- Sample BUAD 691

Содержание

- 2. About Coach Founded in 1941 in New York Distributes products primarily through company stores in North

- 3. Can Coach Continue to Grow? Highly successful growth 2000-2011 Sales +11% CAGR Net income increased 55x

- 4. External Environment Political Tax Policy Environmental Leather goods/PETA Sociocultural -“Affordable” luxury demand -Brand relevance & loyalty

- 5. “Affordable” Luxury Driving Forces Design & brand reputation Lead fashion/style trends Brand loyalty, exclusivity Quality Sturdy,

- 6. Porter’s Five Forces Substitutes -Many competitors at higher & lower prices -Brand loyalty, reputation mitigate threat

- 7. Global Handbag Market Analysis In 2010, world spend $224 billion on luxury goods Gender split -

- 8. Key Competitors Competitors around the globe Sales dependent on diffusion lines Coach seen as high end

- 9. Key Factors for Success Political Tax Policy Environmental Growing demand in emerging markets Sociocultural Popular with

- 10. Major Business Strategy Primary consumer is mid to upper class women Trying to reach more men

- 11. Core & Distinctive Competencies Retailing- architecture in stores Sales Reps – sales training of the workers

- 12. Value Chain & SWOT Value Chain Differentiation Accessibility Direct/Indirect Channels Distribution Channels Supply Chain SWOT Brand

- 13. Distribution Company Stores Retail Stores Factory Outlets Department Stores Direct to Consumer Internet Sales Catalog Sales

- 14. International Presence Coach seeks to become a Global Lifestyle brand Growth initiatives Store expansion in US,

- 15. Key Question Can Coach's current positioning strategy be sustained in light of external and internal analyses?

- 16. Key Financials Strong Financial Results Sales Growth – strong sales growth 2007-2011 COGS – growing faster

- 17. Solid Balance Sheet Current Ratio: 2011- 1,452,388/593,017= 2.45 2010- 1,302,641/529,036= 2.46 ROA: 2011- 880,800/2,635,116= 33.43 2010-

- 18. Share Price Trends 2009-2011 In 2009, Coach acquired Image X group Provided greater control over the

- 19. Causes of SG&A Expense Increases SG&A up $700 milion from 2007-2011 Wholesale distribution in international markets

- 20. Differentiation Recommendation Maintain a Broad Differentiation Strategy Provide both tangible and intangible features in products Continue

- 21. Marketing Recommendation (Broad Differentiation - Marketing Emphasis) Invest in non-traditional marketing – such as publicity &

- 22. Constant Innovation Recommendation (Broad Differentiation – Product Emphasis) Stress Constant Innovation Consider carefully expand non-handbag leather

- 23. Blue Ocean Recommendation Blue Ocean Strategy Offer a fully customizable line of products Gives customer opportunity

- 24. Sub-brand Recommendation Consider launching an up-market sub-brand at higher prices to compete against traditional players now

- 25. International Recommendations Accelerate growth in Asia Focus on growing male segment Male specific stores 25% market

- 27. Скачать презентацию

About Coach

Founded in 1941 in New York

Distributes products primarily through company

About Coach

Founded in 1941 in New York

Distributes products primarily through company

Can Coach Continue to Grow?

Highly successful growth 2000-2011

Sales +11% CAGR

Net

Can Coach Continue to Grow?

Highly successful growth 2000-2011

Sales +11% CAGR

Net

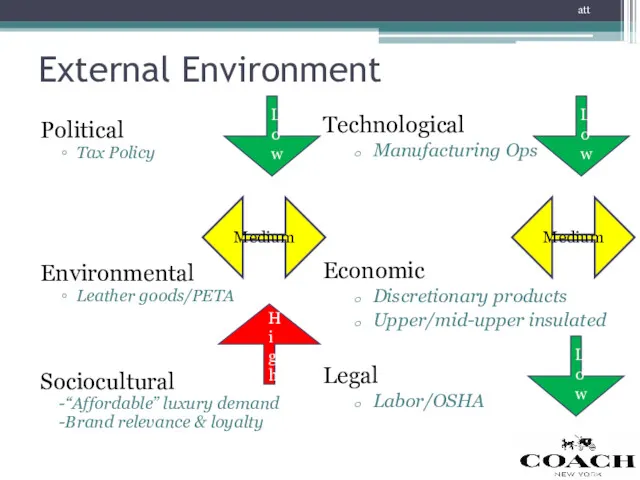

External Environment

Political

Tax Policy

Environmental

Leather goods/PETA

Sociocultural

-“Affordable” luxury demand

-Brand relevance & loyalty

Technological

Manufacturing Ops

Economic

Discretionary products

Upper/mid-upper

External Environment

Political

Tax Policy

Environmental

Leather goods/PETA

Sociocultural

-“Affordable” luxury demand

-Brand relevance & loyalty

Technological

Manufacturing Ops

Economic

Discretionary products

Upper/mid-upper

“Affordable” Luxury Driving Forces

Design & brand reputation

Lead fashion/style trends

Brand loyalty, exclusivity

Quality

Sturdy,

“Affordable” Luxury Driving Forces

Design & brand reputation

Lead fashion/style trends

Brand loyalty, exclusivity

Quality

Sturdy,

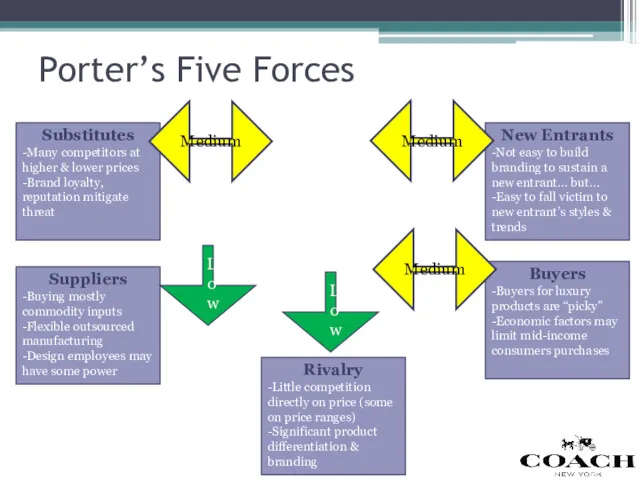

Porter’s Five Forces

Substitutes

-Many competitors at higher & lower prices

-Brand loyalty, reputation

Porter’s Five Forces

Substitutes

-Many competitors at higher & lower prices

-Brand loyalty, reputation

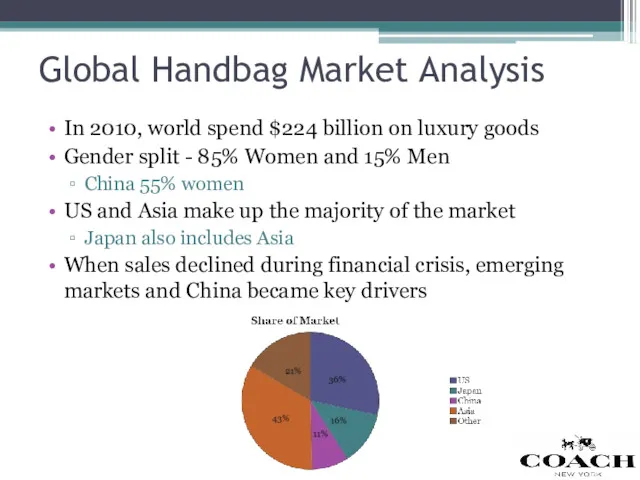

Global Handbag Market Analysis

In 2010, world spend $224 billion on luxury

Global Handbag Market Analysis

In 2010, world spend $224 billion on luxury

Key Competitors

Competitors around the globe

Sales dependent on diffusion lines

Coach seen as

Key Competitors

Competitors around the globe

Sales dependent on diffusion lines

Coach seen as

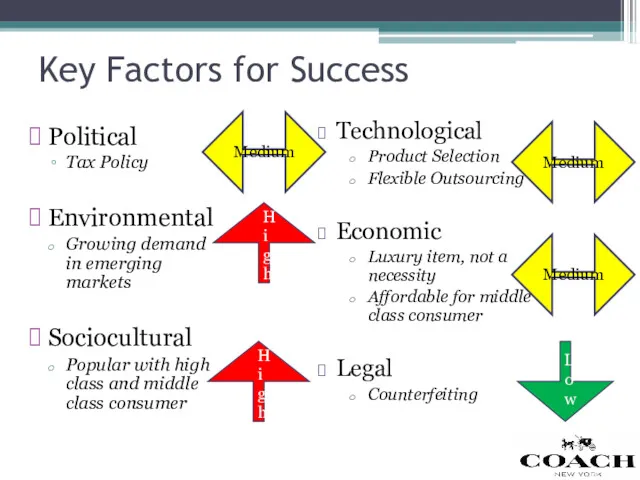

Key Factors for Success

Political

Tax Policy

Environmental

Growing demand in emerging markets

Sociocultural

Popular with high

Key Factors for Success

Political

Tax Policy

Environmental

Growing demand in emerging markets

Sociocultural

Popular with high

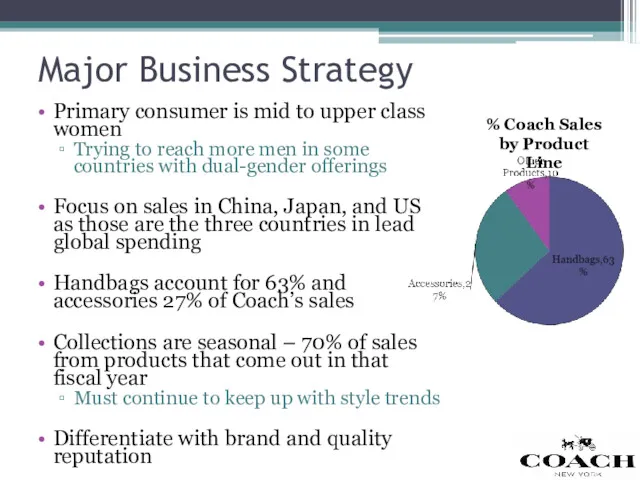

Major Business Strategy

Primary consumer is mid to upper class women

Trying to

Major Business Strategy

Primary consumer is mid to upper class women

Trying to

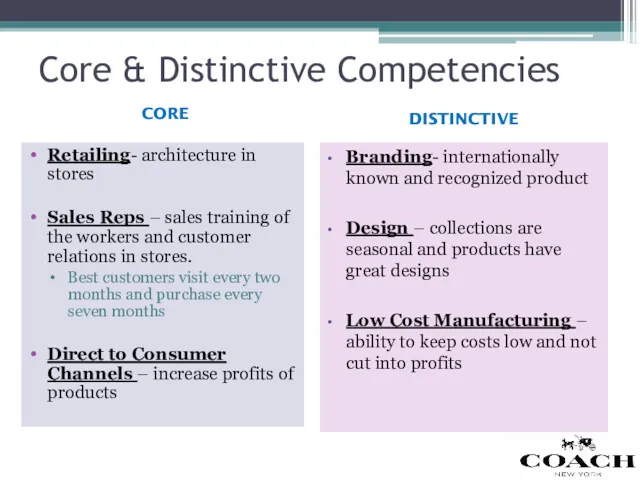

Core & Distinctive Competencies

Retailing- architecture in stores

Sales Reps – sales training

Core & Distinctive Competencies

Retailing- architecture in stores

Sales Reps – sales training

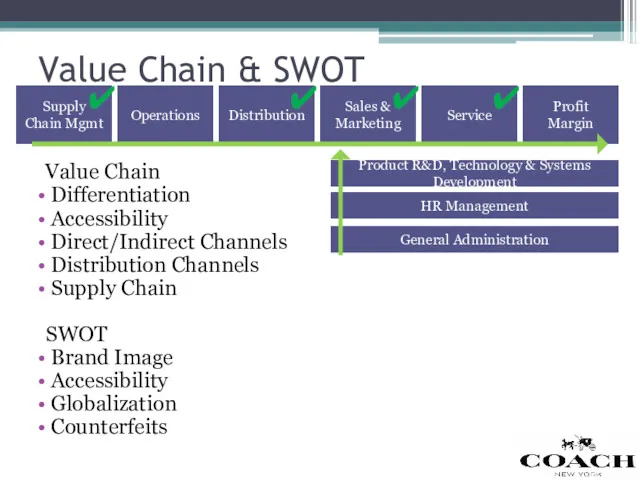

Value Chain & SWOT

Value Chain

Differentiation

Accessibility

Direct/Indirect Channels

Distribution Channels

Value Chain & SWOT

Value Chain

Differentiation

Accessibility

Direct/Indirect Channels

Distribution Channels

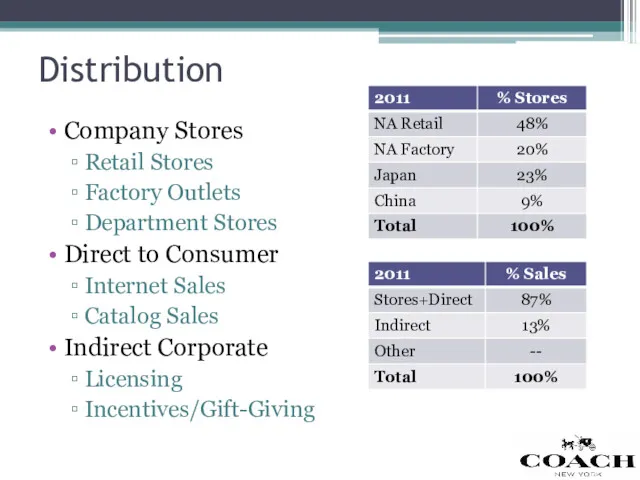

Distribution

Company Stores

Retail Stores

Factory Outlets

Department Stores

Direct to Consumer

Internet Sales

Catalog Sales

Indirect Corporate

Licensing

Incentives/Gift-Giving

Distribution

Company Stores

Retail Stores

Factory Outlets

Department Stores

Direct to Consumer

Internet Sales

Catalog Sales

Indirect Corporate

Licensing

Incentives/Gift-Giving

International Presence

Coach seeks to become a Global Lifestyle brand

Growth initiatives

Store expansion

International Presence

Coach seeks to become a Global Lifestyle brand

Growth initiatives

Store expansion

Key Question

Can Coach's current positioning strategy be sustained in light of

Key Question

Can Coach's current positioning strategy be sustained in light of

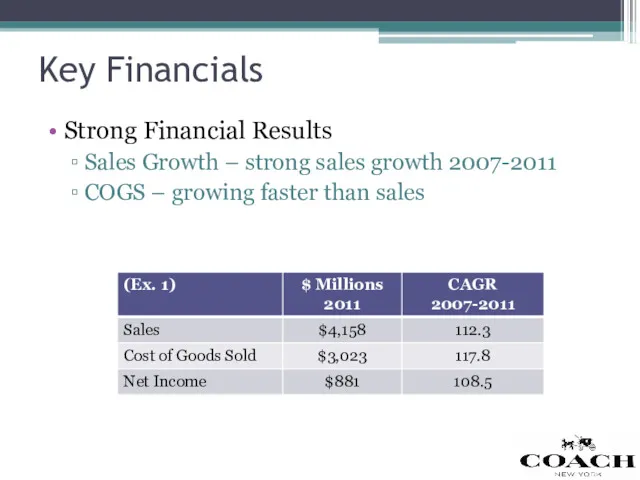

Key Financials

Strong Financial Results

Sales Growth – strong sales growth 2007-2011

COGS

Key Financials

Strong Financial Results

Sales Growth – strong sales growth 2007-2011

COGS

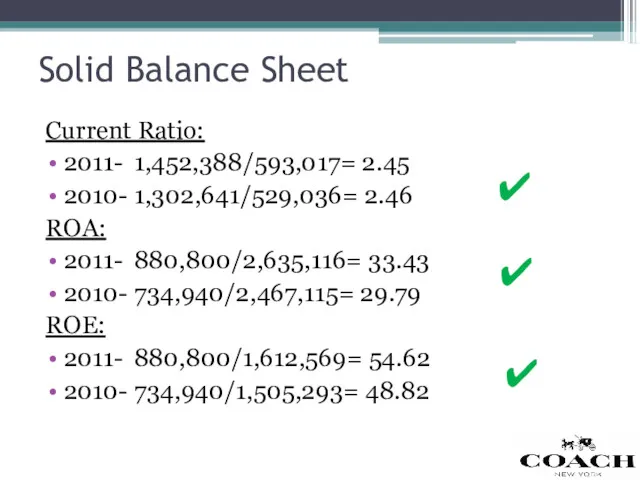

Solid Balance Sheet

Current Ratio:

2011- 1,452,388/593,017= 2.45

2010- 1,302,641/529,036= 2.46

ROA:

2011- 880,800/2,635,116= 33.43

2010- 734,940/2,467,115= 29.79

ROE:

2011- 880,800/1,612,569= 54.62

2010- 734,940/1,505,293=

Solid Balance Sheet

Current Ratio:

2011- 1,452,388/593,017= 2.45

2010- 1,302,641/529,036= 2.46

ROA:

2011- 880,800/2,635,116= 33.43

2010- 734,940/2,467,115= 29.79

ROE:

2011- 880,800/1,612,569= 54.62

2010- 734,940/1,505,293=

Share Price Trends 2009-2011

In 2009, Coach acquired Image X group

Provided greater

Share Price Trends 2009-2011

In 2009, Coach acquired Image X group

Provided greater

Causes of SG&A Expense Increases

SG&A up $700 milion from 2007-2011

Wholesale distribution

Causes of SG&A Expense Increases

SG&A up $700 milion from 2007-2011

Wholesale distribution

Differentiation Recommendation

Maintain a Broad Differentiation Strategy

Provide both tangible and intangible features

Differentiation Recommendation

Maintain a Broad Differentiation Strategy

Provide both tangible and intangible features

Marketing Recommendation

(Broad Differentiation - Marketing Emphasis)

Invest in non-traditional marketing – such

Marketing Recommendation

(Broad Differentiation - Marketing Emphasis)

Invest in non-traditional marketing – such

Constant Innovation Recommendation

(Broad Differentiation – Product Emphasis)

Stress Constant Innovation

Consider carefully expand

Constant Innovation Recommendation

(Broad Differentiation – Product Emphasis)

Stress Constant Innovation

Consider carefully expand

Blue Ocean Recommendation

Blue Ocean Strategy

Offer a fully customizable line of products

Gives

Blue Ocean Recommendation

Blue Ocean Strategy

Offer a fully customizable line of products

Gives

Sub-brand Recommendation

Consider launching an up-market sub-brand at higher prices to compete

Sub-brand Recommendation

Consider launching an up-market sub-brand at higher prices to compete

International Recommendations

Accelerate growth in Asia

Focus on growing male segment

Male specific

International Recommendations

Accelerate growth in Asia

Focus on growing male segment

Male specific

Испания, остров Майорка

Испания, остров Майорка ПРЕЗЕНТАЦИЯ дистрибьюторской компании ИП ПЕТИН К. П

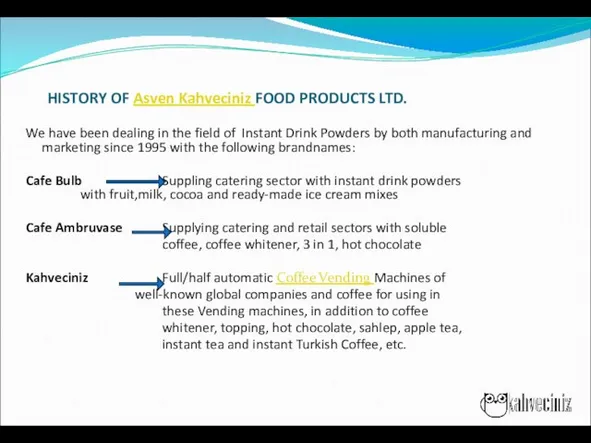

ПРЕЗЕНТАЦИЯ дистрибьюторской компании ИП ПЕТИН К. П History of Asven Kahveciniz Food products LTD

History of Asven Kahveciniz Food products LTD Online shopping behavior of customers

Online shopping behavior of customers Спілкування менеджера з клієнтом

Спілкування менеджера з клієнтом SMM стратегия (название бренда/продукта)

SMM стратегия (название бренда/продукта) Анализ рынка

Анализ рынка Коммуникационная политика. Реклама в системе маркетинговых коммуникаций

Коммуникационная политика. Реклама в системе маркетинговых коммуникаций Типология гостей

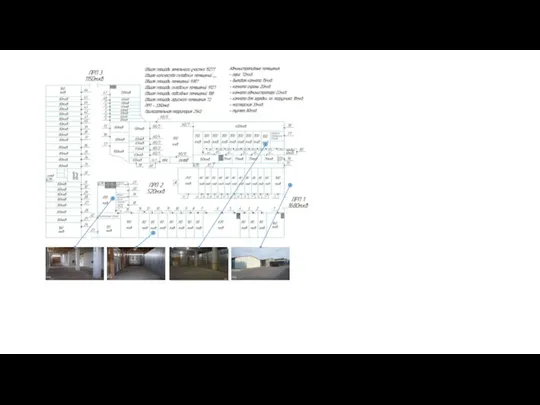

Типология гостей Сдача помещений в аренду

Сдача помещений в аренду Системный курс-практикум Маркетинг PRO. Модуль 15. Реклама и медиапланирование

Системный курс-практикум Маркетинг PRO. Модуль 15. Реклама и медиапланирование Key elements of brand Amazon Kindle

Key elements of brand Amazon Kindle Орифлейм компаниясының мүмкіндіктері

Орифлейм компаниясының мүмкіндіктері Управление инновационным проектом

Управление инновационным проектом Методы управления инновациями

Методы управления инновациями Дорожные сервисы

Дорожные сервисы ТОВ Ромни-Кондитер

ТОВ Ромни-Кондитер 97% природная алоэ-забота о коже и волосах. Компания ВИТЭКС

97% природная алоэ-забота о коже и волосах. Компания ВИТЭКС Моя микрозелень. Вертикальные фермы

Моя микрозелень. Вертикальные фермы Эффективная презентация компании и ее предложений. Занятие 3

Эффективная презентация компании и ее предложений. Занятие 3 5 постулатов посадочной страницы

5 постулатов посадочной страницы Создание и продвижение бренда (на примере кондитерской фабрики Россия филиал, в г. Самара ООО Нестле Россия)

Создание и продвижение бренда (на примере кондитерской фабрики Россия филиал, в г. Самара ООО Нестле Россия) Маркетинговая деятельность как условие конкурентоспособности оптовой организации на рынке лекарственных препаратов

Маркетинговая деятельность как условие конкурентоспособности оптовой организации на рынке лекарственных препаратов Dspm. Фундаментальные основы продаж

Dspm. Фундаментальные основы продаж Создание туристского продукта. Маркетинг сельских территорий

Создание туристского продукта. Маркетинг сельских территорий Маркетинг в образовательной организации: актуальные проблемы реализации в современных условиях модернизации образования

Маркетинг в образовательной организации: актуальные проблемы реализации в современных условиях модернизации образования Холудексан

Холудексан AZIMUT Hotel Sochi – Ваш незабываемый отдых в Сочи

AZIMUT Hotel Sochi – Ваш незабываемый отдых в Сочи