- Strategic and operating review

Содержание

- 2. AGENDA TRADING UPDATE LEARNINGS DEEP DIVE: CUSTOMER PROPOSITION CONCLUSION / Q&A I. II. III. IV.

- 3. SAMARA FIRST WEEKS OF TRADING UPDATE First weeks sales: Sales budget: Sales % by category: EPOS

- 4. MARKETING & CUSTOMER FEEDBACK Store Launch- Marketing Initial customer feedback Quote customers: “XXXXX” Quick feedback research

- 5. TV COMMERCIAL GUIDELINE: play video or other elements of the marketing campaign as appropriate that demonstrate

- 6. ST PETERSBURG- NEXT OPENING GUIDELINE: What went well in Samara? What went not so well? Learning

- 7. AGENDA TRADING UPDATE LEARNINGS DEEP DIVE: CUSTOMER PROPOSITION CONCLUSION / Q&A I. II. III. IV. GUIDELINE:

- 8. Be #1 home improvement retailer in Russia by offering a wide range of quality products at

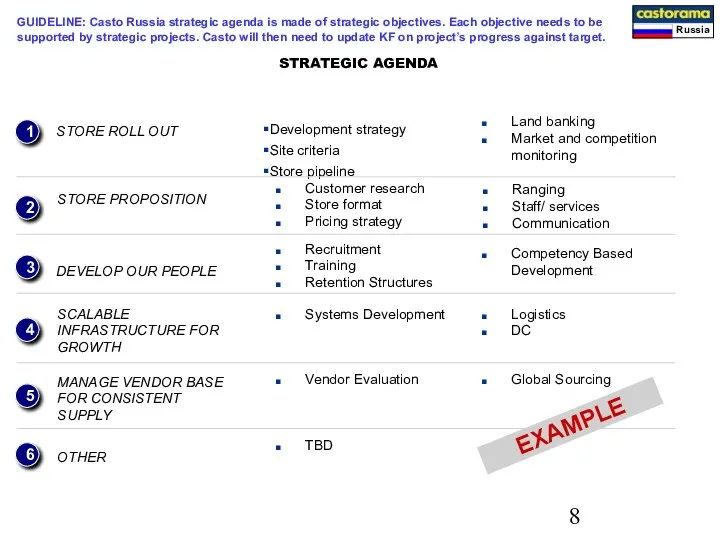

- 9. STRATEGIC AGENDA Development strategy Site criteria Store pipeline STORE ROLL OUT 1 2 3 4 5

- 10. PROGRESS AGAINST STRATEGIC AGENDA IN 2005 OBJECTIVES PROGRESS/ UPDATE Demonstrate progress vs. target 1. STORE ROLL

- 11. OBJECTIVE 1: STORE ROLL OUT KEY LEARNING GUIDELINE: Explain your learning for the year regarding roll

- 12. OBJECTIVE 2: STORE PROPOSITION KEY LEARNING GUIDELINE: Store blue print, key elements of the commercial offer

- 13. OBJECTIVE 3: DEVELOP OUR PEOPLE KEY LEARNING GUIDELINE: Key learning related to recruitment, training needs, local

- 14. OBJECTIVE 4: INFRASTRUCTURE KEY LEARNING I - GUIDELINE: Learning related to what structure will need to

- 15. OBJECTIVE 5: VENDOR BASE KEY LEARNING GUIDELINE: Learning related to vendor, their capacities, 20/80, local vendor

- 16. OBJECTIVE 6: OTHER STRATEGIC OBJECTIVE’S KEY LEARNING GUIDELINE: Others

- 17. SUMMARY OF KEY ACHIEVEMENTS: 2005 XX sites identified and XX Capex approved First stores is ready

- 18. SUMMARY OF KEY CHALLENGES: 2005 Sourcing and KAL? People development, recruitment? Skills? Facilities? Competition development? OBI?

- 19. AGENDA TRADING UPDATE LEARNINGS DEEP DIVE: CUSTOMER PROPOSITION 1. CUSTOMER 2. COMPETITION 3. STORE FORMAT 4.

- 20. LIST OF RESEARCHES THAT HAVE BEEN DONE GUIDELINE: Update this list of researches as for Feb..

- 21. 55% women (as main instigators) 45% men (as main doers) 25-60 years old Married with 1

- 22. RUSSIAN CUSTOMER ARE HEAVY PURCHASERS OF HOME IMPROVEMENT PRODUCT About 80% of respondents made renovation within

- 23. ! ! ! The most important choice criteria: assortment, quality, brands, prices. Then follow special offers,

- 24. REGIONAL DIFFERENCES SHOWS STRONGER DIY POTENTIAL IN THE REGIONS AND GROWING DIFM IN MOSCOW About 40-60%

- 25. ….AND WE NOW UNDERSTAND THE DRIVERS OF REGIONAL DIFFERENCES Source: The Statistics Bureau of respective cities

- 26. Car ownership and Car usage for DIY purchases Most of respondents (more than 60%) in Moscow

- 27. MARKET RESEARCH PROGRAMME IS IN PLACE TO KEEP LEARNING ABOUT CUSTOMERS Reality Customer Experience Customer Perception

- 28. AGENDA TRADING UPDATE LEARNINGS DEEP DIVE: CUSTOMER PROPOSITION 1. CUSTOMER 2. COMPETITION 3. STORE FORMAT 4.

- 29. MOSCOW VS. ST PETERSBURG DIY MARKET Spending for DIY goods Average spending is about 19 800

- 30. Moscow DIY market. Evaluation of Stores vs. Markets Stores Markets Markets win on price, stores on

- 31. MAIN COMPETITORS DEVELOPMENT 2006 STORES* 2005 STORES 2005 SALES XX XX X X XX XX X

- 32. HOME IMPROVEMENT COMPETITOR PERFORMANCE Local International Kashirski Dvor Starik Khottabych Tvoi Dom Maksi Dom Mel’nitsa Mytischinskaya

- 33. MOSCOW COMPETITON REVIEW Source: GFK ad-hoc research “Segment Monitoring of Consumer Habits in DIY Segment –

- 34. MOSCOW COMPETITON MAP Insert map of Moscow competition and stores under construction

- 35. Source: GFK ad-hoc research “Segment Monitoring of Consumer Habits in DIY Segment – Moscow, St. Petersburg”,

- 36. ST PETERSBURG COMPETITON MAP Insert map of St Petersburg competition and stores under construction

- 37. SAMARA COMPETITON REVIEW W/h Mon-Sat W/h Sunday Area Staff Assortment description Additional Summary Bystrosklad Ptichiy market

- 38. AGENDA TRADING UPDATE LEARNINGS DEEP DIVE: CUSTOMER PROPOSITION 1. CUSTOMER 2. COMPETITION 3. STORE FORMAT 4.

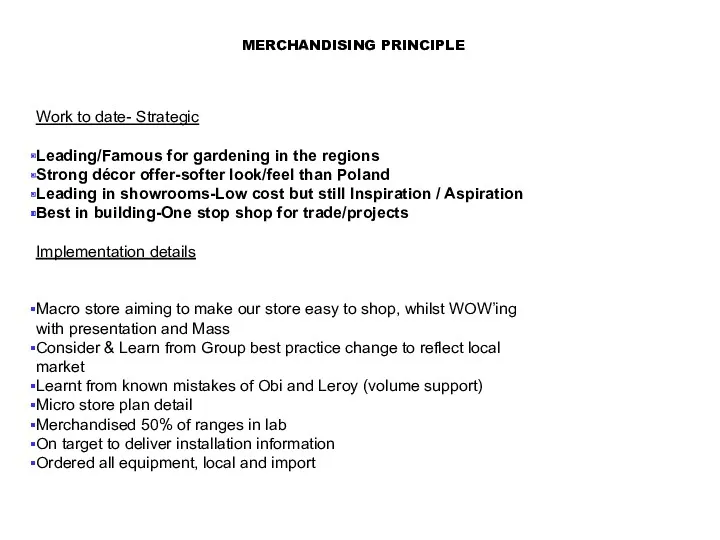

- 39. Work to date- Strategic Leading/Famous for gardening in the regions Strong décor offer-softer look/feel than Poland

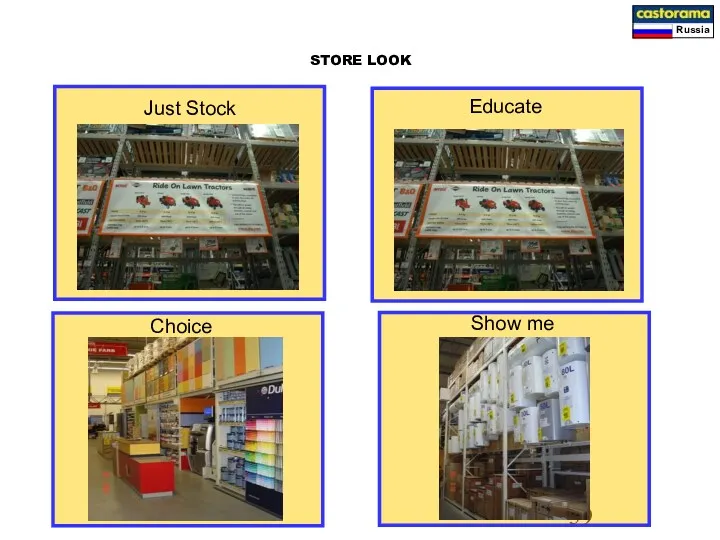

- 40. Just Stock Just Stock Educate STORE LOOK Show me Choice

- 41. STORE LOOK Pallet replenishment How to display, touch and feel & SRP “Stock to show”, “stock

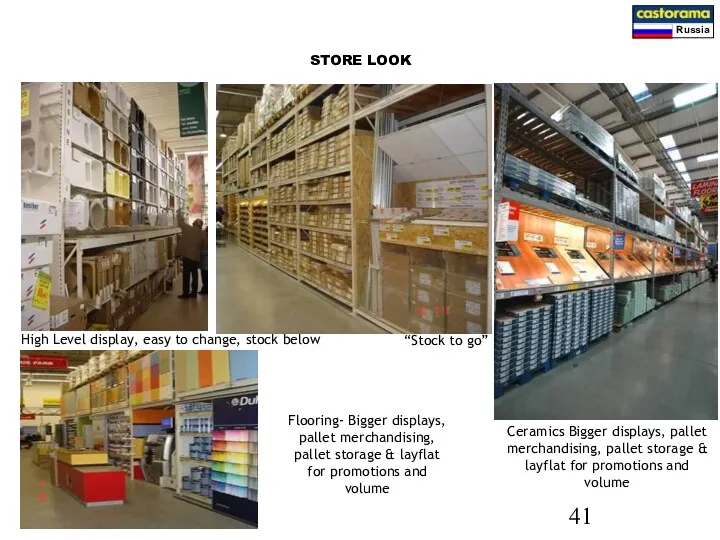

- 42. High Level display, easy to change, stock below “Stock to go” Flooring- Bigger displays, pallet merchandising,

- 45. Demonstrations Finance offer Home delivery Timber, glass, pipe cutting Café Bar Taxi service Info re installation

- 46. AGENDA TRADING UPDATE LEARNINGS DEEP DIVE: CUSTOMER PROPOSITION 1. CUSTOMER 2. COMPETITION 3. STORE FORMAT 4.

- 47. KEY POSITIONING ELEMENTS At least 30% of all renovations are done with involvement of professionals. Professionals

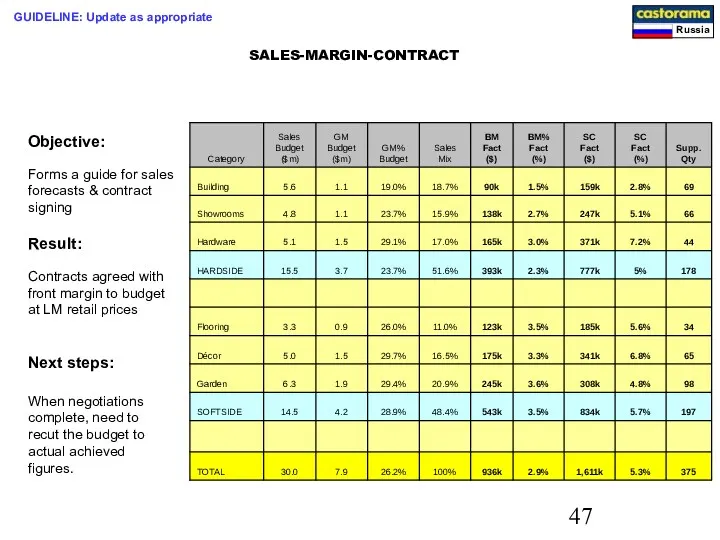

- 48. Objective: Forms a guide for sales forecasts & contract signing Result: Contracts agreed with front margin

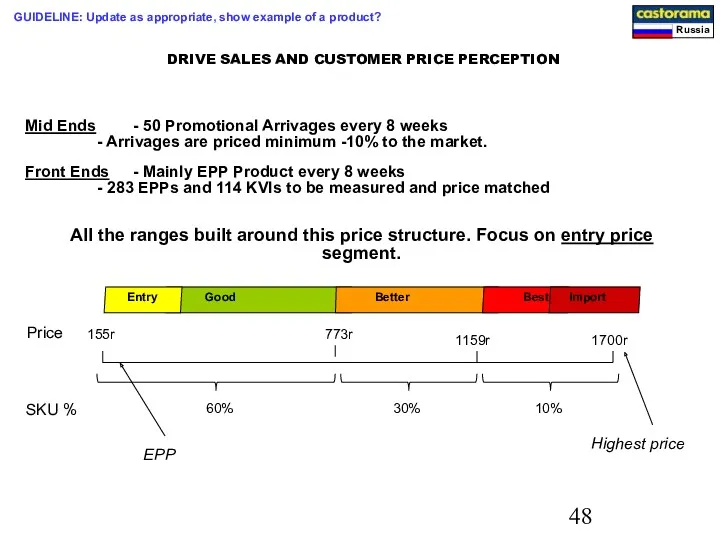

- 49. DRIVE SALES AND CUSTOMER PRICE PERCEPTION Mid Ends - 50 Promotional Arrivages every 8 weeks -

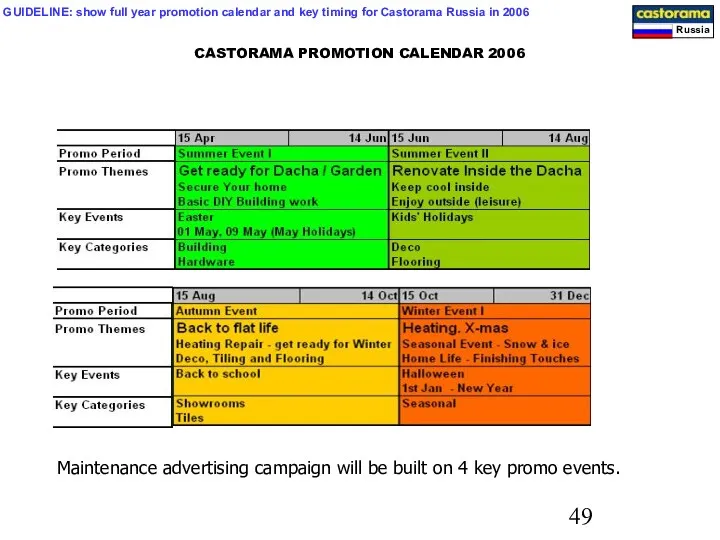

- 50. CASTORAMA PROMOTION CALENDAR 2006 Maintenance advertising campaign will be built on 4 key promo events. GUIDELINE:

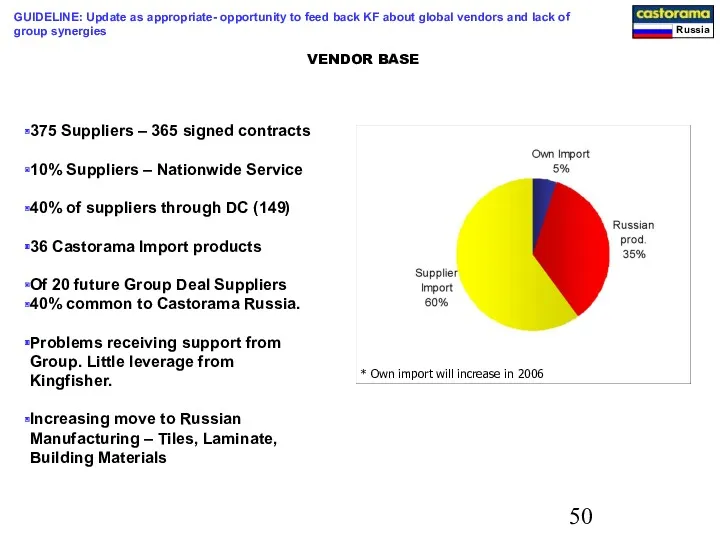

- 51. 375 Suppliers – 365 signed contracts 10% Suppliers – Nationwide Service 40% of suppliers through DC

- 52. AGENDA TRADING UPDATE LEARNINGS DEEP DIVE: CUSTOMER PROPOSITION 1. CUSTOMER 2. COMPETITION 3. STORE FORMAT 4.

- 53. IMPORT Current Status Volume: 5% of total throughput (till end 2006) Purpose: Arrivage for store opening

- 54. DISTRIBUTION Current Status Total flow 35% of total throughput (5% imports +30% cross-docked) Stockholding: imports 90

- 55. EQUIPMENT Background According to Russian Law, foreign investors have the right to import into Russia certain

- 56. DISTRIBUTION CENTRE OVERVIEW Located on the main road to Moscow GUIDELINE: Update as appropriate Show store

- 57. AGENDA TRADING UPDATE LEARNINGS DEEP DIVE: CUSTOMER PROPOSITION FINANCIAL UPDATE CONCLUSION / Q&A I. II. III.

- 58. SUMMARY P&L COMMENT 2005 ACTUAL £ m % OF SALES Comments Comments Comments Comments Comments VAR

- 59. CAPITAL EXPENDITURE £ ‘m Property Land+ Building Retail Fit out/ HO New Store CAPEX Total Store

- 60. AGENDA TRADING UPDATE LEARNINGS DEEP DIVE: CUSTOMER PROPOSITION FINANCIAL UPDATE CONCLUSION / Q&A I. II. III.

- 61. CONCLUSION GUIDELINE: SUMMARY OF THE KEY MESSAGES TO KINGFISHER, state your key achievements again and your

- 62. Thank you ! Q&A

- 64. Скачать презентацию

AGENDA

TRADING UPDATE

LEARNINGS

DEEP DIVE: CUSTOMER PROPOSITION

CONCLUSION / Q&A

I.

II.

III.

IV.

AGENDA

TRADING UPDATE

LEARNINGS

DEEP DIVE: CUSTOMER PROPOSITION

CONCLUSION / Q&A

I.

II.

III.

IV.

SAMARA FIRST WEEKS OF TRADING UPDATE

First weeks sales:

Sales budget:

Sales % by

SAMARA FIRST WEEKS OF TRADING UPDATE

First weeks sales:

Sales budget:

Sales % by

MARKETING & CUSTOMER FEEDBACK

Store Launch- Marketing

Initial customer feedback

Quote customers: “XXXXX”

Quick feedback

MARKETING & CUSTOMER FEEDBACK

Store Launch- Marketing

Initial customer feedback

Quote customers: “XXXXX”

Quick feedback

TV COMMERCIAL

GUIDELINE: play video or other elements of the marketing campaign

TV COMMERCIAL

GUIDELINE: play video or other elements of the marketing campaign

ST PETERSBURG- NEXT OPENING

GUIDELINE: What went well in Samara? What

ST PETERSBURG- NEXT OPENING

GUIDELINE: What went well in Samara? What

AGENDA

TRADING UPDATE

LEARNINGS

DEEP DIVE: CUSTOMER PROPOSITION

CONCLUSION / Q&A

I.

II.

III.

IV.

GUIDELINE: Part II aims at

AGENDA

TRADING UPDATE

LEARNINGS

DEEP DIVE: CUSTOMER PROPOSITION

CONCLUSION / Q&A

I.

II.

III.

IV.

GUIDELINE: Part II aims at

Be #1 home improvement retailer in Russia by offering a wide

Be #1 home improvement retailer in Russia by offering a wide

STRATEGIC AGENDA

Development strategy

Site criteria

Store pipeline

STORE ROLL OUT

1

2

3

4

5

6

STORE PROPOSITION

OTHER

DEVELOP OUR PEOPLE

SCALABLE INFRASTRUCTURE

STRATEGIC AGENDA

Development strategy

Site criteria

Store pipeline

STORE ROLL OUT

1

2

3

4

5

6

STORE PROPOSITION

OTHER

DEVELOP OUR PEOPLE

SCALABLE INFRASTRUCTURE

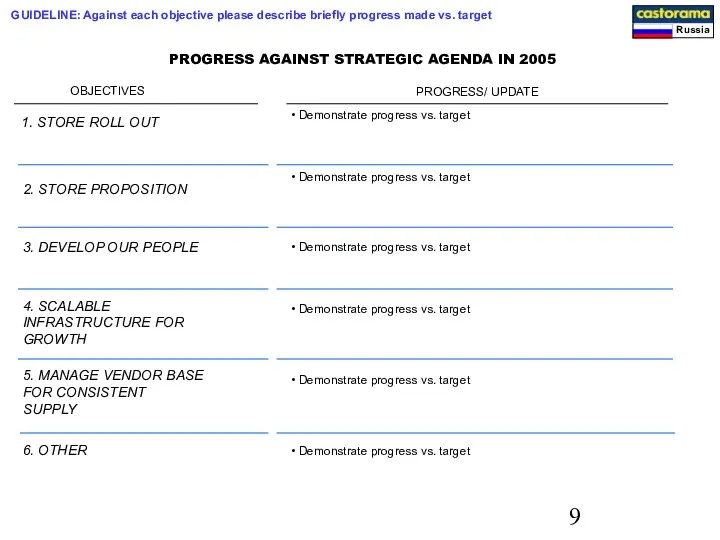

PROGRESS AGAINST STRATEGIC AGENDA IN 2005

OBJECTIVES

PROGRESS/ UPDATE

Demonstrate progress vs. target

1.

PROGRESS AGAINST STRATEGIC AGENDA IN 2005

OBJECTIVES

PROGRESS/ UPDATE

Demonstrate progress vs. target

1.

OBJECTIVE 1: STORE ROLL OUT KEY LEARNING

GUIDELINE: Explain your learning

OBJECTIVE 1: STORE ROLL OUT KEY LEARNING

GUIDELINE: Explain your learning

OBJECTIVE 2: STORE PROPOSITION KEY LEARNING

GUIDELINE: Store blue print, key elements

OBJECTIVE 2: STORE PROPOSITION KEY LEARNING

GUIDELINE: Store blue print, key elements

OBJECTIVE 3: DEVELOP OUR PEOPLE KEY LEARNING

GUIDELINE: Key learning related to

OBJECTIVE 3: DEVELOP OUR PEOPLE KEY LEARNING

GUIDELINE: Key learning related to

OBJECTIVE 4: INFRASTRUCTURE KEY LEARNING

I -

GUIDELINE: Learning related to

OBJECTIVE 4: INFRASTRUCTURE KEY LEARNING

I -

GUIDELINE: Learning related to

OBJECTIVE 5: VENDOR BASE KEY LEARNING

GUIDELINE: Learning related to vendor,

OBJECTIVE 5: VENDOR BASE KEY LEARNING

GUIDELINE: Learning related to vendor,

OBJECTIVE 6: OTHER STRATEGIC OBJECTIVE’S KEY LEARNING

GUIDELINE: Others

OBJECTIVE 6: OTHER STRATEGIC OBJECTIVE’S KEY LEARNING

GUIDELINE: Others

SUMMARY OF KEY ACHIEVEMENTS: 2005

XX sites identified and XX Capex approved

SUMMARY OF KEY ACHIEVEMENTS: 2005

XX sites identified and XX Capex approved

SUMMARY OF KEY CHALLENGES: 2005

Sourcing and KAL?

People development, recruitment? Skills? Facilities?

Competition

SUMMARY OF KEY CHALLENGES: 2005

Sourcing and KAL?

People development, recruitment? Skills? Facilities?

Competition

AGENDA

TRADING UPDATE

LEARNINGS

DEEP DIVE: CUSTOMER PROPOSITION

1. CUSTOMER

2. COMPETITION

3. STORE FORMAT

4. COMMERCIAL

AGENDA

TRADING UPDATE

LEARNINGS

DEEP DIVE: CUSTOMER PROPOSITION

1. CUSTOMER

2. COMPETITION

3. STORE FORMAT

4. COMMERCIAL

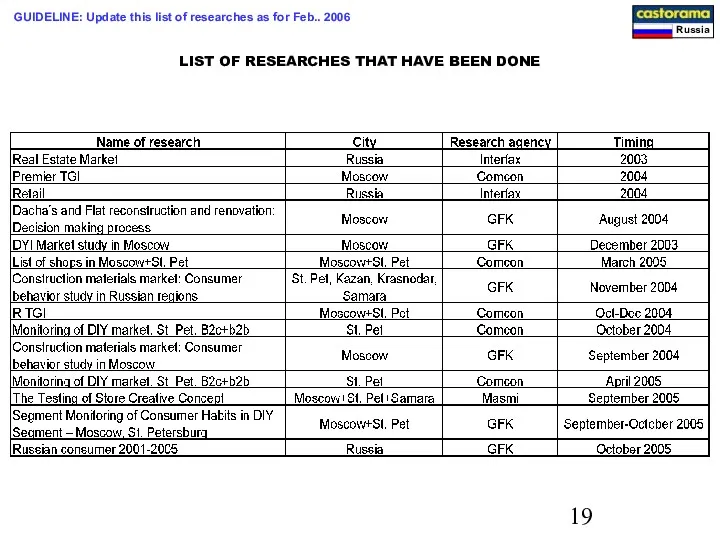

LIST OF RESEARCHES THAT HAVE BEEN DONE

GUIDELINE: Update this list of

LIST OF RESEARCHES THAT HAVE BEEN DONE

GUIDELINE: Update this list of

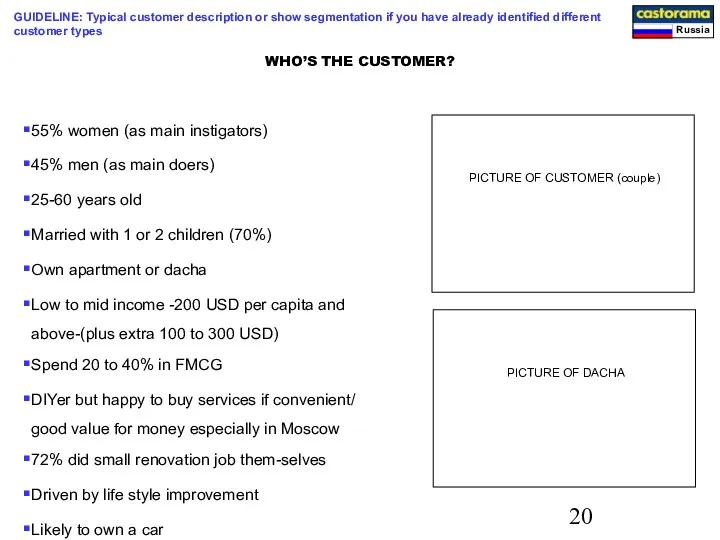

55% women (as main instigators)

45% men (as main doers)

25-60 years old

55% women (as main instigators)

45% men (as main doers)

25-60 years old

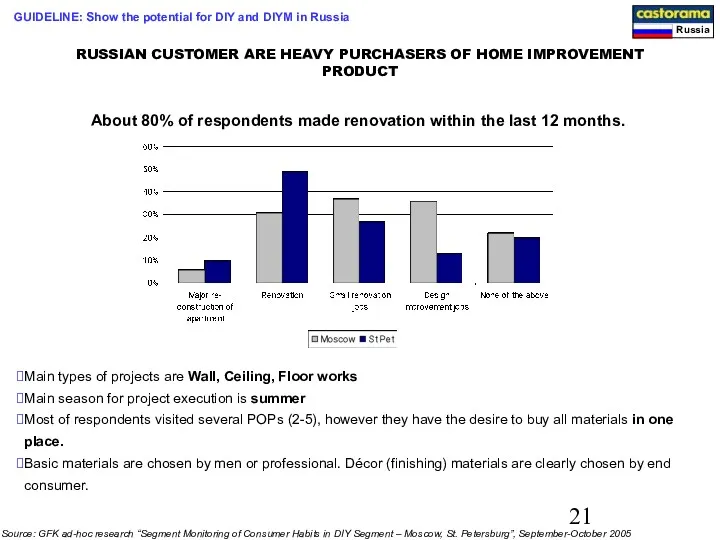

RUSSIAN CUSTOMER ARE HEAVY PURCHASERS OF HOME IMPROVEMENT PRODUCT

About 80%

RUSSIAN CUSTOMER ARE HEAVY PURCHASERS OF HOME IMPROVEMENT PRODUCT

About 80%

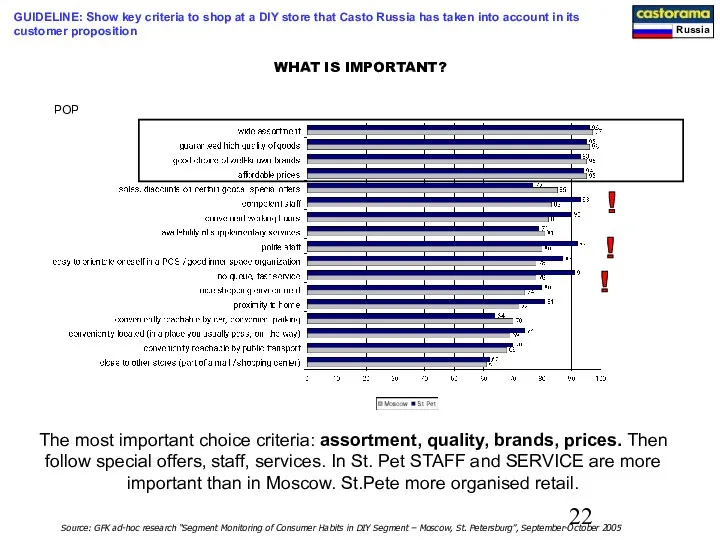

!

!

!

The most important choice criteria: assortment, quality, brands, prices. Then follow

!

!

!

The most important choice criteria: assortment, quality, brands, prices. Then follow

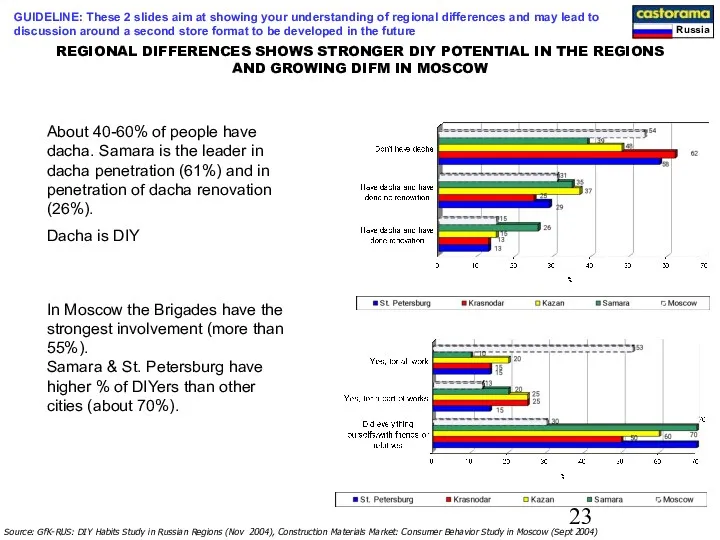

REGIONAL DIFFERENCES SHOWS STRONGER DIY POTENTIAL IN THE REGIONS AND GROWING

REGIONAL DIFFERENCES SHOWS STRONGER DIY POTENTIAL IN THE REGIONS AND GROWING

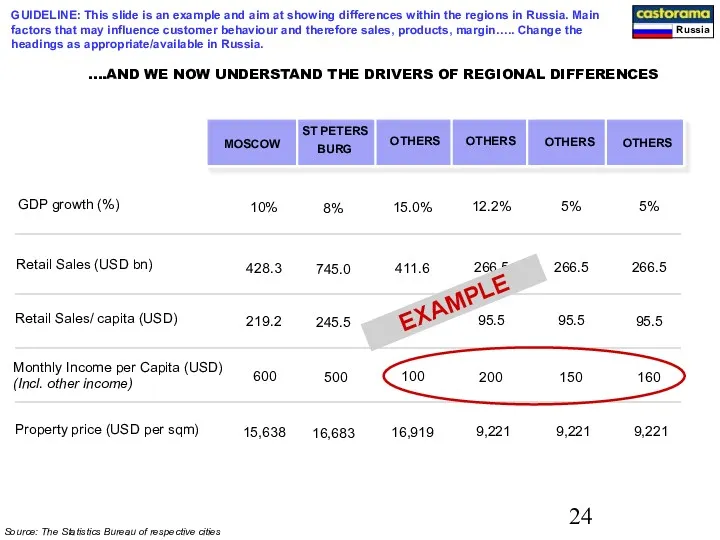

….AND WE NOW UNDERSTAND THE DRIVERS OF REGIONAL DIFFERENCES

Source: The Statistics

….AND WE NOW UNDERSTAND THE DRIVERS OF REGIONAL DIFFERENCES

Source: The Statistics

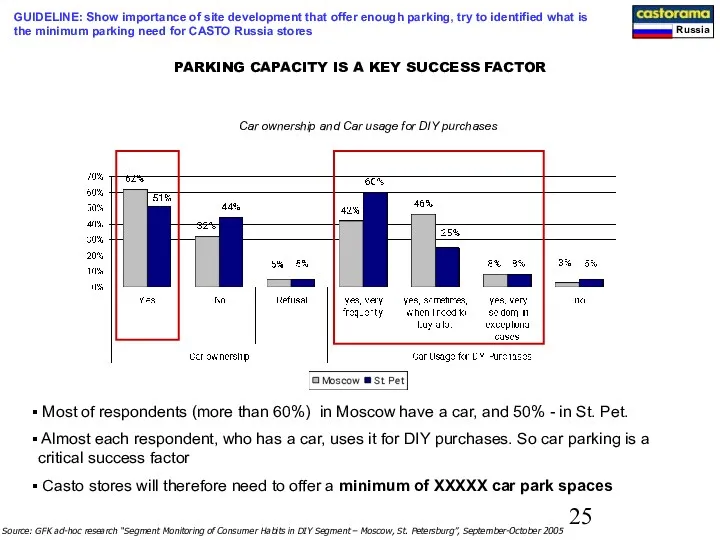

Car ownership and Car usage for DIY purchases

Most of respondents

Car ownership and Car usage for DIY purchases

Most of respondents

MARKET RESEARCH PROGRAMME IS IN PLACE TO KEEP LEARNING ABOUT CUSTOMERS

Reality

Customer

MARKET RESEARCH PROGRAMME IS IN PLACE TO KEEP LEARNING ABOUT CUSTOMERS

Reality

Customer

AGENDA

TRADING UPDATE

LEARNINGS

DEEP DIVE: CUSTOMER PROPOSITION

1. CUSTOMER

2. COMPETITION

3. STORE FORMAT

4. COMMERCIAL

AGENDA

TRADING UPDATE

LEARNINGS

DEEP DIVE: CUSTOMER PROPOSITION

1. CUSTOMER

2. COMPETITION

3. STORE FORMAT

4. COMMERCIAL

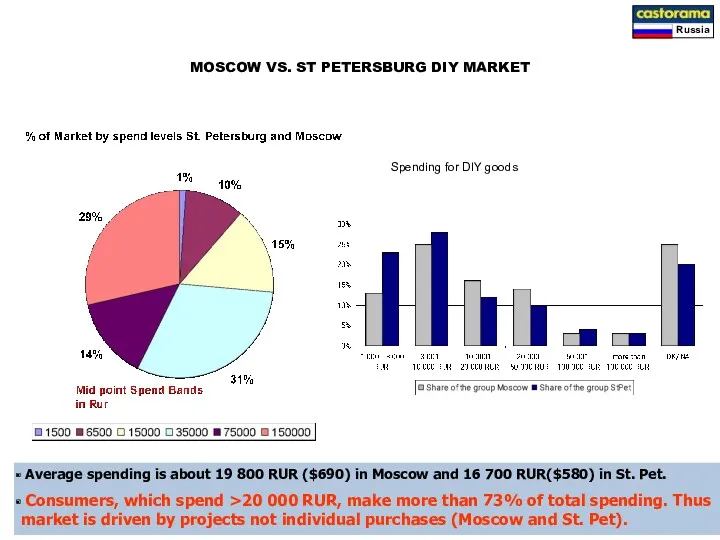

MOSCOW VS. ST PETERSBURG DIY MARKET

Spending for DIY goods

Average spending

MOSCOW VS. ST PETERSBURG DIY MARKET

Spending for DIY goods

Average spending

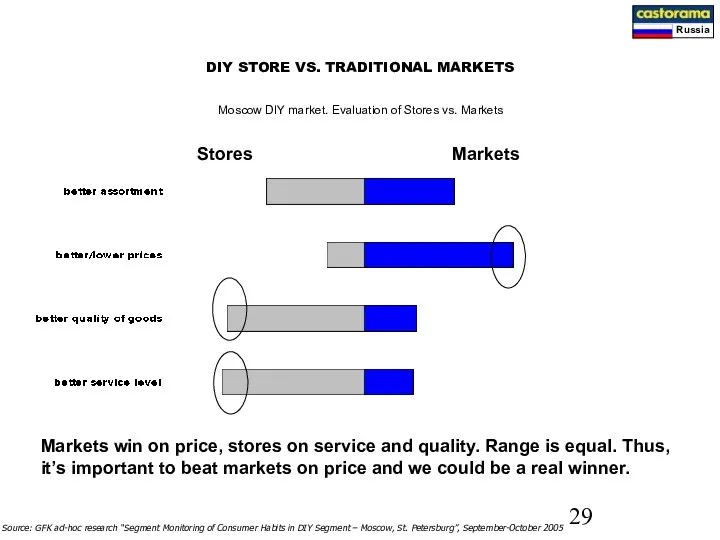

Moscow DIY market. Evaluation of Stores vs. Markets

Stores

Markets

Markets win on price,

Moscow DIY market. Evaluation of Stores vs. Markets

Stores

Markets

Markets win on price,

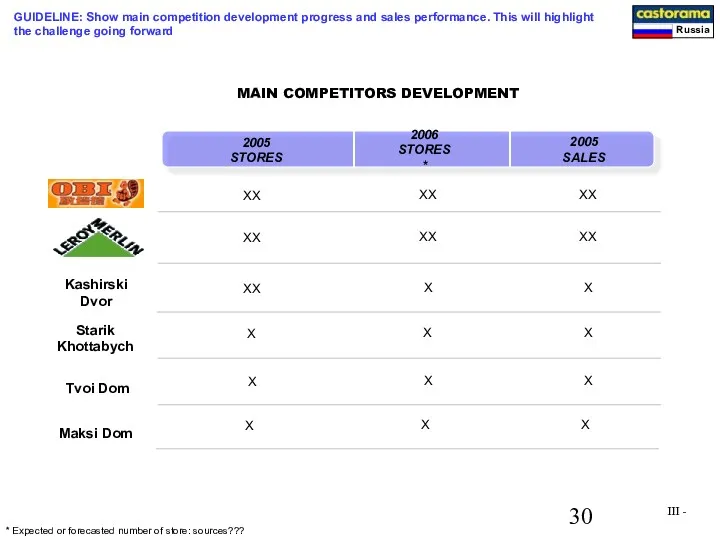

MAIN COMPETITORS DEVELOPMENT

2006

STORES*

2005

STORES

2005 SALES

XX

XX

X

X

XX

XX

X

X

X

XX

XX

X

X

X

XX

III -

Kashirski Dvor

Starik Khottabych

Tvoi Dom

Maksi Dom

X

X

X

*

MAIN COMPETITORS DEVELOPMENT

2006

STORES*

2005

STORES

2005 SALES

XX

XX

X

X

XX

XX

X

X

X

XX

XX

X

X

X

XX

III -

Kashirski Dvor

Starik Khottabych

Tvoi Dom

Maksi Dom

X

X

X

*

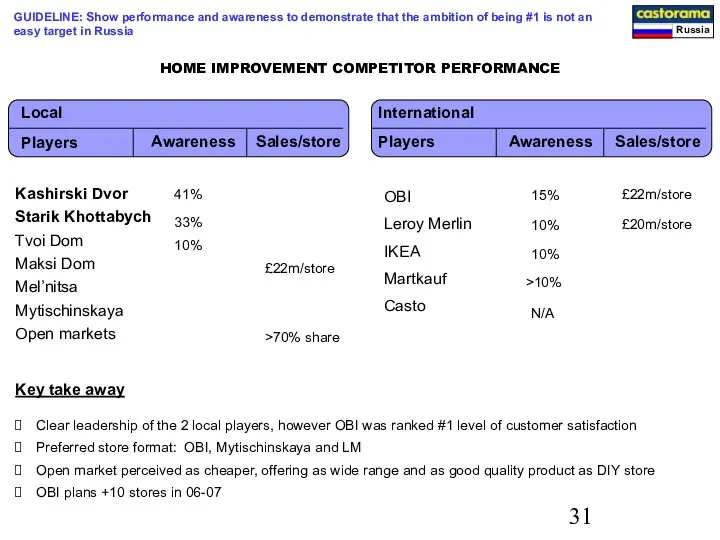

HOME IMPROVEMENT COMPETITOR PERFORMANCE

Local

International

Kashirski Dvor

Starik Khottabych

Tvoi Dom

Maksi Dom

Mel’nitsa

Mytischinskaya

Open

HOME IMPROVEMENT COMPETITOR PERFORMANCE

Local

International

Kashirski Dvor

Starik Khottabych

Tvoi Dom

Maksi Dom

Mel’nitsa

Mytischinskaya

Open

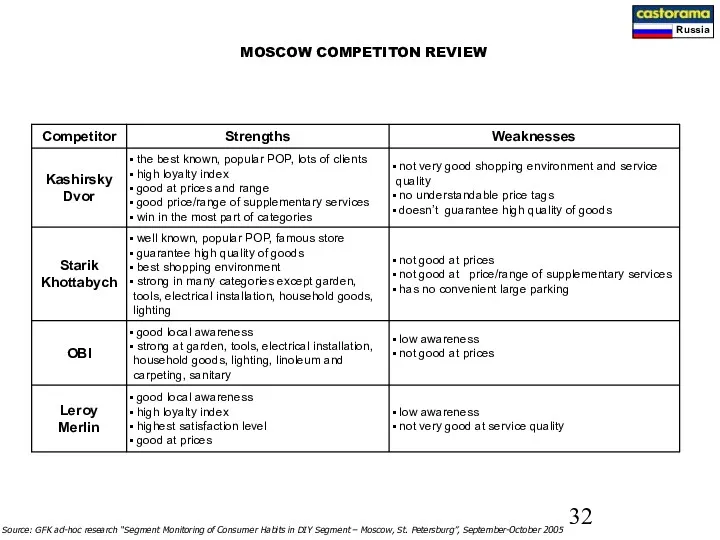

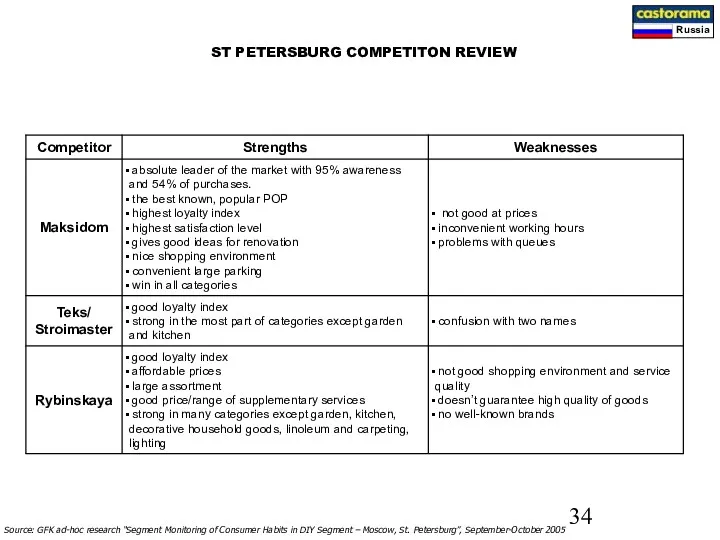

MOSCOW COMPETITON REVIEW

Source: GFK ad-hoc research “Segment Monitoring of Consumer Habits

MOSCOW COMPETITON REVIEW

Source: GFK ad-hoc research “Segment Monitoring of Consumer Habits

MOSCOW COMPETITON MAP

Insert map of Moscow competition and stores under construction

MOSCOW COMPETITON MAP

Insert map of Moscow competition and stores under construction

Source: GFK ad-hoc research “Segment Monitoring of Consumer Habits in DIY

Source: GFK ad-hoc research “Segment Monitoring of Consumer Habits in DIY

ST PETERSBURG COMPETITON MAP

Insert map of St Petersburg competition and stores

ST PETERSBURG COMPETITON MAP

Insert map of St Petersburg competition and stores

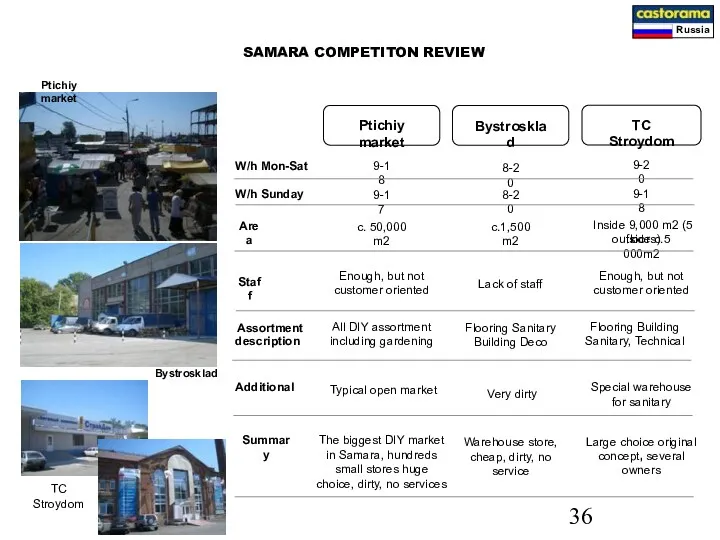

SAMARA COMPETITON REVIEW

W/h Mon-Sat

W/h Sunday

Area

Staff

Assortment

description

Additional

Summary

Bystrosklad

Ptichiy market

TC Stroydom

Inside 9,000 m2 (5

SAMARA COMPETITON REVIEW

W/h Mon-Sat

W/h Sunday

Area

Staff

Assortment

description

Additional

Summary

Bystrosklad

Ptichiy market

TC Stroydom

Inside 9,000 m2 (5

AGENDA

TRADING UPDATE

LEARNINGS

DEEP DIVE: CUSTOMER PROPOSITION

1. CUSTOMER

2. COMPETITION

3. STORE FORMAT

4. COMMERCIAL

AGENDA

TRADING UPDATE

LEARNINGS

DEEP DIVE: CUSTOMER PROPOSITION

1. CUSTOMER

2. COMPETITION

3. STORE FORMAT

4. COMMERCIAL

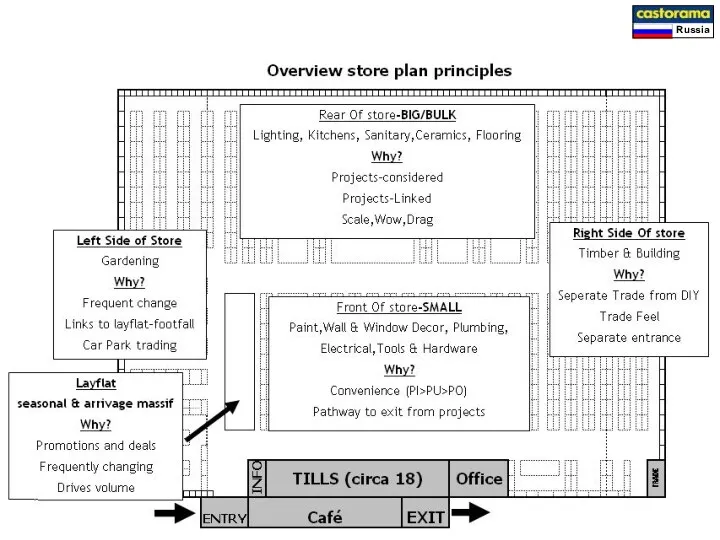

Work to date- Strategic

Leading/Famous for gardening in the regions

Strong décor offer-softer

Work to date- Strategic

Leading/Famous for gardening in the regions

Strong décor offer-softer

Just Stock

Just Stock

Educate

STORE LOOK

Show me

Choice

Just Stock

Just Stock

Educate

STORE LOOK

Show me

Choice

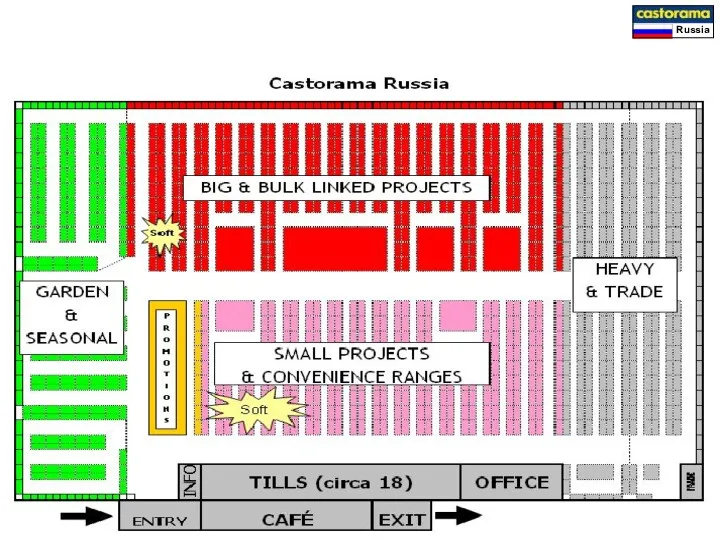

STORE LOOK

Pallet replenishment

How to display, touch and feel & SRP

“Stock to

STORE LOOK

Pallet replenishment

How to display, touch and feel & SRP

“Stock to

High Level display, easy to change, stock below

“Stock to go”

Flooring- Bigger

High Level display, easy to change, stock below

“Stock to go”

Flooring- Bigger

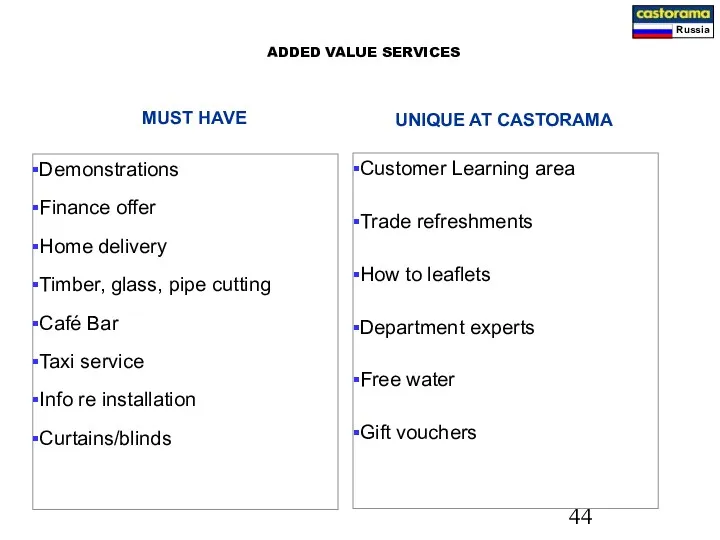

Demonstrations

Finance offer

Home delivery

Timber, glass, pipe cutting

Café Bar

Taxi service

Info re installation

Curtains/blinds

Customer

Demonstrations

Finance offer

Home delivery

Timber, glass, pipe cutting

Café Bar

Taxi service

Info re installation

Curtains/blinds

Customer

AGENDA

TRADING UPDATE

LEARNINGS

DEEP DIVE: CUSTOMER PROPOSITION

1. CUSTOMER

2. COMPETITION

3. STORE FORMAT

4. COMMERCIAL

AGENDA

TRADING UPDATE

LEARNINGS

DEEP DIVE: CUSTOMER PROPOSITION

1. CUSTOMER

2. COMPETITION

3. STORE FORMAT

4. COMMERCIAL

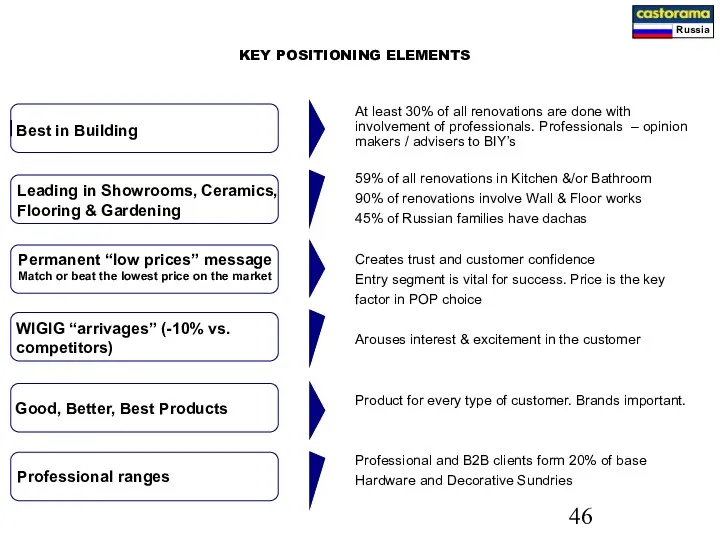

KEY POSITIONING ELEMENTS

At least 30% of all renovations are done with

KEY POSITIONING ELEMENTS

At least 30% of all renovations are done with

Objective:

Forms a guide for sales

forecasts & contract

signing

Result:

Contracts agreed with

Objective:

Forms a guide for sales

forecasts & contract

signing

Result:

Contracts agreed with

DRIVE SALES AND CUSTOMER PRICE PERCEPTION

Mid Ends - 50 Promotional Arrivages

DRIVE SALES AND CUSTOMER PRICE PERCEPTION

Mid Ends - 50 Promotional Arrivages

CASTORAMA PROMOTION CALENDAR 2006

Maintenance advertising campaign will be built on 4

CASTORAMA PROMOTION CALENDAR 2006

Maintenance advertising campaign will be built on 4

375 Suppliers – 365 signed contracts

10% Suppliers – Nationwide Service

40% of

375 Suppliers – 365 signed contracts

10% Suppliers – Nationwide Service

40% of

AGENDA

TRADING UPDATE

LEARNINGS

DEEP DIVE: CUSTOMER PROPOSITION

1. CUSTOMER

2. COMPETITION

3. STORE FORMAT

4. COMMERCIAL

AGENDA

TRADING UPDATE

LEARNINGS

DEEP DIVE: CUSTOMER PROPOSITION

1. CUSTOMER

2. COMPETITION

3. STORE FORMAT

4. COMMERCIAL

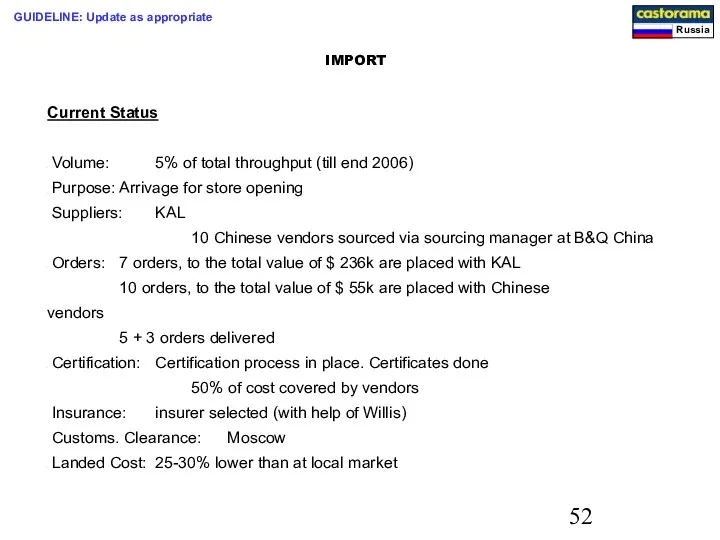

IMPORT

Current Status

Volume: 5% of total throughput (till end 2006)

Purpose: Arrivage for

IMPORT

Current Status

Volume: 5% of total throughput (till end 2006)

Purpose: Arrivage for

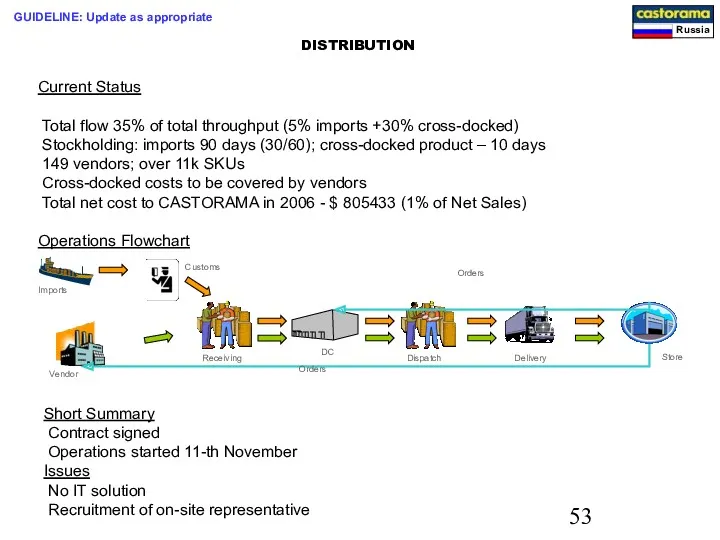

DISTRIBUTION

Current Status

Total flow 35% of total throughput (5% imports +30%

DISTRIBUTION

Current Status

Total flow 35% of total throughput (5% imports +30%

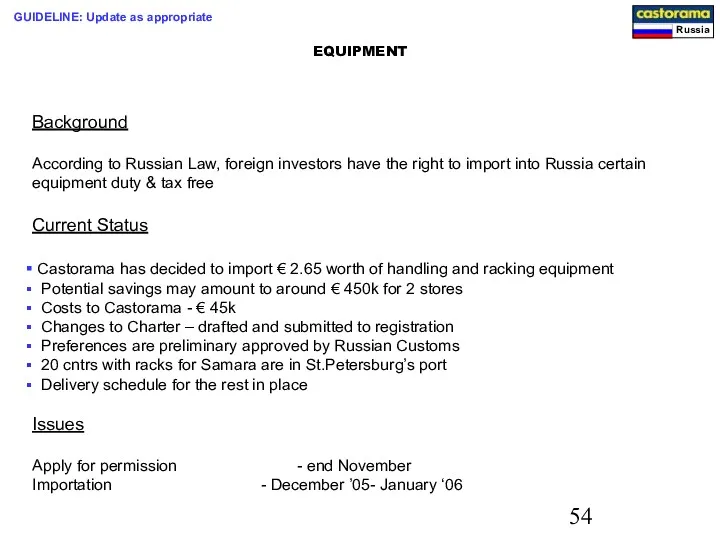

EQUIPMENT

Background

According to Russian Law, foreign investors have the right to import

EQUIPMENT

Background

According to Russian Law, foreign investors have the right to import

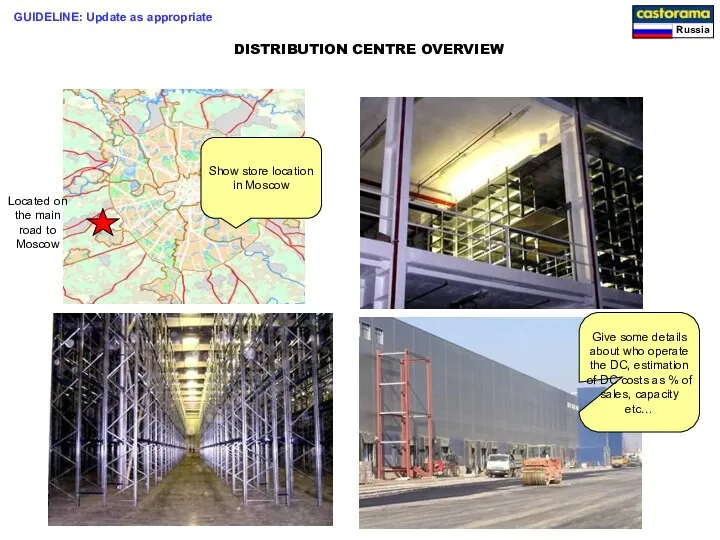

DISTRIBUTION CENTRE OVERVIEW

Located on the main road to Moscow

GUIDELINE: Update as

DISTRIBUTION CENTRE OVERVIEW

Located on the main road to Moscow

GUIDELINE: Update as

AGENDA

TRADING UPDATE

LEARNINGS

DEEP DIVE: CUSTOMER PROPOSITION

FINANCIAL UPDATE

CONCLUSION / Q&A

I.

II.

III.

IV

V.

GUIDELINE: Quick review of

AGENDA

TRADING UPDATE

LEARNINGS

DEEP DIVE: CUSTOMER PROPOSITION

FINANCIAL UPDATE

CONCLUSION / Q&A

I.

II.

III.

IV

V.

GUIDELINE: Quick review of

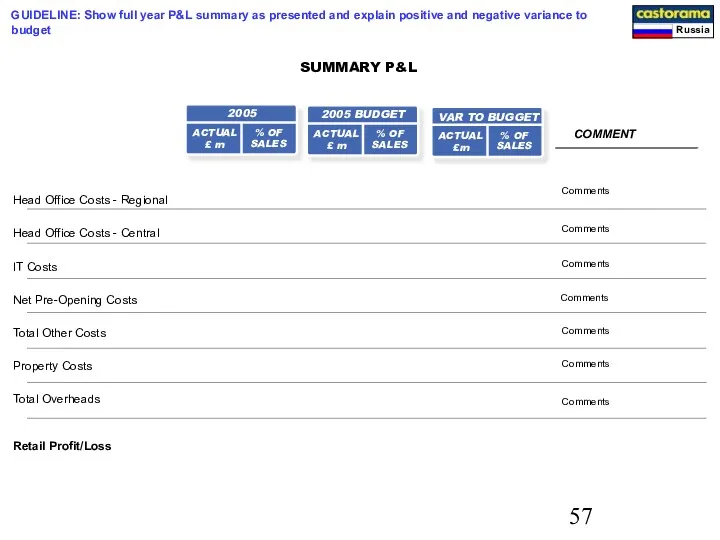

SUMMARY P&L

COMMENT

2005

ACTUAL

£ m

% OF SALES

Comments

Comments

Comments

Comments

Comments

VAR TO BUGGET

ACTUAL

£m

% OF SALES

2005 BUDGET

ACTUAL

£ m

%

SUMMARY P&L

COMMENT

2005

ACTUAL

£ m

% OF SALES

Comments

Comments

Comments

Comments

Comments

VAR TO BUGGET

ACTUAL

£m

% OF SALES

2005 BUDGET

ACTUAL

£ m

%

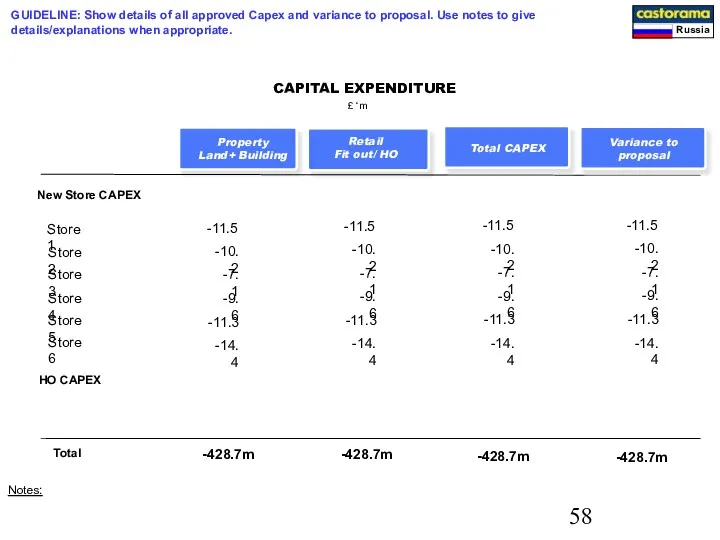

CAPITAL EXPENDITURE

£ ‘m

Property

Land+ Building

Retail

Fit out/ HO

New Store CAPEX

Total

Store 2

-10.2

Store 3

-7.1

Store

CAPITAL EXPENDITURE

£ ‘m

Property

Land+ Building

Retail

Fit out/ HO

New Store CAPEX

Total

Store 2

-10.2

Store 3

-7.1

Store

AGENDA

TRADING UPDATE

LEARNINGS

DEEP DIVE: CUSTOMER PROPOSITION

FINANCIAL UPDATE

CONCLUSION / Q&A

I.

II.

III.

IV

V.

AGENDA

TRADING UPDATE

LEARNINGS

DEEP DIVE: CUSTOMER PROPOSITION

FINANCIAL UPDATE

CONCLUSION / Q&A

I.

II.

III.

IV

V.

CONCLUSION

GUIDELINE: SUMMARY OF THE KEY MESSAGES TO KINGFISHER, state your key

CONCLUSION

GUIDELINE: SUMMARY OF THE KEY MESSAGES TO KINGFISHER, state your key

Thank you !

Q&A

Thank you !

Q&A

Современный рынок наружной (outdoor) рекламы в России и мире

Современный рынок наружной (outdoor) рекламы в России и мире Знаки соответствия и обращения на рынке

Знаки соответствия и обращения на рынке Производственно-торговая компания БЕЛАНД

Производственно-торговая компания БЕЛАНД Передова мережа станцій оренди павербанків

Передова мережа станцій оренди павербанків Стандарты работы персонала автоцентров холдинга

Стандарты работы персонала автоцентров холдинга Удачников для успешного хозяйства

Удачников для успешного хозяйства Компания АВК-технология

Компания АВК-технология Маркетинговое исследование для компании ABBYY

Маркетинговое исследование для компании ABBYY Проведение рекламной акции Подарок при покупке контактных линз Acuvue

Проведение рекламной акции Подарок при покупке контактных линз Acuvue Основные элементы комплекса интернет-маркетинга

Основные элементы комплекса интернет-маркетинга Производственная стратегия предприятия

Производственная стратегия предприятия Мастер-группа Бизнес-Эксперт. Программы лояльности

Мастер-группа Бизнес-Эксперт. Программы лояльности Осенние новинки

Осенние новинки Брендинг. Как построить эффективный бренд. Текущий аудит бренда

Брендинг. Как построить эффективный бренд. Текущий аудит бренда Коммерческая недвижимость. ЖК Жемчужина

Коммерческая недвижимость. ЖК Жемчужина Implementing Marketing Plans

Implementing Marketing Plans Система продвижения компании на рынке брокерских услуг на примере компании Открытие Брокер

Система продвижения компании на рынке брокерских услуг на примере компании Открытие Брокер Секреты Здоровья, Молодости, Красоты и Долголетия!

Секреты Здоровья, Молодости, Красоты и Долголетия! Структура ринку засобів розміщення в Україні та за кордоном

Структура ринку засобів розміщення в Україні та за кордоном Россия и Индия: Экономико-статистический анализ внешней торговли товарами

Россия и Индия: Экономико-статистический анализ внешней торговли товарами Международная реклама

Международная реклама Ваш успешный праздник

Ваш успешный праздник Концепции маркетинга

Концепции маркетинга Позиционирование. Тема 5

Позиционирование. Тема 5 Безопасное и эффективное использование TRX Suspension Training

Безопасное и эффективное использование TRX Suspension Training Макет сайта и как примерно должен выглядеть сайт по проведению розыгрышей товаров

Макет сайта и как примерно должен выглядеть сайт по проведению розыгрышей товаров Маркетинг – философия современного бизнеса

Маркетинг – философия современного бизнеса Goodwill. Interactive Depression Storytelling App

Goodwill. Interactive Depression Storytelling App