- Microeconomics. The costs of production. Chapter 20

Содержание

- 2. Ch 20 Learning Objectives Why economic costs include both explicit costs and implicit costs. How the

- 3. Economic Costs Economic costs - payments a firm must make, or incomes it must provide, to

- 4. Explicit Costs Cash Payments a firm makes to those who supply labor services, materials, fuel, transportation

- 5. Implicit Costs Implicit costs - opportunity costs of using its self-owned, self-employed resources. Money payments that

- 6. T-shirts example: Accounting profits - $57,000 Ignores implicit costs Overstates economic success

- 7. Normal Profits Normal profits are considered an implicit cost because they are the minimum payments required

- 8. Economic Profits Economic or pure profits are total revenue less all costs (explicit and implicit including

- 9. Short Run Time period that is too brief for a firm to alter its plant capacity.

- 10. Long-run The long run is a period of time long enough for a firm to change

- 11. Economic Profit Versus Accounting Profits Economic Profit Accounting Costs (Explicit Costs Only) Accounting Profit Explicit Costs

- 12. Short-Run Production Relationships Total Product (TP) Marginal Product (MP) Average Product (AP)

- 13. Law of Diminishing returns Assumes technology is fixed & techniques for production do not change. As

- 14. Increasing Marginal Returns Law of Diminishing Returns 0 1 2 3 4 5 6 7 8

- 15. Law of Diminishing Returns Graphical Portrayal TP MP AP Increasing Marginal Returns Diminishing Marginal Returns Negative

- 16. Law of Diminishing Returns Example For example, a farmer will find that a certain number of

- 17. The law of diminishing returns assumes all units of variable inputs—workers in this case—are of equal

- 18. Short-Run Production Costs Fixed Costs Variable Costs Total Cost TC = TFC + TVC

- 19. Short-Run Production Relationships Short‑run production reflects the law of diminishing returns that states that as successive

- 20. Short Run Production Costs Fixed, variable and total costs 1. Total fixed costs are those costs

- 21. Short Run Production Costs Per unit or average 1. Average fixed cost is the total fixed

- 22. Short Run Production Costs Marginal cost - additional cost of producing one more unit of output

- 23. Short Run Production Costs Cost curves will shift if the resource prices change or if technology

- 24. Short-Run Production Costs Per-Unit or Average Costs Average Fixed Cost (AFC) Average Variable Cost (AVC) Average

- 25. Short-Run Production Costs Total Cost, Fixed and Variable Costs TFC TC TVC Total Cost Variable Cost

- 26. Short-Run Production Costs Average and Marginal Costs AFC MC ATC AVC AVC AFC

- 27. Short-Run Production Costs MC and Marginal Product Marginal Decisions Relation of MC to AVC and ATC

- 28. Short-Run Production Costs MP AP MC AVC Quantity of Output Quantity of Labor Production Curves Cost

- 29. Long-run In the long‑run, all production costs are variable, i.e., long-run costs reflect changes in plant

- 30. Economies of Scale a.k.a. Economies of mass production As plant size increases, a number of factors

- 31. Diseconomies of Scale Over time, thee expansion of a firm may lead to diseconomies of scale

- 32. Economies or diseconomies of scale exist in the long run. 1. Economies of scale or economies

- 33. Long-Run Production Costs Firm Size and Costs Long-Run Cost Curve Economies of Scale Labor Specialization Managerial

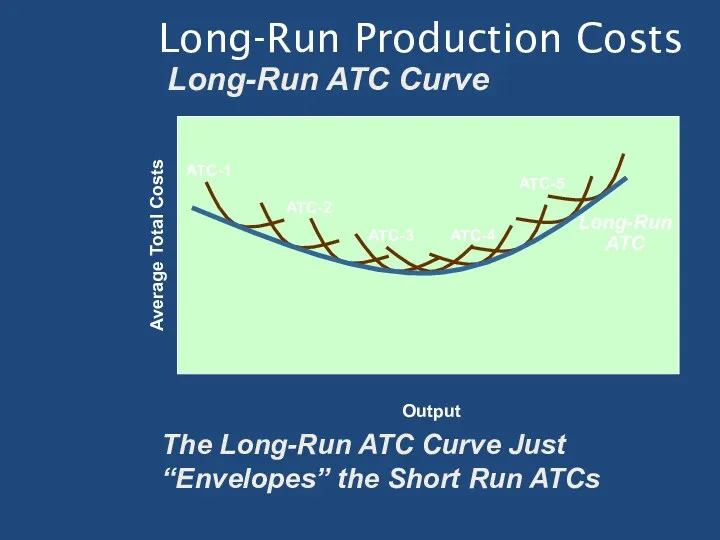

- 34. Long-Run Production Costs Long-Run ATC Curve Average Total Costs ATC-1 ATC-2 ATC-3 ATC-4 ATC-5 Output Any

- 35. Long-Run Production Costs Long-Run ATC Curve Long-Run ATC Average Total Costs ATC-1 ATC-2 ATC-3 ATC-4 ATC-5

- 36. Long-Run Production Costs Alternative Long-Run ATC Shapes Output Long-Run ATC Curve Where Economies Of Scale Exist

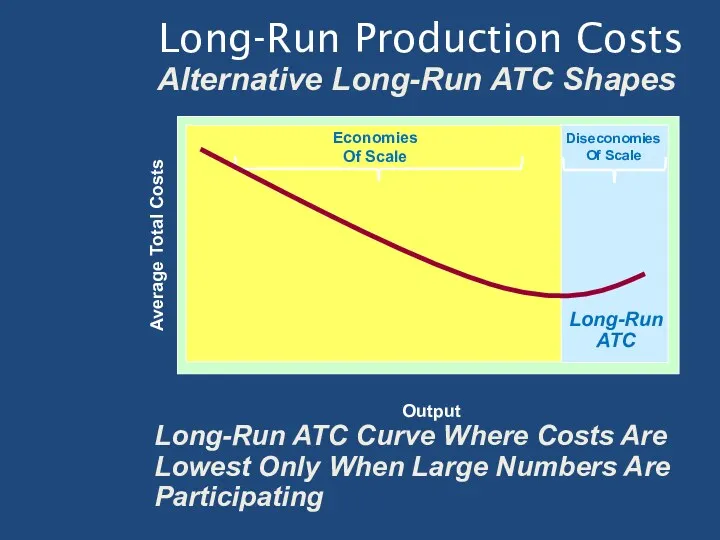

- 37. Long-Run Production Costs Alternative Long-Run ATC Shapes Output Long-Run ATC Curve Where Costs Are Lowest Only

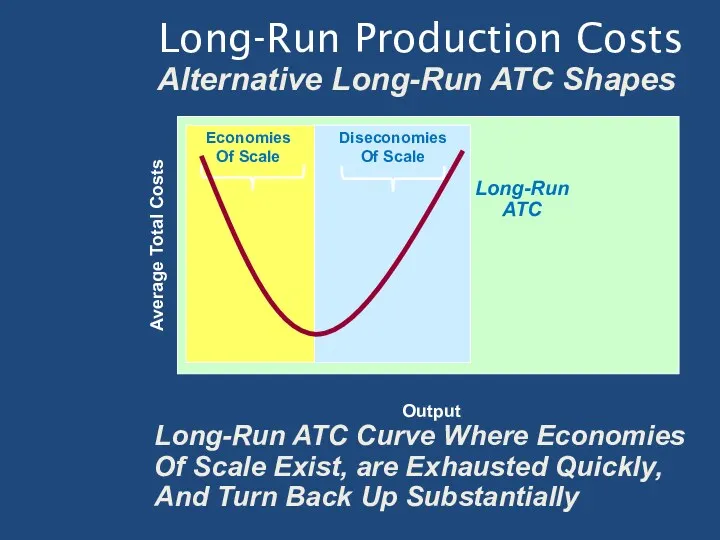

- 38. Long-Run Production Costs Alternative Long-Run ATC Shapes Output Long-Run ATC Curve Where Economies Of Scale Exist,

- 39. Minimum Efficient Scale and Industry Structure Minimum Efficient Scale (MES) Natural Monopoly Applications and Illustrations Rising

- 40. Don’t Cry Over Sunk Costs Sunk Costs Irrelevant in Decision Making Once Incurred, They Cannot Be

- 42. Скачать презентацию

Ch 20 Learning Objectives

Why economic costs include both explicit costs and

Ch 20 Learning Objectives

Why economic costs include both explicit costs and

Economic Costs

Economic costs - payments a firm must make, or incomes

Economic Costs

Economic costs - payments a firm must make, or incomes

Explicit Costs

Cash Payments a firm makes to those who supply labor

Explicit Costs

Cash Payments a firm makes to those who supply labor

Implicit Costs

Implicit costs - opportunity costs of using its self-owned, self-employed

Implicit Costs

Implicit costs - opportunity costs of using its self-owned, self-employed

T-shirts example: Accounting profits - $57,000

Ignores implicit costs

Overstates economic success

T-shirts example: Accounting profits - $57,000

Ignores implicit costs

Overstates economic success

Normal Profits

Normal profits are considered an implicit cost because they are

Normal Profits

Normal profits are considered an implicit cost because they are

Economic Profits

Economic or pure profits are total revenue less all costs

Economic Profits

Economic or pure profits are total revenue less all costs

Short Run

Time period that is too brief for a firm to

Short Run

Time period that is too brief for a firm to

Long-run

The long run is a period of time long enough for

Long-run

The long run is a period of time long enough for

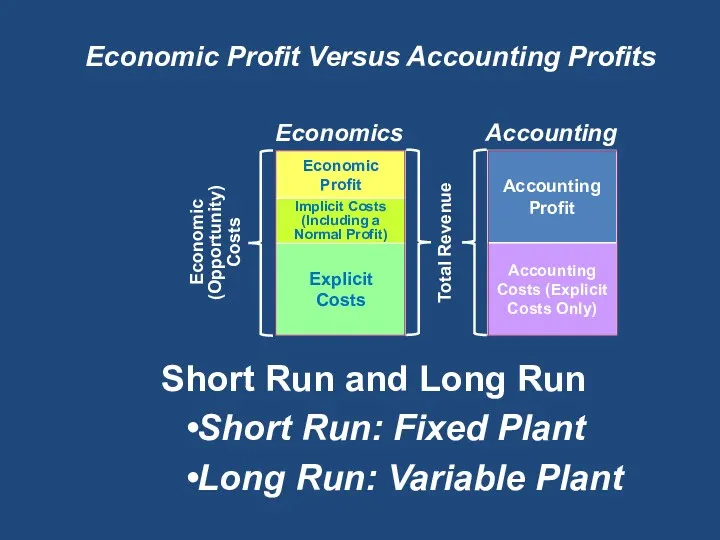

Economic Profit Versus Accounting Profits

Economic

Profit

Accounting

Costs (Explicit

Costs Only)

Accounting

Profit

Explicit

Costs

Implicit Costs

(Including a

Normal Profit)

Economic

(Opportunity)

Costs

Total

Economic Profit Versus Accounting Profits

Economic

Profit

Accounting

Costs (Explicit

Costs Only)

Accounting

Profit

Explicit

Costs

Implicit Costs

(Including a

Normal Profit)

Economic

(Opportunity)

Costs

Total

Short-Run Production Relationships

Total Product (TP)

Marginal Product (MP)

Average Product (AP)

Short-Run Production Relationships

Total Product (TP)

Marginal Product (MP)

Average Product (AP)

Law of Diminishing returns

Assumes technology is fixed & techniques for production

Law of Diminishing returns

Assumes technology is fixed & techniques for production

Increasing

Marginal

Returns

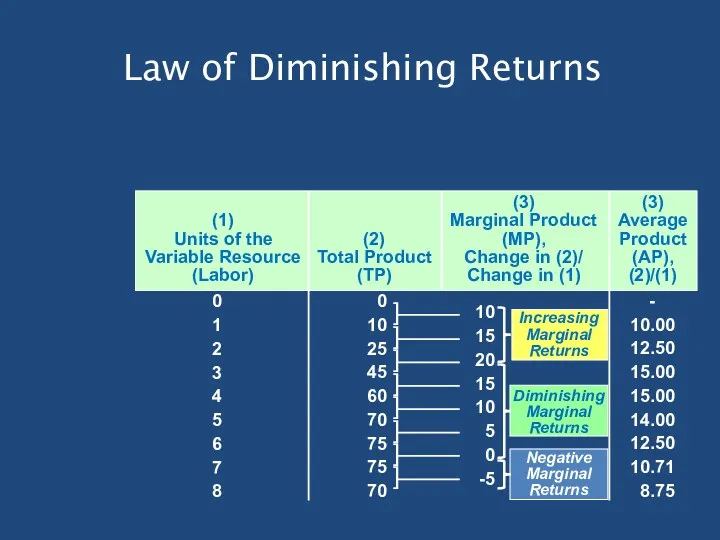

Law of Diminishing Returns

0

1

2

3

4

5

6

7

8

0

10

25

45

60

70

75

75

70

10

15

20

15

10

5

0

-5

-

10.00

12.50

15.00

15.00

14.00

12.50

10.71

8.75

Diminishing

Marginal

Returns

Negative

Marginal

Returns

Increasing

Marginal

Returns

Law of Diminishing Returns

0

1

2

3

4

5

6

7

8

0

10

25

45

60

70

75

75

70

10

15

20

15

10

5

0

-5

-

10.00

12.50

15.00

15.00

14.00

12.50

10.71

8.75

Diminishing

Marginal

Returns

Negative

Marginal

Returns

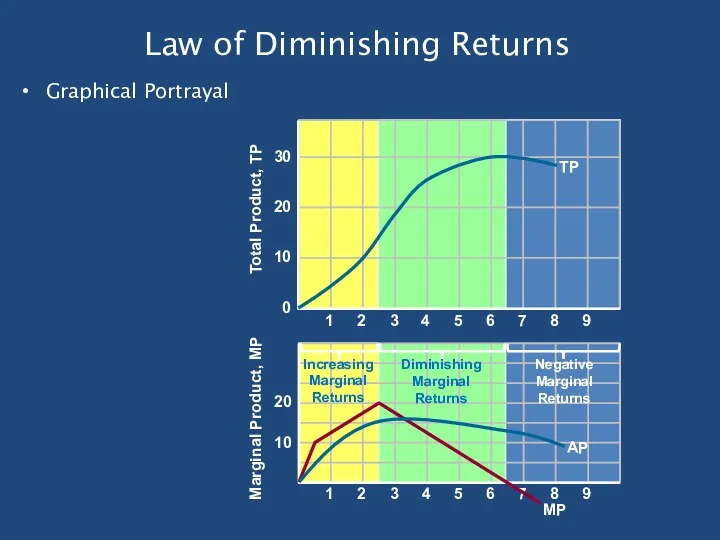

Law of Diminishing Returns

Graphical Portrayal

TP

MP

AP

Increasing

Marginal

Returns

Diminishing

Marginal

Returns

Negative

Marginal

Returns

Law of Diminishing Returns

Graphical Portrayal

TP

MP

AP

Increasing

Marginal

Returns

Diminishing

Marginal

Returns

Negative

Marginal

Returns

Law of Diminishing Returns Example

For example, a farmer will find that

Law of Diminishing Returns Example

For example, a farmer will find that

The law of diminishing returns assumes all units of variable inputs—workers

The law of diminishing returns assumes all units of variable inputs—workers

Short-Run Production Costs

Fixed Costs

Variable Costs

Total Cost

TC = TFC + TVC

Short-Run Production Costs

Fixed Costs

Variable Costs

Total Cost

TC = TFC + TVC

Short-Run Production Relationships

Short‑run production reflects the law of diminishing returns that

Short-Run Production Relationships

Short‑run production reflects the law of diminishing returns that

Short Run Production Costs

Fixed, variable and total costs

1. Total fixed costs

Short Run Production Costs

Fixed, variable and total costs

1. Total fixed costs

Short Run Production Costs

Per unit or average

1. Average fixed cost

Short Run Production Costs

Per unit or average

1. Average fixed cost

Short Run Production Costs

Marginal cost - additional cost of producing one

Short Run Production Costs

Marginal cost - additional cost of producing one

Short Run Production Costs

Cost curves will shift if the resource prices

Short Run Production Costs

Cost curves will shift if the resource prices

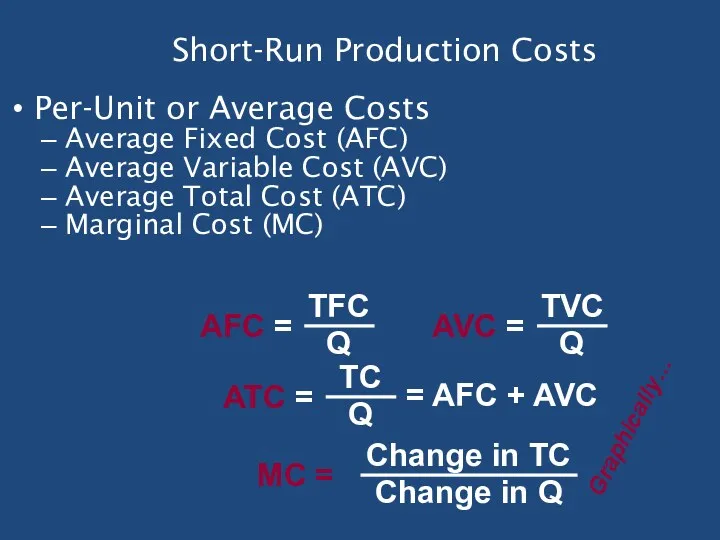

Short-Run Production Costs

Per-Unit or Average Costs

Average Fixed Cost (AFC)

Average Variable Cost

Short-Run Production Costs

Per-Unit or Average Costs

Average Fixed Cost (AFC)

Average Variable Cost

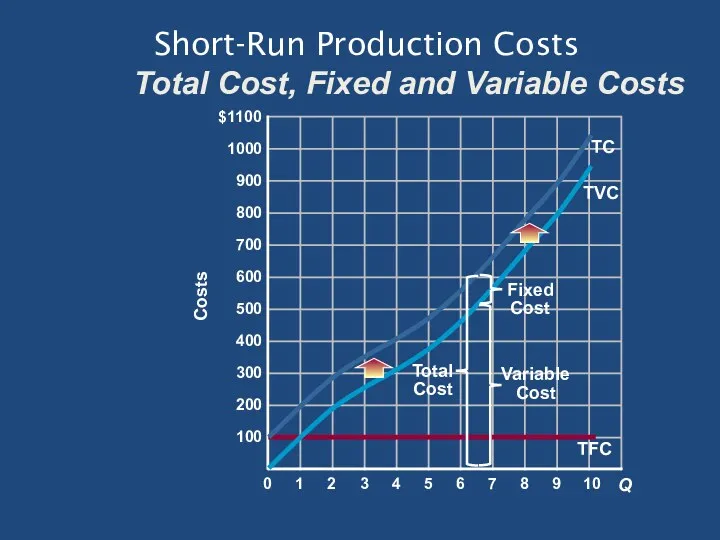

Short-Run Production Costs

Total Cost, Fixed and Variable Costs

TFC

TC

TVC

Total

Cost

Variable

Cost

Fixed

Cost

Short-Run Production Costs

Total Cost, Fixed and Variable Costs

TFC

TC

TVC

Total

Cost

Variable

Cost

Fixed

Cost

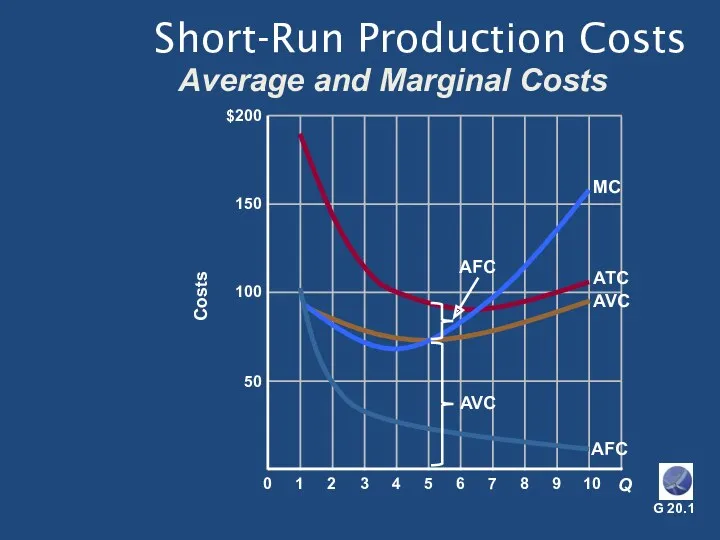

Short-Run Production Costs

Average and Marginal Costs

AFC

MC

ATC

AVC

AVC

AFC

Short-Run Production Costs

Average and Marginal Costs

AFC

MC

ATC

AVC

AVC

AFC

Short-Run Production Costs

MC and Marginal Product

Marginal Decisions

Relation of MC to AVC

Short-Run Production Costs

MC and Marginal Product

Marginal Decisions

Relation of MC to AVC

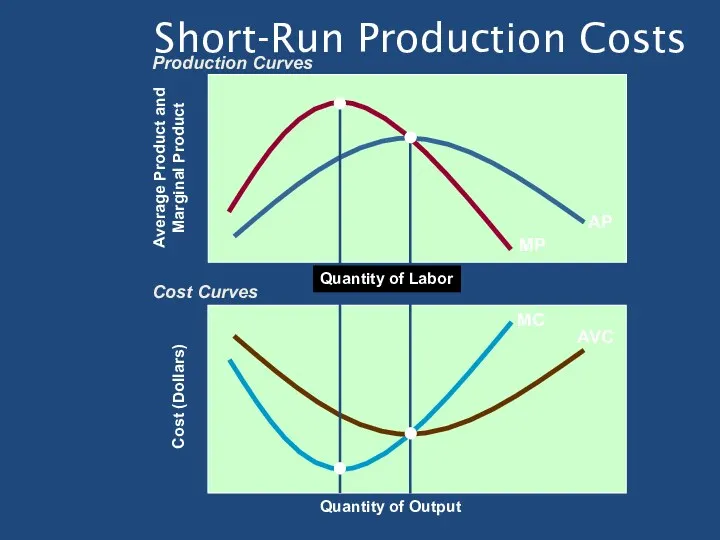

Short-Run Production Costs

MP

AP

MC

AVC

Quantity of Output

Quantity of Labor

Production Curves

Cost Curves

Short-Run Production Costs

MP

AP

MC

AVC

Quantity of Output

Quantity of Labor

Production Curves

Cost Curves

Long-run

In the long‑run, all production costs are variable, i.e., long-run costs

Long-run

In the long‑run, all production costs are variable, i.e., long-run costs

Economies of Scale

a.k.a. Economies of mass production

As plant size increases, a

Economies of Scale

a.k.a. Economies of mass production

As plant size increases, a

Diseconomies of Scale

Over time, thee expansion of a firm may lead

Diseconomies of Scale

Over time, thee expansion of a firm may lead

Economies or diseconomies of scale exist in the long run.

1. Economies of

Economies or diseconomies of scale exist in the long run.

1. Economies of

Long-Run Production Costs

Firm Size and Costs

Long-Run Cost Curve

Economies of Scale

Labor Specialization

Managerial

Long-Run Production Costs

Firm Size and Costs

Long-Run Cost Curve

Economies of Scale

Labor Specialization

Managerial

Long-Run Production Costs

Long-Run ATC Curve

Average Total Costs

ATC-1

ATC-2

ATC-3

ATC-4

ATC-5

Output

Any Number of Short-Run Optimum

Long-Run Production Costs

Long-Run ATC Curve

Average Total Costs

ATC-1

ATC-2

ATC-3

ATC-4

ATC-5

Output

Any Number of Short-Run Optimum

Long-Run Production Costs

Long-Run ATC Curve

Long-Run

ATC

Average Total Costs

ATC-1

ATC-2

ATC-3

ATC-4

ATC-5

Output

The Long-Run ATC Curve Just

“Envelopes”

Long-Run Production Costs

Long-Run ATC Curve

Long-Run

ATC

Average Total Costs

ATC-1

ATC-2

ATC-3

ATC-4

ATC-5

Output

The Long-Run ATC Curve Just

“Envelopes”

Long-Run Production Costs

Alternative Long-Run ATC Shapes

Output

Long-Run ATC Curve Where Economies

Of Scale

Long-Run Production Costs

Alternative Long-Run ATC Shapes

Output

Long-Run ATC Curve Where Economies

Of Scale

Long-Run Production Costs

Alternative Long-Run ATC Shapes

Output

Long-Run ATC Curve Where Costs Are

Lowest

Long-Run Production Costs

Alternative Long-Run ATC Shapes

Output

Long-Run ATC Curve Where Costs Are

Lowest

Long-Run Production Costs

Alternative Long-Run ATC Shapes

Output

Long-Run ATC Curve Where Economies

Of Scale

Long-Run Production Costs

Alternative Long-Run ATC Shapes

Output

Long-Run ATC Curve Where Economies

Of Scale

Minimum Efficient Scale and Industry Structure

Minimum Efficient Scale (MES)

Natural Monopoly

Applications and

Minimum Efficient Scale and Industry Structure

Minimum Efficient Scale (MES)

Natural Monopoly

Applications and

Don’t Cry Over Sunk Costs

Sunk Costs Irrelevant in Decision Making

Once Incurred,

Don’t Cry Over Sunk Costs

Sunk Costs Irrelevant in Decision Making

Once Incurred,

Международная миграция рабочей силы

Международная миграция рабочей силы Введение в социально-экономическую статистику (СЭС)

Введение в социально-экономическую статистику (СЭС) Великие географические открытия. Часть 1

Великие географические открытия. Часть 1 Концепции построения ЛС при управлении запасами

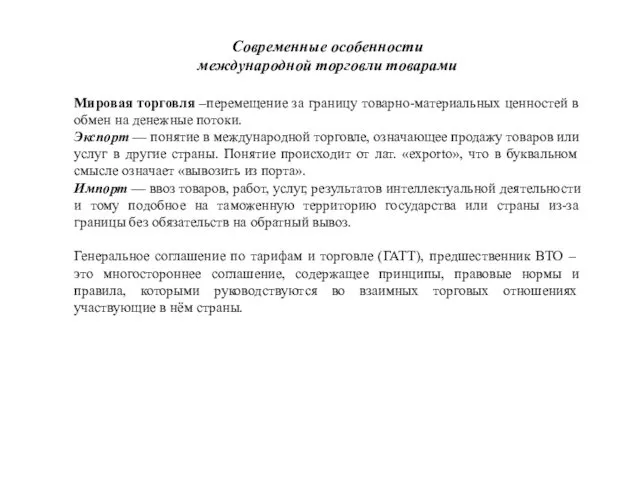

Концепции построения ЛС при управлении запасами Современные особенности международной торговли товарами

Современные особенности международной торговли товарами Государственная промышленная и научнотехническая политика, как инструменты регулирования экономики

Государственная промышленная и научнотехническая политика, как инструменты регулирования экономики Типы рыночных структур

Типы рыночных структур Поведение потребителя

Поведение потребителя Эндогенные теории экономического роста

Эндогенные теории экономического роста Потребности и ресурсы. Проблема выбора в экономике

Потребности и ресурсы. Проблема выбора в экономике Экономические и математически методы экономического анализа

Экономические и математически методы экономического анализа Современное рыночное хозяйство

Современное рыночное хозяйство Сетевые технологии планирования и управления в условиях неопределённости

Сетевые технологии планирования и управления в условиях неопределённости Принятие решений как особый вид человеческой деятельности

Принятие решений как особый вид человеческой деятельности Исламдық қаржы орталықтары

Исламдық қаржы орталықтары Статистика национального богатства. Валовой внутренний продукт

Статистика национального богатства. Валовой внутренний продукт Личные финансы: сущность и особенности. (Лекция 3)

Личные финансы: сущность и особенности. (Лекция 3) Мировая экономика и международные экономические отношения

Мировая экономика и международные экономические отношения Основы поведения субъектов рыночной экономики.Общая и предельная полезность. Закон убывающей предельной полезности. Кривые безразличия

Основы поведения субъектов рыночной экономики.Общая и предельная полезность. Закон убывающей предельной полезности. Кривые безразличия Методика и техника изучения затрат рабочего времени. Хронометраж, фотографии рабочего времени

Методика и техника изучения затрат рабочего времени. Хронометраж, фотографии рабочего времени Стратегическое планирование в Республике Казахстан

Стратегическое планирование в Республике Казахстан Фармакоэкономический анализ и его методы

Фармакоэкономический анализ и его методы Характеристика рыночного хозяйства Франции

Характеристика рыночного хозяйства Франции Цели устойчивого развития

Цели устойчивого развития Система государственного прогнозирования в РФ

Система государственного прогнозирования в РФ Итоговое собрание АСП Атополе Мото Кудрово. Итоги января 2023

Итоговое собрание АСП Атополе Мото Кудрово. Итоги января 2023 Моделі соціального інвестування розвинутих країн світу

Моделі соціального інвестування розвинутих країн світу ИСО-ның ұйымдастырушылық құрылымы

ИСО-ның ұйымдастырушылық құрылымы