- Economy of Russia

Содержание

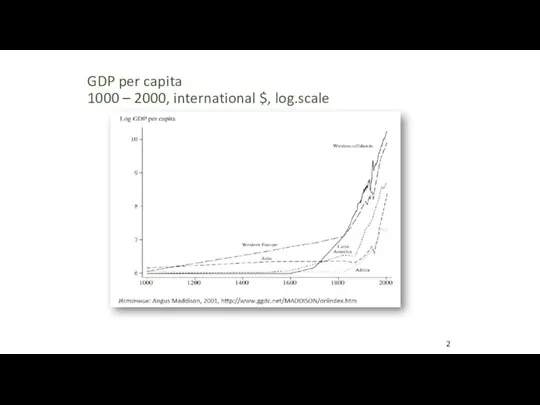

- 2. GDP per capita 1000 – 2000, international $, log.scale 2

- 3. Attempt to reconstruct the world economy dynamics 3

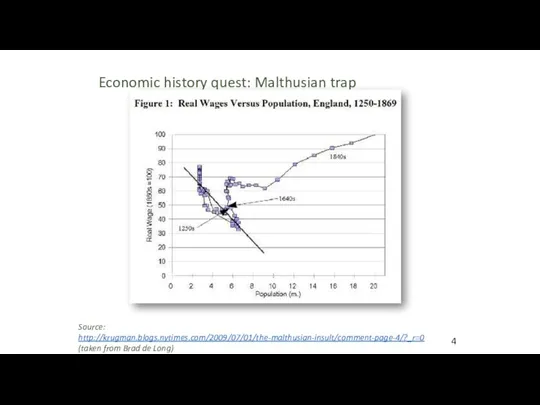

- 4. Economic history quest: Malthusian trap Source: http://krugman.blogs.nytimes.com/2009/07/01/the-malthusian-insult/comment-page-4/?_r=0 (taken from Brad de Long) 4

- 5. Development rates of countries differ Environment: tropics, moderate, North, heath, islands and remote areas Primary states

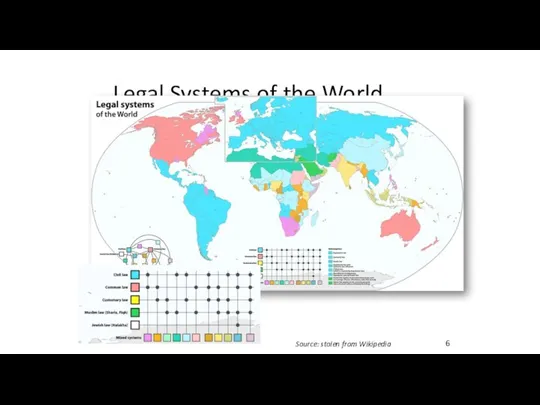

- 6. Legal Systems of the World Source: stolen from Wikipedia 6

- 7. The Great Divergence China, India, Japan, Arabs were helpless against Turkey and Europe in XV-XVI cent.

- 8. Key problems of the Russian history Millennium+ with no peace, regular wars… Big wars – Borders

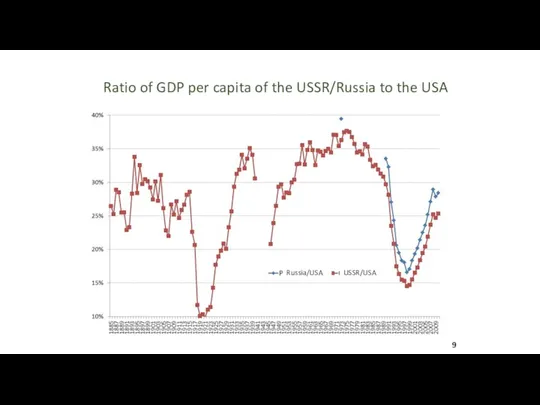

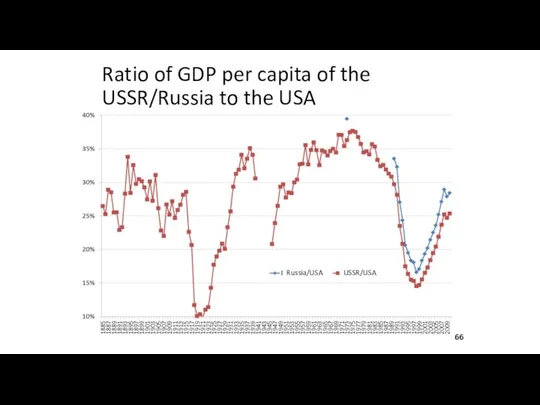

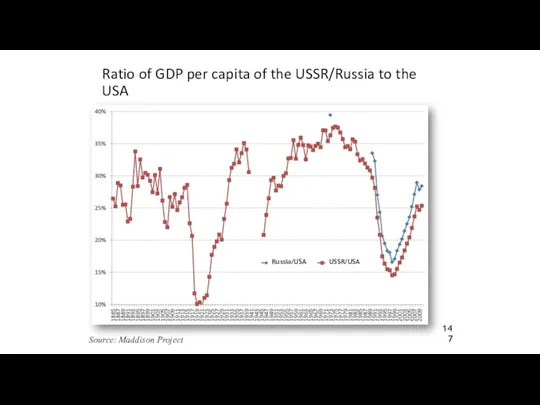

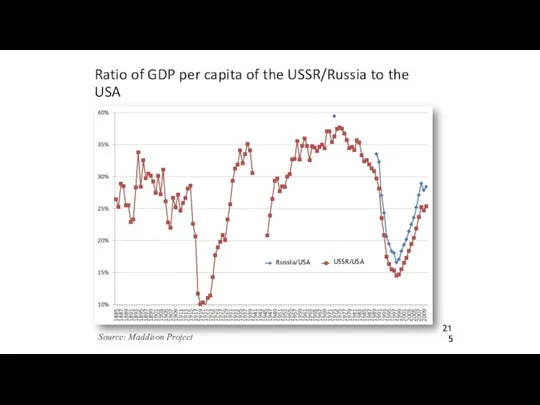

- 9. Ratio of GDP per capita of the USSR/Russia to the USA Russia/USA USSR/USA

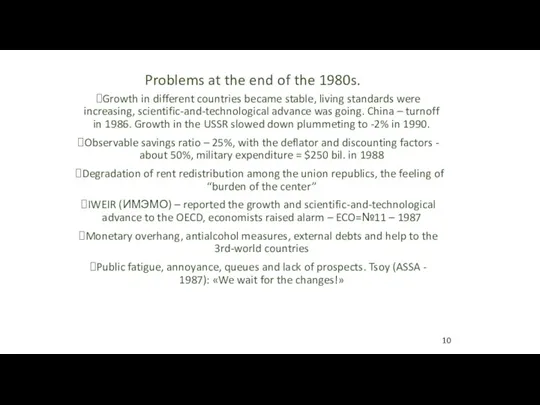

- 10. Problems at the end of the 1980s. Growth in different countries became stable, living standards were

- 11. Moscow princedom, 1533 (in red) Moscow – Central Federal Region, 2013 (green borders)

- 12. History – till 1533 Russian elites – “driving under influence”: Normans since VIII century, Byzantium since

- 13. History – 1533- 1991 (1) 1533 – turning point for enlarging – post Saint Bartholomew massacre

- 14. History – 1533- 1991 (2) WWI and Romanov’s Crush, Revolution out of mainstream; Purges and industrialization

- 15. Remaining European empires Empires were established by ”cool” adventurers followed by boyars and Streltsy Old empires

- 16. Договора Руси с Византией, 860… 912 Нестор - В Повести временных лет об этом договоре сказано:

- 17. Договора Руси с Византией, 860… 912 Русско-византийский договор (907-912). Заключен после успешного похода на Константинополь князя

- 18. 1533 – 1917, 1991 – the Big Bang Ivan the “Terrible”: Siberia – Baltic and South

- 19. Empire is what it is By A.N. Kuropatkin, the Nikolai II Minister of War count, there

- 20. What exactly has to be transformed during a country transition? The most crucial thing is property

- 21. How deals on territorial changes are hold Potential elites and legitimacy Negotiations, elites` interests Arrangements (referendums

- 22. Might the development and transformation issues be resolved? Goals of the transformation: democracy and market economy

- 23. Difficulties and losses of the transitional period boost phobias: Foreign capital as a threat Corruption omnipotence

- 24. …and utopias: Ideal policy exists Governance instead of initiative All-purpose instruments Sudden leaps for no reason

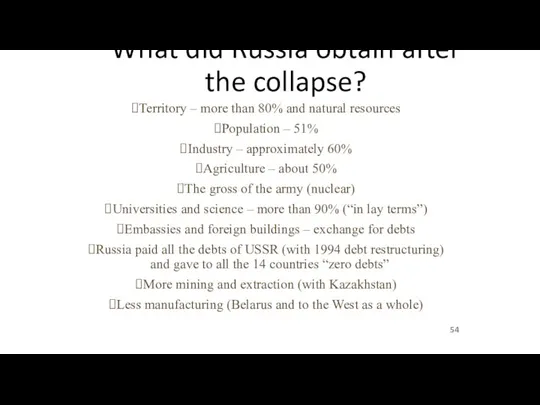

- 25. What did Russia obtained after the collapse? Territory – more than 80% and natural resources Population

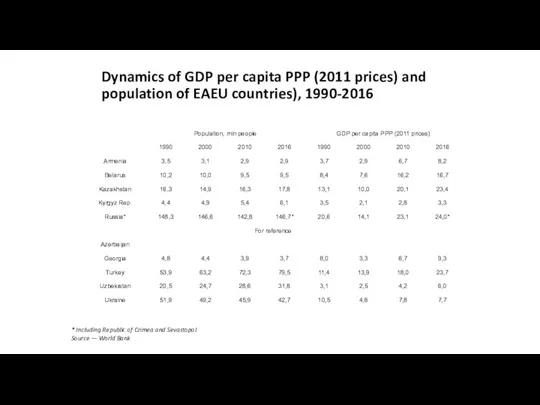

- 26. Dynamics of GDP per capita PPP (2011 prices) and population of EAEU countries), 1990-2016 * Including

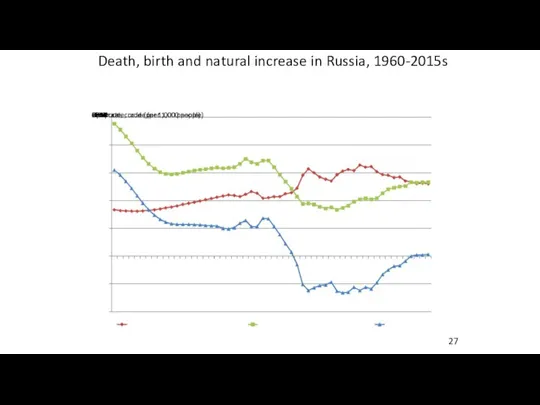

- 27. Death, birth and natural increase in Russia, 1960-2015s 27

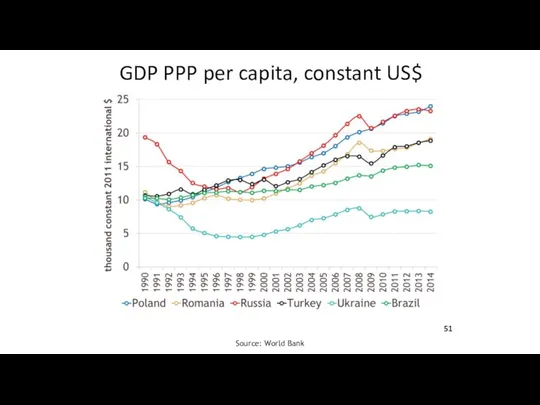

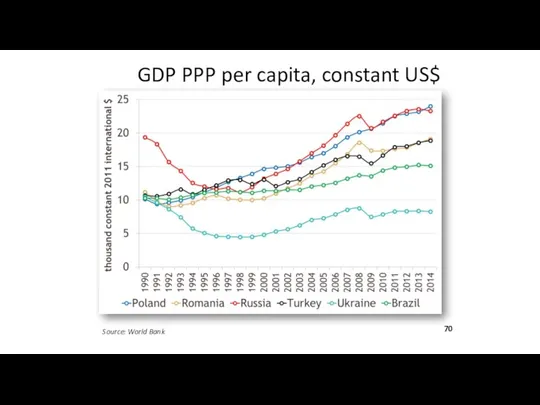

- 28. Source: World Bank GDP PPP per capita, constant US$

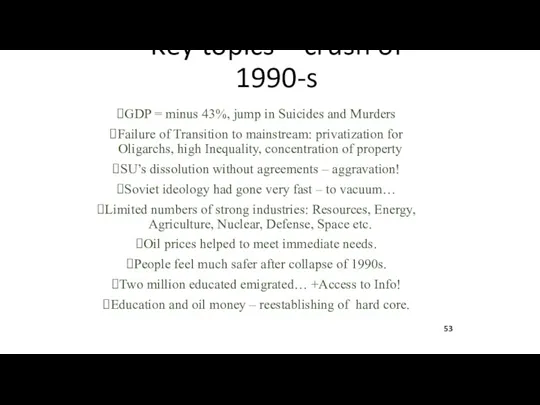

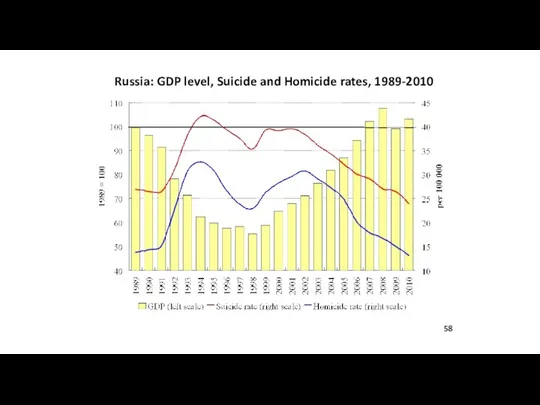

- 29. Key topics – crush of 1990-s GDP = minus 43%, jump in Suicides and Murders Failure

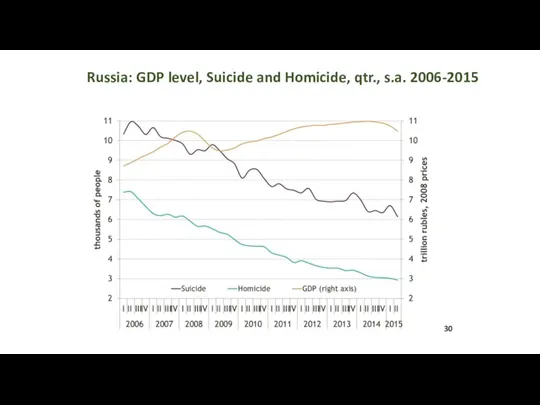

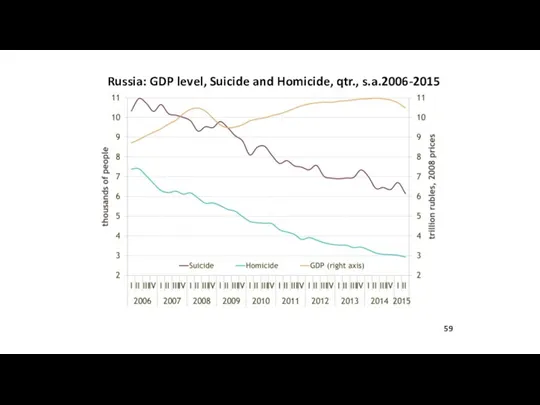

- 30. Russia: GDP level, Suicide and Homicide, qtr., s.a. 2006-2015

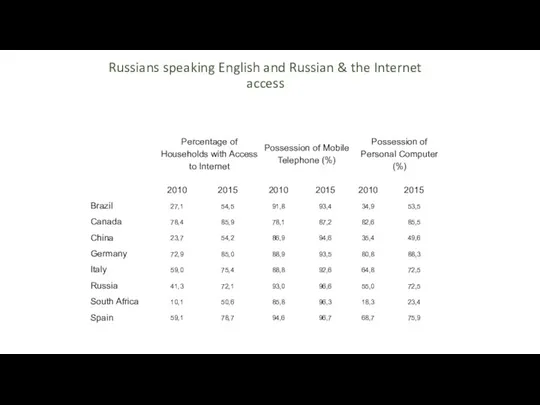

- 31. Russians speaking English and Russian & the Internet access

- 32. Society after 1/4 Century of Transition Current Russian Socio-economic realty is the result partly of Soviet

- 33. Key topics – Cold war in minds of Elites Russians never lost Cold War, better forget

- 34. Trap of the middle level development? The «500 days» program 1990; attempts of 1991; IMF and

- 35. Leonid Grigoryev – some publications Elites - the Choice for Modernization in “Russia: the Challenges of

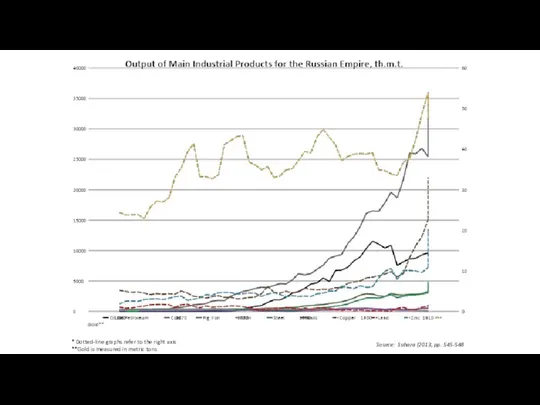

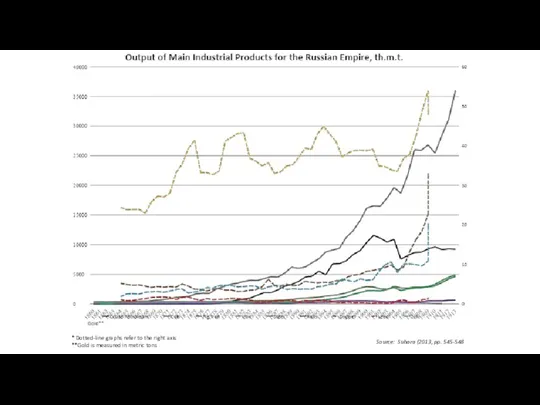

- 36. * Dotted-line graphs refer to the right axis **Gold is measured in metric tons Source: Suhara

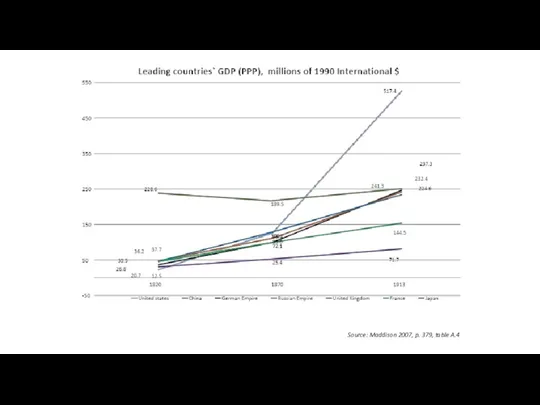

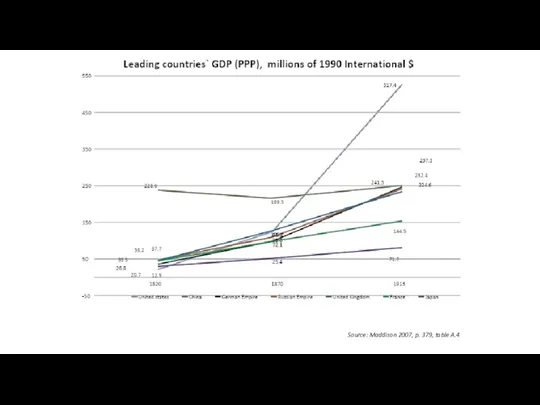

- 37. Source: Maddison 2007, p. 379, table A.4

- 38. Literature, basic: 1. Mau V., Drobyshevskaya T. "Modernization and the Russian Economy: Three Hundred Years of

- 39. Transformations of 1917-2018 (ideology, ownership, country’s configuration) and objective reasons for problems. 21.01.2019 Professor Leonid Grigoryev,

- 40. Topics for discussion: Russian in 1913 – Development V Institutions European politics and WWI WWI –

- 41. History Millennium+ with no peace, regular invasions Normans, Byzantium, Nomads before Mongols Big wars – Borders

- 42. The Empire Map

- 43. Periods of Russian History in XX-XXI C Tsar Nikolai II – till 1917 Revolution and Civil

- 44. Source: Maddison 2007, p. 379, table A.4

- 45. * Dotted-line graphs refer to the right axis **Gold is measured in metric tons Source: Suhara

- 46. Real national income per head, 1913 to 1927/28: year-on-year percent change on Soviet territory and at

- 47. Postwar recovery: The GDPs of selected Eurasian countries in 1928, percent of 1913 31 Source: Markevich

- 48. European Empires and Unions Empires were established by ”cool” adventurers followed by “Boyars and Streltsy” =

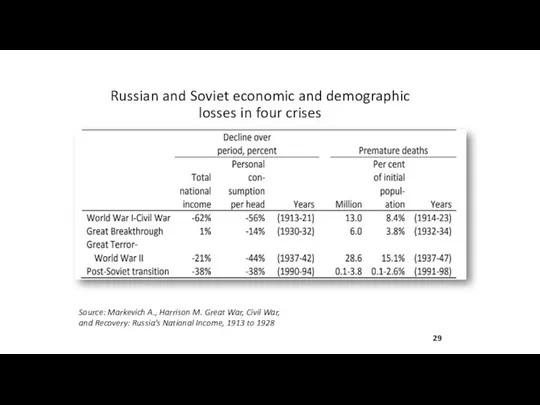

- 49. Russian and Soviet economic and demographic losses in four crises Source: Markevich A., Harrison M. Great

- 50. 1990 - 2018 Three Transformations: State configuration Politics and ideology Ownership Steps of 1992: free trade,

- 51. Source: World Bank GDP PPP per capita, constant US$

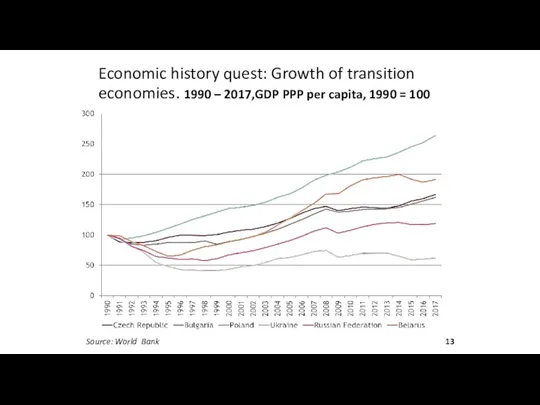

- 52. Source: World Bank Economic history quest: Growth of transition economies. 1990 – 2017,GDP PPP per capita,

- 53. Key topics – crush of 1990-s GDP = minus 43%, jump in Suicides and Murders Failure

- 54. What did Russia obtain after the collapse? Territory – more than 80% and natural resources Population

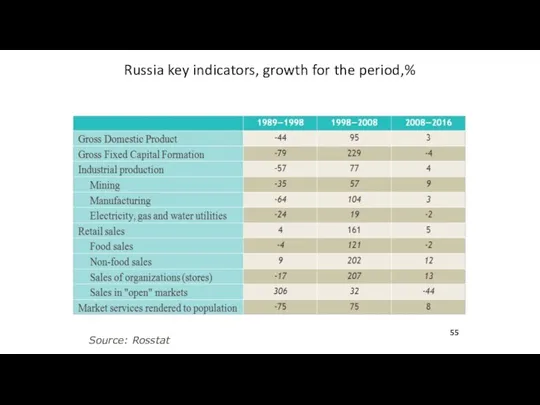

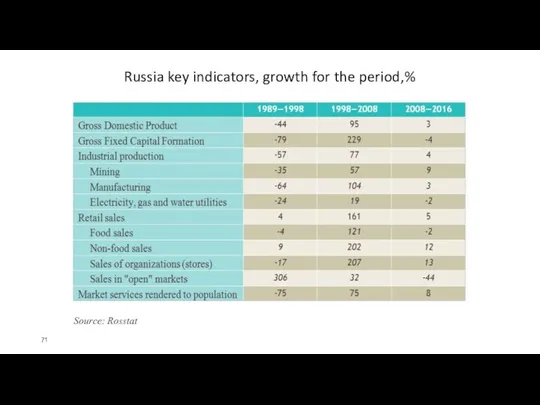

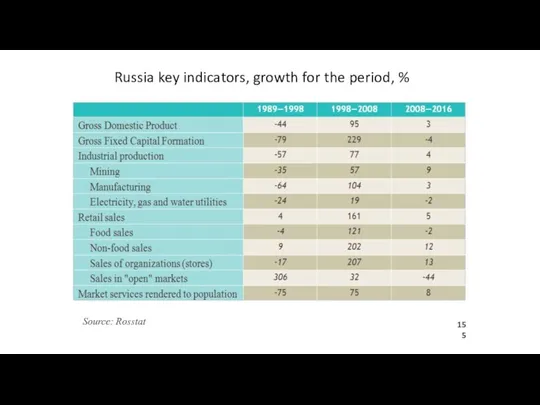

- 55. Russia key indicators, growth for the period,% Source: Rosstat

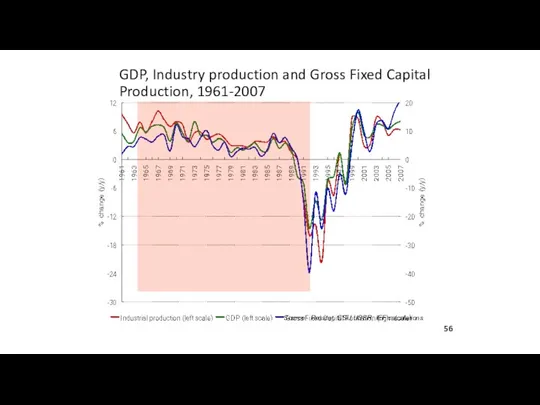

- 56. GDP, Industry production and Gross Fixed Capital Production, 1961-2007 Source: Rosstat, CSU USSR, IEF calculations

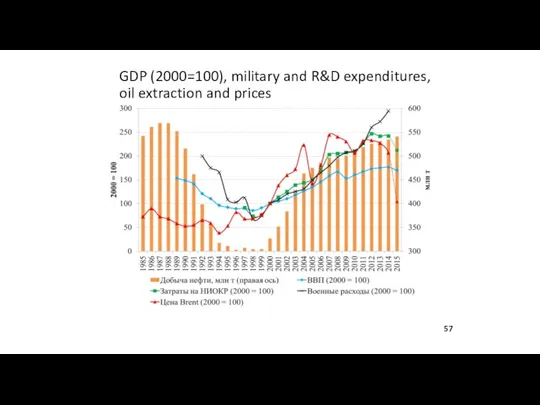

- 57. GDP (2000=100), military and R&D expenditures, oil extraction and prices

- 58. Russia: GDP level, Suicide and Homicide rates, 1989-2010

- 59. Russia: GDP level, Suicide and Homicide, qtr., s.a.2006-2015

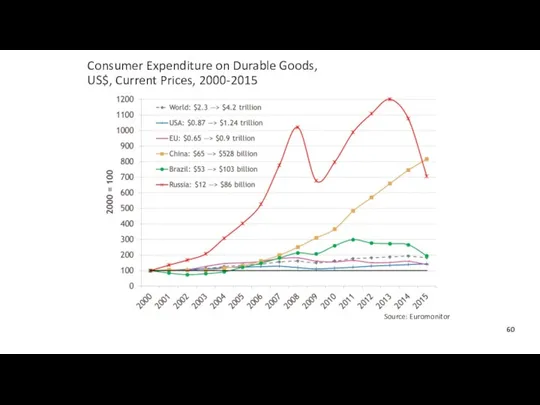

- 60. Consumer Expenditure on Durable Goods, US$, Current Prices, 2000-2015 Source: Euromonitor

- 61. Society after 1/4 Century of Transition Current Russian Socio-economic realty is the result partly of Soviet

- 62. Key topics – Cold war in minds of Elites Russians never lost Cold War, better forget

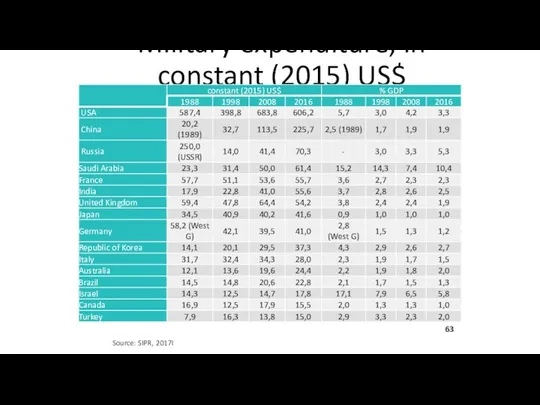

- 63. Military expenditure, in constant (2015) US$ Source: SIPR, 2017I

- 64. Russians know English and Russian & got access

- 65. Logic of this Presentation Objective problem of Russian history and institutions with limited information and prejudices

- 66. Ratio of GDP per capita of the USSR/Russia to the USA Russia/USA USSR/USA

- 67. Literature: “Transition to Market Economy” (in collaboration), Moscow, 1990, a.k.a. "500 days. Transition to the Market",

- 68. Russia - transformations of 1990-2018 Privatization and Ownership and corporate governance "Even God cannot change the

- 69. No warning for the People of the USSR "No leader has yet had the courage to

- 70. Source: World Bank GDP PPP per capita, constant US$

- 71. Russia key indicators, growth for the period,% Source: Rosstat

- 72. Key topics – crush of 1990-s GDP = minus 43%, jump in Suicides and Murders Failure

- 73. Transformation Debates 1987-1992 1987 – "ECO" = 70 years since 1917; Aganbegian, Kornai, Gaidar, Yasin –

- 74. "Soviets need a unified Free Economy" (1/2) Leonid Grigoriev – New York Times: 12 Sept. 1991

- 75. "Soviets need a unified Free Economy" (2/2) Leonid Grigoriev – New York Times: 12 Sept. 1991

- 76. Global Choice of privatization To privatize: Lands, houses, infrastructure, firms, natural resources, financial assets, human capital

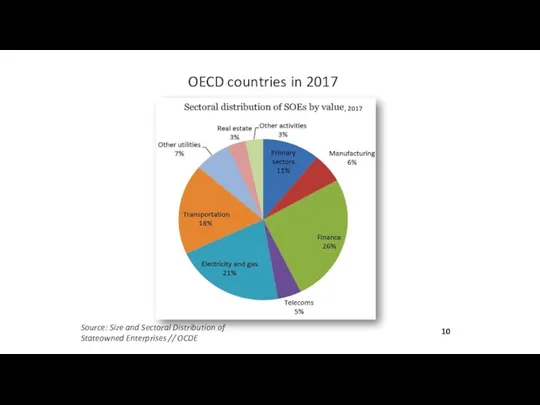

- 77. OECD countries in 2017 Source: Size and Sectoral Distribution of Stateowned Enterprises // OCDE 10

- 78. 1990 - 2018 Three Transformations State configuration = dissolution of the USSR into 15 Politics and

- 79. Ronald Сoase and transaction costs Stigler 1966: "the Coase theorem thus asserts that under perfect competition

- 80. Bundle of Rights – Honore 1961 – Ownership (1/2) (1) The Right to Possess: The right

- 81. Bundle of Rights – Honore 1961 – Ownership (2/2) (3) Right to manage is the right

- 82. Privatization and Choice of Objectives Interests in Privatization differ: Nation – soft transition to new institutes

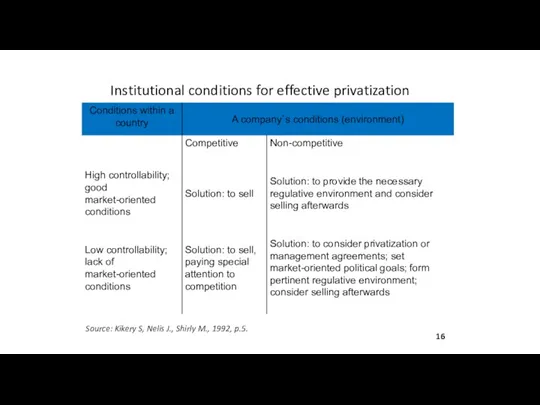

- 83. Institutional conditions for effective privatization Source: Kikery S, Nelis J., Shirly M., 1992, p.5. 16

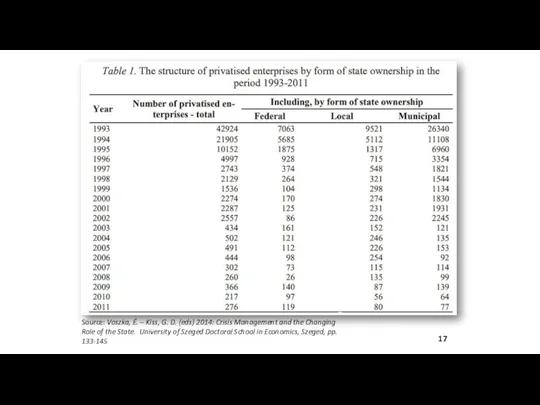

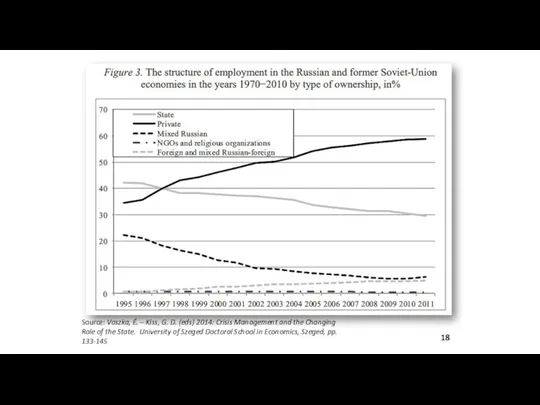

- 84. 17 Source: Voszka, É. – Kiss, G. D. (eds) 2014: Crisis Management and the Changing Role

- 85. Source: Voszka, É. – Kiss, G. D. (eds) 2014: Crisis Management and the Changing Role of

- 86. Share of public SOE`s in total employment, 2012 (%) 19

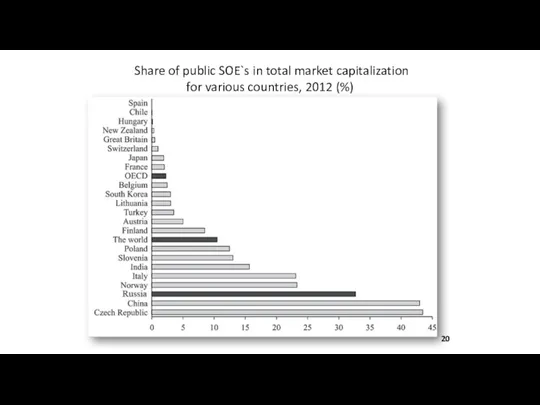

- 87. Share of public SOE`s in total market capitalization for various countries, 2012 (%) 20

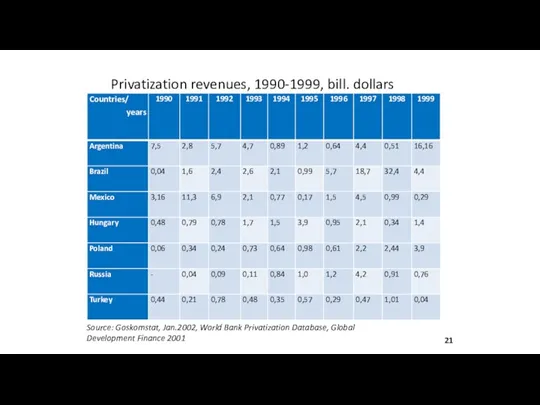

- 88. Privatization revenues, 1990-1999, bill. dollars Source: Goskomstat, Jan.2002, World Bank Privatization Database, Global Development Finance 2001

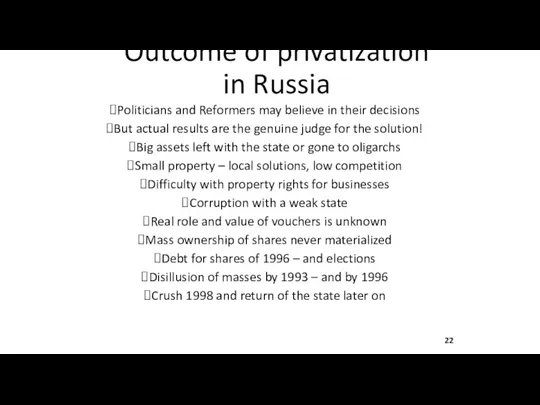

- 89. Outcome of privatization in Russia Politicians and Reformers may believe in their decisions But actual results

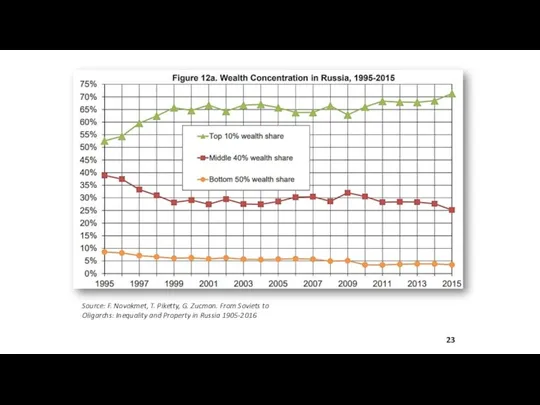

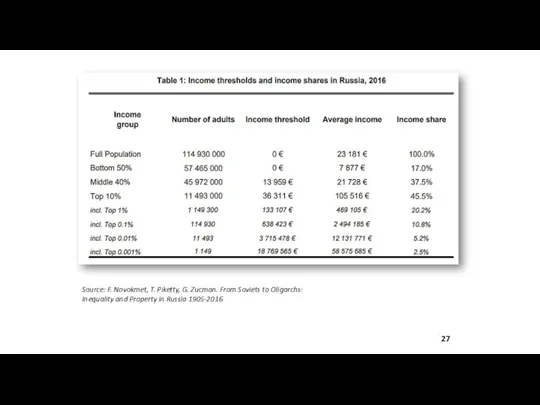

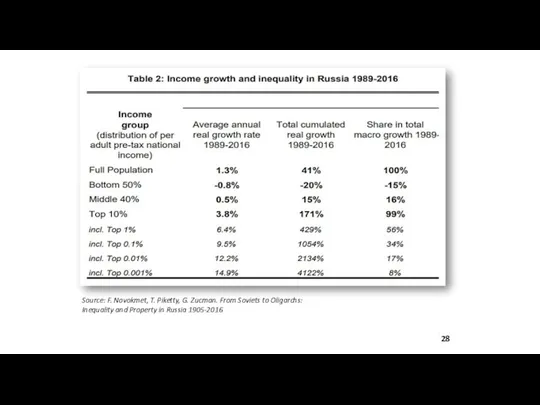

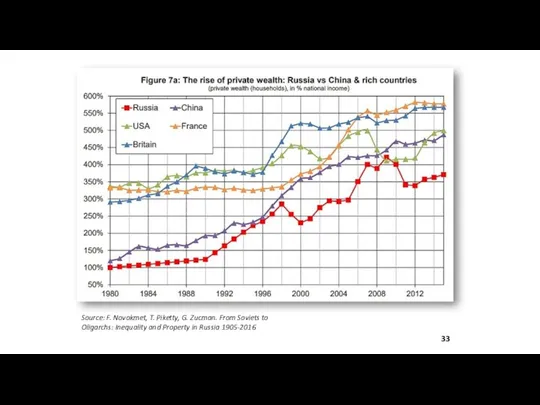

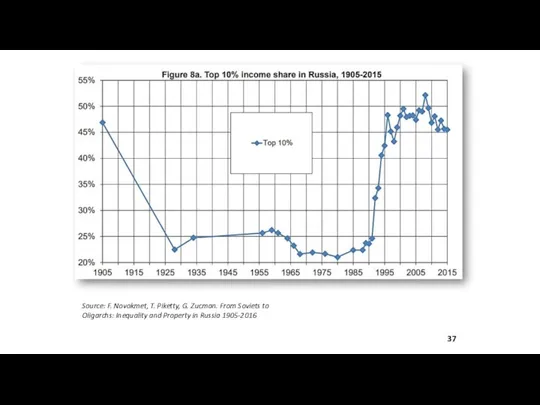

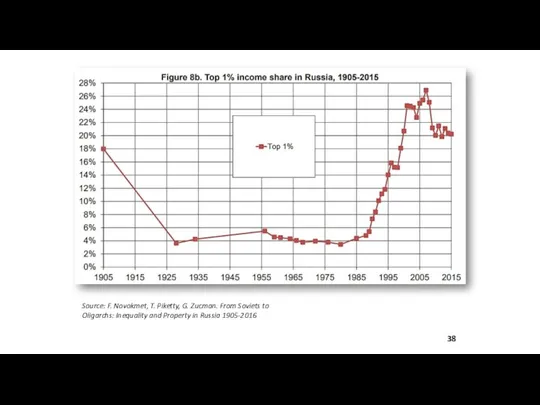

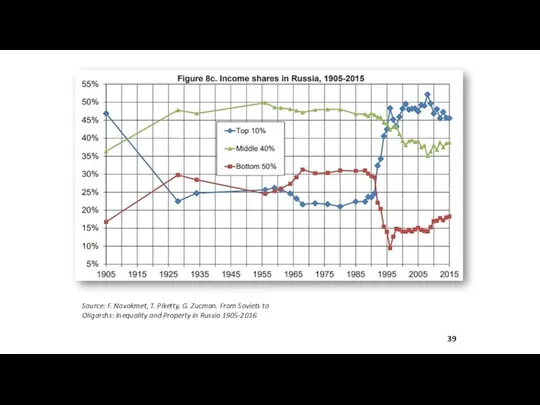

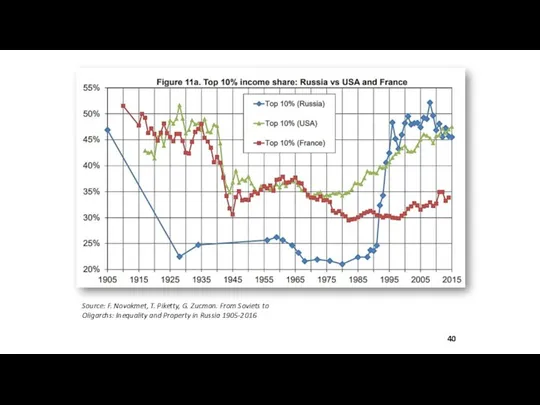

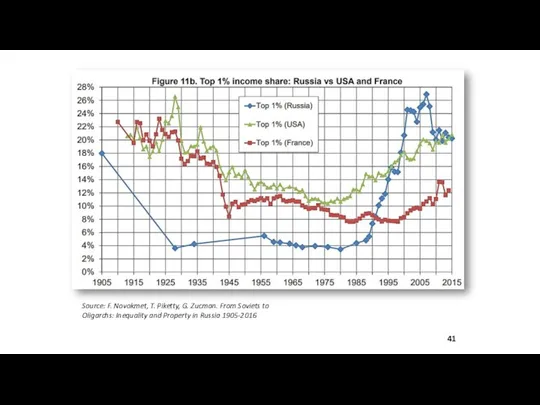

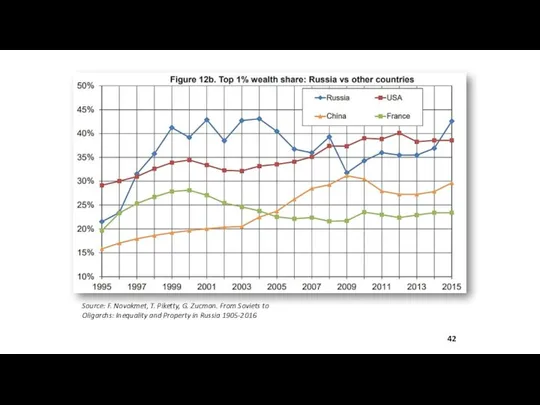

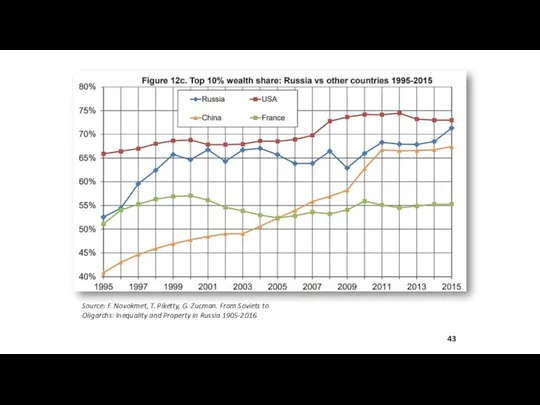

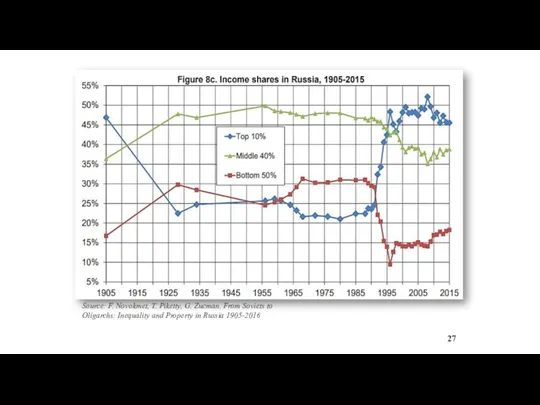

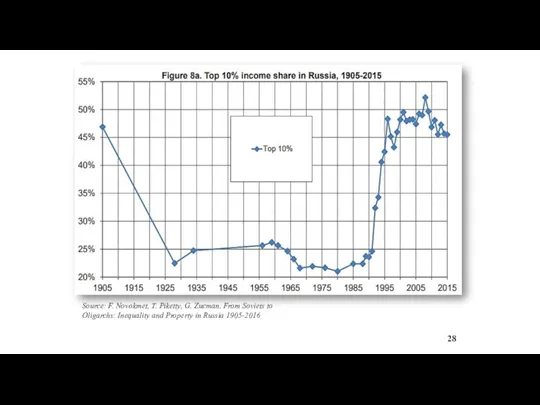

- 90. Source: F. Novokmet, T. Piketty, G. Zucman. From Soviets to Oligarchs: Inequality and Property in Russia

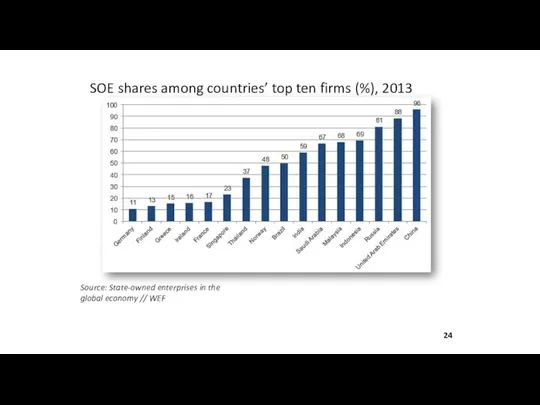

- 91. SOE shares among countries’ top ten firms (%), 2013 Source: State-owned enterprises in the global economy

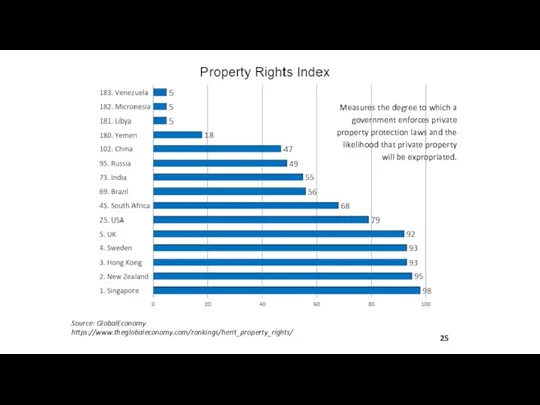

- 92. Source: GlobalEconomy https://www.theglobaleconomy.com/rankings/herit_property_rights/ Measures the degree to which a government enforces private property protection laws and

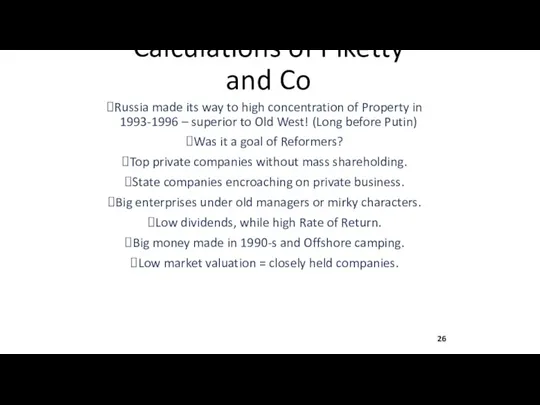

- 93. Calculations of Piketty and Co Russia made its way to high concentration of Property in 1993-1996

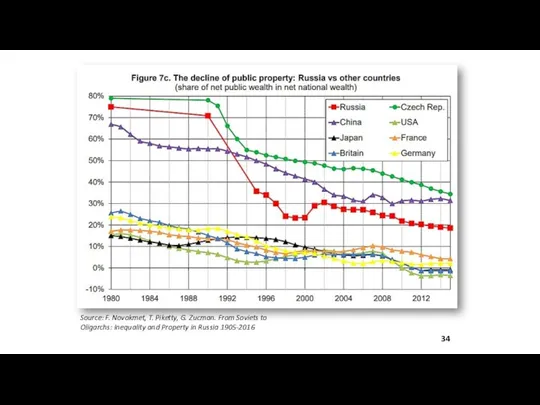

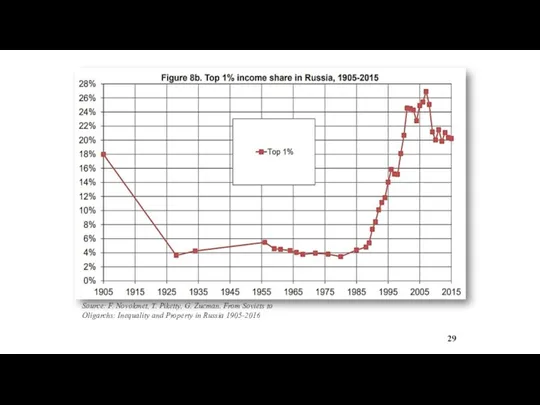

- 94. Source: F. Novokmet, T. Piketty, G. Zucman. From Soviets to Oligarchs: Inequality and Property in Russia

- 95. Source: F. Novokmet, T. Piketty, G. Zucman. From Soviets to Oligarchs: Inequality and Property in Russia

- 96. Source: F. Novokmet, T. Piketty, G. Zucman. From Soviets to Oligarchs: Inequality and Property in Russia

- 97. Source: F. Novokmet, T. Piketty, G. Zucman. From Soviets to Oligarchs: Inequality and Property in Russia

- 98. Source: F. Novokmet, T. Piketty, G. Zucman. From Soviets to Oligarchs: Inequality and Property in Russia

- 99. Source: F. Novokmet, T. Piketty, G. Zucman. From Soviets to Oligarchs: Inequality and Property in Russia

- 100. Source: F. Novokmet, T. Piketty, G. Zucman. From Soviets to Oligarchs: Inequality and Property in Russia

- 101. Source: F. Novokmet, T. Piketty, G. Zucman. From Soviets to Oligarchs: Inequality and Property in Russia

- 102. Byproducts of Wealth Distribution Inequality may be measured differently. Might have been a correct approach –

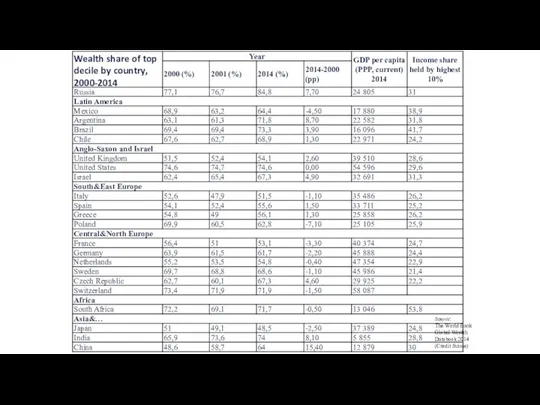

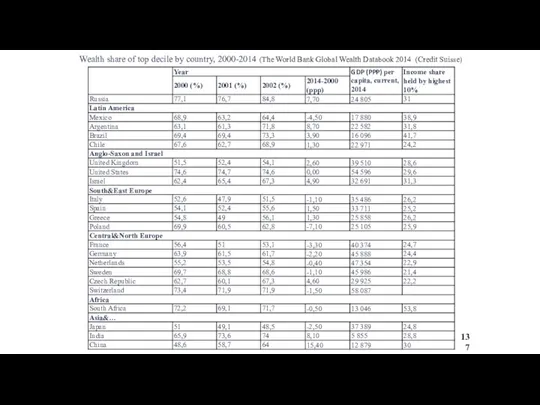

- 103. Source: The World Bank Global Wealth Databook 2014 (Credit Suisse) Wealth share of top decile by

- 104. Source: F. Novokmet, T. Piketty, G. Zucman. From Soviets to Oligarchs: Inequality and Property in Russia

- 105. Source: F. Novokmet, T. Piketty, G. Zucman. From Soviets to Oligarchs: Inequality and Property in Russia

- 106. Source: F. Novokmet, T. Piketty, G. Zucman. From Soviets to Oligarchs: Inequality and Property in Russia

- 107. Source: F. Novokmet, T. Piketty, G. Zucman. From Soviets to Oligarchs: Inequality and Property in Russia

- 108. Source: F. Novokmet, T. Piketty, G. Zucman. From Soviets to Oligarchs: Inequality and Property in Russia

- 109. Source: F. Novokmet, T. Piketty, G. Zucman. From Soviets to Oligarchs: Inequality and Property in Russia

- 110. Source: F. Novokmet, T. Piketty, G. Zucman. From Soviets to Oligarchs: Inequality and Property in Russia

- 111. Literature: Kornai Y. The Socialist System: The Political Economy of Communism. Oxford University Press, chapter 3,

- 112. Leonid Grigoryev – some publications Grigoryev L. "Ulterior Property Rights" (chapter) in "The Post-Soviet Economy". Edited

- 113. Global Structure Inequality: Income and Wealth (4.02. 2019) Tenured Professor Leonid Grigoryev Higher School of Economics,

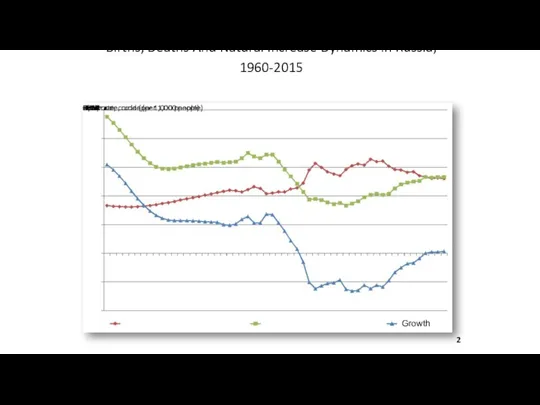

- 114. Births, Deaths And Natural Increase Dynamics in Russia, 1960-2015 2

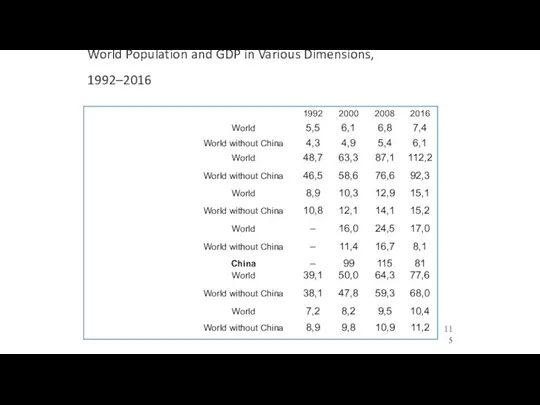

- 115. World Population and GDP in Various Dimensions, 1992–2016

- 116. Key points (1/2): Inequality between countries changes, Clusters go apart. Global economic growth has not changed

- 117. Key points (2/2): Domestic inequality is rigid, Growth is not changing distances for deciles. As we

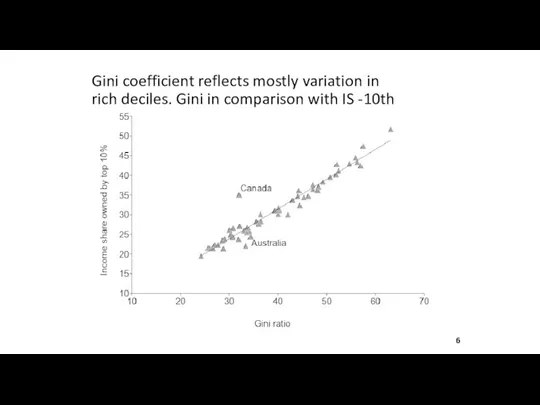

- 118. Gini coefficient reflects mostly variation in rich deciles. Gini in comparison with IS -10th 6

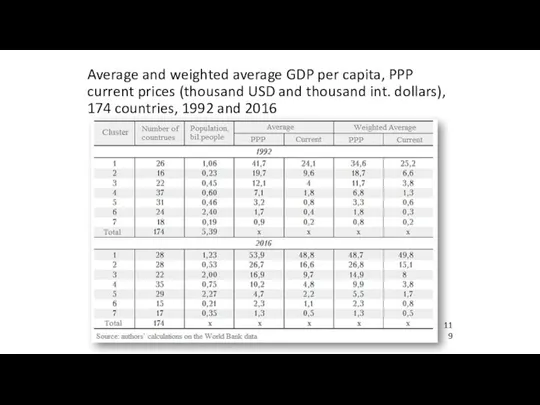

- 119. Average and weighted average GDP per capita, PPP current prices (thousand USD and thousand int. dollars),

- 120. UN sustainable development goal №10. Reduce inequalities (1/2) Socio-economic parameters of various countries, 2000 and 2013/14

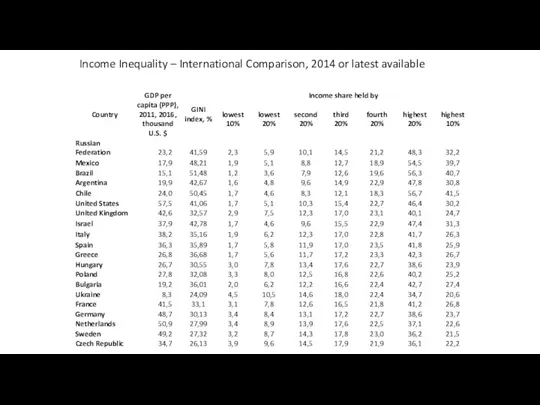

- 121. Income Inequality – International Comparison, 2014 or latest available

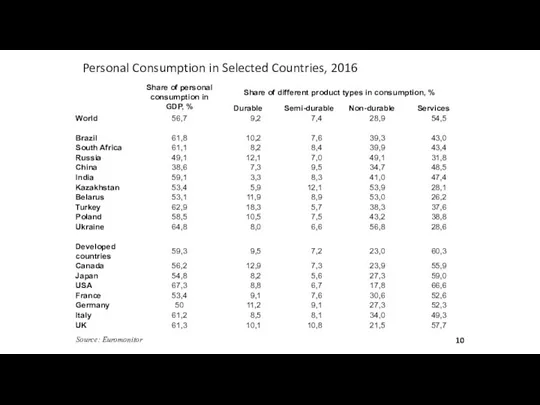

- 122. Personal Consumption in Selected Countries, 2016 Source: Euromonitor 10

- 123. Attitudes and Happiness Transformation has reduced expectations of state support. Not Russia is the center of

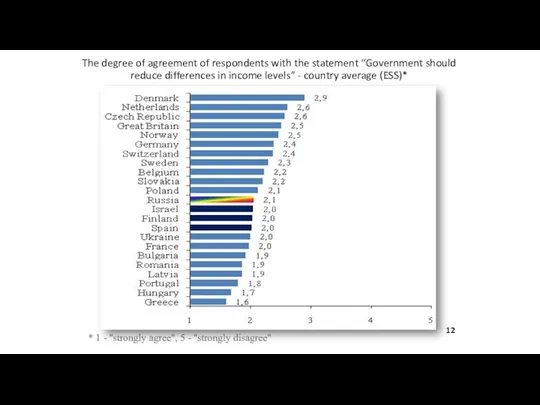

- 124. The degree of agreement of respondents with the statement “Government should reduce differences in income levels”

- 125. Level of life satisfaction in BRICS countries by income level, 1990-2014, % 13

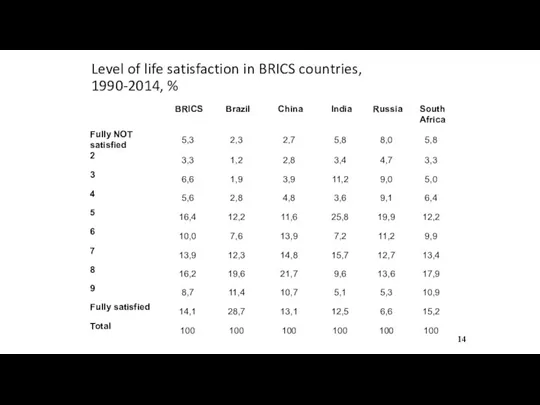

- 126. Level of life satisfaction in BRICS countries, 1990-2014, % 14

- 127. Access to Internet, mobile phone and personal computer usage, % households, 2010, 2015 15

- 128. Russia: from quasi egalitarian to? Yasin’s work of 2010: only top 20% are better off to

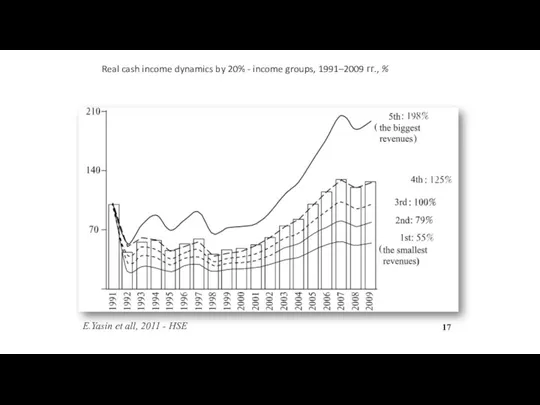

- 129. Real cash income dynamics by 20% - income groups, 1991–2009 гг., % E.Yasin et all, 2011

- 130. Re-stratification of the society I could not find a study of the “navigation” of social groups

- 131. Seven Stratas of Society Upper class – income, rent, etc.: (1) Upper upper and (2) Lower

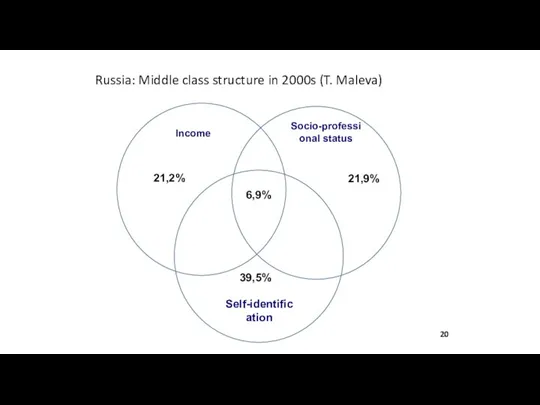

- 132. Russia: Middle class structure in 2000s (T. Maleva) 20

- 133. Dynamics of inequality in Russia (1/2) High social inequality in Russia has formed in the 1990s;

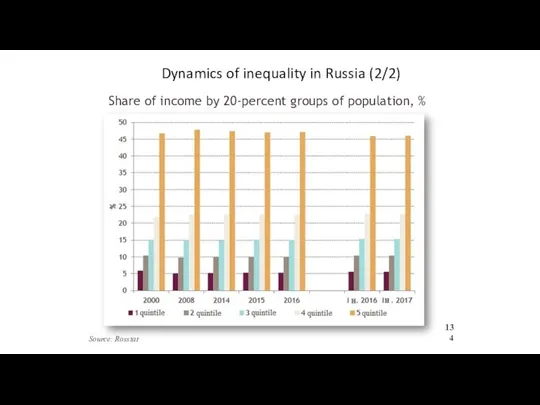

- 134. Dynamics of inequality in Russia (2/2) Share of income by 20-percent groups of population, % Source:

- 135. Transformation of society: features 10 years of economic decline (minus 43) lead to different cumulative degree

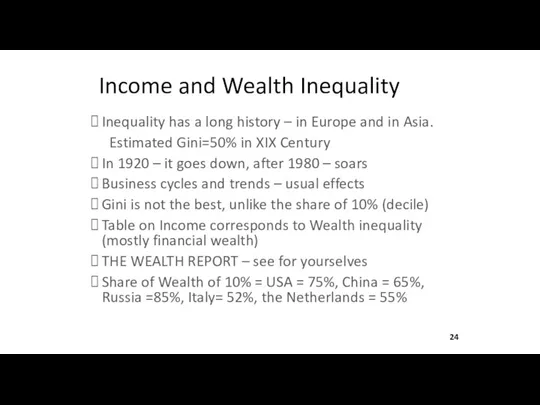

- 136. Income and Wealth Inequality Inequality has a long history – in Europe and in Asia. Estimated

- 137. Wealth share of top decile by country, 2000-2014 (The World Bank Global Wealth Databook 2014 (Credit

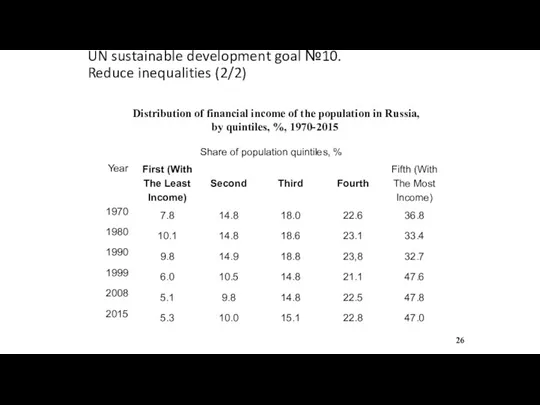

- 138. UN sustainable development goal №10. Reduce inequalities (2/2) Distribution of financial income of the population in

- 139. Source: F. Novokmet, T. Piketty, G. Zucman. From Soviets to Oligarchs: Inequality and Property in Russia

- 140. Source: F. Novokmet, T. Piketty, G. Zucman. From Soviets to Oligarchs: Inequality and Property in Russia

- 141. Source: F. Novokmet, T. Piketty, G. Zucman. From Soviets to Oligarchs: Inequality and Property in Russia

- 142. Conclusion: Russia Russia has made the detour from European income distribution to Latin American one. We

- 143. 31

- 144. Literature – 1 Atkinson Anthony “Inequality. What can be done?”, Cambridge, Harvard Un. Press, 2015. Grigoryev

- 145. Literature - 2 Григорьев Л.М, Павлюшина В.А. Социальное неравенство в мире и в России. Доклад о

- 146. Growth and Macro 11.02.2019 Professor Leonid Grigoryev HSE, Moscow www.leonidgrigoryev.com

- 147. Ratio of GDP per capita of the USSR/Russia to the USA Source: Maddison Project

- 148. Growth factors – long-run demand Infrastructure – roads and communications, Housing = new tendencies – two

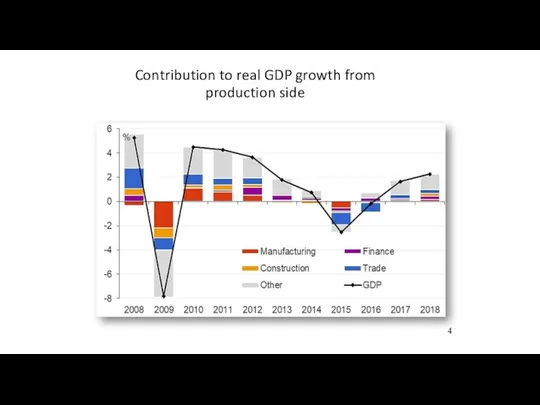

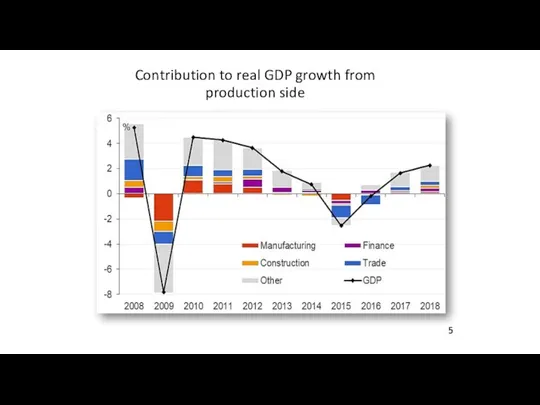

- 149. Contribution to real GDP growth from production side 4

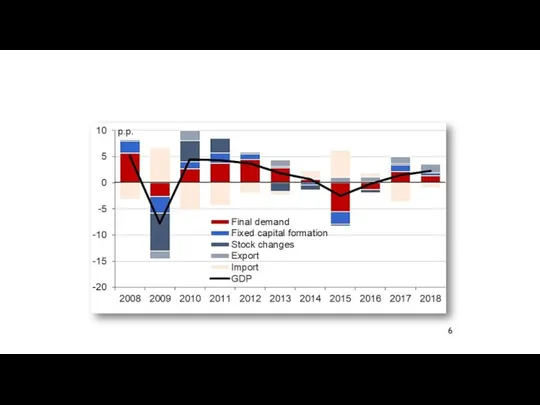

- 150. Contribution to real GDP growth from demand side 5

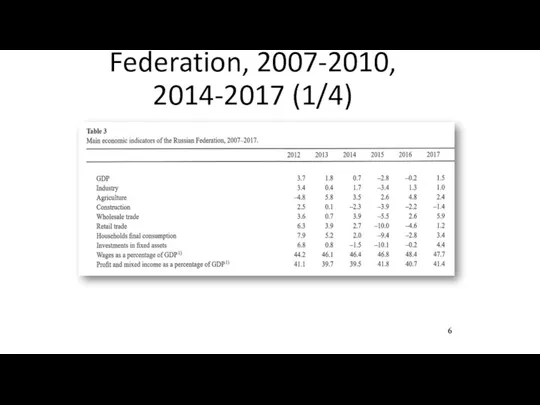

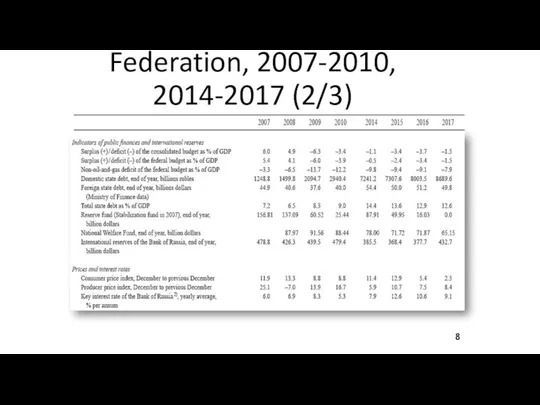

- 151. Main economic indicators of the Russian Federation, 2007-2010, 2014-2017 (1/4) 6

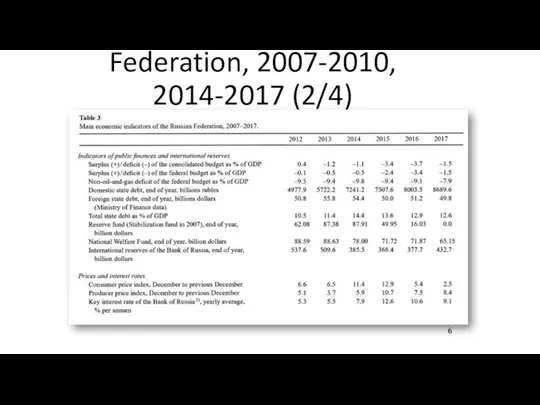

- 152. Main economic indicators of the Russian Federation, 2007-2010, 2014-2017 (2/4) 6

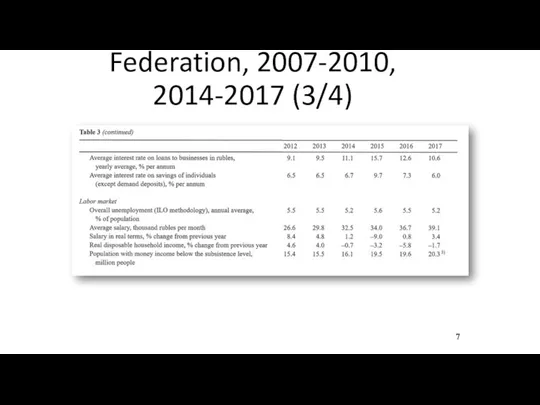

- 153. Main economic indicators of the Russian Federation, 2007-2010, 2014-2017 (3/4) 7

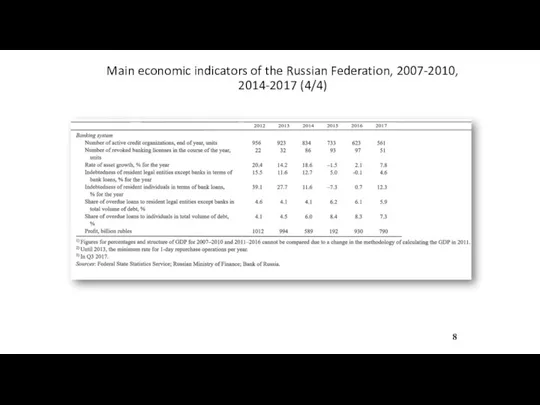

- 154. Main economic indicators of the Russian Federation, 2007-2010, 2014-2017 (4/4) 8

- 155. Russia key indicators, growth for the period, % Source: Rosstat

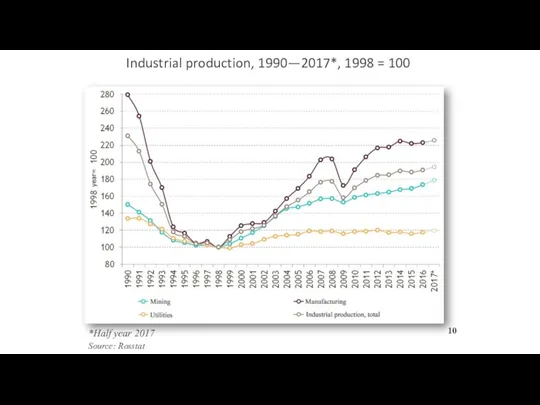

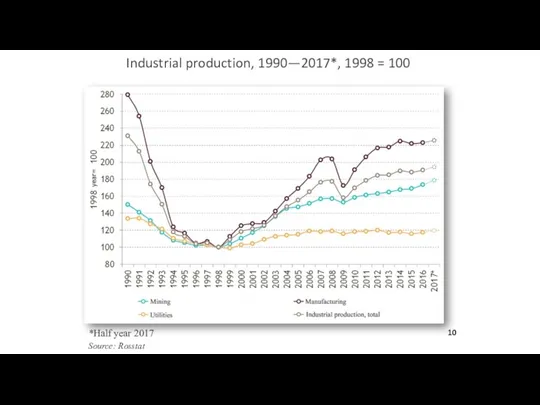

- 156. Industrial production, 1990—2017*, 1998 = 100 *Half year 2017 Source: Rosstat 10

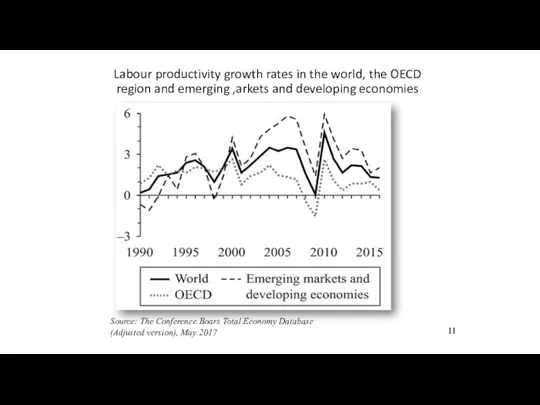

- 157. Labour productivity growth rates in the world, the OECD region and emerging ,arkets and developing economies

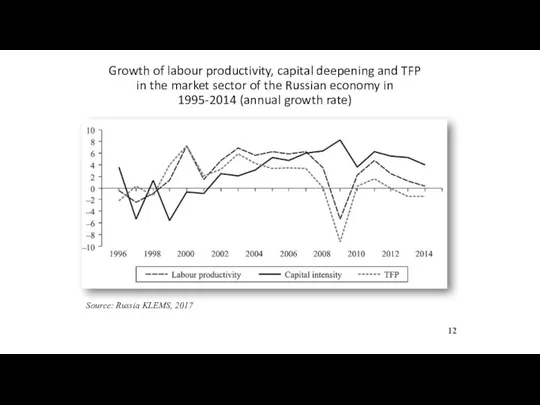

- 158. Growth of labour productivity, capital deepening and TFP in the market sector of the Russian economy

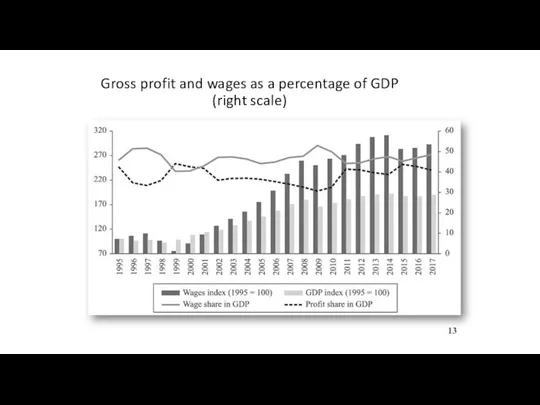

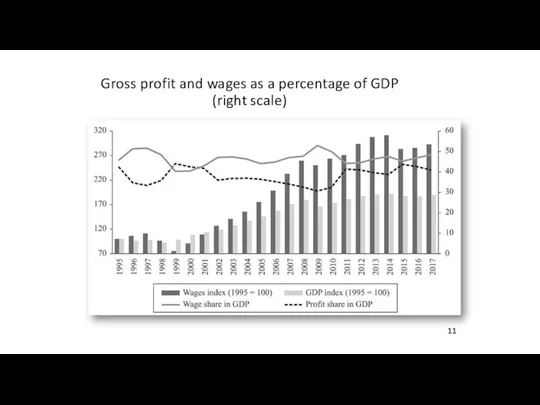

- 159. Gross profit and wages as a percentage of GDP (right scale) 13

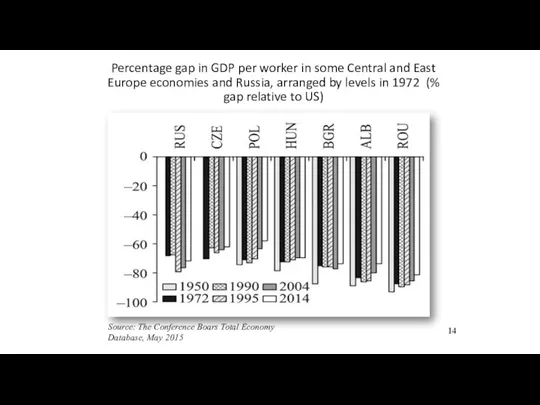

- 160. Percentage gap in GDP per worker in some Central and East Europe economies and Russia, arranged

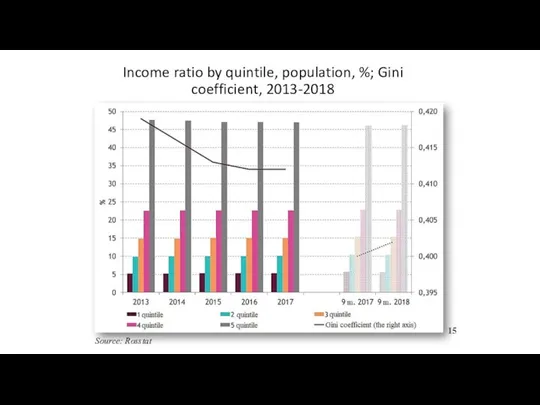

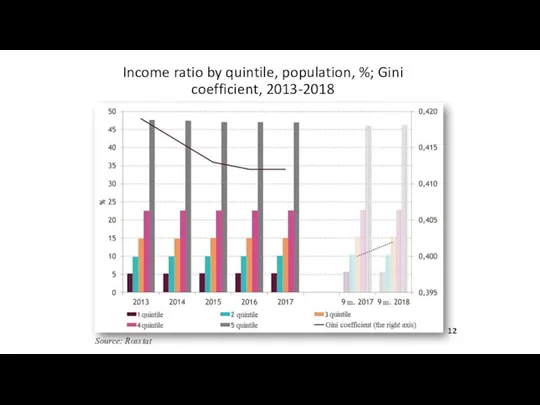

- 161. Income ratio by quintile, population, %; Gini coefficient, 2013-2018 Source: Rosstat 15

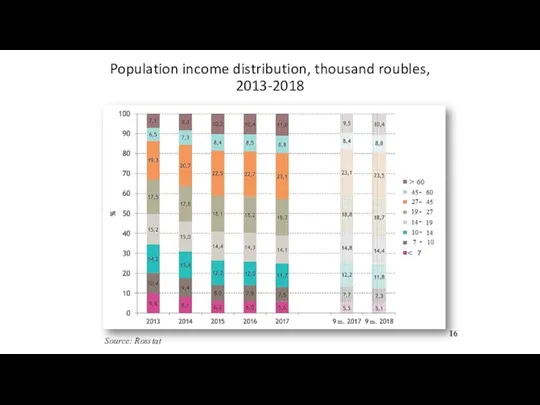

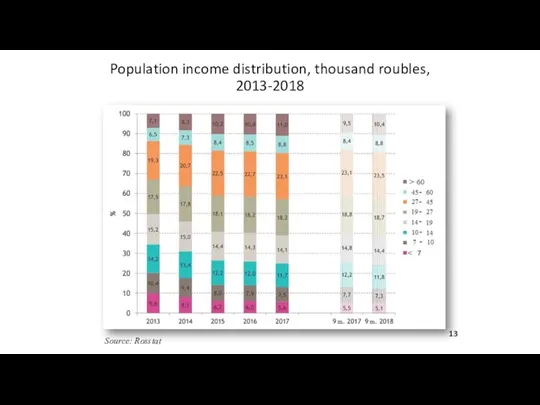

- 162. Population income distribution, thousand roubles, 2013-2018 Source: Rosstat 16

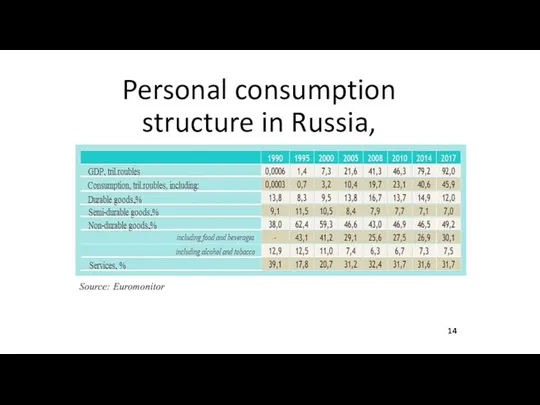

- 163. Personal consumption structure in Russia, 1990-2017 Source: Euromonitor 17

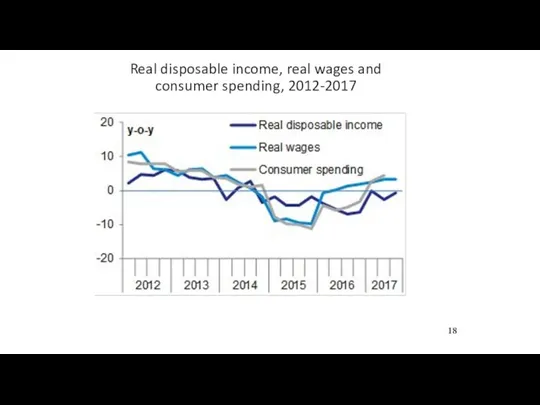

- 164. Real disposable income, real wages and consumer spending, 2012-2017 18

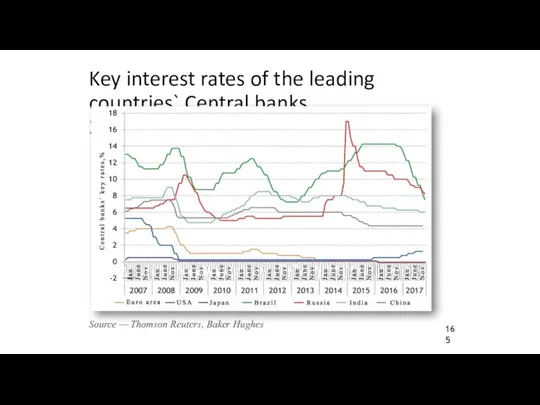

- 165. Key interest rates of the leading countries` Central banks, 2007–2017 Source — Thomson Reuters, Baker Hughes

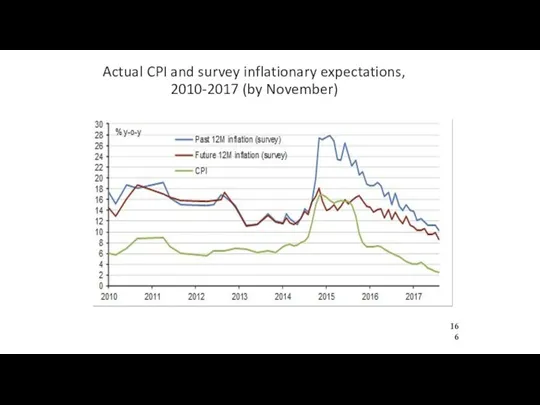

- 166. Actual CPI and survey inflationary expectations, 2010-2017 (by November)

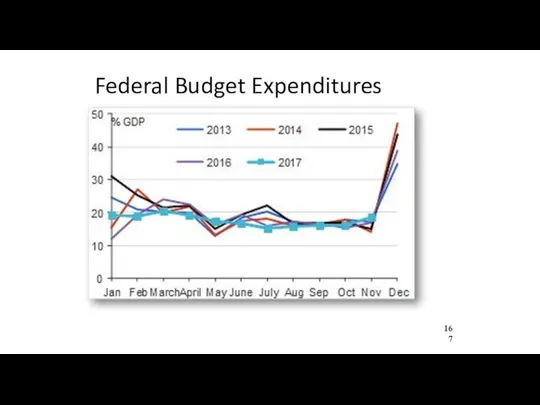

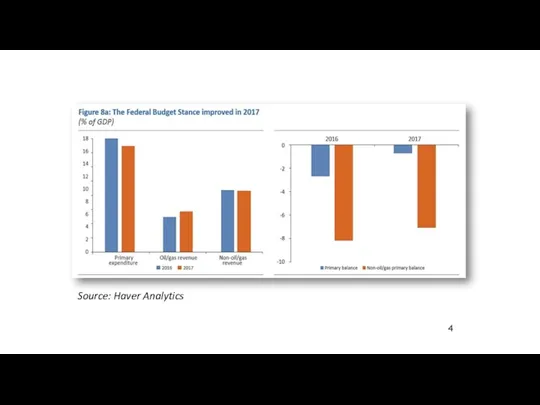

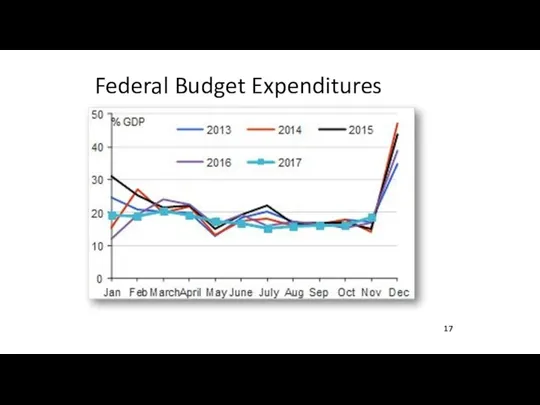

- 167. Federal Budget Expenditures

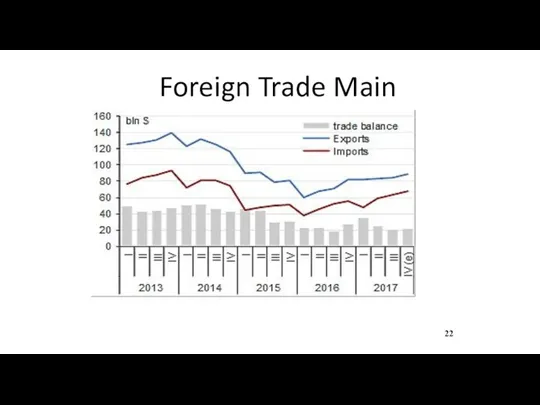

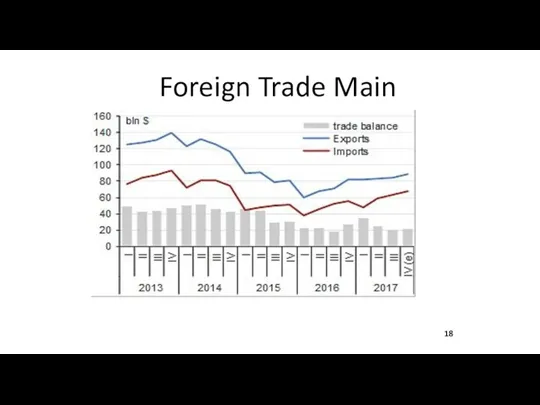

- 168. Foreign Trade Main Parameters 22

- 169. Military expenditure, in constant (2015) US$ Source: SIPR, 2017I

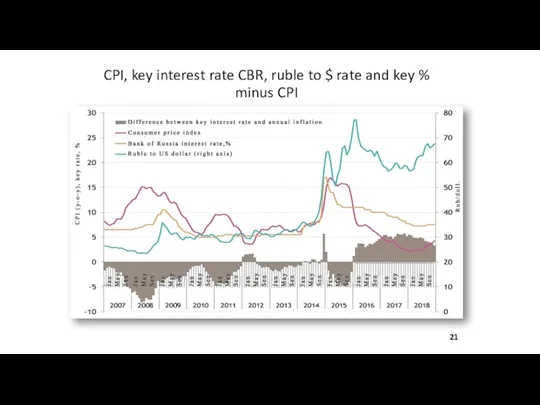

- 170. CPI, key interest rate CBR, ruble to $ rate and key % minus CPI 24

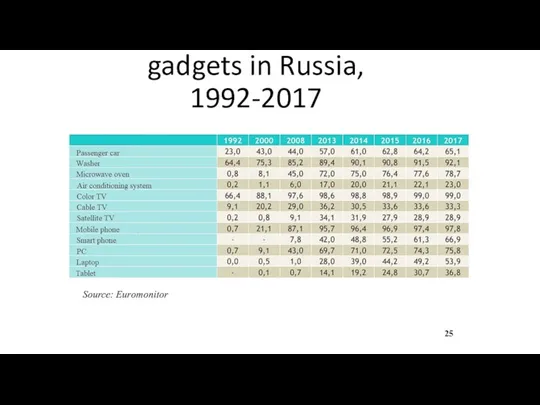

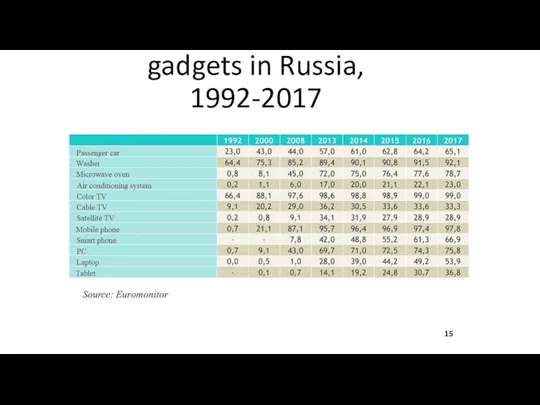

- 171. Share of households in possession of some household durables and gadgets in Russia, 1992-2017 Source: Euromonitor

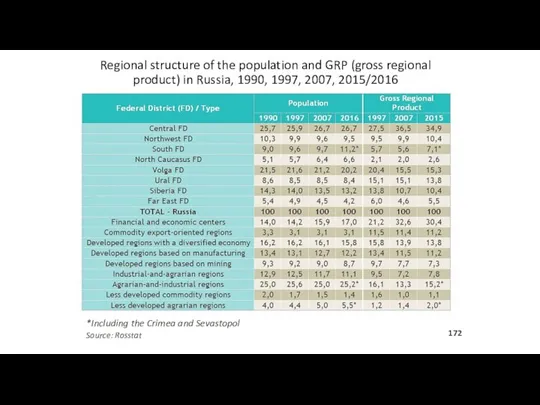

- 172. Regional structure of the population and GRP (gross regional product) in Russia, 1990, 1997, 2007, 2015/2016

- 173. Retail sales 2015-2016, per capita by type of regions Source: Rosstat, Analytical center calculations

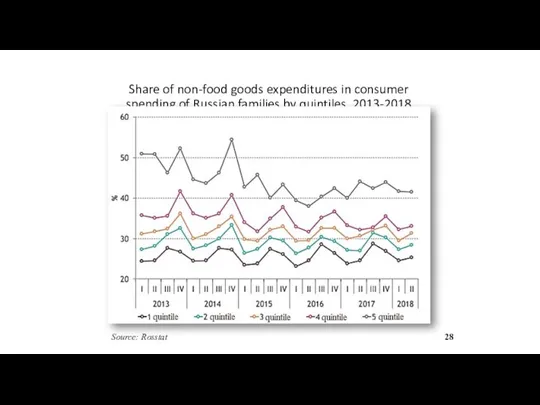

- 174. Share of non-food goods expenditures in consumer spending of Russian families by quintiles, 2013-2018 Source: Rosstat

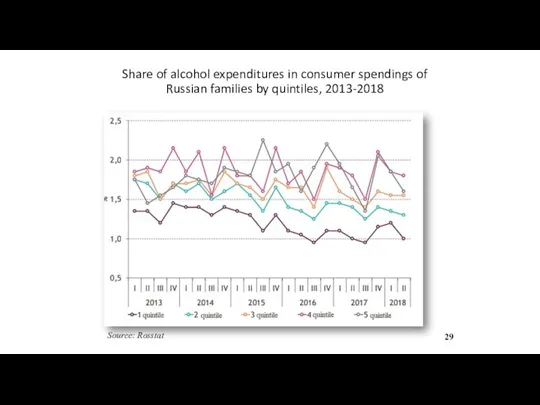

- 175. Share of alcohol expenditures in consumer spendings of Russian families by quintiles, 2013-2018 Source: Rosstat 29

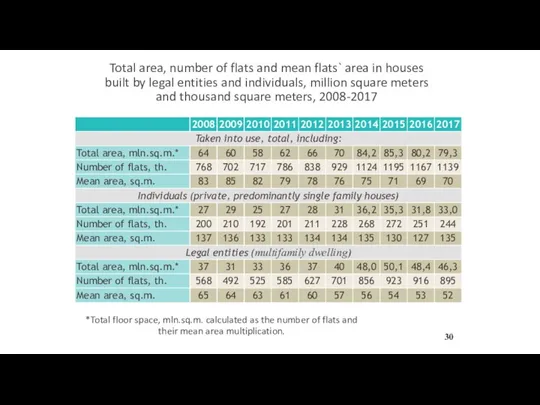

- 176. Total area, number of flats and mean flats` area in houses built by legal entities and

- 177. Recession and implications Recession is difficult for everybody Unofficial evaluations gave the loss of GDP to

- 178. Conclusion: Russia Russia has made the detour from European income distribution to Latin American one in

- 179. Literature: Voskoboynikov, I. "Sources of long run economic growth in Russia before and after the global

- 180. Professor Leonid Grigoryev www.leonidgrigoryev.com Economy & Energy 18.02.2019

- 181. Energy – history and theory Energy waves – replacement by efficiency, costs, for mass use of

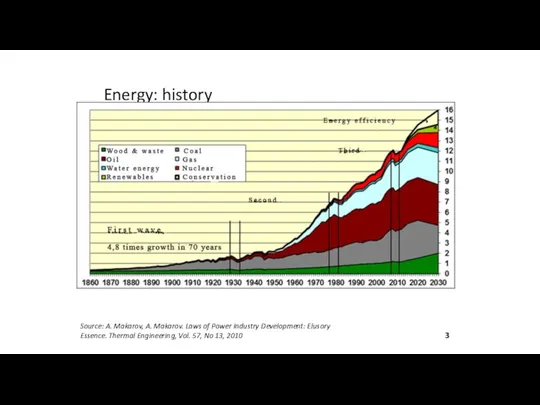

- 182. Energy: history Source: A. Makarov, A. Makarov. Laws of Power Industry Development: Elusory Essence. Thermal Engineering,

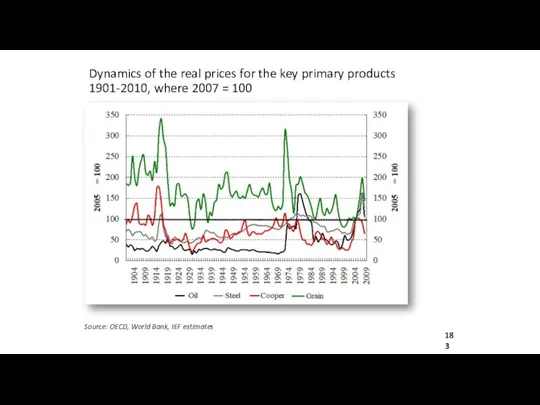

- 183. Dynamics of the real prices for the key primary products 1901-2010, where 2007 = 100 Source:

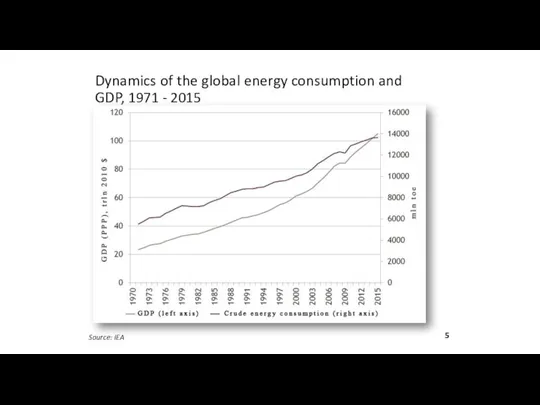

- 184. Dynamics of the global energy consumption and GDP, 1971 - 2015 Source: IEA 5

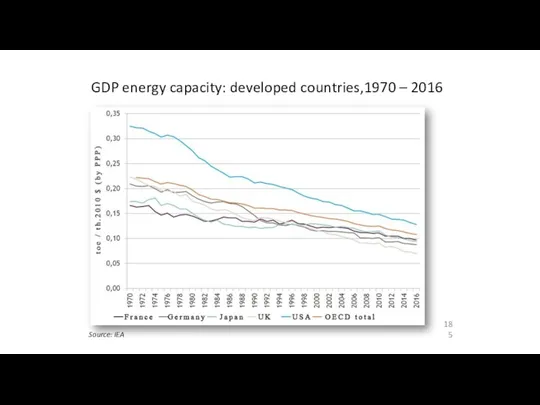

- 185. GDP energy capacity: developed countries,1970 – 2016 Source: IEA

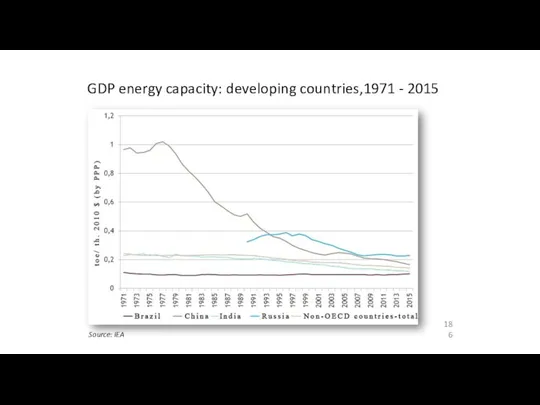

- 186. GDP energy capacity: developing countries,1971 - 2015 Source: IEA

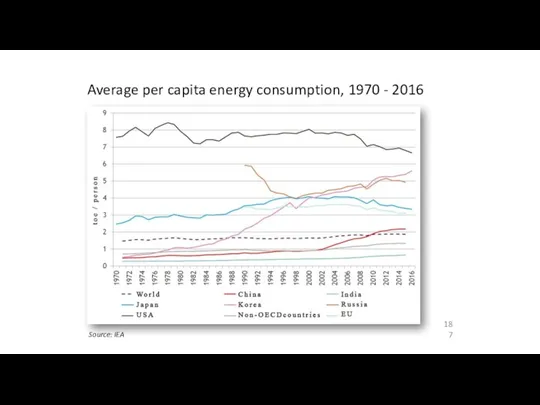

- 187. Average per capita energy consumption, 1970 - 2016 Source: IEA

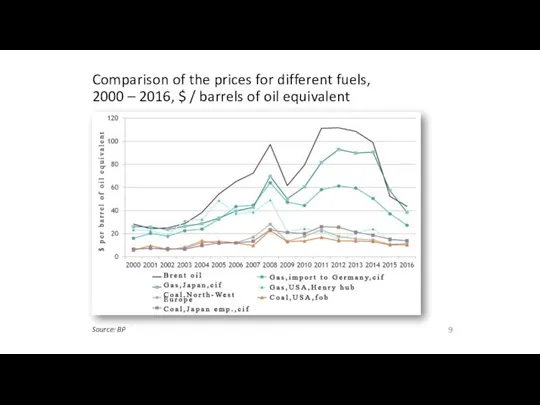

- 188. Comparison of the prices for different fuels, 2000 – 2016, $ / barrels of oil equivalent

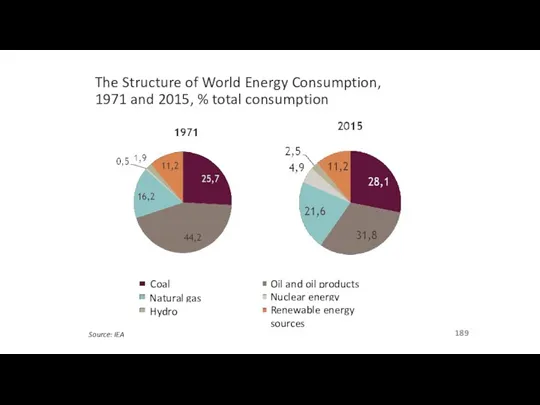

- 189. The Structure of World Energy Consumption, 1971 and 2015, % total consumption Source: IEA

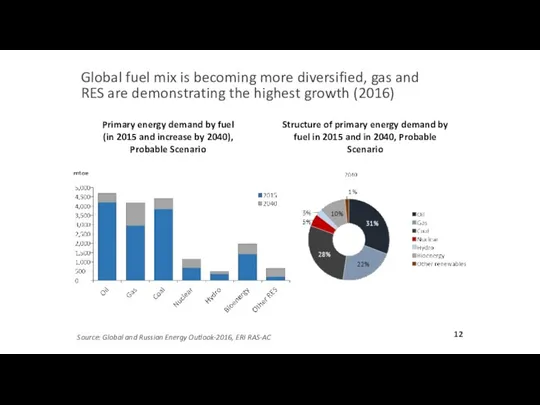

- 190. Primary energy demand by fuel (in 2015 and increase by 2040), Probable Scenario Source: Global and

- 191. Geopolitics & Rational Changes Growth and Energy consumption Embargo of Arab OPEC 1973 and Fear of

- 192. World GDP and Trade Growth rate, %, 1995‑2018 Source: IMF, WEO April 2017 Edition

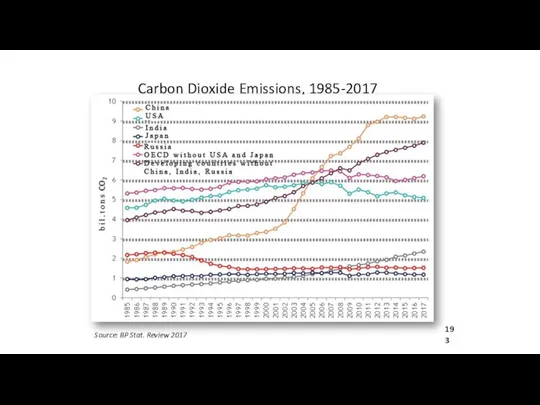

- 193. Carbon Dioxide Emissions, 1985-2017 Source: BP Stat. Review 2017

- 194. Geopolitics steps over trade, development and Global problems’ solutions World is losing stability but keeps talking

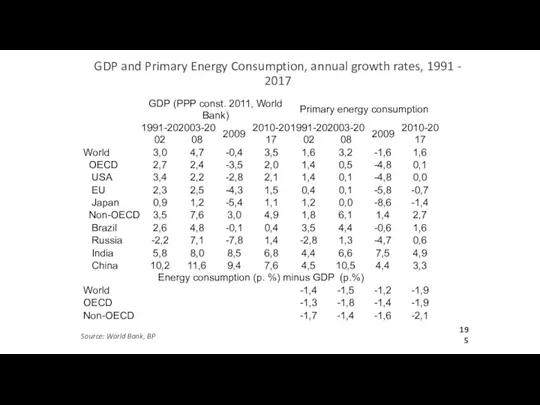

- 195. GDP and Primary Energy Consumption, annual growth rates, 1991 - 2017 Source: World Bank, BP

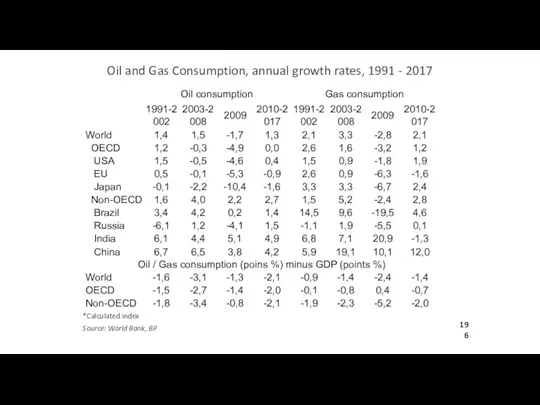

- 196. Oil and Gas Consumption, annual growth rates, 1991 - 2017 Source: World Bank, BP *Calculated index

- 197. Coal consumption and Electricity generation, annual growth rates, 1991 - 2017 Source: World Bank, BP *Calculated

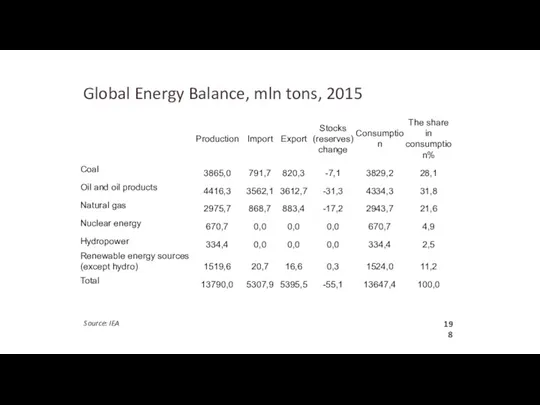

- 198. Global Energy Balance, mln tons, 2015 Source: IEA

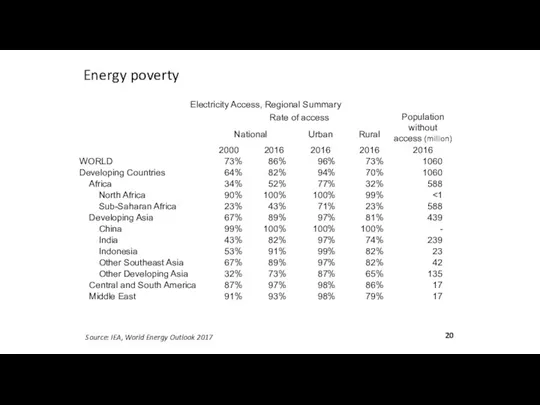

- 199. Energy poverty Source: IEA, World Energy Outlook 2017 20

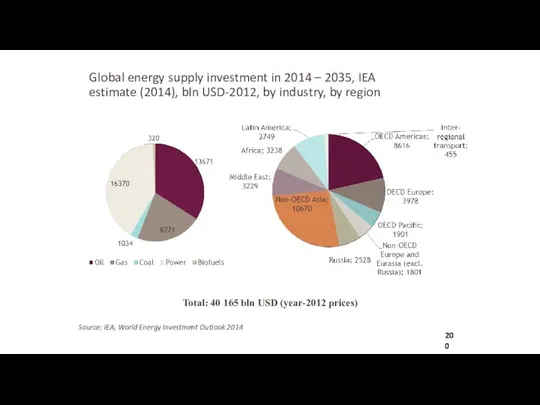

- 200. Global energy supply investment in 2014 – 2035, IEA estimate (2014), bln USD-2012, by industry, by

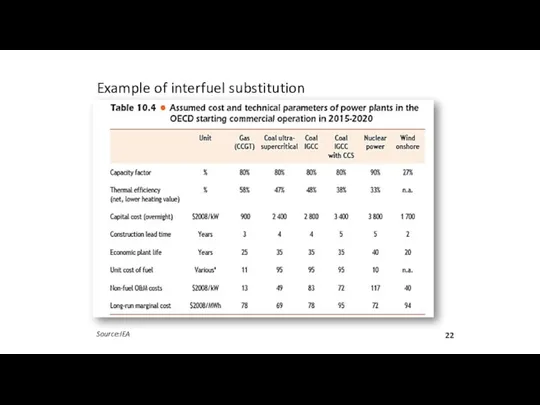

- 201. Example of interfuel substitution Source:IEA 22

- 202. OPEC & RUSSIA

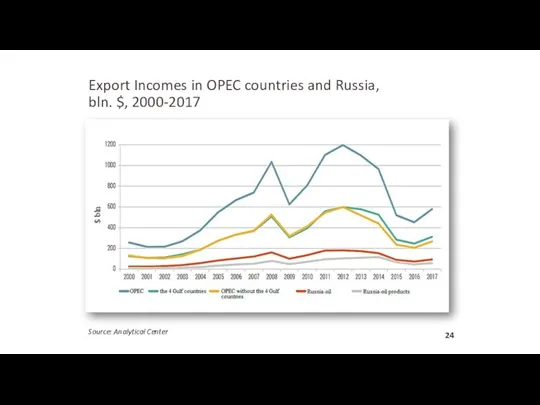

- 203. Export Incomes in OPEC countries and Russia, bln. $, 2000-2017 Source: Analytical Center 24

- 204. The acceptable price in budget leveraging, 2000-2017

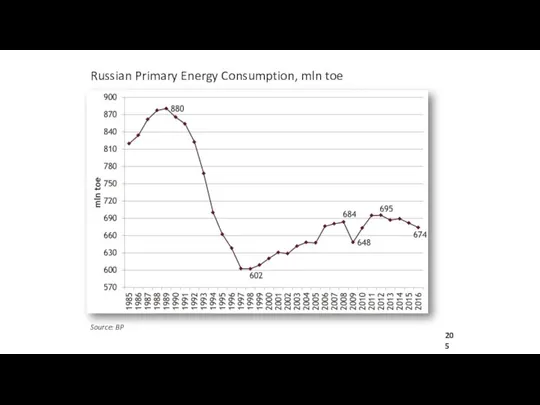

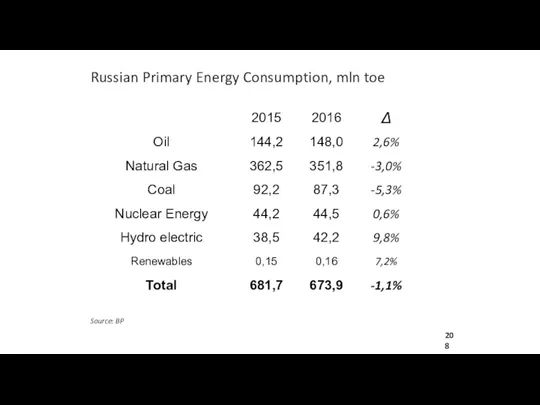

- 205. Source: BP Russian Primary Energy Consumption, mln toe

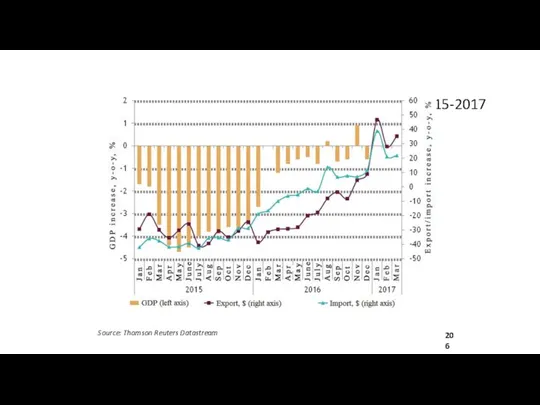

- 206. GDP, export and import of Russia, y/y, 2015-2017 Source: Thomson Reuters Datastream

- 207. Russian export of energy, mln toe Source: ERI RAS

- 208. Source: BP Russian Primary Energy Consumption, mln toe

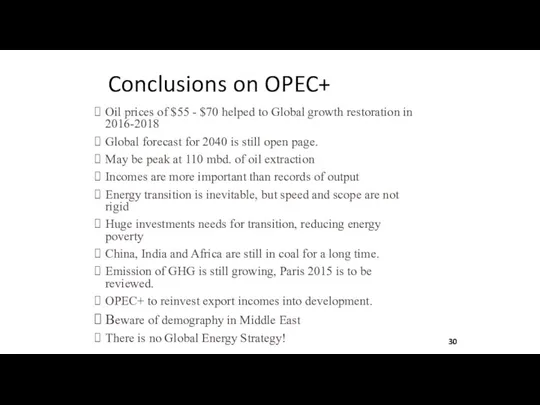

- 209. Conclusions on OPEC+ Oil prices of $55 - $70 helped to Global growth restoration in 2016-2018

- 210. World Energy Transition and Future World is undergoing Energy transition, but still not that fast as

- 211. Literature 1 Григорьев Л.М., Чапыгина А.В. «Саудовская Аравия – нефть и развитие», «Мировая Энергетическая политика», №7,

- 212. Literature 2 “Global and Russian Energy Outlook Up To 2040”, IES, RAS,2016 “Domestic Debates on Climate

- 213. Macro & 4.03.2019 Professor Leonid Grigoryev HSE, Moscow www.leonidgrigoryev.com

- 214. Upcoming events 4 of March – Macro light questions for students 11 of March – lecture

- 215. Ratio of GDP per capita of the USSR/Russia to the USA Source: Maddison Project

- 216. Growth factors – long-run demand Infrastructure – roads and communications, Housing = new tendencies – two

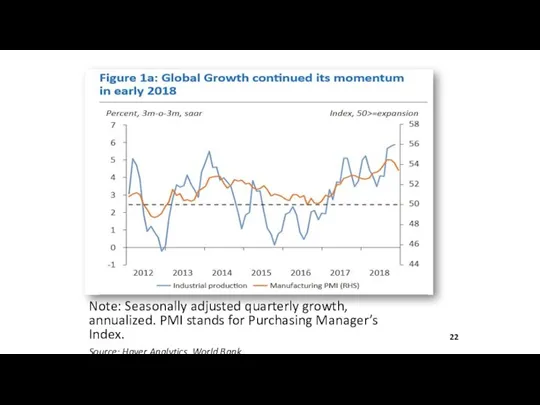

- 217. Source: Haver Analytics 4

- 218. Contribution to real GDP growth from production side 5

- 219. Contribution to real GDP growth from demand side 6

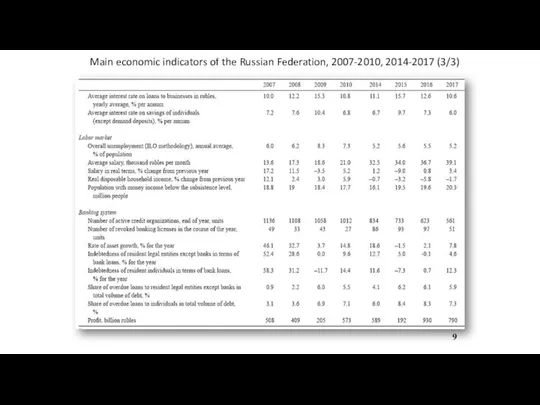

- 220. Main economic indicators of the Russian Federation, 2007-2010, 2014-2017 (1/3) 7

- 221. Main economic indicators of the Russian Federation, 2007-2010, 2014-2017 (2/3) 8

- 222. Main economic indicators of the Russian Federation, 2007-2010, 2014-2017 (3/3) 9

- 223. Industrial production, 1990—2017*, 1998 = 100 *Half year 2017 Source: Rosstat 10

- 224. Gross profit and wages as a percentage of GDP (right scale) 11

- 225. Income ratio by quintile, population, %; Gini coefficient, 2013-2018 Source: Rosstat 12

- 226. Population income distribution, thousand roubles, 2013-2018 Source: Rosstat 13

- 227. Personal consumption structure in Russia, 1990-2017 Source: Euromonitor 14

- 228. Share of households in possession of some household durables and gadgets in Russia, 1992-2017 Source: Euromonitor

- 229. Actual CPI and survey inflationary expectations, 2010-2017 (by November) 16

- 230. Federal Budget Expenditures 17

- 231. Foreign Trade Main Parameters 18

- 232. Military expenditure, in constant (2015) US$ 19 Source: SIPR, 2017I

- 233. Relative Stability of main economic indicators

- 234. CPI, key interest rate CBR, ruble to $ rate and key % minus CPI 21

- 235. Note: Seasonally adjusted quarterly growth, annualized. PMI stands for Purchasing Manager’s Index. Source: Haver Analytics, World

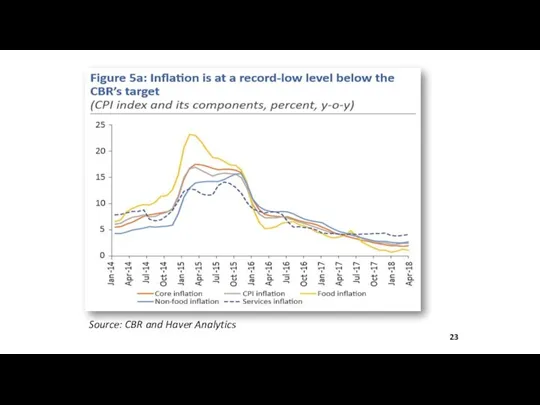

- 236. Source: CBR and Haver Analytics 23

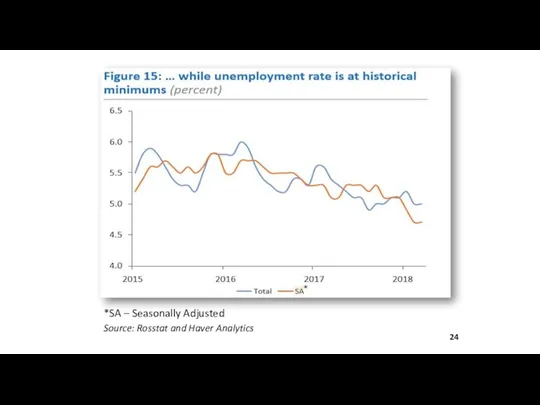

- 237. *SA – Seasonally Adjusted Source: Rosstat and Haver Analytics 24

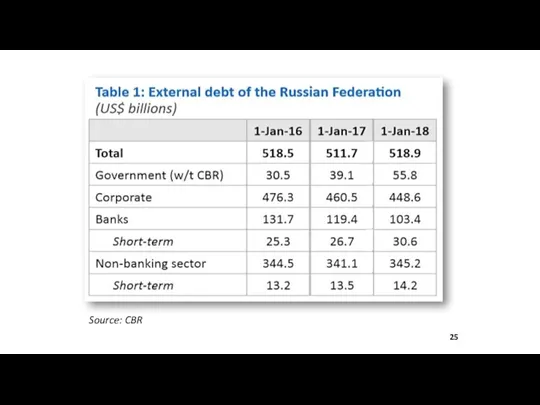

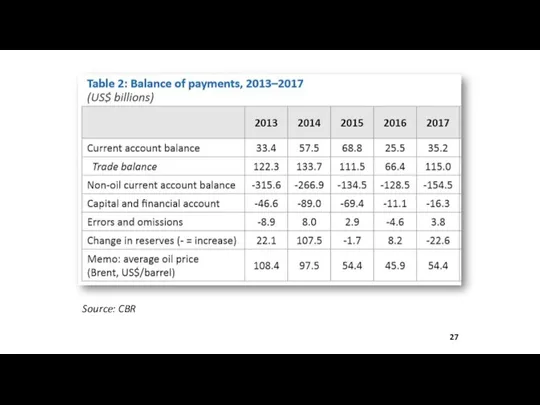

- 238. Source: CBR 25

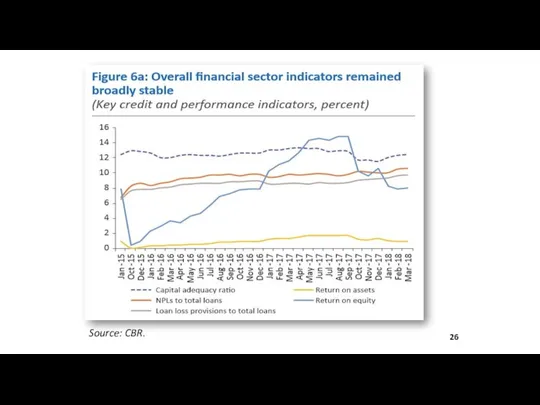

- 239. Source: CBR. 26

- 240. Source: CBR 27

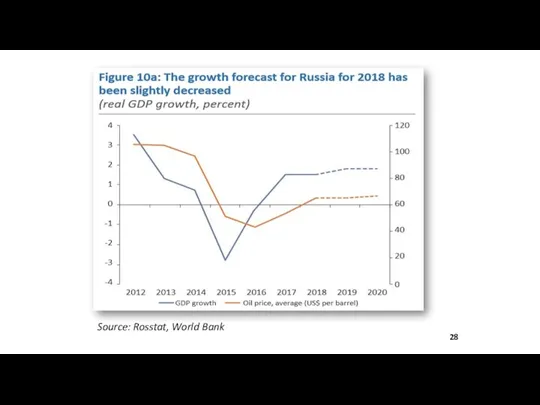

- 241. Source: Rosstat, World Bank 28

- 242. Recession and implications Recession is difficult for everybody Unofficial evaluations gave the loss of GDP to

- 243. Conclusion: Russia Russia has made the detour from European income distribution to Latin American one in

- 245. Скачать презентацию

GDP per capita

1000 – 2000, international $, log.scale

2

GDP per capita

1000 – 2000, international $, log.scale

2

Attempt to reconstruct the world economy dynamics

3

Attempt to reconstruct the world economy dynamics

3

Economic history quest: Malthusian trap

Source: http://krugman.blogs.nytimes.com/2009/07/01/the-malthusian-insult/comment-page-4/?_r=0 (taken from Brad de Long)

4

Economic history quest: Malthusian trap

Source: http://krugman.blogs.nytimes.com/2009/07/01/the-malthusian-insult/comment-page-4/?_r=0 (taken from Brad de Long)

4

Development rates of countries differ

Environment: tropics, moderate, North, heath, islands and

Development rates of countries differ

Environment: tropics, moderate, North, heath, islands and

Legal Systems of the World

Source: stolen from Wikipedia

6

Legal Systems of the World

Source: stolen from Wikipedia

6

The Great Divergence

China, India, Japan, Arabs were helpless against Turkey and

The Great Divergence

China, India, Japan, Arabs were helpless against Turkey and

Key problems of the Russian history

Millennium+ with no peace, regular wars…

Big

Key problems of the Russian history

Millennium+ with no peace, regular wars…

Big

Ratio of GDP per capita of the USSR/Russia to the USA

Russia/USA

USSR/USA

Ratio of GDP per capita of the USSR/Russia to the USA

Russia/USA

USSR/USA

Problems at the end of the 1980s.

Growth in different countries became

Problems at the end of the 1980s.

Growth in different countries became

Moscow princedom, 1533 (in red)

Moscow – Central Federal Region, 2013 (green

Moscow princedom, 1533 (in red) Moscow – Central Federal Region, 2013 (green

History – till 1533

Russian elites – “driving under influence”: Normans since

History – till 1533

Russian elites – “driving under influence”: Normans since

History – 1533- 1991 (1)

1533 – turning point for enlarging

History – 1533- 1991 (1)

1533 – turning point for enlarging

History – 1533- 1991 (2)

WWI and Romanov’s Crush, Revolution out

History – 1533- 1991 (2)

WWI and Romanov’s Crush, Revolution out

Remaining European empires

Empires were established by ”cool” adventurers followed by boyars

Remaining European empires

Empires were established by ”cool” adventurers followed by boyars

Договора Руси с Византией, 860… 912

Нестор - В Повести временных лет об этом

Договора Руси с Византией, 860… 912

Нестор - В Повести временных лет об этом

Договора Руси с Византией, 860… 912

Русско-византийский договор (907-912). Заключен после успешного

Договора Руси с Византией, 860… 912

Русско-византийский договор (907-912). Заключен после успешного

1533 – 1917, 1991 – the Big Bang

Ivan the “Terrible”: Siberia

1533 – 1917, 1991 – the Big Bang

Ivan the “Terrible”: Siberia

Empire is what it is

By A.N. Kuropatkin, the Nikolai II Minister

Empire is what it is

By A.N. Kuropatkin, the Nikolai II Minister

What exactly has to be transformed during a country transition?

The most

What exactly has to be transformed during a country transition?

The most

How deals on territorial changes are hold

Potential elites and legitimacy

Negotiations, elites`

How deals on territorial changes are hold

Potential elites and legitimacy

Negotiations, elites`

Might the development and transformation issues be resolved?

Goals of the transformation:

Might the development and transformation issues be resolved?

Goals of the transformation:

Difficulties and losses of the transitional period boost phobias:

Foreign capital as

Difficulties and losses of the transitional period boost phobias:

Foreign capital as

…and utopias:

Ideal policy exists

Governance instead of initiative

All-purpose instruments

Sudden leaps for no

…and utopias:

Ideal policy exists

Governance instead of initiative

All-purpose instruments

Sudden leaps for no

What did Russia obtained after the collapse?

Territory – more than 80%

What did Russia obtained after the collapse?

Territory – more than 80%

Dynamics of GDP per capita PPP (2011 prices) and population of

Dynamics of GDP per capita PPP (2011 prices) and population of

Death, birth and natural increase in Russia, 1960-2015s

27

Death, birth and natural increase in Russia, 1960-2015s

27

Source: World Bank

GDP PPP per capita, constant US$

Source: World Bank

GDP PPP per capita, constant US$

Key topics – crush of 1990-s

GDP = minus 43%, jump in

Key topics – crush of 1990-s

GDP = minus 43%, jump in

Russia: GDP level, Suicide and Homicide, qtr., s.a. 2006-2015

Russia: GDP level, Suicide and Homicide, qtr., s.a. 2006-2015

Russians speaking English and Russian & the Internet access

Russians speaking English and Russian & the Internet access

Society after 1/4 Century of Transition

Current Russian Socio-economic realty is the

Society after 1/4 Century of Transition

Current Russian Socio-economic realty is the

Key topics – Cold war in minds of Elites

Russians never lost

Key topics – Cold war in minds of Elites

Russians never lost

Trap of the middle level development?

The «500 days» program 1990;

Trap of the middle level development?

The «500 days» program 1990;

Leonid Grigoryev – some publications

Elites - the Choice for Modernization

Leonid Grigoryev – some publications

Elites - the Choice for Modernization

* Dotted-line graphs refer to the right axis

**Gold is measured in

* Dotted-line graphs refer to the right axis

**Gold is measured in

Source: Maddison 2007, p. 379, table A.4

Source: Maddison 2007, p. 379, table A.4

Literature, basic:

1. Mau V., Drobyshevskaya T. "Modernization and the Russian Economy:

Literature, basic:

1. Mau V., Drobyshevskaya T. "Modernization and the Russian Economy:

Transformations of 1917-2018

(ideology, ownership, country’s configuration)

and objective reasons for

Transformations of 1917-2018 (ideology, ownership, country’s configuration) and objective reasons for

Topics for discussion:

Russian in 1913 – Development V Institutions

European politics and

Topics for discussion:

Russian in 1913 – Development V Institutions

European politics and

History

Millennium+ with no peace, regular invasions

Normans, Byzantium, Nomads before Mongols

Big

History

Millennium+ with no peace, regular invasions

Normans, Byzantium, Nomads before Mongols

Big

The Empire Map

The Empire Map

Periods of Russian History in XX-XXI C

Tsar Nikolai II – till

Periods of Russian History in XX-XXI C

Tsar Nikolai II – till

Source: Maddison 2007, p. 379, table A.4

Source: Maddison 2007, p. 379, table A.4

* Dotted-line graphs refer to the right axis

**Gold is measured in

* Dotted-line graphs refer to the right axis

**Gold is measured in

Real national income per head, 1913 to 1927/28: year-on-year percent change

Real national income per head, 1913 to 1927/28: year-on-year percent change

Postwar recovery: The GDPs of selected Eurasian countries in 1928, percent

Postwar recovery: The GDPs of selected Eurasian countries in 1928, percent

European Empires and Unions

Empires were established by ”cool” adventurers followed by

European Empires and Unions

Empires were established by ”cool” adventurers followed by

Russian and Soviet economic and demographic losses in four crises

Source: Markevich

Russian and Soviet economic and demographic losses in four crises

Source: Markevich

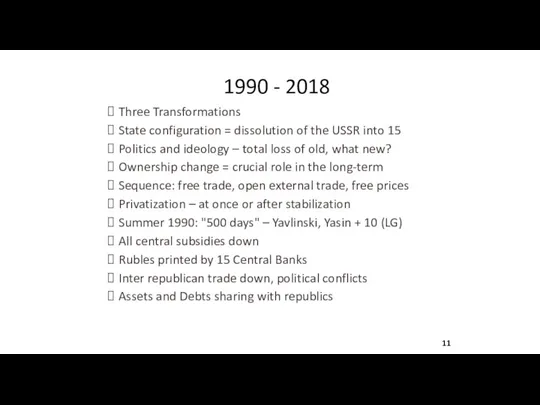

1990 - 2018

Three Transformations:

State configuration

Politics and ideology

Ownership

Steps of 1992: free trade,

1990 - 2018

Three Transformations:

State configuration

Politics and ideology

Ownership

Steps of 1992: free trade,

Source: World Bank

GDP PPP per capita, constant US$

Source: World Bank

GDP PPP per capita, constant US$

Source: World Bank

Economic history quest: Growth of transition economies. 1990 –

Source: World Bank

Economic history quest: Growth of transition economies. 1990 –

Key topics – crush of 1990-s

GDP = minus 43%, jump in

Key topics – crush of 1990-s

GDP = minus 43%, jump in

What did Russia obtain after the collapse?

Territory – more than 80%

What did Russia obtain after the collapse?

Territory – more than 80%

Russia key indicators, growth for the period,%

Source: Rosstat

Russia key indicators, growth for the period,%

Source: Rosstat

GDP, Industry production and Gross Fixed Capital Production, 1961-2007

Source: Rosstat, CSU

GDP, Industry production and Gross Fixed Capital Production, 1961-2007

Source: Rosstat, CSU

GDP (2000=100), military and R&D expenditures, oil extraction and prices

GDP (2000=100), military and R&D expenditures, oil extraction and prices

Russia: GDP level, Suicide and Homicide rates, 1989-2010

Russia: GDP level, Suicide and Homicide rates, 1989-2010

Russia: GDP level, Suicide and Homicide, qtr., s.a.2006-2015

Russia: GDP level, Suicide and Homicide, qtr., s.a.2006-2015

Consumer Expenditure on Durable Goods,

US$, Current Prices, 2000-2015

Source: Euromonitor

Consumer Expenditure on Durable Goods,

US$, Current Prices, 2000-2015

Source: Euromonitor

Society after 1/4 Century of Transition

Current Russian Socio-economic realty is the

Society after 1/4 Century of Transition

Current Russian Socio-economic realty is the

Key topics – Cold war in minds of Elites

Russians never lost

Key topics – Cold war in minds of Elites

Russians never lost

Military expenditure, in constant (2015) US$

Source: SIPR, 2017I

Military expenditure, in constant (2015) US$

Source: SIPR, 2017I

Russians know English and Russian & got access

Russians know English and Russian & got access

Logic of this Presentation

Objective problem of Russian history and institutions with

Logic of this Presentation

Objective problem of Russian history and institutions with

Ratio of GDP per capita of the USSR/Russia to the USA

Russia/USA

USSR/USA

Ratio of GDP per capita of the USSR/Russia to the USA

Russia/USA

USSR/USA

Literature:

“Transition to Market Economy” (in collaboration), Moscow, 1990, a.k.a. "500 days.

Literature:

“Transition to Market Economy” (in collaboration), Moscow, 1990, a.k.a. "500 days.

Russia - transformations of 1990-2018

Privatization and Ownership

and corporate governance

"Even

Russia - transformations of 1990-2018 Privatization and Ownership and corporate governance "Even

No warning for the People of the USSR

"No leader has yet

No warning for the People of the USSR

"No leader has yet

Source: World Bank

GDP PPP per capita, constant US$

Source: World Bank

GDP PPP per capita, constant US$

Russia key indicators, growth for the period,%

Source: Rosstat

Russia key indicators, growth for the period,%

Source: Rosstat

Key topics – crush of 1990-s

GDP = minus 43%, jump in

Key topics – crush of 1990-s

GDP = minus 43%, jump in

Transformation Debates 1987-1992

1987 – "ECO" = 70 years since 1917; Aganbegian,

Transformation Debates 1987-1992

1987 – "ECO" = 70 years since 1917; Aganbegian,

"Soviets need a unified Free Economy" (1/2)

Leonid Grigoriev – New York

"Soviets need a unified Free Economy" (1/2) Leonid Grigoriev – New York

"Soviets need a unified Free Economy" (2/2)

Leonid Grigoriev – New York

"Soviets need a unified Free Economy" (2/2) Leonid Grigoriev – New York

Global Choice of privatization

To privatize:

Lands, houses, infrastructure, firms, natural resources,

Global Choice of privatization

To privatize:

Lands, houses, infrastructure, firms, natural resources,

OECD countries in 2017

Source: Size and Sectoral Distribution of Stateowned

OECD countries in 2017

Source: Size and Sectoral Distribution of Stateowned

1990 - 2018

Three Transformations

State configuration = dissolution of the USSR into

1990 - 2018

Three Transformations

State configuration = dissolution of the USSR into

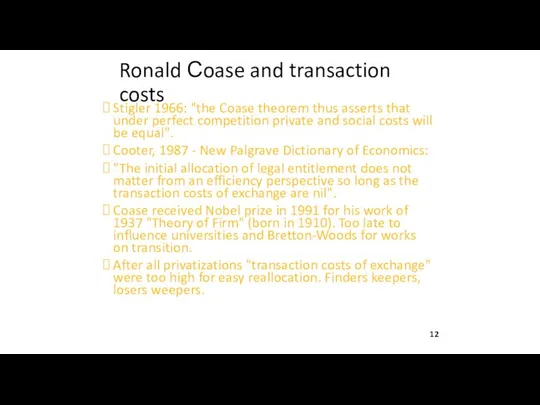

Ronald Сoase and transaction costs

Stigler 1966: "the Coase theorem thus asserts

Ronald Сoase and transaction costs

Stigler 1966: "the Coase theorem thus asserts

Bundle of Rights – Honore 1961 – Ownership (1/2)

(1) The

Bundle of Rights – Honore 1961 – Ownership (1/2)

(1) The

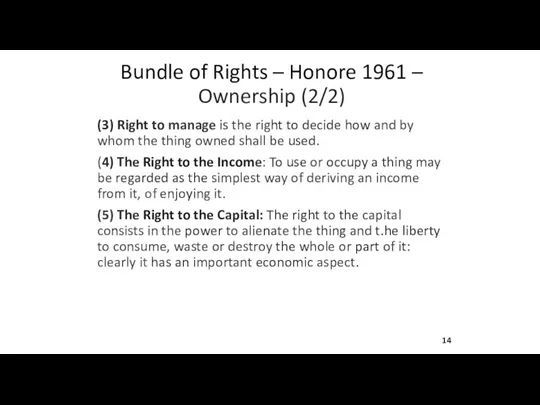

Bundle of Rights – Honore 1961 – Ownership (2/2)

(3) Right

Bundle of Rights – Honore 1961 – Ownership (2/2)

(3) Right

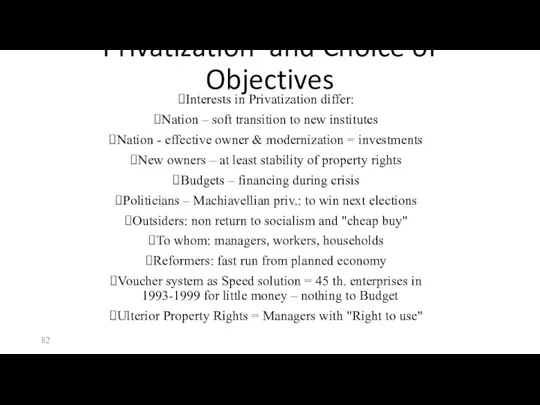

Privatization and Choice of Objectives

Interests in Privatization differ:

Nation – soft transition

Privatization and Choice of Objectives

Interests in Privatization differ:

Nation – soft transition

Institutional conditions for effective privatization

Source: Kikery S, Nelis J., Shirly M.,

Institutional conditions for effective privatization

Source: Kikery S, Nelis J., Shirly M.,

17

Source: Voszka, É. – Kiss, G. D. (eds) 2014: Crisis Management

17

Source: Voszka, É. – Kiss, G. D. (eds) 2014: Crisis Management

Source: Voszka, É. – Kiss, G. D. (eds) 2014: Crisis Management

Source: Voszka, É. – Kiss, G. D. (eds) 2014: Crisis Management

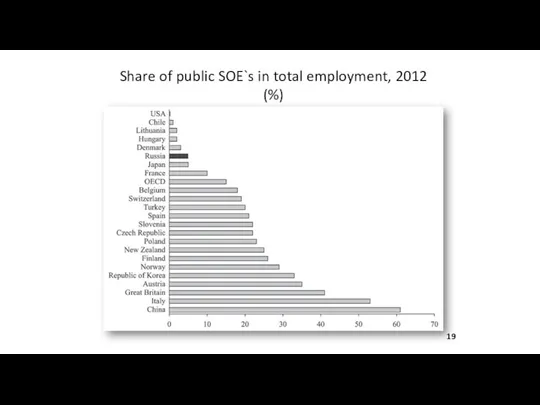

Share of public SOE`s in total employment, 2012 (%)

19

Share of public SOE`s in total employment, 2012 (%)

19

Share of public SOE`s in total market capitalization for various countries,

Share of public SOE`s in total market capitalization for various countries,

Privatization revenues, 1990-1999, bill. dollars

Source: Goskomstat, Jan.2002, World Bank Privatization Database,

Privatization revenues, 1990-1999, bill. dollars

Source: Goskomstat, Jan.2002, World Bank Privatization Database,

Outcome of privatization in Russia

Politicians and Reformers may believe in their

Outcome of privatization in Russia

Politicians and Reformers may believe in their

Source: F. Novokmet, T. Piketty, G. Zucman. From Soviets to Oligarchs:

Source: F. Novokmet, T. Piketty, G. Zucman. From Soviets to Oligarchs:

SOE shares among countries’ top ten firms (%), 2013

Source: State-owned enterprises

SOE shares among countries’ top ten firms (%), 2013

Source: State-owned enterprises

Source: GlobalEconomy https://www.theglobaleconomy.com/rankings/herit_property_rights/

Measures the degree to which a government enforces private

Source: GlobalEconomy https://www.theglobaleconomy.com/rankings/herit_property_rights/

Measures the degree to which a government enforces private

Calculations of Piketty and Co

Russia made its way to high concentration

Calculations of Piketty and Co

Russia made its way to high concentration

Source: F. Novokmet, T. Piketty, G. Zucman. From Soviets to Oligarchs:

Source: F. Novokmet, T. Piketty, G. Zucman. From Soviets to Oligarchs:

Source: F. Novokmet, T. Piketty, G. Zucman. From Soviets to Oligarchs:

Inequality

Source: F. Novokmet, T. Piketty, G. Zucman. From Soviets to Oligarchs:

Inequality

Source: F. Novokmet, T. Piketty, G. Zucman. From Soviets to Oligarchs:

Source: F. Novokmet, T. Piketty, G. Zucman. From Soviets to Oligarchs:

Source: F. Novokmet, T. Piketty, G. Zucman. From Soviets to Oligarchs:

Source: F. Novokmet, T. Piketty, G. Zucman. From Soviets to Oligarchs:

Source: F. Novokmet, T. Piketty, G. Zucman. From Soviets to Oligarchs:

Source: F. Novokmet, T. Piketty, G. Zucman. From Soviets to Oligarchs:

Source: F. Novokmet, T. Piketty, G. Zucman. From Soviets to Oligarchs:

Source: F. Novokmet, T. Piketty, G. Zucman. From Soviets to Oligarchs:

Source: F. Novokmet, T. Piketty, G. Zucman. From Soviets to Oligarchs:

Source: F. Novokmet, T. Piketty, G. Zucman. From Soviets to Oligarchs:

Source: F. Novokmet, T. Piketty, G. Zucman. From Soviets to Oligarchs:

Source: F. Novokmet, T. Piketty, G. Zucman. From Soviets to Oligarchs:

Byproducts of Wealth Distribution

Inequality may be measured differently. Might have been

Byproducts of Wealth Distribution

Inequality may be measured differently. Might have been

Source:

The World Bank

Global Wealth Databook 2014 (Credit Suisse)

Wealth share

Source:

The World Bank

Global Wealth Databook 2014 (Credit Suisse)

Wealth share

Source: F. Novokmet, T. Piketty, G. Zucman. From Soviets to Oligarchs:

Source: F. Novokmet, T. Piketty, G. Zucman. From Soviets to Oligarchs:

Source: F. Novokmet, T. Piketty, G. Zucman. From Soviets to Oligarchs:

Source: F. Novokmet, T. Piketty, G. Zucman. From Soviets to Oligarchs:

Source: F. Novokmet, T. Piketty, G. Zucman. From Soviets to Oligarchs:

Source: F. Novokmet, T. Piketty, G. Zucman. From Soviets to Oligarchs:

Source: F. Novokmet, T. Piketty, G. Zucman. From Soviets to Oligarchs:

Source: F. Novokmet, T. Piketty, G. Zucman. From Soviets to Oligarchs:

Source: F. Novokmet, T. Piketty, G. Zucman. From Soviets to Oligarchs:

Source: F. Novokmet, T. Piketty, G. Zucman. From Soviets to Oligarchs:

Source: F. Novokmet, T. Piketty, G. Zucman. From Soviets to Oligarchs:

Source: F. Novokmet, T. Piketty, G. Zucman. From Soviets to Oligarchs:

Source: F. Novokmet, T. Piketty, G. Zucman. From Soviets to Oligarchs:

Source: F. Novokmet, T. Piketty, G. Zucman. From Soviets to Oligarchs:

Literature:

Kornai Y. The Socialist System: The Political Economy of Communism. Oxford

Literature:

Kornai Y. The Socialist System: The Political Economy of Communism. Oxford

Leonid Grigoryev – some publications

Grigoryev L. "Ulterior Property Rights"

Leonid Grigoryev – some publications

Grigoryev L. "Ulterior Property Rights"

Global Structure

Inequality:

Income and Wealth

(4.02. 2019)

Tenured Professor Leonid Grigoryev

Global Structure

Inequality:

Income and Wealth

(4.02. 2019)

Tenured Professor Leonid Grigoryev

Births, Deaths And Natural Increase Dynamics in Russia, 1960-2015

2

Births, Deaths And Natural Increase Dynamics in Russia, 1960-2015

2

World Population and GDP in Various Dimensions, 1992–2016

World Population and GDP in Various Dimensions, 1992–2016

Key points (1/2):

Inequality between countries changes, Clusters go apart.

Global

Key points (1/2):

Inequality between countries changes, Clusters go apart.

Global

Key points (2/2):

Domestic inequality is rigid, Growth is not changing

Key points (2/2):

Domestic inequality is rigid, Growth is not changing

Gini coefficient reflects mostly variation in rich deciles. Gini in comparison

Gini coefficient reflects mostly variation in rich deciles. Gini in comparison

Average and weighted average GDP per capita, PPP current prices (thousand

Average and weighted average GDP per capita, PPP current prices (thousand

UN sustainable development goal №10.

Reduce inequalities (1/2)

Socio-economic parameters of

UN sustainable development goal №10.

Reduce inequalities (1/2)

Socio-economic parameters of

Income Inequality – International Comparison, 2014 or latest available

Income Inequality – International Comparison, 2014 or latest available

Personal Consumption in Selected Countries, 2016

Source: Euromonitor

10

Personal Consumption in Selected Countries, 2016

Source: Euromonitor

10

Attitudes and Happiness

Transformation has reduced expectations of state support. Not Russia

Attitudes and Happiness

Transformation has reduced expectations of state support. Not Russia

The degree of agreement of respondents with the statement “Government should

The degree of agreement of respondents with the statement “Government should

Level of life satisfaction in BRICS countries by income level, 1990-2014,

Level of life satisfaction in BRICS countries by income level, 1990-2014,

Level of life satisfaction in BRICS countries, 1990-2014, %

14

Level of life satisfaction in BRICS countries, 1990-2014, %

14

Access to Internet, mobile phone and personal computer usage, % households,

Access to Internet, mobile phone and personal computer usage, % households,

Russia: from quasi egalitarian to?

Yasin’s work of 2010: only top 20%

Russia: from quasi egalitarian to?

Yasin’s work of 2010: only top 20%

Real cash income dynamics by 20% - income groups, 1991–2009 гг.,

Real cash income dynamics by 20% - income groups, 1991–2009 гг.,

Re-stratification of the society

I could not find a study of the

Re-stratification of the society

I could not find a study of the

Seven Stratas of Society

Upper class – income, rent, etc.: (1) Upper

Seven Stratas of Society

Upper class – income, rent, etc.: (1) Upper

Russia: Middle class structure in 2000s (T. Maleva)

20

Russia: Middle class structure in 2000s (T. Maleva)

20

Dynamics of inequality in Russia (1/2)

High social inequality in Russia has

Dynamics of inequality in Russia (1/2)

High social inequality in Russia has

Dynamics of inequality in Russia (2/2)

Share of income by 20-percent groups

Dynamics of inequality in Russia (2/2)

Share of income by 20-percent groups

Transformation of society: features

10 years of economic decline (minus 43) lead

Transformation of society: features

10 years of economic decline (minus 43) lead

Income and Wealth Inequality

Inequality has a long history – in Europe

Income and Wealth Inequality

Inequality has a long history – in Europe

Wealth share of top decile by country, 2000-2014 (The World Bank

Wealth share of top decile by country, 2000-2014 (The World Bank

UN sustainable development goal №10.

Reduce inequalities (2/2)

Distribution of financial

UN sustainable development goal №10.

Reduce inequalities (2/2)

Distribution of financial

Source: F. Novokmet, T. Piketty, G. Zucman. From Soviets to Oligarchs:

Source: F. Novokmet, T. Piketty, G. Zucman. From Soviets to Oligarchs:

Source: F. Novokmet, T. Piketty, G. Zucman. From Soviets to Oligarchs:

Source: F. Novokmet, T. Piketty, G. Zucman. From Soviets to Oligarchs:

Source: F. Novokmet, T. Piketty, G. Zucman. From Soviets to Oligarchs:

Source: F. Novokmet, T. Piketty, G. Zucman. From Soviets to Oligarchs:

Conclusion: Russia

Russia has made the detour from European income

Conclusion: Russia

Russia has made the detour from European income

31

31

Literature – 1

Atkinson Anthony “Inequality. What can be done?”, Cambridge,

Literature – 1

Atkinson Anthony “Inequality. What can be done?”, Cambridge,

Literature - 2

Григорьев Л.М, Павлюшина В.А. Социальное неравенство в мире

Literature - 2

Григорьев Л.М, Павлюшина В.А. Социальное неравенство в мире

Growth and Macro

11.02.2019

Professor Leonid Grigoryev

HSE, Moscow

www.leonidgrigoryev.com

Growth and Macro

11.02.2019

Professor Leonid Grigoryev

HSE, Moscow

www.leonidgrigoryev.com

Ratio of GDP per capita of the USSR/Russia to the USA

Source:

Ratio of GDP per capita of the USSR/Russia to the USA

Source:

Growth factors – long-run demand

Infrastructure – roads and communications,

Housing = new

Growth factors – long-run demand

Infrastructure – roads and communications,

Housing = new

Contribution to real GDP growth from production side

4

Contribution to real GDP growth from production side

4

Contribution to real GDP growth from demand side

5

Contribution to real GDP growth from demand side

5

Main economic indicators of the Russian Federation, 2007-2010, 2014-2017 (1/4)

6

Main economic indicators of the Russian Federation, 2007-2010, 2014-2017 (1/4)

6

Main economic indicators of the Russian Federation, 2007-2010, 2014-2017 (2/4)

6

Main economic indicators of the Russian Federation, 2007-2010, 2014-2017 (2/4)

6

Main economic indicators of the Russian Federation, 2007-2010, 2014-2017 (3/4)

7

Main economic indicators of the Russian Federation, 2007-2010, 2014-2017 (3/4)

7

Main economic indicators of the Russian Federation, 2007-2010,

2014-2017 (4/4)

8

Main economic indicators of the Russian Federation, 2007-2010,

2014-2017 (4/4)

8

Russia key indicators, growth for the period, %

Source: Rosstat

Russia key indicators, growth for the period, %

Source: Rosstat

Industrial production, 1990—2017*, 1998 = 100

*Half year 2017

Source: Rosstat

10

Industrial production, 1990—2017*, 1998 = 100

*Half year 2017

Source: Rosstat

10

Labour productivity growth rates in the world, the OECD region and

Labour productivity growth rates in the world, the OECD region and

Growth of labour productivity, capital deepening and TFP in the market

Growth of labour productivity, capital deepening and TFP in the market

Gross profit and wages as a percentage of GDP (right scale)

13

Gross profit and wages as a percentage of GDP (right scale)

13

Percentage gap in GDP per worker in some Central and East

Percentage gap in GDP per worker in some Central and East

Income ratio by quintile, population, %; Gini coefficient, 2013-2018

Source: Rosstat

15

Income ratio by quintile, population, %; Gini coefficient, 2013-2018

Source: Rosstat

15

Population income distribution, thousand roubles, 2013-2018

Source: Rosstat

16

Population income distribution, thousand roubles, 2013-2018

Source: Rosstat

16

Personal consumption structure in Russia, 1990-2017

Source: Euromonitor

17

Personal consumption structure in Russia, 1990-2017

Source: Euromonitor

17

Real disposable income, real wages and consumer spending, 2012-2017

18

Real disposable income, real wages and consumer spending, 2012-2017

18

Key interest rates of the leading countries` Central banks, 2007–2017

Source — Thomson

Key interest rates of the leading countries` Central banks, 2007–2017

Source — Thomson

Actual CPI and survey inflationary expectations, 2010-2017 (by November)

Actual CPI and survey inflationary expectations, 2010-2017 (by November)

Federal Budget Expenditures

Federal Budget Expenditures

Foreign Trade Main Parameters

22

Foreign Trade Main Parameters

22

Military expenditure, in constant (2015) US$

Source: SIPR, 2017I

Military expenditure, in constant (2015) US$

Source: SIPR, 2017I

CPI, key interest rate CBR, ruble to $ rate and key

CPI, key interest rate CBR, ruble to $ rate and key

Share of households in possession of some household durables and gadgets

Share of households in possession of some household durables and gadgets

Regional structure of the population and GRP (gross regional product) in

Regional structure of the population and GRP (gross regional product) in

Retail sales 2015-2016, per capita by type of regions

Source: Rosstat, Analytical

Retail sales 2015-2016, per capita by type of regions

Source: Rosstat, Analytical

Share of non-food goods expenditures in consumer spending of Russian families

Share of non-food goods expenditures in consumer spending of Russian families

Share of alcohol expenditures in consumer spendings of Russian families by

Share of alcohol expenditures in consumer spendings of Russian families by

Total area, number of flats and mean flats` area in houses

Total area, number of flats and mean flats` area in houses

Recession and implications

Recession is difficult for everybody

Unofficial evaluations gave the loss

Recession and implications

Recession is difficult for everybody

Unofficial evaluations gave the loss

Conclusion: Russia

Russia has made the detour from European income distribution

Conclusion: Russia

Russia has made the detour from European income distribution

Literature:

Voskoboynikov, I. "Sources of long run economic growth in Russia before

Literature:

Voskoboynikov, I. "Sources of long run economic growth in Russia before

Professor Leonid Grigoryev

www.leonidgrigoryev.com

Economy & Energy

18.02.2019

Professor Leonid Grigoryev

www.leonidgrigoryev.com

Economy & Energy

18.02.2019

Energy – history and theory

Energy waves – replacement by efficiency, costs,

Energy – history and theory

Energy waves – replacement by efficiency, costs,

Energy: history

Source: A. Makarov, A. Makarov. Laws of Power Industry Development:

Energy: history

Source: A. Makarov, A. Makarov. Laws of Power Industry Development:

Dynamics of the real prices for the key primary products

1901-2010, where

Dynamics of the real prices for the key primary products 1901-2010, where

Dynamics of the global energy consumption and GDP, 1971 - 2015

Source:

Dynamics of the global energy consumption and GDP, 1971 - 2015

Source:

GDP energy capacity: developed countries,1970 – 2016

Source: IEA

GDP energy capacity: developed countries,1970 – 2016

Source: IEA

GDP energy capacity: developing countries,1971 - 2015

Source: IEA

GDP energy capacity: developing countries,1971 - 2015

Source: IEA

Average per capita energy consumption, 1970 - 2016

Source: IEA

Average per capita energy consumption, 1970 - 2016

Source: IEA

Comparison of the prices for different fuels,

2000 – 2016, $

Comparison of the prices for different fuels, 2000 – 2016, $

The Structure of World Energy Consumption,

1971 and 2015, % total consumption

Source:

The Structure of World Energy Consumption,

1971 and 2015, % total consumption

Source:

Primary energy demand by fuel

(in 2015 and increase by 2040),

Primary energy demand by fuel

(in 2015 and increase by 2040),

Geopolitics & Rational Changes

Growth and Energy consumption

Embargo of Arab OPEC 1973

Geopolitics & Rational Changes

Growth and Energy consumption

Embargo of Arab OPEC 1973

World GDP and Trade Growth rate, %, 1995‑2018

Source: IMF, WEO April

World GDP and Trade Growth rate, %, 1995‑2018

Source: IMF, WEO April

Carbon Dioxide Emissions, 1985-2017

Source: BP Stat. Review 2017

Carbon Dioxide Emissions, 1985-2017

Source: BP Stat. Review 2017

Geopolitics steps over trade, development

and Global problems’ solutions

World is losing stability

Geopolitics steps over trade, development

and Global problems’ solutions

World is losing stability

GDP and Primary Energy Consumption, annual growth rates, 1991 - 2017

Source:

GDP and Primary Energy Consumption, annual growth rates, 1991 - 2017

Source:

Oil and Gas Consumption, annual growth rates, 1991 - 2017

Source: World

Oil and Gas Consumption, annual growth rates, 1991 - 2017

Source: World

Coal consumption and Electricity generation, annual growth rates, 1991 - 2017

Source:

Coal consumption and Electricity generation, annual growth rates, 1991 - 2017

Source:

Global Energy Balance, mln tons, 2015

Source: IEA

Global Energy Balance, mln tons, 2015

Source: IEA

Energy poverty

Source: IEA, World Energy Outlook 2017

20

Energy poverty

Source: IEA, World Energy Outlook 2017

20

Global energy supply investment in 2014 – 2035, IEA estimate (2014),

Global energy supply investment in 2014 – 2035, IEA estimate (2014),

Example of interfuel substitution

Source:IEA

22

Example of interfuel substitution

Source:IEA

22

OPEC & RUSSIA

OPEC & RUSSIA

Export Incomes in OPEC countries and Russia,

bln. $, 2000-2017

Source: Analytical

Export Incomes in OPEC countries and Russia,

bln. $, 2000-2017

Source: Analytical

The acceptable price in budget leveraging, 2000-2017

The acceptable price in budget leveraging, 2000-2017

Source: BP

Russian Primary Energy Consumption, mln toe

Source: BP

Russian Primary Energy Consumption, mln toe

GDP, export and import of Russia, y/y, 2015-2017

Source: Thomson Reuters Datastream

GDP, export and import of Russia, y/y, 2015-2017

Source: Thomson Reuters Datastream

Russian export of energy, mln toe

Source: ERI RAS

Russian export of energy, mln toe

Source: ERI RAS

Source: BP

Russian Primary Energy Consumption, mln toe

Source: BP

Russian Primary Energy Consumption, mln toe

Conclusions on OPEC+

Oil prices of $55 - $70 helped to Global

Conclusions on OPEC+

Oil prices of $55 - $70 helped to Global

World Energy Transition and Future

World is undergoing Energy transition, but still

World Energy Transition and Future

World is undergoing Energy transition, but still

Literature 1

Григорьев Л.М., Чапыгина А.В. «Саудовская Аравия – нефть и развитие»,

Literature 1

Григорьев Л.М., Чапыгина А.В. «Саудовская Аравия – нефть и развитие»,

Literature 2

“Global and Russian Energy Outlook Up To 2040”, IES, RAS,2016

Literature 2

“Global and Russian Energy Outlook Up To 2040”, IES, RAS,2016

Macro &

4.03.2019

Professor Leonid Grigoryev

HSE, Moscow

www.leonidgrigoryev.com

Macro &

4.03.2019

Professor Leonid Grigoryev

HSE, Moscow

www.leonidgrigoryev.com

Upcoming events

4 of March – Macro light questions for students

11

Upcoming events

4 of March – Macro light questions for students

11

Ratio of GDP per capita of the USSR/Russia to the USA

Source:

Ratio of GDP per capita of the USSR/Russia to the USA

Source:

Growth factors – long-run demand

Infrastructure – roads and communications,

Housing = new

Growth factors – long-run demand

Infrastructure – roads and communications,

Housing = new

Source: Haver Analytics

4

Source: Haver Analytics

4

Contribution to real GDP growth from production side

5

Contribution to real GDP growth from production side

5

Contribution to real GDP growth from demand side

6

Contribution to real GDP growth from demand side

6

Main economic indicators of the Russian Federation, 2007-2010, 2014-2017 (1/3)

7

Main economic indicators of the Russian Federation, 2007-2010, 2014-2017 (1/3)

7

Main economic indicators of the Russian Federation, 2007-2010, 2014-2017 (2/3)

8

Main economic indicators of the Russian Federation, 2007-2010, 2014-2017 (2/3)

8

Main economic indicators of the Russian Federation, 2007-2010, 2014-2017 (3/3)

9

Main economic indicators of the Russian Federation, 2007-2010, 2014-2017 (3/3)

9

Industrial production, 1990—2017*, 1998 = 100

*Half year 2017

Source: Rosstat

10

Industrial production, 1990—2017*, 1998 = 100

*Half year 2017

Source: Rosstat

10

Gross profit and wages as a percentage of GDP (right scale)

11

Gross profit and wages as a percentage of GDP (right scale)

11

Income ratio by quintile, population, %; Gini coefficient, 2013-2018

Source: Rosstat

12

Income ratio by quintile, population, %; Gini coefficient, 2013-2018

Source: Rosstat

12

Population income distribution, thousand roubles, 2013-2018

Source: Rosstat

13

Population income distribution, thousand roubles, 2013-2018

Source: Rosstat

13

Personal consumption structure in Russia, 1990-2017

Source: Euromonitor

14

Personal consumption structure in Russia, 1990-2017

Source: Euromonitor

14

Share of households in possession of some household durables and gadgets

Share of households in possession of some household durables and gadgets

Actual CPI and survey inflationary expectations, 2010-2017 (by November)

16

Actual CPI and survey inflationary expectations, 2010-2017 (by November)

16

Federal Budget Expenditures

17

Federal Budget Expenditures

17

Foreign Trade Main Parameters

18

Foreign Trade Main Parameters

18

Military expenditure, in constant (2015) US$

19

Source: SIPR, 2017I

Military expenditure, in constant (2015) US$

19

Source: SIPR, 2017I

Relative Stability

of main economic indicators

Relative Stability

of main economic indicators

CPI, key interest rate CBR, ruble to $ rate and key

CPI, key interest rate CBR, ruble to $ rate and key

Note: Seasonally adjusted quarterly growth, annualized. PMI stands for Purchasing Manager’s

Note: Seasonally adjusted quarterly growth, annualized. PMI stands for Purchasing Manager’s

Source: CBR and Haver Analytics

23

Source: CBR and Haver Analytics

23

*SA – Seasonally Adjusted

Source: Rosstat and Haver Analytics

24

*SA – Seasonally Adjusted

Source: Rosstat and Haver Analytics

24

Source: CBR

25

Source: CBR

25

Source: CBR.

26

Source: CBR.

26

Source: CBR

27

Source: CBR

27

Source: Rosstat, World Bank

28

Source: Rosstat, World Bank

28

Recession and implications

Recession is difficult for everybody

Unofficial evaluations gave the loss

Recession and implications

Recession is difficult for everybody

Unofficial evaluations gave the loss

Conclusion: Russia

Russia has made the detour from European income distribution

Conclusion: Russia

Russia has made the detour from European income distribution

Reported questions. What is important?

Reported questions. What is important? Moscow is the capital of Russia

Moscow is the capital of Russia Millionaire-modal auxiliares

Millionaire-modal auxiliares First conditional for possibilities

First conditional for possibilities Virus which gave birth to racism

Virus which gave birth to racism Инфинитив и герундий

Инфинитив и герундий Study the advertisement. Preparation

Study the advertisement. Preparation Gap year in Ukraine

Gap year in Ukraine My family!

My family! Learning Styles

Learning Styles Let's go to school

Let's go to school The Means of Communication

The Means of Communication Интерактивный тренажер Colors and Animals - 1

Интерактивный тренажер Colors and Animals - 1 Новая Зеландия

Новая Зеландия Sports activities games

Sports activities games Food – basic processes

Food – basic processes Describing pictures

Describing pictures [w ] White, Well, Winter, Welcome Well, welcome white winter!

[w ] White, Well, Winter, Welcome Well, welcome white winter! ЕГЭ. Английский язык. Вариант 7

ЕГЭ. Английский язык. Вариант 7 Degrees of Comparison of Adjectives

Degrees of Comparison of Adjectives Using games in a foreign language classroom

Using games in a foreign language classroom Present Perfect or Past Simple

Present Perfect or Past Simple My lovely house game teacher switcher

My lovely house game teacher switcher An ICT role in key sectors of development of society. Standards in the field of ICT

An ICT role in key sectors of development of society. Standards in the field of ICT Мало Present Simple

Мало Present Simple Как написать эссе (письменное высказывание с элементами рассуждения) по английскому языку

Как написать эссе (письменное высказывание с элементами рассуждения) по английскому языку Passive voice in present

Passive voice in present Progress check

Progress check