- Opertive controlling for the students

Содержание

- 2. LECTURE OPERATIVE CONTROLLING PLAN 1. TYPES OF CONTROLLING AND DIFFERENCES BETWEEN THEM. 2. NECESSITY AND THE

- 4. The objective of strategic controlling is to ensure the survival of a company and to track

- 5. Strategic controlling tools are: Balanced scoreboard and managing costs during the life-cycle Portfolio analysis of directions

- 6. The objective of operative controlling is to create a system of managing the achievement of current

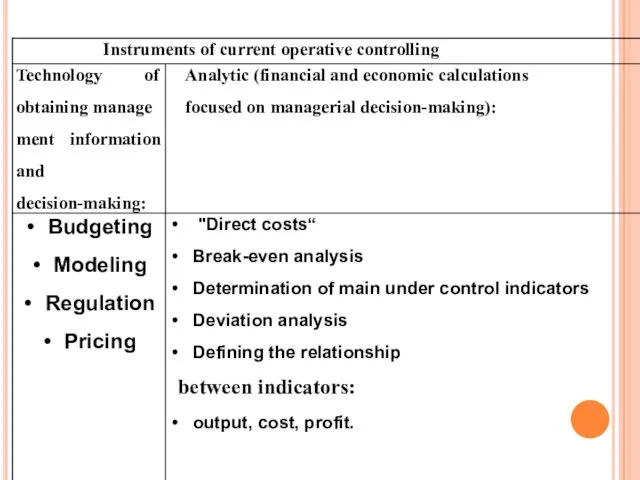

- 7. Operative controlling tools are managerial accounting and a budgeting system. Managerial accounting considers requirements to organizing

- 10. The purpose of operational controlling - formation of the system of control to perform current tasks

- 11. The goals of controlling system: a) General 1. efficiency (liquidity) 2. performance 3. profitability в) Subjectiv

- 12. The formal part of the controlling includes: 1. Cost reduction 2. Increase of labor productivity 3.

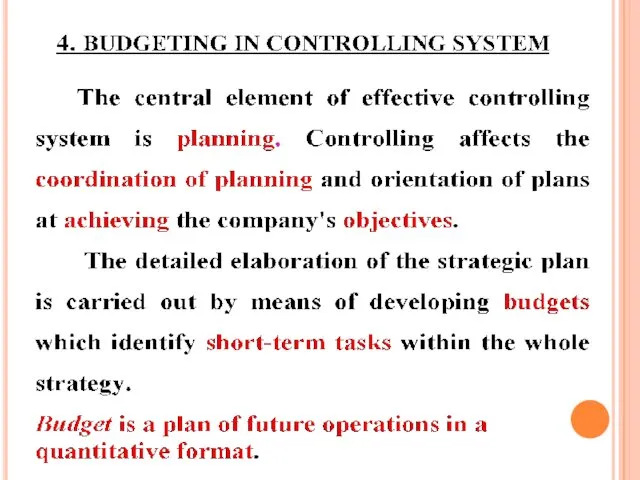

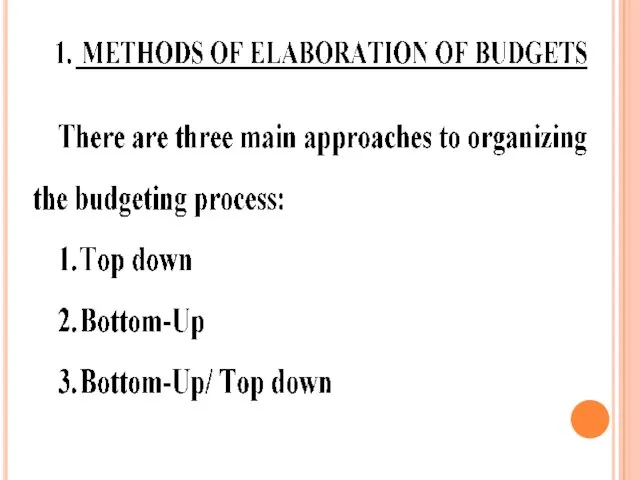

- 13. 3. Planification of tasks of enterprise. Instruments of controlling. Operational planning covers, usually one year. It

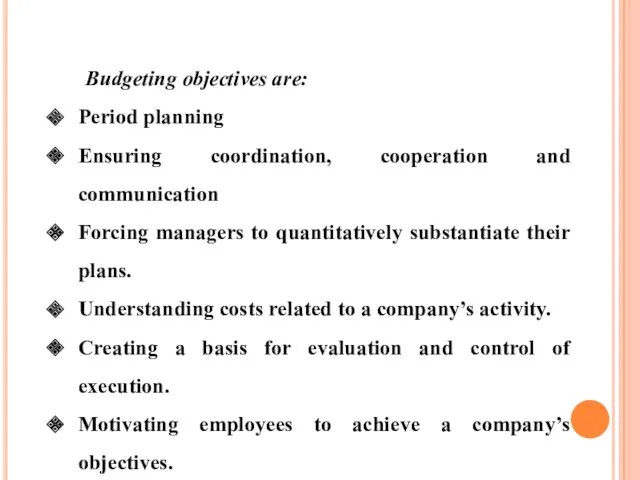

- 17. Budgeting objectives are: Period planning Ensuring coordination, cooperation and communication Forcing managers to quantitatively substantiate their

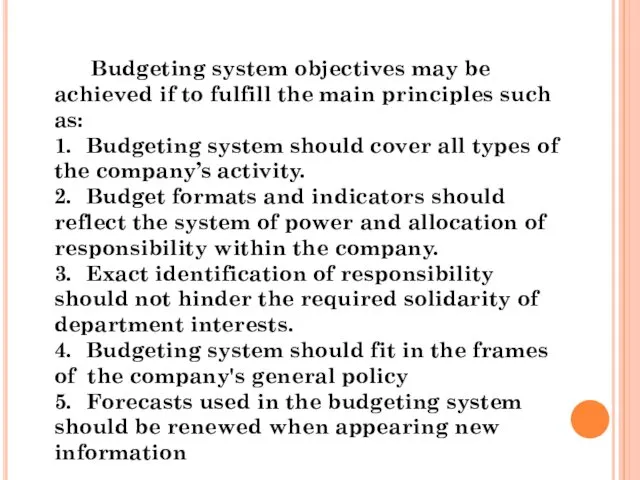

- 18. Budgeting system objectives may be achieved if to fulfill the main principles such as: 1. Budgeting

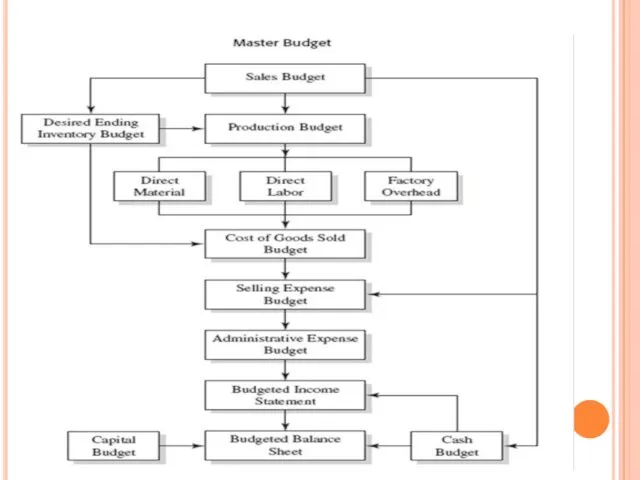

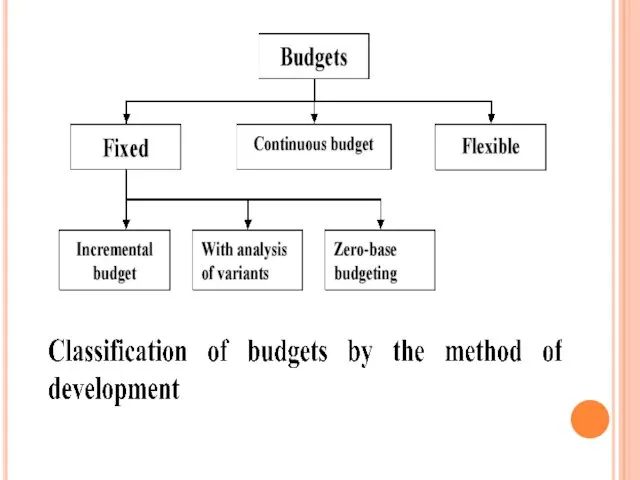

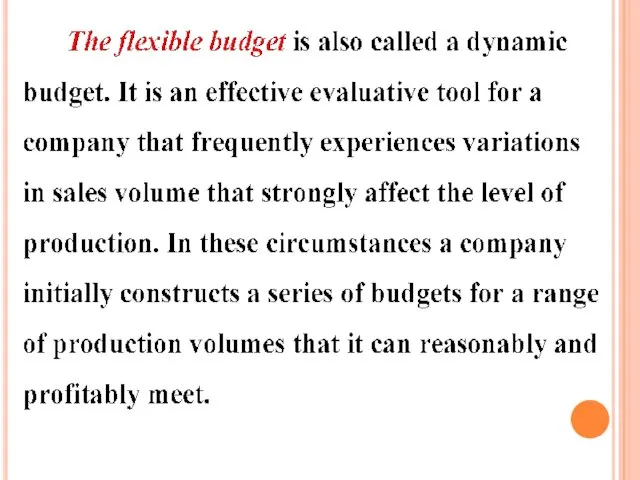

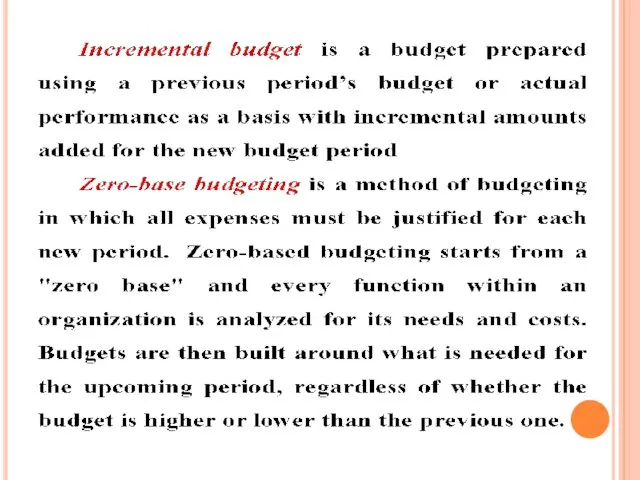

- 19. 5. TYPES OF BUDGETS AND THEIR CHARACTERISTIC Depending on the purpose it is possible to identify

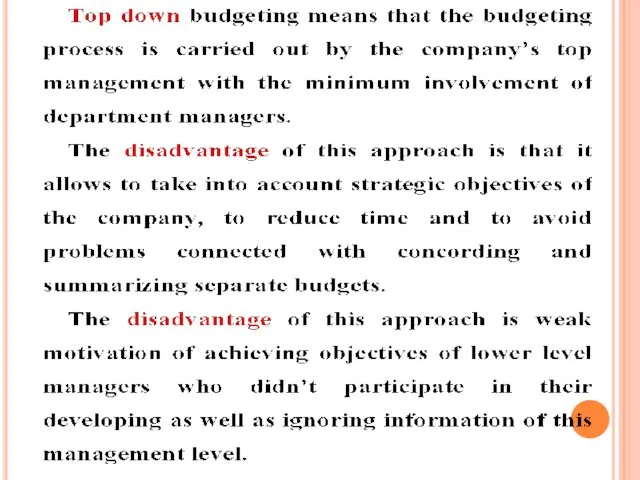

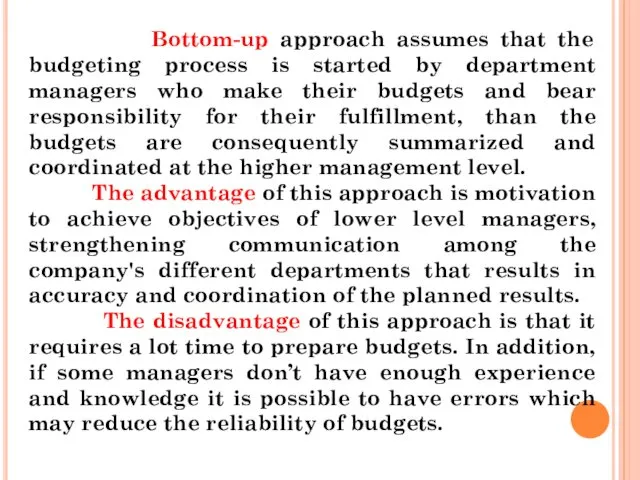

- 27. Bottom-up approach assumes that the budgeting process is started by department managers who make their budgets

- 29. Скачать презентацию

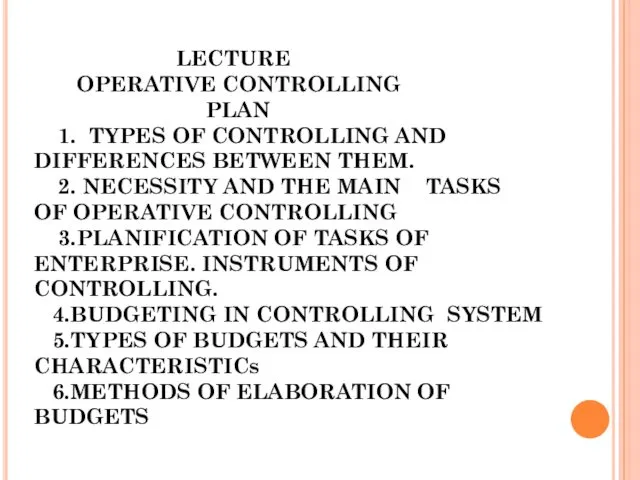

LECTURE

OPERATIVE CONTROLLING

PLAN

1. TYPES OF CONTROLLING AND DIFFERENCES

LECTURE

OPERATIVE CONTROLLING

PLAN

1. TYPES OF CONTROLLING AND DIFFERENCES

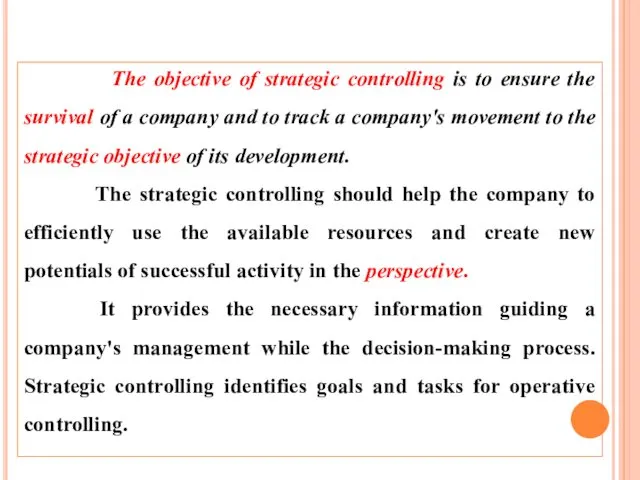

The objective of strategic controlling is to ensure the survival

The objective of strategic controlling is to ensure the survival

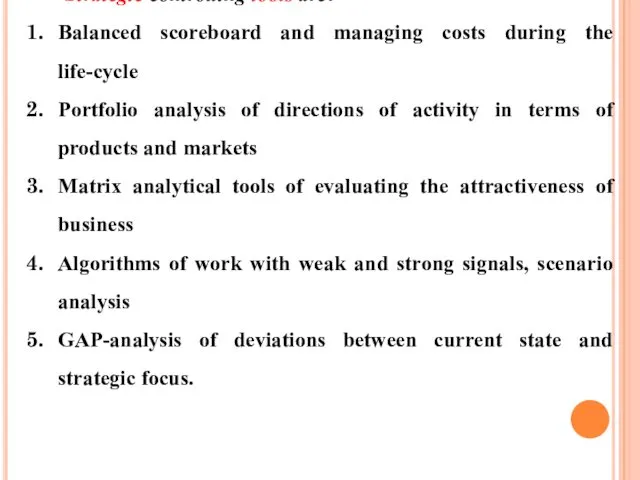

Strategic controlling tools are:

Balanced scoreboard and managing costs during the life-cycle

Portfolio

Strategic controlling tools are:

Balanced scoreboard and managing costs during the life-cycle

Portfolio

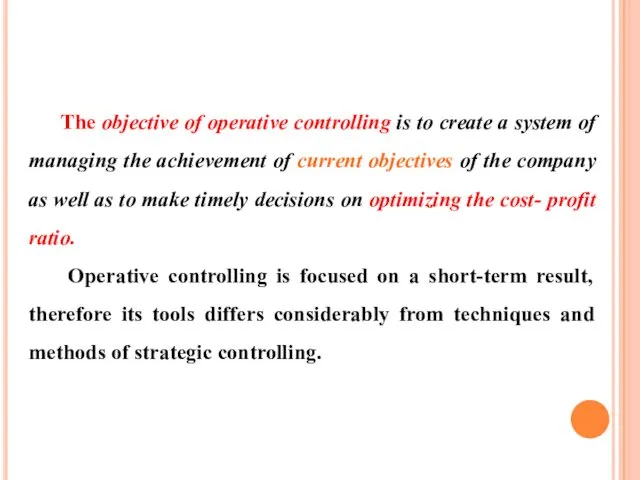

The objective of operative controlling is to create a system of

The objective of operative controlling is to create a system of

Operative controlling tools are managerial accounting and a budgeting system.

Managerial

Operative controlling tools are managerial accounting and a budgeting system.

Managerial

The purpose of operational controlling - formation of the system

The purpose of operational controlling - formation of the system

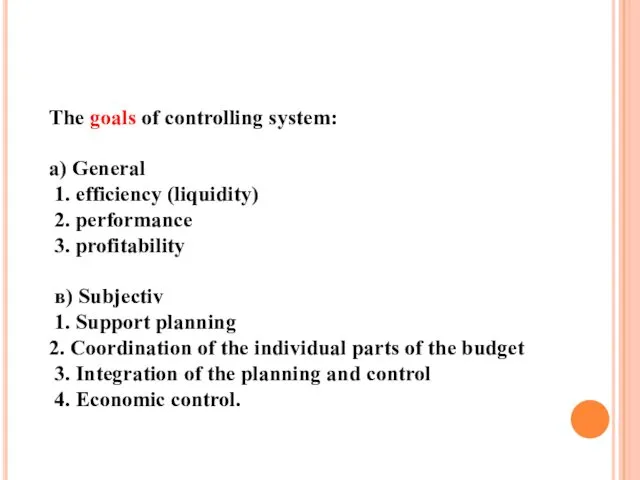

The goals of controlling system:

a) General

1. efficiency (liquidity)

2.

The goals of controlling system:

a) General

1. efficiency (liquidity)

2.

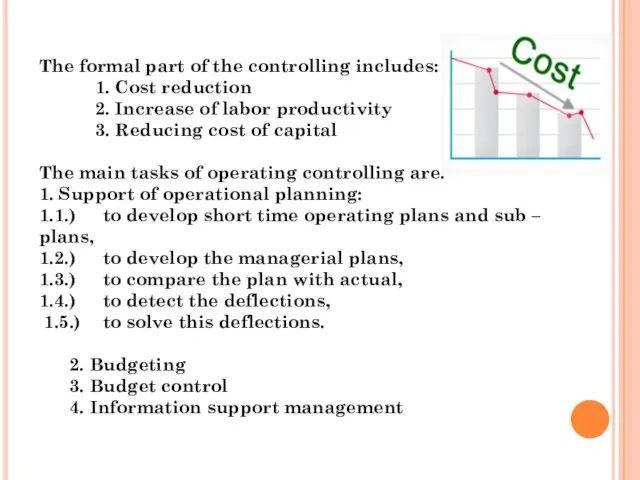

The formal part of the controlling includes:

1. Cost reduction

The formal part of the controlling includes:

1. Cost reduction

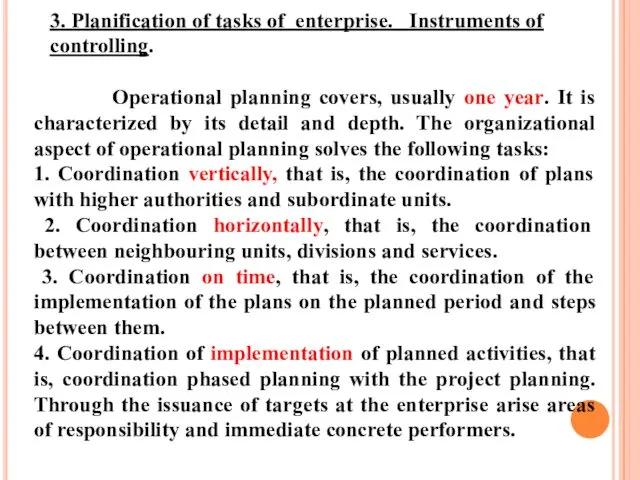

3. Planification of tasks of enterprise. Instruments of controlling.

Operational planning covers,

3. Planification of tasks of enterprise. Instruments of controlling.

Operational planning covers,

Budgeting objectives are:

Period planning

Ensuring coordination, cooperation and communication

Forcing managers to quantitatively

Budgeting objectives are:

Period planning

Ensuring coordination, cooperation and communication

Forcing managers to quantitatively

Budgeting system objectives may be achieved if to fulfill the

Budgeting system objectives may be achieved if to fulfill the

5. TYPES OF BUDGETS AND THEIR CHARACTERISTIC

Depending on the purpose it

Depending on the purpose it

Bottom-up approach assumes that the budgeting process is started by

Bottom-up approach assumes that the budgeting process is started by

Ходьба и бег (1-4 класс)

Ходьба и бег (1-4 класс) Внеклассное мероприятие по математике в 6-ых классах по теме Математический ринг

Внеклассное мероприятие по математике в 6-ых классах по теме Математический ринг Поле чудес

Поле чудес Мастерство работника. Профессиональные знания, квалификация

Мастерство работника. Профессиональные знания, квалификация Урок Золотое правило нравственности

Урок Золотое правило нравственности Семейное древо профессий моей семьи

Семейное древо профессий моей семьи Презентация Курительные смеси

Презентация Курительные смеси Внеклассное мероприятие Конституция России – основной закон нашей страны

Внеклассное мероприятие Конституция России – основной закон нашей страны Профилактика жестокого обращения с детьми

Профилактика жестокого обращения с детьми Классный час СПИД -смертельная угроза человечеству.

Классный час СПИД -смертельная угроза человечеству. Мир вокруг нас

Мир вокруг нас Презентация Пионеры -герои

Презентация Пионеры -герои Творческий подход к изучению иностранного языка как один из способов реализации индивидуального подхода в обучении

Творческий подход к изучению иностранного языка как один из способов реализации индивидуального подхода в обучении Методика организации групповой работы на уроках математики в начальной школе

Методика организации групповой работы на уроках математики в начальной школе Дошкольная педагогика как отрасль педагогической науки

Дошкольная педагогика как отрасль педагогической науки Презентация к классному часу в 6 классе на тему: Новый год.

Презентация к классному часу в 6 классе на тему: Новый год. Формирование здорового образа жизни у младших школьников посредством проведения тематических классных часов

Формирование здорового образа жизни у младших школьников посредством проведения тематических классных часов тема Детская агрессия

тема Детская агрессия Педагогическая деятельность

Педагогическая деятельность Сынып бөлмесін, сынып мүліктерін бүлдірмей ұста

Сынып бөлмесін, сынып мүліктерін бүлдірмей ұста Кто в доме хозяин. Лучшая подростковая трудовая бригада 2018 г. МБУ РМ МПК Единство Михневский сектор

Кто в доме хозяин. Лучшая подростковая трудовая бригада 2018 г. МБУ РМ МПК Единство Михневский сектор Патріотичне виховання в початкових класах

Патріотичне виховання в початкових класах Классный час Из камня его гимнастерка

Классный час Из камня его гимнастерка Роботостроение своими руками

Роботостроение своими руками Наглядное моделирование, как средство развития связной устной речи старших дошкольников с тяжёлыми нарушениями речи

Наглядное моделирование, как средство развития связной устной речи старших дошкольников с тяжёлыми нарушениями речи Проблема и авторская позиция в тексте

Проблема и авторская позиция в тексте Предупреждение и устранение дислексии через систему педагогических игр и игровых упражнений у младших школьников с речевыми нарушениями.

Предупреждение и устранение дислексии через систему педагогических игр и игровых упражнений у младших школьников с речевыми нарушениями. Информационно-образовательный портал Лаборатория юного инженера как средство развития технической одаренности детей

Информационно-образовательный портал Лаборатория юного инженера как средство развития технической одаренности детей