- Forecasting Free Cash Flow of an Industrial Enterprise Using Fuzzy Set Tools

Содержание

- 2. The problem of forecasting companies’ cash flows is important in the growing uncertainty of the business

- 3. Methods of Cash Flow Forecasting

- 4. Revenues as a Key Element to be Forecasted Revenues generated by various centers of financial responsibilities

- 5. Fuzzy Time Series (1) When discussing fuzzy time series {Ỹ(t)}, it should be noted that such

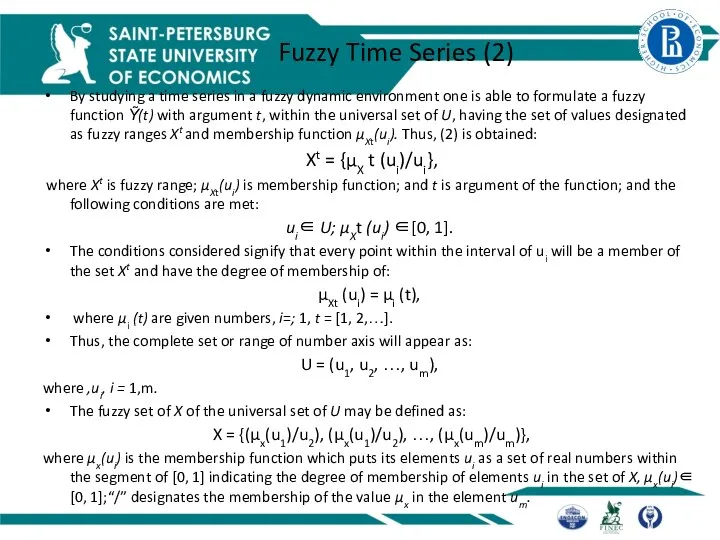

- 6. Fuzzy Time Series (2) By studying a time series in a fuzzy dynamic environment one is

- 7. Stages for forecasting with Fussy Time Series (1)

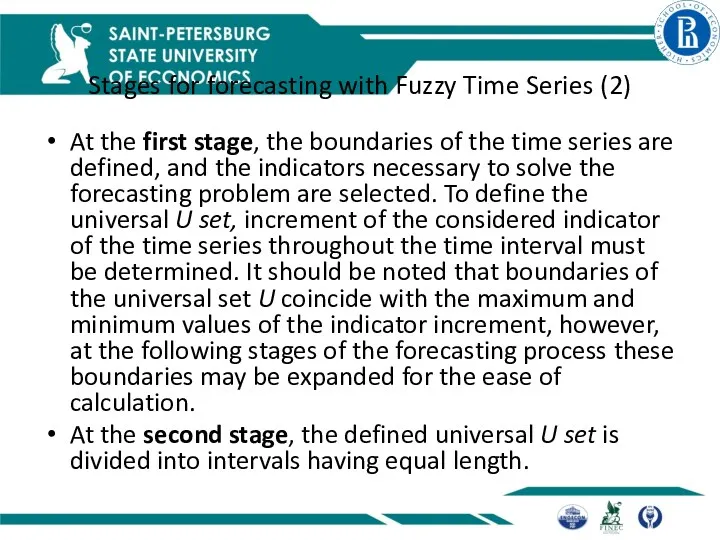

- 8. Stages for forecasting with Fuzzy Time Series (2) At the first stage, the boundaries of the

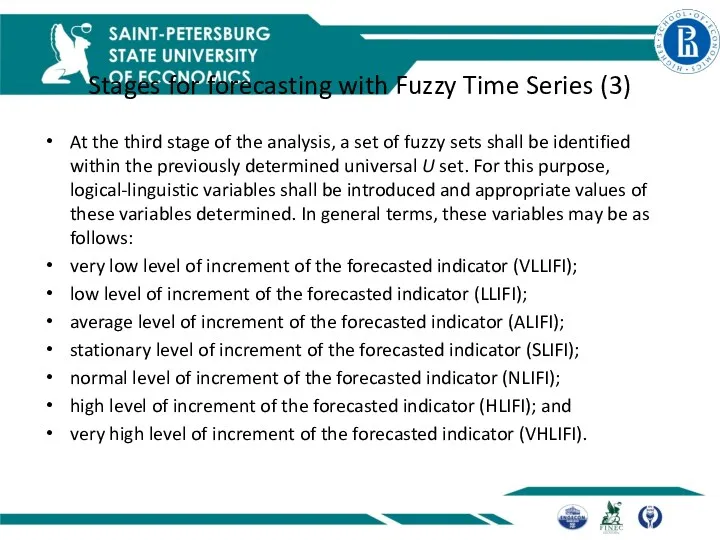

- 9. Stages for forecasting with Fuzzy Time Series (3) At the third stage of the analysis, a

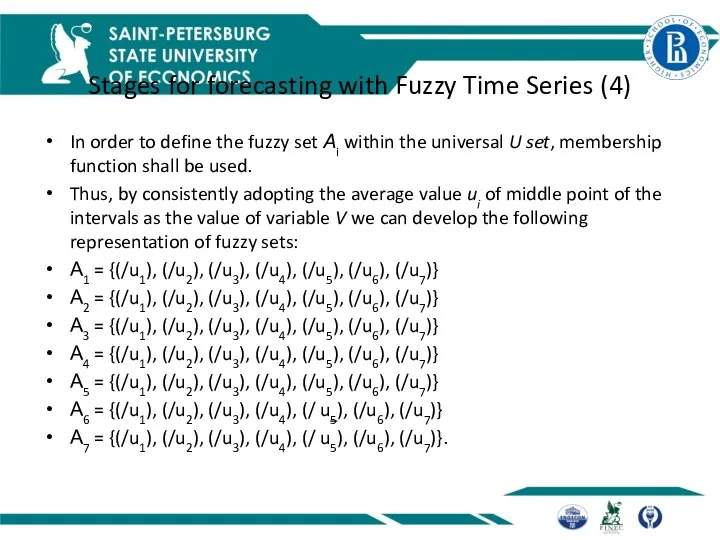

- 10. Stages for forecasting with Fuzzy Time Series (4) In order to define the fuzzy set Аi

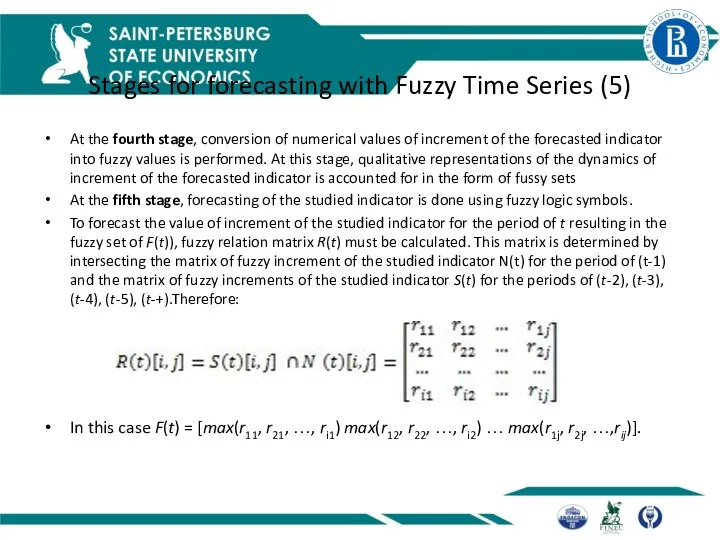

- 11. Stages for forecasting with Fuzzy Time Series (5) At the fourth stage, conversion of numerical values

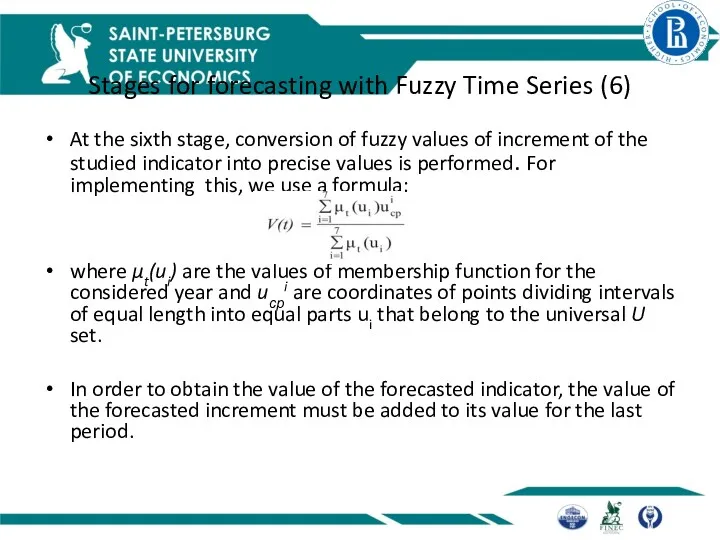

- 12. Stages for forecasting with Fuzzy Time Series (6) At the sixth stage, conversion of fuzzy values

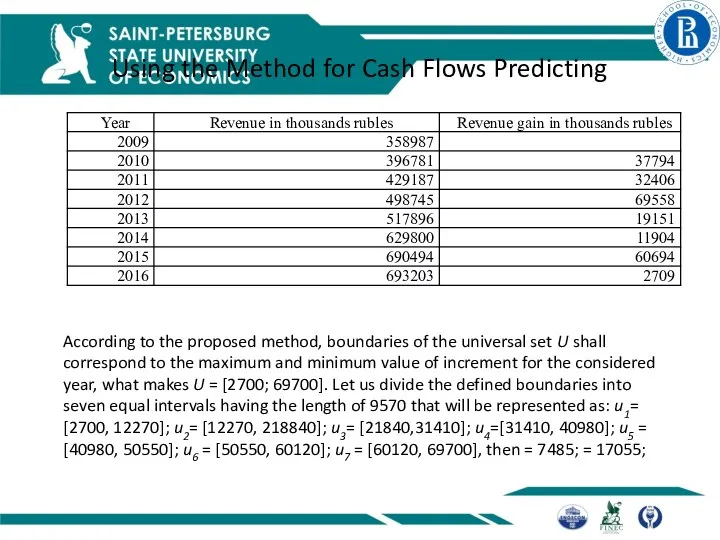

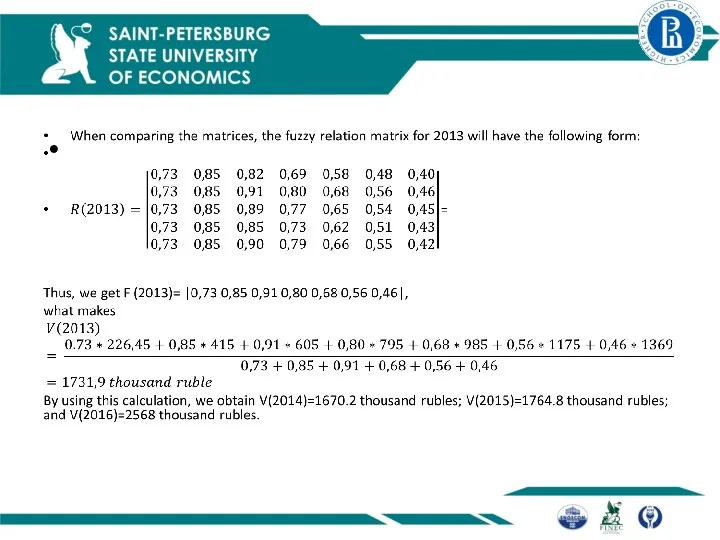

- 13. Using the Method for Cash Flows Predicting According to the proposed method, boundaries of the universal

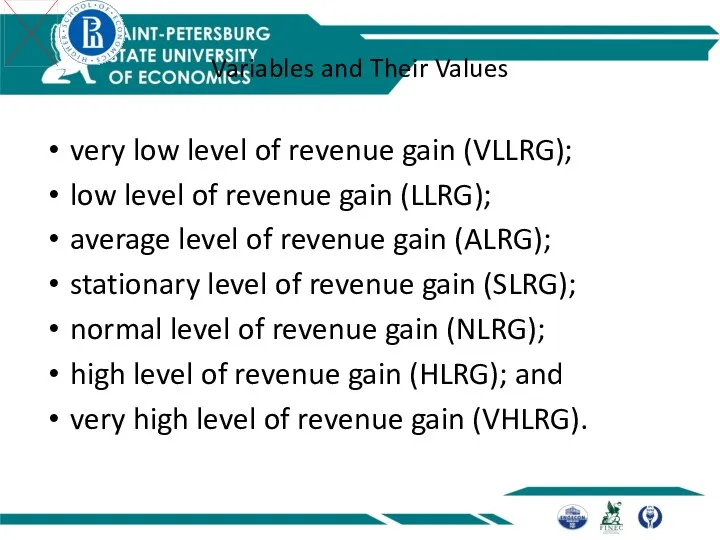

- 14. Variables and Their Values very low level of revenue gain (VLLRG); low level of revenue gain

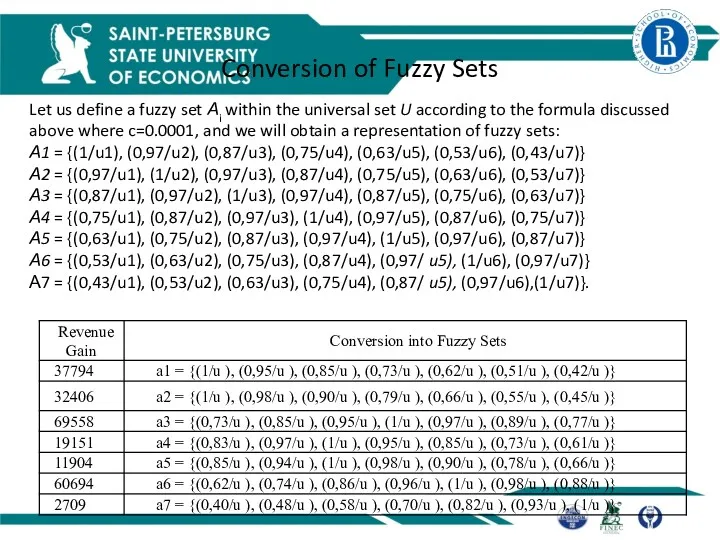

- 15. Conversion of Fuzzy Sets Let us define a fuzzy set Аi within the universal set U

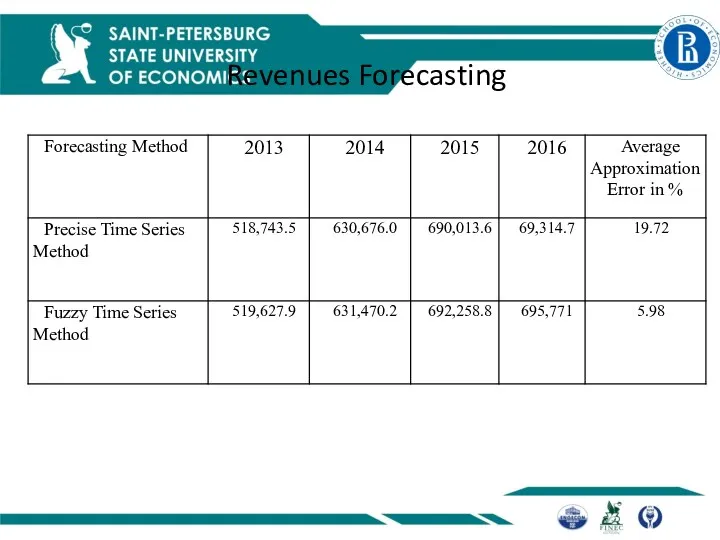

- 17. Revenues Forecasting

- 18. Conclusion The proposed forecasting method based on fuzzy sets is an addition to the existing quantitative

- 20. Скачать презентацию

The problem of forecasting companies’ cash flows is important in the

The problem of forecasting companies’ cash flows is important in the

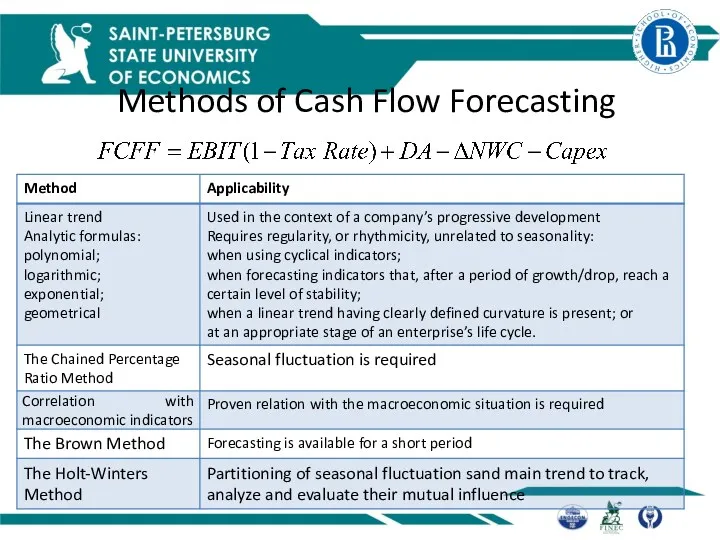

Methods of Cash Flow Forecasting

Methods of Cash Flow Forecasting

Revenues as a Key Element to be Forecasted

Revenues generated by various

Revenues as a Key Element to be Forecasted

Revenues generated by various

Fuzzy Time Series (1)

When discussing fuzzy time series {Ỹ(t)}, it should

Fuzzy Time Series (1)

When discussing fuzzy time series {Ỹ(t)}, it should

Fuzzy Time Series (2)

By studying a time series in a fuzzy

Fuzzy Time Series (2)

By studying a time series in a fuzzy

Stages for forecasting with Fussy Time Series (1)

Stages for forecasting with Fussy Time Series (1)

Stages for forecasting with Fuzzy Time Series (2)

At the first stage,

Stages for forecasting with Fuzzy Time Series (2)

At the first stage,

Stages for forecasting with Fuzzy Time Series (3)

At the third stage

Stages for forecasting with Fuzzy Time Series (3)

At the third stage

Stages for forecasting with Fuzzy Time Series (4)

In order to define

Stages for forecasting with Fuzzy Time Series (4)

In order to define

Stages for forecasting with Fuzzy Time Series (5)

At the fourth stage,

Stages for forecasting with Fuzzy Time Series (5)

At the fourth stage,

Stages for forecasting with Fuzzy Time Series (6)

At the sixth stage,

Stages for forecasting with Fuzzy Time Series (6)

At the sixth stage,

Using the Method for Cash Flows Predicting

According to the proposed method,

Using the Method for Cash Flows Predicting

According to the proposed method,

Variables and Their Values

very low level of revenue gain (VLLRG);

low level

Variables and Their Values

very low level of revenue gain (VLLRG);

low level

Conversion of Fuzzy Sets

Let us define a fuzzy set Аi within

Conversion of Fuzzy Sets

Let us define a fuzzy set Аi within

Revenues Forecasting

Revenues Forecasting

Conclusion

The proposed forecasting method based on fuzzy sets is an addition

Conclusion

The proposed forecasting method based on fuzzy sets is an addition

Өндірістін тиімділігін жене табыстылыгын аныктайтын шығындар

Өндірістін тиімділігін жене табыстылыгын аныктайтын шығындар Оценка потенциальных возможностей компании по освоению внешнего рынка

Оценка потенциальных возможностей компании по освоению внешнего рынка Земельные ресурсы

Земельные ресурсы Национальное богатство

Национальное богатство Міжнародні товарні ринки

Міжнародні товарні ринки Теория фирмы. Продолжение

Теория фирмы. Продолжение Введение в макроэкономику. Макроэкономические показатели. Макроэкономика и ее основные проблемы

Введение в макроэкономику. Макроэкономические показатели. Макроэкономика и ее основные проблемы Организация стран — экспортёров нефти (OPEC)

Организация стран — экспортёров нефти (OPEC) Теневая экономика в России

Теневая экономика в России Глобальные проблемы

Глобальные проблемы Анализ вероятности банкротства организации. Анализ предпринимательского риска

Анализ вероятности банкротства организации. Анализ предпринимательского риска Глобальные проблемы в мировой экономике

Глобальные проблемы в мировой экономике Кейнсианская теория денег

Кейнсианская теория денег АСЕАН - история создания, цели, задачи, членство, результаты деятельности

АСЕАН - история создания, цели, задачи, членство, результаты деятельности Экономическая оценка природных ресурсов

Экономическая оценка природных ресурсов Денежно-кредитная политика

Денежно-кредитная политика Экономическая конкуренция

Экономическая конкуренция Социально-экономическая статистика

Социально-экономическая статистика Ризик-менеджмент фінансової стійкості соціально-економічної регіональної системи в контексті Програми діяльності Кабінету Міністрів Ук

Ризик-менеджмент фінансової стійкості соціально-економічної регіональної системи в контексті Програми діяльності Кабінету Міністрів Ук Шерінгова економіка

Шерінгова економіка Економіка і соціологія праці

Економіка і соціологія праці Индикаторы устойчивого развития

Индикаторы устойчивого развития Роль и функции цен в рыночной экономике

Роль и функции цен в рыночной экономике Группа компаний Р-ФАРМ. Инновационные технологии здоровья

Группа компаний Р-ФАРМ. Инновационные технологии здоровья Тезисы стратегии социально-экономического развития Калужской области до 2040 года

Тезисы стратегии социально-экономического развития Калужской области до 2040 года Прогнозирование. Классификация экономического прогнозирования

Прогнозирование. Классификация экономического прогнозирования Экономические системы. Рыночная экономика и ее модели

Экономические системы. Рыночная экономика и ее модели Экономика и экология: новые модели развития

Экономика и экология: новые модели развития