- Firm behavior and the organization of industry. The costs of production

Содержание

- 2. 13 The Costs of Production

- 3. The Market Forces of Supply and Demand Supply and demand are the two words that economists

- 4. WHAT ARE COSTS? According to the Law of Supply: Firms are willing to produce and sell

- 5. WHAT ARE COSTS? The Firm’s Objective The economic goal of the firm is to maximize profits.

- 6. Total Revenue, Total Cost, and Profit Total Revenue The amount a firm receives for the sale

- 7. Total Revenue, Total Cost, and Profit Profit is the firm’s total revenue minus its total cost.

- 8. Costs as Opportunity Costs A firm’s cost of production includes all the opportunity costs of making

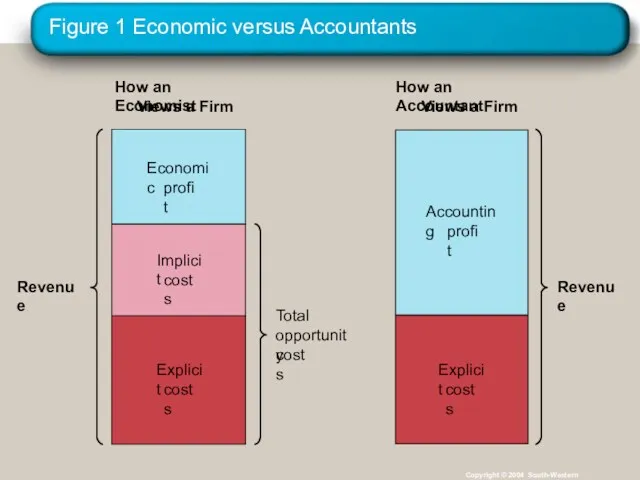

- 9. Economic Profit versus Accounting Profit Economists measure a firm’s economic profit as total revenue minus total

- 10. Economic Profit versus Accounting Profit When total revenue exceeds both explicit and implicit costs, the firm

- 11. Figure 1 Economic versus Accountants Copyright © 2004 South-Western How an Economist Views a Firm How

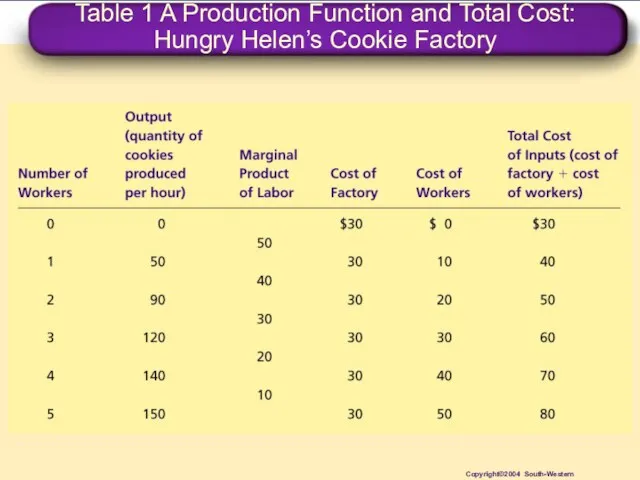

- 12. Table 1 A Production Function and Total Cost: Hungry Helen’s Cookie Factory Copyright©2004 South-Western

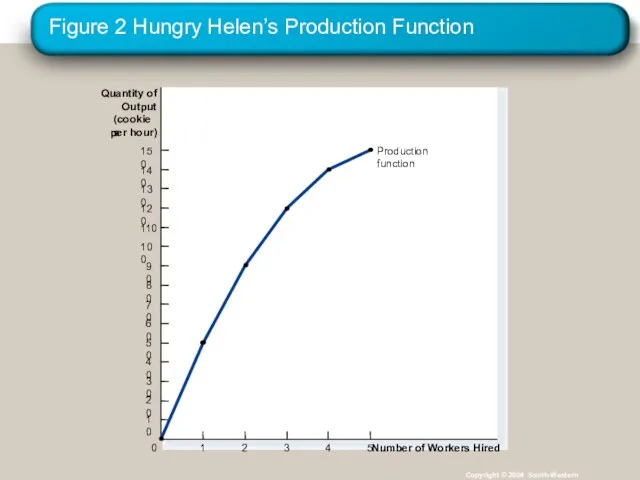

- 13. PRODUCTION AND COSTS The Production Function The production function shows the relationship between quantity of inputs

- 14. The Production Function Marginal Product The marginal product of any input in the production process is

- 15. The Production Function Diminishing Marginal Product Diminishing marginal product is the property whereby the marginal product

- 16. Figure 2 Hungry Helen’s Production Function Copyright © 2004 South-Western Quantity of Output (cookies per hour)

- 17. The Production Function Diminishing Marginal Product The slope of the production function measures the marginal product

- 18. From the Production Function to the Total-Cost Curve The relationship between the quantity a firm can

- 19. Table 1 A Production Function and Total Cost: Hungry Helen’s Cookie Factory Copyright©2004 South-Western

- 20. Figure 3 Hungry Helen’s Total-Cost Curve Copyright © 2004 South-Western Total Cost $80 70 60 50

- 21. THE VARIOUS MEASURES OF COST Costs of production may be divided into fixed costs and variable

- 22. Fixed and Variable Costs Fixed costs are those costs that do not vary with the quantity

- 23. Fixed and Variable Costs Total Costs Total Fixed Costs (TFC) Total Variable Costs (TVC) Total Costs

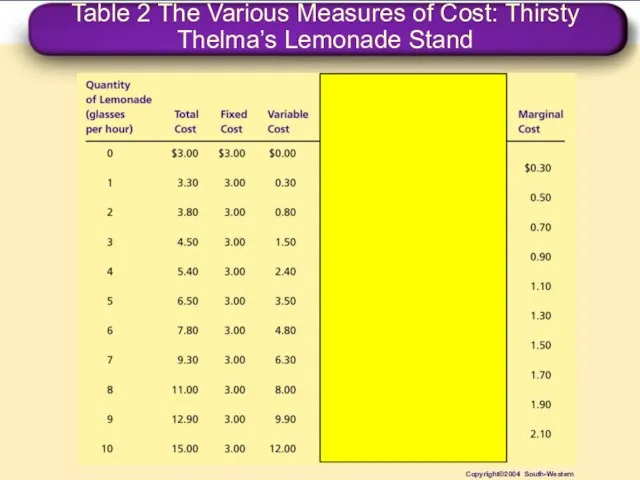

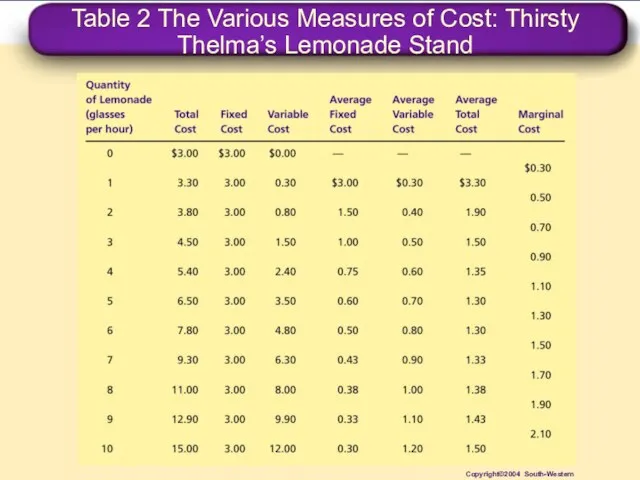

- 24. Table 2 The Various Measures of Cost: Thirsty Thelma’s Lemonade Stand Copyright©2004 South-Western

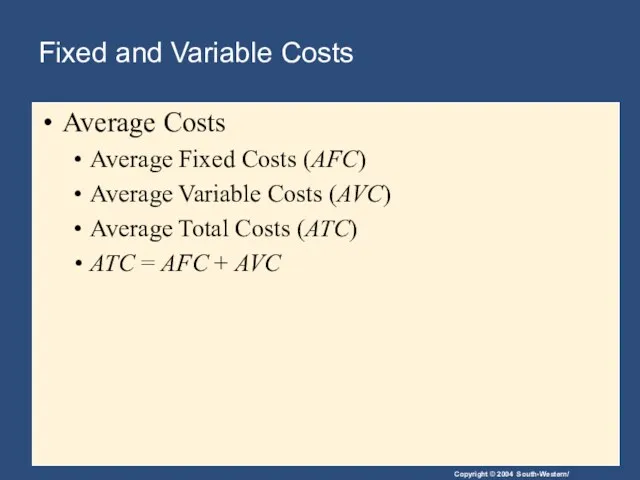

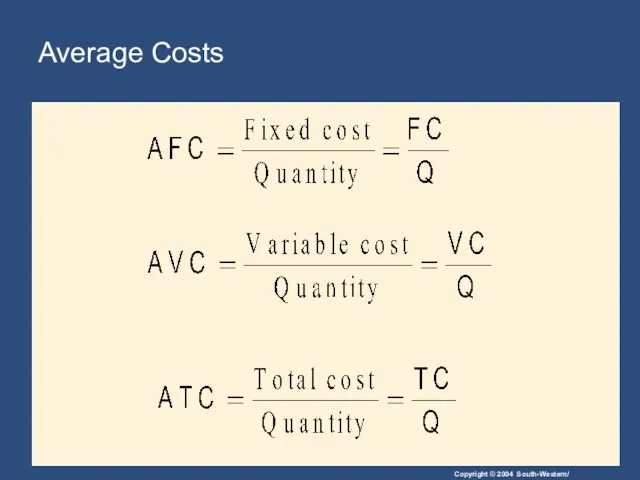

- 25. Fixed and Variable Costs Average Costs Average costs can be determined by dividing the firm’s costs

- 26. Fixed and Variable Costs Average Costs Average Fixed Costs (AFC) Average Variable Costs (AVC) Average Total

- 27. Average Costs

- 28. Table 2 The Various Measures of Cost: Thirsty Thelma’s Lemonade Stand Copyright©2004 South-Western

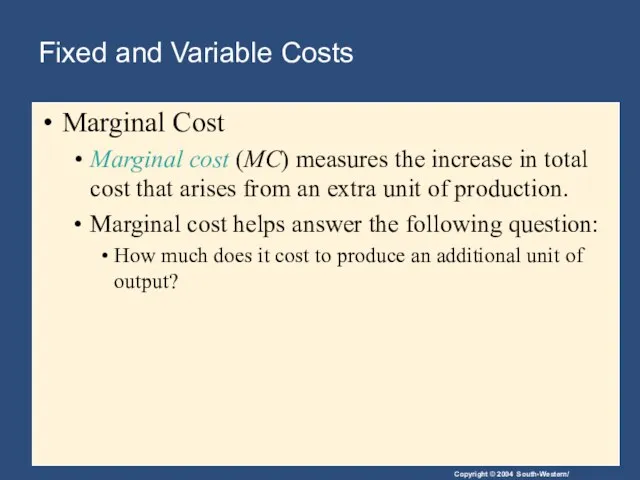

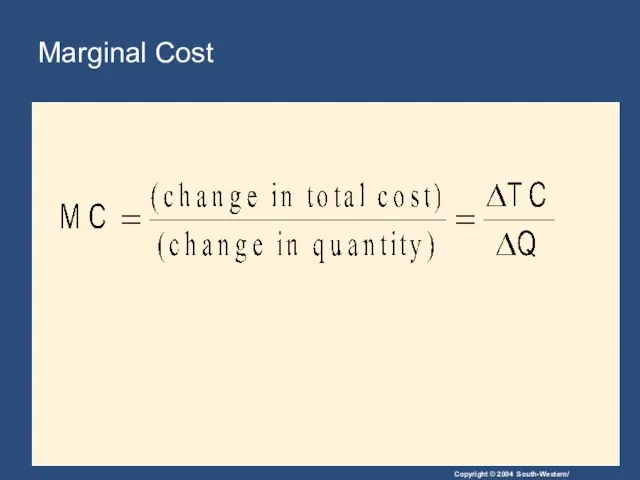

- 29. Fixed and Variable Costs Marginal Cost Marginal cost (MC) measures the increase in total cost that

- 30. Marginal Cost

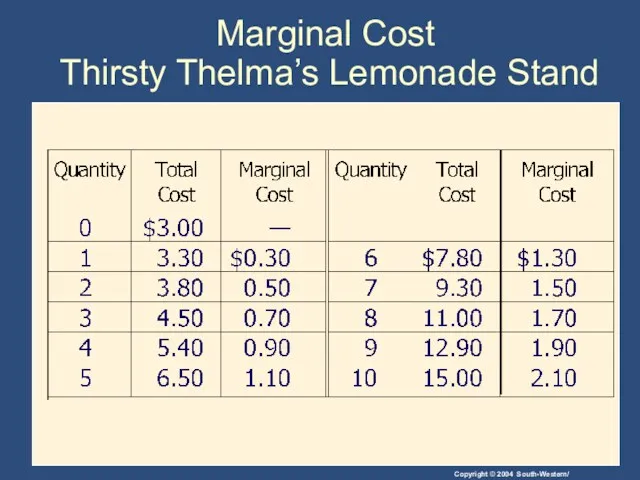

- 31. Marginal Cost Thirsty Thelma’s Lemonade Stand

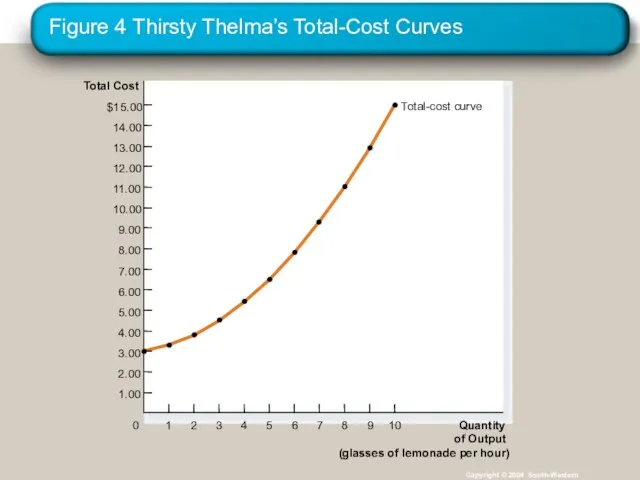

- 32. Figure 4 Thirsty Thelma’s Total-Cost Curves Copyright © 2004 South-Western Total Cost $15.00 14.00 13.00 12.00

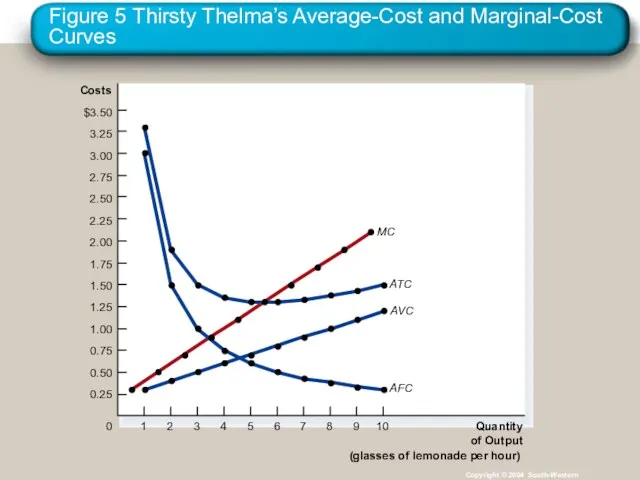

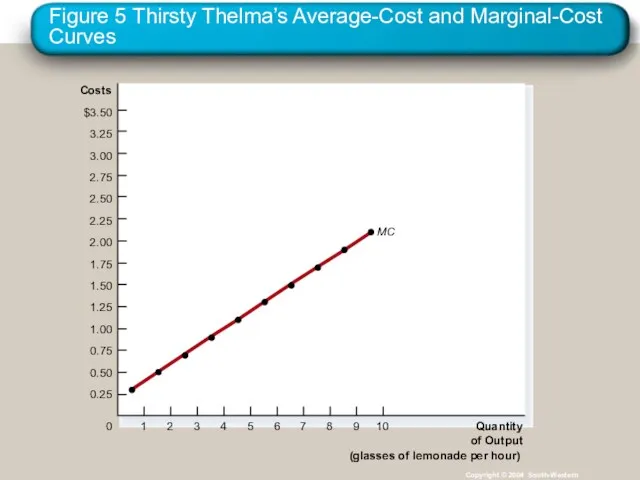

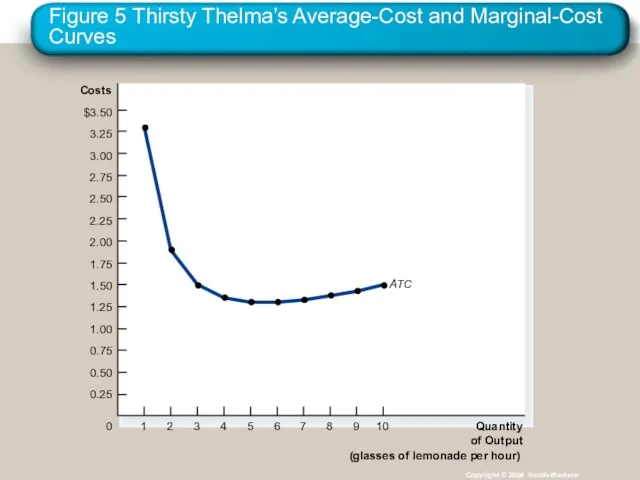

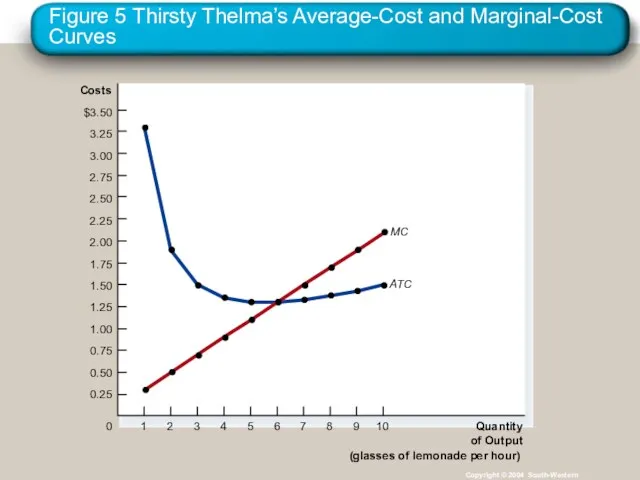

- 33. Figure 5 Thirsty Thelma’s Average-Cost and Marginal-Cost Curves Copyright © 2004 South-Western Costs $3.50 3.25 3.00

- 34. Cost Curves and Their Shapes Marginal cost rises with the amount of output produced. This reflects

- 35. Figure 5 Thirsty Thelma’s Average-Cost and Marginal-Cost Curves Copyright © 2004 South-Western Costs $3.50 3.25 3.00

- 36. Cost Curves and Their Shapes The average total-cost curve is U-shaped. At very low levels of

- 37. Cost Curves and Their Shapes The bottom of the U-shaped ATC curve occurs at the quantity

- 38. Figure 5 Thirsty Thelma’s Average-Cost and Marginal-Cost Curves Copyright © 2004 South-Western Costs $3.50 3.25 3.00

- 39. Cost Curves and Their Shapes Relationship between Marginal Cost and Average Total Cost Whenever marginal cost

- 40. Cost Curves and Their Shapes Relationship Between Marginal Cost and Average Total Cost The marginal-cost curve

- 41. Figure 5 Thirsty Thelma’s Average-Cost and Marginal-Cost Curves Copyright © 2004 South-Western Costs $3.50 3.25 3.00

- 42. Typical Cost Curves It is now time to examine the relationships that exist between the different

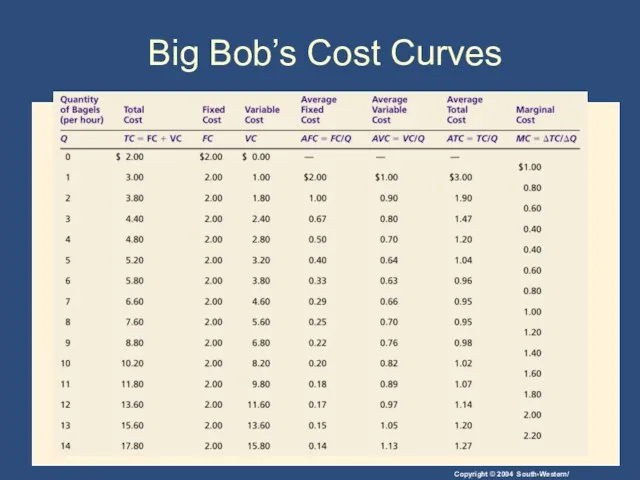

- 43. Big Bob’s Cost Curves

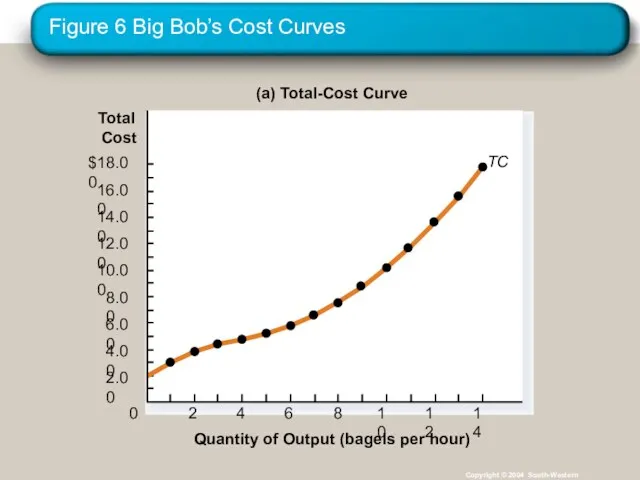

- 44. Figure 6 Big Bob’s Cost Curves Copyright © 2004 South-Western (a) Total-Cost Curve $18.00 16.00 14.00

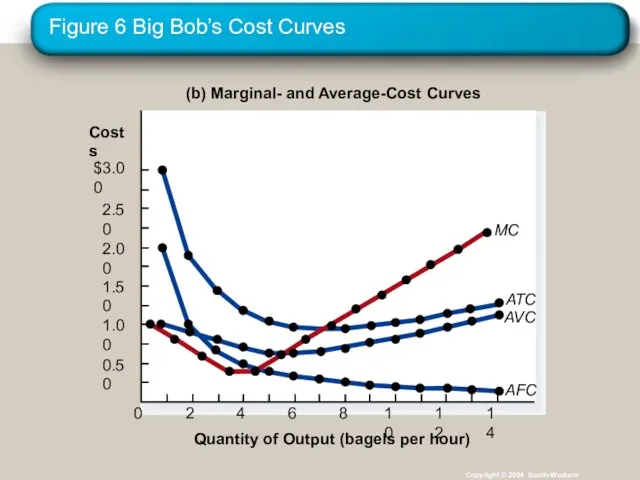

- 45. Figure 6 Big Bob’s Cost Curves Copyright © 2004 South-Western (b) Marginal- and Average-Cost Curves Quantity

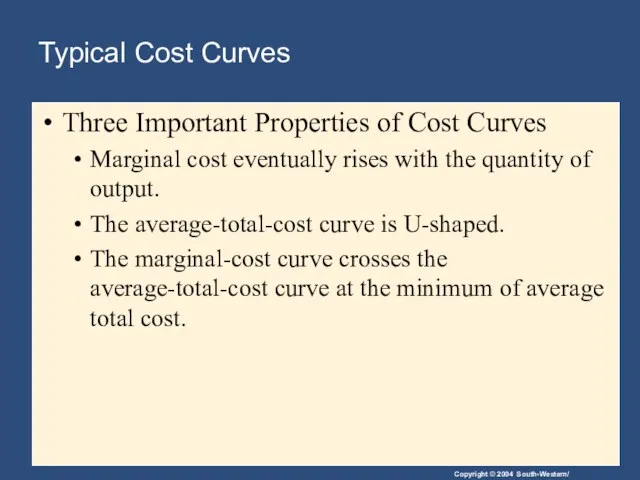

- 46. Typical Cost Curves Three Important Properties of Cost Curves Marginal cost eventually rises with the quantity

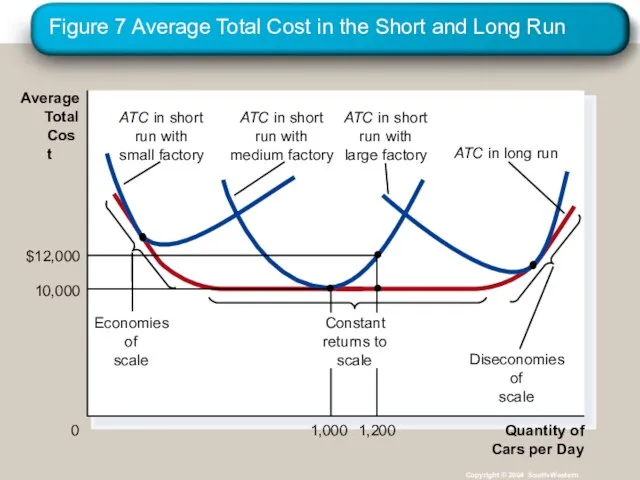

- 47. COSTS IN THE SHORT RUN AND IN THE LONG RUN For many firms, the division of

- 48. COSTS IN THE SHORT RUN AND IN THE LONG RUN Because many costs are fixed in

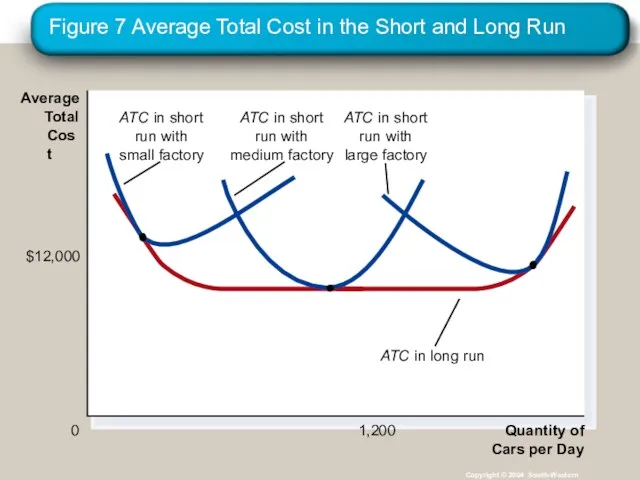

- 49. Figure 7 Average Total Cost in the Short and Long Run Copyright © 2004 South-Western Quantity

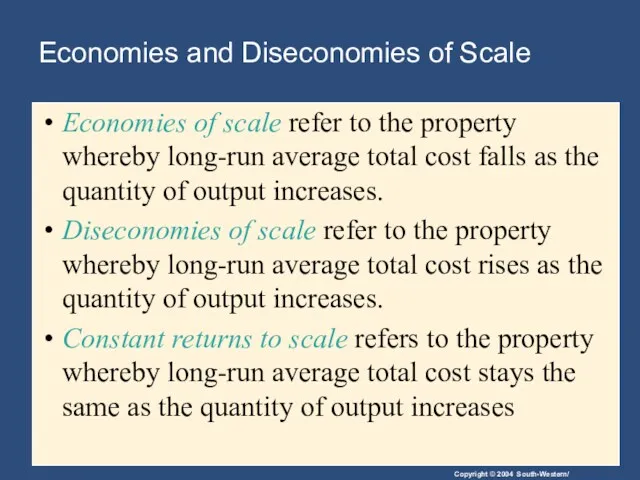

- 50. Economies and Diseconomies of Scale Economies of scale refer to the property whereby long-run average total

- 51. Figure 7 Average Total Cost in the Short and Long Run Copyright © 2004 South-Western Quantity

- 52. Summary The goal of firms is to maximize profit, which equals total revenue minus total cost.

- 53. Summary A firm’s costs reflect its production process. A typical firm’s production function gets flatter as

- 54. Summary Average total cost is total cost divided by the quantity of output. Marginal cost is

- 56. Скачать презентацию

13

The Costs of Production

13

The Costs of Production

The Market Forces of Supply and Demand

Supply and demand are the

The Market Forces of Supply and Demand

Supply and demand are the

WHAT ARE COSTS?

According to the Law of Supply:

Firms are willing to

WHAT ARE COSTS?

According to the Law of Supply:

Firms are willing to

WHAT ARE COSTS?

The Firm’s Objective

The economic goal of the firm is

WHAT ARE COSTS?

The Firm’s Objective

The economic goal of the firm is

Total Revenue, Total Cost, and Profit

Total Revenue

The amount a firm receives

Total Revenue, Total Cost, and Profit

Total Revenue

The amount a firm receives

Total Revenue, Total Cost, and Profit

Profit is the firm’s total revenue

Total Revenue, Total Cost, and Profit

Profit is the firm’s total revenue

Costs as Opportunity Costs

A firm’s cost of production includes all the

Costs as Opportunity Costs

A firm’s cost of production includes all the

Economic Profit versus Accounting Profit

Economists measure a firm’s economic profit as

Economic Profit versus Accounting Profit

Economists measure a firm’s economic profit as

Economic Profit versus Accounting Profit

When total revenue exceeds both explicit and

Economic Profit versus Accounting Profit

When total revenue exceeds both explicit and

Figure 1 Economic versus Accountants

Copyright © 2004 South-Western

How an Economist

Views a

Figure 1 Economic versus Accountants

Copyright © 2004 South-Western

How an Economist

Views a

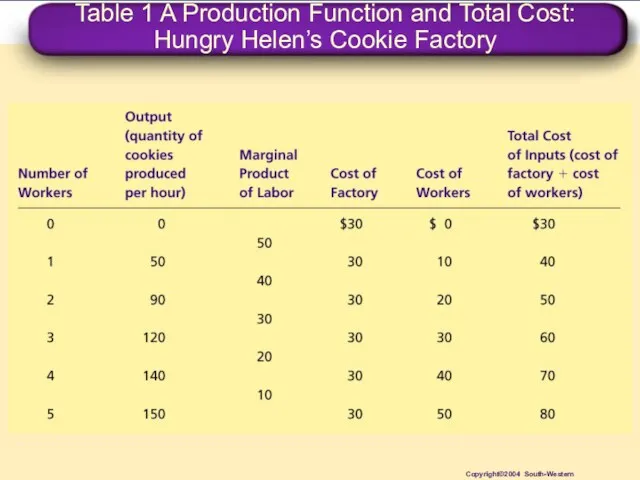

Table 1 A Production Function and Total Cost: Hungry Helen’s Cookie

Table 1 A Production Function and Total Cost: Hungry Helen’s Cookie

PRODUCTION AND COSTS

The Production Function

The production function shows the relationship between

PRODUCTION AND COSTS

The Production Function

The production function shows the relationship between

The Production Function

Marginal Product

The marginal product of any input in

The Production Function

Marginal Product

The marginal product of any input in

The Production Function

Diminishing Marginal Product

Diminishing marginal product is the property

The Production Function

Diminishing Marginal Product

Diminishing marginal product is the property

Figure 2 Hungry Helen’s Production Function

Copyright © 2004 South-Western

Quantity of

Output

(cookies

per hour)

150

140

130

120

110

100

90

80

70

60

50

40

30

20

10

Number

Figure 2 Hungry Helen’s Production Function

Copyright © 2004 South-Western

Quantity of

Output

(cookies

per hour)

150

140

130

120

110

100

90

80

70

60

50

40

30

20

10

Number

The Production Function

Diminishing Marginal Product

The slope of the production

The Production Function

Diminishing Marginal Product

The slope of the production

From the Production Function to the Total-Cost Curve

The relationship between the

From the Production Function to the Total-Cost Curve

The relationship between the

Table 1 A Production Function and Total Cost: Hungry Helen’s Cookie

Table 1 A Production Function and Total Cost: Hungry Helen’s Cookie

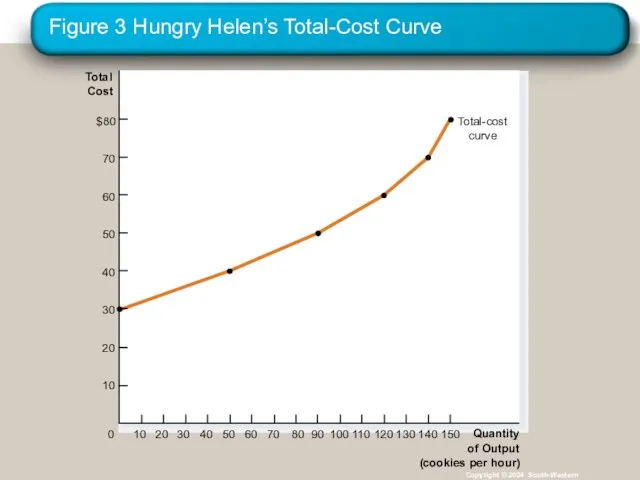

Figure 3 Hungry Helen’s Total-Cost Curve

Copyright © 2004 South-Western

Total

Cost

$80

70

60

50

40

30

20

10

Quantity

of Output

(cookies per

Figure 3 Hungry Helen’s Total-Cost Curve

Copyright © 2004 South-Western

Total

Cost

$80

70

60

50

40

30

20

10

Quantity

of Output

(cookies per

THE VARIOUS MEASURES OF COST

Costs of production may be divided into

THE VARIOUS MEASURES OF COST

Costs of production may be divided into

Fixed and Variable Costs

Fixed costs are those costs that do not

Fixed and Variable Costs

Fixed costs are those costs that do not

Fixed and Variable Costs

Total Costs

Total Fixed Costs (TFC)

Total Variable Costs (TVC)

Total

Fixed and Variable Costs

Total Costs

Total Fixed Costs (TFC)

Total Variable Costs (TVC)

Total

Table 2 The Various Measures of Cost: Thirsty Thelma’s Lemonade Stand

Copyright©2004

Table 2 The Various Measures of Cost: Thirsty Thelma’s Lemonade Stand

Copyright©2004

Fixed and Variable Costs

Average Costs

Average costs can be determined by dividing

Fixed and Variable Costs

Average Costs

Average costs can be determined by dividing

Fixed and Variable Costs

Average Costs

Average Fixed Costs (AFC)

Average Variable Costs (AVC)

Average

Fixed and Variable Costs

Average Costs

Average Fixed Costs (AFC)

Average Variable Costs (AVC)

Average

Average Costs

Average Costs

Table 2 The Various Measures of Cost: Thirsty Thelma’s Lemonade Stand

Copyright©2004

Table 2 The Various Measures of Cost: Thirsty Thelma’s Lemonade Stand

Copyright©2004

Fixed and Variable Costs

Marginal Cost

Marginal cost (MC) measures the increase in

Fixed and Variable Costs

Marginal Cost

Marginal cost (MC) measures the increase in

Marginal Cost

Marginal Cost

Marginal Cost

Thirsty Thelma’s Lemonade Stand

Marginal Cost

Thirsty Thelma’s Lemonade Stand

Figure 4 Thirsty Thelma’s Total-Cost Curves

Copyright © 2004 South-Western

Total Cost

$15.00

14.00

13.00

12.00

11.00

10.00

9.00

8.00

7.00

6.00

5.00

4.00

3.00

2.00

1.00

Quantity

of Output

(glasses

Figure 4 Thirsty Thelma’s Total-Cost Curves

Copyright © 2004 South-Western

Total Cost

$15.00

14.00

13.00

12.00

11.00

10.00

9.00

8.00

7.00

6.00

5.00

4.00

3.00

2.00

1.00

Quantity

of Output

(glasses

Figure 5 Thirsty Thelma’s Average-Cost and Marginal-Cost Curves

Copyright © 2004 South-Western

Costs

$3.50

3.25

3.00

2.75

2.50

2.25

2.00

1.75

1.50

1.25

1.00

0.75

0.50

0.25

Quantity

of

Figure 5 Thirsty Thelma’s Average-Cost and Marginal-Cost Curves

Copyright © 2004 South-Western

Costs

$3.50

3.25

3.00

2.75

2.50

2.25

2.00

1.75

1.50

1.25

1.00

0.75

0.50

0.25

Quantity

of

Cost Curves and Their Shapes

Marginal cost rises with the amount of

Cost Curves and Their Shapes

Marginal cost rises with the amount of

Figure 5 Thirsty Thelma’s Average-Cost and Marginal-Cost Curves

Copyright © 2004 South-Western

Costs

$3.50

3.25

3.00

2.75

2.50

2.25

2.00

1.75

1.50

1.25

1.00

0.75

0.50

0.25

Quantity

of

Figure 5 Thirsty Thelma’s Average-Cost and Marginal-Cost Curves

Copyright © 2004 South-Western

Costs

$3.50

3.25

3.00

2.75

2.50

2.25

2.00

1.75

1.50

1.25

1.00

0.75

0.50

0.25

Quantity

of

Cost Curves and Their Shapes

The average total-cost curve is U-shaped.

At very

Cost Curves and Their Shapes

The average total-cost curve is U-shaped.

At very

Cost Curves and Their Shapes

The bottom of the U-shaped ATC curve

Cost Curves and Their Shapes

The bottom of the U-shaped ATC curve

Figure 5 Thirsty Thelma’s Average-Cost and Marginal-Cost Curves

Copyright © 2004 South-Western

Costs

$3.50

3.25

3.00

2.75

2.50

2.25

2.00

1.75

1.50

1.25

1.00

0.75

0.50

0.25

Quantity

of

Figure 5 Thirsty Thelma’s Average-Cost and Marginal-Cost Curves

Copyright © 2004 South-Western

Costs

$3.50

3.25

3.00

2.75

2.50

2.25

2.00

1.75

1.50

1.25

1.00

0.75

0.50

0.25

Quantity

of

Cost Curves and Their Shapes

Relationship between Marginal Cost and Average

Cost Curves and Their Shapes

Relationship between Marginal Cost and Average

Cost Curves and Their Shapes

Relationship Between Marginal Cost and Average

Cost Curves and Their Shapes

Relationship Between Marginal Cost and Average

Figure 5 Thirsty Thelma’s Average-Cost and Marginal-Cost Curves

Copyright © 2004 South-Western

Costs

$3.50

3.25

3.00

2.75

2.50

2.25

2.00

1.75

1.50

1.25

1.00

0.75

0.50

0.25

Quantity

of

Figure 5 Thirsty Thelma’s Average-Cost and Marginal-Cost Curves

Copyright © 2004 South-Western

Costs

$3.50

3.25

3.00

2.75

2.50

2.25

2.00

1.75

1.50

1.25

1.00

0.75

0.50

0.25

Quantity

of

Typical Cost Curves

It is now time to examine the relationships that

Typical Cost Curves

It is now time to examine the relationships that

Big Bob’s Cost Curves

Big Bob’s Cost Curves

Figure 6 Big Bob’s Cost Curves

Copyright © 2004 South-Western

(a) Total-Cost Curve

$18.00

16.00

14.00

12.00

10.00

8.00

6.00

4.00

Quantity

Figure 6 Big Bob’s Cost Curves

Copyright © 2004 South-Western

(a) Total-Cost Curve

$18.00

16.00

14.00

12.00

10.00

8.00

6.00

4.00

Quantity

Figure 6 Big Bob’s Cost Curves

Copyright © 2004 South-Western

(b) Marginal- and

Figure 6 Big Bob’s Cost Curves

Copyright © 2004 South-Western

(b) Marginal- and

Typical Cost Curves

Three Important Properties of Cost Curves

Marginal cost eventually

Typical Cost Curves

Three Important Properties of Cost Curves

Marginal cost eventually

COSTS IN THE SHORT RUN AND IN THE LONG RUN

For many

COSTS IN THE SHORT RUN AND IN THE LONG RUN

For many

COSTS IN THE SHORT RUN AND IN THE LONG RUN

Because many

COSTS IN THE SHORT RUN AND IN THE LONG RUN

Because many

Figure 7 Average Total Cost in the Short and Long Run

Copyright

Figure 7 Average Total Cost in the Short and Long Run

Copyright

Economies and Diseconomies of Scale

Economies of scale refer to the property

Economies and Diseconomies of Scale

Economies of scale refer to the property

Figure 7 Average Total Cost in the Short and Long Run

Copyright

Figure 7 Average Total Cost in the Short and Long Run

Copyright

Summary

The goal of firms is to maximize profit, which equals total

Summary

The goal of firms is to maximize profit, which equals total

Summary

A firm’s costs reflect its production process.

A typical firm’s production function

Summary

A firm’s costs reflect its production process.

A typical firm’s production function

Summary

Average total cost is total cost divided by the quantity of

Summary

Average total cost is total cost divided by the quantity of

Андрей Миронов: жизнь в кадре

Андрей Миронов: жизнь в кадре Жомарт және адамгершілігі жоғары

Жомарт және адамгершілігі жоғары Проект по ПДД

Проект по ПДД Одноатомные спирты. Химические свойства (презентация).

Одноатомные спирты. Химические свойства (презентация). Монтаж РЭА

Монтаж РЭА Птицы нашего края

Птицы нашего края Презентация Волшебное тесто

Презентация Волшебное тесто Устройство памяти и процессора. Память ЭВМ

Устройство памяти и процессора. Память ЭВМ НФ Детский епархиальный образовательный центр УФ Клявлинский

НФ Детский епархиальный образовательный центр УФ Клявлинский Классный час на тему: Москва - город открытых сердец

Классный час на тему: Москва - город открытых сердец Презентация Гео-декор - оформление участка детского сада

Презентация Гео-декор - оформление участка детского сада Презентация История первого письма

Презентация История первого письма День учителя. Фотошоп

День учителя. Фотошоп Государство и право Англии в средние века

Государство и право Англии в средние века АСК 2 урок Природные особенности Смоленской области

АСК 2 урок Природные особенности Смоленской области Польза дождевых червей

Польза дождевых червей Реалізація програмного комплексу ip-телефонії на основі PBX Asterisk

Реалізація програмного комплексу ip-телефонії на основі PBX Asterisk Изготовление биполярной ИС с изоляцией транзисторов p-n-переходом

Изготовление биполярной ИС с изоляцией транзисторов p-n-переходом Испытание машин

Испытание машин Prezentatsia_Organizatsia_predprinimatelskoy_deyat

Prezentatsia_Organizatsia_predprinimatelskoy_deyat Физминутка

Физминутка Business vocabulary Idioms

Business vocabulary Idioms Содержание и технологии педагогической деятельности по ранней профориентации детей дошкольного возраста

Содержание и технологии педагогической деятельности по ранней профориентации детей дошкольного возраста Механика грунтов, основания и фундаменты

Механика грунтов, основания и фундаменты Struktury organizacyjne

Struktury organizacyjne Фотосинтез процесі

Фотосинтез процесі Регулятор напряжения генератора в схеме ЭВ.10

Регулятор напряжения генератора в схеме ЭВ.10 Классный час Будь здоров.

Классный час Будь здоров.