- Oil and gas accounting

Содержание

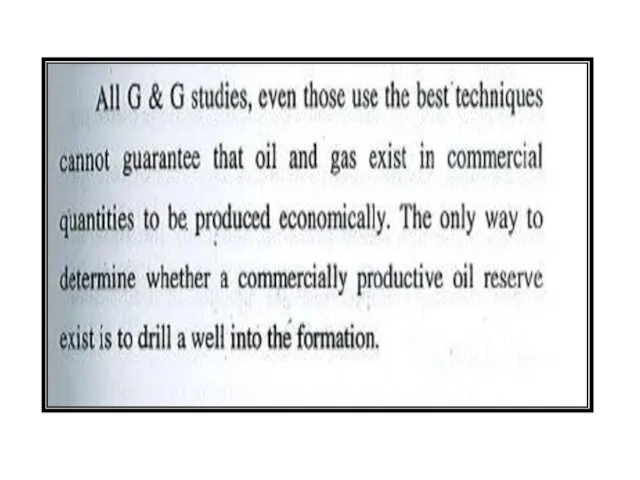

- 2. All G&G studies, even those use the best techniques cannot guarantee that oil and gas exist

- 3. In the case of th devlopment wells 22% of the devlopment wells drilled in th united

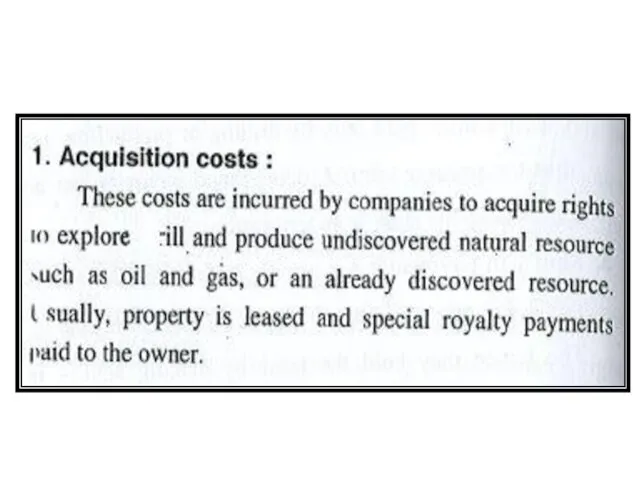

- 4. Acquisition of property : Acquisition means the procurement of the legal right to explore for and

- 5. Oil and Gas Leases : A petroleum company cannot conduct any activity before obtaining the rights

- 9. *

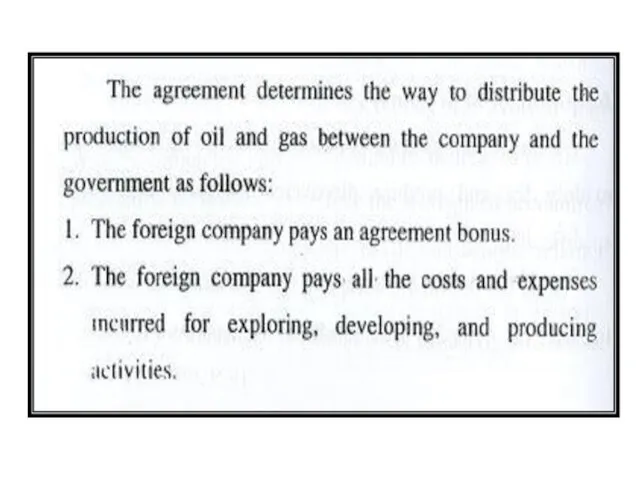

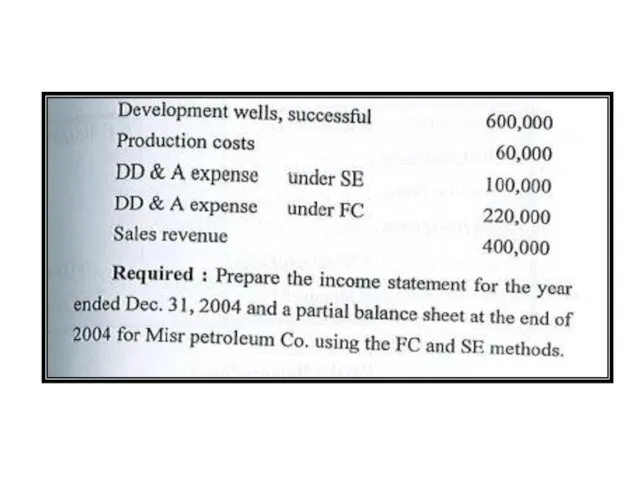

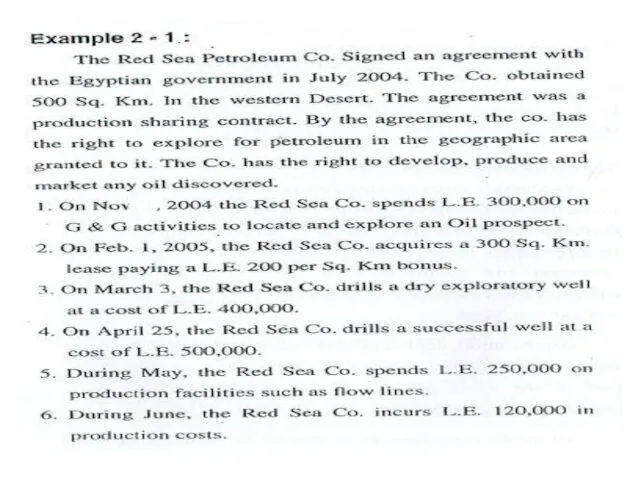

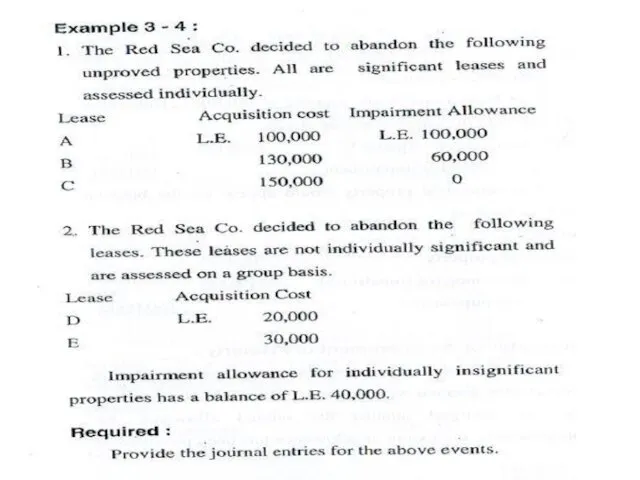

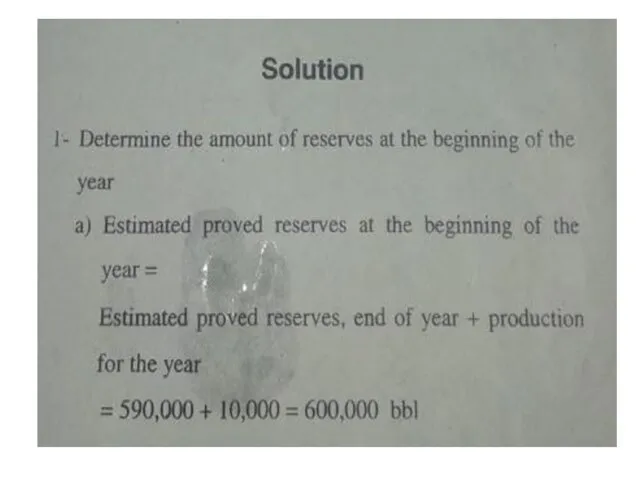

- 27. Successful efforts Accounting (SE) we discussed now the four basic type of costs they are :

- 28. The acquisition costs Acquisition costs incurred are capitalized as unproved property. If proved reserves are found

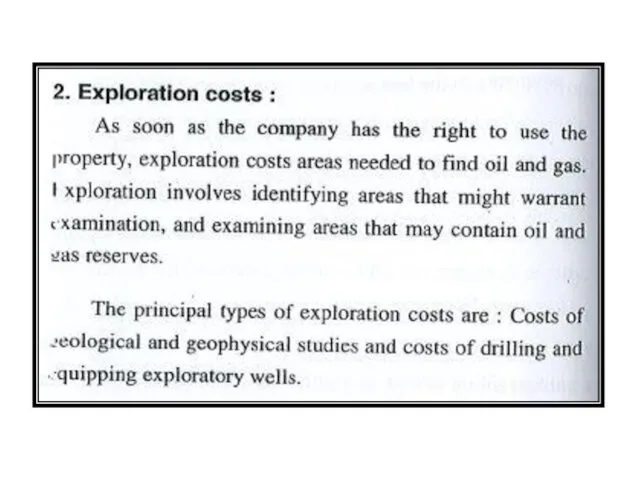

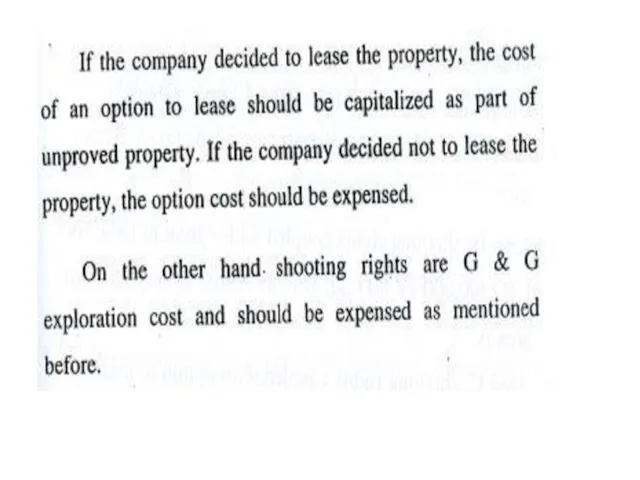

- 29. The exploration costs The costs include two categories : A ) predrilling exploration costs are to

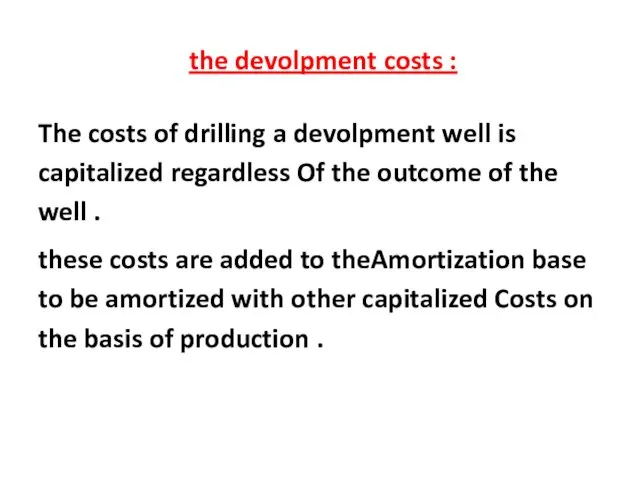

- 30. the devolpment costs : The costs of drilling a devolpment well is capitalized regardless Of the

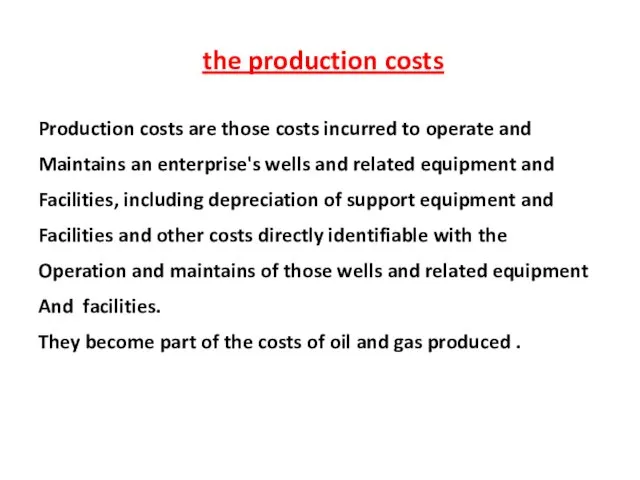

- 31. the production costs Production costs are those costs incurred to operate and Maintains an enterprise's wells

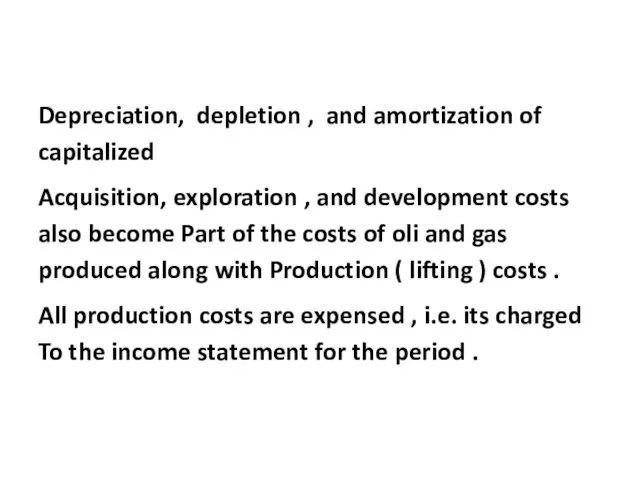

- 32. Depreciation, depletion , and amortization of capitalized Acquisition, exploration , and development costs also become Part

- 75. Скачать презентацию

All G&G studies, even those use the best techniques cannot guarantee

All G&G studies, even those use the best techniques cannot guarantee

In the case of th devlopment wells 22% of the devlopment

In the case of th devlopment wells 22% of the devlopment

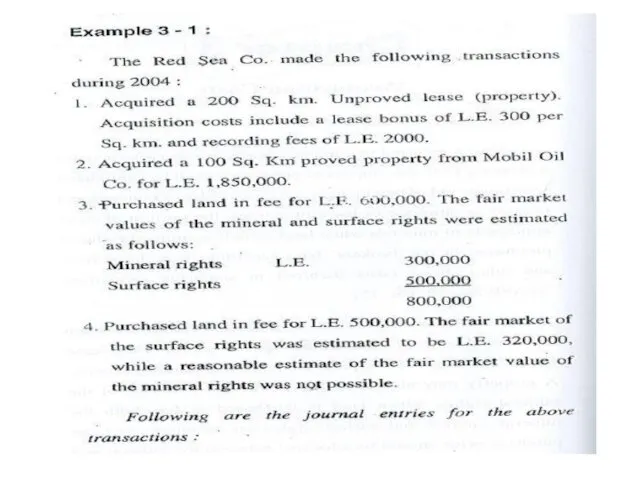

Acquisition of property :

Acquisition means the procurement of the legal

right

Acquisition of property :

Acquisition means the procurement of the legal

right

Oil and Gas Leases :

A petroleum company cannot conduct any activity

Oil and Gas Leases :

A petroleum company cannot conduct any activity

*

*

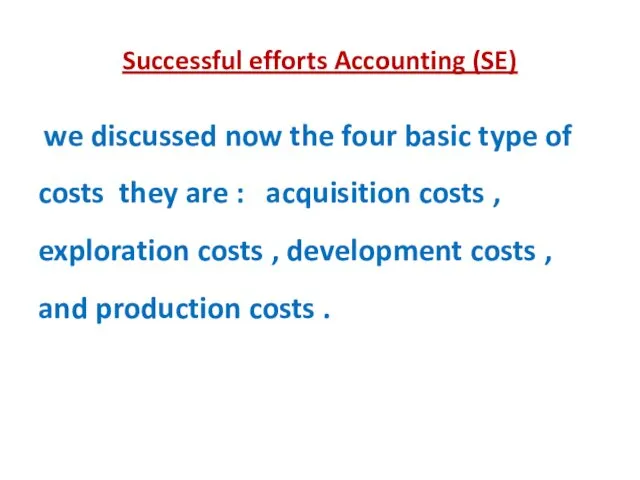

Successful efforts Accounting (SE)

we discussed now the four basic type

Successful efforts Accounting (SE)

we discussed now the four basic type

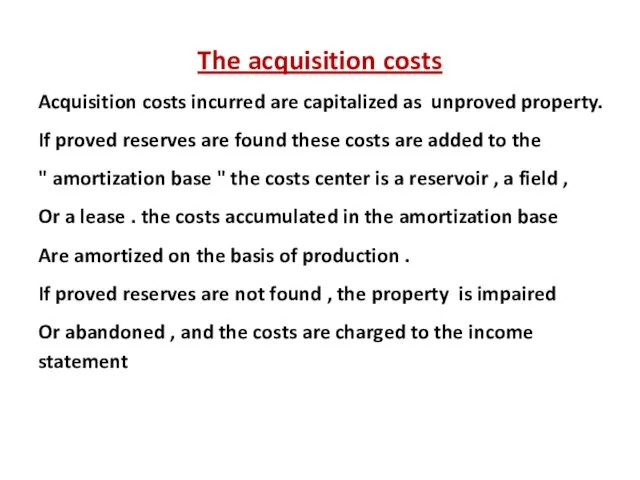

The acquisition costs

Acquisition costs incurred are capitalized as unproved property.

The acquisition costs

Acquisition costs incurred are capitalized as unproved property.

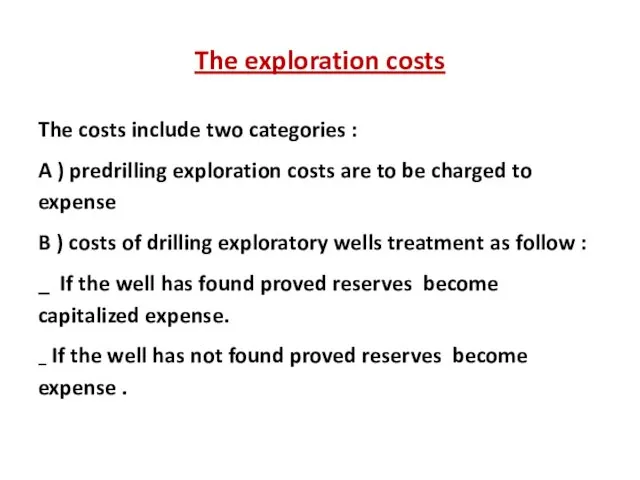

The exploration costs

The costs include two categories :

A )

The exploration costs

The costs include two categories :

A )

the devolpment costs :

The costs of drilling a devolpment well

the devolpment costs :

The costs of drilling a devolpment well

the production costs

Production costs are those costs incurred to

the production costs

Production costs are those costs incurred to

Depreciation, depletion , and amortization of capitalized

Acquisition, exploration , and development

Depreciation, depletion , and amortization of capitalized

Acquisition, exploration , and development

Цифровая схемотехника. Диодно-транзисторная логика

Цифровая схемотехника. Диодно-транзисторная логика Мои увлечения Мои наряды , мой стиль.

Мои увлечения Мои наряды , мой стиль. Переработка мусора

Переработка мусора Электрорадиоэлементы и электронные узлы

Электрорадиоэлементы и электронные узлы Электрические и электронные аппараты. Лекция №5

Электрические и электронные аппараты. Лекция №5 Психологічне консультування в сфері освіти

Психологічне консультування в сфері освіти Наноқұрылымды материалдар, олардың қасиеттері және практикада қолданылуы

Наноқұрылымды материалдар, олардың қасиеттері және практикада қолданылуы В гостях у сказки

В гостях у сказки разработка урока по черчению

разработка урока по черчению Презентация к уроку Галерея знаменитых петербуржцев первой пол.XIX века глазами К.П.Брюллова

Презентация к уроку Галерея знаменитых петербуржцев первой пол.XIX века глазами К.П.Брюллова Мастер-класс по декоративно прикладному творчеству:Изготовление панно из ракушек.

Мастер-класс по декоративно прикладному творчеству:Изготовление панно из ракушек. Технические решения и проектирование подсистем автоматического управления в ЭСБ различного функционального назначения (Часть 11)

Технические решения и проектирование подсистем автоматического управления в ЭСБ различного функционального назначения (Часть 11) МГПУ, ИИЯ. Почему тебе нужно именно сюда

МГПУ, ИИЯ. Почему тебе нужно именно сюда Обстоятельства, исключающие преступность деяния

Обстоятельства, исключающие преступность деяния Притчі Христові. Притча про виноградарів

Притчі Христові. Притча про виноградарів Энгр. И проверочный тест для повторения

Энгр. И проверочный тест для повторения Change. Предвыборная компания в институте

Change. Предвыборная компания в институте Физическое напутствие выпускникам

Физическое напутствие выпускникам Дробление. Биологическое значение дробления

Дробление. Биологическое значение дробления Ч-слоговая разминка (2)

Ч-слоговая разминка (2) Россия 1991-1999 годы. Экономические реформы. Либерализация цен

Россия 1991-1999 годы. Экономические реформы. Либерализация цен Invata sa te comporti civilizat

Invata sa te comporti civilizat Онлайн-кассы: применение, подбор оптимальной ККТ, наиболее частые ошибки

Онлайн-кассы: применение, подбор оптимальной ККТ, наиболее частые ошибки Занятие №81 - Ритм. Мелодия. Гармония

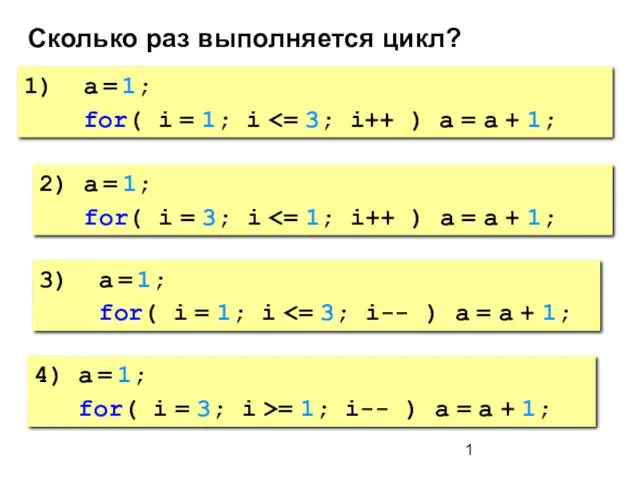

Занятие №81 - Ритм. Мелодия. Гармония Функции. Лекция 5 по алгоритмизации и программированию

Функции. Лекция 5 по алгоритмизации и программированию Организация строительства многоэтажного жилого дома в г. Новосибирске

Организация строительства многоэтажного жилого дома в г. Новосибирске Патогенез плохих выступлений

Патогенез плохих выступлений Презентация отчёта по тематической неделе смеха

Презентация отчёта по тематической неделе смеха