- Technical Analysis

Содержание

- 2. 1.GENERAL PRINCIPLES AND ASSUMPTIONS Technical analysis is a form of security analysis that uses price and

- 3. Another tenet of technical analysis is that the market brings together the collective wisdom of multiple

- 4. 2.TECHNICAL ANALYSIS TOOLS The primary tools used in technical analysis are charts and indicators. Charts provide

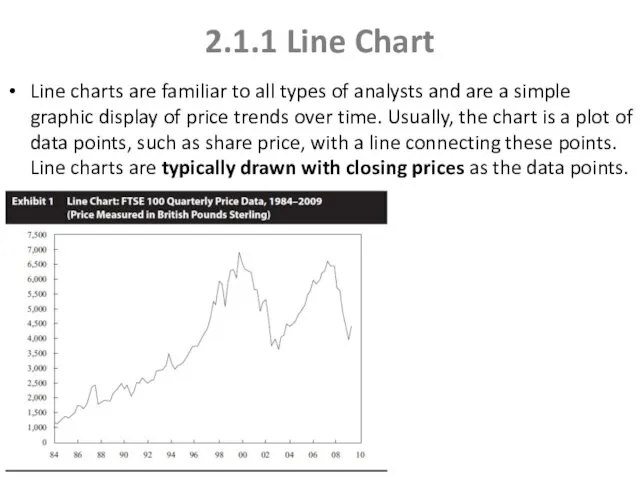

- 5. 2.1.1 Line Chart Line charts are familiar to all types of analysts and are a simple

- 6. 2.1.2 Bar Chart A bar chart, in contrast, has four bits of data in each entry—the

- 7. 2.1.3 Candlestick Chart Candlestick charts trace their roots to Japan, where technical analysis has been in

- 8. 2.1.4 Point and Figure Chart Point and figure charts were widely used in the United States

- 9. Volume, Time Intervals Volume is used to assess the strength or conviction of buyers and sellers

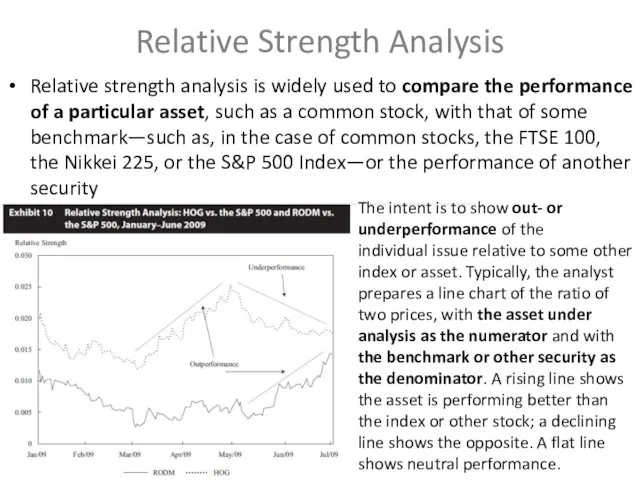

- 10. Relative Strength Analysis Relative strength analysis is widely used to compare the performance of a particular

- 11. TREND The concept of a trend is perhaps the most important aspect of technical analysis. Trend

- 12. CHART PATTERNS Chart patterns are formations that appear in price charts that create some type of

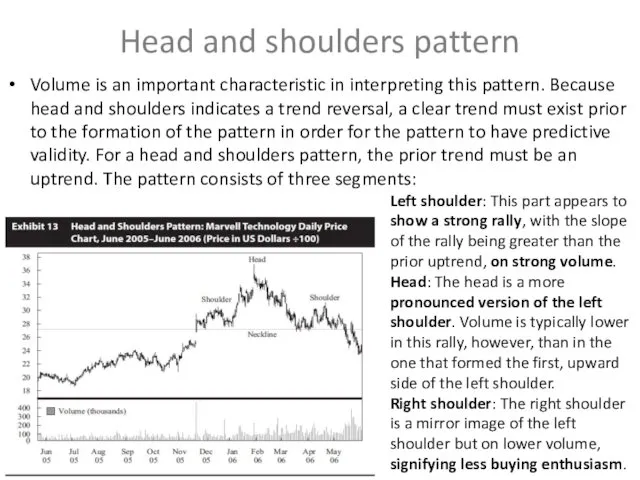

- 13. Head and shoulders pattern Volume is an important characteristic in interpreting this pattern. Because head and

- 14. Inverse Head and Shoulders The head and shoulders pattern can also form upside down and act

- 15. Setting Price Targets with Head and Shoulders Patterns Once the neckline is breached, the security is

- 16. Double Tops A double top is when an uptrend reverses twice at roughly the same high

- 17. Double bottoms Double bottoms are formed when the price reaches a low, rebounds, and then sells

- 18. The reason of Double Tops and Bottoms patterns For an uptrend, a double top implies that

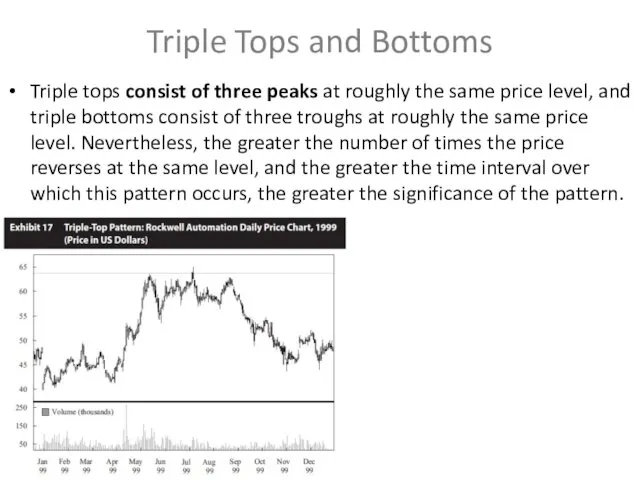

- 19. Triple Tops and Bottoms Triple tops consist of three peaks at roughly the same price level,

- 20. Continuation Patterns Continuation patterns indicate that a market trend in place prior to the pattern formation

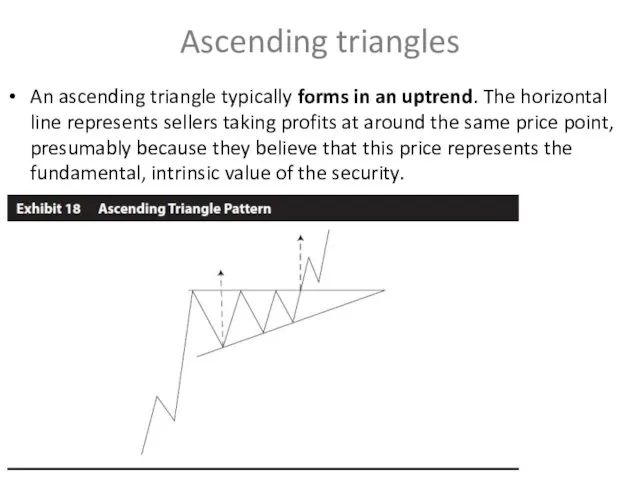

- 21. Ascending triangles An ascending triangle typically forms in an uptrend. The horizontal line represents sellers taking

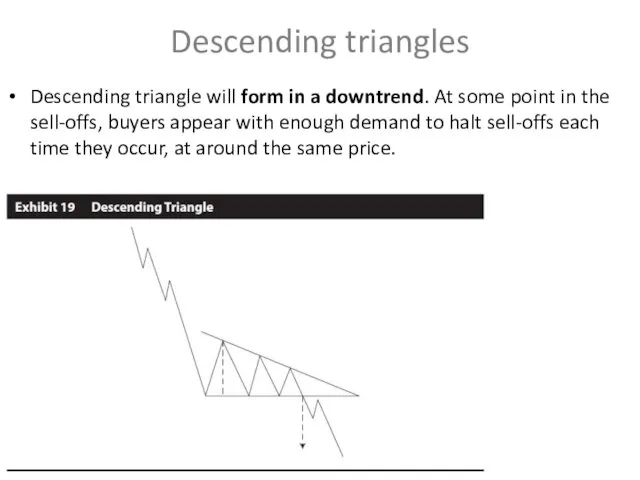

- 22. Descending triangles Descending triangle will form in a downtrend. At some point in the sell-offs, buyers

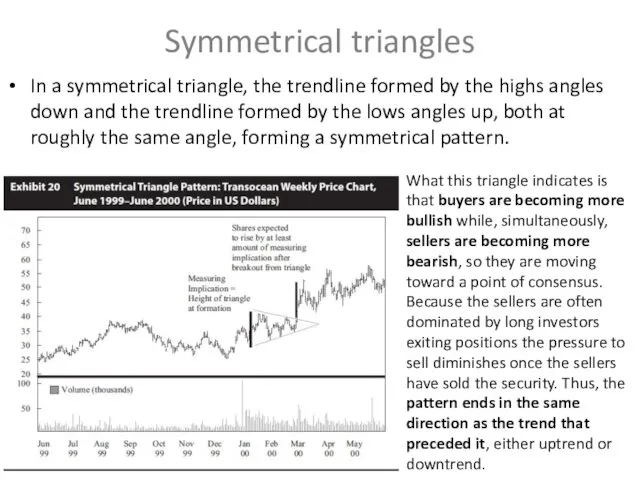

- 23. Symmetrical triangles In a symmetrical triangle, the trendline formed by the highs angles down and the

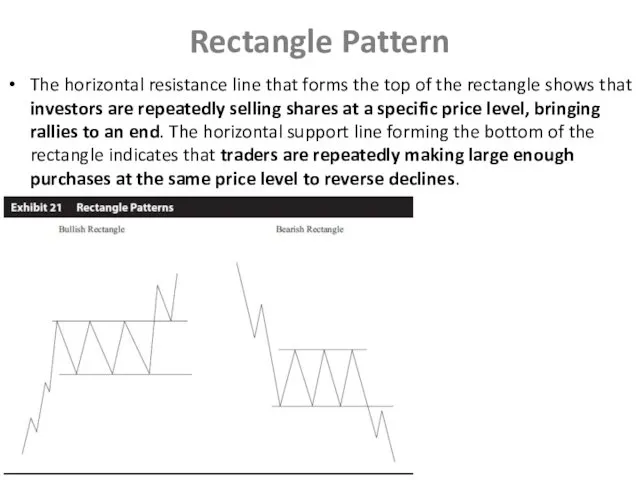

- 24. Rectangle Pattern The horizontal resistance line that forms the top of the rectangle shows that investors

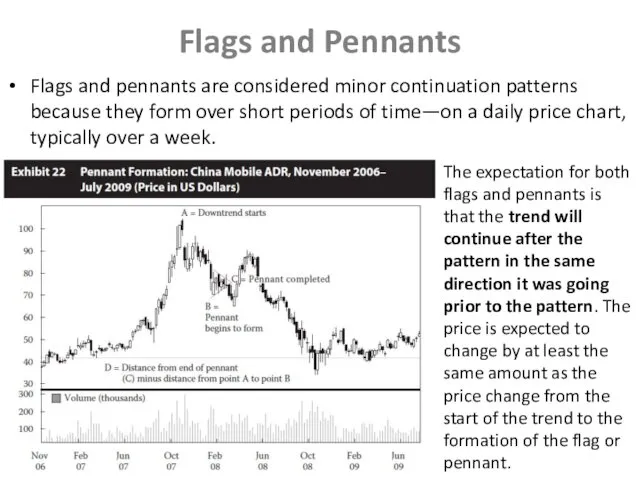

- 25. Flags and Pennants Flags and pennants are considered minor continuation patterns because they form over short

- 26. 2.2 Technical Indicators The technical analyst uses a variety of technical indicators to supplement the information

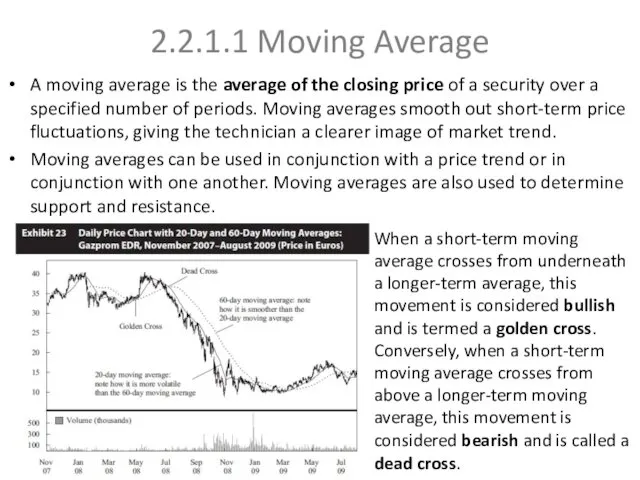

- 27. 2.2.1.1 Moving Average A moving average is the average of the closing price of a security

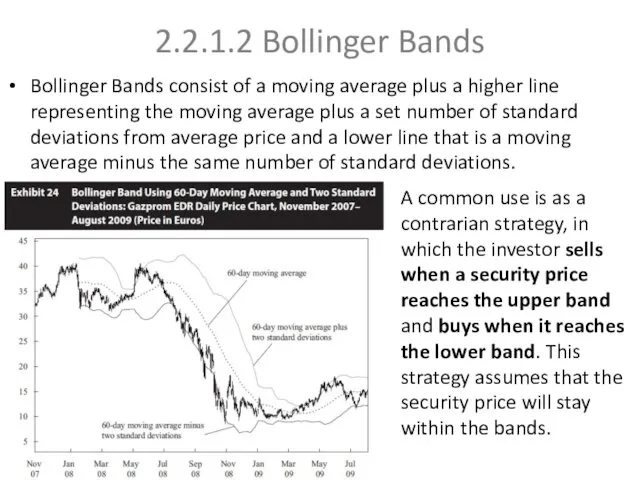

- 28. 2.2.1.2 Bollinger Bands Bollinger Bands consist of a moving average plus a higher line representing the

- 29. 2.2.2 Momentum Oscillators One of the key challenges in using indicators overlaid on a price chart

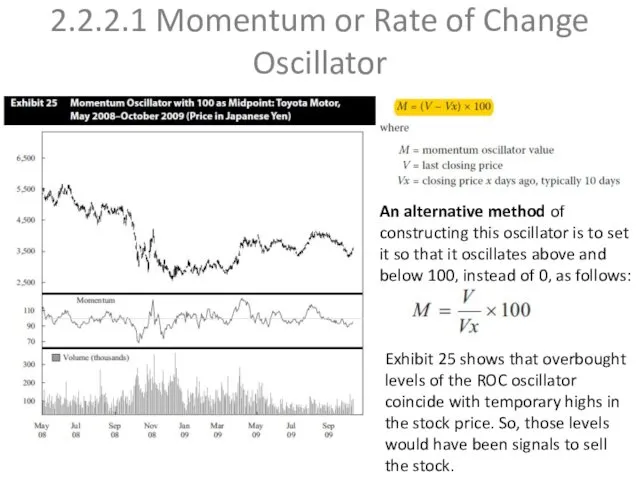

- 30. 2.2.2.1 Momentum or Rate of Change Oscillator An alternative method of constructing this oscillator is to

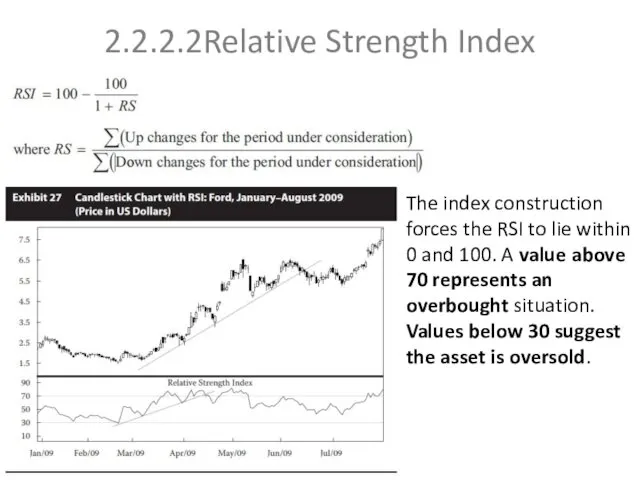

- 31. 2.2.2.2Relative Strength Index The index construction forces the RSI to lie within 0 and 100. A

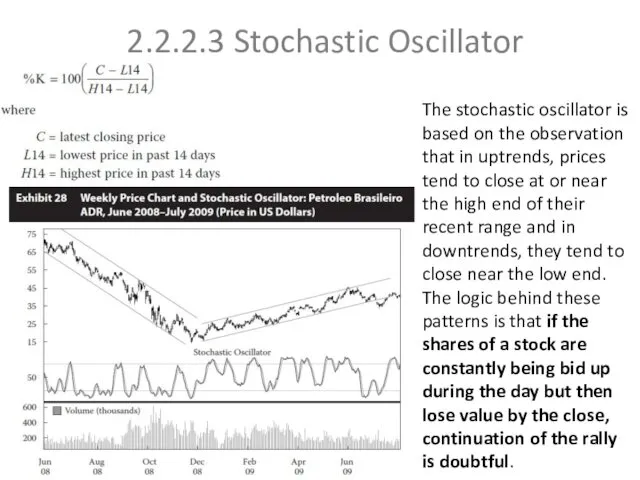

- 32. 2.2.2.3 Stochastic Oscillator The stochastic oscillator is based on the observation that in uptrends, prices tend

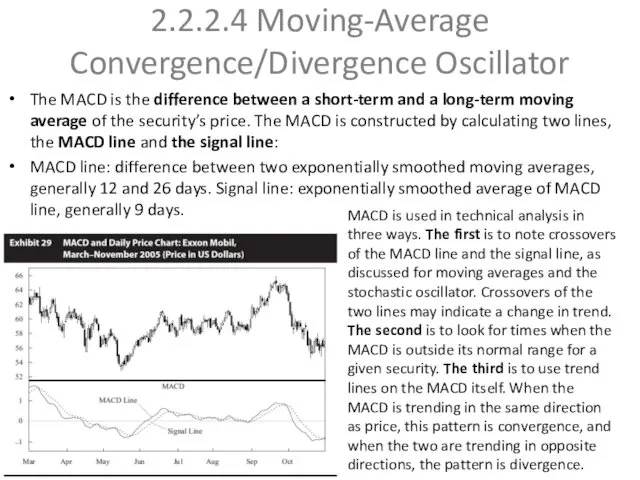

- 33. 2.2.2.4 Moving-Average Convergence/Divergence Oscillator The MACD is the difference between a short-term and a long-term moving

- 34. 2.2.3 Sentiment Indicators Sentiment indicators attempt to gauge investor activity for signs of increasing bullishness or

- 35. 2.2.3.2 Calculated Statistical Indices The other category of sentiment indicators are indicators that are calculated from

- 36. Margin debt and Short interest Margin debt is also often used as an indication of sentiment.

- 37. 2.2.4 Flow-of-Funds Indicators Flow-of-funds indicators help technicians gauge potential changes in supply and demand for securities.

- 38. Margin debt is also widely used as a flow-of-funds indicator because margin loans may increase the

- 39. Putting more shares on the market increases the aggregate supply of shares available for investors to

- 40. INTERMARKET ANALYSIS Intermarket analysis is based on the principle that all markets are interrelated and influence

- 42. Скачать презентацию

1.GENERAL PRINCIPLES AND ASSUMPTIONS

Technical analysis is a form of security analysis

1.GENERAL PRINCIPLES AND ASSUMPTIONS

Technical analysis is a form of security analysis

Another tenet of technical analysis is that the market brings together

Another tenet of technical analysis is that the market brings together

2.TECHNICAL ANALYSIS TOOLS

The primary tools used in technical analysis are charts

2.TECHNICAL ANALYSIS TOOLS

The primary tools used in technical analysis are charts

2.1.1 Line Chart

Line charts are familiar to all types of analysts

2.1.1 Line Chart

Line charts are familiar to all types of analysts

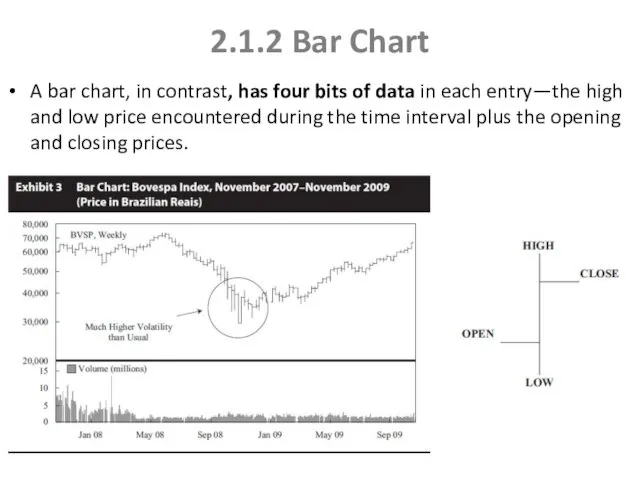

2.1.2 Bar Chart

A bar chart, in contrast, has four bits of

2.1.2 Bar Chart

A bar chart, in contrast, has four bits of

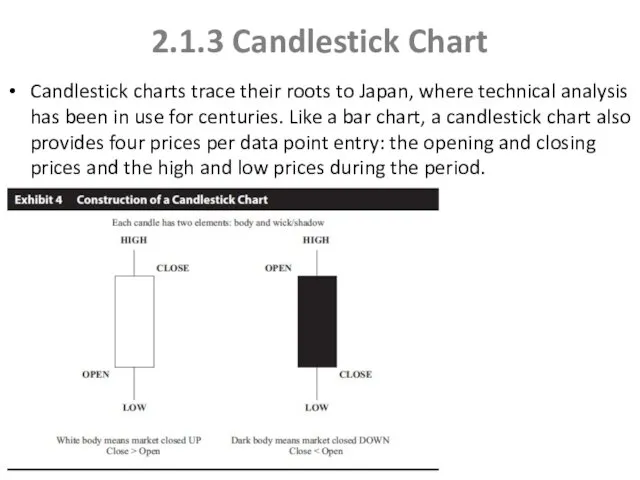

2.1.3 Candlestick Chart

Candlestick charts trace their roots to Japan, where technical

2.1.3 Candlestick Chart

Candlestick charts trace their roots to Japan, where technical

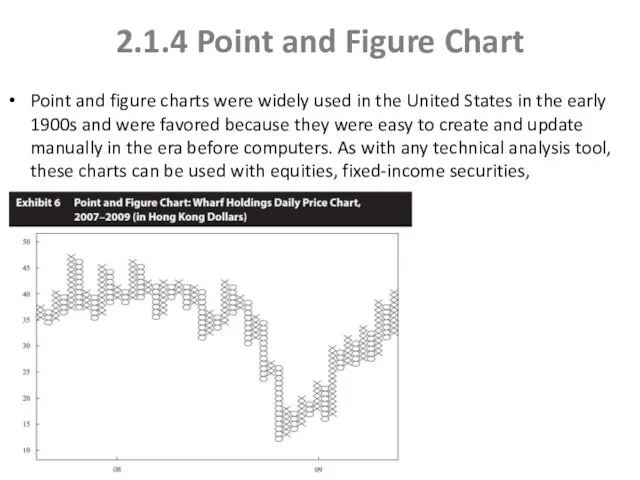

2.1.4 Point and Figure Chart

Point and figure charts were widely used

2.1.4 Point and Figure Chart

Point and figure charts were widely used

Volume, Time Intervals

Volume is used to assess the strength or conviction

Volume, Time Intervals

Volume is used to assess the strength or conviction

Relative Strength Analysis

Relative strength analysis is widely used to compare the

Relative Strength Analysis

Relative strength analysis is widely used to compare the

TREND

The concept of a trend is perhaps the most important aspect

TREND

The concept of a trend is perhaps the most important aspect

CHART PATTERNS

Chart patterns are formations that appear in price charts that

CHART PATTERNS

Chart patterns are formations that appear in price charts that

Head and shoulders pattern

Volume is an important characteristic in interpreting this

Head and shoulders pattern

Volume is an important characteristic in interpreting this

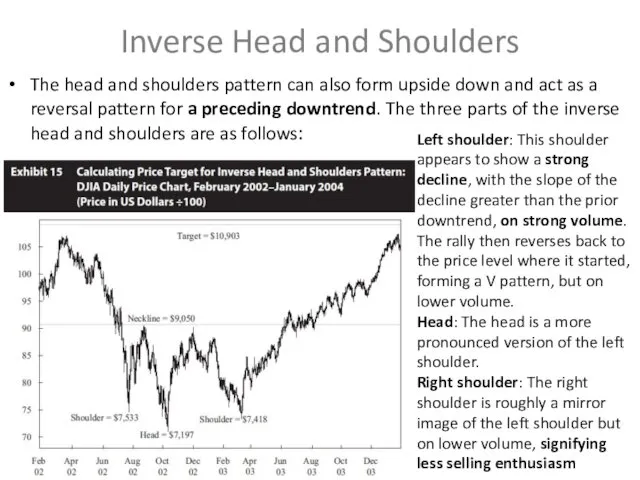

Inverse Head and Shoulders

The head and shoulders pattern can also form

Inverse Head and Shoulders

The head and shoulders pattern can also form

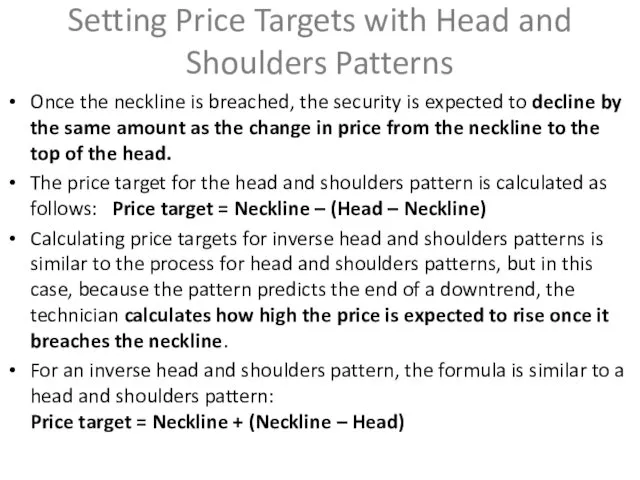

Setting Price Targets with Head and Shoulders Patterns

Once the neckline is

Setting Price Targets with Head and Shoulders Patterns

Once the neckline is

Double Tops

A double top is when an uptrend reverses twice at

Double Tops

A double top is when an uptrend reverses twice at

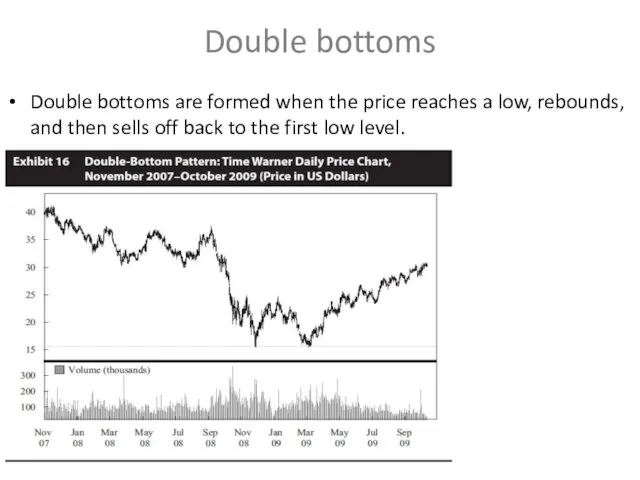

Double bottoms

Double bottoms are formed when the price reaches a low,

Double bottoms

Double bottoms are formed when the price reaches a low,

The reason of Double Tops and Bottoms patterns

For an uptrend, a

The reason of Double Tops and Bottoms patterns

For an uptrend, a

Triple Tops and Bottoms

Triple tops consist of three peaks at roughly

Triple Tops and Bottoms

Triple tops consist of three peaks at roughly

Continuation Patterns

Continuation patterns indicate that a market trend in place prior

Continuation Patterns

Continuation patterns indicate that a market trend in place prior

Ascending triangles

An ascending triangle typically forms in an uptrend. The horizontal

Ascending triangles

An ascending triangle typically forms in an uptrend. The horizontal

Descending triangles

Descending triangle will form in a downtrend. At some point

Descending triangles

Descending triangle will form in a downtrend. At some point

Symmetrical triangles

In a symmetrical triangle, the trendline formed by the highs

Symmetrical triangles

In a symmetrical triangle, the trendline formed by the highs

Rectangle Pattern

The horizontal resistance line that forms the top of the

Rectangle Pattern

The horizontal resistance line that forms the top of the

Flags and Pennants

Flags and pennants are considered minor continuation patterns because

Flags and Pennants

Flags and pennants are considered minor continuation patterns because

2.2 Technical Indicators

The technical analyst uses a variety of technical indicators

2.2 Technical Indicators

The technical analyst uses a variety of technical indicators

2.2.1.1 Moving Average

A moving average is the average of the closing

2.2.1.1 Moving Average

A moving average is the average of the closing

2.2.1.2 Bollinger Bands

Bollinger Bands consist of a moving average plus a

2.2.1.2 Bollinger Bands

Bollinger Bands consist of a moving average plus a

2.2.2 Momentum Oscillators

One of the key challenges in using indicators overlaid

2.2.2 Momentum Oscillators

One of the key challenges in using indicators overlaid

2.2.2.1 Momentum or Rate of Change Oscillator

An alternative method of constructing

2.2.2.1 Momentum or Rate of Change Oscillator

An alternative method of constructing

2.2.2.2Relative Strength Index

The index construction forces the RSI to lie within

2.2.2.2Relative Strength Index

The index construction forces the RSI to lie within

2.2.2.3 Stochastic Oscillator

The stochastic oscillator is based on the observation that

2.2.2.3 Stochastic Oscillator

The stochastic oscillator is based on the observation that

2.2.2.4 Moving-Average Convergence/Divergence Oscillator

The MACD is the difference between a short-term

2.2.2.4 Moving-Average Convergence/Divergence Oscillator

The MACD is the difference between a short-term

2.2.3 Sentiment Indicators

Sentiment indicators attempt to gauge investor activity for signs

2.2.3 Sentiment Indicators

Sentiment indicators attempt to gauge investor activity for signs

2.2.3.2 Calculated Statistical Indices

The other category of sentiment indicators are indicators

2.2.3.2 Calculated Statistical Indices

The other category of sentiment indicators are indicators

Margin debt and Short interest

Margin debt is also often used

Margin debt and Short interest

Margin debt is also often used

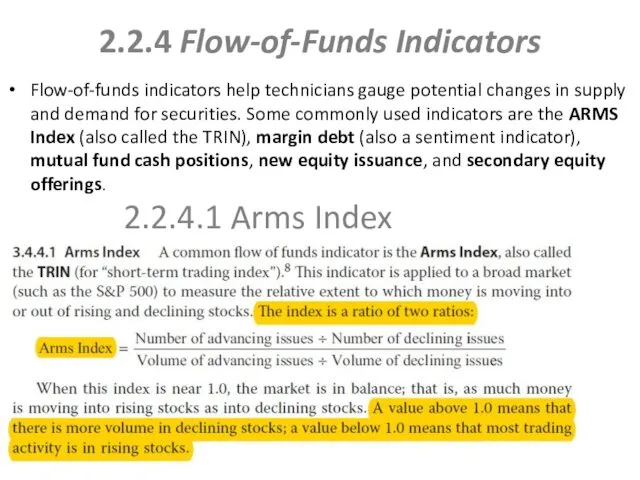

2.2.4 Flow-of-Funds Indicators

Flow-of-funds indicators help technicians gauge potential changes in supply

2.2.4 Flow-of-Funds Indicators

Flow-of-funds indicators help technicians gauge potential changes in supply

Margin debt is also widely used as a flow-of-funds indicator because

Margin debt is also widely used as a flow-of-funds indicator because

Putting more shares on the market increases the aggregate supply of

INTERMARKET ANALYSIS

Intermarket analysis is based on the principle that all markets

INTERMARKET ANALYSIS

Intermarket analysis is based on the principle that all markets

World economics intro

World economics intro Изучение динамики социально-экономических явлений

Изучение динамики социально-экономических явлений Голландская болезнь в России 2000-х годов. Негативный эффект, оказываемый укреплением реального курса национальной валюты

Голландская болезнь в России 2000-х годов. Негативный эффект, оказываемый укреплением реального курса национальной валюты Экономика и ее роль в жизни общества

Экономика и ее роль в жизни общества Қазақстанның үшінші жаңғыруы: жахандық бəссекеге кабілектіллік

Қазақстанның үшінші жаңғыруы: жахандық бəссекеге кабілектіллік Экономический анализ. Анализ маркетинговой деятельности предприятия

Экономический анализ. Анализ маркетинговой деятельности предприятия Совокупный спрос и совокупное предложение

Совокупный спрос и совокупное предложение Особенности инвестиционной деятельности в Австрии

Особенности инвестиционной деятельности в Австрии Рынок и его функции

Рынок и его функции Основные макроэкономические показатели

Основные макроэкономические показатели Особенности методики школьного экономического образования. (Лекция 2)

Особенности методики школьного экономического образования. (Лекция 2) Действие основных экономических законов на фармацевтическом рынке

Действие основных экономических законов на фармацевтическом рынке Первичный сектор экономики. (8 класс)

Первичный сектор экономики. (8 класс) Потребительский рынок

Потребительский рынок Economics of innovation. Lecture 3: Innovation, Demand and Consumption

Economics of innovation. Lecture 3: Innovation, Demand and Consumption Тема 7. Кругооборот і оборот капіталу. Лекція 1. Рух капіталу, його стадії і форми. Функціональні форми капіталу

Тема 7. Кругооборот і оборот капіталу. Лекція 1. Рух капіталу, його стадії і форми. Функціональні форми капіталу Формы и методы государственного регулирования

Формы и методы государственного регулирования Теория спроса и предложения

Теория спроса и предложения Экономическое районирование Калужской области

Экономическое районирование Калужской области Основы общественного производства. (Тема 2)

Основы общественного производства. (Тема 2) Евросоюз: начало распада или временные трудности?

Евросоюз: начало распада или временные трудности? Предмет и методы ЭТ. Базовые экономические категории. Лекция 1

Предмет и методы ЭТ. Базовые экономические категории. Лекция 1 Сущность прогнозирования и планирования в экономике

Сущность прогнозирования и планирования в экономике Жүкті қоймалау, жүк тарасы, орау және қайта өңдеу

Жүкті қоймалау, жүк тарасы, орау және қайта өңдеу Альтернативная стоимость

Альтернативная стоимость Обмен. Виды обмена

Обмен. Виды обмена Обеспечение экономической состоятельности организации

Обеспечение экономической состоятельности организации Прогнозирование и планирование сбыта продукции

Прогнозирование и планирование сбыта продукции