- Financial markets: Debt market in details. Lecture 6

Содержание

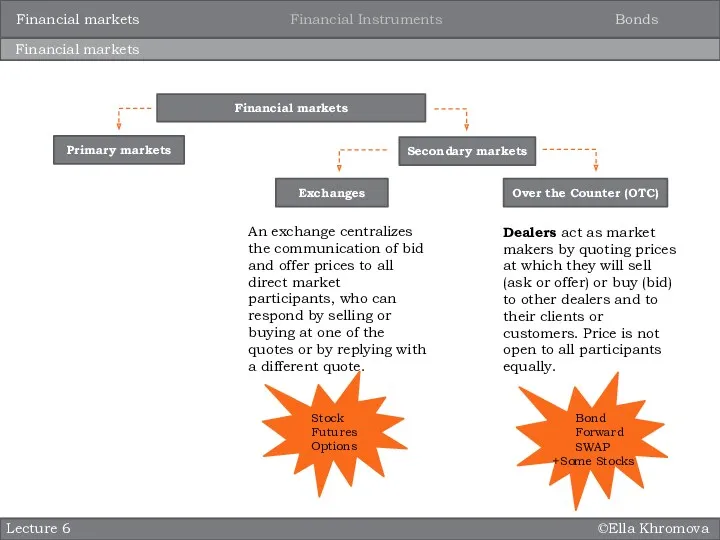

- 2. ©Ella Khromova Financial markets Bonds Financial Instruments Financial markets Lecture 6 Primary markets Secondary markets Over

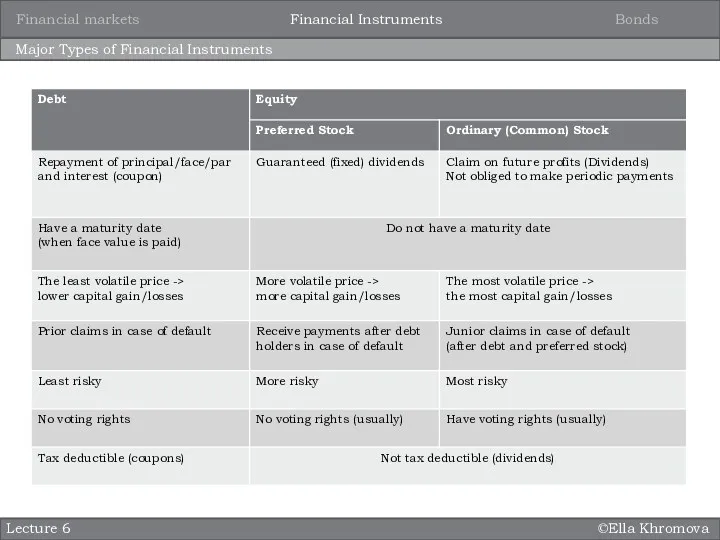

- 3. ©Ella Khromova Major Types of Financial Instruments Bonds Financial Instruments Financial markets Lecture 6

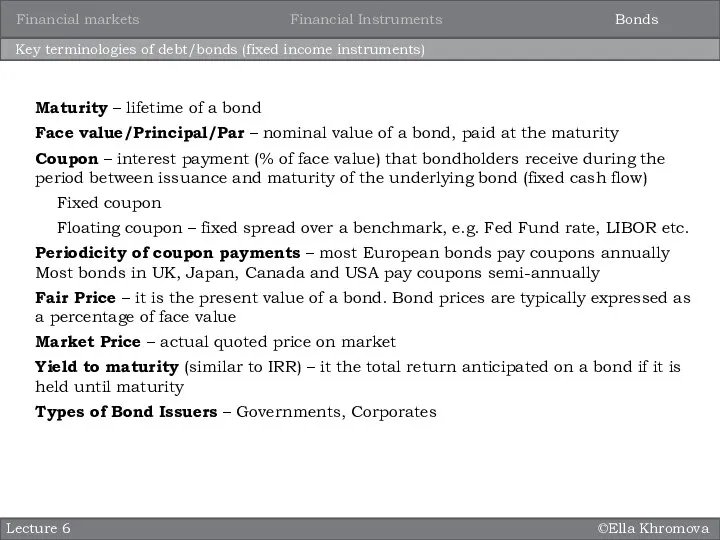

- 4. ©Ella Khromova Key terminologies of debt/bonds (fixed income instruments) Lecture 6 Maturity – lifetime of a

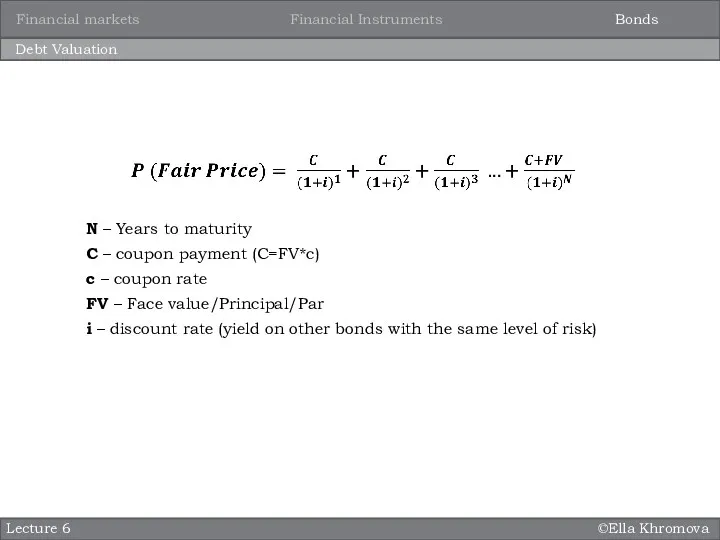

- 5. ©Ella Khromova Debt Valuation Lecture 6 N – Years to maturity C – coupon payment (C=FV*c)

- 6. ©Ella Khromova Debt Valuation: Example Lecture 6 French government bonds, known as OATs (short for Obligations

- 7. ©Ella Khromova Classification of bonds based on cash-flow Lecture 6 Straight/Bullet coupon bond – Periodic payments

- 8. ©Ella Khromova YTM Lecture 6 N – Years to maturity C – coupon payment (C=FV*c) c

- 9. ©Ella Khromova YTM: Example Lecture 6 French government bonds, known as OATs (short for Obligations Assimilables

- 10. ©Ella Khromova YTM: Quick calculation Lecture 6 French government bonds, known as OATs (short for Obligations

- 11. ©Ella Khromova Exercise 2 Practice 4 What is the intrinsic (fair) value for a 2 year

- 12. ©Ella Khromova Investment strategy Lecture 6 How to compare bonds? Where to invest? YTM Potential capital

- 13. ©Ella Khromova Bloomberg Lecture 6 Bonds Financial Instruments Financial markets

- 14. ©Ella Khromova Bloomberg Lecture 6 Bonds Financial Instruments Financial markets Change in price (modified duration)

- 15. ©Ella Khromova Exercise 1 Practice 4 Bonds LIBOR (London Interbank Offered Rate) is a benchmark rate

- 16. ©Ella Khromova Practice 4 Exercise 1 Bonds

- 17. ©Ella Khromova Practice 4 Exercise 1 Bonds

- 19. Скачать презентацию

©Ella Khromova

Financial markets

Bonds

Financial Instruments

Financial markets

Lecture 6

Primary markets

Secondary markets

Over the Counter (OTC)

An

©Ella Khromova

Financial markets

Bonds

Financial Instruments

Financial markets

Lecture 6

Primary markets

Secondary markets

Over the Counter (OTC)

An

©Ella Khromova

Major Types of Financial Instruments

Bonds

Financial Instruments

Financial markets

Lecture 6

©Ella Khromova

Major Types of Financial Instruments

Bonds

Financial Instruments

Financial markets

Lecture 6

©Ella Khromova

Key terminologies of debt/bonds (fixed income instruments)

Lecture 6

Maturity – lifetime

©Ella Khromova

Key terminologies of debt/bonds (fixed income instruments)

Lecture 6

Maturity – lifetime

©Ella Khromova

Debt Valuation

Lecture 6

N – Years to maturity

C – coupon payment

©Ella Khromova

Debt Valuation

Lecture 6

N – Years to maturity

C – coupon payment

©Ella Khromova

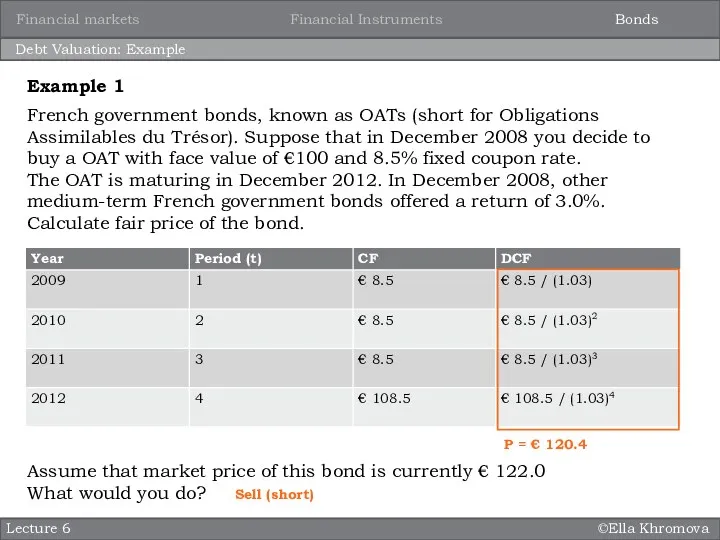

Debt Valuation: Example

Lecture 6

French government bonds, known as OATs (short

©Ella Khromova

Debt Valuation: Example

Lecture 6

French government bonds, known as OATs (short

©Ella Khromova

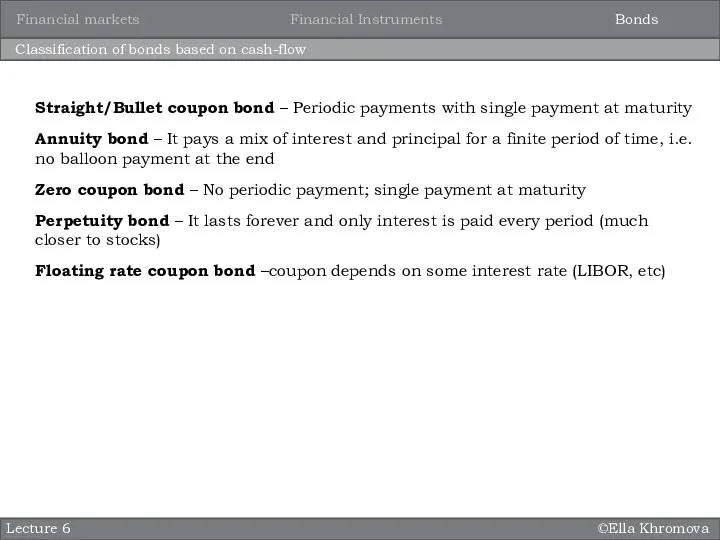

Classification of bonds based on cash-flow

Lecture 6

Straight/Bullet coupon bond –

©Ella Khromova

Classification of bonds based on cash-flow

Lecture 6

Straight/Bullet coupon bond –

©Ella Khromova

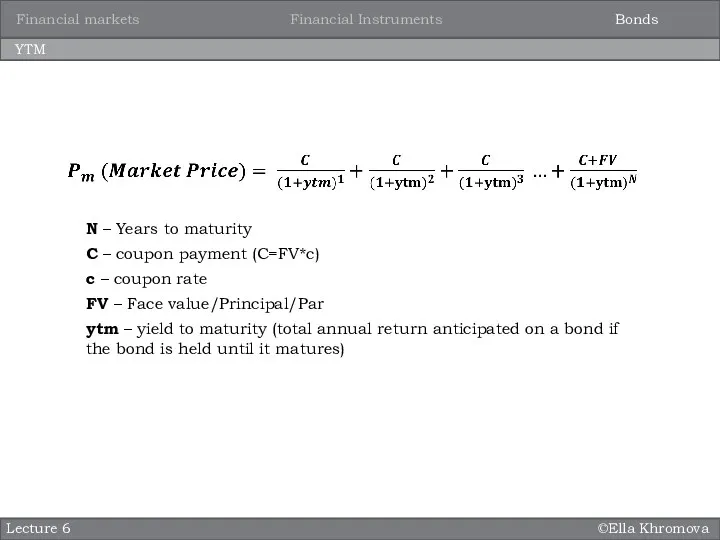

YTM

Lecture 6

N – Years to maturity

C – coupon payment (C=FV*c)

c

©Ella Khromova

YTM

Lecture 6

N – Years to maturity

C – coupon payment (C=FV*c)

c

©Ella Khromova

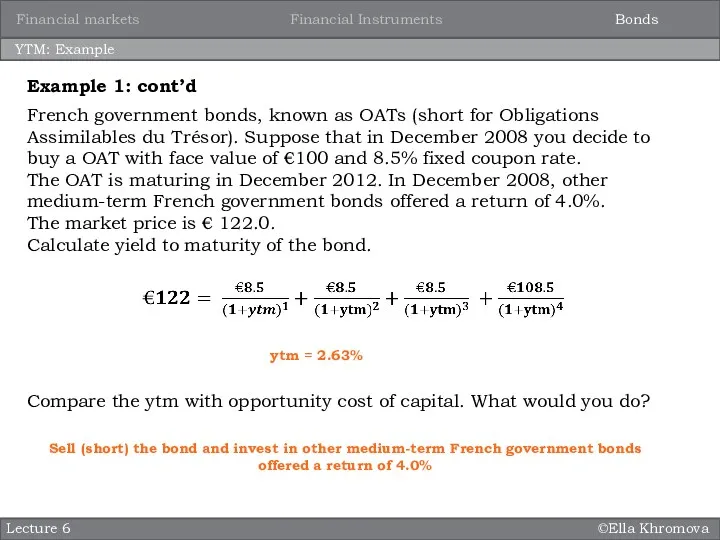

YTM: Example

Lecture 6

French government bonds, known as OATs (short for

©Ella Khromova

YTM: Example

Lecture 6

French government bonds, known as OATs (short for

©Ella Khromova

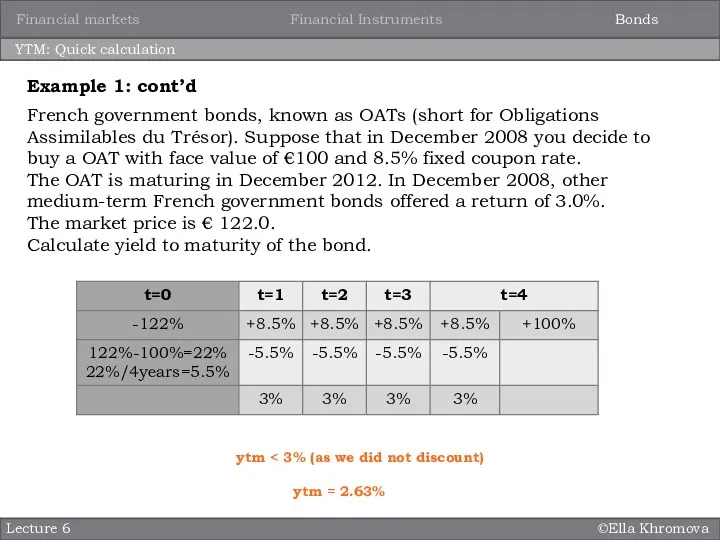

YTM: Quick calculation

Lecture 6

French government bonds, known as OATs (short

©Ella Khromova

YTM: Quick calculation

Lecture 6

French government bonds, known as OATs (short

©Ella Khromova

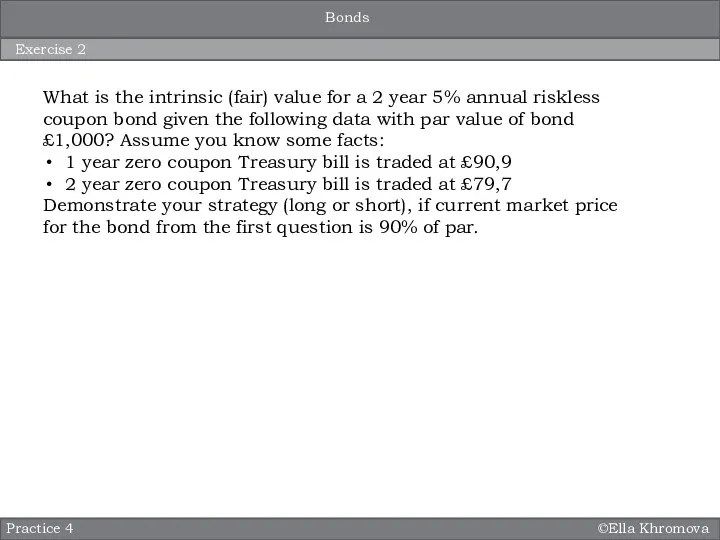

Exercise 2

Practice 4

What is the intrinsic (fair) value for a

©Ella Khromova

Exercise 2

Practice 4

What is the intrinsic (fair) value for a

©Ella Khromova

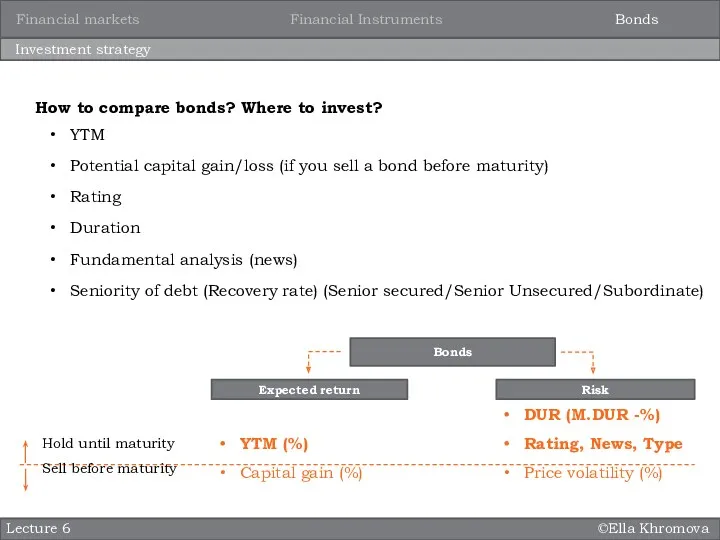

Investment strategy

Lecture 6

How to compare bonds? Where to invest?

YTM

Potential capital

©Ella Khromova

Investment strategy

Lecture 6

How to compare bonds? Where to invest?

YTM

Potential capital

©Ella Khromova

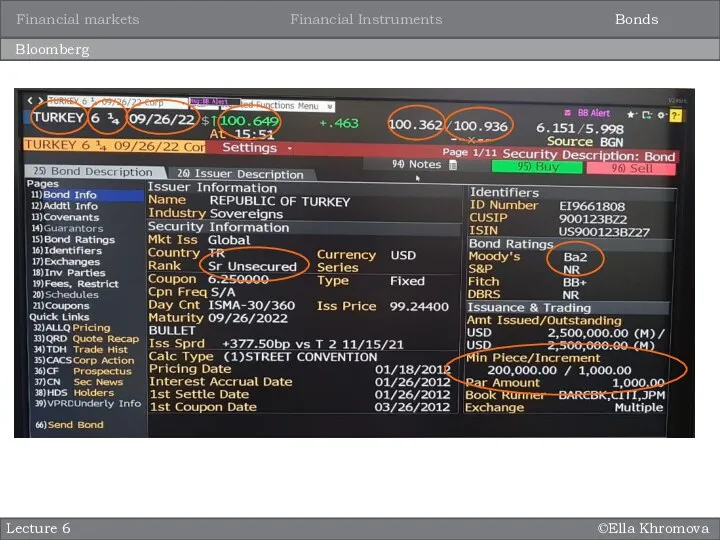

Bloomberg

Lecture 6

Bonds

Financial Instruments

Financial markets

©Ella Khromova

Bloomberg

Lecture 6

Bonds

Financial Instruments

Financial markets

©Ella Khromova

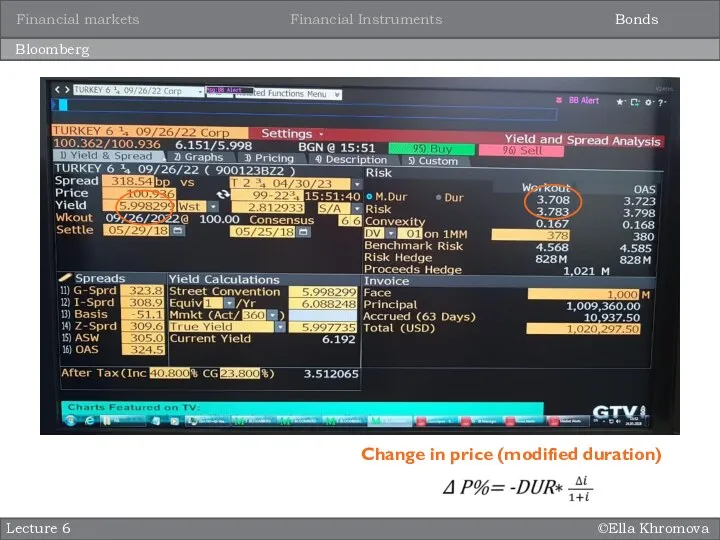

Bloomberg

Lecture 6

Bonds

Financial Instruments

Financial markets

Change in price (modified duration)

©Ella Khromova

Bloomberg

Lecture 6

Bonds

Financial Instruments

Financial markets

Change in price (modified duration)

©Ella Khromova

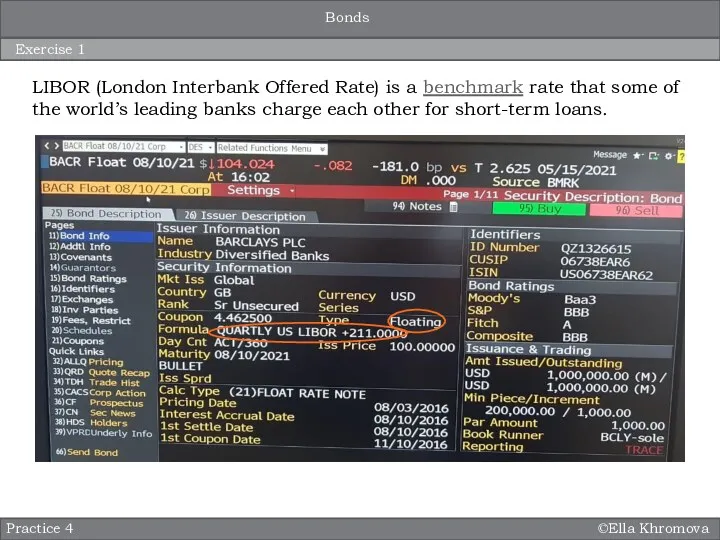

Exercise 1

Practice 4

Bonds

LIBOR (London Interbank Offered Rate) is a benchmark rate that

©Ella Khromova

Exercise 1

Practice 4

Bonds

LIBOR (London Interbank Offered Rate) is a benchmark rate that

©Ella Khromova

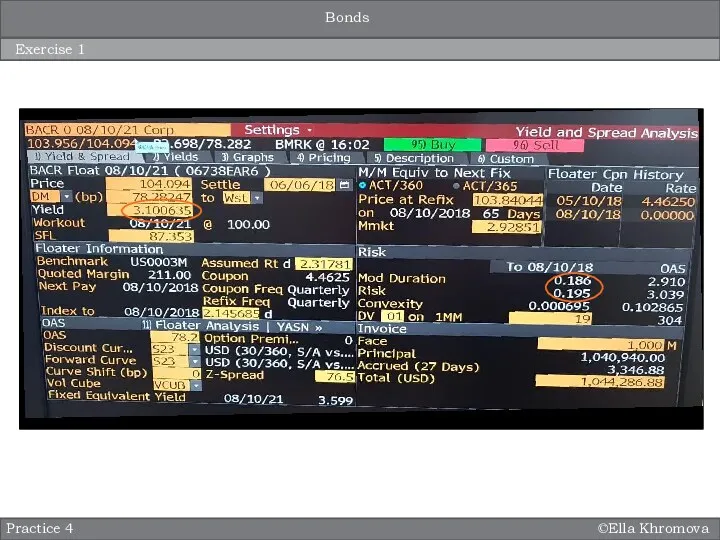

Practice 4

Exercise 1

Bonds

©Ella Khromova

Practice 4

Exercise 1

Bonds

©Ella Khromova

Practice 4

Exercise 1

Bonds

©Ella Khromova

Practice 4

Exercise 1

Bonds

Социальная сфера в системе национальной экономики

Социальная сфера в системе национальной экономики Совершенная конкуренция, как тип рынка

Совершенная конкуренция, как тип рынка Роль государства в обеспечении устойчивости и конкурентоспособности предприятий горнодобывающей отрасли Арктической зоны РФ

Роль государства в обеспечении устойчивости и конкурентоспособности предприятий горнодобывающей отрасли Арктической зоны РФ Общество как сложная динамическая система

Общество как сложная динамическая система Инфрақұрылым түсінігі

Инфрақұрылым түсінігі Энергосбережение и повышение энергетической эффективности

Энергосбережение и повышение энергетической эффективности Информационные ресурсы и технологии в экономике

Информационные ресурсы и технологии в экономике Дальневосточный федеральный округ

Дальневосточный федеральный округ Статус территории опережающего социально-экономического развития

Статус территории опережающего социально-экономического развития Teorie regionálního rozvoje

Teorie regionálního rozvoje Социология богатых и бедных

Социология богатых и бедных Инфляция и семейная экономика

Инфляция и семейная экономика Инвестиции в основной капитал

Инвестиции в основной капитал Саладағы экономика

Саладағы экономика Защита экономических интересов государства при осуществлении внешней торговли

Защита экономических интересов государства при осуществлении внешней торговли Содружество независимых государств (СНГ)

Содружество независимых государств (СНГ) Рынок как объект управления. Рынок. Структура рынка

Рынок как объект управления. Рынок. Структура рынка Современные тренды развития мирового туризма

Современные тренды развития мирового туризма Товар. Классификация товаров

Товар. Классификация товаров Economia de piață. (Curs 2)

Economia de piață. (Curs 2) Результаты Уругвайского раунда переговоров ГАТТ

Результаты Уругвайского раунда переговоров ГАТТ Интеграционные процессы в АТР (азиатско-тихоокеанский регион) и их особенности

Интеграционные процессы в АТР (азиатско-тихоокеанский регион) и их особенности Модернизация экономики севера

Модернизация экономики севера Международные компании и инновационное развитие мировой экономики

Международные компании и инновационное развитие мировой экономики Институционализм. Сущность, этапы развития и методология

Институционализм. Сущность, этапы развития и методология Экономические циклы

Экономические циклы Разделение и кооперация труда

Разделение и кооперация труда Жилищная экономика и жилищная политика. (Тема 8)

Жилищная экономика и жилищная политика. (Тема 8)