- Chapter 17. Options markets: introduction

Содержание

- 2. 17- Derivatives are securities that get their value from the price of other securities. Derivatives are

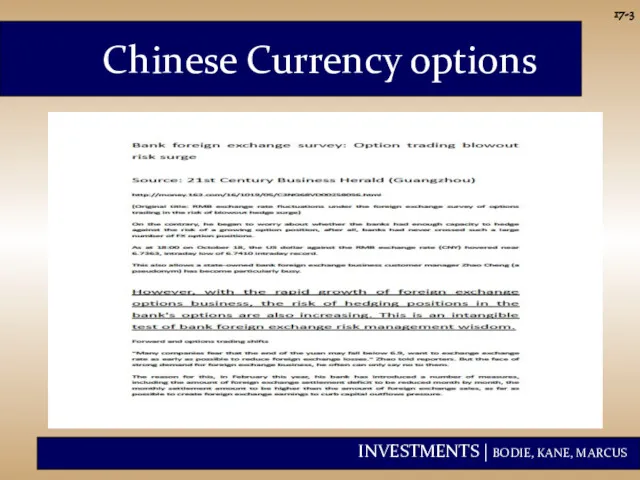

- 3. Chinese Currency options 17-

- 4. 17- The Option Contract: Calls A call option gives its holder the right to buy an

- 5. Option quotation 17-

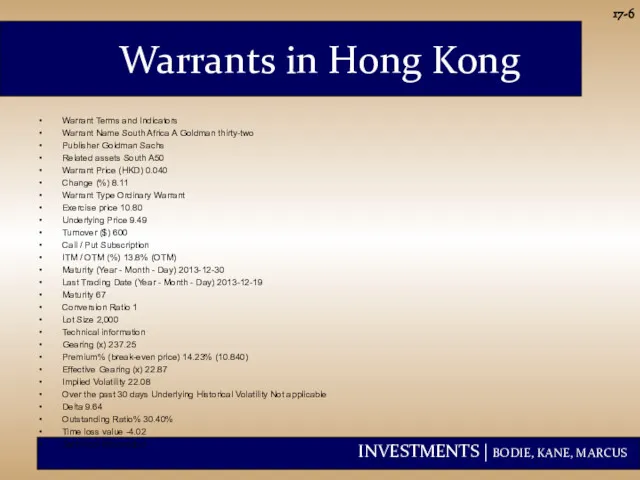

- 6. Warrants in Hong Kong Warrant Terms and Indicators Warrant Name South Africa A Goldman thirty-two Publisher

- 7. The Chinese Warrants Bubble, by Wei Xiong et al. In 2005-2008, over a dozen put warrants

- 8. 17- The Option Contract: Puts A put option gives its holder the right to sell an

- 9. 17- The Option Contract The purchase price of the option is called the premium. Sellers (writers)

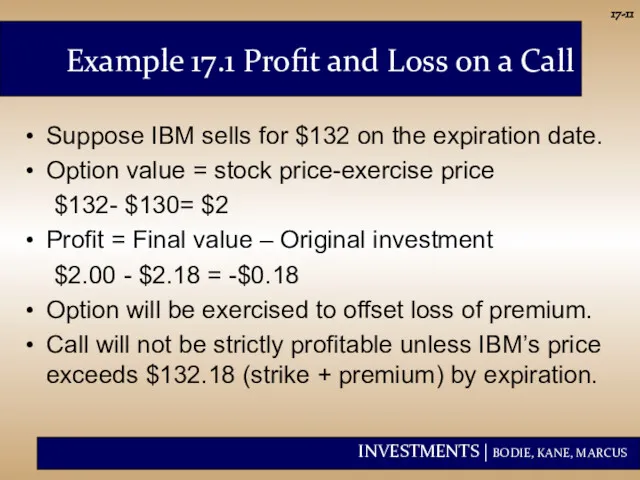

- 10. 17- Example 17.1 Profit and Loss on a Call A January 2010 call on IBM with

- 11. 17- Example 17.1 Profit and Loss on a Call Suppose IBM sells for $132 on the

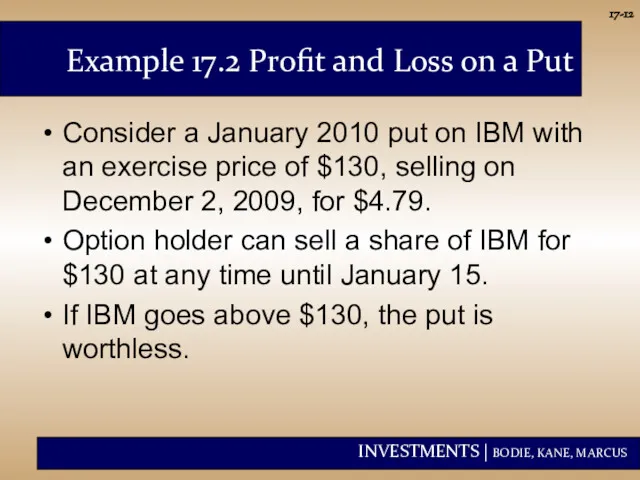

- 12. 17- Example 17.2 Profit and Loss on a Put Consider a January 2010 put on IBM

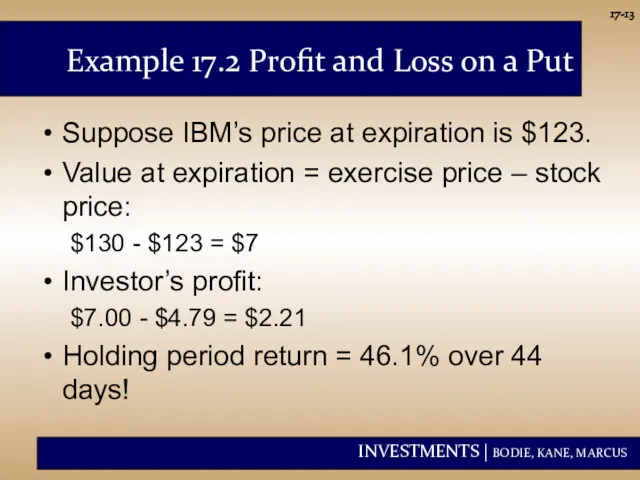

- 13. 17- Example 17.2 Profit and Loss on a Put Suppose IBM’s price at expiration is $123.

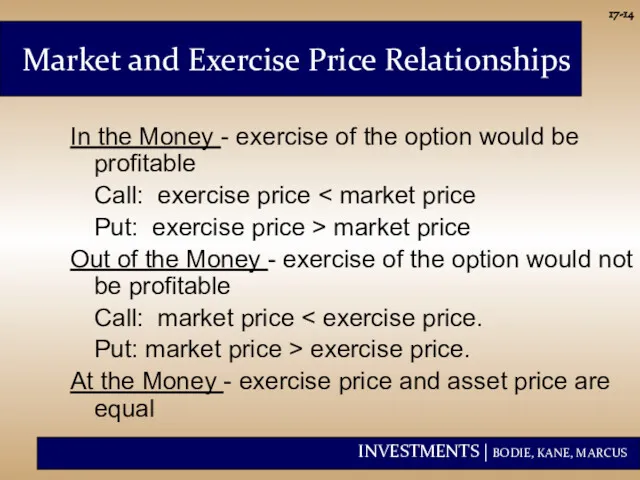

- 14. 17- In the Money - exercise of the option would be profitable Call: exercise price Put:

- 15. 17- American - the option can be exercised at any time before expiration or maturity European

- 16. 17- Stock Options Index Options Futures Options Foreign Currency Options (e.g. Chinese Currency options) Interest Rate

- 17. 17- Notation Stock Price = ST Exercise Price = X Payoff to Call Holder (ST -

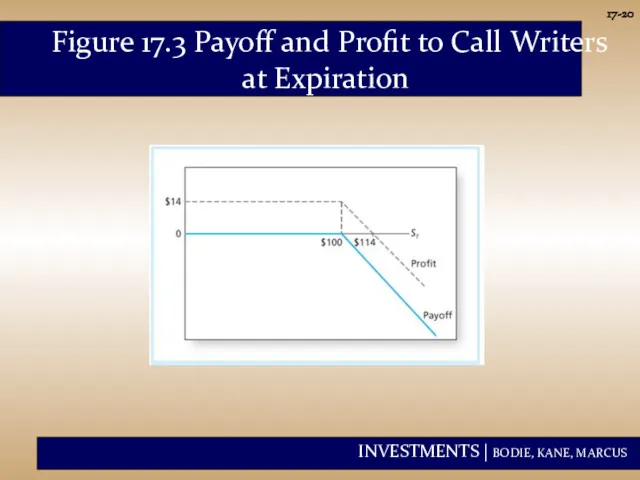

- 18. 17- Payoff to Call Writer - (ST - X) if ST >X 0 if ST Profit

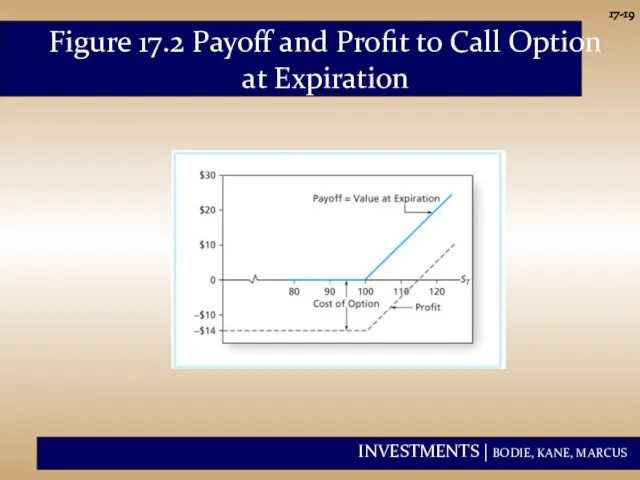

- 19. 17- Figure 17.2 Payoff and Profit to Call Option at Expiration

- 20. 17- Figure 17.3 Payoff and Profit to Call Writers at Expiration

- 21. 17- Payoffs to Put Holder 0 if ST > X (X - ST) if ST Profit

- 22. 17- Payoffs to Put Writer 0 if ST > X -(X - ST) if ST Profits

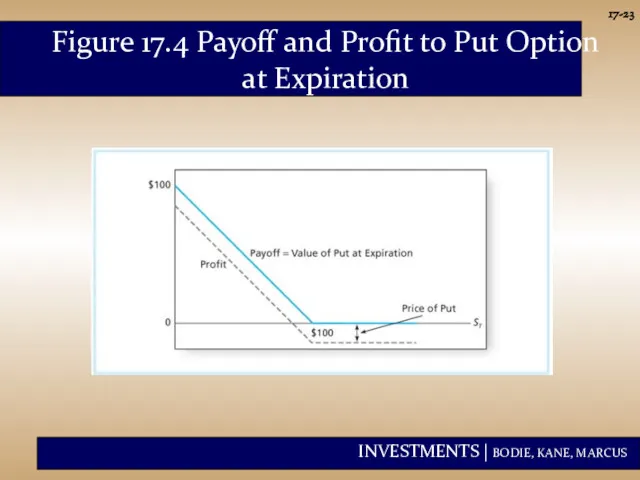

- 23. 17- Figure 17.4 Payoff and Profit to Put Option at Expiration

- 24. 17- Option versus Stock Investments Could a call option strategy be preferable to a direct stock

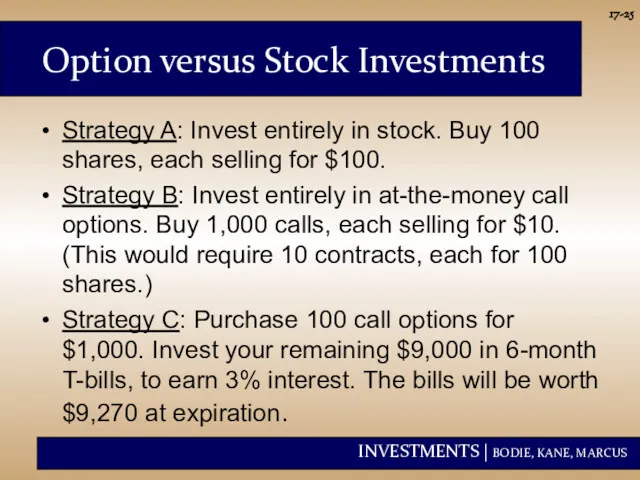

- 25. 17- Option versus Stock Investments Strategy A: Invest entirely in stock. Buy 100 shares, each selling

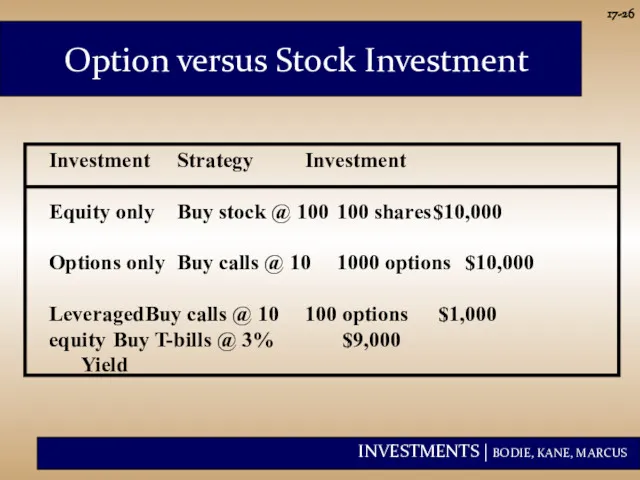

- 26. 17- Investment Strategy Investment Equity only Buy stock @ 100 100 shares $10,000 Options only Buy

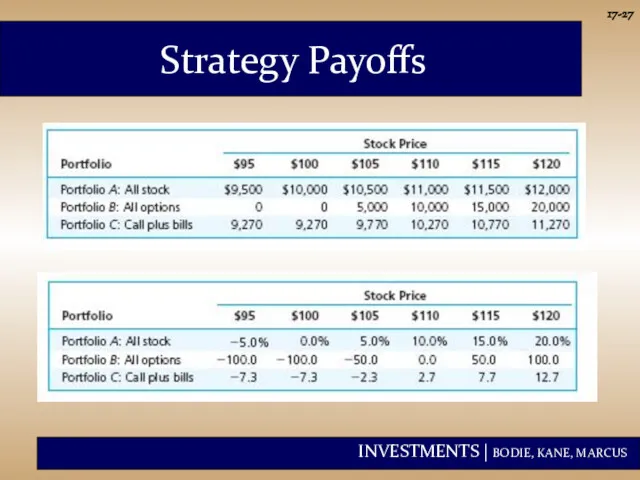

- 27. 17- Strategy Payoffs

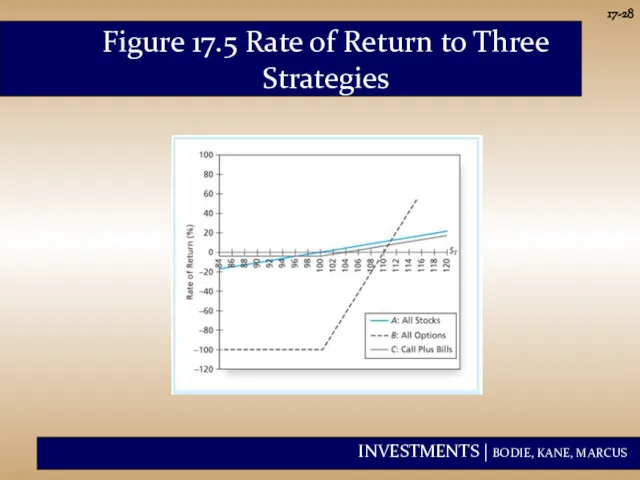

- 28. 17- Figure 17.5 Rate of Return to Three Strategies

- 29. 17- Strategy Conclusions Figure 17.5 shows that the all-option portfolio, B, responds more than proportionately to

- 30. 17- Protective Put Conclusions Puts can be used as insurance against stock price declines. Protective puts

- 31. 17- Covered Calls Purchase stock and write calls against it. Call writer gives up any stock

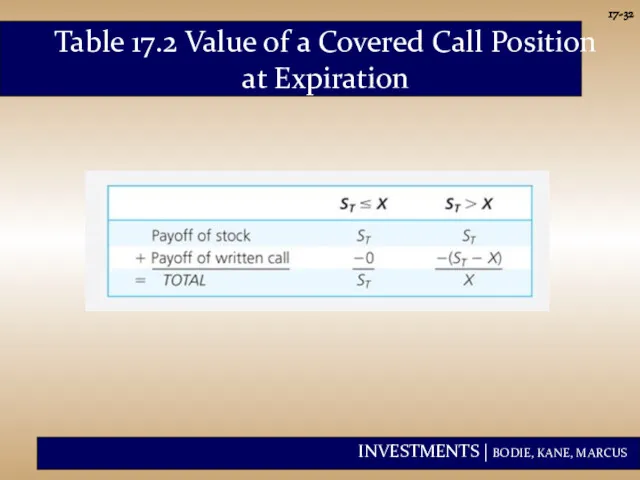

- 32. 17- Table 17.2 Value of a Covered Call Position at Expiration

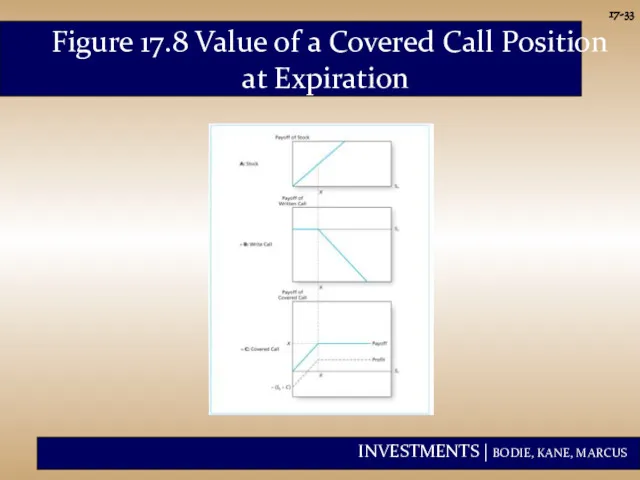

- 33. 17- Figure 17.8 Value of a Covered Call Position at Expiration

- 34. 17- Straddle Long straddle: Buy call and put with same exercise price and maturity. The straddle

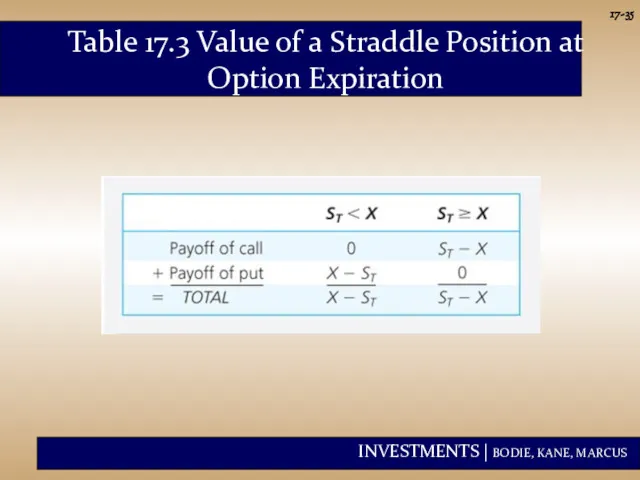

- 35. 17- Table 17.3 Value of a Straddle Position at Option Expiration

- 36. 17- Figure 17.9 Value of a Straddle at Expiration

- 37. 17- Spreads A spread is a combination of two or more calls (or two or more

- 38. 17- Table 17.4 Value of a Bullish Spread Position at Expiration

- 39. 17- Figure 17.10 Value of a Bullish Spread Position at Expiration

- 40. 17- Collars A collar is an options strategy that brackets the value of a portfolio between

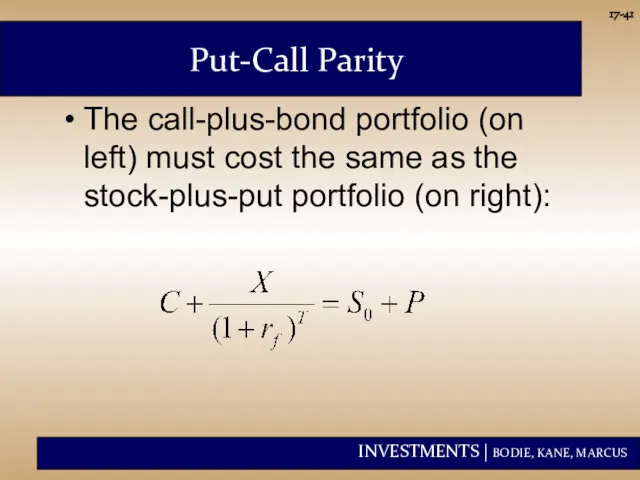

- 41. 17- The call-plus-bond portfolio (on left) must cost the same as the stock-plus-put portfolio (on right):

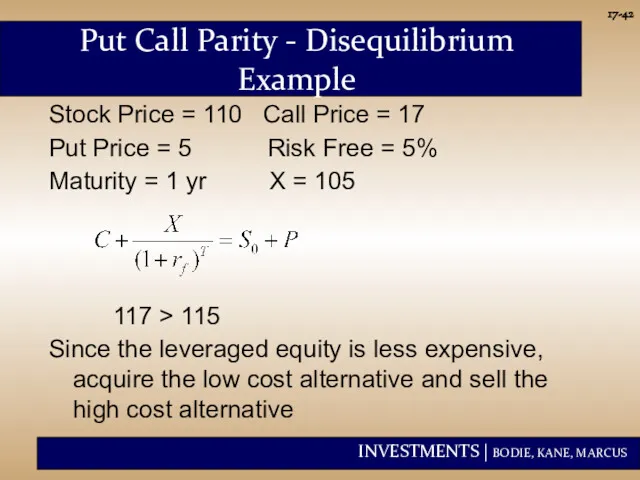

- 42. 17- Stock Price = 110 Call Price = 17 Put Price = 5 Risk Free =

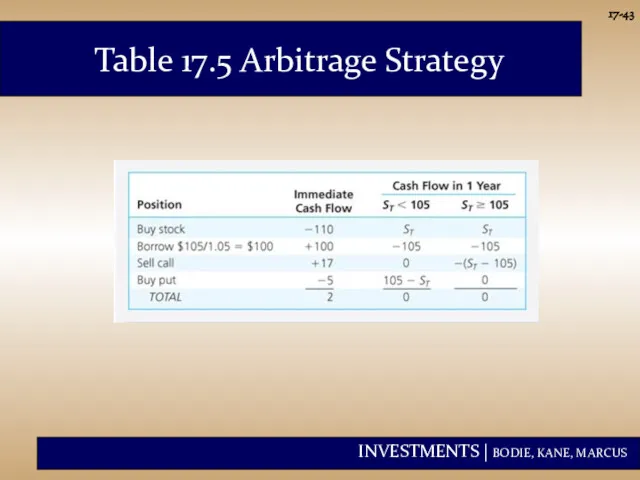

- 43. 17- Table 17.5 Arbitrage Strategy

- 45. Скачать презентацию

17-

Derivatives are securities that get their value from the price of

17-

Derivatives are securities that get their value from the price of

Chinese Currency options

17-

Chinese Currency options

17-

17-

The Option Contract: Calls

A call option gives its holder the right

17-

The Option Contract: Calls

A call option gives its holder the right

Option quotation

17-

Option quotation

17-

Warrants in Hong Kong

Warrant Terms and Indicators

Warrant Name South Africa A

Warrants in Hong Kong

Warrant Terms and Indicators

Warrant Name South Africa A

The Chinese Warrants Bubble, by Wei Xiong et al.

In 2005-2008, over

The Chinese Warrants Bubble, by Wei Xiong et al.

In 2005-2008, over

17-

The Option Contract: Puts

A put option gives its holder the right

17-

The Option Contract: Puts

A put option gives its holder the right

17-

The Option Contract

The purchase price of the option is called the

17-

The Option Contract

The purchase price of the option is called the

17-

Example 17.1 Profit and Loss on a Call

A January 2010 call

17-

Example 17.1 Profit and Loss on a Call

A January 2010 call

17-

Example 17.1 Profit and Loss on a Call

Suppose IBM sells for

17-

Example 17.1 Profit and Loss on a Call

Suppose IBM sells for

17-

Example 17.2 Profit and Loss on a Put

Consider a January 2010

17-

Example 17.2 Profit and Loss on a Put

Consider a January 2010

17-

Example 17.2 Profit and Loss on a Put

Suppose IBM’s price at

17-

Example 17.2 Profit and Loss on a Put

Suppose IBM’s price at

17-

In the Money - exercise of the option would be profitable

Call:

17-

In the Money - exercise of the option would be profitable

Call:

17-

American - the option can be exercised at any time before

17-

American - the option can be exercised at any time before

17-

Stock Options

Index Options

Futures Options

Foreign Currency Options (e.g. Chinese Currency options)

Interest Rate

17-

Stock Options

Index Options

Futures Options

Foreign Currency Options (e.g. Chinese Currency options)

Interest Rate

17-

Notation

Stock Price = ST Exercise Price = X

Payoff to Call

17-

Notation

Stock Price = ST Exercise Price = X

Payoff to Call

17-

Payoff to Call Writer

- (ST - X) if ST >X

17-

Payoff to Call Writer

- (ST - X) if ST >X

17-

Figure 17.2 Payoff and Profit to Call Option at Expiration

17-

Figure 17.2 Payoff and Profit to Call Option at Expiration

17-

Figure 17.3 Payoff and Profit to Call Writers at Expiration

17-

Figure 17.3 Payoff and Profit to Call Writers at Expiration

17-

Payoffs to Put Holder

0 if ST > X

(X - ST) if ST

17-

Payoffs to Put Holder

0 if ST > X

(X - ST) if ST

17-

Payoffs to Put Writer

0 if ST > X

-(X - ST) if ST <

17-

Payoffs to Put Writer

0 if ST > X

-(X - ST) if ST <

17-

Figure 17.4 Payoff and Profit to Put Option at Expiration

17-

Figure 17.4 Payoff and Profit to Put Option at Expiration

17-

Option versus Stock Investments

Could a call option strategy be preferable to

17-

Option versus Stock Investments

Could a call option strategy be preferable to

17-

Option versus Stock Investments

Strategy A: Invest entirely in stock. Buy 100

17-

Option versus Stock Investments

Strategy A: Invest entirely in stock. Buy 100

17-

Investment Strategy Investment

Equity only Buy stock @ 100 100 shares $10,000

Options only Buy calls @ 10 1000 options $10,000

Leveraged Buy

17-

Investment Strategy Investment

Equity only Buy stock @ 100 100 shares $10,000

Options only Buy calls @ 10 1000 options $10,000

Leveraged Buy

17-

Strategy Payoffs

17-

Strategy Payoffs

17-

Figure 17.5 Rate of Return to Three Strategies

17-

Figure 17.5 Rate of Return to Three Strategies

17-

Strategy Conclusions

Figure 17.5 shows that the all-option portfolio, B, responds more

17-

Strategy Conclusions

Figure 17.5 shows that the all-option portfolio, B, responds more

17-

Protective Put Conclusions

Puts can be used as insurance against stock price

17-

Protective Put Conclusions

Puts can be used as insurance against stock price

17-

Covered Calls

Purchase stock and write calls against it.

Call writer gives up

17-

Covered Calls

Purchase stock and write calls against it.

Call writer gives up

17-

Table 17.2 Value of a Covered Call Position at Expiration

17-

Table 17.2 Value of a Covered Call Position at Expiration

17-

Figure 17.8 Value of a Covered Call Position at Expiration

17-

Figure 17.8 Value of a Covered Call Position at Expiration

17-

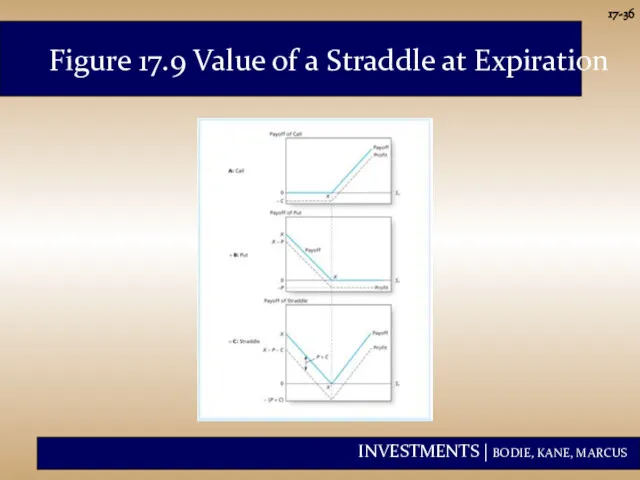

Straddle

Long straddle: Buy call and put with same exercise price and

17-

Straddle

Long straddle: Buy call and put with same exercise price and

17-

Table 17.3 Value of a Straddle Position at Option Expiration

17-

Table 17.3 Value of a Straddle Position at Option Expiration

17-

Figure 17.9 Value of a Straddle at Expiration

17-

Figure 17.9 Value of a Straddle at Expiration

17-

Spreads

A spread is a combination of two or more calls (or

17-

Spreads

A spread is a combination of two or more calls (or

17-

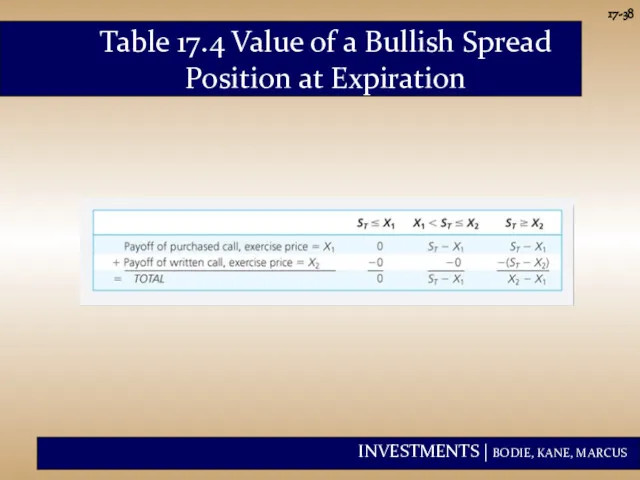

Table 17.4 Value of a Bullish Spread Position at Expiration

17-

Table 17.4 Value of a Bullish Spread Position at Expiration

17-

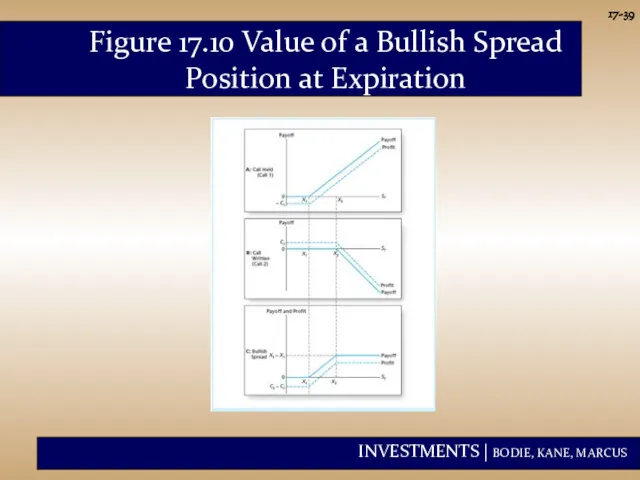

Figure 17.10 Value of a Bullish Spread Position at Expiration

17-

Figure 17.10 Value of a Bullish Spread Position at Expiration

17-

Collars

A collar is an options strategy that brackets the value of

17-

Collars

A collar is an options strategy that brackets the value of

17-

The call-plus-bond portfolio (on left) must cost the same as the

17-

The call-plus-bond portfolio (on left) must cost the same as the

17-

Stock Price = 110 Call Price = 17

Put Price = 5

17-

Stock Price = 110 Call Price = 17

Put Price = 5

17-

Table 17.5 Arbitrage Strategy

17-

Table 17.5 Arbitrage Strategy

Заключительные положения управления проектами. Эффективность управления проектами

Заключительные положения управления проектами. Эффективность управления проектами История развития экономической мысли

История развития экономической мысли Основные сквозные технологии цифровой экономики. Большие данные

Основные сквозные технологии цифровой экономики. Большие данные Циклічність економічного розвитку

Циклічність економічного розвитку Государственное регулирование экономики, её сущность

Государственное регулирование экономики, её сущность Основы теории потребления

Основы теории потребления Понятие, содержание и субъекты экономической деятельности и экономических отношений

Понятие, содержание и субъекты экономической деятельности и экономических отношений Показатели рентабельности

Показатели рентабельности Платежи при недропользовании в РФ

Платежи при недропользовании в РФ Глобальні проблеми людства

Глобальні проблеми людства Экономика строительной отрасли

Экономика строительной отрасли Общественное благосостояние и система показателей уровня и качества жизни как важнейшие категории социального государства

Общественное благосостояние и система показателей уровня и качества жизни как важнейшие категории социального государства Итоги выполнения основных экономических показателей деятельности ФГУП СВЯЗЬ - безопасность

Итоги выполнения основных экономических показателей деятельности ФГУП СВЯЗЬ - безопасность Финансирование инвестиционного проекта. Лекция 6. Инвестиционный анализ

Финансирование инвестиционного проекта. Лекция 6. Инвестиционный анализ Модель Кагана

Модель Кагана Организация и механизмы торговли на розничном рынке электроэнергии

Организация и механизмы торговли на розничном рынке электроэнергии Viduseiropas valstis

Viduseiropas valstis Международная торговля и право ВТО (всемирная торговая организация)

Международная торговля и право ВТО (всемирная торговая организация) Человек и экономика. Семейный бюджет (7 класс)

Человек и экономика. Семейный бюджет (7 класс) Типологизация регионов России. Старопромышленные регоны

Типологизация регионов России. Старопромышленные регоны Роль экономики в жизни общества

Роль экономики в жизни общества Управление ассортиментом продукции торгового предприятия

Управление ассортиментом продукции торгового предприятия Основы квалиметрии

Основы квалиметрии Макроэкономические показатели. Тема 4

Макроэкономические показатели. Тема 4 Инвестиционный паспорт Татищевского муниципального района Саратовской области

Инвестиционный паспорт Татищевского муниципального района Саратовской области Сущность и особенности международной экономической деятельности

Сущность и особенности международной экономической деятельности Стратегии в сфере финансового и денежно-кредитного регулирования

Стратегии в сфере финансового и денежно-кредитного регулирования Экономическое развитие России в начале XX века

Экономическое развитие России в начале XX века