- Operations management

Содержание

- 2. Chapter 16: Business costs Scale of Production and break-even analysis

- 3. Business costs All business activity involves some kind of cost. Managers need to think about because:

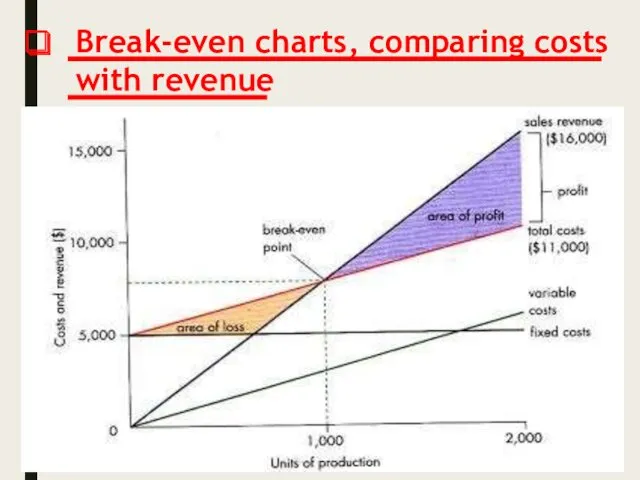

- 4. Break-even charts, comparing costs with revenue

- 5. Uses of break-even charts There are other benefits from the break-even chart other than identifying the

- 6. Disadvantages: The graph assumes that all goods produced are sold. Fixed costs will change if the

- 7. Break-even point: the calculation method. It is possible to calculate the breakeven point with ought having

- 8. Business costs: other definitions There are other types of costs to be analysed that is split

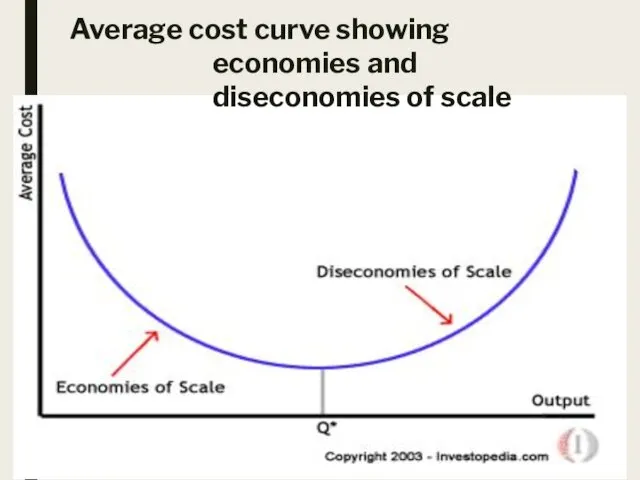

- 9. Economies and Diseconomies of scale: Economies of scale: are factors that lead to a reduction in

- 10. However, there are diseconomies of scale which increases average costs when a business grows: Poor communication:

- 11. Average cost curve showing economies and diseconomies of scale

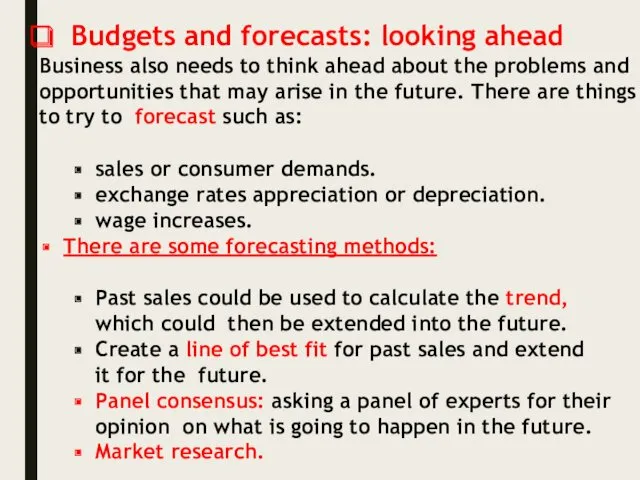

- 12. Budgets and forecasts: looking ahead Business also needs to think ahead about the problems and opportunities

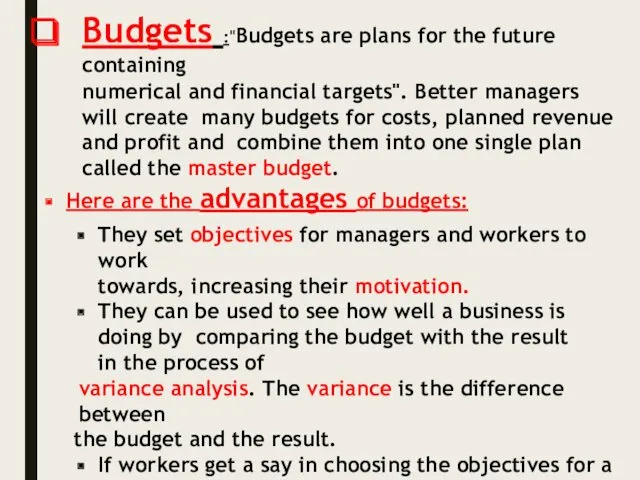

- 13. Budgets :"Budgets are plans for the future containing numerical and financial targets". Better managers will create

- 14. All in all, budgeting is useful for: reviewing past activities. controlling current business activity - following

- 15. 4.4 Chapter 18: Location decisions

- 16. Location of industry The location of a business is considered when it starts-up or when its

- 17. Market Need to be near to transport perishable goods. Need to be near to cut transportation

- 18. Availability of labour Wages of the labourers. How skilled they are. Government influence Grants/subsidies. Restrictions on

- 19. They like. Pleasant weather, etc… Climate E.g. to reduce heating costs in a warmer climate. Some

- 20. Customer parking available/nearby Convenience for the customer. Availability of suitable vacant premises Goods sites (e.g. in

- 21. Factors that influence a business to relocate either at home or abroad The present site is

- 22. Government grants To attract businesses to locate in development areas. To attract foreign investment. To bypass

- 23. Personal preference of owners Near their homes. Technology Technology allows businesses to locate in cheaper sites.

- 25. Скачать презентацию

Chapter 16: Business costs Scale of Production and break-even analysis

Chapter 16: Business costs Scale of Production and break-even analysis

Business costs

All business activity involves some kind of cost. Managers need

Business costs

All business activity involves some kind of cost. Managers need

Break-even charts, comparing costs with revenue

Break-even charts, comparing costs with revenue

Uses of break-even charts

There are other benefits from the break-even chart

Uses of break-even charts

There are other benefits from the break-even chart

Disadvantages:

The graph assumes that all goods produced are sold.

Fixed costs will

Disadvantages:

The graph assumes that all goods produced are sold.

Fixed costs will

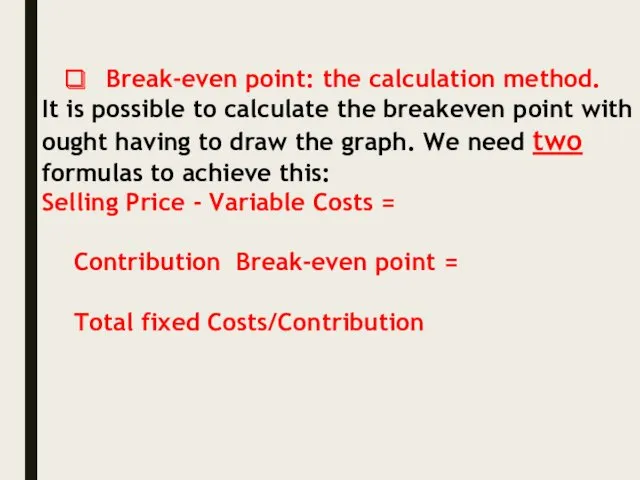

Break-even point: the calculation method.

It is possible to calculate the breakeven

Break-even point: the calculation method.

It is possible to calculate the breakeven

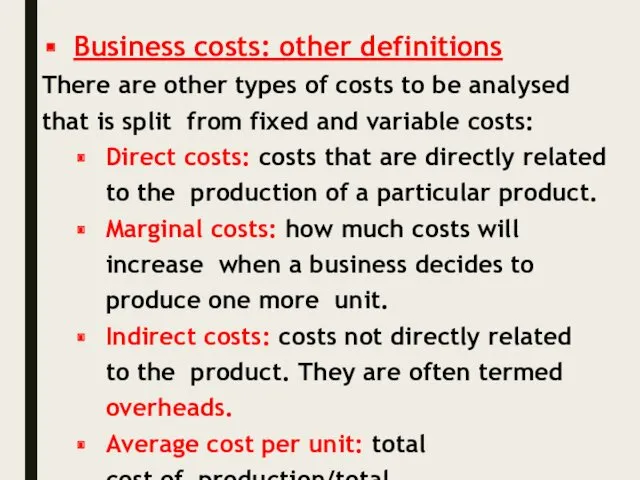

Business costs: other definitions

There are other types of costs to be

Business costs: other definitions

There are other types of costs to be

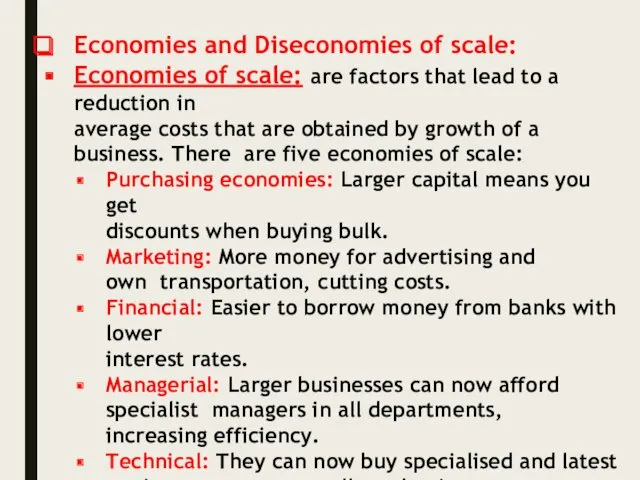

Economies and Diseconomies of scale:

Economies of scale: are factors that lead

Economies and Diseconomies of scale:

Economies of scale: are factors that lead

However, there are diseconomies of scale which increases average costs when

However, there are diseconomies of scale which increases average costs when

Average cost curve showing economies and diseconomies of scale

Average cost curve showing economies and diseconomies of scale

Budgets and forecasts: looking ahead

Business also needs to think ahead about

Budgets and forecasts: looking ahead

Business also needs to think ahead about

Budgets :"Budgets are plans for the future containing

numerical and financial targets".

Budgets :"Budgets are plans for the future containing

numerical and financial targets".

All in all, budgeting is useful for:

reviewing past activities.

controlling current business

All in all, budgeting is useful for:

reviewing past activities.

controlling current business

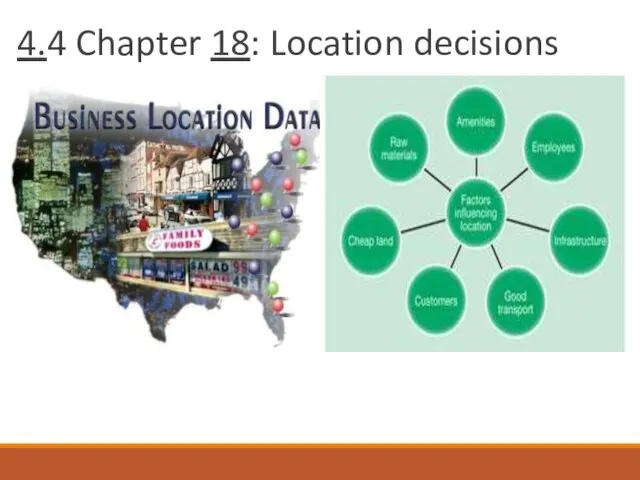

4.4 Chapter 18: Location decisions

4.4 Chapter 18: Location decisions

Location of industry

The location of a business is considered when it

Location of industry

The location of a business is considered when it

Market

Need to be near to transport perishable goods.

Need to be near

Market

Need to be near to transport perishable goods.

Need to be near

Availability of labour

Wages of the labourers.

How skilled they are.

Government influence

Grants/subsidies.

Restrictions on

Availability of labour

Wages of the labourers.

How skilled they are.

Government influence

Grants/subsidies.

Restrictions on

They like.

Pleasant weather, etc…

Climate

E.g. to reduce heating costs in a warmer

They like.

Pleasant weather, etc…

Climate

E.g. to reduce heating costs in a warmer

Customer parking available/nearby

Convenience for the customer.

Availability of suitable vacant premises

Goods sites

Customer parking available/nearby

Convenience for the customer.

Availability of suitable vacant premises

Goods sites

Factors that influence a business to relocate either at home or

Factors that influence a business to relocate either at home or

Government grants

To attract businesses to locate in development areas.

To attract foreign

Government grants

To attract businesses to locate in development areas.

To attract foreign

Personal preference of owners

Near their homes.

Technology

Technology allows businesses to locate in

Personal preference of owners

Near their homes.

Technology

Technology allows businesses to locate in

Коммуникативная культура в деловом общении

Коммуникативная культура в деловом общении Моделирование и оптимизация процессов и систем сервиса: понятия процесс и системы сервиса. Характеристика курса

Моделирование и оптимизация процессов и систем сервиса: понятия процесс и системы сервиса. Характеристика курса Структура организации. Внешняя и внутренняя среда организации

Структура организации. Внешняя и внутренняя среда организации МАИС. Методы активизации использования интуиции и опыта специалистов

МАИС. Методы активизации использования интуиции и опыта специалистов Процесс управленческого консультирования

Процесс управленческого консультирования Модели управления организационными изменениями

Модели управления организационными изменениями Функції соціально-культурного менеджменту та методи управління

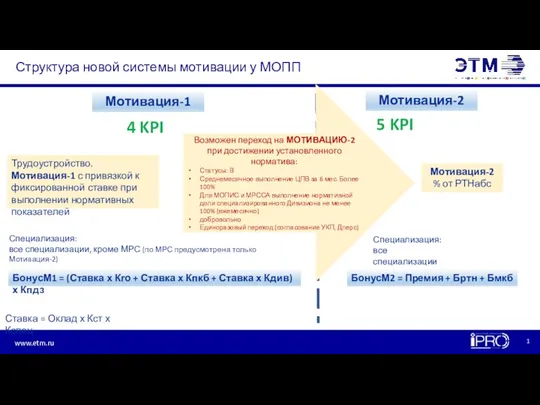

Функції соціально-культурного менеджменту та методи управління Структура новой системы мотивации у МОПП

Структура новой системы мотивации у МОПП Управление жизненным циклом организации. Анализ организационного поведения

Управление жизненным циклом организации. Анализ организационного поведения Definicja. Funkcje celu. Podejście do formułowania celu

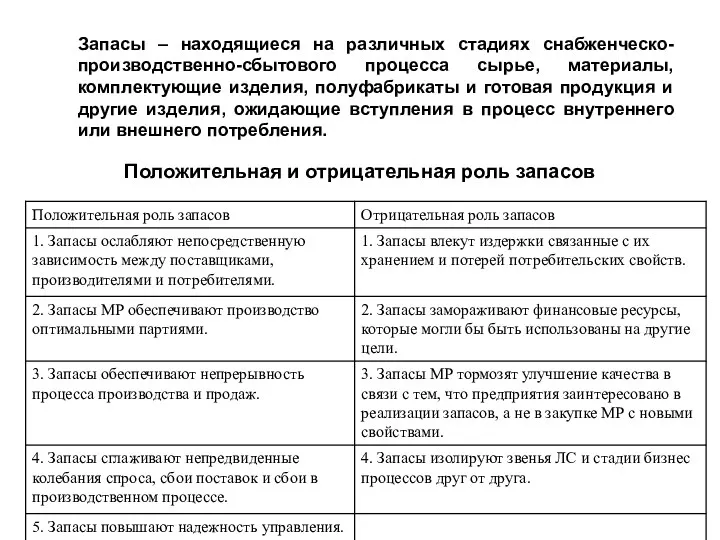

Definicja. Funkcje celu. Podejście do formułowania celu Положительная и отрицательная роль запасов. Модель управления запасами

Положительная и отрицательная роль запасов. Модель управления запасами Делегирование полномочий

Делегирование полномочий Маршутирование. 50 торговых точек на маршруте

Маршутирование. 50 торговых точек на маршруте Организация работ на проекте ПАО Россети Центр и ПАО Россети Центр и Приволжье

Организация работ на проекте ПАО Россети Центр и ПАО Россети Центр и Приволжье Социально-психологический климат в коллективе

Социально-психологический климат в коллективе Виды простых технических средств охраны и ограничения доступа

Виды простых технических средств охраны и ограничения доступа Совершенствование системы обучения персонала компании

Совершенствование системы обучения персонала компании Адаптация персонала

Адаптация персонала Статистическое изучение взаимосвязи

Статистическое изучение взаимосвязи Підвищення ефективності функціонування логістичної системи при використанні автомобільного і залізничного видів транспорту

Підвищення ефективності функціонування логістичної системи при використанні автомобільного і залізничного видів транспорту Методика проведения swot – анализа

Методика проведения swot – анализа Экономика и организация производства (общественное питание)

Экономика и организация производства (общественное питание) Менеджменттегі коммуникация

Менеджменттегі коммуникация Стратегиялық менеджмент түсінігі

Стратегиялық менеджмент түсінігі Нормирование труда на механизированных полевых работах

Нормирование труда на механизированных полевых работах Прогнозирование доходов. УЭФ-Л 10-11

Прогнозирование доходов. УЭФ-Л 10-11 Процессы инициации. Разработка паспорта проекта. Управление заинтересованными сторонами

Процессы инициации. Разработка паспорта проекта. Управление заинтересованными сторонами Служба управления персоналом

Служба управления персоналом