- Strategy and Analysis in Using Net Present Value. Decision Trees

Содержание

- 2. Chapter Outline 8.1 Decision Trees 8.2 Sensitivity Analysis, Scenario Analysis, and Break-Even Analysis 8.3 Monte Carlo

- 3. 8.1 Decision Trees Allow us to graphically represent the alternatives available to us in each period

- 4. Example of Decision Tree Do not study Study finance Squares represent decisions to be made. Circles

- 5. Stewart Pharmaceuticals The Stewart Pharmaceuticals Corporation is considering investing in developing a drug that cures the

- 6. Stewart Pharmaceuticals NPV of Full-Scale Production following Successful Test Note that the NPV is calculated as

- 7. Stewart Pharmaceuticals NPV of Full-Scale Production following Unsuccessful Test Note that the NPV is calculated as

- 8. Decision Tree for Stewart Pharmaceutical Do not test Test Failure Success Do not invest Invest The

- 9. Stewart Pharmaceutical: Decision to Test Let’s move back to the first stage, where the decision boils

- 10. 8.3 Sensitivity Analysis, Scenario Analysis, and Break-Even Analysis Allows us to look the behind the NPV

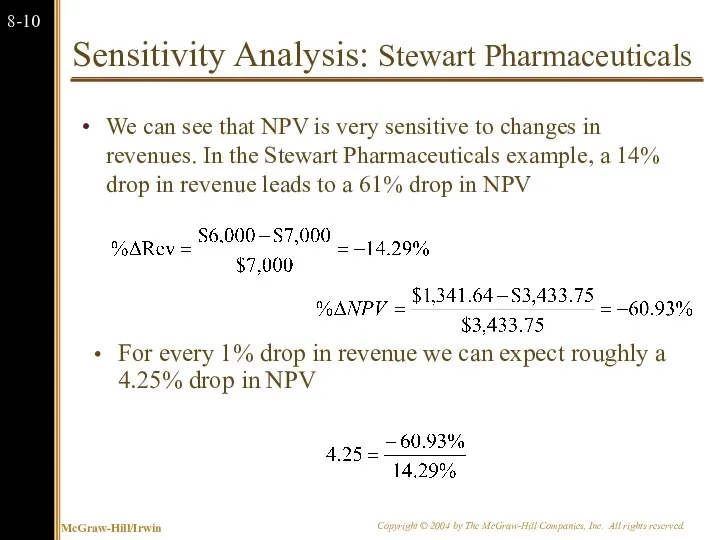

- 11. Sensitivity Analysis: Stewart Pharmaceuticals We can see that NPV is very sensitive to changes in revenues.

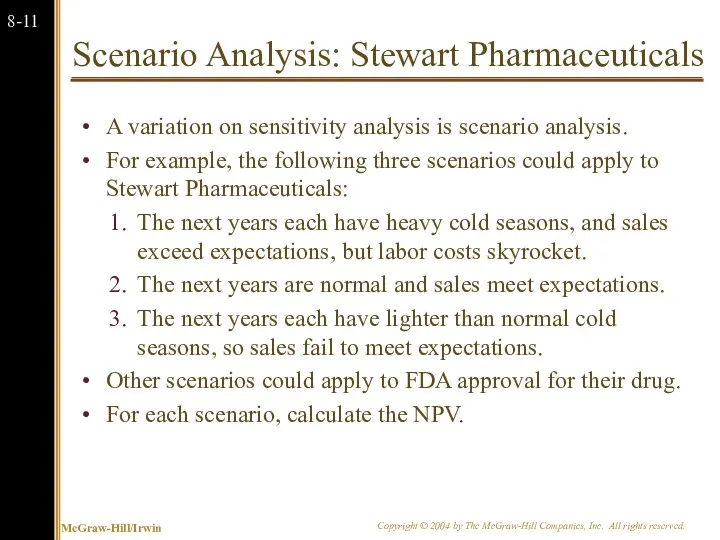

- 12. Scenario Analysis: Stewart Pharmaceuticals A variation on sensitivity analysis is scenario analysis. For example, the following

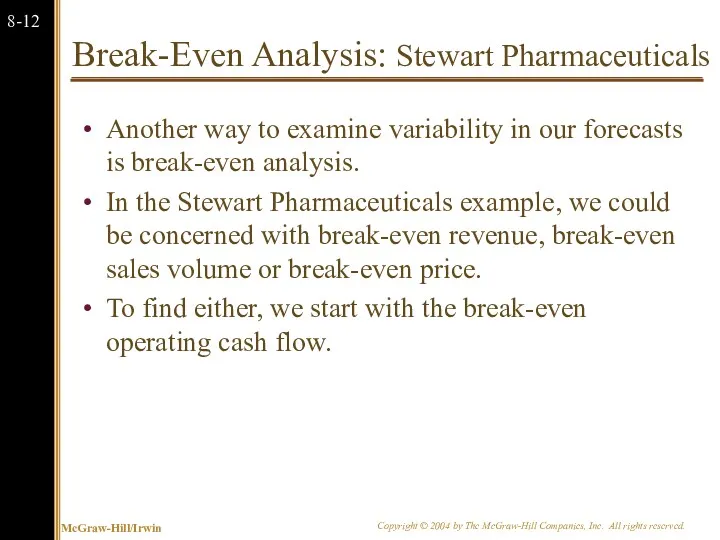

- 13. Break-Even Analysis: Stewart Pharmaceuticals Another way to examine variability in our forecasts is break-even analysis. In

- 14. Break-Even Analysis: Stewart Pharmaceuticals The project requires an investment of $1,600. In order to cover our

- 15. Break-Even Revenue Stewart Pharmaceuticals Work backwards from OCFBE to Break-Even Revenue Revenue $5,358.72 Variable cost $3,000

- 16. Break-Even Analysis: PBE Now that we have break-even revenue as $5,358.72 million we can calculate break-even

- 17. Break-Even Analysis: Dorm Beds Recall the “Dorm beds” example from the previous chapter. We could be

- 18. Dorm Beds Example Consider a project to supply the University of Missouri with 10,000 dormitory beds

- 19. Dorm Beds Example The project will last for 3 years. Annual fixed costs will be $25,000

- 20. Dorm Beds OCF0 What is the OCF in year zero for this project? Cost of New

- 21. Dorm Beds OCF1,2 What is the OCF in years 1 and 2 for this project? Revenue

- 22. Dorm Beds OCF3 We get our $10,000 NWC back and sell the equipment. The after-tax salvage

- 23. Dorm Beds “Base-Case” NPV First, set your calculator to 1 payment per year. Then, use the

- 24. Dorm Beds Break-Even Analysis In this example, we should be concerned with break-even price. Let’s start

- 25. Dorm Beds Break-Even Analysis The PV of the cost of this project is the sum of

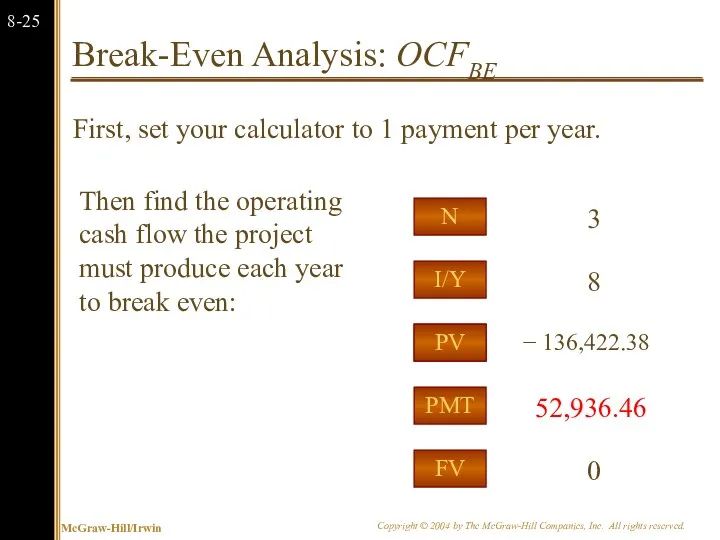

- 26. Break-Even Analysis: OCFBE First, set your calculator to 1 payment per year. PMT I/Y FV PV

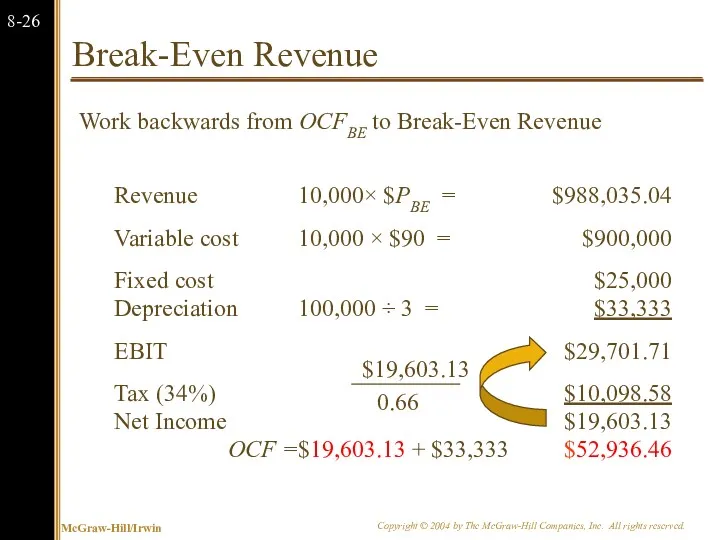

- 27. Break-Even Revenue Work backwards from OCFBE to Break-Even Revenue Revenue 10,000× $PBE = $988,035.04 Variable cost

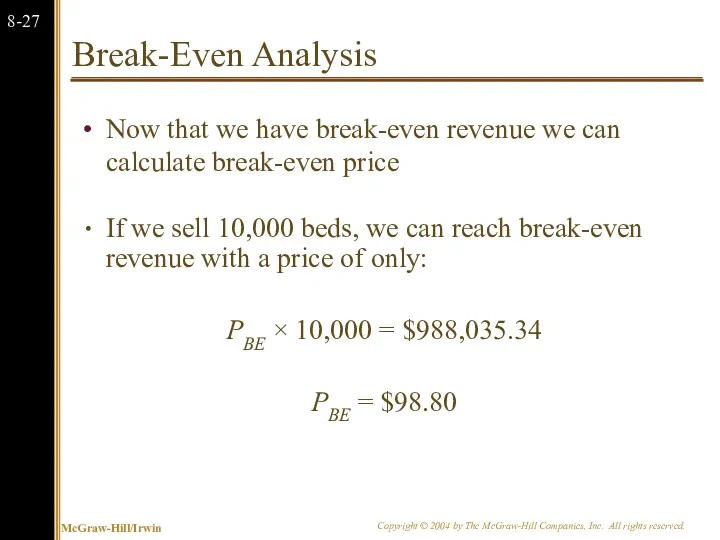

- 28. Break-Even Analysis Now that we have break-even revenue we can calculate break-even price If we sell

- 29. Common Mistake in Break-Even What’s wrong with this line of reasoning? With a price of $200

- 30. Don’t Forget that Variable Cost Varies Revenue QBE × $200 = $88,035.04 + QBE× $110 Variable

- 31. Break-Even Analysis With a contribution margin of $110 per bed, we can reach break-even revenue with

- 32. Break-Even Lease Payment Joe Machens is contemplating leasing the University of Missouri a fleet of 10

- 33. Break-Even Lease Payment: Depreciation Let’s cash flow this out from Joe’s perspective. The operating cash flow

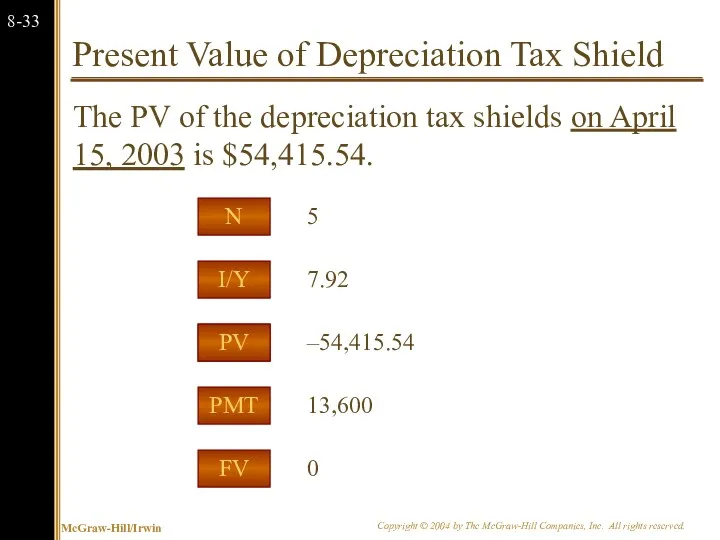

- 34. Present Value of Depreciation Tax Shield The PV of the depreciation tax shields on April 15,

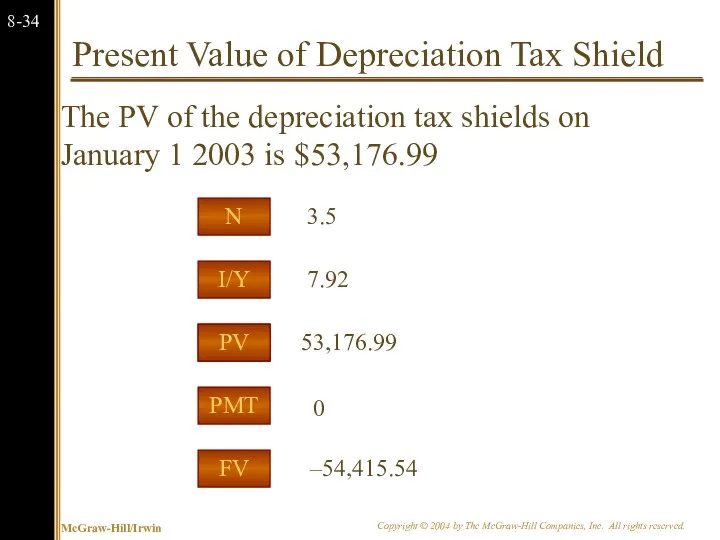

- 35. Present Value of Depreciation Tax Shield The PV of the depreciation tax shields on January 1

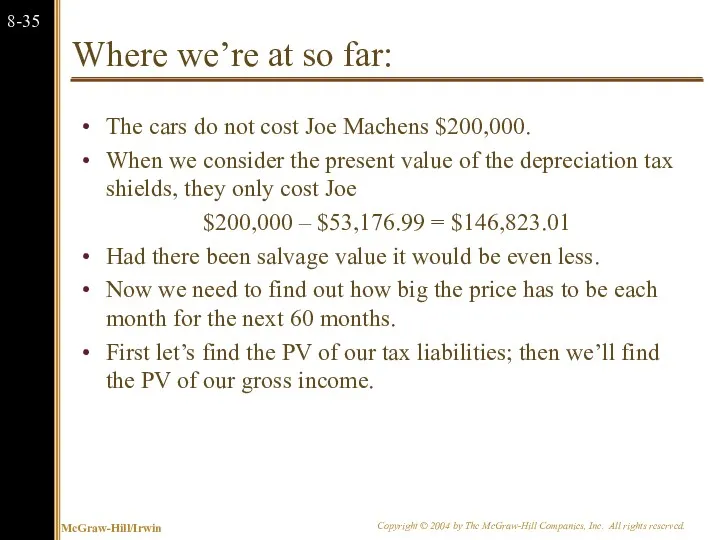

- 36. Where we’re at so far: The cars do not cost Joe Machens $200,000. When we consider

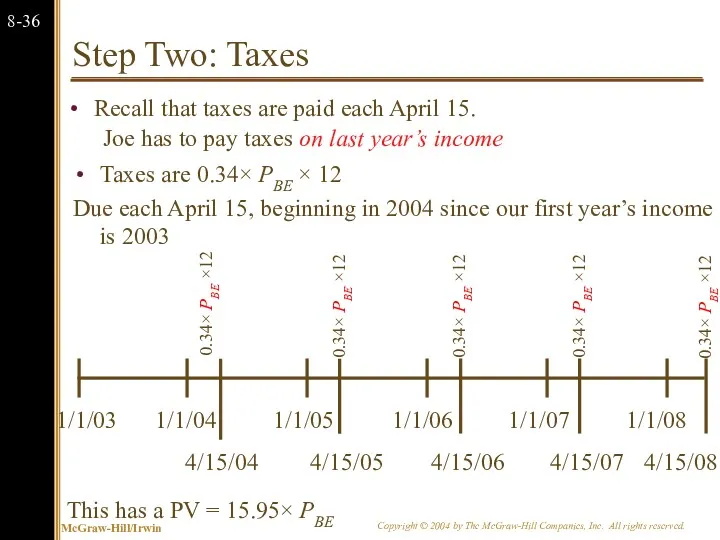

- 37. Step Two: Taxes Joe has to pay taxes on last year’s income 1/1/03 1/1/04 1/1/05 1/1/06

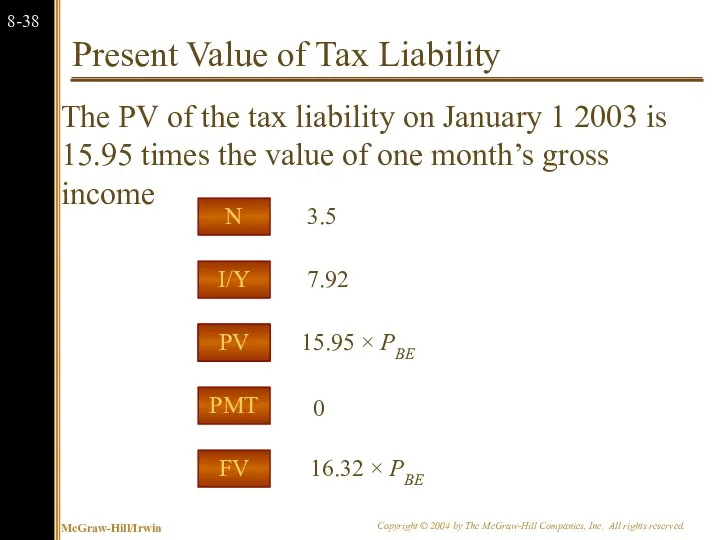

- 38. Present Value of Tax Liability The PV of the tax liability is 16.32 times one month’s

- 39. Present Value of Tax Liability The PV of the tax liability on January 1 2003 is

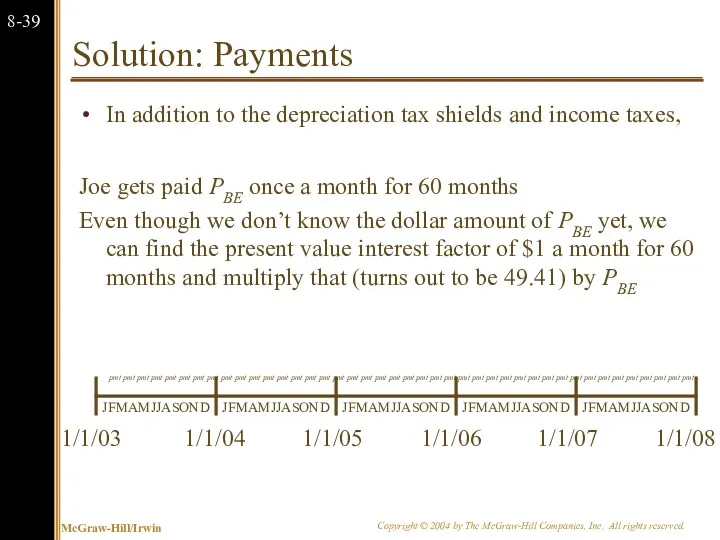

- 40. Solution: Payments In addition to the depreciation tax shields and income taxes, Joe gets paid PBE

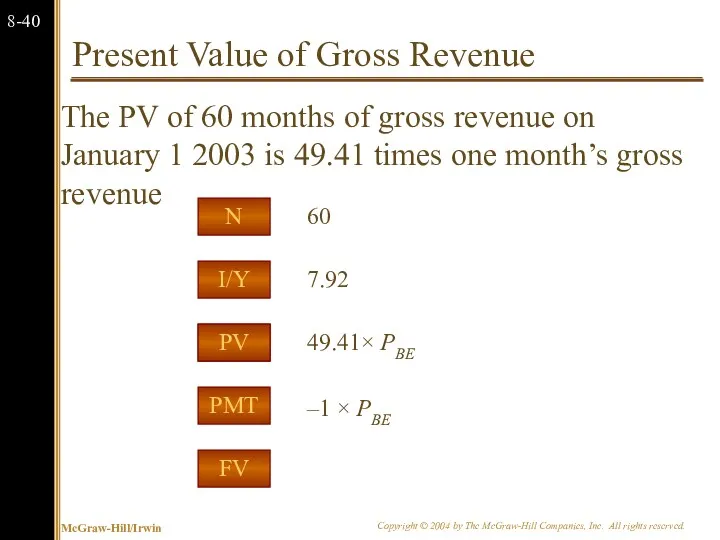

- 41. Present Value of Gross Revenue The PV of 60 months of gross revenue on January 1

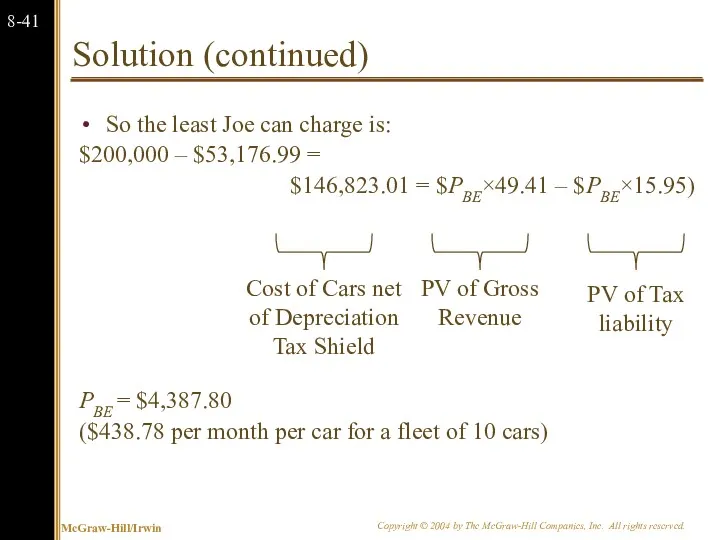

- 42. Solution (continued) So the least Joe can charge is: $200,000 – $53,176.99 = $146,823.01 = $PBE×49.41

- 43. Summary Joe Machens This problem was a bit more complicated than previous problems because of the

- 44. 8.3 Monte Carlo Simulation Monte Carlo simulation is a further attempt to model real-world uncertainty. This

- 45. 8.3 Monte Carlo Simulation Imagine a serious blackjack player who wants to know if he should

- 46. 8.3 Monte Carlo Simulation Monte Carlo simulation of capital budgeting projects is often viewed as a

- 47. 8.4 Options One of the fundamental insights of modern finance theory is that options have value.

- 48. Options The Option to Expand Has value if demand turns out to be higher than expected.

- 49. The Option to Expand Imagine a start-up firm, Campusteria, Inc. which plans to open private (for-profit)

- 50. Campusteria pro forma Income Statement We plan to sell 25 meal plans at $200 per month

- 51. The Option to Expand: Valuing a Start-Up Note that while the Campusteria test site has a

- 52. Discounted Cash Flows and Options We can calculate the market value of a project as the

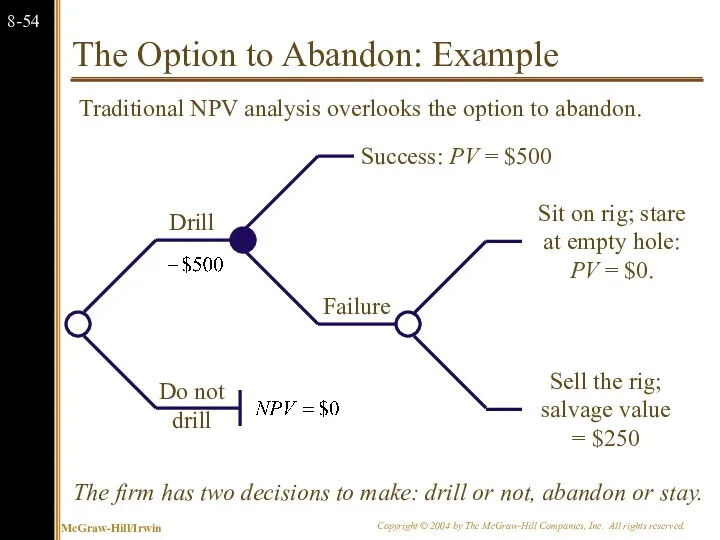

- 53. The Option to Abandon: Example Suppose that we are drilling an oil well. The drilling rig

- 54. The Option to Abandon: Example Traditional NPV analysis would indicate rejection of the project.

- 55. The Option to Abandon: Example The firm has two decisions to make: drill or not, abandon

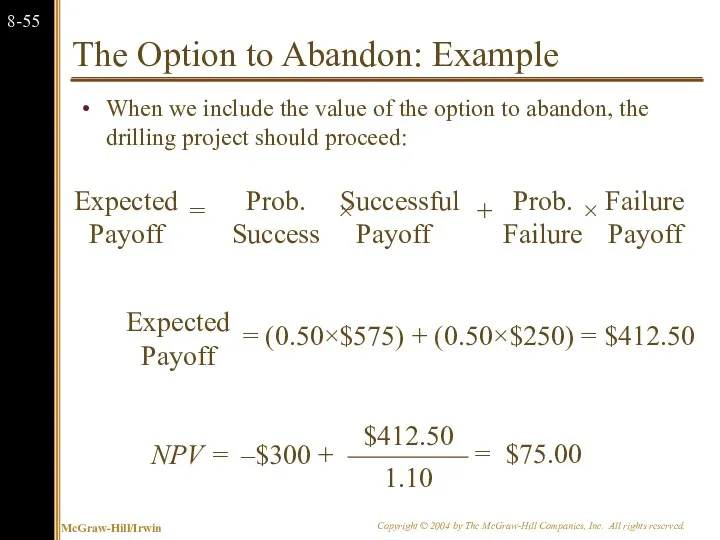

- 56. The Option to Abandon: Example When we include the value of the option to abandon, the

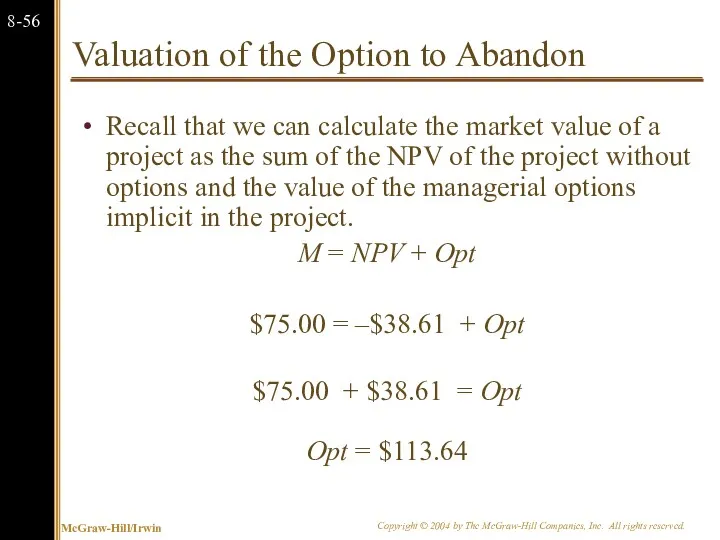

- 57. Valuation of the Option to Abandon Recall that we can calculate the market value of a

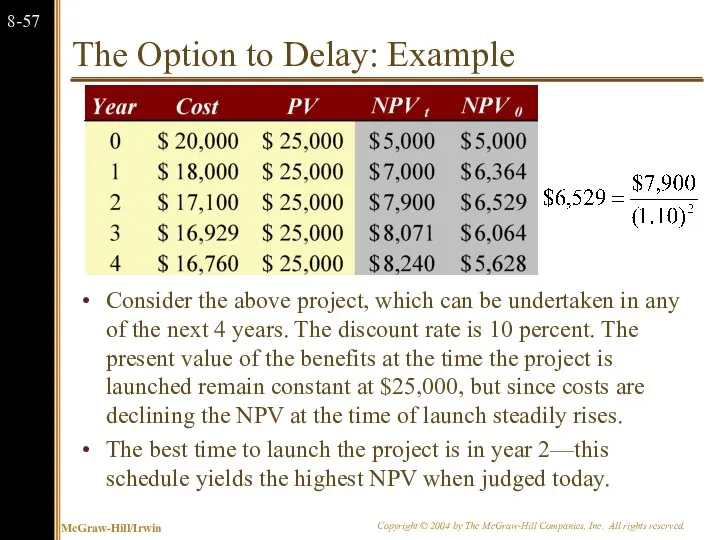

- 58. The Option to Delay: Example Consider the above project, which can be undertaken in any of

- 60. Скачать презентацию

Chapter Outline

8.1 Decision Trees

8.2 Sensitivity Analysis, Scenario Analysis, and

Break-Even

Chapter Outline

8.1 Decision Trees

8.2 Sensitivity Analysis, Scenario Analysis, and

Break-Even

8.1 Decision Trees

Allow us to graphically represent the alternatives available to

8.1 Decision Trees

Allow us to graphically represent the alternatives available to

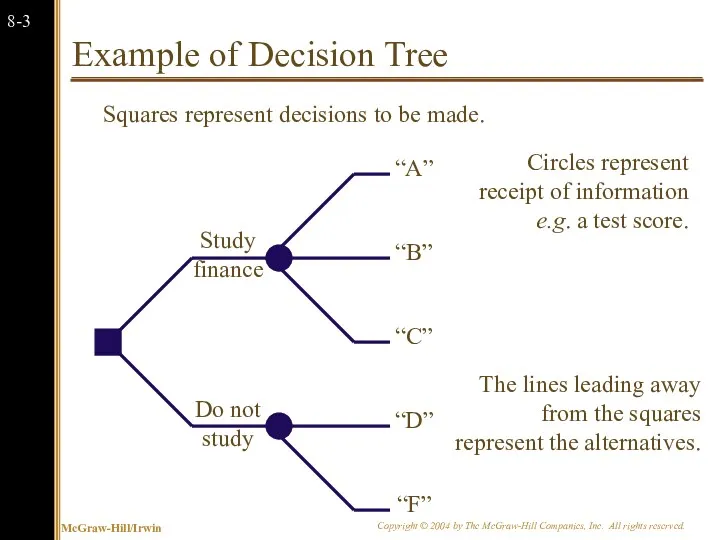

Example of Decision Tree

Do not study

Study finance

Squares represent decisions to be

Example of Decision Tree

Do not study

Study finance

Squares represent decisions to be

Stewart Pharmaceuticals

The Stewart Pharmaceuticals Corporation is considering investing in developing

Stewart Pharmaceuticals

The Stewart Pharmaceuticals Corporation is considering investing in developing

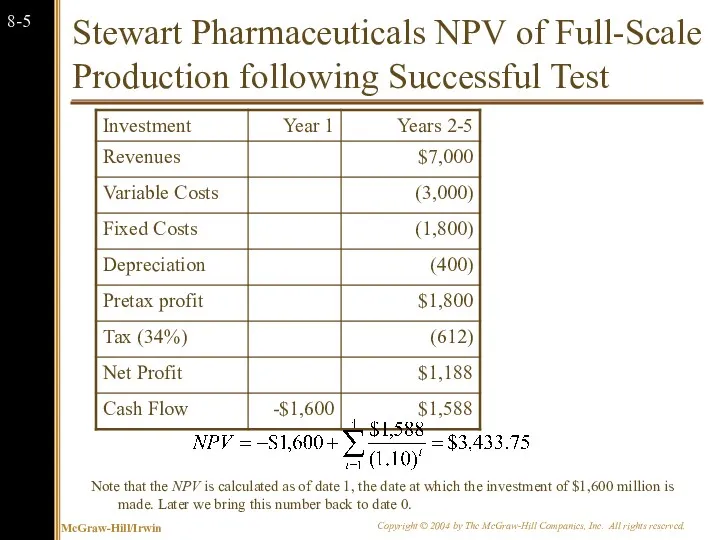

Stewart Pharmaceuticals NPV of Full-Scale Production following Successful Test

Note that the

Stewart Pharmaceuticals NPV of Full-Scale Production following Successful Test

Note that the

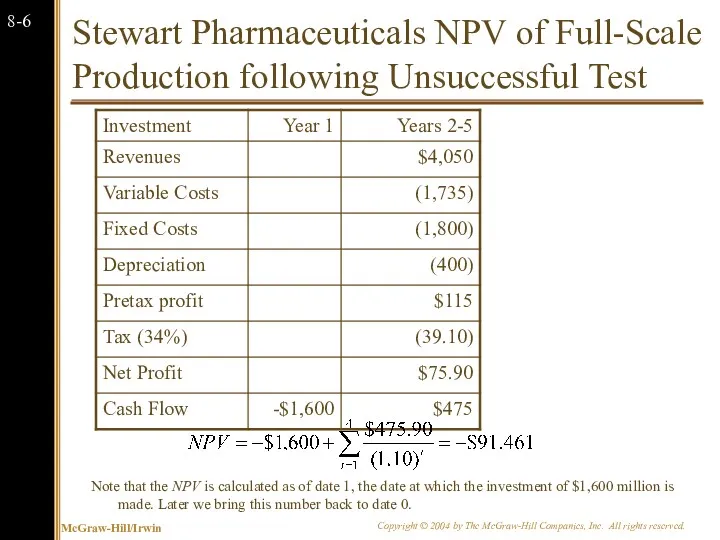

Stewart Pharmaceuticals NPV of Full-Scale Production following Unsuccessful Test

Note that the

Stewart Pharmaceuticals NPV of Full-Scale Production following Unsuccessful Test

Note that the

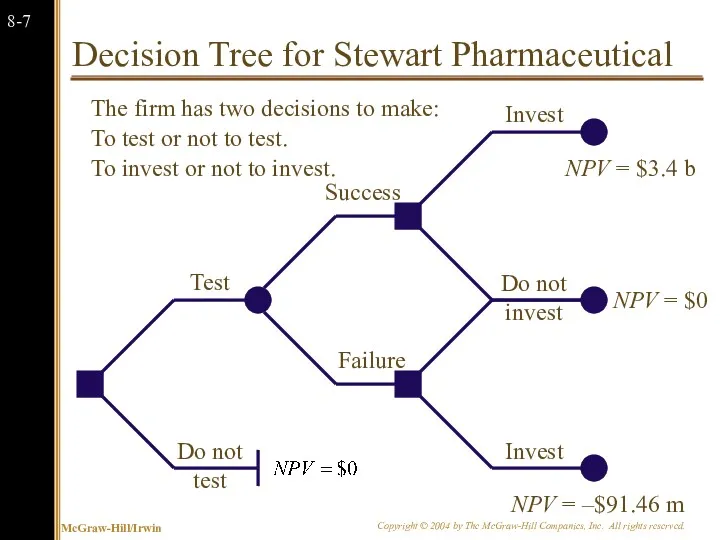

Decision Tree for Stewart Pharmaceutical

Do not test

Test

Failure

Success

Do not invest

Invest

The firm has

Decision Tree for Stewart Pharmaceutical

Do not test

Test

Failure

Success

Do not invest

Invest

The firm has

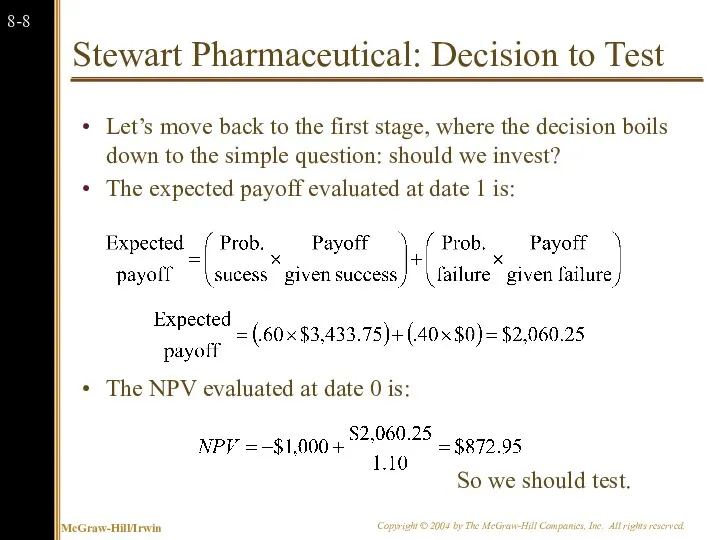

Stewart Pharmaceutical: Decision to Test

Let’s move back to the first stage,

Stewart Pharmaceutical: Decision to Test

Let’s move back to the first stage,

8.3 Sensitivity Analysis, Scenario Analysis, and Break-Even Analysis

Allows us to look

8.3 Sensitivity Analysis, Scenario Analysis, and Break-Even Analysis

Allows us to look

Sensitivity Analysis: Stewart Pharmaceuticals

We can see that NPV is very

Sensitivity Analysis: Stewart Pharmaceuticals

We can see that NPV is very

Scenario Analysis: Stewart Pharmaceuticals

A variation on sensitivity analysis is scenario

Scenario Analysis: Stewart Pharmaceuticals

A variation on sensitivity analysis is scenario

Break-Even Analysis: Stewart Pharmaceuticals

Another way to examine variability in our

Break-Even Analysis: Stewart Pharmaceuticals

Another way to examine variability in our

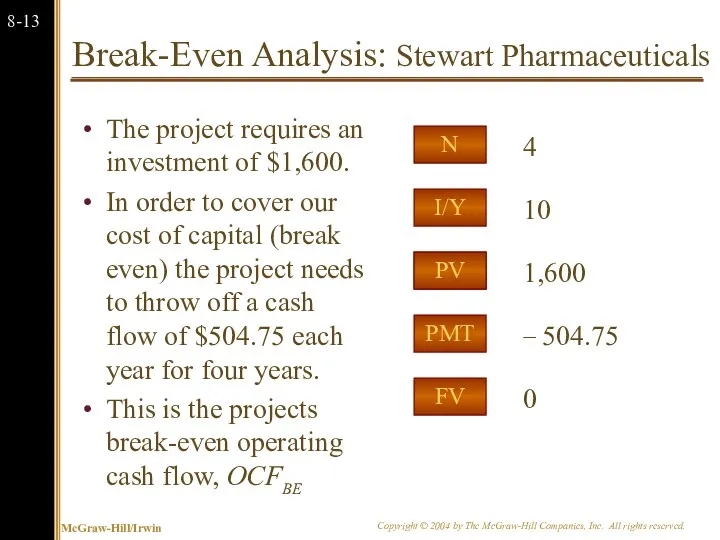

Break-Even Analysis: Stewart Pharmaceuticals

The project requires an investment of $1,600.

In

Break-Even Analysis: Stewart Pharmaceuticals

The project requires an investment of $1,600.

In

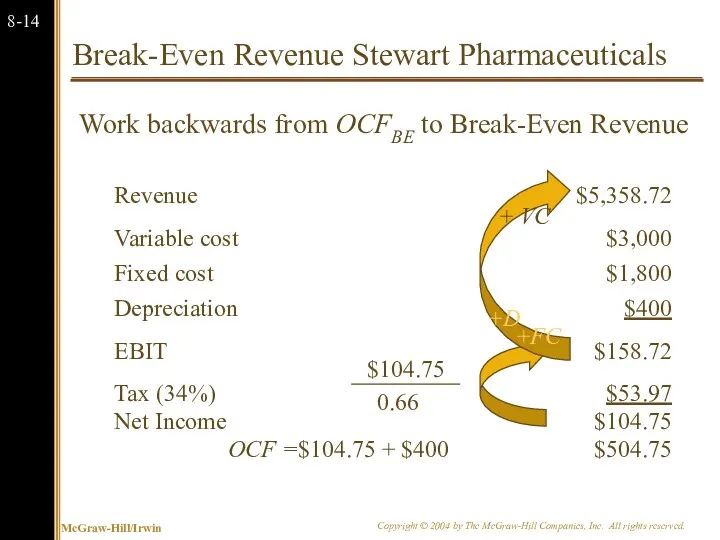

Break-Even Revenue Stewart Pharmaceuticals

Work backwards from OCFBE to Break-Even Revenue

Revenue

$5,358.72

Variable

Break-Even Revenue Stewart Pharmaceuticals

Work backwards from OCFBE to Break-Even Revenue

Revenue

$5,358.72

Variable

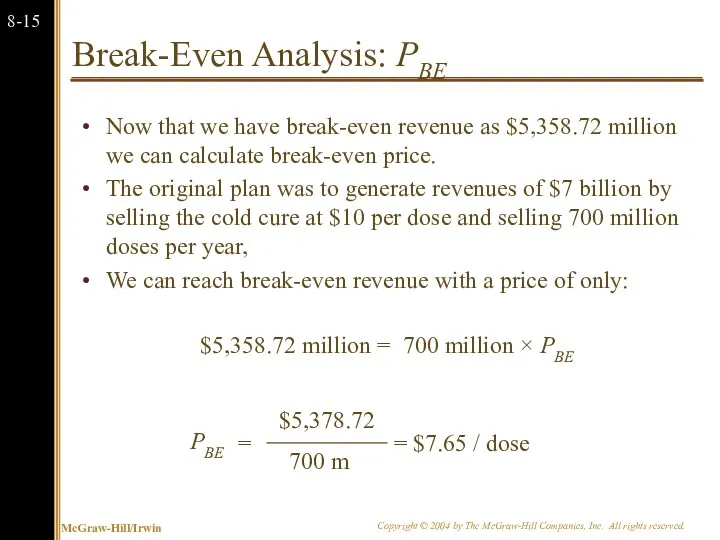

Break-Even Analysis: PBE

Now that we have break-even revenue as $5,358.72 million

Break-Even Analysis: PBE

Now that we have break-even revenue as $5,358.72 million

Break-Even Analysis: Dorm Beds

Recall the “Dorm beds” example from the previous

Break-Even Analysis: Dorm Beds

Recall the “Dorm beds” example from the previous

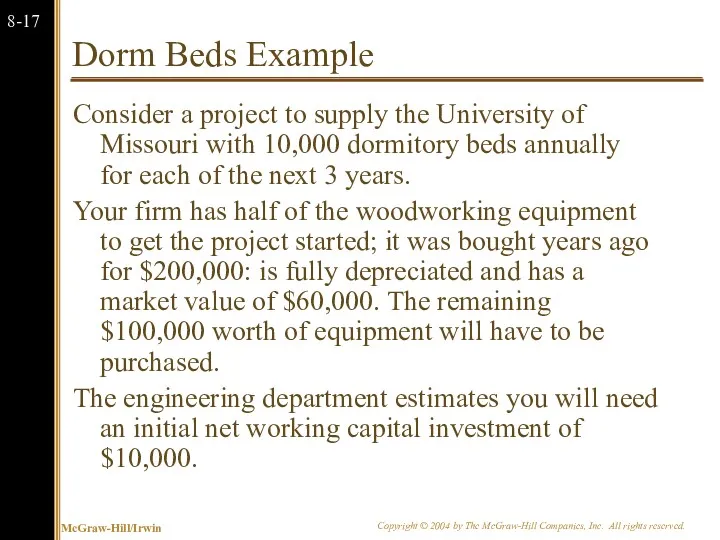

Dorm Beds Example

Consider a project to supply the University of Missouri

Dorm Beds Example

Consider a project to supply the University of Missouri

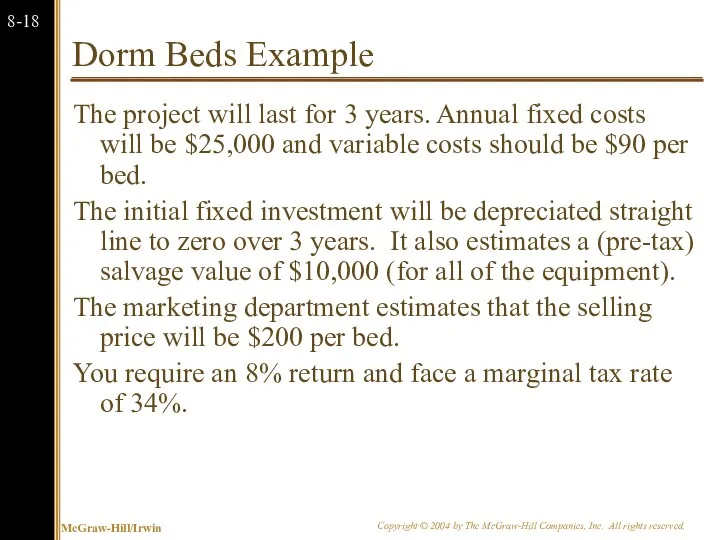

Dorm Beds Example

The project will last for 3 years. Annual fixed

Dorm Beds Example

The project will last for 3 years. Annual fixed

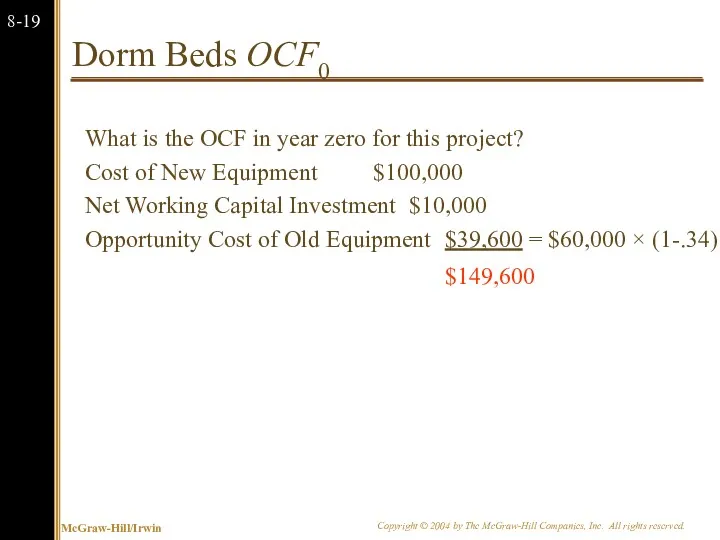

Dorm Beds OCF0

What is the OCF in year zero for this

Dorm Beds OCF0

What is the OCF in year zero for this

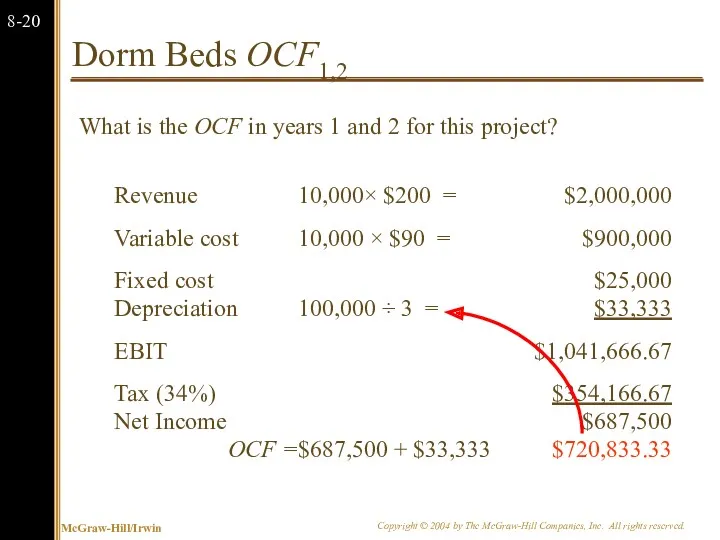

Dorm Beds OCF1,2

What is the OCF in years 1 and 2

Dorm Beds OCF1,2

What is the OCF in years 1 and 2

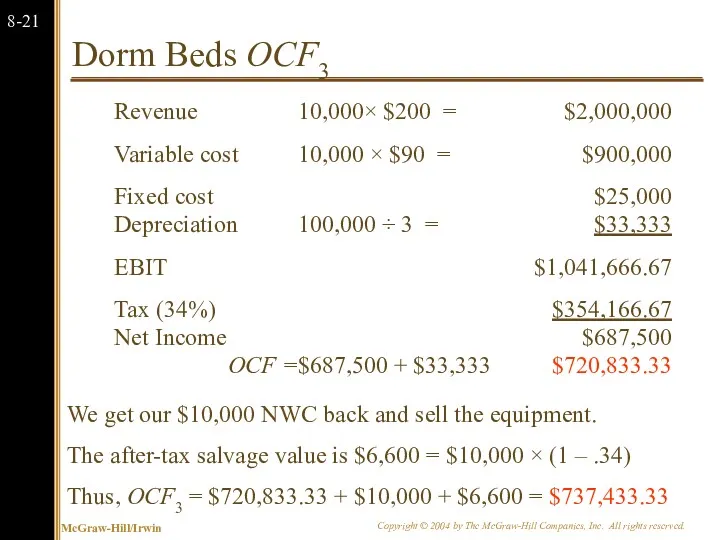

Dorm Beds OCF3

We get our $10,000 NWC back and sell the

Dorm Beds OCF3

We get our $10,000 NWC back and sell the

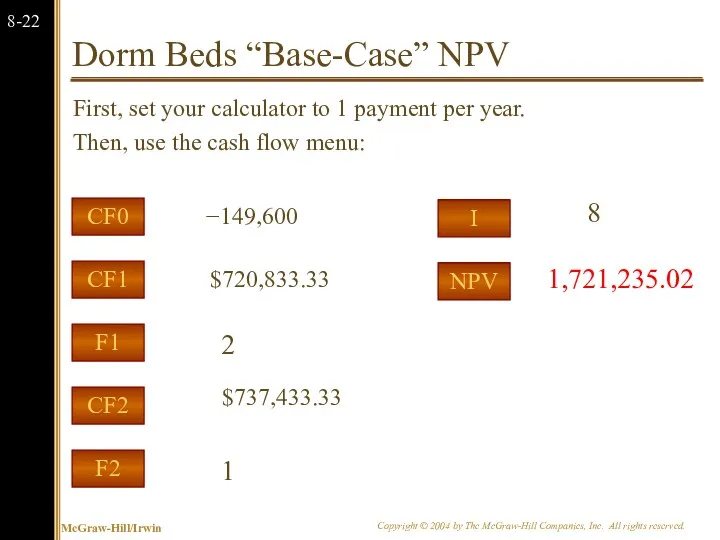

Dorm Beds “Base-Case” NPV

First, set your calculator to 1 payment per

Dorm Beds “Base-Case” NPV

First, set your calculator to 1 payment per

Dorm Beds Break-Even Analysis

In this example, we should be concerned with

Dorm Beds Break-Even Analysis

In this example, we should be concerned with

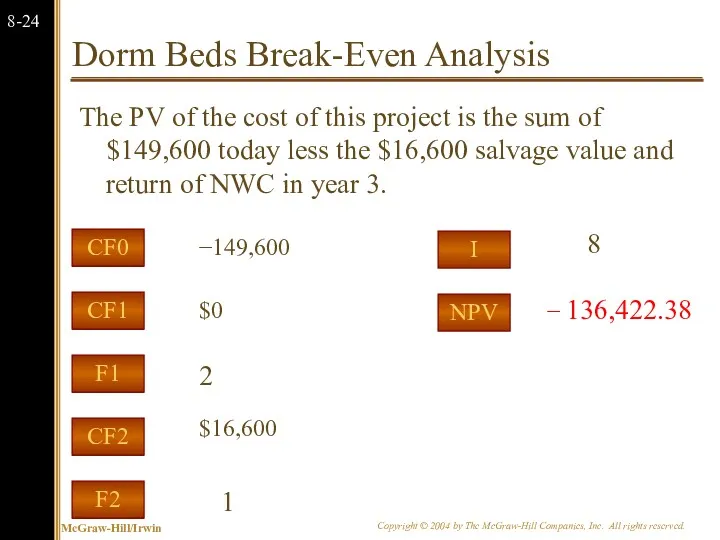

Dorm Beds Break-Even Analysis

The PV of the cost of this project

Dorm Beds Break-Even Analysis

The PV of the cost of this project

Break-Even Analysis: OCFBE

First, set your calculator to 1 payment per year.

Break-Even Analysis: OCFBE

First, set your calculator to 1 payment per year.

Break-Even Revenue

Work backwards from OCFBE to Break-Even Revenue

Revenue

10,000× $PBE =

$988,035.04

Variable

Break-Even Revenue

Work backwards from OCFBE to Break-Even Revenue

Revenue

10,000× $PBE =

$988,035.04

Variable

Break-Even Analysis

Now that we have break-even revenue we can calculate break-even

Break-Even Analysis

Now that we have break-even revenue we can calculate break-even

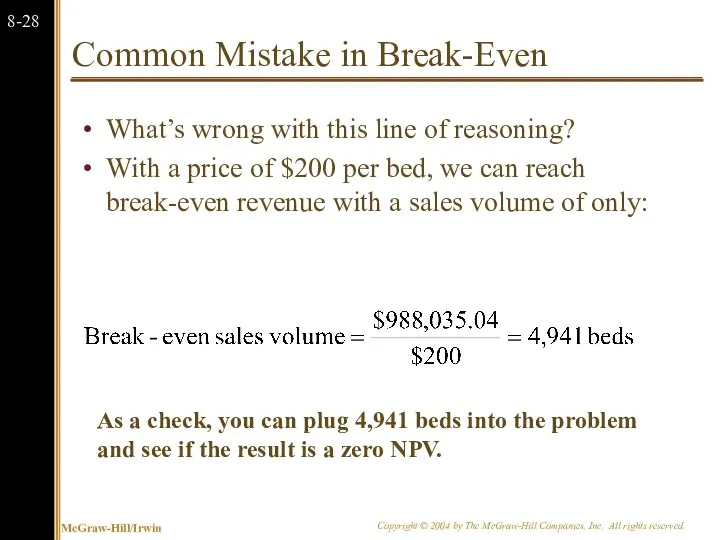

Common Mistake in Break-Even

What’s wrong with this line of reasoning?

With a

Common Mistake in Break-Even

What’s wrong with this line of reasoning?

With a

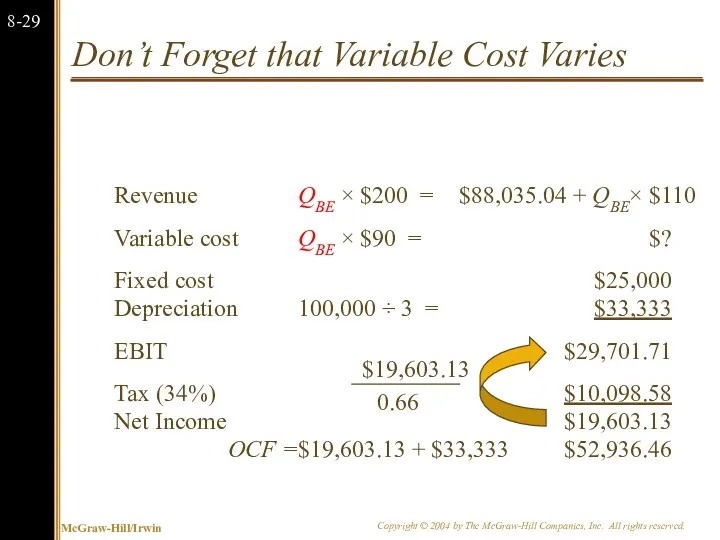

Don’t Forget that Variable Cost Varies

Revenue

QBE × $200 =

$88,035.04 +

Don’t Forget that Variable Cost Varies

Revenue

QBE × $200 =

$88,035.04 +

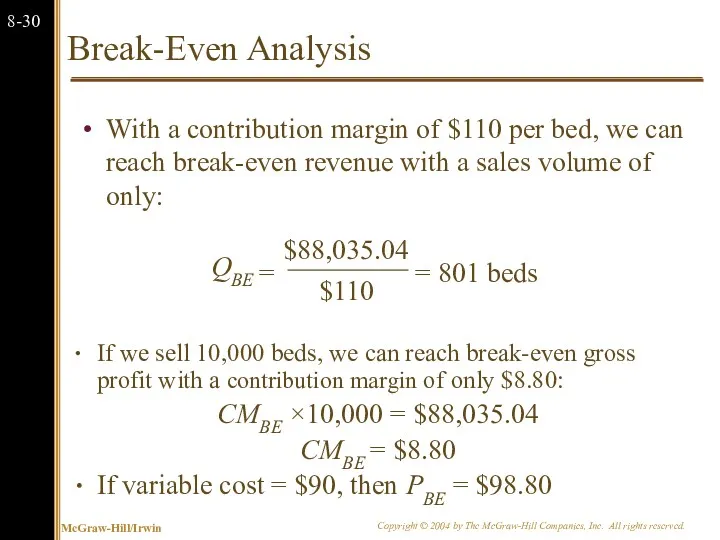

Break-Even Analysis

With a contribution margin of $110 per bed, we can

Break-Even Analysis

With a contribution margin of $110 per bed, we can

Break-Even Lease Payment

Joe Machens is contemplating leasing the University of Missouri

Break-Even Lease Payment

Joe Machens is contemplating leasing the University of Missouri

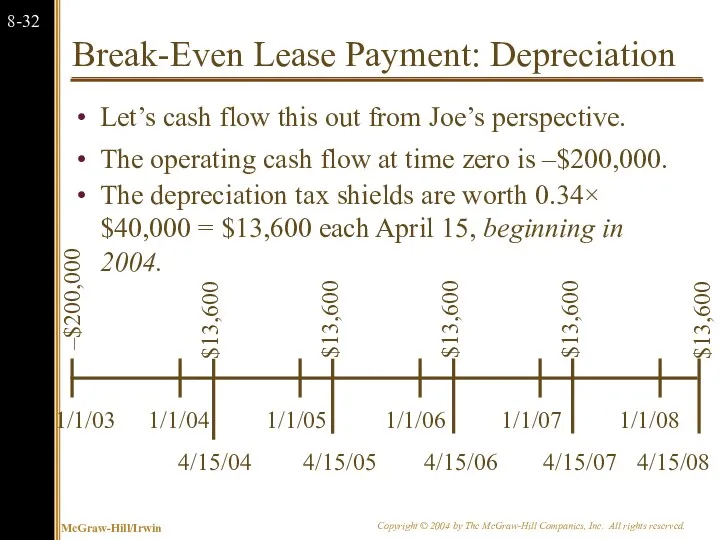

Break-Even Lease Payment: Depreciation

Let’s cash flow this out from Joe’s perspective.

The

Break-Even Lease Payment: Depreciation

Let’s cash flow this out from Joe’s perspective.

The

Present Value of Depreciation Tax Shield

The PV of the depreciation tax

Present Value of Depreciation Tax Shield

The PV of the depreciation tax

Present Value of Depreciation Tax Shield

The PV of the depreciation tax

Present Value of Depreciation Tax Shield

The PV of the depreciation tax

Where we’re at so far:

The cars do not cost Joe Machens

Where we’re at so far:

The cars do not cost Joe Machens

Step Two: Taxes

Joe has to pay taxes on last year’s income

1/1/03

1/1/04

1/1/05

1/1/06

1/1/07

1/1/08

Taxes

Step Two: Taxes

Joe has to pay taxes on last year’s income

1/1/03

1/1/04

1/1/05

1/1/06

1/1/07

1/1/08

Taxes

Present Value of Tax Liability

The PV of the tax liability is

Present Value of Tax Liability

The PV of the tax liability is

Present Value of Tax Liability

The PV of the tax liability on

Present Value of Tax Liability

The PV of the tax liability on

Solution: Payments

In addition to the depreciation tax shields and income taxes,

Solution: Payments

In addition to the depreciation tax shields and income taxes,

Present Value of Gross Revenue

The PV of 60 months of gross

Present Value of Gross Revenue

The PV of 60 months of gross

Solution (continued)

So the least Joe can charge is:

$200,000 – $53,176.99

Solution (continued)

So the least Joe can charge is:

$200,000 – $53,176.99

Summary Joe Machens

This problem was a bit more complicated than previous

Summary Joe Machens

This problem was a bit more complicated than previous

8.3 Monte Carlo Simulation

Monte Carlo simulation is a further attempt to

8.3 Monte Carlo Simulation

Monte Carlo simulation is a further attempt to

8.3 Monte Carlo Simulation

Imagine a serious blackjack player who wants to

8.3 Monte Carlo Simulation

Imagine a serious blackjack player who wants to

8.3 Monte Carlo Simulation

Monte Carlo simulation of capital budgeting projects is

8.3 Monte Carlo Simulation

Monte Carlo simulation of capital budgeting projects is

8.4 Options

One of the fundamental insights of modern finance theory is

8.4 Options

One of the fundamental insights of modern finance theory is

Options

The Option to Expand

Has value if demand turns out to be

Options

The Option to Expand

Has value if demand turns out to be

The Option to Expand

Imagine a start-up firm, Campusteria, Inc. which plans

The Option to Expand

Imagine a start-up firm, Campusteria, Inc. which plans

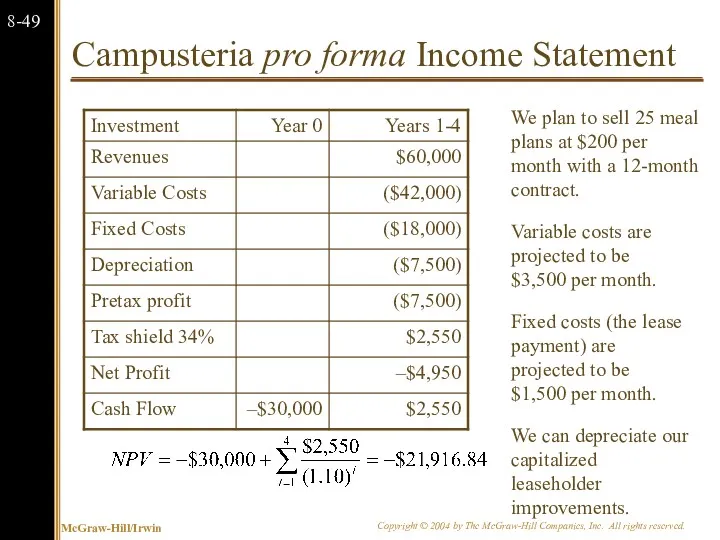

Campusteria pro forma Income Statement

We plan to sell 25 meal plans

Campusteria pro forma Income Statement

We plan to sell 25 meal plans

The Option to Expand: Valuing a Start-Up

Note that while the Campusteria

The Option to Expand: Valuing a Start-Up

Note that while the Campusteria

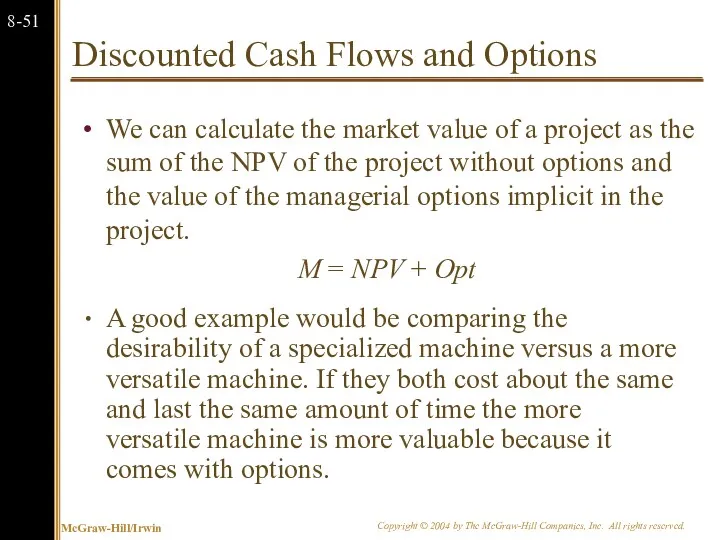

Discounted Cash Flows and Options

We can calculate the market value of

Discounted Cash Flows and Options

We can calculate the market value of

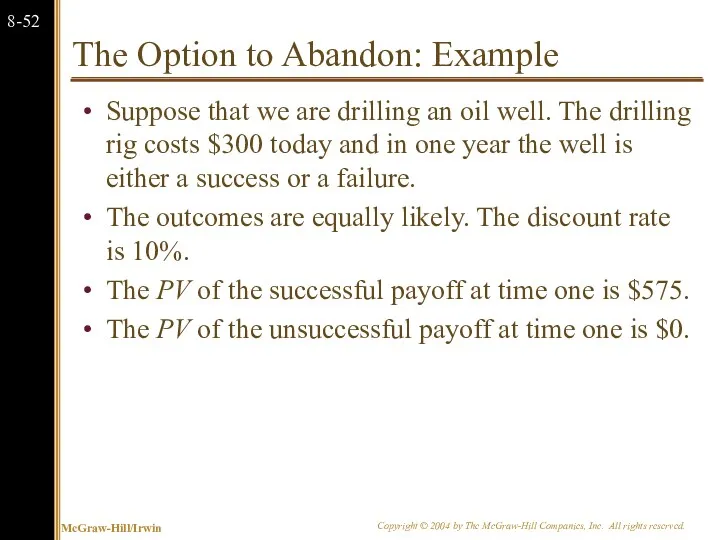

The Option to Abandon: Example

Suppose that we are drilling an oil

The Option to Abandon: Example

Suppose that we are drilling an oil

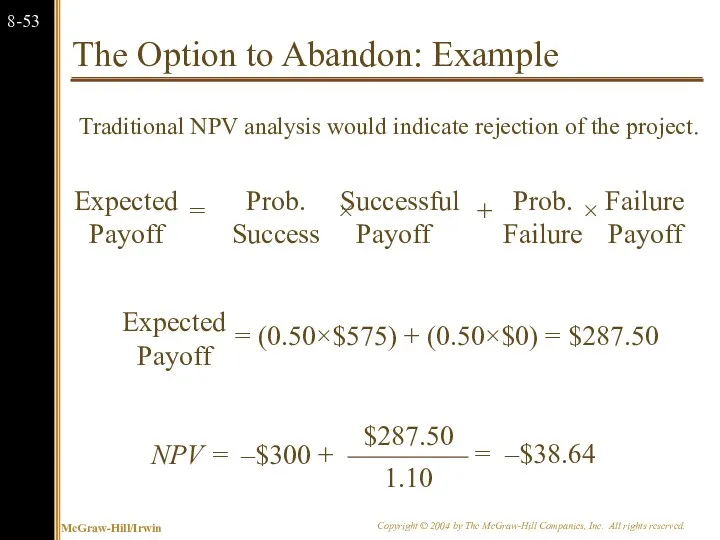

The Option to Abandon: Example

Traditional NPV analysis would indicate rejection

The Option to Abandon: Example

Traditional NPV analysis would indicate rejection

The Option to Abandon: Example

The firm has two decisions to make:

The Option to Abandon: Example

The firm has two decisions to make:

The Option to Abandon: Example

When we include the value of

The Option to Abandon: Example

When we include the value of

Valuation of the Option to Abandon

Recall that we can calculate the

Valuation of the Option to Abandon

Recall that we can calculate the

The Option to Delay: Example

Consider the above project, which can be

The Option to Delay: Example

Consider the above project, which can be

Акция! 20+1 мотивация оптовых клиентов на закупку кофейных напитков 3в1

Акция! 20+1 мотивация оптовых клиентов на закупку кофейных напитков 3в1 Vodafone PPM booklet

Vodafone PPM booklet Компания Atomy

Компания Atomy 2018 GRO GLOBAL. Здоровый сон младенца

2018 GRO GLOBAL. Здоровый сон младенца Применение средств и методов поведенческой экономики в маркетинговой деятельности туристического предприятия

Применение средств и методов поведенческой экономики в маркетинговой деятельности туристического предприятия Project: Global Social Media Plan // May Topic: Cornering Light Format: Film Date: date related

Project: Global Social Media Plan // May Topic: Cornering Light Format: Film Date: date related Маркетинговые исследования

Маркетинговые исследования ООО “Рус Клин Компани”, бренд Эко Сити Лайф

ООО “Рус Клин Компани”, бренд Эко Сити Лайф Brand Introduction. PART Market Competitiveness

Brand Introduction. PART Market Competitiveness Подготовка к экзамену. WebPromo Experts

Подготовка к экзамену. WebPromo Experts Product concepts

Product concepts Развитие социальной рекламы на телевидении в России

Развитие социальной рекламы на телевидении в России Зимний уход за кожей лица. АРГО

Зимний уход за кожей лица. АРГО Техника продаж. Работа с возражениями

Техника продаж. Работа с возражениями Помещение (147 м2) в аренду. Характеристика помещения

Помещение (147 м2) в аренду. Характеристика помещения Project: Global Social Media Plan // September Topic: Fashion Month 1 Subline: The Arteon strikes a pose Format: Image

Project: Global Social Media Plan // September Topic: Fashion Month 1 Subline: The Arteon strikes a pose Format: Image Коммерческое предложение по размещению рекламы в лифтах г. Электросталь, г. Ногинск

Коммерческое предложение по размещению рекламы в лифтах г. Электросталь, г. Ногинск Маркетинговые коммуникации

Маркетинговые коммуникации Виртуальная АТС

Виртуальная АТС Project: Global Social Media Plan // February Topic: Fashion Shows 1 Format: image Date: Seasonal Content

Project: Global Social Media Plan // February Topic: Fashion Shows 1 Format: image Date: Seasonal Content Презентация продукта торговый эквайринг

Презентация продукта торговый эквайринг Adversting

Adversting Марка одежды Сomme des garcons

Марка одежды Сomme des garcons Этапы работы над рекламным проектом в стиле шоу

Этапы работы над рекламным проектом в стиле шоу Экспертное продвижение в INSTAGRAM. Обеспечим рост продаж вашему бизнесу

Экспертное продвижение в INSTAGRAM. Обеспечим рост продаж вашему бизнесу Создание собственных онлайн-курсов

Создание собственных онлайн-курсов Оптовые поставки детской обуви. ООО АНАЛИТИКА

Оптовые поставки детской обуви. ООО АНАЛИТИКА Электронная коммерция в Интернете

Электронная коммерция в Интернете