- Cost Management

Содержание

- 2. Objectives of Project’s Cost Management To guarantee that all expenses will be covered – Budgeting: Itemizing

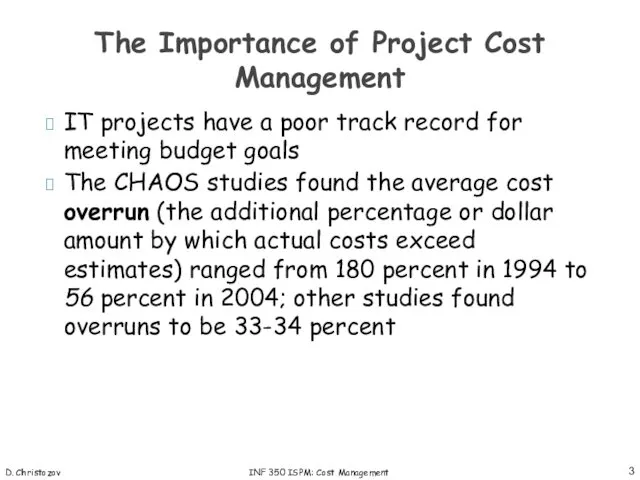

- 3. D. Christozov INF 350 ISPM: Cost Management IT projects have a poor track record for meeting

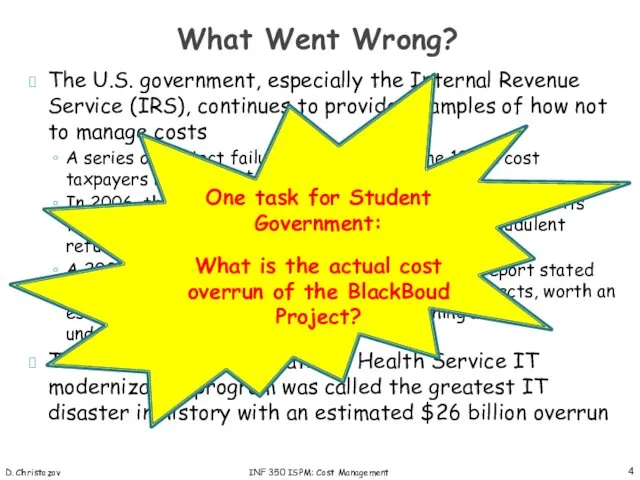

- 4. D. Christozov INF 350 ISPM: Cost Management The U.S. government, especially the Internal Revenue Service (IRS),

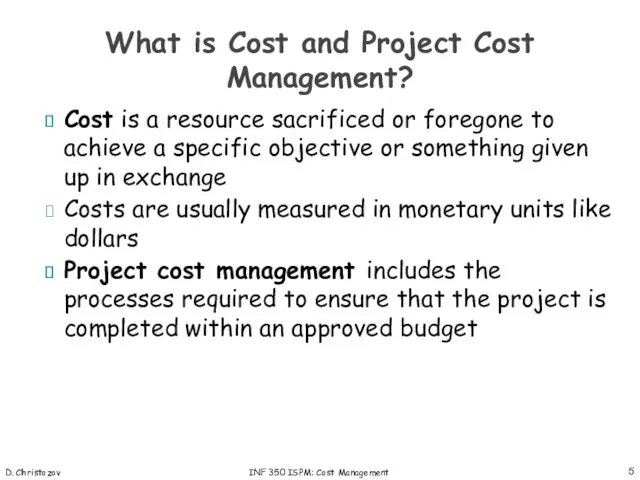

- 5. D. Christozov INF 350 ISPM: Cost Management Cost is a resource sacrificed or foregone to achieve

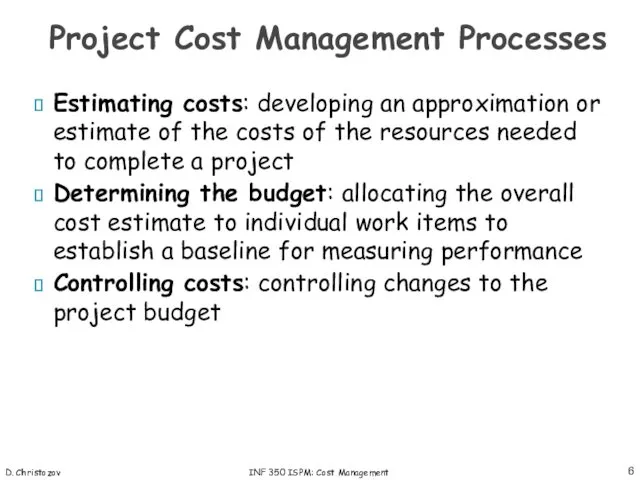

- 6. D. Christozov INF 350 ISPM: Cost Management Estimating costs: developing an approximation or estimate of the

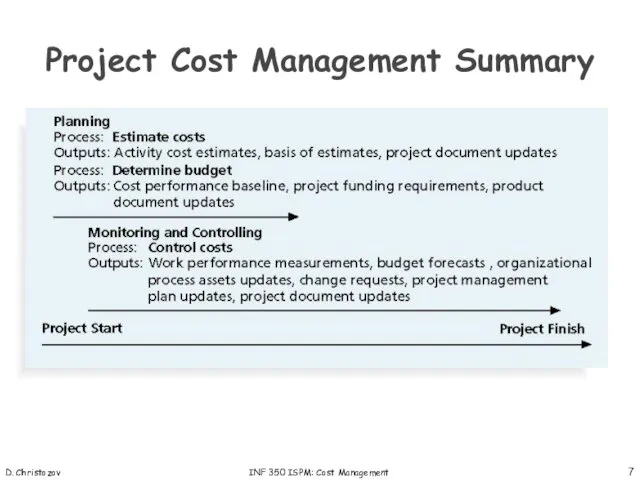

- 7. D. Christozov INF 350 ISPM: Cost Management Project Cost Management Summary

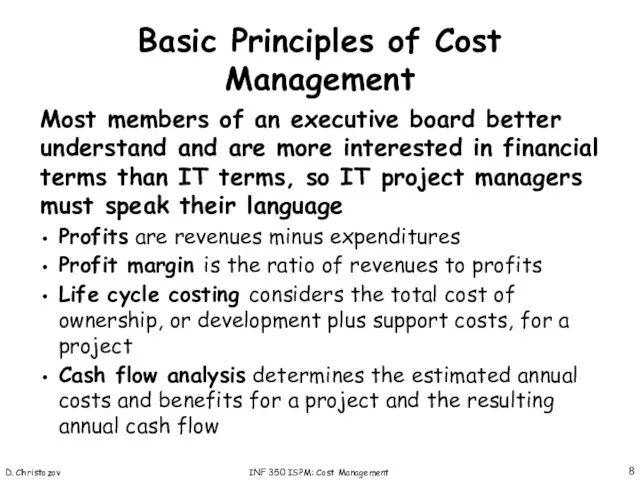

- 8. D. Christozov INF 350 ISPM: Cost Management Most members of an executive board better understand and

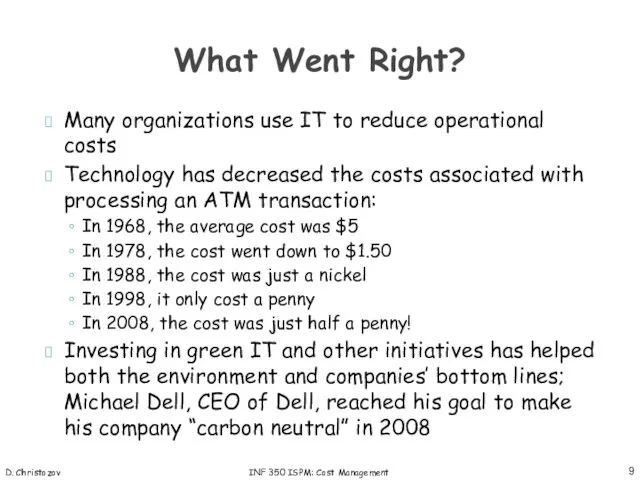

- 9. D. Christozov INF 350 ISPM: Cost Management Many organizations use IT to reduce operational costs Technology

- 10. D. Christozov INF 350 ISPM: Cost Management Tangible costs or benefits are those costs or benefits

- 11. D. Christozov INF 350 ISPM: Cost Management Learning curve theory states that when many items are

- 12. D. Christozov INF 350 ISPM: Cost Management Project managers must take cost estimates seriously if they

- 13. D. Christozov INF 350 ISPM: Cost Management Types of Cost Estimates

- 14. D. Christozov INF 350 ISPM: Cost Management A cost management plan is a document that describes

- 15. D. Christozov INF 350 ISPM: Cost Management Basic tools and techniques for cost estimates: Analogous or

- 16. D. Christozov INF 350 ISPM: Cost Management Estimates are done too quickly Lack of estimating experience

- 17. D. Christozov INF 350 ISPM: Cost Management Before creating an estimate, know what it will be

- 18. D. Christozov INF 350 ISPM: Cost Management Surveyor Pro Project Cost Estimate

- 19. D. Christozov INF 350 ISPM: Cost Management Surveyor Pro Software Development Estimate

- 20. D. Christozov INF 350 ISPM: Cost Management Cost budgeting involves allocating the project cost estimate to

- 21. D. Christozov INF 350 ISPM: Cost Management Surveyor Pro Project Cost Baseline

- 22. D. Christozov INF 350 ISPM: Cost Management Project cost control includes: Monitoring cost performance Ensuring that

- 23. D. Christozov INF 350 ISPM: Cost Management Many organizations collect and control an entire suite of

- 24. D. Christozov INF 350 ISPM: Cost Management Schlumberger saved $3 million in one year by organizing

- 25. D. Christozov INF 350 ISPM: Cost Management A global survey released by Borland Software in 2006

- 26. D. Christozov INF 350 ISPM: Cost Management Cost-Benefit and Cash-Flow Steps: Identifying and estimating all of

- 27. D. Christozov INF 350 ISPM: Cost Management Cash-flow Measures Pay-back period: break-even point Return of Investments

- 28. D. Christozov INF 350 ISPM: Cost Management Cash-flow Measures Return on investment (ROI or accounting rate

- 29. D. Christozov INF 350 ISPM: Cost Management Cash-flow Measures Net present value: PV = (value in

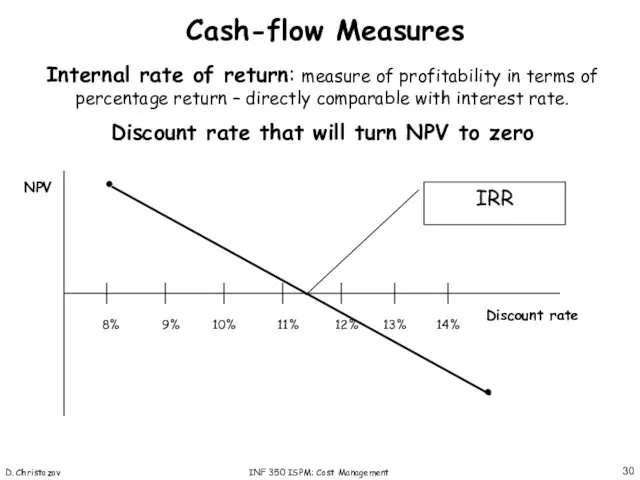

- 30. D. Christozov INF 350 ISPM: Cost Management Cash-flow Measures Internal rate of return: measure of profitability

- 31. D. Christozov INF 270 PIS: Change Management

- 32. D. Christozov INF 350 ISPM: Cost Management EVM is a project performance measurement technique that integrates

- 33. D. Christozov INF 350 ISPM: Cost Management The planned value (PV), formerly called the budgeted cost

- 34. D. Christozov INF 350 ISPM: Cost Management Rate of performance (RP) is the ratio of actual

- 35. D. Christozov INF 350 ISPM: Cost Management Earned Value Calculations for One Activity after Week One

- 36. D. Christozov INF 350 ISPM: Cost Management Earned Value Formulas

- 37. D. Christozov INF 350 ISPM: Cost Management Negative numbers for cost and schedule variance indicate problems

- 39. Скачать презентацию

Objectives of Project’s

Cost Management

To guarantee that all expenses will be

Objectives of Project’s

Cost Management

To guarantee that all expenses will be

D. Christozov

INF 350 ISPM: Cost Management

IT projects have a poor track

D. Christozov

INF 350 ISPM: Cost Management

IT projects have a poor track

D. Christozov

INF 350 ISPM: Cost Management

The U.S. government, especially the Internal

D. Christozov

INF 350 ISPM: Cost Management

The U.S. government, especially the Internal

D. Christozov

INF 350 ISPM: Cost Management

Cost is a resource sacrificed or

D. Christozov

INF 350 ISPM: Cost Management

Cost is a resource sacrificed or

D. Christozov

INF 350 ISPM: Cost Management

Estimating costs: developing an approximation or

D. Christozov

INF 350 ISPM: Cost Management

Estimating costs: developing an approximation or

D. Christozov

INF 350 ISPM: Cost Management

Project Cost Management Summary

D. Christozov

INF 350 ISPM: Cost Management

Project Cost Management Summary

D. Christozov

INF 350 ISPM: Cost Management

Most members of an executive board

D. Christozov

INF 350 ISPM: Cost Management

Most members of an executive board

D. Christozov

INF 350 ISPM: Cost Management

Many organizations use IT to reduce

D. Christozov

INF 350 ISPM: Cost Management

Many organizations use IT to reduce

D. Christozov

INF 350 ISPM: Cost Management

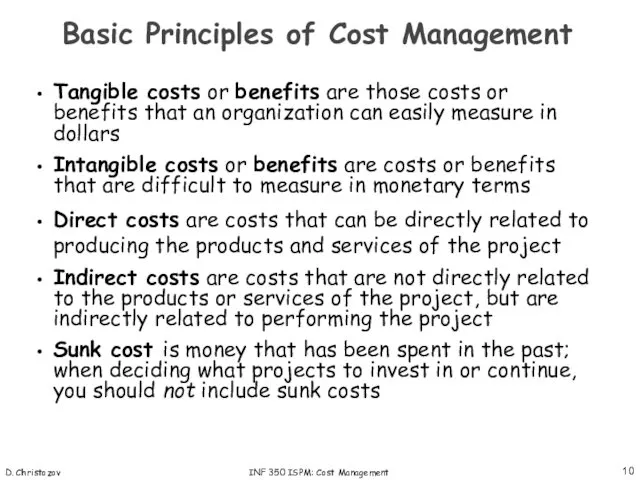

Tangible costs or benefits are those

D. Christozov

INF 350 ISPM: Cost Management

Tangible costs or benefits are those

D. Christozov

INF 350 ISPM: Cost Management

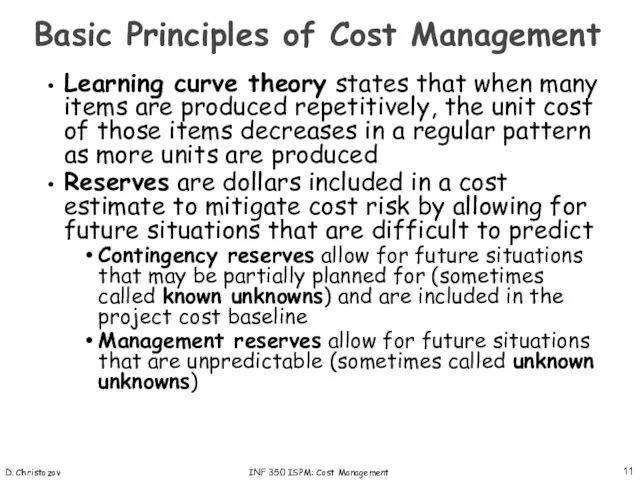

Learning curve theory states that when

D. Christozov

INF 350 ISPM: Cost Management

Learning curve theory states that when

D. Christozov

INF 350 ISPM: Cost Management

Project managers must take cost estimates

D. Christozov

INF 350 ISPM: Cost Management

Project managers must take cost estimates

D. Christozov

INF 350 ISPM: Cost Management

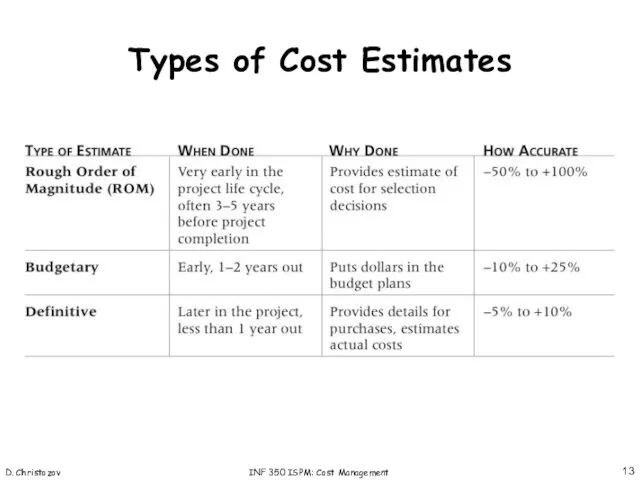

Types of Cost Estimates

D. Christozov

INF 350 ISPM: Cost Management

Types of Cost Estimates

D. Christozov

INF 350 ISPM: Cost Management

A cost management plan is a

D. Christozov

INF 350 ISPM: Cost Management

A cost management plan is a

D. Christozov

INF 350 ISPM: Cost Management

Basic tools and techniques for cost

D. Christozov

INF 350 ISPM: Cost Management

Basic tools and techniques for cost

D. Christozov

INF 350 ISPM: Cost Management

Estimates are done too quickly

Lack of

D. Christozov

INF 350 ISPM: Cost Management

Estimates are done too quickly

Lack of

D. Christozov

INF 350 ISPM: Cost Management

Before creating an estimate, know what

D. Christozov

INF 350 ISPM: Cost Management

Before creating an estimate, know what

D. Christozov

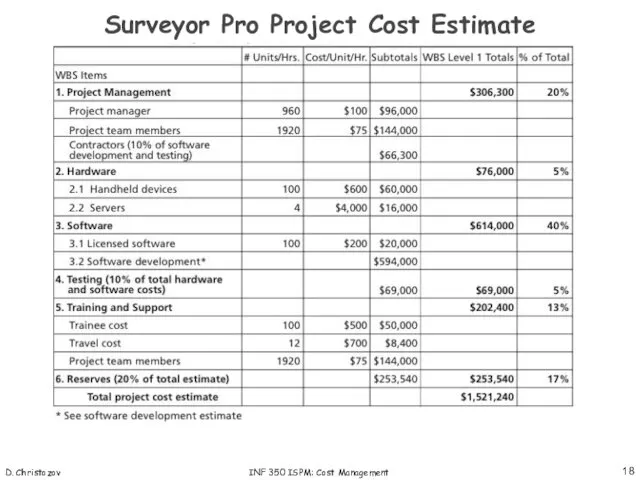

INF 350 ISPM: Cost Management

Surveyor Pro Project Cost Estimate

D. Christozov

INF 350 ISPM: Cost Management

Surveyor Pro Project Cost Estimate

D. Christozov

INF 350 ISPM: Cost Management

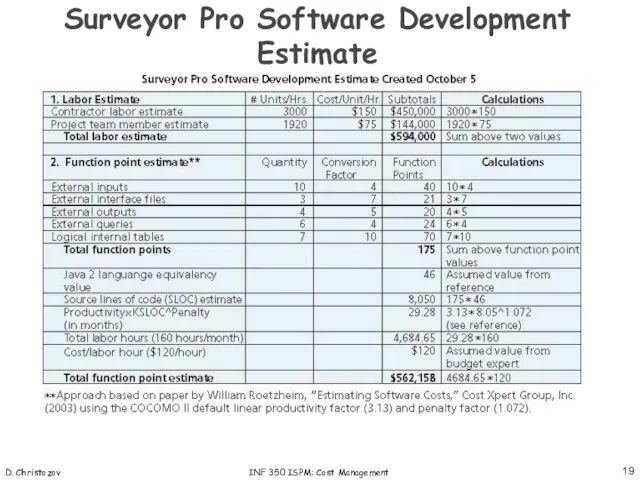

Surveyor Pro Software Development Estimate

D. Christozov

INF 350 ISPM: Cost Management

Surveyor Pro Software Development Estimate

D. Christozov

INF 350 ISPM: Cost Management

Cost budgeting involves allocating the project

D. Christozov

INF 350 ISPM: Cost Management

Cost budgeting involves allocating the project

D. Christozov

INF 350 ISPM: Cost Management

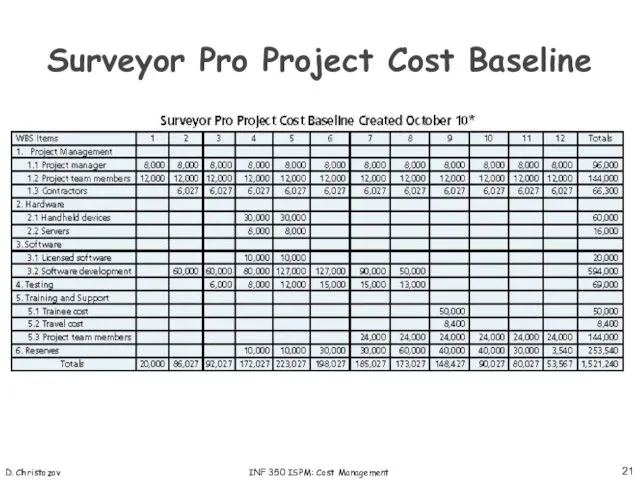

Surveyor Pro Project Cost Baseline

D. Christozov

INF 350 ISPM: Cost Management

Surveyor Pro Project Cost Baseline

D. Christozov

INF 350 ISPM: Cost Management

Project cost control includes:

Monitoring cost performance

Ensuring

D. Christozov

INF 350 ISPM: Cost Management

Project cost control includes:

Monitoring cost performance

Ensuring

D. Christozov

INF 350 ISPM: Cost Management

Many organizations collect and control an

D. Christozov

INF 350 ISPM: Cost Management

Many organizations collect and control an

D. Christozov

INF 350 ISPM: Cost Management

Schlumberger saved $3 million in one

D. Christozov

INF 350 ISPM: Cost Management

Schlumberger saved $3 million in one

D. Christozov

INF 350 ISPM: Cost Management

A global survey released by Borland

D. Christozov

INF 350 ISPM: Cost Management

A global survey released by Borland

D. Christozov

INF 350 ISPM: Cost Management

Cost-Benefit and Cash-Flow

Steps:

Identifying and estimating all

D. Christozov

INF 350 ISPM: Cost Management

Cost-Benefit and Cash-Flow

Steps:

Identifying and estimating all

D. Christozov

INF 350 ISPM: Cost Management

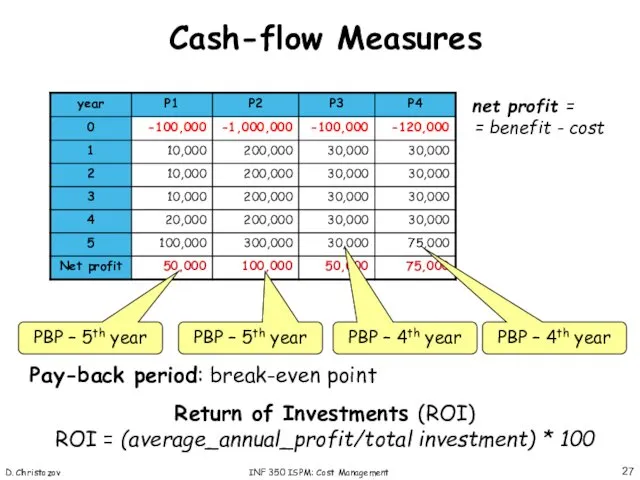

Cash-flow Measures

Pay-back period: break-even point

Return of

D. Christozov

INF 350 ISPM: Cost Management

Cash-flow Measures

Pay-back period: break-even point

Return of

D. Christozov

INF 350 ISPM: Cost Management

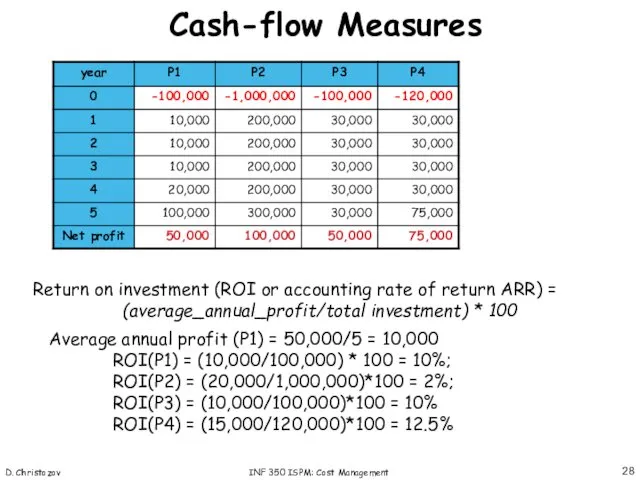

Cash-flow Measures

Return on investment (ROI or

D. Christozov

INF 350 ISPM: Cost Management

Cash-flow Measures

Return on investment (ROI or

D. Christozov

INF 350 ISPM: Cost Management

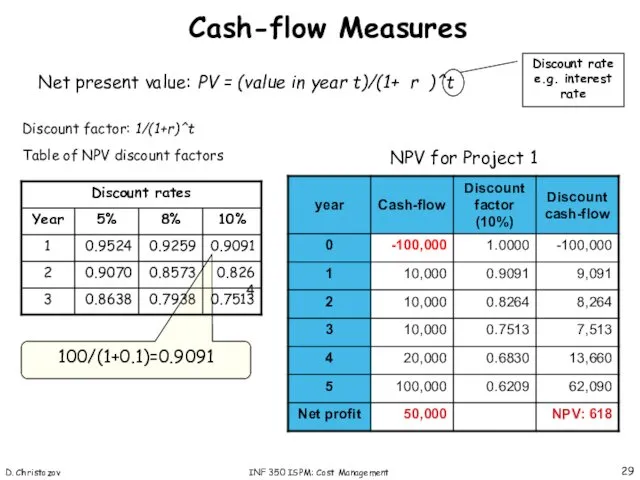

Cash-flow Measures

Net present value: PV =

D. Christozov

INF 350 ISPM: Cost Management

Cash-flow Measures

Net present value: PV =

D. Christozov

INF 350 ISPM: Cost Management

Cash-flow Measures

Internal rate of return: measure

D. Christozov

INF 350 ISPM: Cost Management

Cash-flow Measures

Internal rate of return: measure

D. Christozov

INF 270 PIS: Change Management

D. Christozov

INF 270 PIS: Change Management

D. Christozov

INF 350 ISPM: Cost Management

EVM is a project performance measurement

D. Christozov

INF 350 ISPM: Cost Management

EVM is a project performance measurement

D. Christozov

INF 350 ISPM: Cost Management

The planned value (PV), formerly called

D. Christozov

INF 350 ISPM: Cost Management

The planned value (PV), formerly called

D. Christozov

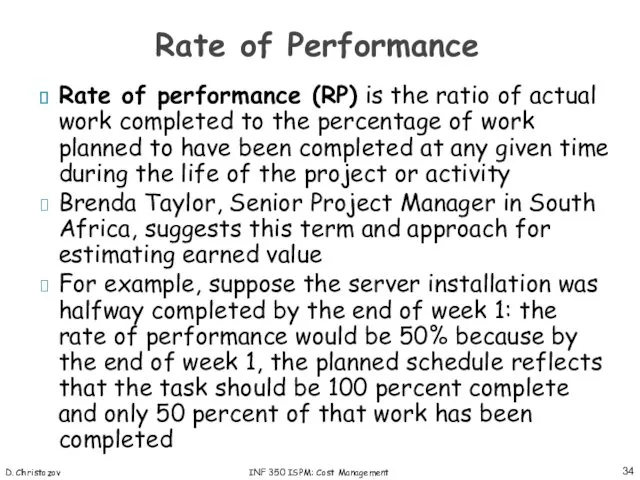

INF 350 ISPM: Cost Management

Rate of performance (RP) is the

D. Christozov

INF 350 ISPM: Cost Management

Rate of performance (RP) is the

D. Christozov

INF 350 ISPM: Cost Management

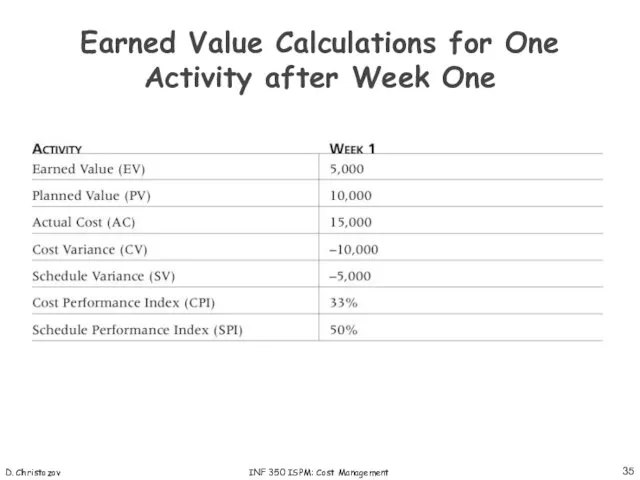

Earned Value Calculations for One Activity

D. Christozov

INF 350 ISPM: Cost Management

Earned Value Calculations for One Activity

D. Christozov

INF 350 ISPM: Cost Management

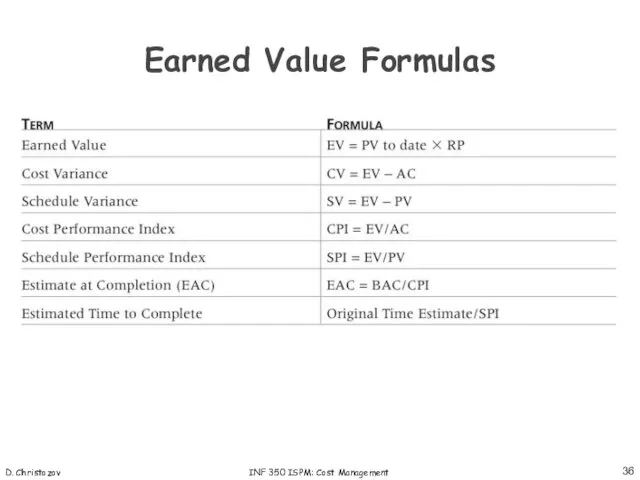

Earned Value Formulas

D. Christozov

INF 350 ISPM: Cost Management

Earned Value Formulas

D. Christozov

INF 350 ISPM: Cost Management

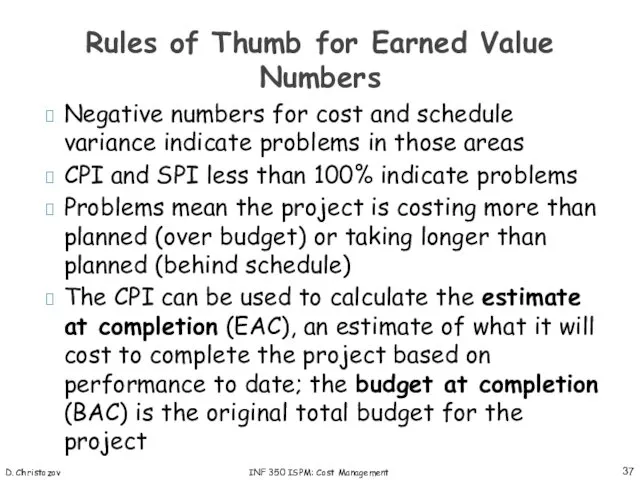

Negative numbers for cost and schedule

D. Christozov

INF 350 ISPM: Cost Management

Negative numbers for cost and schedule

Менеджмент в здравоохранении

Менеджмент в здравоохранении Лидерство в организации

Лидерство в организации Логистика: миссия, цель, объект, предмет и задачи, проблемы и результат

Логистика: миссия, цель, объект, предмет и задачи, проблемы и результат Повышение эффективности использования основных производственных фондов спортивного сооружения

Повышение эффективности использования основных производственных фондов спортивного сооружения Планування часу

Планування часу Управление инновационным проектом

Управление инновационным проектом Сбытовая деятельность предприятия

Сбытовая деятельность предприятия Кадровая политика организации

Кадровая политика организации Телефонный этикет

Телефонный этикет Formation of a system of management methods and their classification

Formation of a system of management methods and their classification Имидж делового человека

Имидж делового человека Методы качественного оценивания систем

Методы качественного оценивания систем Сапа менеджмент жүйесінің халықаралық стандарты. Сапа менеджменті жүйесін стандарттарын жетілдіру

Сапа менеджмент жүйесінің халықаралық стандарты. Сапа менеджменті жүйесін стандарттарын жетілдіру Приёмка товара. Сроки и нормативы приёмки

Приёмка товара. Сроки и нормативы приёмки Управление проектами. Сущность проекта. Жизненный цикл проекта

Управление проектами. Сущность проекта. Жизненный цикл проекта Анализ видов деятельности в ценностной цепочке

Анализ видов деятельности в ценностной цепочке 1Внешняя и внутренняя срда организации

1Внешняя и внутренняя срда организации Методы управления в органах внутренних дел

Методы управления в органах внутренних дел Теории менеджмента

Теории менеджмента Определение и предметная область проекта. Лекция 4

Определение и предметная область проекта. Лекция 4 Сущность и содержание понятия менеджмент

Сущность и содержание понятия менеджмент Теоретический анализ концепций лидерства

Теоретический анализ концепций лидерства Управление инновациями

Управление инновациями Управление проектами и риски

Управление проектами и риски Мотивация персонала

Мотивация персонала Мотивация персонала

Мотивация персонала 3 еркіндік дәрежелі дельта-роботты жобалау және басқару

3 еркіндік дәрежелі дельта-роботты жобалау және басқару Функции управления проектом

Функции управления проектом