- Косвенные иски

Содержание

- 2. Производные иски ”Производный иск – это дитя неспокойного брака акционеров и менеджмента, и трещина в этом

- 3. Agency problem/ проблема агентских издержек Система корпоративного управления во всем мире с переменным успехом пытается разрешить

- 4. Производные иски Решение agency problem - выработка таких механизмов eх post контроля, которые бы стимулировали управленцев

- 5. Dodge vs. Ford Motor Co. Хозяйственная корпорация создается и служит первоочередно извлечению прибыли для ее участников.

- 6. пп.5 п.2 Постановления Пленума ВАС РФ от 30.07.2013 N 62 «При определении интересов юридического лица следует

- 7. Определение ВАС РФ от 28.10.2010 No 8794/09 …Коммерческая организация создается с целью извлечения прибыли, а его

- 8. Механизмы корпоративного контроля/ Фидуциарные обязанности В странах англосаксонского права, это триада обязанностей директоров перед компанией: Обязанность

- 9. Механизмы корпоративного контроля/ Косвенный иск Cohen v. Beneficial Industrial Loan Corp.: по мере развития предпринимательских отношений

- 10. Косвенный иск Производный иск позволяет корпоративным участникам выступать своего рода надзирателями при менеджерах компании и от

- 11. Cт. 23.1 Федеральных правил гражданского судопроизводства США «Данное правило применяется, когда один или несколько акционеров или

- 12. Ключевая проблема косвенных исков Поиск точки равновесия между необходимостью наделения инвесторов правами привлекать к ответственности руководителей,

- 13. Ключевая проблема косвенных исков Дмитрий Степанов: Все корпоративное законодательство можно представить в виде тривиального набора сдержек

- 14. Ключевая проблема косвенных исков Бейнбридж: «Если А предоставить право перепроверять каждое решение Б, то все, что

- 15. Ключевая проблема косвенных исков Механизмы контроля со стороны корпоративных участников должны быть всякий раз соотнесены с

- 16. Smith v. Van Gorkom, 488 A.2d 858 (Del. 1985) “Правило делового суждения (“The business judgment rule”)

- 17. П. 1 Постановления Пленума ВАС РФ №62 «Поскольку судебный контроль призван обеспечивать защиту прав юридических лиц

- 18. История развития косвенных исков Паулианов иск (actio Pauliana): возможность оспаривания кредитором сделки, стороны которых преследовали цель

- 19. История развития косвенный исков Глава III.1 Закона о банкротстве: право оспаривать подозрительные сделки должника и сделки

- 20. История развития косвенных исков Однако исторически право на производный иск – то есть право представительствовать от

- 21. Решение Государственного высшего торгового суда Германии (Reichsoberhandelsgerisht) 1877 г. «Акционер не имеет права на предъявление косвенного

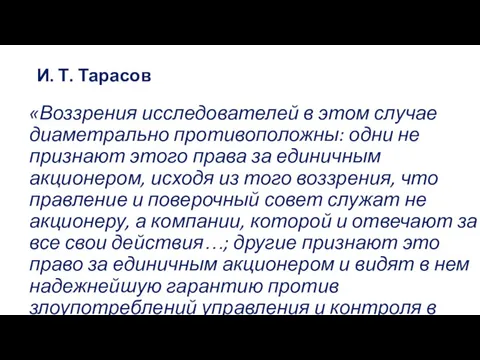

- 22. И. Т. Тарасов «Воззрения исследователей в этом случае диаметрально противоположны: одни не признают этого права за

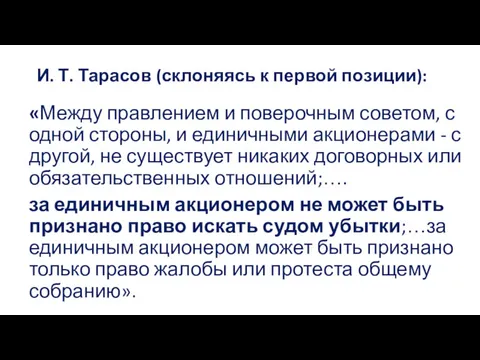

- 23. И. Т. Тарасов (склоняясь к первой позиции): «Между правлением и поверочным советом, с одной стороны, и

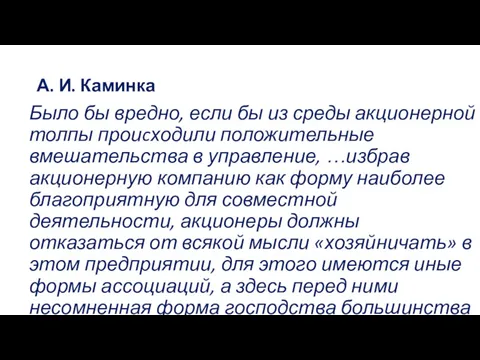

- 24. А. И. Каминка Было бы вредно, если бы из среды акционерной толпы проиcходили положительные вмешательства в

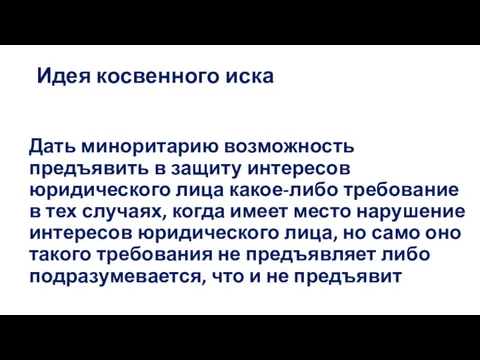

- 25. Идея косвенного иска Дать миноритарию возможность предъявить в защиту интересов юридического лица какое-либо требование в тех

- 26. ПОЧЕМУ ИСК ПРОИЗВОДНЫЙ (КОСВЕННЫЙ)(DERIVATIVE)? (1) Данный иск является косвенным, так как выгода самих акционеров – заявителей

- 27. ПОЧЕМУ ИСК ПРОИЗВОДНЫЙ (КОСВЕННЫЙ)(DERIVATIVE)? (2) В случае удовлетворения требований, предъявленного в рамках косвенного иска, участники «обретают

- 28. ПОЧЕМУ ИСК ПРОИЗВОДНЫЙ (КОСВЕННЫЙ)(DERIVATIVE)? (3) У заявителя есть юридически значимое требование лишь в том объеме, в

- 29. Применение косвенных исков по аналогии к трастам До дела Foss (1843) английские и американские суды применяли

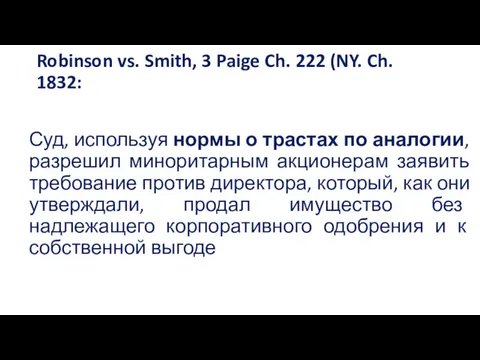

- 30. Robinson vs. Smith, 3 Paige Ch. 222 (NY. Ch. 1832: Суд, используя нормы о трастах по

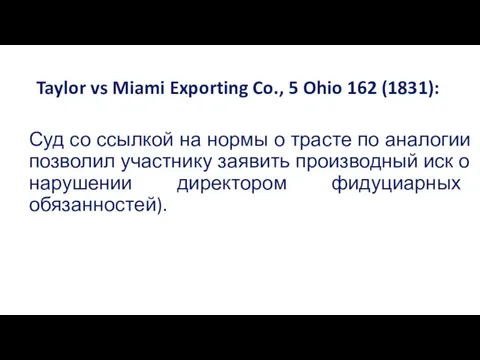

- 31. Taylor vs Miami Exporting Co., 5 Ohio 162 (1831): Суд со ссылкой на нормы о трасте

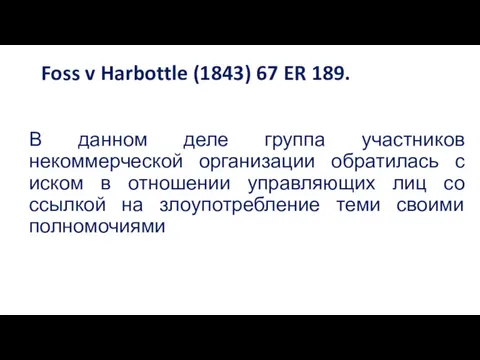

- 32. Foss v Harbottle (1843) 67 ER 189. В данном деле группа участников некоммерческой организации обратилась с

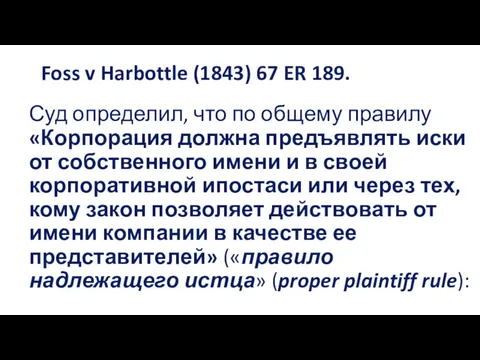

- 33. Foss v Harbottle (1843) 67 ER 189. Суд определил, что по общему правилу «Корпорация должна предъявлять

- 34. Foss v Harbottle (1843) 67 ER 189. Принцип большинства (majority principle rule): если cestui que trust

- 35. Foss v Harbottle (1843) 67 ER 189. Судья Дженкинс: «Там, где предполагаемое нарушение является следствием сделки,

- 36. Foss v Harbottle (1843) 67 ER 189 НО! Есть исключения: если речь идет о действиях незаконных

- 37. Shareholders Derivative Actions Rule 23.1. Derivative Actions/ Contemporaneous ownership requirement The complaint must: allege that the

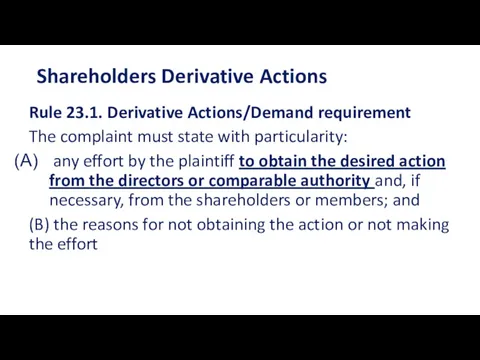

- 38. Shareholders Derivative Actions Rule 23.1. Derivative Actions/Demand requirement The complaint must state with particularity: any effort

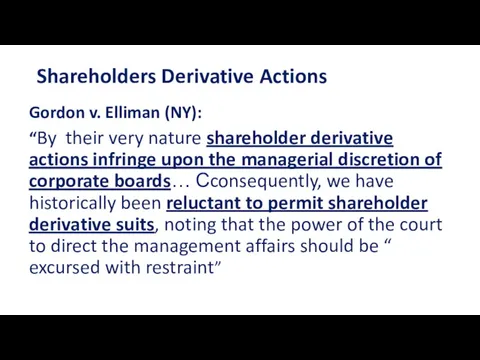

- 39. Shareholders Derivative Actions Gordon v. Elliman (NY): “By their very nature shareholder derivative actions infringe upon

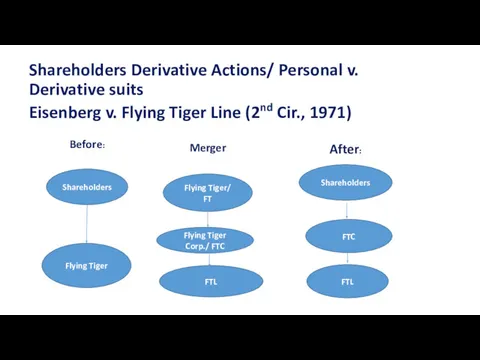

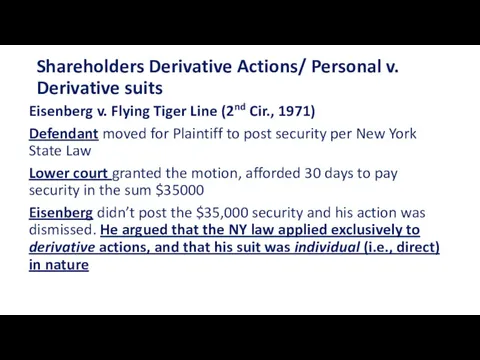

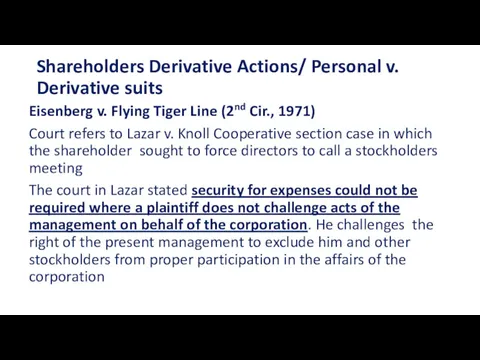

- 40. Shareholders Derivative Actions/ Personal v. Derivative suits Eisenberg v. Flying Tiger Line (2nd Cir., 1971) Flying

- 41. Shareholders Derivative Actions/ Personal v. Derivative suits Eisenberg v. Flying Tiger Line (2nd Cir., 1971) Facts:

- 42. Shareholders Derivative Actions/ Personal v. Derivative suits Eisenberg v. Flying Tiger Line (2nd Cir., 1971) Defendant

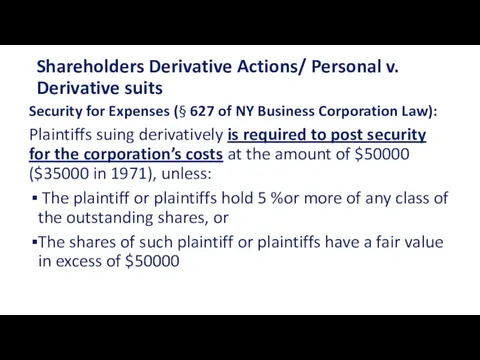

- 43. Shareholders Derivative Actions/ Personal v. Derivative suits Security for Expenses (§ 627 of NY Business Corporation

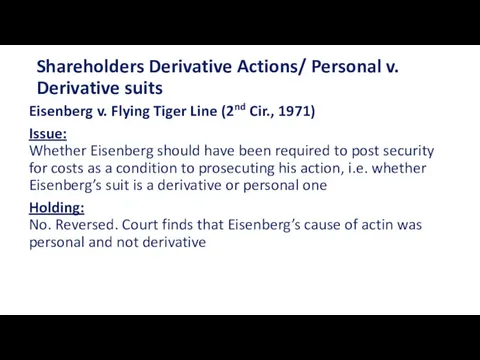

- 44. Shareholders Derivative Actions/ Personal v. Derivative suits Eisenberg v. Flying Tiger Line (2nd Cir., 1971) Issue:

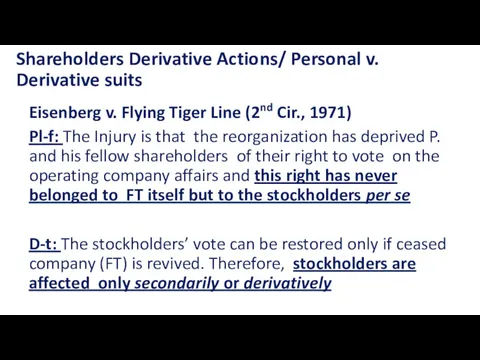

- 45. Shareholders Derivative Actions/ Personal v. Derivative suits Eisenberg v. Flying Tiger Line (2nd Cir., 1971) Pl-f:

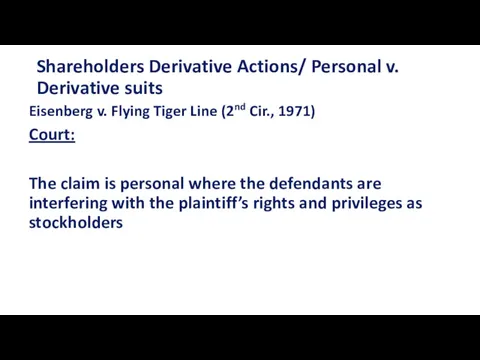

- 46. Shareholders Derivative Actions/ Personal v. Derivative suits Eisenberg v. Flying Tiger Line (2nd Cir., 1971) Court

- 47. Shareholders Derivative Actions/ Personal v. Derivative suits Eisenberg v. Flying Tiger Line (2nd Cir., 1971) Court:

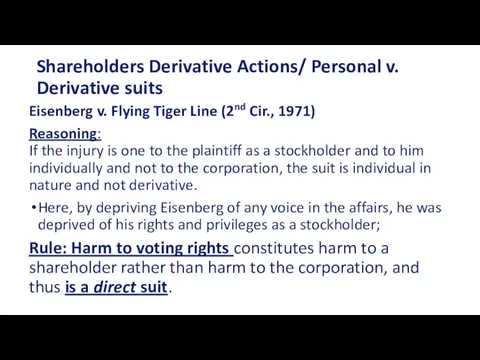

- 48. Shareholders Derivative Actions/ Personal v. Derivative suits Eisenberg v. Flying Tiger Line (2nd Cir., 1971) Reasoning:

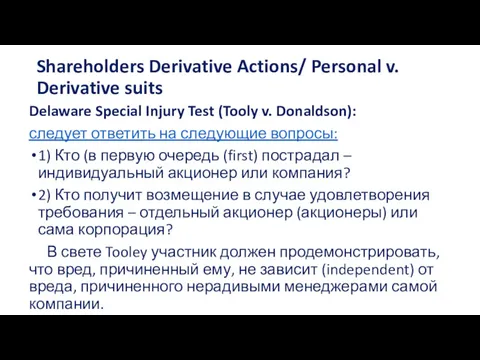

- 49. Shareholders Derivative Actions/ Personal v. Derivative suits Delaware Special Injury Test (Tooly v. Donaldson): следует ответить

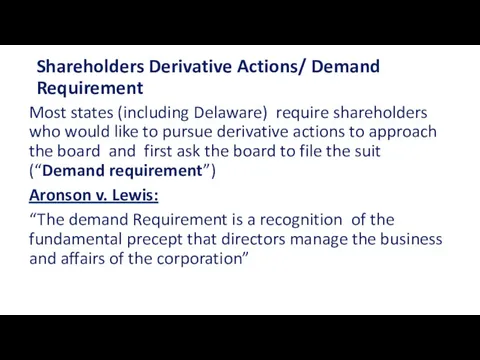

- 50. Shareholders Derivative Actions/ Demand Requirement Most states (including Delaware) require shareholders who would like to pursue

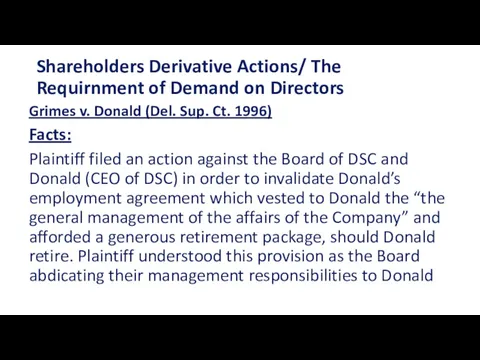

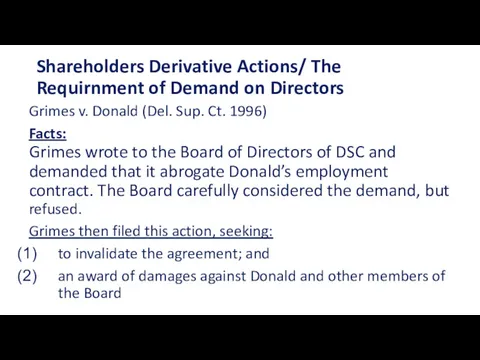

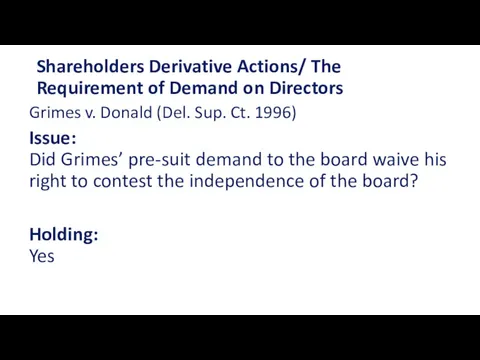

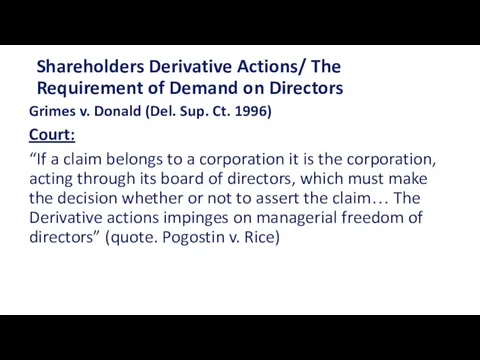

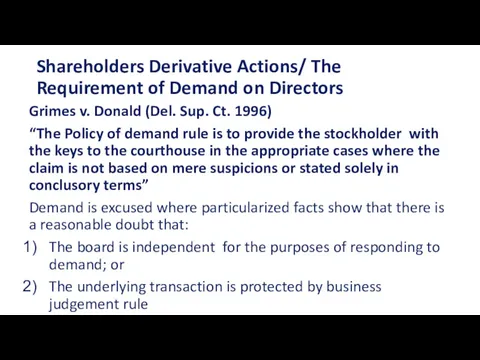

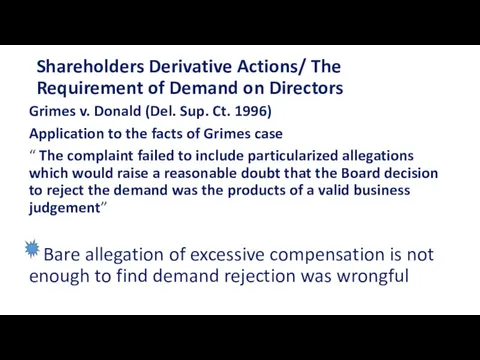

- 51. Shareholders Derivative Actions/ The Requirnment of Demand on Directors Grimes v. Donald (Del. Sup. Ct. 1996)

- 52. Shareholders Derivative Actions/ The Requirnment of Demand on Directors Grimes v. Donald (Del. Sup. Ct. 1996)

- 53. Shareholders Derivative Actions/ The Requirement of Demand on Directors Grimes v. Donald (Del. Sup. Ct. 1996)

- 54. Shareholders Derivative Actions/ The Requirement of Demand on Directors Grimes v. Donald (Del. Sup. Ct. 1996)

- 55. Shareholders Derivative Actions/ The Requirement of Demand on Directors Grimes v. Donald (Del. Sup. Ct. 1996)

- 56. Shareholders Derivative Actions/ The Requirement of Demand on Directors Grimes v. Donald (Del. Sup. Ct. 1996)

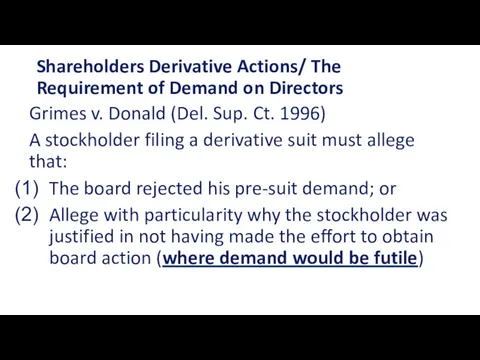

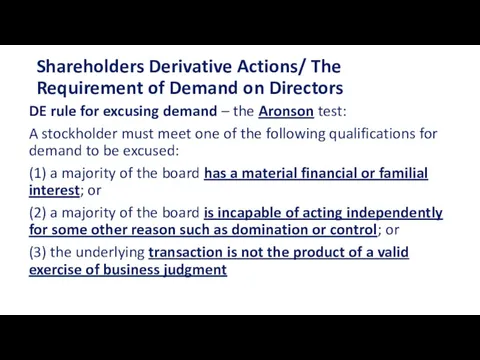

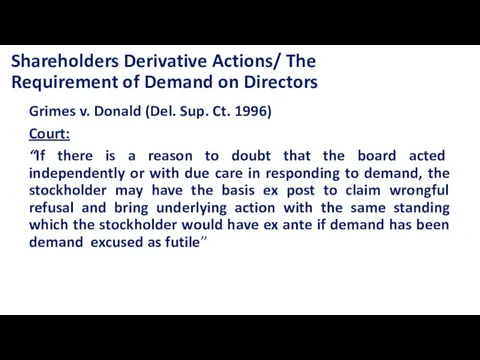

- 57. Shareholders Derivative Actions/ The Requirement of Demand on Directors DE rule for excusing demand – the

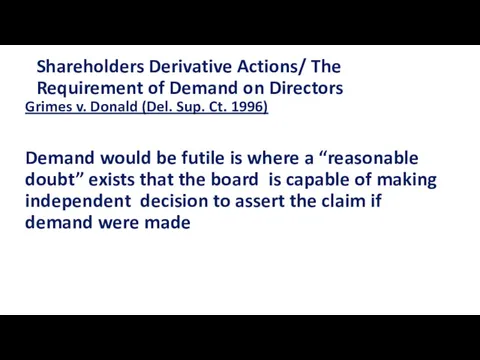

- 58. Shareholders Derivative Actions/ The Requirement of Demand on Directors Grimes v. Donald (Del. Sup. Ct. 1996)

- 59. Shareholders Derivative Actions/ The Requirement of Demand on Directors Grimes v. Donald (Del. Sup. Ct. 1996)

- 60. Shareholders Derivative Actions/ The Requirement of Demand on Directors Grimes v. Donald (Del. Sup. Ct. 1996)

- 61. Shareholders Derivative Actions/ The Requirement of Demand on Directors Grimes v. Donald (Del. Sup. Ct. 1996)

- 62. Shareholders Derivative Actions/ The Requirement of Demand on Directors Grimes v. Donald (Del. Sup. Ct. 1996)

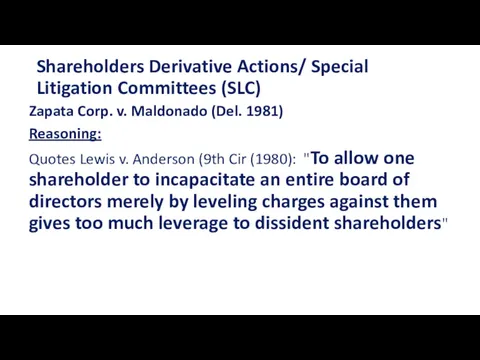

- 63. Shareholders Derivative Actions/ Special Litigation Committees (SLC) Zapata Corp. v. Maldonado (Del. 1981) Reasoning: Quotes Lewis

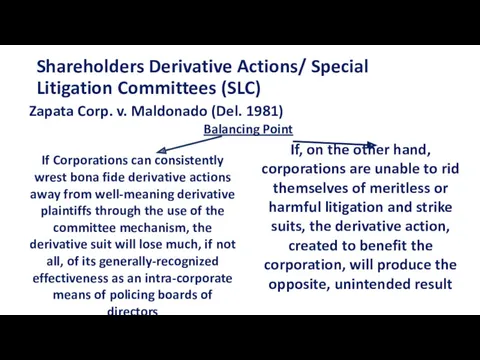

- 64. Shareholders Derivative Actions/ Special Litigation Committees (SLC) Zapata Corp. v. Maldonado (Del. 1981) Balancing Point If

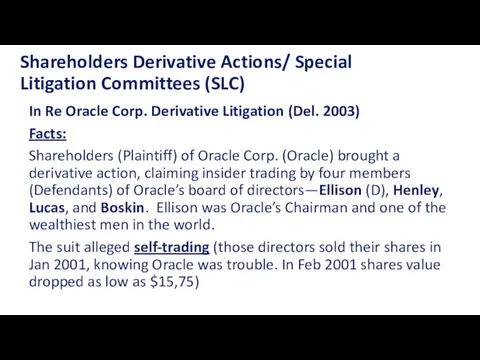

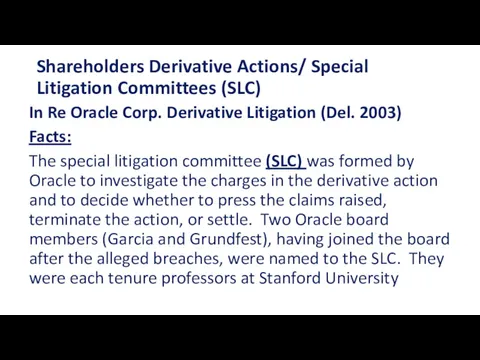

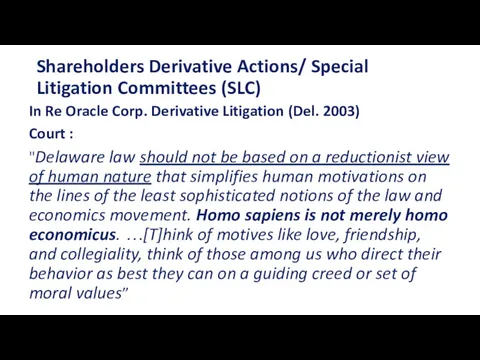

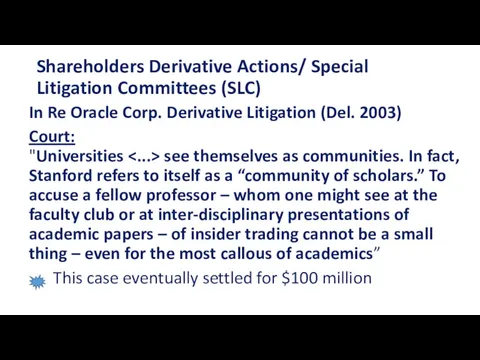

- 65. Shareholders Derivative Actions/ Special Litigation Committees (SLC) In Re Oracle Corp. Derivative Litigation (Del. 2003) Facts:

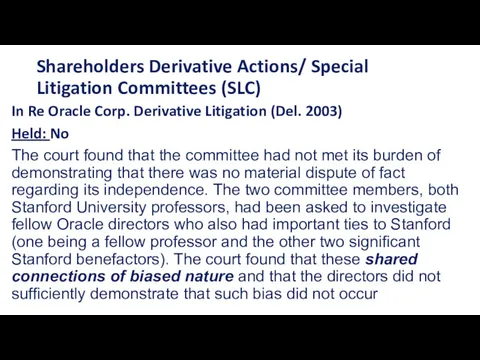

- 66. Shareholders Derivative Actions/ Special Litigation Committees (SLC) In Re Oracle Corp. Derivative Litigation (Del. 2003) Facts:

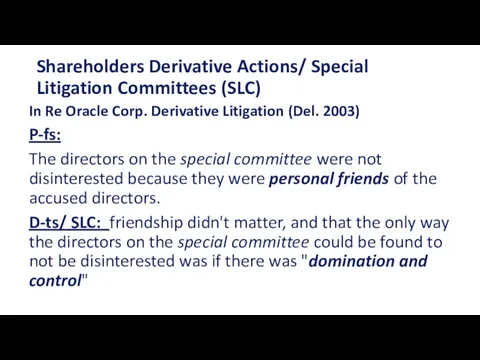

- 67. Shareholders Derivative Actions/ Special Litigation Committees (SLC) In Re Oracle Corp. Derivative Litigation (Del. 2003) P-fs:

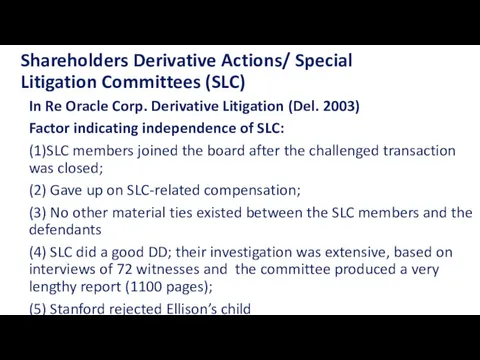

- 68. Shareholders Derivative Actions/ Special Litigation Committees (SLC) In Re Oracle Corp. Derivative Litigation (Del. 2003) Factor

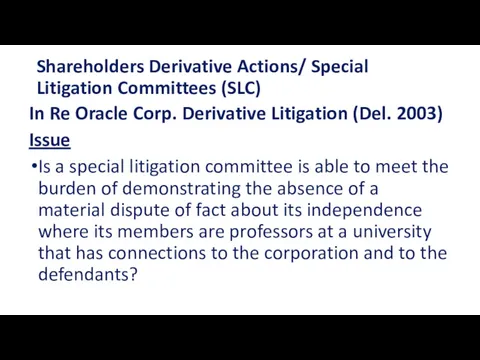

- 69. Shareholders Derivative Actions/ Special Litigation Committees (SLC) In Re Oracle Corp. Derivative Litigation (Del. 2003) Issue

- 70. Shareholders Derivative Actions/ Special Litigation Committees (SLC) In Re Oracle Corp. Derivative Litigation (Del. 2003) Held:

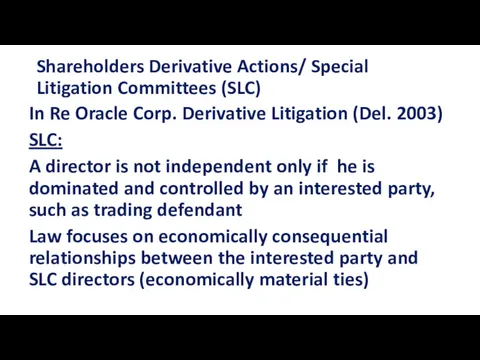

- 71. Shareholders Derivative Actions/ Special Litigation Committees (SLC) In Re Oracle Corp. Derivative Litigation (Del. 2003) SLC:

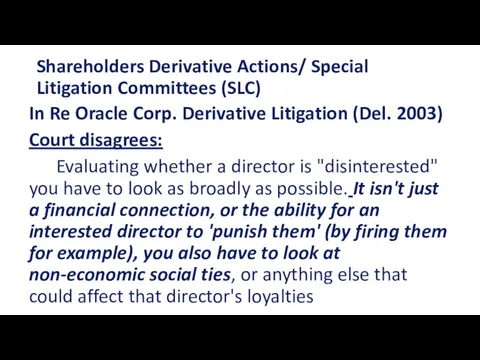

- 72. Shareholders Derivative Actions/ Special Litigation Committees (SLC) In Re Oracle Corp. Derivative Litigation (Del. 2003) Court

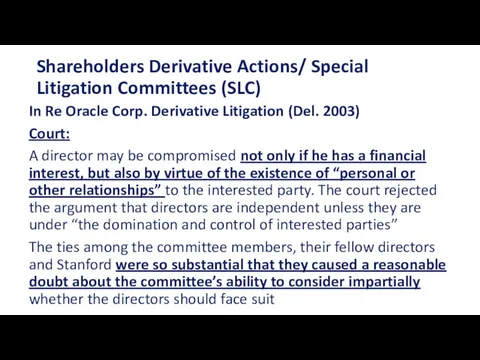

- 73. Shareholders Derivative Actions/ Special Litigation Committees (SLC) In Re Oracle Corp. Derivative Litigation (Del. 2003) Court:

- 74. Shareholders Derivative Actions/ Special Litigation Committees (SLC) In Re Oracle Corp. Derivative Litigation (Del. 2003) Court

- 75. Shareholders Derivative Actions/ Special Litigation Committees (SLC) In Re Oracle Corp. Derivative Litigation (Del. 2003) Court:

- 77. Скачать презентацию

Производные иски

”Производный иск – это дитя неспокойного брака акционеров и менеджмента,

Производные иски

”Производный иск – это дитя неспокойного брака акционеров и менеджмента,

Agency problem/ проблема агентских издержек

Система корпоративного управления во всем мире с

Agency problem/ проблема агентских издержек

Система корпоративного управления во всем мире с

Производные иски

Решение agency problem - выработка таких механизмов eх post контроля,

Производные иски

Решение agency problem - выработка таких механизмов eх post контроля,

Dodge vs. Ford Motor Co.

Хозяйственная корпорация создается и служит первоочередно

Dodge vs. Ford Motor Co.

Хозяйственная корпорация создается и служит первоочередно

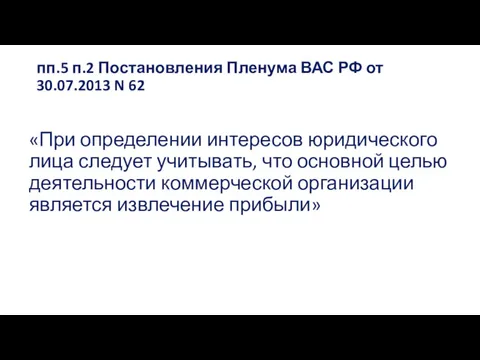

пп.5 п.2 Постановления Пленума ВАС РФ от 30.07.2013 N 62

«При

пп.5 п.2 Постановления Пленума ВАС РФ от 30.07.2013 N 62

«При

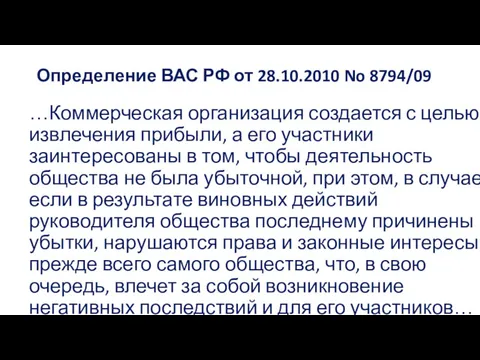

Определение ВАС РФ от 28.10.2010 No 8794/09

…Коммерческая организация создается с

Определение ВАС РФ от 28.10.2010 No 8794/09

…Коммерческая организация создается с

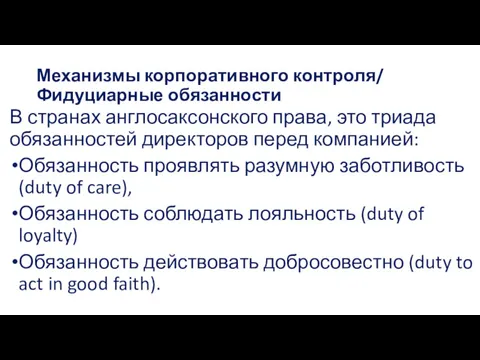

Механизмы корпоративного контроля/ Фидуциарные обязанности

В странах англосаксонского права, это триада обязанностей

Механизмы корпоративного контроля/ Фидуциарные обязанности

В странах англосаксонского права, это триада обязанностей

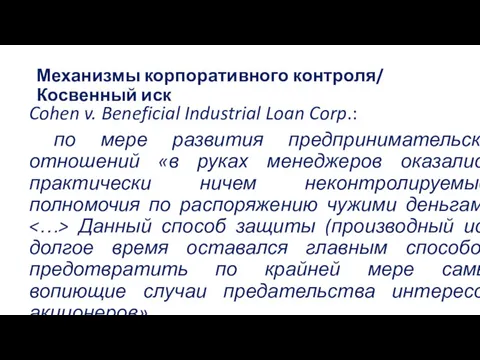

Механизмы корпоративного контроля/ Косвенный иск

Cohen v. Beneficial Industrial Loan Corp.:

по

Механизмы корпоративного контроля/ Косвенный иск

Cohen v. Beneficial Industrial Loan Corp.:

по

Косвенный иск

Производный иск позволяет корпоративным участникам выступать своего рода надзирателями при

Косвенный иск

Производный иск позволяет корпоративным участникам выступать своего рода надзирателями при

Cт. 23.1 Федеральных правил гражданского судопроизводства США

«Данное правило применяется, когда

Cт. 23.1 Федеральных правил гражданского судопроизводства США

«Данное правило применяется, когда

Ключевая проблема косвенных исков

Поиск точки равновесия между необходимостью наделения инвесторов правами

Ключевая проблема косвенных исков

Поиск точки равновесия между необходимостью наделения инвесторов правами

Ключевая проблема косвенных исков

Дмитрий Степанов:

Все корпоративное законодательство можно представить в

Ключевая проблема косвенных исков

Дмитрий Степанов:

Все корпоративное законодательство можно представить в

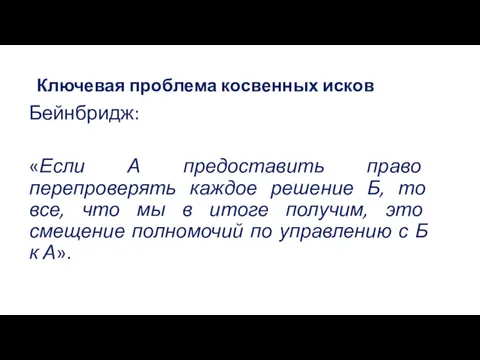

Ключевая проблема косвенных исков

Бейнбридж:

«Если А предоставить право перепроверять каждое решение

Ключевая проблема косвенных исков

Бейнбридж:

«Если А предоставить право перепроверять каждое решение

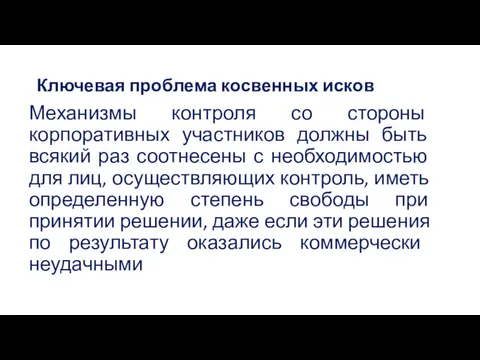

Ключевая проблема косвенных исков

Механизмы контроля со стороны корпоративных участников должны быть

Ключевая проблема косвенных исков

Механизмы контроля со стороны корпоративных участников должны быть

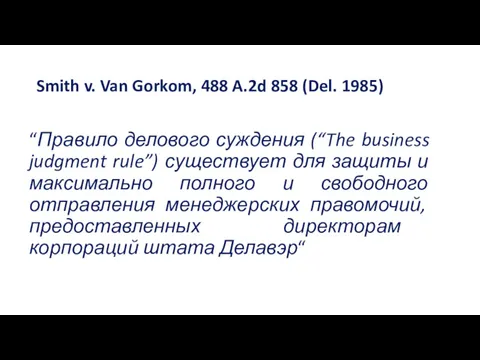

Smith v. Van Gorkom, 488 A.2d 858 (Del. 1985)

“Правило делового суждения

Smith v. Van Gorkom, 488 A.2d 858 (Del. 1985)

“Правило делового суждения

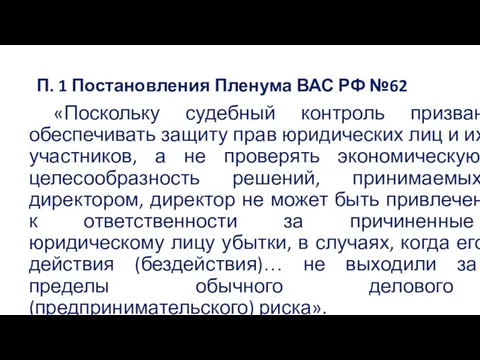

П. 1 Постановления Пленума ВАС РФ №62

«Поскольку судебный контроль призван

П. 1 Постановления Пленума ВАС РФ №62

«Поскольку судебный контроль призван

История развития косвенных исков

Паулианов иск (actio Pauliana): возможность оспаривания кредитором сделки,

История развития косвенных исков

Паулианов иск (actio Pauliana): возможность оспаривания кредитором сделки,

История развития косвенный исков

Глава III.1 Закона о банкротстве: право оспаривать

История развития косвенный исков

Глава III.1 Закона о банкротстве: право оспаривать

История развития косвенных исков

Однако исторически право на производный иск – то

История развития косвенных исков

Однако исторически право на производный иск – то

Решение Государственного высшего торгового суда Германии (Reichsoberhandelsgerisht) 1877 г.

«Акционер не имеет

Решение Государственного высшего торгового суда Германии (Reichsoberhandelsgerisht) 1877 г.

«Акционер не имеет

И. Т. Тарасов

«Воззрения исследователей в этом случае диаметрально противоположны: одни

И. Т. Тарасов

«Воззрения исследователей в этом случае диаметрально противоположны: одни

И. Т. Тарасов (склоняясь к первой позиции):

«Между правлением и поверочным советом,

И. Т. Тарасов (склоняясь к первой позиции):

«Между правлением и поверочным советом,

А. И. Каминка

Было бы вредно, если бы из среды акционерной толпы

А. И. Каминка

Было бы вредно, если бы из среды акционерной толпы

Идея косвенного иска

Дать миноритарию возможность предъявить в защиту интересов юридического

Идея косвенного иска

Дать миноритарию возможность предъявить в защиту интересов юридического

ПОЧЕМУ ИСК ПРОИЗВОДНЫЙ (КОСВЕННЫЙ)(DERIVATIVE)?

(1) Данный иск является косвенным, так как выгода

ПОЧЕМУ ИСК ПРОИЗВОДНЫЙ (КОСВЕННЫЙ)(DERIVATIVE)?

(1) Данный иск является косвенным, так как выгода

ПОЧЕМУ ИСК ПРОИЗВОДНЫЙ (КОСВЕННЫЙ)(DERIVATIVE)?

(2) В случае удовлетворения требований, предъявленного в рамках

ПОЧЕМУ ИСК ПРОИЗВОДНЫЙ (КОСВЕННЫЙ)(DERIVATIVE)?

(2) В случае удовлетворения требований, предъявленного в рамках

ПОЧЕМУ ИСК ПРОИЗВОДНЫЙ (КОСВЕННЫЙ)(DERIVATIVE)?

(3) У заявителя есть юридически значимое требование лишь

ПОЧЕМУ ИСК ПРОИЗВОДНЫЙ (КОСВЕННЫЙ)(DERIVATIVE)?

(3) У заявителя есть юридически значимое требование лишь

Применение косвенных исков по аналогии к трастам

До дела Foss (1843)

Применение косвенных исков по аналогии к трастам

До дела Foss (1843)

Robinson vs. Smith, 3 Paige Ch. 222 (NY. Ch. 1832:

Суд,

Robinson vs. Smith, 3 Paige Ch. 222 (NY. Ch. 1832:

Суд,

Taylor vs Miami Exporting Co., 5 Ohio 162 (1831):

Суд со ссылкой

Taylor vs Miami Exporting Co., 5 Ohio 162 (1831):

Суд со ссылкой

Foss v Harbottle (1843) 67 ER 189.

В данном деле

Foss v Harbottle (1843) 67 ER 189.

В данном деле

Foss v Harbottle (1843) 67 ER 189.

Суд определил, что

Foss v Harbottle (1843) 67 ER 189.

Суд определил, что

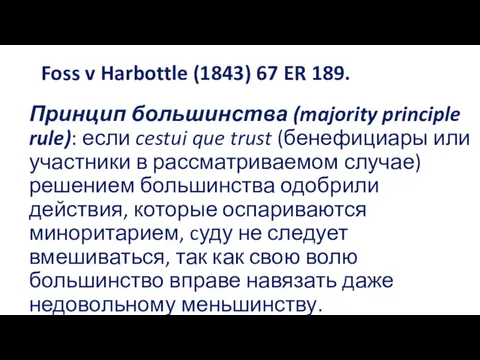

Foss v Harbottle (1843) 67 ER 189.

Принцип большинства (majority

Foss v Harbottle (1843) 67 ER 189.

Принцип большинства (majority

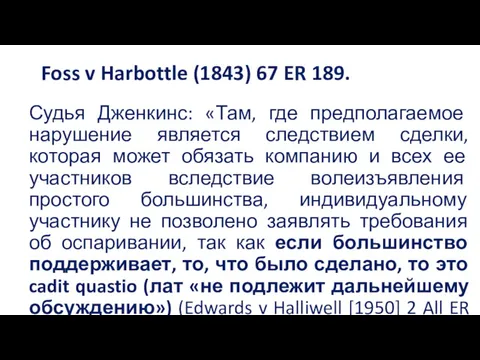

Foss v Harbottle (1843) 67 ER 189.

Судья Дженкинс: «Там,

Foss v Harbottle (1843) 67 ER 189.

Судья Дженкинс: «Там,

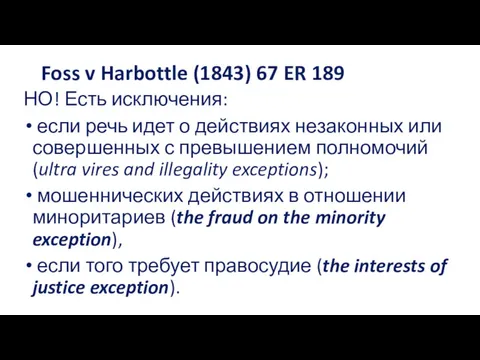

Foss v Harbottle (1843) 67 ER 189

НО! Есть исключения:

Foss v Harbottle (1843) 67 ER 189

НО! Есть исключения:

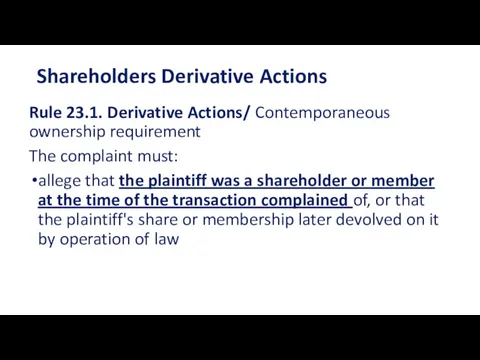

Shareholders Derivative Actions

Rule 23.1. Derivative Actions/ Contemporaneous ownership requirement

The complaint

Shareholders Derivative Actions

Rule 23.1. Derivative Actions/ Contemporaneous ownership requirement

The complaint

Shareholders Derivative Actions

Rule 23.1. Derivative Actions/Demand requirement

The complaint must state with

Shareholders Derivative Actions

Rule 23.1. Derivative Actions/Demand requirement

The complaint must state with

Shareholders Derivative Actions

Gordon v. Elliman (NY):

“By their very nature shareholder derivative

Shareholders Derivative Actions

Gordon v. Elliman (NY):

“By their very nature shareholder derivative

Shareholders Derivative Actions/ Personal v. Derivative suits

Eisenberg v. Flying Tiger Line

Shareholders Derivative Actions/ Personal v. Derivative suits

Eisenberg v. Flying Tiger Line

Shareholders Derivative Actions/ Personal v. Derivative suits

Eisenberg v. Flying Tiger Line

Shareholders Derivative Actions/ Personal v. Derivative suits

Eisenberg v. Flying Tiger Line

Shareholders Derivative Actions/ Personal v. Derivative suits

Eisenberg v. Flying Tiger Line

Shareholders Derivative Actions/ Personal v. Derivative suits

Eisenberg v. Flying Tiger Line

Shareholders Derivative Actions/ Personal v. Derivative suits

Security for Expenses (§ 627

Shareholders Derivative Actions/ Personal v. Derivative suits

Security for Expenses (§ 627

Shareholders Derivative Actions/ Personal v. Derivative suits

Eisenberg v. Flying Tiger Line

Shareholders Derivative Actions/ Personal v. Derivative suits

Eisenberg v. Flying Tiger Line

Shareholders Derivative Actions/ Personal v. Derivative suits

Eisenberg v. Flying Tiger Line

Shareholders Derivative Actions/ Personal v. Derivative suits

Eisenberg v. Flying Tiger Line

Shareholders Derivative Actions/ Personal v. Derivative suits

Eisenberg v. Flying Tiger Line

Shareholders Derivative Actions/ Personal v. Derivative suits

Eisenberg v. Flying Tiger Line

Shareholders Derivative Actions/ Personal v. Derivative suits

Eisenberg v. Flying Tiger Line

Shareholders Derivative Actions/ Personal v. Derivative suits

Eisenberg v. Flying Tiger Line

Shareholders Derivative Actions/ Personal v. Derivative suits

Eisenberg v. Flying Tiger Line

Shareholders Derivative Actions/ Personal v. Derivative suits

Eisenberg v. Flying Tiger Line

Shareholders Derivative Actions/ Personal v. Derivative suits

Delaware Special Injury Test (Tooly

Shareholders Derivative Actions/ Personal v. Derivative suits

Delaware Special Injury Test (Tooly

Shareholders Derivative Actions/ Demand Requirement

Most states (including Delaware) require shareholders who

Shareholders Derivative Actions/ Demand Requirement

Most states (including Delaware) require shareholders who

Shareholders Derivative Actions/ The Requirnment of Demand on Directors

Grimes v. Donald

Shareholders Derivative Actions/ The Requirnment of Demand on Directors

Grimes v. Donald

Shareholders Derivative Actions/ The Requirnment of Demand on Directors

Grimes v. Donald

Shareholders Derivative Actions/ The Requirnment of Demand on Directors

Grimes v. Donald

Shareholders Derivative Actions/ The Requirement of Demand on Directors

Grimes v. Donald

Shareholders Derivative Actions/ The Requirement of Demand on Directors

Grimes v. Donald

Shareholders Derivative Actions/ The Requirement of Demand on Directors

Grimes v. Donald

Shareholders Derivative Actions/ The Requirement of Demand on Directors

Grimes v. Donald

Shareholders Derivative Actions/ The Requirement of Demand on Directors

Grimes v. Donald

Shareholders Derivative Actions/ The Requirement of Demand on Directors

Grimes v. Donald

Shareholders Derivative Actions/ The Requirement of Demand on Directors

Grimes v. Donald

Shareholders Derivative Actions/ The Requirement of Demand on Directors

Grimes v. Donald

Shareholders Derivative Actions/ The Requirement of Demand on Directors

DE rule for

Shareholders Derivative Actions/ The Requirement of Demand on Directors

DE rule for

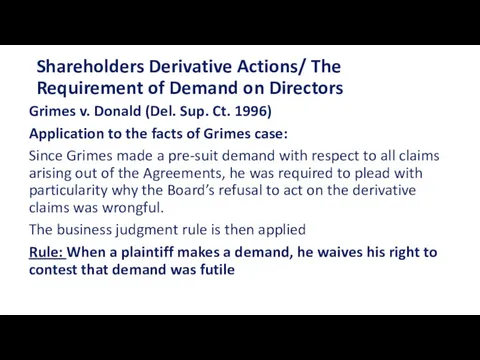

Shareholders Derivative Actions/ The Requirement of Demand on Directors

Grimes v. Donald

Shareholders Derivative Actions/ The Requirement of Demand on Directors

Grimes v. Donald

Shareholders Derivative Actions/ The Requirement of Demand on Directors

Grimes v. Donald

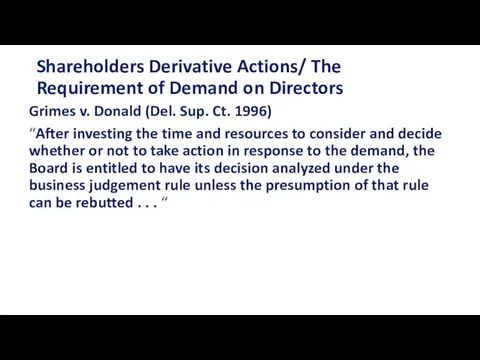

Shareholders Derivative Actions/ The Requirement of Demand on Directors

Grimes v. Donald

Shareholders Derivative Actions/ The Requirement of Demand on Directors

Grimes v. Donald

Shareholders Derivative Actions/ The Requirement of Demand on Directors

Grimes v. Donald

Shareholders Derivative Actions/ The Requirement of Demand on Directors

Grimes v. Donald

Shareholders Derivative Actions/ The Requirement of Demand on Directors

Grimes v. Donald

Shareholders Derivative Actions/ The Requirement of Demand on Directors

Grimes v. Donald

Shareholders Derivative Actions/ The Requirement of Demand on Directors

Grimes v. Donald

Shareholders Derivative Actions/ Special Litigation Committees (SLC)

Zapata Corp. v. Maldonado (Del.

Shareholders Derivative Actions/ Special Litigation Committees (SLC)

Zapata Corp. v. Maldonado (Del.

Shareholders Derivative Actions/ Special Litigation Committees (SLC)

Zapata Corp. v. Maldonado (Del.

Shareholders Derivative Actions/ Special Litigation Committees (SLC)

Zapata Corp. v. Maldonado (Del.

Shareholders Derivative Actions/ Special Litigation Committees (SLC)

In Re Oracle Corp. Derivative

Shareholders Derivative Actions/ Special Litigation Committees (SLC)

In Re Oracle Corp. Derivative

Shareholders Derivative Actions/ Special Litigation Committees (SLC)

In Re Oracle Corp. Derivative

Shareholders Derivative Actions/ Special Litigation Committees (SLC)

In Re Oracle Corp. Derivative

Shareholders Derivative Actions/ Special Litigation Committees (SLC)

In Re Oracle Corp. Derivative

Shareholders Derivative Actions/ Special Litigation Committees (SLC)

In Re Oracle Corp. Derivative

Shareholders Derivative Actions/ Special Litigation Committees (SLC)

In Re Oracle Corp. Derivative

Shareholders Derivative Actions/ Special Litigation Committees (SLC)

In Re Oracle Corp. Derivative

Shareholders Derivative Actions/ Special Litigation Committees (SLC)

In Re Oracle Corp. Derivative

Shareholders Derivative Actions/ Special Litigation Committees (SLC)

In Re Oracle Corp. Derivative

Shareholders Derivative Actions/ Special Litigation Committees (SLC)

In Re Oracle Corp. Derivative

Shareholders Derivative Actions/ Special Litigation Committees (SLC)

In Re Oracle Corp. Derivative

Shareholders Derivative Actions/ Special Litigation Committees (SLC)

In Re Oracle Corp. Derivative

Shareholders Derivative Actions/ Special Litigation Committees (SLC)

In Re Oracle Corp. Derivative

Shareholders Derivative Actions/ Special Litigation Committees (SLC)

In Re Oracle Corp. Derivative

Shareholders Derivative Actions/ Special Litigation Committees (SLC)

In Re Oracle Corp. Derivative

Shareholders Derivative Actions/ Special Litigation Committees (SLC)

In Re Oracle Corp. Derivative

Shareholders Derivative Actions/ Special Litigation Committees (SLC)

In Re Oracle Corp. Derivative

Shareholders Derivative Actions/ Special Litigation Committees (SLC)

In Re Oracle Corp. Derivative

Shareholders Derivative Actions/ Special Litigation Committees (SLC)

In Re Oracle Corp. Derivative

Shareholders Derivative Actions/ Special Litigation Committees (SLC)

In Re Oracle Corp. Derivative

Shareholders Derivative Actions/ Special Litigation Committees (SLC)

In Re Oracle Corp. Derivative

Коммерческая тайна

Коммерческая тайна Конституционные обязанности человека и гражданина

Конституционные обязанности человека и гражданина Обучение по направлению противодействия отмыванию доходов и финансированию терроризма

Обучение по направлению противодействия отмыванию доходов и финансированию терроризма Сертификация. Принципы, цели, задачи. Особенности сертификации транспортных услуг

Сертификация. Принципы, цели, задачи. Особенности сертификации транспортных услуг Собственность: сущность и виды, влияние на общество

Собственность: сущность и виды, влияние на общество Правовой режим земель транспорта

Правовой режим земель транспорта Государство. Характеристика государства. Государственное устройство. Форма государства. Форма правления. Политический режим

Государство. Характеристика государства. Государственное устройство. Форма государства. Форма правления. Политический режим Специфика технологий социальной работы в сфере занятости населения

Специфика технологий социальной работы в сфере занятости населения Право, вопросы кодификатора. (ГИА по обществознанию, 9 класс. Тема 6, часть 2)

Право, вопросы кодификатора. (ГИА по обществознанию, 9 класс. Тема 6, часть 2) Причины образования Российского централизованного государства. Возвышение Москвы

Причины образования Российского централизованного государства. Возвышение Москвы Основания возникновения гражданских правоотношений. Сделки

Основания возникновения гражданских правоотношений. Сделки Международное право

Международное право Охрана изображения гражданина. Право на неприкосновенность личного изображения

Охрана изображения гражданина. Право на неприкосновенность личного изображения Таможенное дело как совокупность методов и средств обеспечения таможенного регулирования

Таможенное дело как совокупность методов и средств обеспечения таможенного регулирования Организация отдельного расследования

Организация отдельного расследования Брейн-ринг Что я знаю о наркотиках?

Брейн-ринг Что я знаю о наркотиках? Письменная и устная консультации специалиста как источник доказательств в судопроизводстве

Письменная и устная консультации специалиста как источник доказательств в судопроизводстве Основні положення Закону України Про Національну поліцію

Основні положення Закону України Про Національну поліцію Объекты гражданских прав

Объекты гражданских прав Қазақстан Республикасының Конституциялық Кеңесі

Қазақстан Республикасының Конституциялық Кеңесі Нормы права. Система права

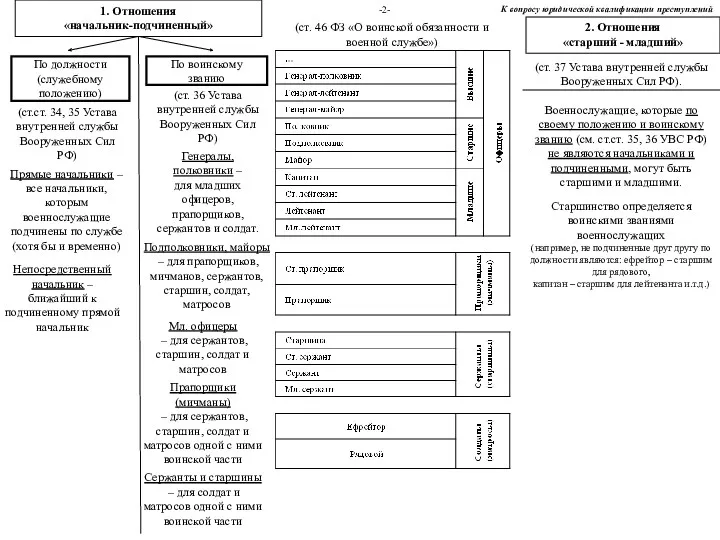

Нормы права. Система права Ст. 46 ФЗ О воинской обязанности и военной службе

Ст. 46 ФЗ О воинской обязанности и военной службе Законодательная власть в Италии и Иране

Законодательная власть в Италии и Иране Правовое государство. (Тема 6)

Правовое государство. (Тема 6) Кадастровый инженер

Кадастровый инженер Әкімшілік құқық бойынша тәртіптік-құқықтық мәжбүрлеу

Әкімшілік құқық бойынша тәртіптік-құқықтық мәжбүрлеу Правосубъектность международных организаций – понятие, признаки и виды международных организаций

Правосубъектность международных организаций – понятие, признаки и виды международных организаций Правосубъектность индивидов в международном праве

Правосубъектность индивидов в международном праве