- Tax elements

Содержание

- 2. CONTENT Definition Elements Definition of elements References

- 3. DEFINITION Tax - compulsory, individually gratuitous payment levied on organizations and individuals in the form of

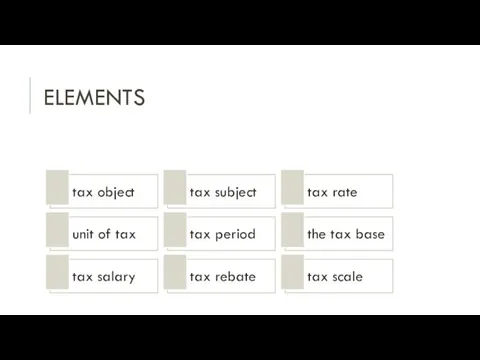

- 4. ELEMENTS

- 5. TAX OBJECT Object of taxation - the sale of goods (works, services), property, profits, income or

- 6. UNIT OF TAX The unit of taxation is a single scale of taxation, which is used

- 7. TAX SALARY Tax salary is the amount of the fee paid by the payer to a

- 8. TAX SUBJECT According to the general norms of the theory of law, the main subjects of

- 9. TAX PERIOD A tax period is a calendar year or another period of time in relation

- 10. TAX REBATE Tax rebate - are the benefits provided to certain categories of taxpayers and payers

- 11. TAX RATE Tax rate - the amount of tax charges per unit of measure of the

- 12. THE TAX BASE Tax base (taxable base) - the value, physical or other characteristics of the

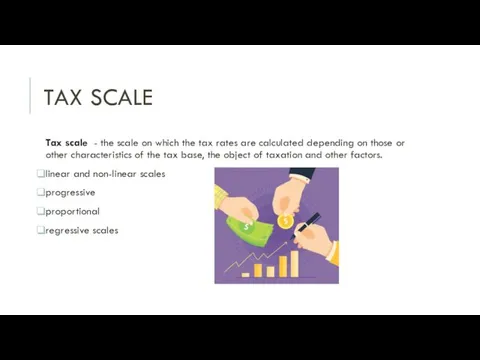

- 13. TAX SCALE Tax scale - the scale on which the tax rates are calculated depending on

- 15. Скачать презентацию

CONTENT

Definition

Elements

Definition of elements

References

CONTENT

Definition

Elements

Definition of elements

References

DEFINITION

Tax - compulsory, individually gratuitous payment levied on organizations and individuals

DEFINITION

Tax - compulsory, individually gratuitous payment levied on organizations and individuals

ELEMENTS

ELEMENTS

TAX OBJECT

Object of taxation - the sale of goods (works, services),

TAX OBJECT

Object of taxation - the sale of goods (works, services),

UNIT OF TAX

The unit of taxation is a single scale of

UNIT OF TAX

The unit of taxation is a single scale of

TAX SALARY

Tax salary is the amount of the fee paid by

TAX SALARY

Tax salary is the amount of the fee paid by

TAX SUBJECT

According to the general norms of the theory of law,

TAX SUBJECT

According to the general norms of the theory of law,

TAX PERIOD

A tax period is a calendar year or another period

TAX PERIOD

A tax period is a calendar year or another period

TAX REBATE

Tax rebate - are the benefits provided to certain categories

TAX REBATE

Tax rebate - are the benefits provided to certain categories

TAX RATE

Tax rate - the amount of tax charges per unit

TAX RATE

Tax rate - the amount of tax charges per unit

THE TAX BASE

Tax base (taxable base) - the value, physical or

THE TAX BASE

Tax base (taxable base) - the value, physical or

TAX SCALE

Tax scale - the scale on which the tax rates

TAX SCALE

Tax scale - the scale on which the tax rates

Твой компьютер

Твой компьютер Медсестринський процес при корості та педикульозі

Медсестринський процес при корості та педикульозі Презентация Взаимодействие с родителями

Презентация Взаимодействие с родителями Анатомия и физиология тонкого и толстого кишечника. Брюшина. Лекция № 30

Анатомия и физиология тонкого и толстого кишечника. Брюшина. Лекция № 30 Происхождение романских языков

Происхождение романских языков Природный глинистый минерал бентонит

Природный глинистый минерал бентонит Игры и упражнения для развития творческого воображения у детей

Игры и упражнения для развития творческого воображения у детей Сотрудничество по программе льготного страхования членов МПО ОАО НК Роснефть

Сотрудничество по программе льготного страхования членов МПО ОАО НК Роснефть Ислам. Мусульмане

Ислам. Мусульмане School. Timetable

School. Timetable Комическое и лирическое в прозе и поэзии Саши Черного. Стиль “Дневника фокса Микки”

Комическое и лирическое в прозе и поэзии Саши Черного. Стиль “Дневника фокса Микки” Численность населения мира

Численность населения мира Расширение территории России XVIII века

Расширение территории России XVIII века Основы поведения субъектов рыночной экономики

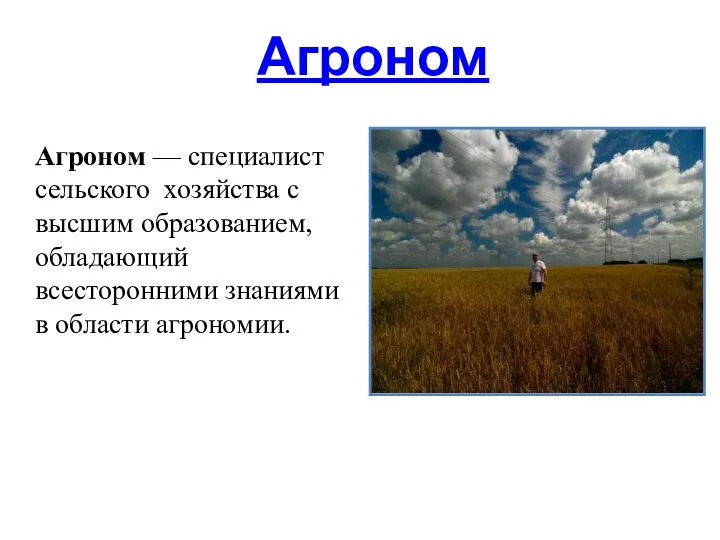

Основы поведения субъектов рыночной экономики химия и биология в профессиях

химия и биология в профессиях Фойе школы-интерната с. Самбург Пуровского района

Фойе школы-интерната с. Самбург Пуровского района Организация и проведение обучающих семинаров Комплексные решения для управления продажами. Изучение финансовых рынков

Организация и проведение обучающих семинаров Комплексные решения для управления продажами. Изучение финансовых рынков Точение конических и фасонных поверхностей. Изготовление ручки напильника. 7 класс

Точение конических и фасонных поверхностей. Изготовление ручки напильника. 7 класс Чингиз Айтматов Буранный полустанок, IV глава Легенда О Манкурте

Чингиз Айтматов Буранный полустанок, IV глава Легенда О Манкурте Формы рельефа суши

Формы рельефа суши Презентация Учебно-методический комплекс

Презентация Учебно-методический комплекс Радиоактивность. Открытие радиоактивности. Природа радиоактивных излучений. Радиоактивные превращения. Изотопы

Радиоактивность. Открытие радиоактивности. Природа радиоактивных излучений. Радиоактивные превращения. Изотопы Родительское собрание. Итоговое собеседование по русскому языку. 9 кл

Родительское собрание. Итоговое собеседование по русскому языку. 9 кл Бактерии, их виды, функции и строение

Бактерии, их виды, функции и строение Новый год в Англии

Новый год в Англии Как увидеть будущее. Анализ цифровых трендов

Как увидеть будущее. Анализ цифровых трендов Fake news

Fake news Туберозный склероз

Туберозный склероз