- Competition Law: Mergers

Содержание

- 2. Core Provisions: Article 101 of the TFEU Article 102 of the TFEU Article 106 of the

- 3. Framework Legislation Council Regulation (EC) No 139/2004 of 20 January 2004 on the control of concentrations

- 4. One firm buys out the shares of another: concentration of economic power in the hands of

- 5. increase in market power, increased market share and decreased number of competitors Mergers : Benefits

- 6. Merger control is about predicting what the market might be like, not knowing and making a

- 7. Market shares of the merging companies (assessed and added); The Herfindahl-Hirschman Index (to calculate the “density”

- 8. Creation of efficiencies enough to outweigh any detriment; Technical and economic progress; A firm which is

- 9. USA: The Clayton Act EU: Art. 81 and 82 of the Treaty on EU 1973 –

- 10. “-” Mergers can have a marked impact on competition: Reduction of competition; Detriment for consumers; Stripping

- 11. “+” Enhancing economic efficiency: Easier to reap economies of scale; Enhancing distribution efficiency Enhancing managerial efficiency

- 12. Does the concentration significantly impede effective competition? (EU) Does the concentration substantially lessen competition? (US, UK)

- 13. A horizontal merger is one between parties that are competitors at the same level of production

- 14. Coordination is more likely to emerge in markets where it is relatively simple to reach a

- 15. Basic forms of non-horizontal mergers: vertical mergers and conglomerate mergers Non-horizontal Mergers

- 16. Between firms that operate at different but complementary levels in the chain of production (e.g., manufacturing

- 17. Conglomerate Mergers happen when companies acquire a large portfolio of related products, though without necessarily dominant

- 18. Mandatory regime - filing of a transaction is compulsory (majority of merger jurisdictions worldwide) “suspensory clause“

- 19. Merger Regulation is the legal base for controlling merger operations between enterprises Mergers are inevitable and

- 20. Merger Regulation will only be applicable if there is a concentration (Art. 3 (1)) Extra-territorial catch

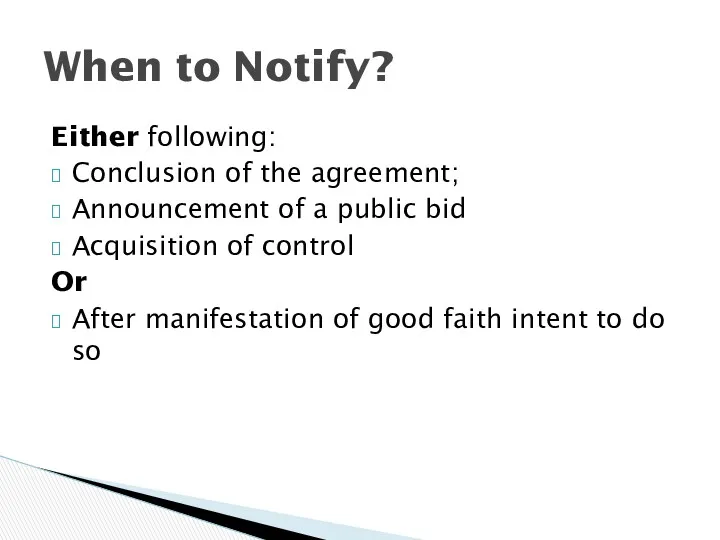

- 21. Either following: Conclusion of the agreement; Announcement of a public bid Acquisition of control Or After

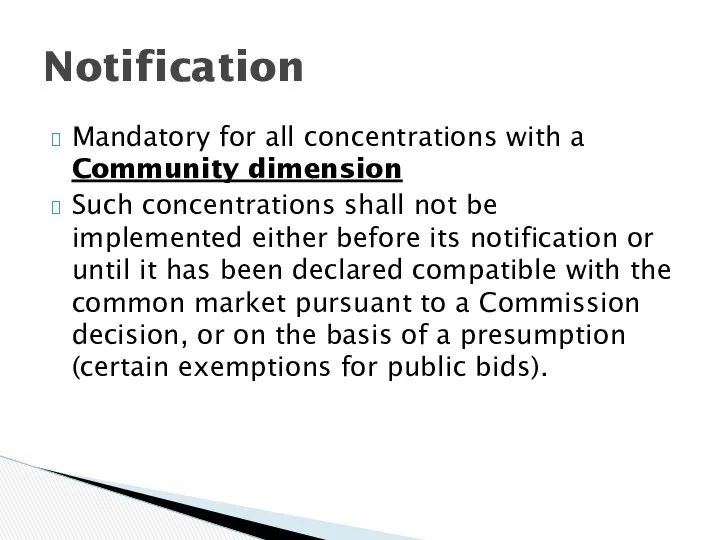

- 22. Mandatory for all concentrations with a Community dimension Such concentrations shall not be implemented either before

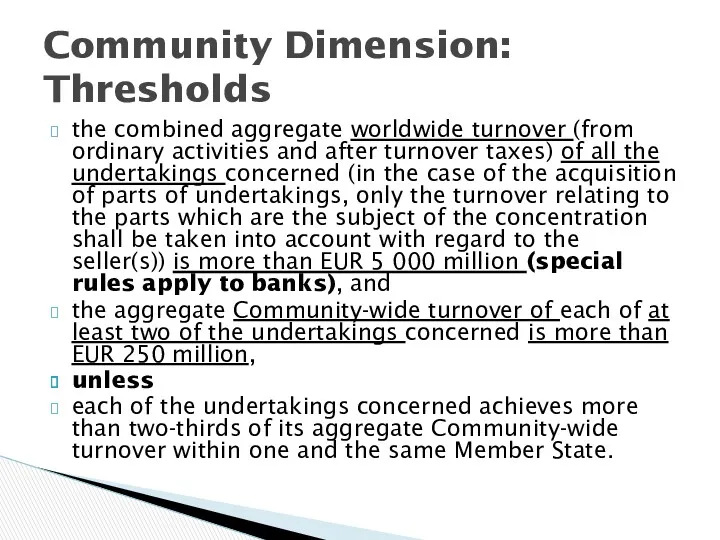

- 23. the combined aggregate worldwide turnover (from ordinary activities and after turnover taxes) of all the undertakings

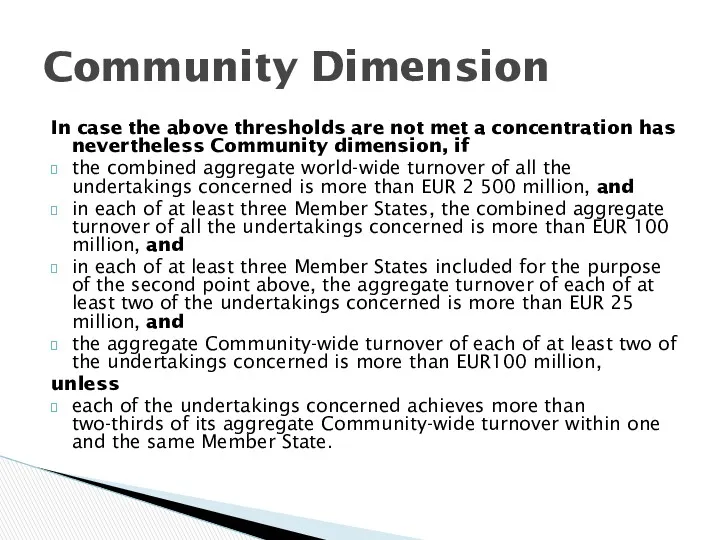

- 24. In case the above thresholds are not met a concentration has nevertheless Community dimension, if the

- 25. Phase I: Initial Examination (Phase I deadline commences on the date when the complete notification is

- 26. Detailed appraisal via: request for information, interviews, inspections carried out by the competent Authorities of the

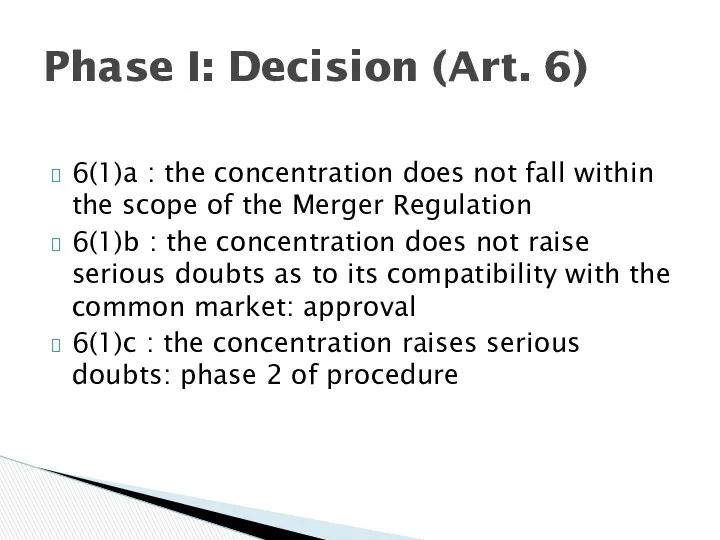

- 27. 6(1)a : the concentration does not fall within the scope of the Merger Regulation 6(1)b :

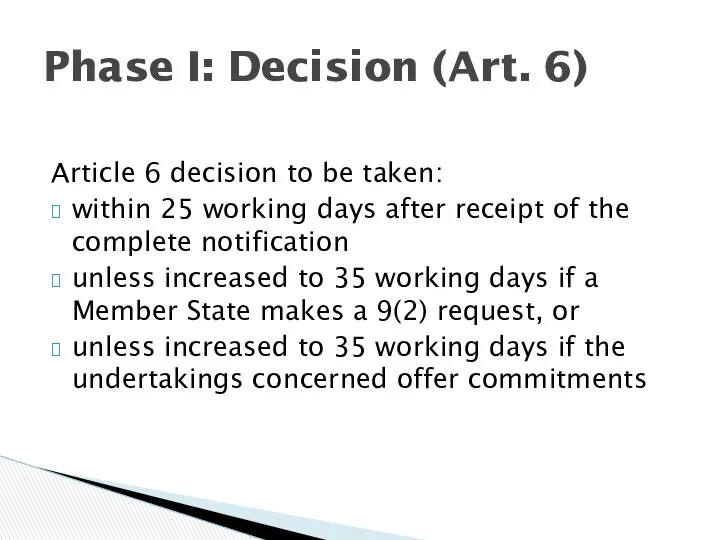

- 28. Article 6 decision to be taken: within 25 working days after receipt of the complete notification

- 29. Detailed appraisal via: request for information, interviews, inspections carried out by the competent Authorities of the

- 30. 8(1): approval in case of compatibility with the common market 8(2): approval with conditions and obligations

- 31. Two months from the date of the decision to lodge an appeal Possibility: Review by the

- 32. Mergers with a Community dimension are, in general, investigated only be the Commission (Art. 21 of

- 33. Cooperation between the European Union and the United States: Best practices on cooperation in merger cases

- 35. Скачать презентацию

Core Provisions:

Article 101 of the TFEU

Article 102 of the TFEU

Article 106

Core Provisions:

Article 101 of the TFEU

Article 102 of the TFEU

Article 106

Framework Legislation

Council Regulation (EC) No 139/2004 of 20 January 2004 on

Framework Legislation

Council Regulation (EC) No 139/2004 of 20 January 2004 on

One firm buys out the shares of another: concentration of economic

One firm buys out the shares of another: concentration of economic

increase in market power,

increased market share and

decreased number of competitors

Mergers :

increased market share and

decreased number of competitors

Mergers :

Merger control is about predicting what the market might be like,

Merger control is about predicting what the market might be like,

Market shares of the merging companies (assessed and added);

The Herfindahl-Hirschman Index

Market shares of the merging companies (assessed and added);

The Herfindahl-Hirschman Index

Creation of efficiencies enough to outweigh any detriment;

Technical and economic progress;

A

Creation of efficiencies enough to outweigh any detriment;

Technical and economic progress;

A

USA: The Clayton Act

EU:

Art. 81 and 82 of the Treaty

USA: The Clayton Act

EU:

Art. 81 and 82 of the Treaty

“-”

Mergers can have a marked impact on competition:

Reduction of competition;

Detriment for

“-”

Mergers can have a marked impact on competition:

Reduction of competition;

Detriment for

“+”

Enhancing economic efficiency:

Easier to reap economies of scale;

Enhancing distribution efficiency

Enhancing managerial

“+”

Enhancing economic efficiency:

Easier to reap economies of scale;

Enhancing distribution efficiency

Enhancing managerial

Does the concentration significantly impede effective competition? (EU)

Does the concentration substantially

Does the concentration significantly impede effective competition? (EU)

Does the concentration substantially

A horizontal merger is one between parties that are competitors at

A horizontal merger is one between parties that are competitors at

Coordination is more likely to emerge in markets where it is

Coordination is more likely to emerge in markets where it is

Basic forms of non-horizontal mergers:

vertical mergers and

conglomerate mergers

Non-horizontal Mergers

vertical mergers and

conglomerate mergers

Non-horizontal Mergers

Between firms that operate at different but complementary levels in the

Between firms that operate at different but complementary levels in the

Conglomerate Mergers happen when companies acquire a large portfolio of related

Conglomerate Mergers happen when companies acquire a large portfolio of related

Mandatory regime - filing of a transaction is compulsory (majority of

Mandatory regime - filing of a transaction is compulsory (majority of

Merger Regulation is the legal base for controlling merger operations between

Merger Regulation will only be applicable if there is a concentration

Merger Regulation will only be applicable if there is a concentration

Either following:

Conclusion of the agreement;

Announcement of a public bid

Acquisition of control

Or

After

Either following:

Conclusion of the agreement;

Announcement of a public bid

Acquisition of control

Or

After

Mandatory for all concentrations with a Community dimension

Such concentrations shall not

Mandatory for all concentrations with a Community dimension

Such concentrations shall not

the combined aggregate worldwide turnover (from ordinary activities and after turnover

the combined aggregate worldwide turnover (from ordinary activities and after turnover

In case the above thresholds are not met a concentration has

In case the above thresholds are not met a concentration has

Phase I: Initial Examination (Phase I deadline commences on the date

Phase I: Initial Examination (Phase I deadline commences on the date

Detailed appraisal via: request for information, interviews, inspections carried out by

6(1)a : the concentration does not fall within the scope of

Article 6 decision to be taken:

within 25 working days after receipt

within 25 working days after receipt

Detailed appraisal via: request for information, interviews, inspections carried out by

Detailed appraisal via: request for information, interviews, inspections carried out by

8(1): approval in case of compatibility with the common market

8(2): approval

8(1): approval in case of compatibility with the common market

8(2): approval

Two months from the date of the decision to lodge an

Two months from the date of the decision to lodge an

Бюджетная система США

Бюджетная система США Ұлттық экономикадағы қаржы және ақша-несие жүйесі

Ұлттық экономикадағы қаржы және ақша-несие жүйесі Демографическая ситуация и демографическая политика

Демографическая ситуация и демографическая политика Классификация товаров

Классификация товаров Основные модели рынка

Основные модели рынка Планирование показателей по труду, фонда заработной платы. УЭФ-Л 9

Планирование показателей по труду, фонда заработной платы. УЭФ-Л 9 Государственное регулирование экономики

Государственное регулирование экономики Ограниченность возможностей рынка

Ограниченность возможностей рынка Сущность инновационного пути развития

Сущность инновационного пути развития Макроэкономическое равновесие. Модель совокупный спрос - совокупное предложение

Макроэкономическое равновесие. Модель совокупный спрос - совокупное предложение Нестабильность. Инфляция и безработица. (Тема 11)

Нестабильность. Инфляция и безработица. (Тема 11) Безработица в России: общая характеристика, динамика, методы снижения

Безработица в России: общая характеристика, динамика, методы снижения Анализ и планирование финансовой деятельности

Анализ и планирование финансовой деятельности АО нефтяная компания Туймаада-нефть

АО нефтяная компания Туймаада-нефть Economic systems a set of rules made by a country that governs the production and distribution of goods and services

Economic systems a set of rules made by a country that governs the production and distribution of goods and services Мәңгілік ел жалпыұлттық идеясының құндылықтары

Мәңгілік ел жалпыұлттық идеясының құндылықтары Свободная торговля и протекционизм. Всемирная торговая организация (ВТО)

Свободная торговля и протекционизм. Всемирная торговая организация (ВТО) Олий таълим ташкилотларида кредитмодуль тизимини ташкил этиш

Олий таълим ташкилотларида кредитмодуль тизимини ташкил этиш Инновационная экономика. Государственная инновационная политика. (Лекция 7)

Инновационная экономика. Государственная инновационная политика. (Лекция 7) Итоги деятельности ФНС России за 2021 год

Итоги деятельности ФНС России за 2021 год Международные корпорации и их роль в мировой экономике

Международные корпорации и их роль в мировой экономике Нарықтық экономика жағдайында компанияның ішкі аудитін ұйымдастыру

Нарықтық экономика жағдайында компанияның ішкі аудитін ұйымдастыру Обществознание. Подготовка к ОГЭ. Общество как форма жизнедеятельности людей. Общество и природа

Обществознание. Подготовка к ОГЭ. Общество как форма жизнедеятельности людей. Общество и природа Презентация по экономике Государственные финансы

Презентация по экономике Государственные финансы Податок на додану вартість

Податок на додану вартість Институциональная теория фирмы. (Тема 9)

Институциональная теория фирмы. (Тема 9) Ущерб от чрезвычайных ситуаций

Ущерб от чрезвычайных ситуаций Экономический кругооборот. Экономические агенты

Экономический кругооборот. Экономические агенты