- Online-banking in Belarus

Содержание

- 2. Online-banking in Belarus. Performed by: Shitenok Valeria.

- 3. YOU CAN WASTE TWO HOURS STANDING IN A QUEUE OR YOU CAN CLICK A MOUSE TWICE

- 4. Content: When did Online-banking appear? What is Online-banking? Online-banking: the arguments “for“. Online-banking: the arguments “against“.

- 5. When? The first online-banking service in United States was introduced in October 1994. The service was

- 6. What is ? This is a system of remote account management via the Internet. Online-banking allows

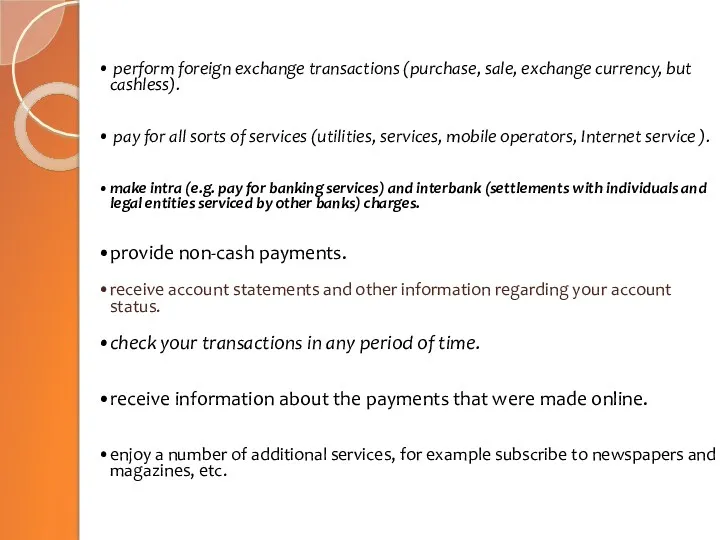

- 7. perform foreign exchange transactions (purchase, sale, exchange currency, but cashless). pay for all sorts of services

- 8. Online-banking: the arguments “for“: 1. The most obvious advantage of Online-banking - time savings. The client

- 9. Online-banking: the arguments “against“. 1. The Bank actually transfers the client functions of the teller. That

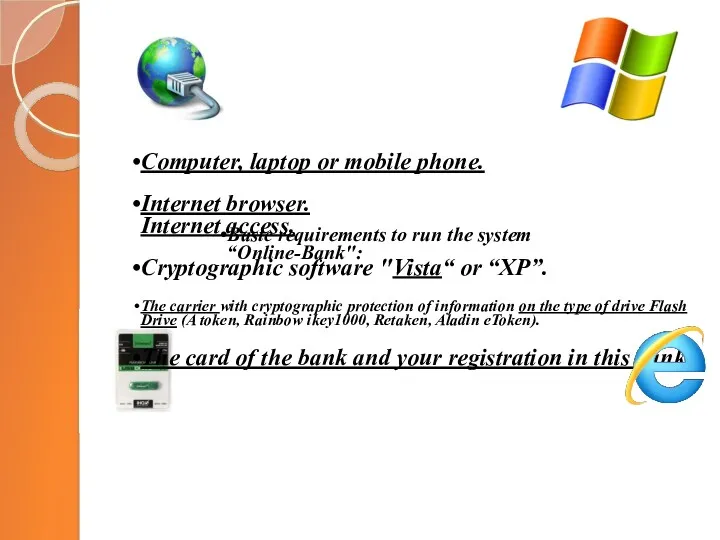

- 10. Computer, laptop or mobile phone. Internet browser. Internet access. Cryptographic software "Vista“ or “XP”. The carrier

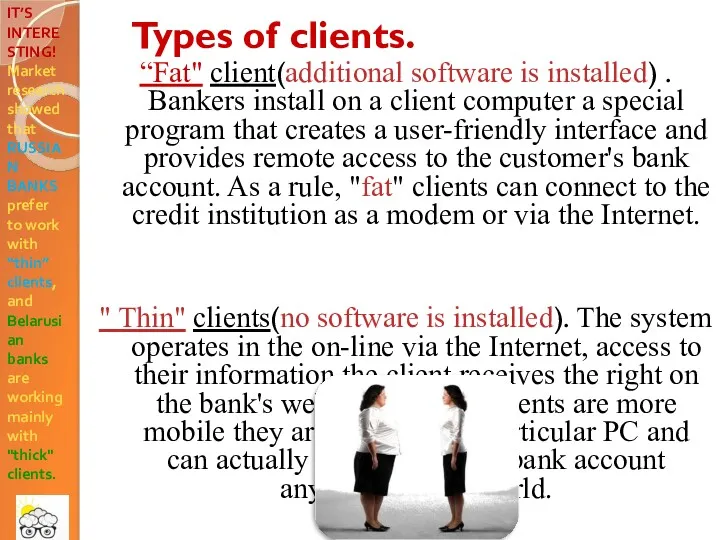

- 11. “Fat" client(additional software is installed) . Bankers install on a client computer a special program that

- 12. The principles of operation of Internet banking. Three schemes of Internet banking:

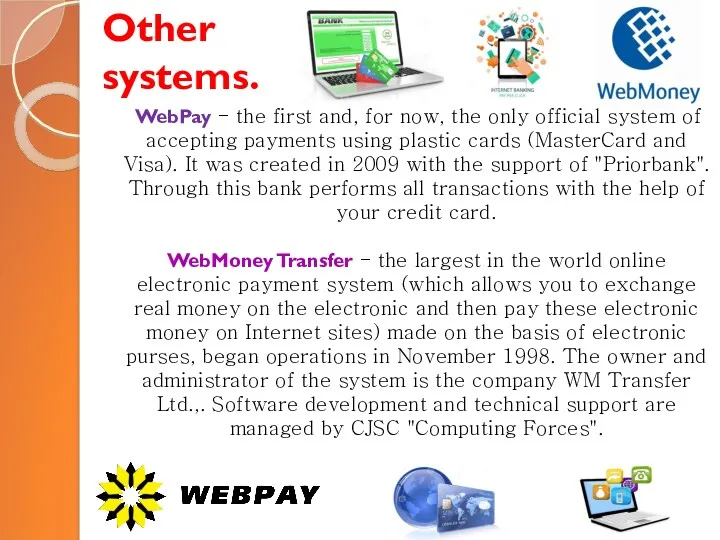

- 13. Other systems. WebPay - the first and, for now, the only official system of accepting payments

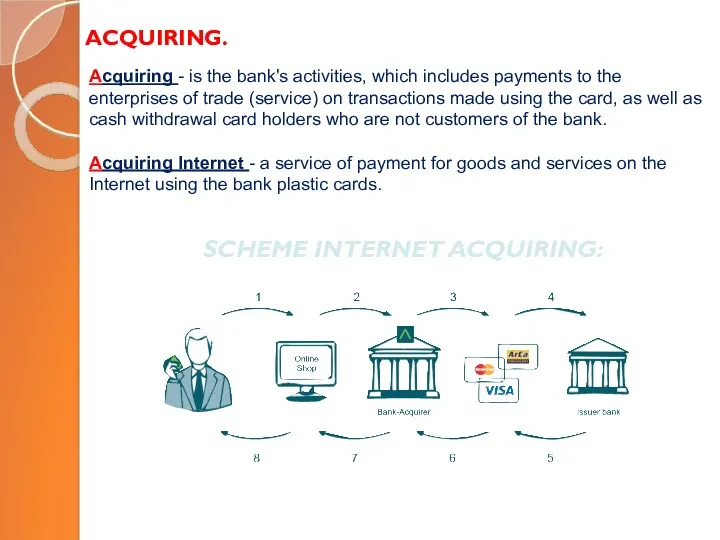

- 14. ACQUIRING. Acquiring - is the bank's activities, which includes payments to the enterprises of trade (service)

- 16. Скачать презентацию

Online-banking in Belarus.

Performed by:

Shitenok Valeria.

Online-banking in Belarus.

Performed by:

Shitenok Valeria.

YOU CAN WASTE TWO HOURS STANDING IN A QUEUE

OR YOU

YOU CAN WASTE TWO HOURS STANDING IN A QUEUE OR YOU

Content:

When did Online-banking appear?

What is Online-banking?

Online-banking: the arguments “for“.

Online-banking: the arguments

Content:

When did Online-banking appear?

What is Online-banking?

Online-banking: the arguments “for“.

Online-banking: the arguments

When?

The first online-banking service in United States was introduced in October

When?

The first online-banking service in United States was introduced in October

What is ?

This is a system of remote account management via

What is ?

This is a system of remote account management via

perform foreign exchange transactions (purchase, sale, exchange currency, but cashless).

perform foreign exchange transactions (purchase, sale, exchange currency, but cashless).

Online-banking: the arguments “for“:

1.

The most obvious advantage of Online-banking

Online-banking: the arguments “for“:

1.

The most obvious advantage of Online-banking

Online-banking: the arguments “against“.

1.

The Bank actually transfers the client

Online-banking: the arguments “against“.

1.

The Bank actually transfers the client

Computer, laptop or mobile phone.

Internet browser.

Internet access.

Cryptographic software "Vista“ or “XP”.

The

Computer, laptop or mobile phone.

Internet browser.

Internet access.

Cryptographic software "Vista“ or “XP”.

The

“Fat" client(additional software is installed) . Bankers install on a client

“Fat" client(additional software is installed) . Bankers install on a client

The principles of operation of Internet banking.

Three schemes of Internet banking:

The principles of operation of Internet banking.

Three schemes of Internet banking:

Other systems.

WebPay - the first and, for now, the only

Other systems.

WebPay - the first and, for now, the only

ACQUIRING.

Acquiring - is the bank's activities, which includes payments to the

ACQUIRING.

Acquiring - is the bank's activities, which includes payments to the

Анализ алгоритмов

Анализ алгоритмов Урок по созданию диаграмм в Excel для финансовых отчетов

Урок по созданию диаграмм в Excel для финансовых отчетов Интернет-этикет сетикет или по-другому нетикет

Интернет-этикет сетикет или по-другому нетикет Как вести себя в Интернете? Безопасность в сети Интернет

Как вести себя в Интернете? Безопасность в сети Интернет Алгоритм и исполнители

Алгоритм и исполнители Общие сведения о языке программирования Паскаль. Начала программирования. Информатика. 8 класс

Общие сведения о языке программирования Паскаль. Начала программирования. Информатика. 8 класс Электронные таблицы. MS Excel

Электронные таблицы. MS Excel Контент-анализ как количественный метод исследования текстов

Контент-анализ как количественный метод исследования текстов Лекция 2016.3. Построение конфигурации. Дерево конфигурации

Лекция 2016.3. Построение конфигурации. Дерево конфигурации Форматирование текста в текстовом редакторе MS Word

Форматирование текста в текстовом редакторе MS Word Приложения по информатике

Приложения по информатике Обратное распространение ошибки. Практика

Обратное распространение ошибки. Практика Цикл с параметром

Цикл с параметром Назначение и возможности табличного процессора MS Excel

Назначение и возможности табличного процессора MS Excel Носії інформації

Носії інформації Виртуальные машины и их операционные системы

Виртуальные машины и их операционные системы Протоколы IPTV

Протоколы IPTV Создание веб-страниц в WORD. Проектирование веб-сайта

Создание веб-страниц в WORD. Проектирование веб-сайта История развития ООП. Базовые понятия ООП: объект, его свойства и методы, класс, интерфейс

История развития ООП. Базовые понятия ООП: объект, его свойства и методы, класс, интерфейс Запись чисел в различных системах счисления

Запись чисел в различных системах счисления Создание структуры базы данных. Семинар 3. Лекция 1. Первое знакомство с базами данных

Создание структуры базы данных. Семинар 3. Лекция 1. Первое знакомство с базами данных Организация ввода и вывода данных. Начала программирования

Организация ввода и вывода данных. Начала программирования Рецензия - отзыв, разбор и оценка

Рецензия - отзыв, разбор и оценка Суммирование элементов массива, вычисления следа матрицы, суммирование двух массивов

Суммирование элементов массива, вычисления следа матрицы, суммирование двух массивов Современные системы автоматизации

Современные системы автоматизации Проектирование информационной системы учета услуг по монтажу и ремонту электрооборудования

Проектирование информационной системы учета услуг по монтажу и ремонту электрооборудования SOFiSTiK: Расчет монолитных железобетонных плит с учетом физической нелинейности 21.05.2013

SOFiSTiK: Расчет монолитных железобетонных плит с учетом физической нелинейности 21.05.2013 Лекция 8. Форматы графических файлов. Формат JPEG

Лекция 8. Форматы графических файлов. Формат JPEG