- Management: Arab World Edition Robbins, Coulter, Sidani, Jamali

Содержание

- 2. Management: Arab World Edition Robbins, Coulter, Sidani, Jamali Chapter 17: Introduction to Controlling Lecturer: [Insert your

- 3. 17.1 What Is Control and Why Is It Important? Define controlling. Discuss the reasons why control

- 4. 17.3 Controlling Organizational Performance Define organizational performance. Describe three most frequently used measures of organizational performance.

- 5. 17.5 Contemporary Issues in Control Describe how managers may have to adjust controls for cross-cultural differences.

- 6. What Is Control and Why Is It Important? 1. Define controlling. 2. Discuss the reasons why

- 7. What Is Control? Controlling The process of monitoring activities to ensure that they are being accomplished

- 8. Why Is Control Important? As the final link in management functions: Planning Controls let managers know

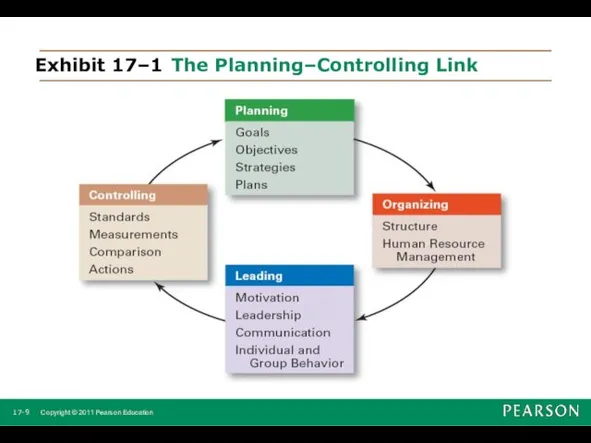

- 9. Exhibit 17–1 The Planning–Controlling Link 17- Copyright © 2011 Pearson Education

- 10. The Control Process 1. Describe the three steps in the control process. 2. Explain why what

- 11. The Control Process The Process of Control 1. Measuring actual performance 2. Comparing actual performance against

- 12. Exhibit 17–2 The Control Process 17- Copyright © 2011 Pearson Education

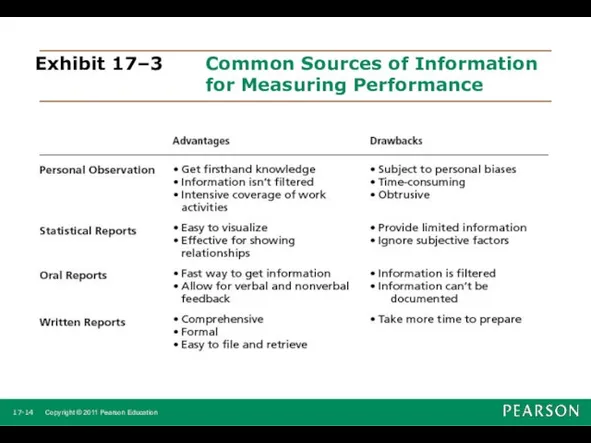

- 13. Step 1: Measuring How and What We Measure Sources of Information (How) Personal observation Statistical reports

- 14. Exhibit 17–3 Common Sources of Information for Measuring Performance 17- Copyright © 2011 Pearson Education

- 15. Step 2: Comparing Determining the degree of variation between actual performance and the standard. Significance of

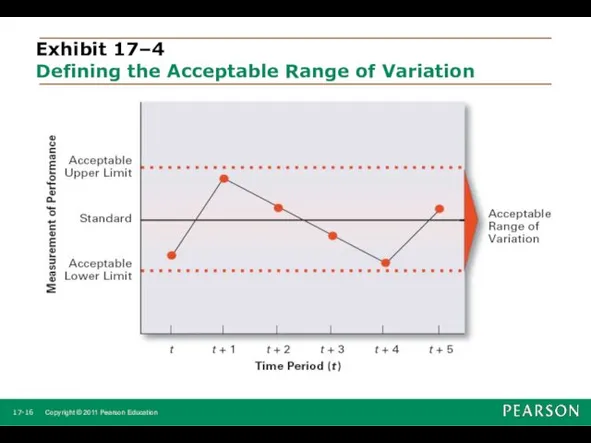

- 16. Exhibit 17–4 Defining the Acceptable Range of Variation 17- Copyright © 2011 Pearson Education

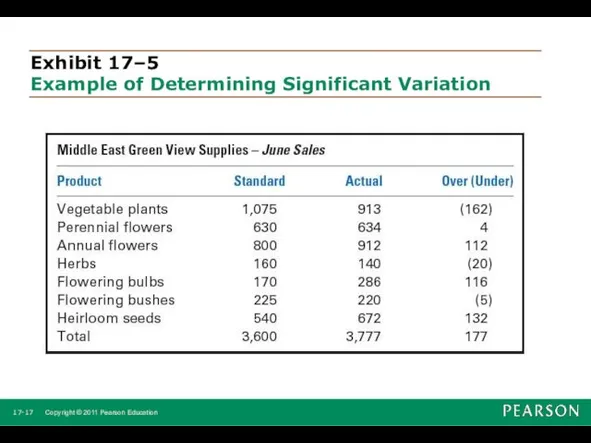

- 17. Exhibit 17–5 Example of Determining Significant Variation 17- Copyright © 2011 Pearson Education

- 18. Step 3: Taking Managerial Action Courses of Action “Doing nothing” Only if deviation is judged to

- 19. Courses of Action (cont’d) Revising the standard Examining the standard to ascertain whether or not the

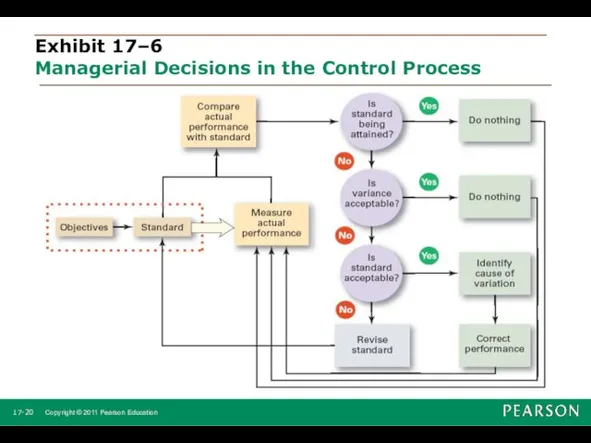

- 20. Exhibit 17–6 Managerial Decisions in the Control Process 17- Copyright © 2011 Pearson Education

- 21. Controlling Organizational Performance 1. Define organizational performance. 2. Describe three most frequently used measures of organizational

- 22. Controlling for Organizational Performance What Is Performance? The end result of an activity. What Is Organizational

- 23. Organizational Performance Measures Organizational Productivity Productivity: the overall output of goods and/or services divided by the

- 24. Organizational Effectiveness Measuring how appropriate organizational goals are and how well the organization is achieving its

- 25. Organizational Performance Measures Industry and Company Rankings Industry rankings on: Profits Return on revenue Return on

- 26. Exhibit 17–7 Some Popular Rankings in the Arab World 17- Copyright © 2011 Pearson Education

- 27. Tools for Measuring Organizational Performance 1. Contrast feedforward, concurrent, and feedback controls. 2. Explain the types

- 28. Feedforward, Concurrent, and Feedback Controls – 1 Feedforward Control A control that prevents anticipated problems before

- 29. Feedback Control A control that takes place after an activity is done. Corrective action is after-the-fact,

- 30. Exhibit 17–8 Types of Control 17- Copyright © 2011 Pearson Education

- 31. Financial Controls Traditional Controls Ratio analysis Liquidity Leverage Activity Profitability Budget Analysis Quantitative standards Deviations 17-

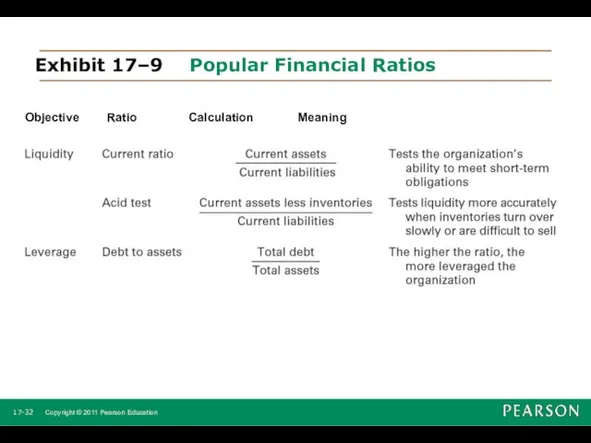

- 32. Exhibit 17–9 Popular Financial Ratios Objective Ratio Calculation Meaning 17- Copyright © 2011 Pearson Education

- 33. Exhibit 17–9 Popular Financial Ratios (cont’d) Objective Ratio Calculation Meaning 17- Copyright © 2011 Pearson Education

- 34. Managing Earnings “Timing” income and expenses to enhance current financial results, which gives an unrealistic picture

- 35. Balanced Scorecard Is a measurement tool that uses goals set by managers in four areas to

- 36. Information Controls Purposes of Information Controls As a tool to help managers control other organizational activities.

- 37. Management Information Systems (MIS) A system used to provide management with needed information on a regular

- 38. Benchmarking of Best Practices Benchmark The standard of excellence against which to measure and compare. Benchmarking

- 39. Exhibit 17-10 Suggestions for Internal Benchmarking 17- Copyright © 2011 Pearson Education

- 40. Contemporary Issues in Control 1. Describe how managers may have to adjust controls for cross-cultural differences.

- 41. Cross-Cultural Issues The use of technology to increase direct corporate control of local operations. Legal constraints

- 42. Workplace Concerns Workplace privacy versus workplace monitoring E-mail, telephone, computer, and Internet usage Productivity, harassment, security,

- 43. Exhibit 17–11 Controlling Employee Theft Sources: Based on A.H. Bell and D.M. Smith. “Protecting the Company

- 44. Exhibit 17–12 Workplace Violence Witnessed yelling or other verbal abuse 42% Yelled at co-workers themselves 29%

- 45. Exhibit 17–13 Controlling Workplace Violence Sources: Based on M. Gorkin, “Five Strategies and Structures for Reducing

- 46. Customer Interactions Service profit chain Is the service sequence from employees to customers to profit. Service

- 47. Corporate Governance The system used to govern a corporation so that the interests of the corporate

- 48. controlling market control bureaucratic control clan control control process range of variation immediate corrective action basic

- 49. management information system (MIS) data information balanced scorecard benchmarking employee theft service profit chain corporate governance

- 51. Скачать презентацию

Management: Arab World Edition

Robbins, Coulter, Sidani, Jamali

Chapter 17: Introduction to

Management: Arab World Edition

Robbins, Coulter, Sidani, Jamali

Chapter 17: Introduction to

17.1 What Is Control and Why Is It Important?

Define controlling.

Discuss the

17.1 What Is Control and Why Is It Important?

Define controlling.

Discuss the

17.3 Controlling Organizational Performance

Define organizational performance.

Describe three most frequently used measures

17.3 Controlling Organizational Performance

Define organizational performance.

Describe three most frequently used measures

17.5 Contemporary Issues in Control

Describe how managers may have to adjust

17.5 Contemporary Issues in Control

Describe how managers may have to adjust

What Is Control and Why Is It Important?

1. Define controlling.

2. Discuss

What Is Control and Why Is It Important?

1. Define controlling.

2. Discuss

What Is Control?

Controlling

The process of monitoring activities to ensure that they

What Is Control?

Controlling

The process of monitoring activities to ensure that they

Why Is Control Important?

As the final link in management functions:

Planning

Controls let

Why Is Control Important?

As the final link in management functions:

Planning

Controls let

Exhibit 17–1 The Planning–Controlling Link

17- Copyright © 2011 Pearson Education

Exhibit 17–1 The Planning–Controlling Link

17- Copyright © 2011 Pearson Education

The Control Process

1. Describe the three steps in the control process.

2. Explain why

The Control Process

1. Describe the three steps in the control process.

2. Explain why

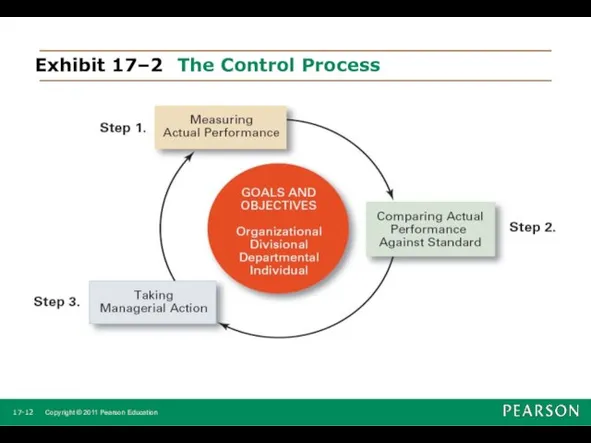

The Control Process

The Process of Control

1. Measuring actual performance

2. Comparing actual performance against

The Control Process

The Process of Control

1. Measuring actual performance

2. Comparing actual performance against

Exhibit 17–2 The Control Process

17- Copyright © 2011 Pearson Education

Exhibit 17–2 The Control Process

17- Copyright © 2011 Pearson Education

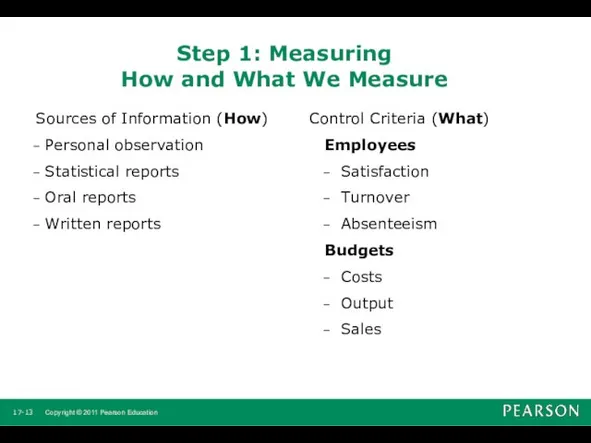

Step 1: Measuring

How and What We Measure

Sources of Information (How)

Personal

Step 1: Measuring

How and What We Measure

Sources of Information (How)

Personal

Exhibit 17–3 Common Sources of Information for Measuring Performance

17- Copyright © 2011

Exhibit 17–3 Common Sources of Information for Measuring Performance

17- Copyright © 2011

Step 2: Comparing

Determining the degree of variation between actual performance and

Step 2: Comparing

Determining the degree of variation between actual performance and

Exhibit 17–4

Defining the Acceptable Range of Variation

17- Copyright © 2011

Exhibit 17–4

Defining the Acceptable Range of Variation

17- Copyright © 2011

Exhibit 17–5

Example of Determining Significant Variation

17- Copyright © 2011 Pearson

Exhibit 17–5

Example of Determining Significant Variation

17- Copyright © 2011 Pearson

Step 3: Taking Managerial Action

Courses of Action

“Doing nothing”

Only if deviation is

Step 3: Taking Managerial Action

Courses of Action

“Doing nothing”

Only if deviation is

Courses of Action (cont’d)

Revising the standard

Examining the standard to ascertain whether

Courses of Action (cont’d)

Revising the standard

Examining the standard to ascertain whether

Exhibit 17–6

Managerial Decisions in the Control Process

17- Copyright © 2011

Exhibit 17–6

Managerial Decisions in the Control Process

17- Copyright © 2011

Controlling Organizational Performance

1. Define organizational performance.

2. Describe three most frequently used measures of

Controlling Organizational Performance

1. Define organizational performance.

2. Describe three most frequently used measures of

Controlling for Organizational Performance

What Is Performance?

The end result of an activity.

What

Controlling for Organizational Performance

What Is Performance?

The end result of an activity.

What

Organizational Performance Measures

Organizational Productivity

Productivity: the overall output of goods and/or

Organizational Performance Measures

Organizational Productivity

Productivity: the overall output of goods and/or

Organizational Effectiveness

Measuring how appropriate organizational goals are and how well the

Organizational Effectiveness

Measuring how appropriate organizational goals are and how well the

Organizational Performance Measures

Industry and Company Rankings

Industry rankings on:

Profits

Return on revenue

Return on

Organizational Performance Measures

Industry and Company Rankings

Industry rankings on:

Profits

Return on revenue

Return on

Exhibit 17–7

Some Popular Rankings in the Arab World

17- Copyright ©

Exhibit 17–7

Some Popular Rankings in the Arab World

17- Copyright ©

Tools for Measuring Organizational Performance

1. Contrast feedforward, concurrent, and feedback controls.

2. Explain the

Tools for Measuring Organizational Performance

1. Contrast feedforward, concurrent, and feedback controls.

2. Explain the

Feedforward, Concurrent, and Feedback Controls – 1

Feedforward Control

A control that

Feedforward, Concurrent, and Feedback Controls – 1

Feedforward Control

A control that

Feedback Control

A control that takes place after an activity is done.

Corrective

Feedback Control

A control that takes place after an activity is done.

Corrective

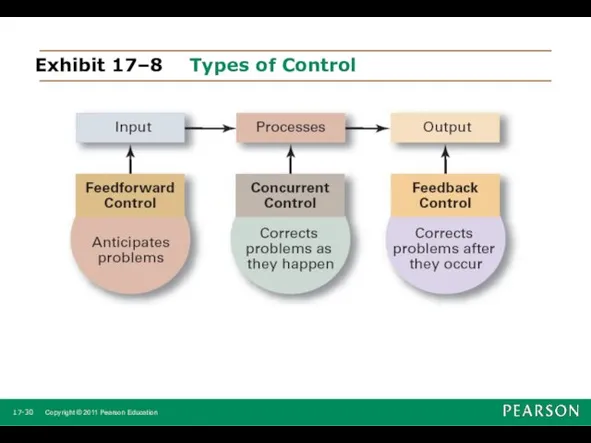

Exhibit 17–8 Types of Control

17- Copyright © 2011 Pearson Education

Exhibit 17–8 Types of Control

17- Copyright © 2011 Pearson Education

Financial Controls

Traditional Controls

Ratio analysis

Liquidity

Leverage

Activity

Profitability

Budget Analysis

Quantitative standards

Deviations

17- Copyright © 2011 Pearson Education

Financial Controls

Traditional Controls

Ratio analysis

Liquidity

Leverage

Activity

Profitability

Budget Analysis

Quantitative standards

Deviations

17- Copyright © 2011 Pearson Education

Exhibit 17–9 Popular Financial Ratios

Objective Ratio Calculation Meaning

17- Copyright © 2011 Pearson Education

Exhibit 17–9 Popular Financial Ratios

Objective Ratio Calculation Meaning

17- Copyright © 2011 Pearson Education

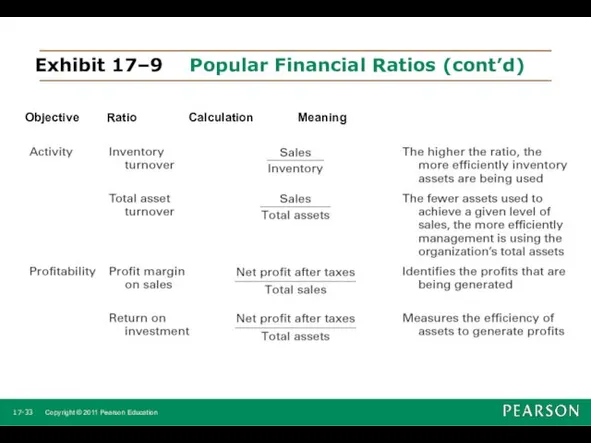

Exhibit 17–9 Popular Financial Ratios (cont’d)

Objective Ratio Calculation Meaning

17- Copyright © 2011 Pearson Education

Exhibit 17–9 Popular Financial Ratios (cont’d)

Objective Ratio Calculation Meaning

17- Copyright © 2011 Pearson Education

Managing Earnings

“Timing” income and expenses to enhance current financial results, which

Managing Earnings

“Timing” income and expenses to enhance current financial results, which

Balanced Scorecard

Is a measurement tool that uses goals set by managers

Balanced Scorecard

Is a measurement tool that uses goals set by managers

Information Controls

Purposes of Information Controls

As a tool to help managers control

Information Controls

Purposes of Information Controls

As a tool to help managers control

Management Information Systems (MIS)

A system used to provide management with needed

Management Information Systems (MIS)

A system used to provide management with needed

Benchmarking of Best Practices

Benchmark

The standard of excellence against which to measure

Benchmarking of Best Practices

Benchmark

The standard of excellence against which to measure

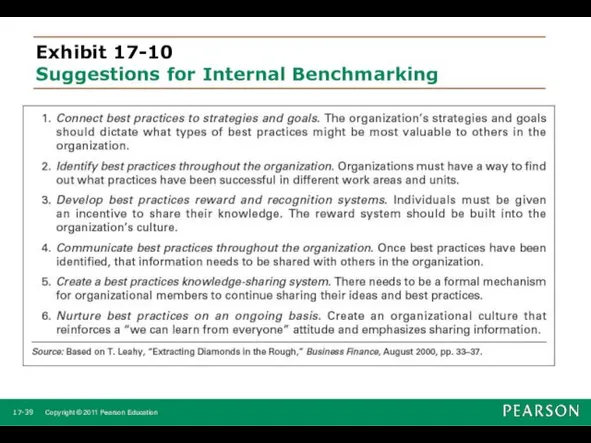

Exhibit 17-10

Suggestions for Internal Benchmarking

17- Copyright © 2011 Pearson Education

Exhibit 17-10

Suggestions for Internal Benchmarking

17- Copyright © 2011 Pearson Education

Contemporary Issues in Control

1. Describe how managers may have to adjust controls

Contemporary Issues in Control

1. Describe how managers may have to adjust controls

Cross-Cultural Issues

The use of technology to increase direct corporate control of

Cross-Cultural Issues

The use of technology to increase direct corporate control of

Workplace Concerns

Workplace privacy versus workplace monitoring

E-mail, telephone, computer, and Internet usage

Productivity,

Workplace Concerns

Workplace privacy versus workplace monitoring

E-mail, telephone, computer, and Internet usage

Productivity,

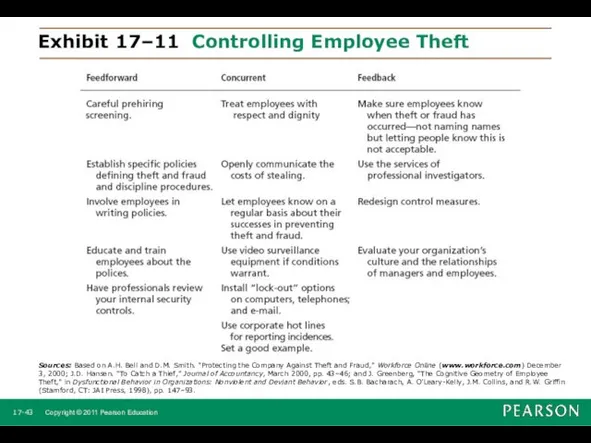

Exhibit 17–11 Controlling Employee Theft

Sources: Based on A.H. Bell and D.M.

Exhibit 17–11 Controlling Employee Theft

Sources: Based on A.H. Bell and D.M.

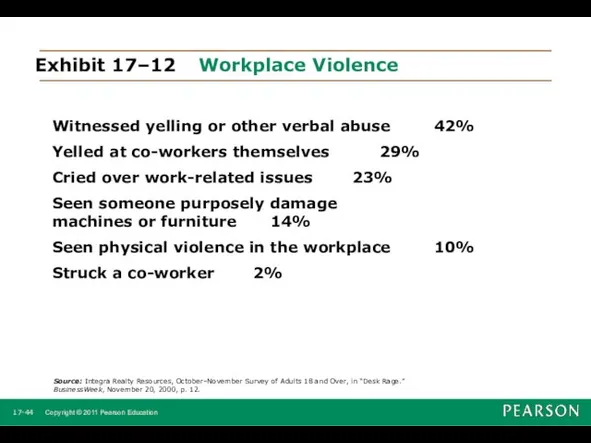

Exhibit 17–12 Workplace Violence

Witnessed yelling or other verbal abuse 42%

Yelled at co-workers themselves 29%

Cried

Exhibit 17–12 Workplace Violence

Witnessed yelling or other verbal abuse 42%

Yelled at co-workers themselves 29%

Cried

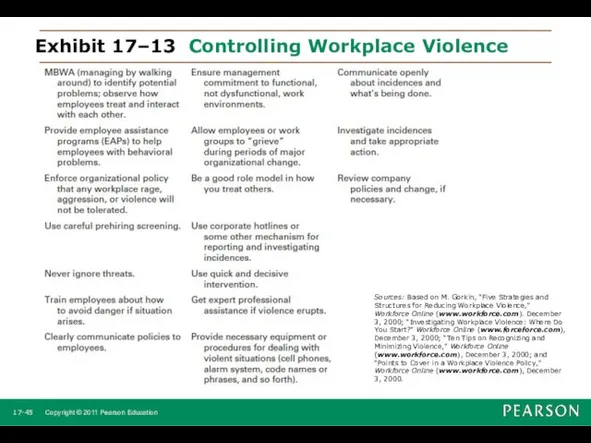

Exhibit 17–13 Controlling Workplace Violence

Sources: Based on M. Gorkin, “Five Strategies

Exhibit 17–13 Controlling Workplace Violence

Sources: Based on M. Gorkin, “Five Strategies

Customer Interactions

Service profit chain

Is the service sequence from employees to customers

Customer Interactions

Service profit chain

Is the service sequence from employees to customers

Corporate Governance

The system used to govern a corporation so that the

Corporate Governance

The system used to govern a corporation so that the

controlling

market control

bureaucratic control

clan control

control process

range of variation

immediate corrective action

basic corrective action

performance

organizational

controlling

market control

bureaucratic control

clan control

control process

range of variation

immediate corrective action

basic corrective action

performance

organizational

management information system (MIS)

data

information

balanced scorecard

benchmarking

employee theft

service profit chain

corporate governance

Terms to Know

management information system (MIS)

data

information

balanced scorecard

benchmarking

employee theft

service profit chain

corporate governance

Terms to Know

Презентация С днём рождения, Тула!

Презентация С днём рождения, Тула! Защита магистерской диссертации. (Лекция 8)

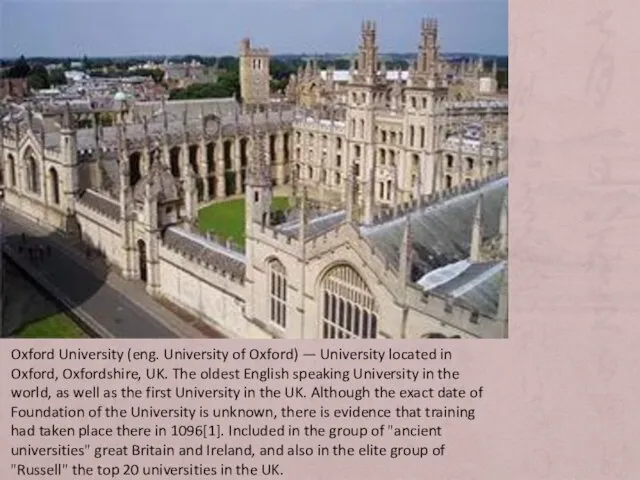

Защита магистерской диссертации. (Лекция 8) Oxford University

Oxford University Пути повышения качества обученности школьников

Пути повышения качества обученности школьников Современный урок в контексте требований ФГОС

Современный урок в контексте требований ФГОС Всероссийский конкурс для школьников Большая перемена

Всероссийский конкурс для школьников Большая перемена Отчет о прохождении учебной практики (практики по получению первичных профессиональных умений и навыков)

Отчет о прохождении учебной практики (практики по получению первичных профессиональных умений и навыков) Специальность Товароведение и экспертиза качества потребительских товаров

Специальность Товароведение и экспертиза качества потребительских товаров КИМы как источники информационного материала

КИМы как источники информационного материала Оксфордский университет. University of Oxford

Оксфордский университет. University of Oxford Федеральное законодательство в области образования обучающихся с ограниченными возможностями здоровья

Федеральное законодательство в области образования обучающихся с ограниченными возможностями здоровья Профильные смены 2021 год

Профильные смены 2021 год Целевая программа мониторинга результатов образовательной деятельности

Целевая программа мониторинга результатов образовательной деятельности Методология научного исследования

Методология научного исследования Московский Государственный Институт Индустрии Туризма имени Ю.А. Сенкевича

Московский Государственный Институт Индустрии Туризма имени Ю.А. Сенкевича Структура книги

Структура книги Рейтинговая технология оценивания знаний учащихся

Рейтинговая технология оценивания знаний учащихся Научное познание. Наука как система знаний и вид духовного производства

Научное познание. Наука как система знаний и вид духовного производства МАИ – ведущий аэрокосмический вуз России с 20 марта 1930

МАИ – ведущий аэрокосмический вуз России с 20 марта 1930 Использование УМК в режимных моментах с детьми старшего дошкольного возраста

Использование УМК в режимных моментах с детьми старшего дошкольного возраста Оформление выпускной квалификационной работы

Оформление выпускной квалификационной работы Презентация Трудные родители.

Презентация Трудные родители. Подготовка к написанию сжатого изложения. ОГЭ 2015

Подготовка к написанию сжатого изложения. ОГЭ 2015 Школы с инновационным пространством

Школы с инновационным пространством Проектная деятельность учащихся. 5-9 классы

Проектная деятельность учащихся. 5-9 классы Система критериального оценивания учебных достижений учащихся

Система критериального оценивания учебных достижений учащихся презентация Изучение уравнений и неравенств в школьном курсе математики

презентация Изучение уравнений и неравенств в школьном курсе математики Растения родного края озера Байкал

Растения родного края озера Байкал