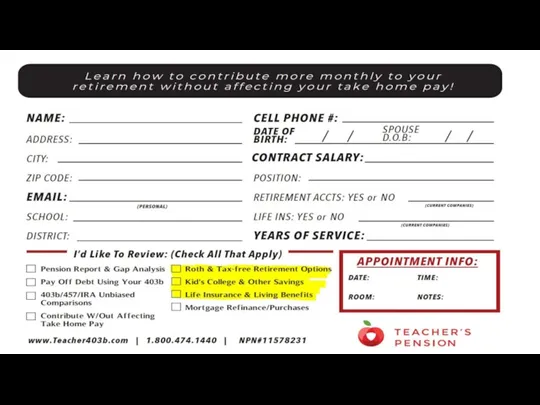

- Pension Report. Social Security

Содержание

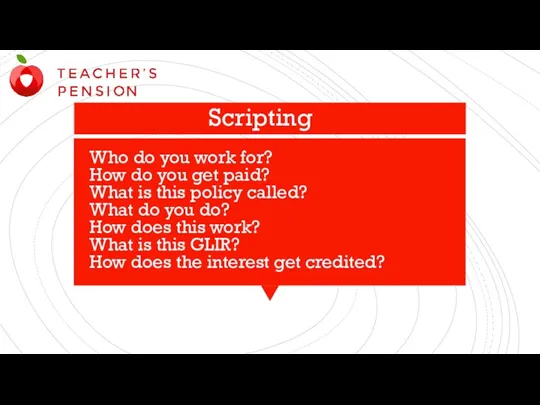

- 3. Who do you work for? How do you get paid? What is this policy called? What

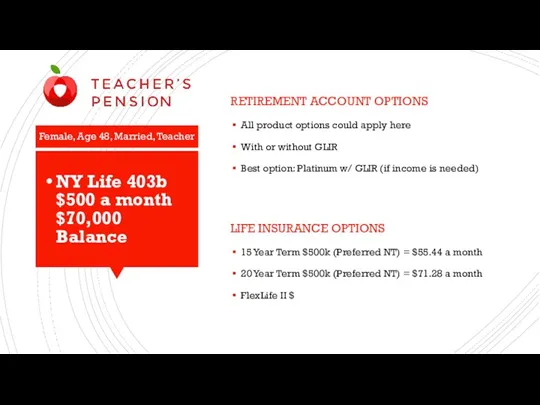

- 5. NY Life 403b $500 a month $70,000 Balance RETIREMENT ACCOUNT OPTIONS All product options could apply

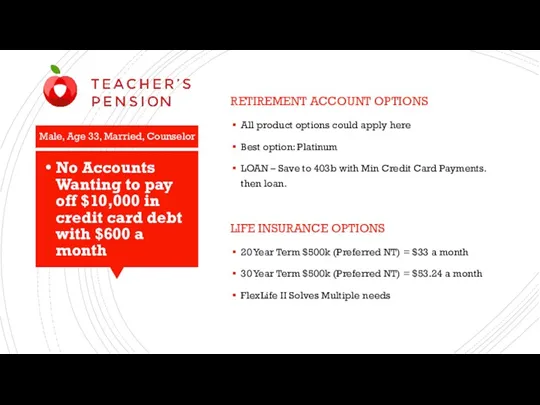

- 6. No Accounts Wanting to pay off $10,000 in credit card debt with $600 a month RETIREMENT

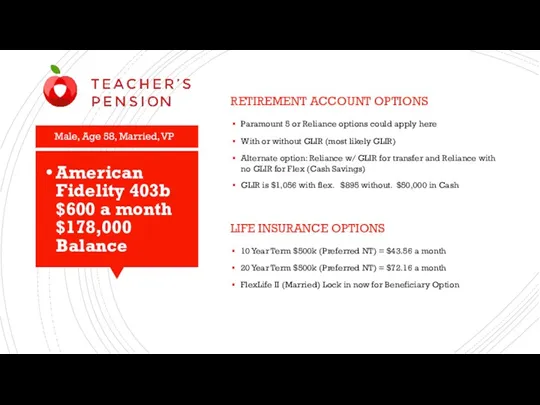

- 7. American Fidelity 403b $600 a month $178,000 Balance RETIREMENT ACCOUNT OPTIONS Paramount 5 or Reliance options

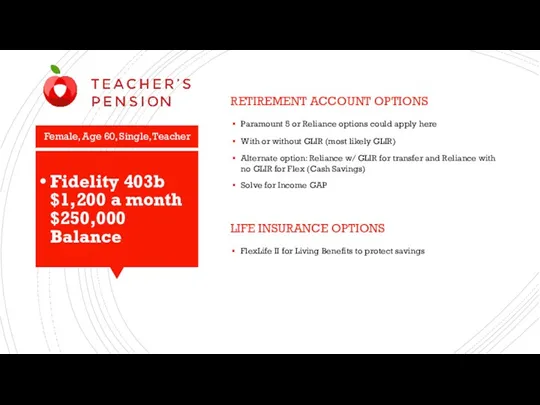

- 8. Fidelity 403b $1,200 a month $250,000 Balance RETIREMENT ACCOUNT OPTIONS Paramount 5 or Reliance options could

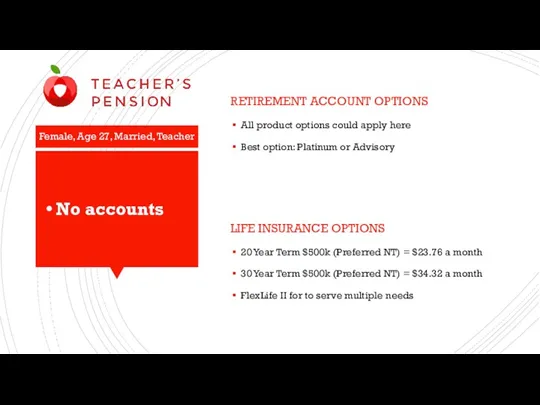

- 9. No accounts RETIREMENT ACCOUNT OPTIONS All product options could apply here Best option: Platinum or Advisory

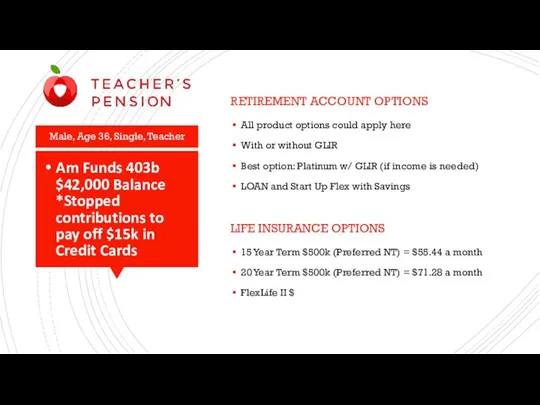

- 10. Am Funds 403b $42,000 Balance *Stopped contributions to pay off $15k in Credit Cards RETIREMENT ACCOUNT

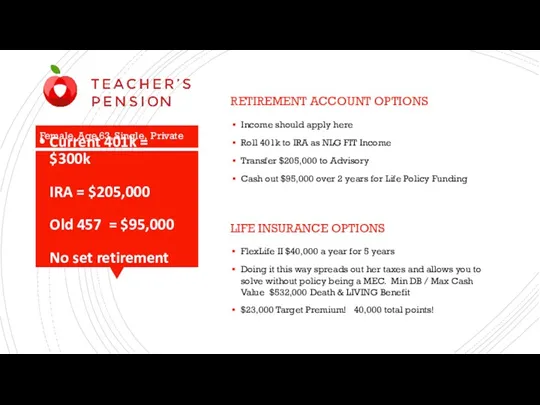

- 11. Current 401k = $300k IRA = $205,000 Old 457 = $95,000 No set retirement date RETIREMENT

- 12. FIT Retirement Series The Evolution of Flexible Premium Annuities National Life Group® is a trade name

- 13. SecurePlus Gold SecurePlus Paramount 5 SecurePlus Reliance Products of the past: One Size Fits All

- 14. More Upside Upside interest crediting potential through strategies with higher caps More Liquidity A new emergency

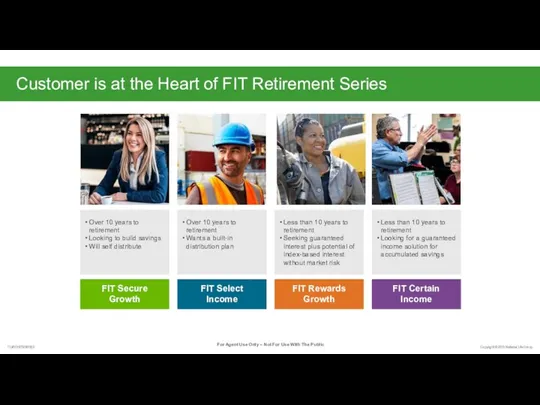

- 15. Customer is at the Heart of FIT Retirement Series Over 10 years to retirement Wants a

- 16. New Product Features

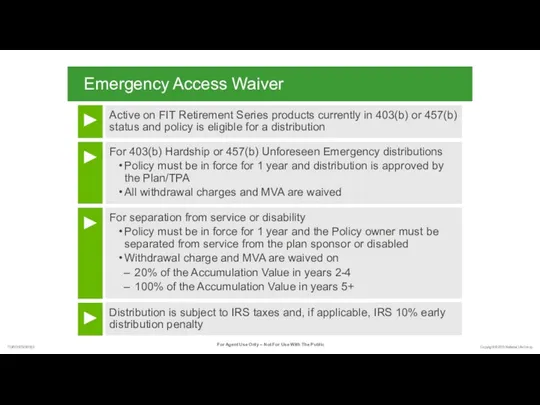

- 17. Emergency Access Waiver Active on FIT Retirement Series products currently in 403(b) or 457(b) status and

- 18. Products That Go With the Flow Regularly scheduled contributions for as little as $100 a month

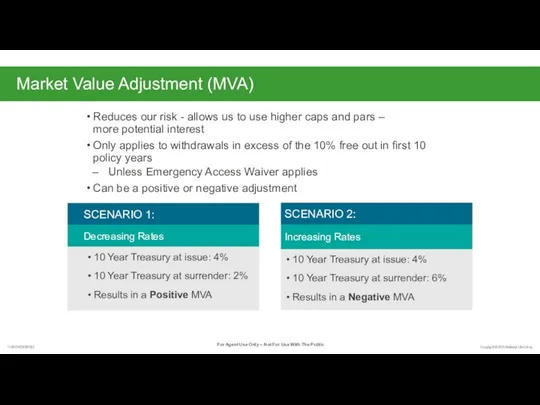

- 19. Market Value Adjustment (MVA) Reduces our risk - allows us to use higher caps and pars

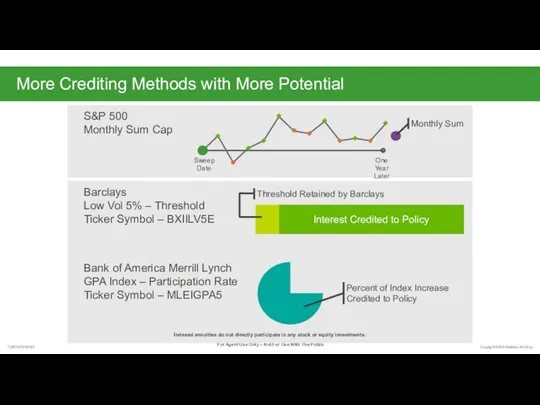

- 20. Barclays Low Vol 5% – Threshold Ticker Symbol – BXIILV5E Bank of America Merrill Lynch GPA

- 21. What is a Volatility Control Index Volatility Control Index Volatility Indexes Market Performance Lower cost, allowing

- 22. Monthly Sum Cap Monthly Cap Tracks the movement of the index on a month-to-month basis Assigns

- 23. FIT Retirement Series: Case Studies

- 24. This is Barbara Barbara has left her old job and wants to continue to build her

- 25. This is Barbara’s FIT MORE Upside potential than a bank product through: Higher caps Indices* Tax-deferred

- 26. This is Wade Wade works for a small company who does not have a 401(k). He

- 27. This is Wade’s FIT MORE Upside potential through: Higher caps Indices* Tax-deferred growth Income rider with

- 28. Market Potential GLIR with Increasing Income Withdrawal percentage for Single Life Level Option shown above; Joint

- 29. GLIR Examples Income calculation example in the 17th policy year at age 67 Multiply by Guarantee

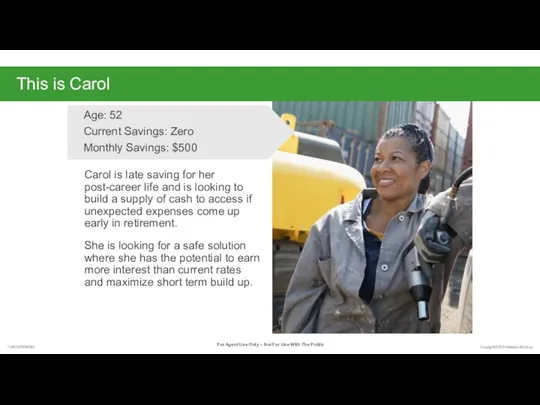

- 30. This is Carol Carol is late saving for her post-career life and is looking to build

- 31. This is Carol’s FIT MORE Upside potential than current interest rates through: 5% immediate interest credit

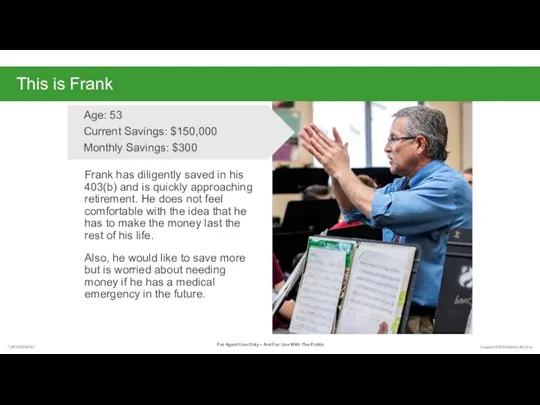

- 32. This is Frank Frank has diligently saved in his 403(b) and is quickly approaching retirement. He

- 33. This is Frank’s FIT MORE Liquidity and income certainty through: Emergency Access Waiver Income rider, at

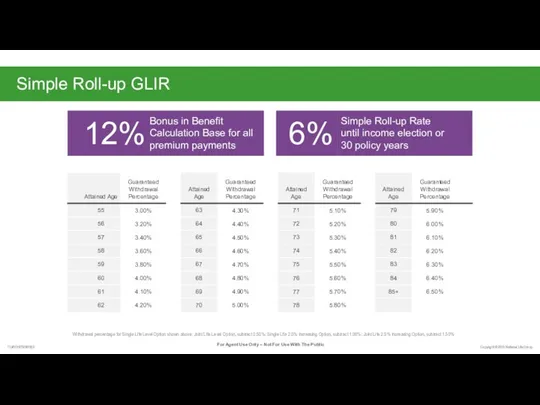

- 34. Simple Roll-up GLIR Withdrawal percentage for Single Life Level Option shown above; Joint Life Level Option,

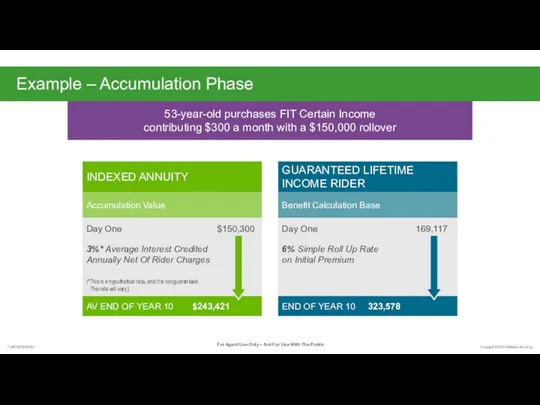

- 35. Example – Accumulation Phase 53-year-old purchases FIT Certain Income contributing $300 a month with a $150,000

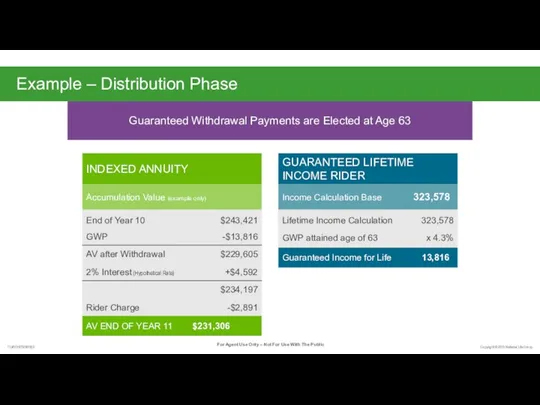

- 36. Guaranteed Withdrawal Payments are Elected at Age 63 Example – Distribution Phase GUARANTEED LIFETIME INCOME RIDER

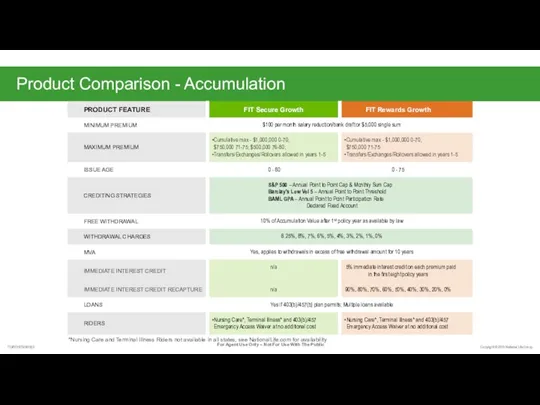

- 37. Product Comparison - Accumulation *Nursing Care and Terminal Illness Riders not available in all states, see

- 38. Product Comparison - Income *Nursing Care and Terminal Illness Riders not available in all states, see

- 39. Rates If the par rate is not specified, it is effectively 100%. If the threshold is

- 40. FIT Retirement Series Illustrations FIT Certain Income and FIT Select Income in Quick Quote on Agent

- 41. Questions?

- 42. Solutions Tailored to Consumer Needs Self Distribute FIT Select Income FIT Secure Growth FIT Rewards Growth

- 43. Barclays Low Vol 5% Index – Ticker symbol: BXIILV5E Selection of 50 companies who’s stock have

- 45. Скачать презентацию

Who do you work for?

How do you get paid?

What is this policy

Who do you work for? How do you get paid? What is this policy

NY Life 403b

$500 a month

$70,000 Balance

RETIREMENT ACCOUNT OPTIONS

All product options could apply

NY Life 403b

$500 a month

$70,000 Balance

RETIREMENT ACCOUNT OPTIONS

All product options could apply

No Accounts

Wanting to pay off $10,000 in credit card debt with $600 a

No Accounts Wanting to pay off $10,000 in credit card debt with $600 a

American Fidelity 403b

$600 a month

$178,000 Balance

RETIREMENT ACCOUNT OPTIONS

Paramount 5 or Reliance options

American Fidelity 403b

$600 a month

$178,000 Balance

RETIREMENT ACCOUNT OPTIONS

Paramount 5 or Reliance options

Fidelity 403b

$1,200 a month

$250,000 Balance

RETIREMENT ACCOUNT OPTIONS

Paramount 5 or Reliance options could

Fidelity 403b

$1,200 a month

$250,000 Balance

RETIREMENT ACCOUNT OPTIONS

Paramount 5 or Reliance options could

No accounts

RETIREMENT ACCOUNT OPTIONS

All product options could apply here

Best option: Platinum or Advisory

LIFE

No accounts

RETIREMENT ACCOUNT OPTIONS

All product options could apply here

Best option: Platinum or Advisory

LIFE

Am Funds 403b

$42,000 Balance

*Stopped contributions to pay off $15k in Credit Cards

RETIREMENT

Am Funds 403b

$42,000 Balance

*Stopped contributions to pay off $15k in Credit Cards

RETIREMENT

Current 401k = $300k

IRA = $205,000

Old 457 = $95,000

No set retirement date

RETIREMENT ACCOUNT

Current 401k = $300k

IRA = $205,000

Old 457 = $95,000

No set retirement date

RETIREMENT ACCOUNT

FIT Retirement Series

The Evolution of Flexible Premium Annuities

National Life Group® is a trade

FIT Retirement Series

The Evolution of Flexible Premium Annuities

National Life Group® is a trade

SecurePlus Gold

SecurePlus Paramount 5

SecurePlus Reliance

Products of the past:

One Size Fits All

SecurePlus Gold

SecurePlus Paramount 5

SecurePlus Reliance

Products of the past:

One Size Fits All

More Upside

Upside interest crediting potential through strategies with higher caps

More Liquidity

A new emergency

More Upside

Upside interest crediting potential through strategies with higher caps

More Liquidity

A new emergency

Customer is at the Heart of FIT Retirement Series

Over 10 years to retirement

Wants

Customer is at the Heart of FIT Retirement Series

Over 10 years to retirement

Wants

New Product Features

New Product Features

Emergency Access Waiver

Active on FIT Retirement Series products currently in 403(b) or 457(b)

Emergency Access Waiver

Active on FIT Retirement Series products currently in 403(b) or 457(b)

Products That Go With the Flow

Regularly scheduled contributions for as little as $100

Products That Go With the Flow

Regularly scheduled contributions for as little as $100

Market Value Adjustment (MVA)

Reduces our risk - allows us to use higher caps

Market Value Adjustment (MVA)

Reduces our risk - allows us to use higher caps

Barclays

Low Vol 5% – Threshold

Ticker Symbol – BXIILV5E

Bank of America Merrill Lynch

GPA Index

Barclays

Low Vol 5% – Threshold

Ticker Symbol – BXIILV5E

Bank of America Merrill Lynch GPA Index

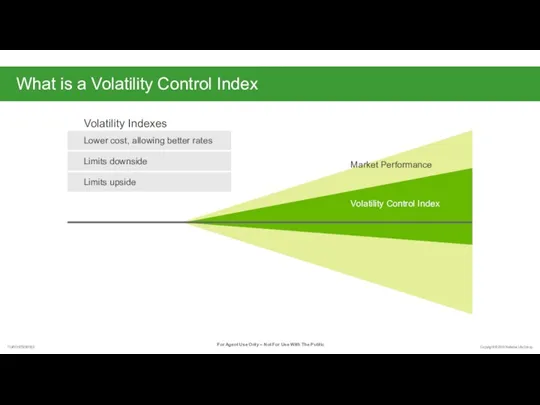

What is a Volatility Control Index

Volatility Control Index

Volatility Indexes

Market Performance

Lower cost, allowing better

What is a Volatility Control Index

Volatility Control Index

Volatility Indexes

Market Performance

Lower cost, allowing better

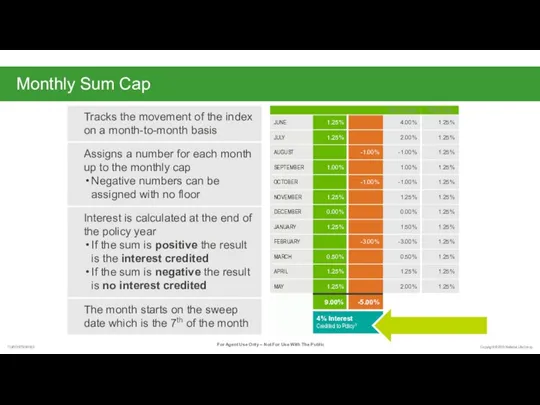

Monthly Sum Cap

Monthly Cap

Tracks the movement of the index on a month-to-month basis

Assigns

Monthly Sum Cap

Monthly Cap

Tracks the movement of the index on a month-to-month basis

Assigns

FIT Retirement Series: Case Studies

FIT Retirement Series: Case Studies

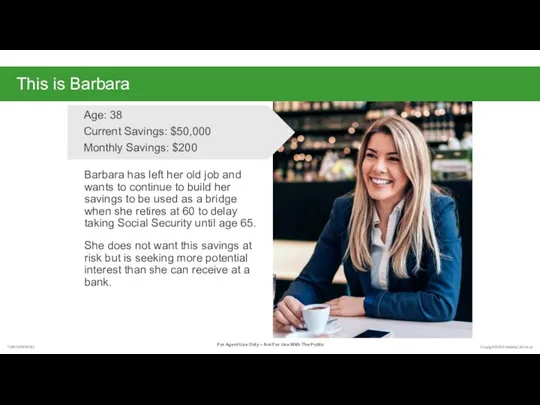

This is Barbara

Barbara has left her old job and wants to continue to

This is Barbara

Barbara has left her old job and wants to continue to

This is Barbara’s FIT

MORE Upside potential than a bank product through:

Higher caps

Indices*

Tax-deferred growth

FIT

This is Barbara’s FIT

MORE Upside potential than a bank product through:

Higher caps

Indices*

Tax-deferred growth

FIT

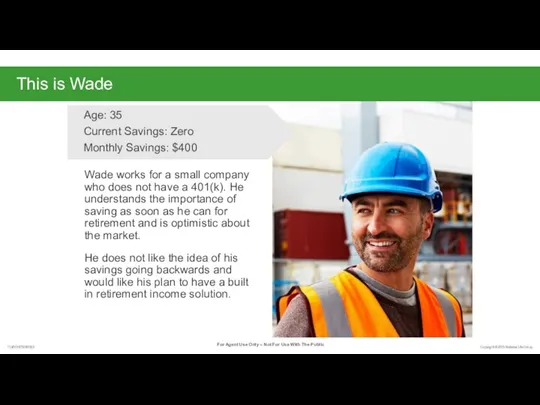

This is Wade

Wade works for a small company who does not have a

This is Wade

Wade works for a small company who does not have a

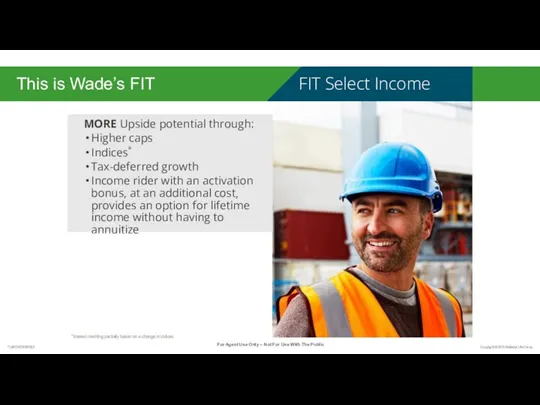

This is Wade’s FIT

MORE Upside potential through:

Higher caps

Indices*

Tax-deferred growth

Income rider with an activation

This is Wade’s FIT

MORE Upside potential through:

Higher caps

Indices*

Tax-deferred growth

Income rider with an activation

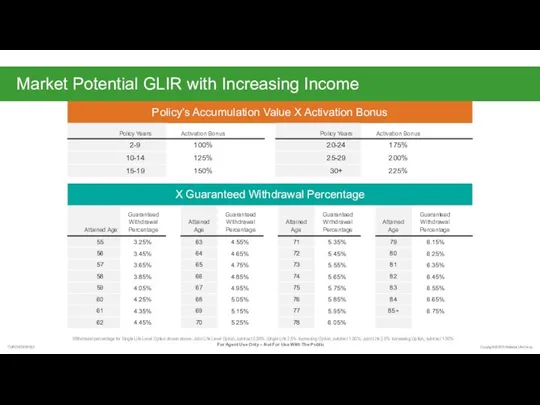

Market Potential GLIR with Increasing Income

Withdrawal percentage for Single Life Level Option shown

Market Potential GLIR with Increasing Income

Withdrawal percentage for Single Life Level Option shown

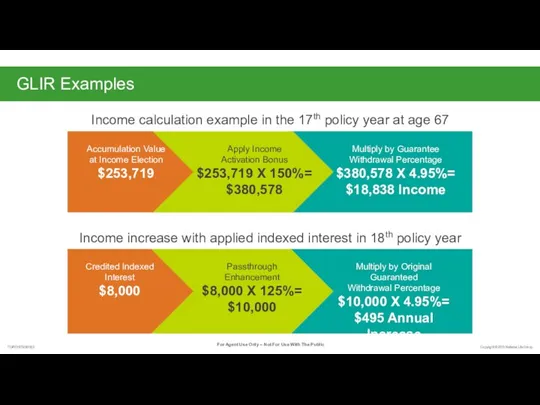

GLIR Examples

Income calculation example in the 17th policy year at age 67

Multiply by

GLIR Examples

Income calculation example in the 17th policy year at age 67

Multiply by

This is Carol

Carol is late saving for her post-career life and is looking

This is Carol

Carol is late saving for her post-career life and is looking

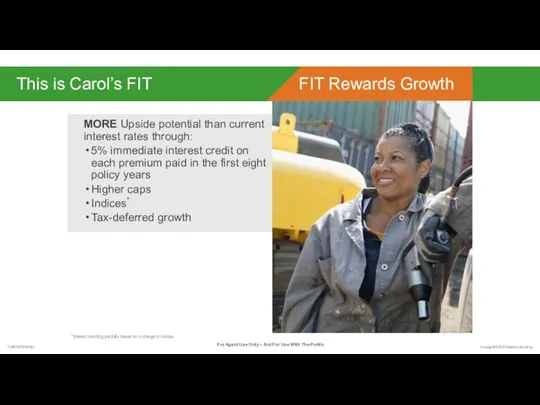

This is Carol’s FIT

MORE Upside potential than current interest rates through:

5% immediate interest

This is Carol’s FIT

MORE Upside potential than current interest rates through:

5% immediate interest

This is Frank

Frank has diligently saved in his 403(b) and is quickly approaching

This is Frank

Frank has diligently saved in his 403(b) and is quickly approaching

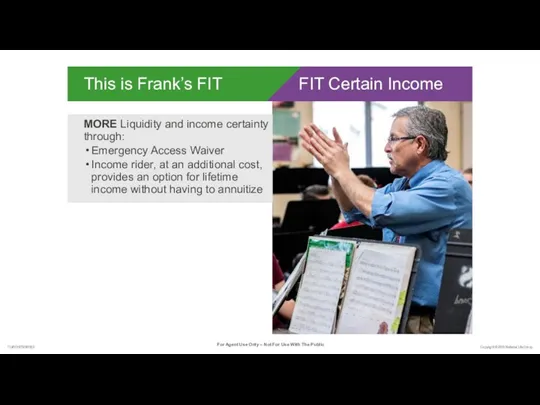

This is Frank’s FIT

MORE Liquidity and income certainty through:

Emergency Access Waiver

Income rider, at

This is Frank’s FIT

MORE Liquidity and income certainty through:

Emergency Access Waiver

Income rider, at

Simple Roll-up GLIR

Withdrawal percentage for Single Life Level Option shown above; Joint Life

Simple Roll-up GLIR

Withdrawal percentage for Single Life Level Option shown above; Joint Life

Example – Accumulation Phase

53-year-old purchases FIT Certain Income

contributing $300 a month with a

Example – Accumulation Phase

53-year-old purchases FIT Certain Income contributing $300 a month with a

Guaranteed Withdrawal Payments are Elected at Age 63

Example – Distribution Phase

GUARANTEED LIFETIME

Guaranteed Withdrawal Payments are Elected at Age 63

Example – Distribution Phase

GUARANTEED LIFETIME

Product Comparison - Accumulation

*Nursing Care and Terminal Illness Riders not available in all

Product Comparison - Accumulation

*Nursing Care and Terminal Illness Riders not available in all

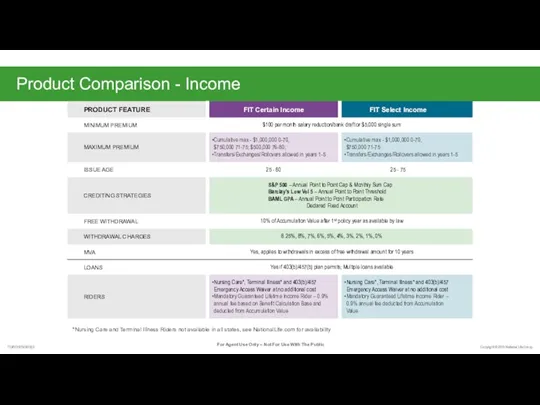

Product Comparison - Income

*Nursing Care and Terminal Illness Riders not available in all

Product Comparison - Income

*Nursing Care and Terminal Illness Riders not available in all

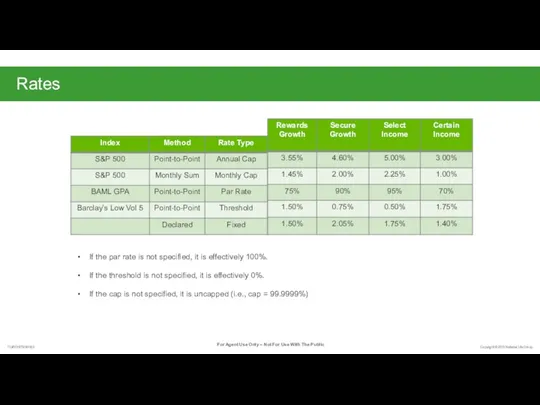

Rates

If the par rate is not specified, it is effectively 100%.

If the threshold

Rates

If the par rate is not specified, it is effectively 100%.

If the threshold

FIT Retirement Series Illustrations

FIT Certain Income

and FIT Select Income

in Quick Quote

on Agent

FIT Retirement Series Illustrations

FIT Certain Income and FIT Select Income in Quick Quote on Agent

Questions?

Questions?

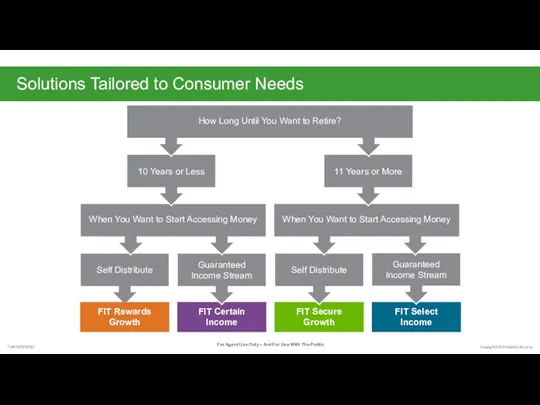

Solutions Tailored to Consumer Needs

Self Distribute

FIT Select Income

FIT Secure Growth

FIT Rewards Growth

FIT Certain

Solutions Tailored to Consumer Needs

Self Distribute

FIT Select Income

FIT Secure Growth

FIT Rewards Growth

FIT Certain

Barclays Low Vol 5% Index – Ticker symbol: BXIILV5E

Selection of 50 companies who’s

Barclays Low Vol 5% Index – Ticker symbol: BXIILV5E

Selection of 50 companies who’s

Законодательная система РФ. (9 класс)

Законодательная система РФ. (9 класс) Основания прекращения прав на землю

Основания прекращения прав на землю Процессуальное право

Процессуальное право Право, вопросы кодификатора. (ГИА по обществознанию, 9 класс. Тема 6, часть 2)

Право, вопросы кодификатора. (ГИА по обществознанию, 9 класс. Тема 6, часть 2) Российское местное самоуправление: итоги муниципальной реформы 2003-2015 г. и направления совершенствования системы МСУ

Российское местное самоуправление: итоги муниципальной реформы 2003-2015 г. и направления совершенствования системы МСУ Обстоятельства, исключающие преступность деяния

Обстоятельства, исключающие преступность деяния Государственный пожарный надзор в Российской Федерации и его задачи

Государственный пожарный надзор в Российской Федерации и его задачи Профилактика безнадзорности и правонарушений несовершеннолетних: компетенции образовательного учреждения

Профилактика безнадзорности и правонарушений несовершеннолетних: компетенции образовательного учреждения Уголовно – процессуальное право Российской Федерации

Уголовно – процессуальное право Российской Федерации Состояние и тенденции развития частных экспертных теорий

Состояние и тенденции развития частных экспертных теорий Кейсы

Кейсы ЗАГС. Описание предметной области

ЗАГС. Описание предметной области Основы противодействия экстремизму

Основы противодействия экстремизму Взаимодействие журналиста и пресс-службы

Взаимодействие журналиста и пресс-службы Юридическая этика

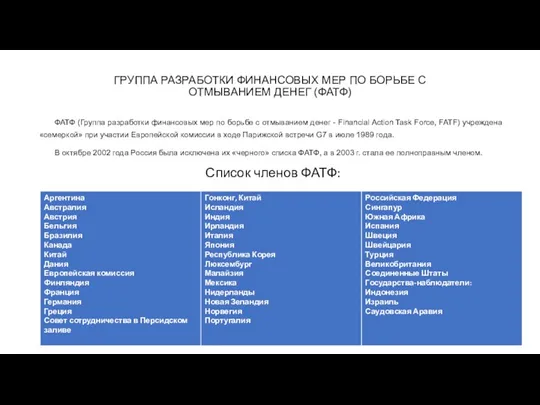

Юридическая этика Группа разработки финансовых мер по борьбе с отмыванием денег

Группа разработки финансовых мер по борьбе с отмыванием денег Описание земельного участка

Описание земельного участка Специальные звания органов внутренних дел Российской Федерации

Специальные звания органов внутренних дел Российской Федерации Правовые основы взаимоотношений полов

Правовые основы взаимоотношений полов Понятие и признаки гражданства

Понятие и признаки гражданства Правоохранительные органы РФ

Правоохранительные органы РФ Система управления трудовыми ресурсами

Система управления трудовыми ресурсами Что такое право

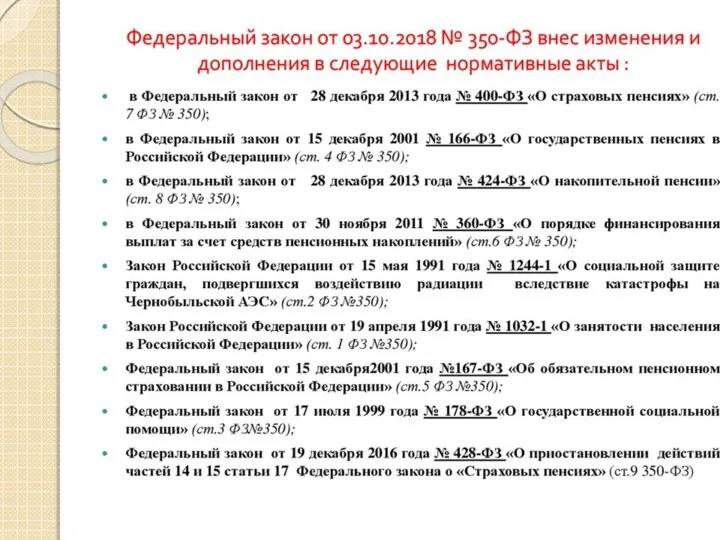

Что такое право Дополнительные социальные гарантии для лиц предпенсионного возраста в области занятости населения

Дополнительные социальные гарантии для лиц предпенсионного возраста в области занятости населения Правовий статус фізичних осіб

Правовий статус фізичних осіб Современные возможности информационно-методического сопровождения специалистов по проблеме жестокого обращения с детьми

Современные возможности информационно-методического сопровождения специалистов по проблеме жестокого обращения с детьми Занятость и трудоустройство. Порядок взаимоотношений работников и работодателей

Занятость и трудоустройство. Порядок взаимоотношений работников и работодателей Права и обязанности граждан. (11 класс)

Права и обязанности граждан. (11 класс)