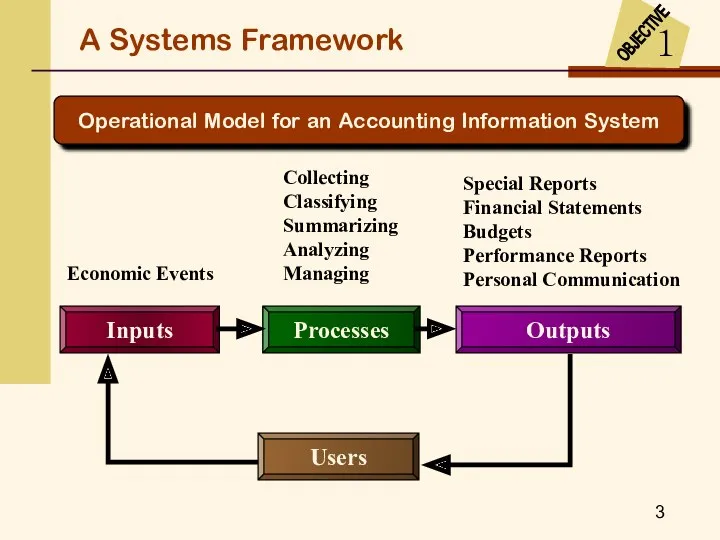

- 3. A Systems Framework OBJECTIVE 1 Operational Model for an Accounting Information System Collecting Classifying Summarizing Analyzing

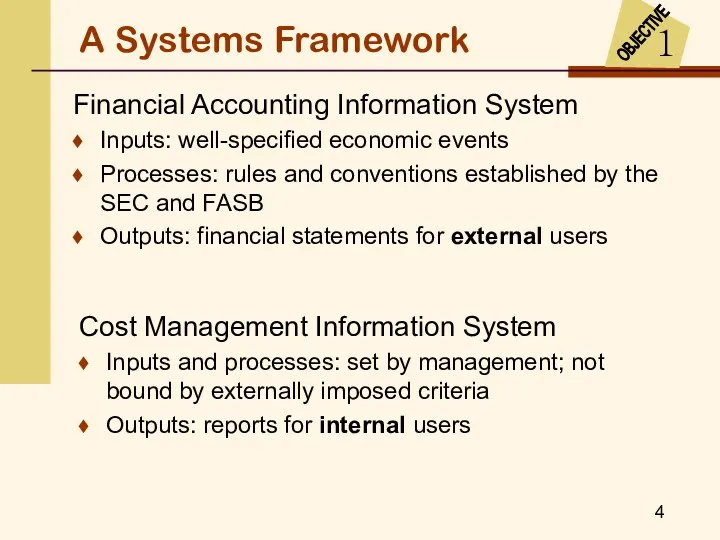

- 4. Financial Accounting Information System Inputs: well-specified economic events Processes: rules and conventions established by the SEC

- 5. A Systems Framework The cost management information system has three broad objectives that provide information for--

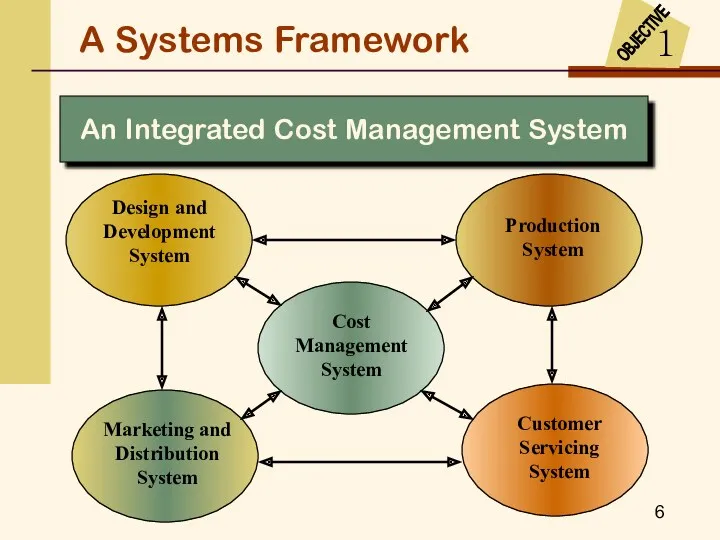

- 6. An Integrated Cost Management System Design and Development System Customer Servicing System Marketing and Distribution System

- 7. A Systems Framework 1 OBJECTIVE The Subsystems of the Accounting Information System Accounting Information System Assigns

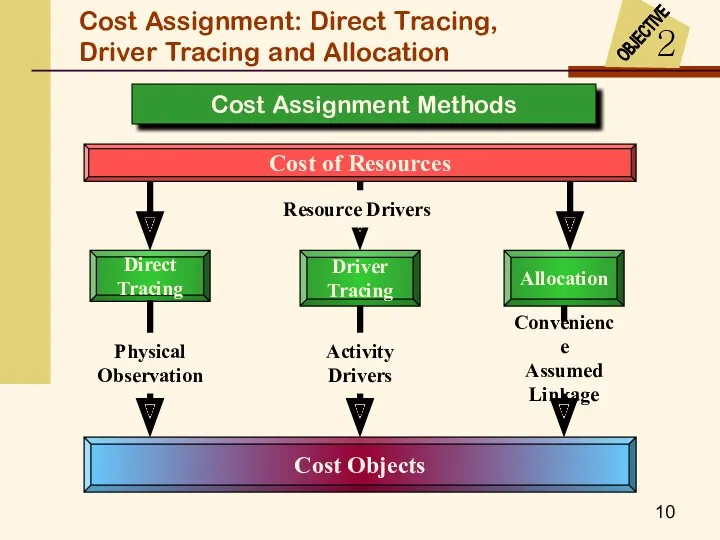

- 8. Cost Assignment: Direct Tracing, Driver Tracing and Allocation 2 OBJECTIVE A cost object is any item,

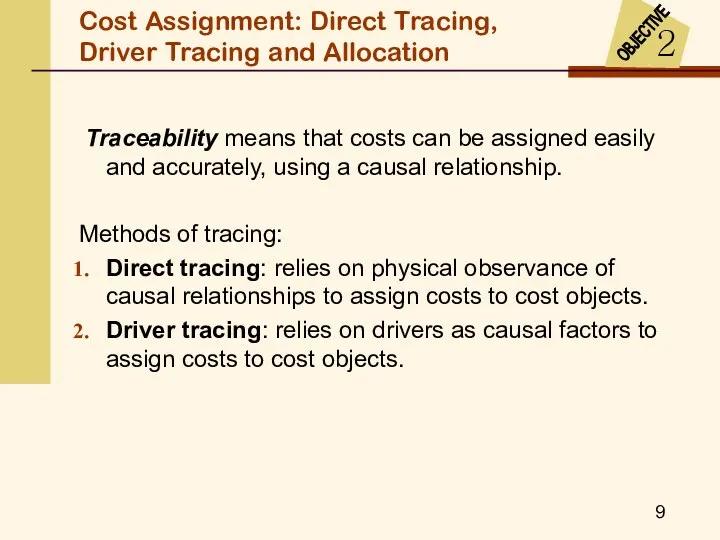

- 9. Cost Assignment: Direct Tracing, Driver Tracing and Allocation 2 OBJECTIVE Traceability means that costs can be

- 10. Cost Assignment Methods Cost Assignment: Direct Tracing, Driver Tracing and Allocation

- 11. Cost Assignment Methods Cost Assignment: Direct Tracing, Driver Tracing and Allocation

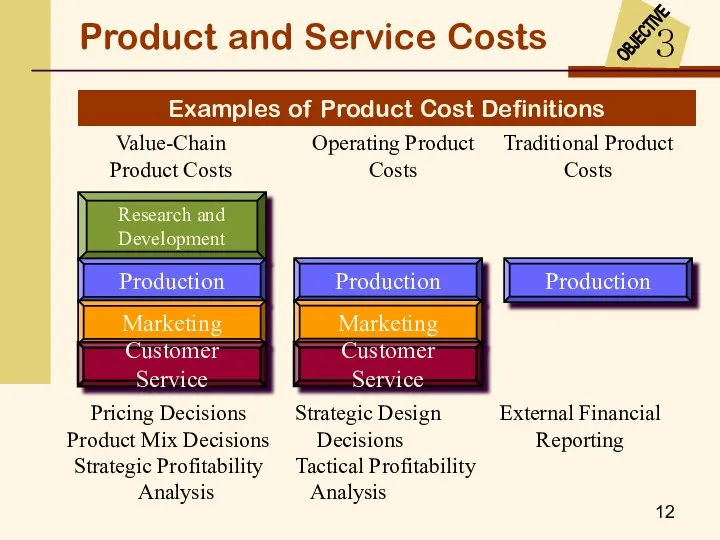

- 12. Examples of Product Cost Definitions Pricing Decisions Product Mix Decisions Strategic Profitability Analysis Strategic Design Decisions

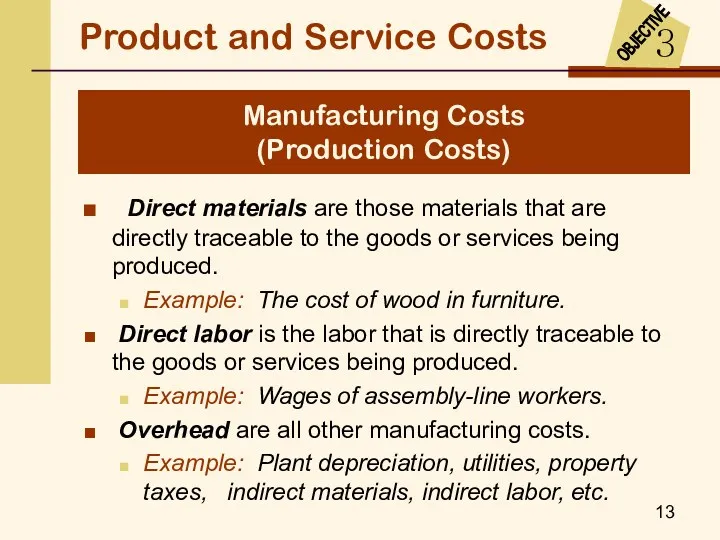

- 13. Direct materials are those materials that are directly traceable to the goods or services being produced.

- 14. Product and Service Costs Manufacturing costs are assigned to products and carried in inventories until the

- 15. Marketing (selling) costs are the costs necessary to market, distribute, and service a product or service.

- 16. Product and Service Costs For external financial reporting, marketing and administrative costs are not inventoried. They

- 17. Production or Manufacturing Costs Nonproduction or Operating Costs Product and Service Costs Production and Nonproduction Costs

- 18. External Financial Statements From the Cost of Goods Sold Schedule

- 19. External Financial Statements continued

- 20. External Financial Statements

- 21. External Financial Statements From the Statement of Cost of Goods Manufactured

- 22. Activity-Based Management Model Cost View Driver Analysis Process View Why? What? How well? Resources Functional-Based and

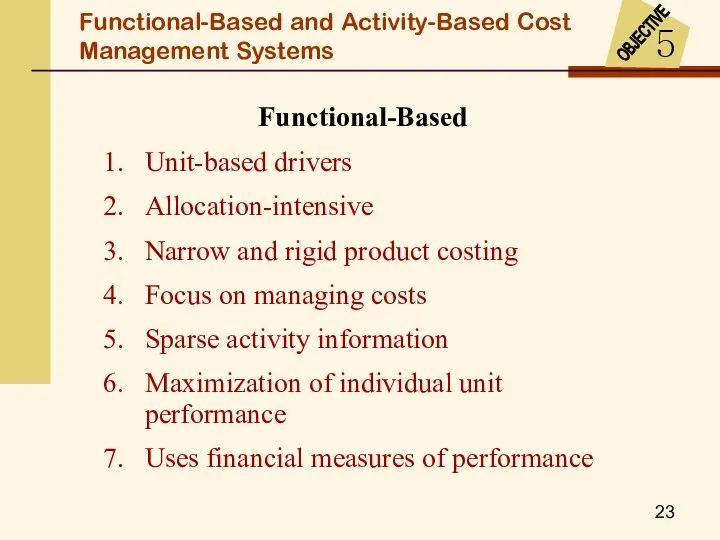

- 23. 1. Unit-based drivers 2. Allocation-intensive 3. Narrow and rigid product costing 4. Focus on managing costs

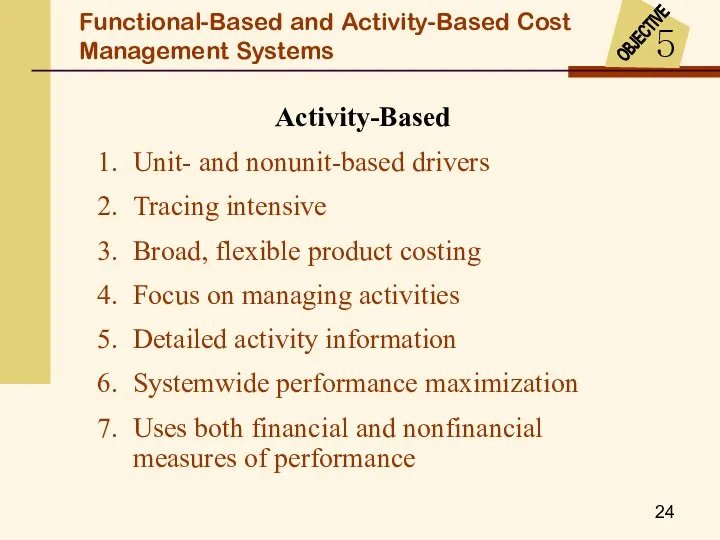

- 24. Activity-Based 1. Unit- and nonunit-based drivers 2. Tracing intensive 3. Broad, flexible product costing 4. Focus

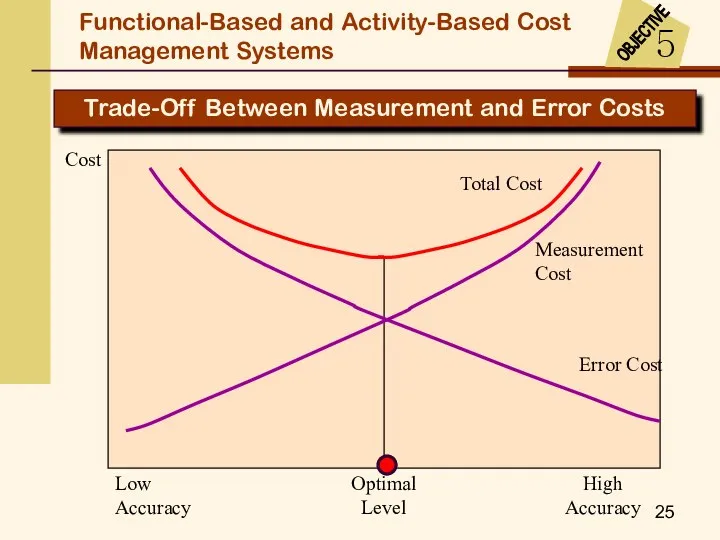

- 25. Low Accuracy High Accuracy Optimal Level Measurement Cost Cost Error Cost Total Cost Trade-Off Between Measurement

- 26. Low High Accuracy New Measurement Cost Cost Old Error Cost Shifting Costs Old Optimum Old Measurement

- 28. Скачать презентацию

Basic Cost

Management Concepts

CHAPTER

2

Basic Cost

Management Concepts

CHAPTER

2

A Systems Framework

OBJECTIVE

1

Operational Model for an Accounting Information System

Collecting

Classifying

Summarizing

Analyzing

Managing

Special Reports

Financial Statements

Budgets

Performance

A Systems Framework

OBJECTIVE

1

Operational Model for an Accounting Information System

Collecting

Classifying

Summarizing

Analyzing

Managing

Special Reports

Financial Statements

Budgets

Performance

Financial Accounting Information System

Inputs: well-specified economic events

Processes: rules and conventions established

Financial Accounting Information System

Inputs: well-specified economic events

Processes: rules and conventions established

A Systems Framework

The cost management information system has three broad objectives

A Systems Framework

The cost management information system has three broad objectives

An Integrated Cost Management System

Design and

Development

System

Customer

Servicing

System

Marketing and

Distribution

System

Cost

Management

System

Production

System

OBJECTIVE

1

A Systems Framework

An Integrated Cost Management System

Design and

Development

System

Customer

Servicing

System

Marketing and

Distribution

System

Cost

Management

System

Production

System

OBJECTIVE

1

A Systems Framework

A Systems Framework

1

OBJECTIVE

The Subsystems of the Accounting Information System

Accounting Information System

Assigns

A Systems Framework

1

OBJECTIVE

The Subsystems of the Accounting Information System

Accounting Information System

Assigns

Cost Assignment: Direct Tracing,

Driver Tracing and Allocation

2

OBJECTIVE

A cost object

Cost Assignment: Direct Tracing,

Driver Tracing and Allocation

2

OBJECTIVE

A cost object

Cost Assignment: Direct Tracing,

Driver Tracing and Allocation

2

OBJECTIVE

Traceability means that

Cost Assignment: Direct Tracing,

Driver Tracing and Allocation

2

OBJECTIVE

Traceability means that

Cost Assignment Methods

Cost Assignment: Direct Tracing,

Driver Tracing and Allocation

Cost Assignment Methods

Cost Assignment: Direct Tracing,

Driver Tracing and Allocation

Cost Assignment Methods

Cost Assignment: Direct Tracing,

Driver Tracing and Allocation

Cost Assignment Methods

Cost Assignment: Direct Tracing,

Driver Tracing and Allocation

Examples of Product Cost Definitions

Pricing Decisions

Product Mix Decisions

Strategic Profitability

Analysis

Strategic Design

Examples of Product Cost Definitions

Pricing Decisions

Product Mix Decisions

Strategic Profitability

Analysis

Strategic Design

Direct materials are those materials that are directly traceable to

Direct materials are those materials that are directly traceable to

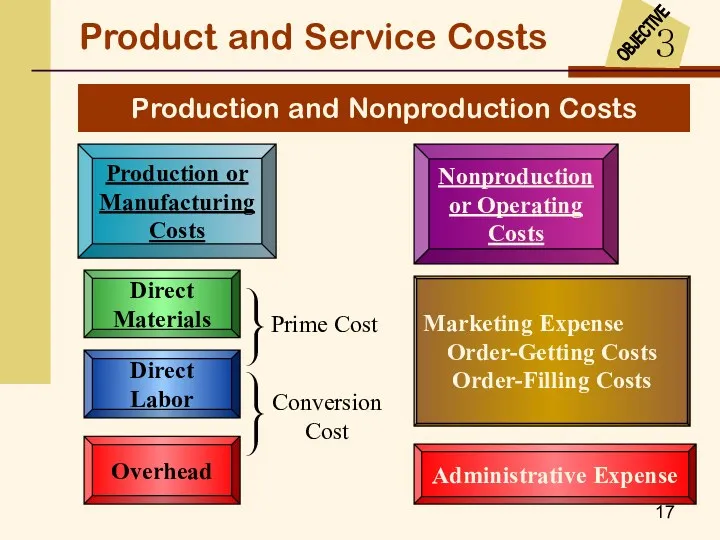

Product and Service Costs

Manufacturing costs are assigned to products and carried

Product and Service Costs

Manufacturing costs are assigned to products and carried

Marketing (selling) costs are the costs necessary to market, distribute,

Marketing (selling) costs are the costs necessary to market, distribute,

Product and Service Costs

For external financial reporting, marketing and administrative costs

Product and Service Costs

For external financial reporting, marketing and administrative costs

Production or Manufacturing Costs

Nonproduction or Operating Costs

Product and Service Costs

Production and

Production or Manufacturing Costs

Nonproduction or Operating Costs

Product and Service Costs

Production and

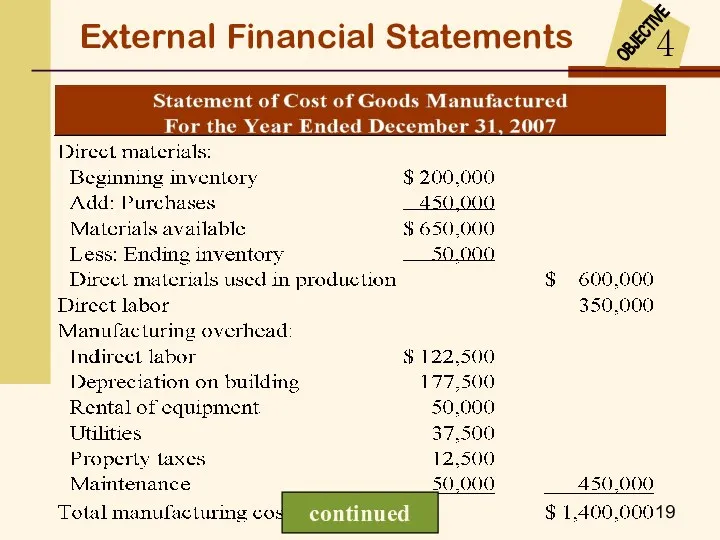

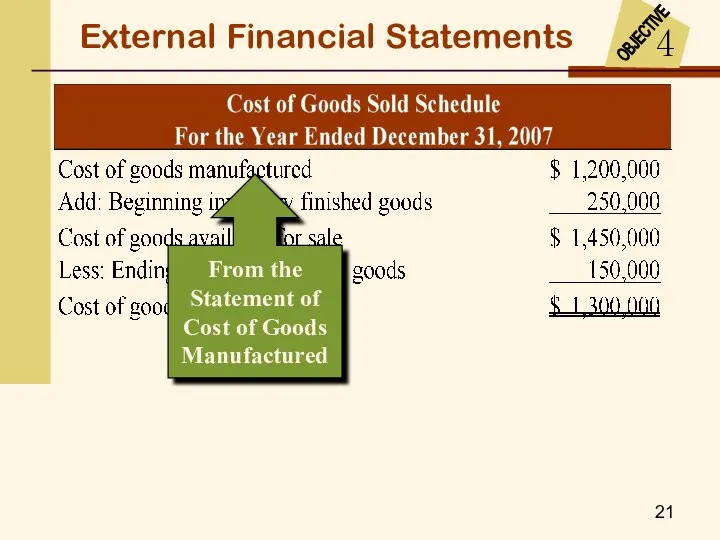

External Financial Statements

From the Cost of Goods Sold Schedule

External Financial Statements

From the Cost of Goods Sold Schedule

External Financial Statements

continued

External Financial Statements

continued

External Financial Statements

External Financial Statements

External Financial Statements

From the Statement of Cost of Goods Manufactured

External Financial Statements

From the Statement of Cost of Goods Manufactured

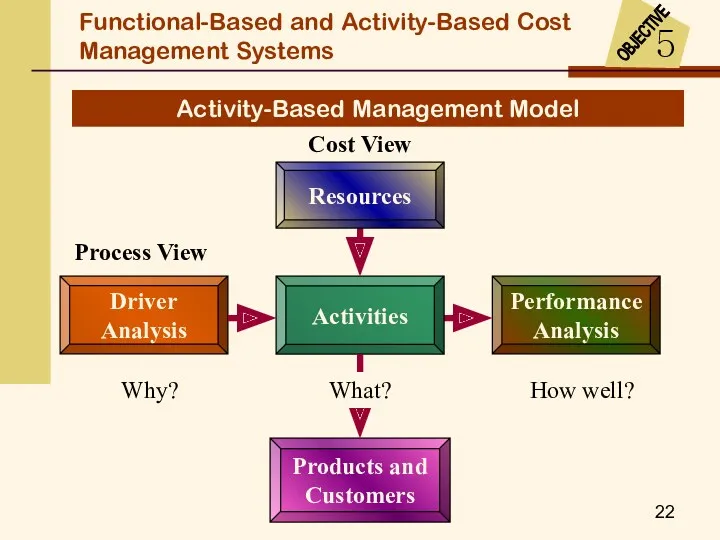

Activity-Based Management Model

Cost View

Driver Analysis

Process View

Why?

What?

How well?

Resources

Functional-Based and Activity-Based Cost Management

Activity-Based Management Model

Cost View

Driver Analysis

Process View

Why?

What?

How well?

Resources

Functional-Based and Activity-Based Cost Management

1. Unit-based drivers

2. Allocation-intensive

3. Narrow and rigid product costing

4. Focus on managing costs

5. Sparse activity

1. Unit-based drivers

2. Allocation-intensive

3. Narrow and rigid product costing

4. Focus on managing costs

5. Sparse activity

Activity-Based

1. Unit- and nonunit-based drivers

2. Tracing intensive

3. Broad, flexible product costing

4. Focus on managing activities

5. Detailed

Activity-Based

1. Unit- and nonunit-based drivers

2. Tracing intensive

3. Broad, flexible product costing

4. Focus on managing activities

5. Detailed

Low Accuracy

High Accuracy

Optimal Level

Measurement Cost

Cost

Error Cost

Total Cost

Trade-Off Between Measurement and Error

Low Accuracy

High Accuracy

Optimal Level

Measurement Cost

Cost

Error Cost

Total Cost

Trade-Off Between Measurement and Error

Low

High

Accuracy

New Measurement Cost

Cost

Old Error Cost

Shifting Costs

Old Optimum

Old Measurement Cost

New Error

Low

High

Accuracy

New Measurement Cost

Cost

Old Error Cost

Shifting Costs

Old Optimum

Old Measurement Cost

New Error

Holidays in Great Britain

Holidays in Great Britain Lecture 5 Categories and types of present-day English and Ukrainian word-formation (part 2)

Lecture 5 Categories and types of present-day English and Ukrainian word-formation (part 2) My favorite sportsman

My favorite sportsman Higher education in the USA

Higher education in the USA A hobby is something you like to do in your free time

A hobby is something you like to do in your free time Update K10 to android 8.1 process

Update K10 to android 8.1 process Memory Game 08 (Body parts)

Memory Game 08 (Body parts) Verbs. What is a verb

Verbs. What is a verb Introduction to the Practice of Medicine - II

Introduction to the Practice of Medicine - II Guess the Countries and Nationalities with profession

Guess the Countries and Nationalities with profession Reported Speech

Reported Speech Betty Schrampfer Azar. Teacher Resource Disc

Betty Schrampfer Azar. Teacher Resource Disc My friends and me

My friends and me Jeopardy game Christmas

Jeopardy game Christmas Companies

Companies Television. For and agains

Television. For and agains Моя семья. Spotlight (5 класс)

Моя семья. Spotlight (5 класс) Participle II

Participle II Тренажёр ОГЭ / ЕГЭ. Pronunciation ABC

Тренажёр ОГЭ / ЕГЭ. Pronunciation ABC Is the Internet the most important part of our life or not

Is the Internet the most important part of our life or not Seasons and the weather

Seasons and the weather Can you remember some types of personalities?

Can you remember some types of personalities? Oxford and Cambridge Universities

Oxford and Cambridge Universities Электронное письмо. ОГЭ - 2020

Электронное письмо. ОГЭ - 2020 Living plants

Living plants Choose this, that, these or those

Choose this, that, these or those Глаголы

Глаголы What kind of country i want to visit

What kind of country i want to visit