- Chapter 13. The Cost of Production

Содержание

- 2. Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition Chapter 13: Page Examine what items are

- 3. Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition Chapter 13: Page Supply and demand are

- 4. Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition Chapter 13: Page According to the Law

- 5. Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition Chapter 13: Page Total Revenue The amount

- 6. Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition Chapter 13: Page A firm’s cost of

- 7. Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition Chapter 13: Page Example: Helen uses $300

- 8. Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition Chapter 13: Page Economists measure a firm’s

- 9. Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition Chapter 13: Page When total revenue exceeds

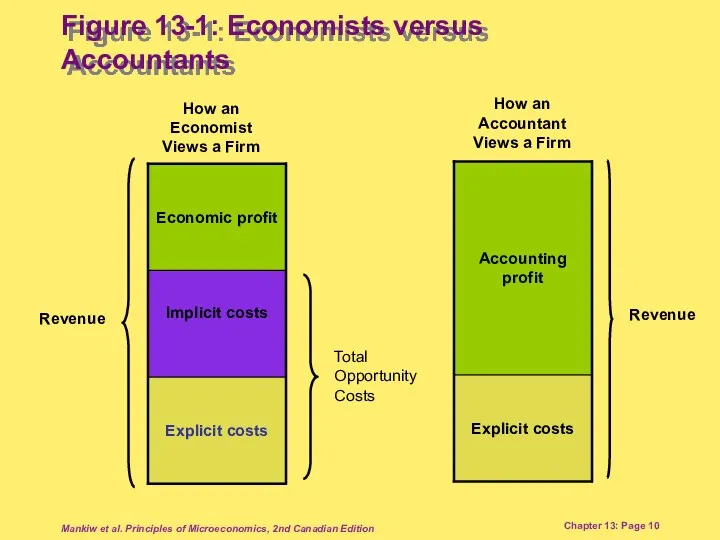

- 10. Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition Chapter 13: Page How an Economist Views

- 11. Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition Chapter 13: Page Assumption: The size of

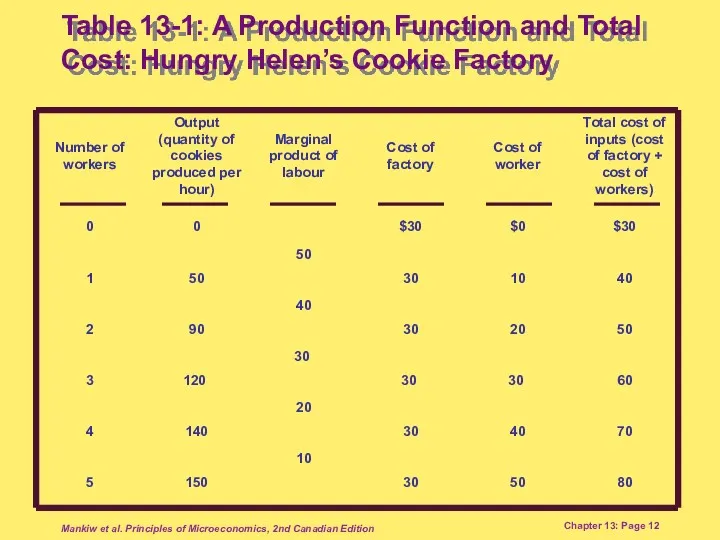

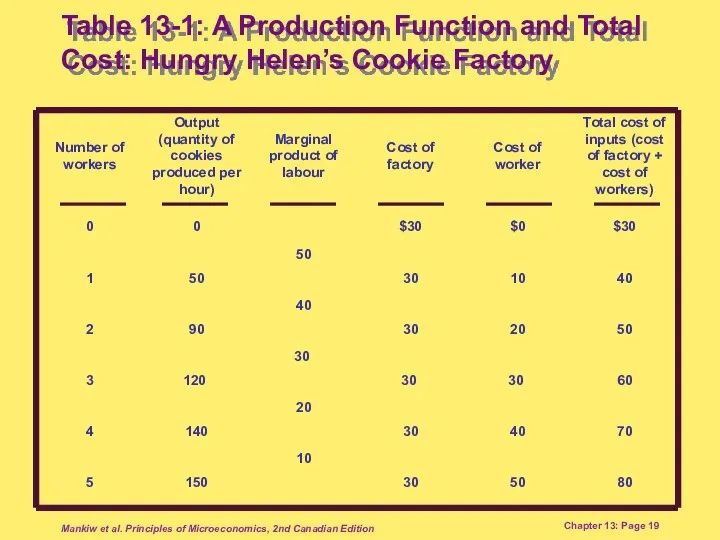

- 12. Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition Chapter 13: Page Table 13-1: A Production

- 13. Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition Chapter 13: Page The Production Function The

- 14. Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition Chapter 13: Page Diminishing Marginal Product Diminishing

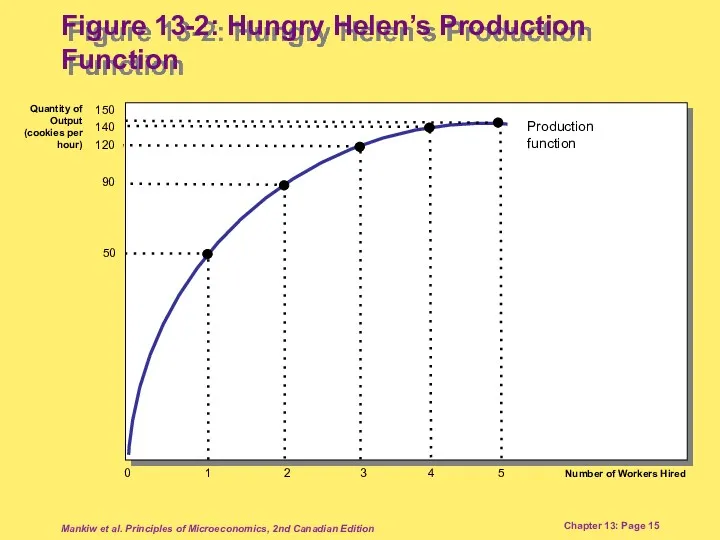

- 15. Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition Chapter 13: Page 0 Number of Workers

- 16. Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition Chapter 13: Page Diminishing Marginal Product Diminishing

- 17. Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition Chapter 13: Page Diminishing Marginal Product The

- 18. Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition Chapter 13: Page The relationship between the

- 19. Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition Chapter 13: Page Table 13-1: A Production

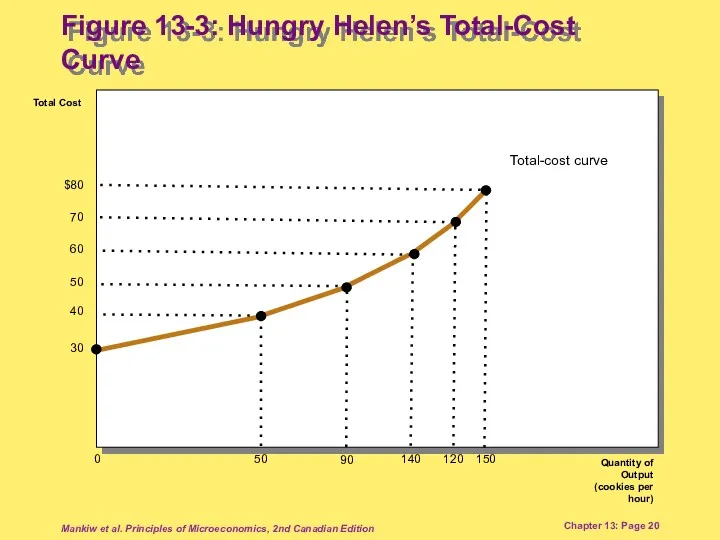

- 20. Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition Chapter 13: Page 0 Total Cost Quantity

- 21. Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition Chapter 13: Page Costs of production may

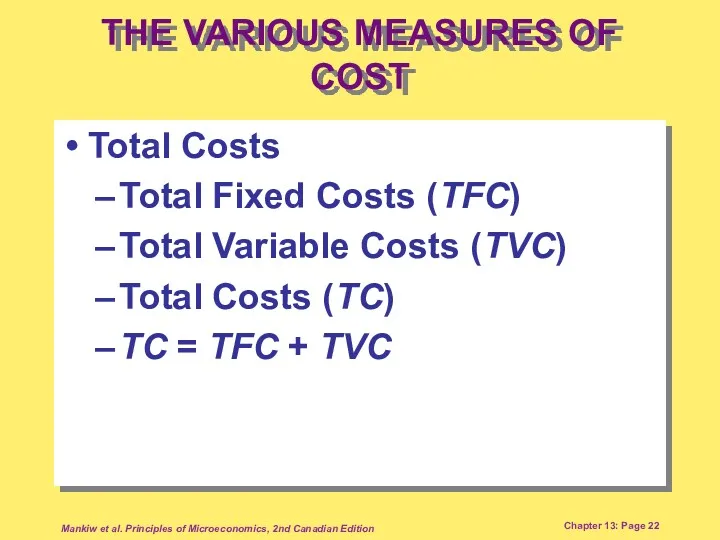

- 22. Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition Chapter 13: Page Total Costs Total Fixed

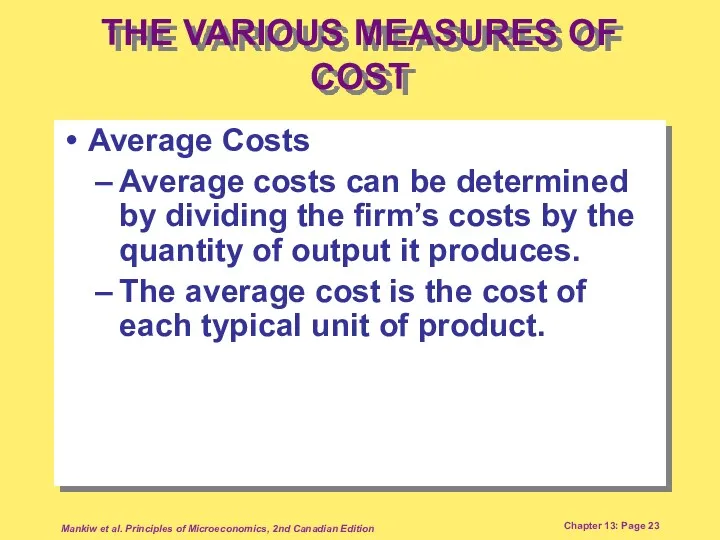

- 23. Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition Chapter 13: Page Average Costs Average costs

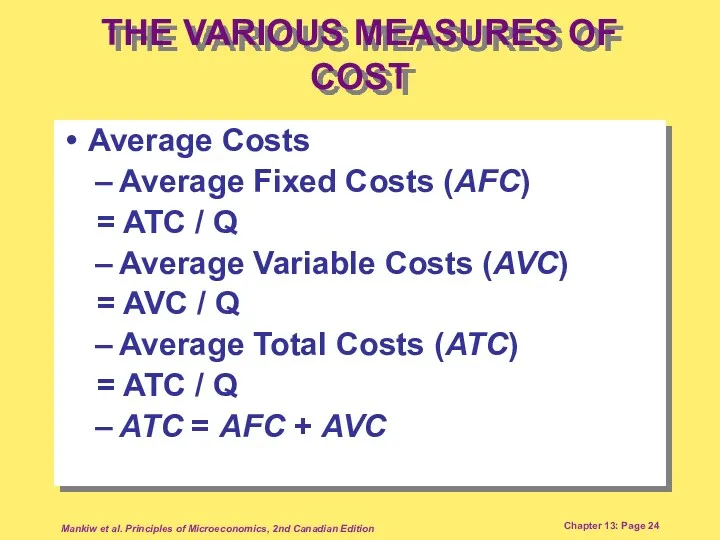

- 24. Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition Chapter 13: Page Average Costs Average Fixed

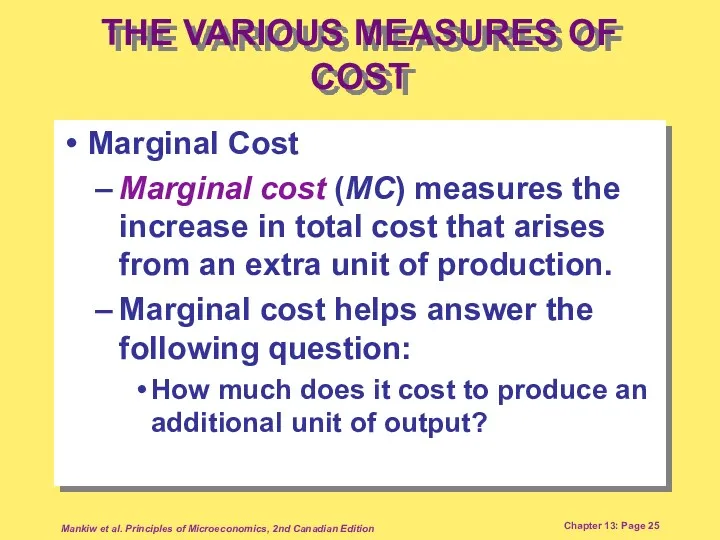

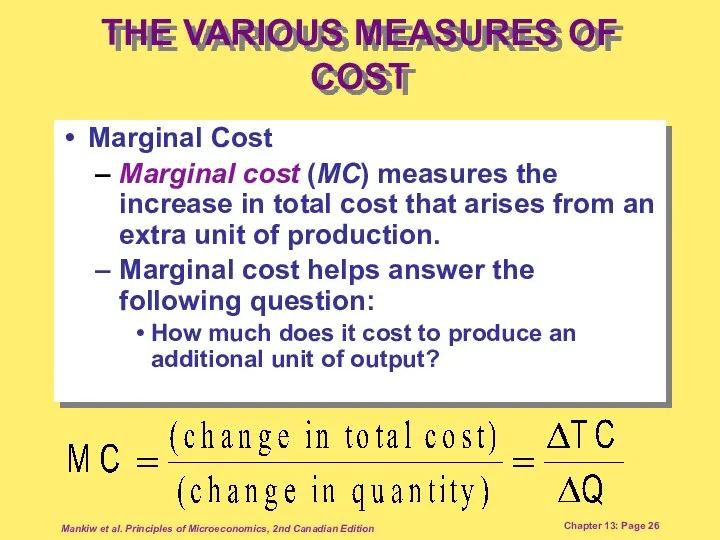

- 25. Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition Chapter 13: Page Marginal Cost Marginal cost

- 26. Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition Chapter 13: Page Marginal Cost Marginal cost

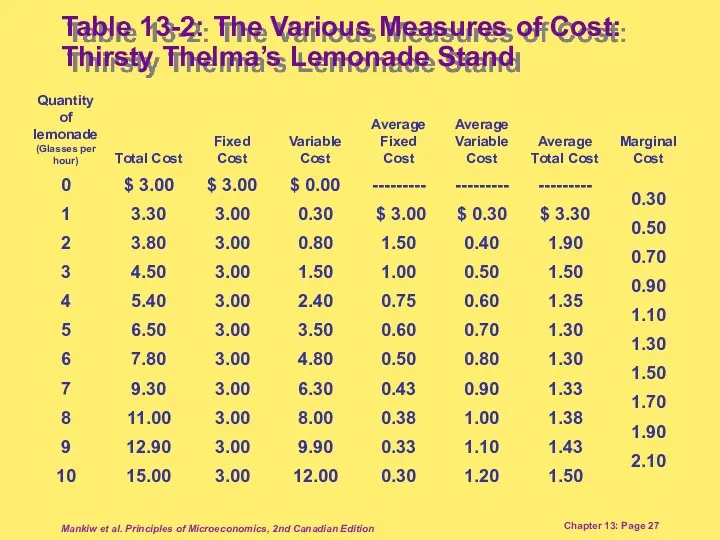

- 27. Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition Chapter 13: Page Table 13-2: The Various

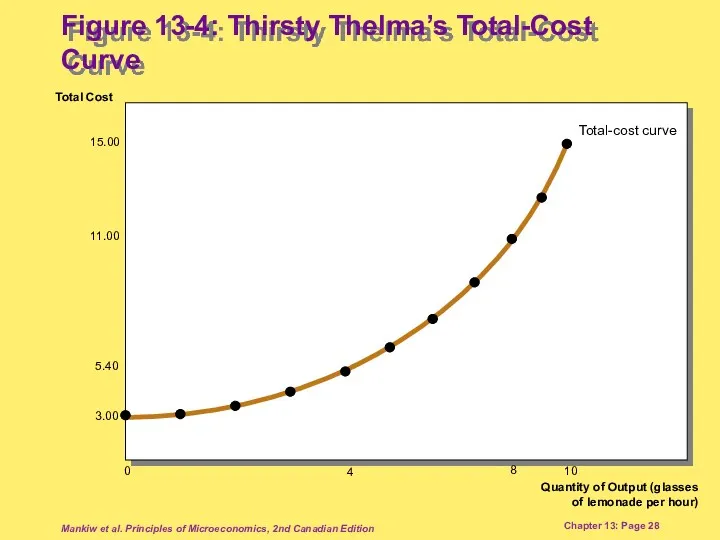

- 28. Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition Chapter 13: Page Total Cost Quantity of

- 29. Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition Chapter 13: Page Cost Curves and their

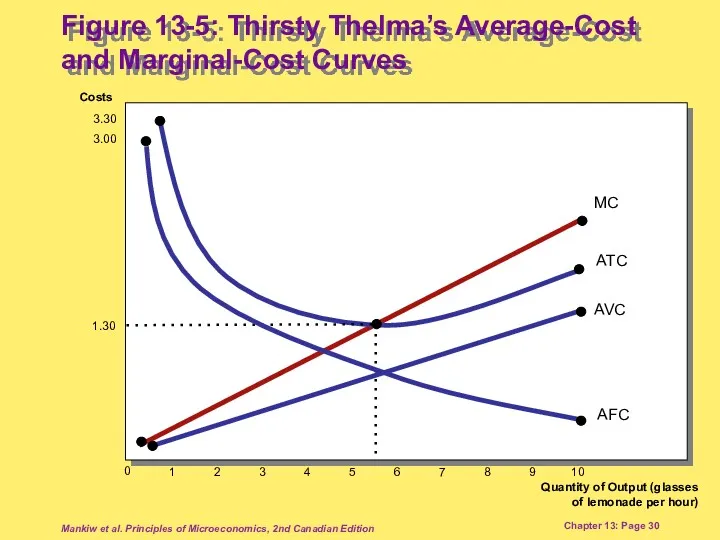

- 30. Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition Chapter 13: Page Costs Quantity of Output

- 31. Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition Chapter 13: Page Marginal cost rises with

- 32. Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition Chapter 13: Page Cost Curves and their

- 33. Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition Chapter 13: Page Typical Cost Curves In

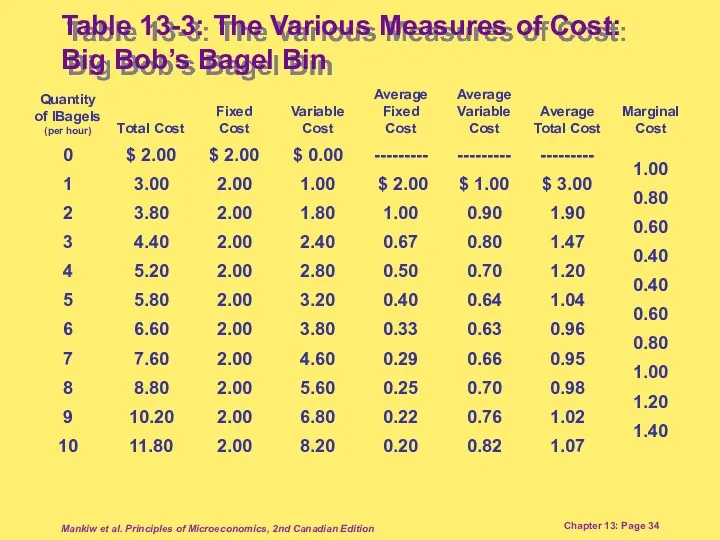

- 34. Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition Chapter 13: Page Table 13-3: The Various

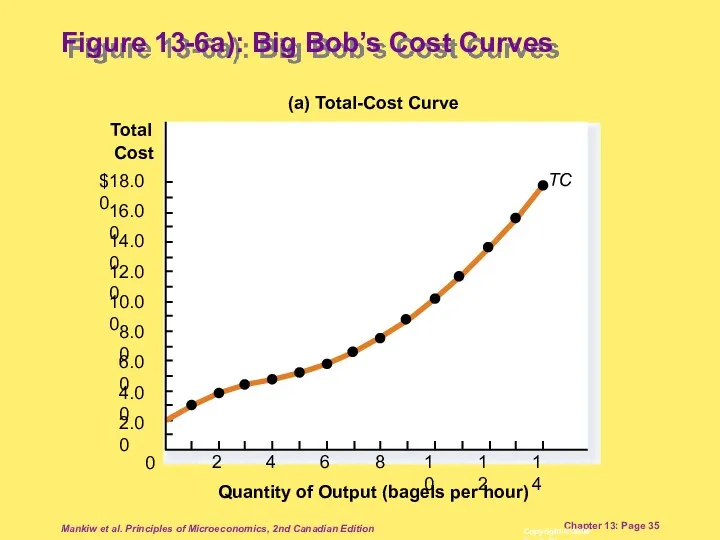

- 35. Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition Chapter 13: Page Figure 13-6a): Big Bob’s

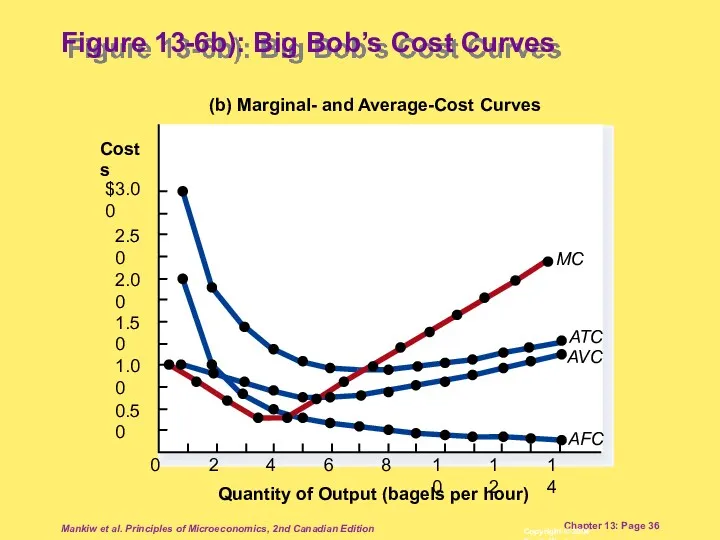

- 36. Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition Chapter 13: Page Figure 13-6b): Big Bob’s

- 37. Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition Chapter 13: Page Typical Cost Curves Three

- 38. Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition Chapter 13: Page THE RELATIONSHIP BETWEEN THE

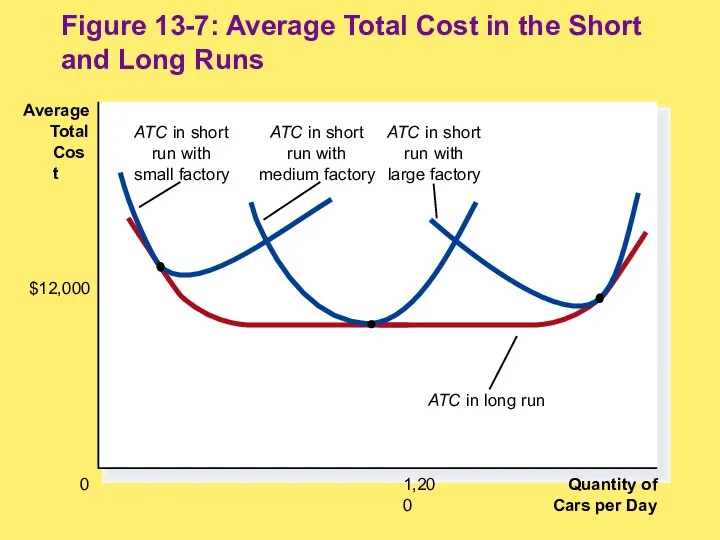

- 39. Quantity of Cars per Day 0 Average Total Cost 1,200 $12,000 Figure 13-7: Average Total Cost

- 40. Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition Chapter 13: Page Economies and Diseconomies of

- 41. Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition Chapter 13: Page Summary The goal of

- 42. Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition Chapter 13: Page Summary A firm’s costs

- 43. Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition Chapter 13: Page Summary A firm’s total

- 44. Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition Chapter 13: Page Summary Marginal cost is

- 45. Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition Chapter 13: Page Summary The average-total-cost curve

- 47. Скачать презентацию

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Quantity of

Cars per Day

0

Average

Total

Cost

1,200

$12,000

Figure 13-7: Average Total Cost in the Short

Quantity of

Cars per Day

0

Average

Total

Cost

1,200

$12,000

Figure 13-7: Average Total Cost in the Short

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Mankiw et al. Principles of Microeconomics, 2nd Canadian Edition

Chapter 13: Page

Глобальные проблемы мира и пути их решения

Глобальные проблемы мира и пути их решения Макроэкономические показатели. Тема 4

Макроэкономические показатели. Тема 4 Сибирский федеральный округ

Сибирский федеральный округ Традиционная аграрная экономика

Традиционная аграрная экономика Государственный бюджет

Государственный бюджет Развитие Дальнего Востока в первой половине XXI века

Развитие Дальнего Востока в первой половине XXI века Влияние инфляции на семейную экономику

Влияние инфляции на семейную экономику Перспективы североамериканской интеграции. НАФТА

Перспективы североамериканской интеграции. НАФТА Содержание предпринимательской деятельности

Содержание предпринимательской деятельности Собственность и экономические системы. (Тема 3)

Собственность и экономические системы. (Тема 3) Расходы и прибыль фирмы

Расходы и прибыль фирмы Введение в микроэкономику

Введение в микроэкономику Марі Еспрі Леон Вальрас

Марі Еспрі Леон Вальрас Государственное регулирование экономики, её сущность

Государственное регулирование экономики, её сущность bezrabotica

bezrabotica Рынок капитала. Предпринимательская способность и экономическая прибыль

Рынок капитала. Предпринимательская способность и экономическая прибыль Португалия

Португалия Типы экономических систем

Типы экономических систем Предпринимательство и фирма

Предпринимательство и фирма Индустрия 4.0. Четвертая промышленная революция

Индустрия 4.0. Четвертая промышленная революция Экономика. Экономические блага и ресурсы

Экономика. Экономические блага и ресурсы Фискальная(налоговобюджетная) политика государства. Тема 4

Фискальная(налоговобюджетная) политика государства. Тема 4 Международные корпорации

Международные корпорации Социальное предпринимательство

Социальное предпринимательство Производственный процесс, технологический процесс, их элементы и организация

Производственный процесс, технологический процесс, их элементы и организация Управление затратами предприятия (на примере ООО РЕГИОН-СТРОЙ)

Управление затратами предприятия (на примере ООО РЕГИОН-СТРОЙ) Підвищення конкурнетоспроможності підприємств житлово-комунального господарства

Підвищення конкурнетоспроможності підприємств житлово-комунального господарства Кривая IS

Кривая IS