- European Union Energy Policy

Содержание

- 2. European Union Energy Policy: Topic 1. Main and additional priorities of the European Union energy policy

- 3. Topic 1. Main and additional priorities of the European Union energy policy Introduction Milestones of EU

- 4. Energy is the irreplaceable part of almost every aspect of modern life from industry to transportation,

- 5. Energy is a fundamental factor in the construction of European Union project. The deep interaction and

- 6. Nevertheless, despite energy’s importance in our daily lives, despite the fact that EU project “took off”

- 7. The EU’s energy dependence (import dependence) ? ? ? Energy is the significant item on the

- 8. The issue gets further complicated with the inclusion of worries about global warming, hazardous effects of

- 9. With these challenges on the background, until recently, climate change and energy efficiency had started to

- 10. Although some of the policies are still up to the individual choices of each Member State

- 11. The milestones of EU energy policy: SUSTAINABILITY COMPETITIVENESS SECURITY OF SUPPLY

- 12. Major European documents constituting these milestones of European energy policy: Green Paper of 2006 The Commission's

- 13. SUSTAINABILITY linked to climate change 80% of greenhouse gas (GHG) emission in the Union is caused

- 14. COMPETITIVENESS aims at liberalization of energy market ? at the opening of energy markets for the

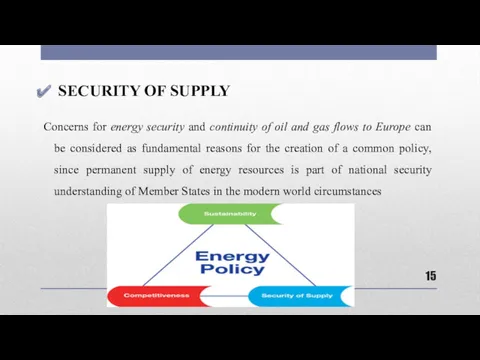

- 15. SECURITY OF SUPPLY Concerns for energy security and continuity of oil and gas flows to Europe

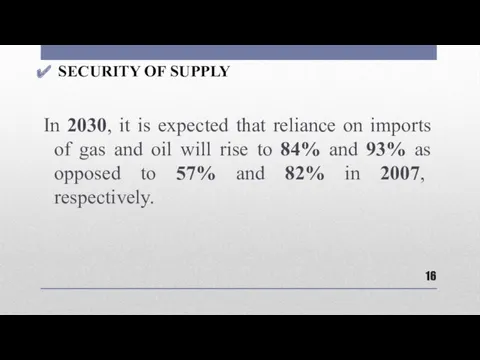

- 16. SECURITY OF SUPPLY In 2030, it is expected that reliance on imports of gas and oil

- 17. SECURITY OF SUPPLY When such a level of dependency is combined with uncertainty about the willingness

- 18. DEVELOPMENT OF EU ENERGY POLICIES OVER TIME

- 19. EVOLUTION OF EUROPEAN ENERGY UNION In the evolution of the EU itself, policies concerning energy and

- 20. European energy policy initiated as a need to be capable of responding to international energy supply

- 21. International Energy Supply Crises ? two major concerns: 1). political instability in producer countries and regional

- 22. THE RESPONSE TO SUCH CRISES: Oil Stock Directive, 1968 An amendment to the directive of 1968,

- 23. The end of Cold War ? the end of ideological, political and economic divisions between eastern

- 24. EUROPEAN ENERGY CHARTER, 1991: competition free transit taxation transparency conditions on environment and sovereignty

- 25. Between 1990 and 2000 – THREE Green Papers on ENERGY = BASELINES for a COMMON policy

- 26. 1994 – the Green Paper “For A European Union Energy Policy” to establish an internal market

- 27. 1996 – the Green Paper “Energy for the Future: Renewable Sources of Energy” incorporation of renewable

- 28. !!! 2000 – the Green Paper “Towards a European Strategy for the Security of Energy Supply”

- 29. 2005 – the Green Paper “Green Paper on Energy Efficiency or Doing More with Less” The

- 30. Russia – Ukraine crises (2006) ? Member States understood the importance of community level actions in

- 31. 2006 – the Green Paper “A European Strategy for Sustainable, Competitive and Secure Energy” competitiveness and

- 32. “An Energy Policy for Europe” introduced “20/20 Package” (2007): reducing GHG emission by 20% improving energy

- 33. 2008 - An EU Energy Security and Solidarity Action Plan infrastructure needs the diversification of energy

- 34. The Kyoto Protocol The Kyoto Protocol (1997) is an international agreement which is intended to lower

- 35. The Energy Labelling Directive requires that appliances be labelled to show their power consumption in such

- 36. EUROPEAN EMISSIONS STANDARDS Each of the standards Euro 1 to Euro 6 (the latest) represent a

- 37. INTELLIGENT ENERGY EUROPE Intelligent Energy – Europe (IEE) offered a helping hand to organisations willing to

- 38. 2011 - A Roadmap for Moving to a Competitive, Low-Carbon Economy in 2050: - reducing emissions

- 39. The latest decisions in this matter have come from the European Council of October 2014. That

- 40. Today the main goal is to establish ENERGY UNION! In 2015, the Framework Strategy for Energy

- 41. Topic 2. Fuel and energy balance of the EU

- 42. The energy balance remains subject to the national level, not common European ? A plurality of

- 43. Oil: Malta, Cyprus, Nuclear energy: France, Sweden, Belgium Coal: Poland, the Czech Republic, Bulgaria Gas: the

- 44. The energy available in the European Union comes from energy produced in the EU and from

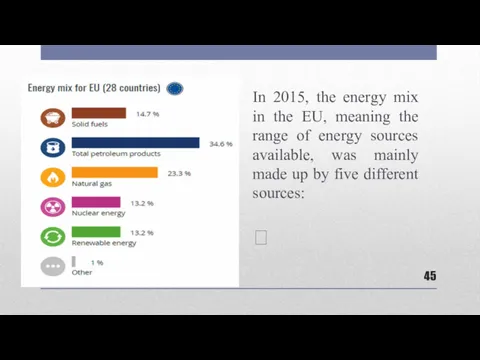

- 45. In 2015, the energy mix in the EU, meaning the range of energy sources available, was

- 46. WHAT DOES THE EU PRODUCE? Nuclear energy (29 % of total EU energy production) was the

- 47. However, the production of energy is very different from one Member State to another. The significance

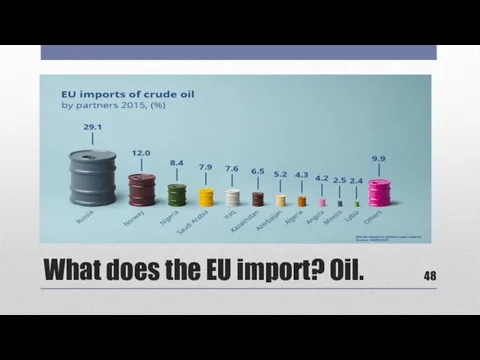

- 48. What does the EU import? Oil.

- 49. What does the EU import? Coal.

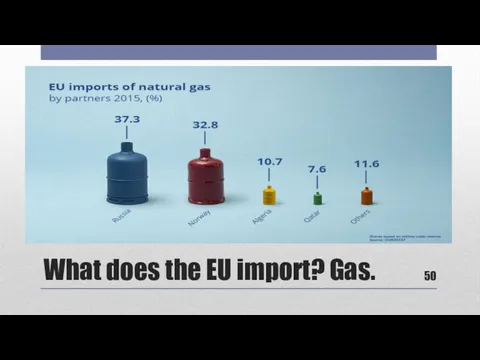

- 50. What does the EU import? Gas.

- 51. How dependent is the EU from energy produced outside the EU? In the EU in 2015,

- 52. GAS. ADVANTAGES: much lower emissions there is no need to maintain a reservoir for crude oil

- 53. The drawback of gas is the difficulty in transporting, high cost of transportation!

- 54. The largest importers of Russian gas in the European Union are Germany and Italy, accounting together

- 55. According to the European Commission, the share of Russian natural gas in the member states' domestic

- 56. Oil. Advantages. Oil is a mix of hydrocarbons that are liquid under atmospheric conditions. Therefore, the

- 57. Based on data from OPEC at the beginning of 2013 the highest proved oil reserves oil

- 58. European dependence on oil imports has grown from 76% in 2000 to over 88% in 2014.

- 59. Oil companies

- 60. More than 40% of the oil was exported from Middle Eastern countries such as Algeria, Iraq,

- 61. Coal Countries exporting coal to EU are Russia, Colombia and Australia with shares of 32.5 %,

- 62. Coal Coal, as the largest artificial contributor to carbon dioxide emissions, has been attacked for its

- 63. Nuclear energy potentially very cheap the lowest carbon emissions Nuclear power plants generate almost 30% of

- 64. Nuclear safety The EU promotes the highest safety standards for all types of civilian nuclear activity,

- 65. Radioactive waste and decommissioning Radioactive waste results from nuclear activities such as electricity generation, medicine, and

- 66. Nuclear energy France is the one country that has the most of its electricity from nuclear

- 67. Nuclear energy Russian nuclear reactors in the EU are in Bulgaria (2), Czech Republic (6), Finland

- 68. Renewable energy The use of renewable energy has many potential benefits, including a reduction in greenhouse

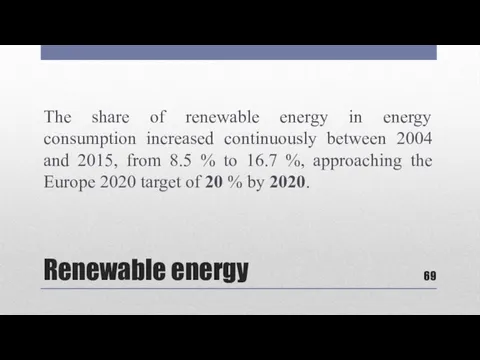

- 69. Renewable energy The share of renewable energy in energy consumption increased continuously between 2004 and 2015,

- 70. Renewable energy The share of renewable energy in the Member States was highest in Sweden (53.9

- 71. Renewable energy This positive development has been prompted by the legally binding (обладающий обязательным характером) targets

- 72. Renewable energy in the EU

- 73. Topic 3. Liberalization of EU gas and energy markets

- 74. Liberalization Process: Legislation The liberalization process of the natural gas market is a result of the

- 75. Liberalization Process In all of the Directives, there are several components that comprise the bulk of

- 76. Liberalization Process The first portion of the liberalization process requires states to grant third parties to

- 77. Liberalization Process The 2003 Directive extended third-party access to gas storage facilities in addition to the

- 78. Liberalization . Unbundling. The next aspect of the Directives is the concept of unbundling. At its

- 79. Liberalization. Interruptible contracts The EU Directives is encouraging shorter and interruptible contracts, starting in 2003. The

- 80. Liberalization. Regulatory authority The last major area of focus in liberalization reform is the creation of

- 81. Liberalization of EU gas market The Third Energy Package consists of two Directives and three Regulations:

- 82. Topic 4. EU energy diplomacy and external actions

- 83. Internal and external energy policies cannot be separated from each other due to their complimentary nature.

- 84. Concerning its ambitious goals about sustainability, renewable resources and fight against climate change the EU is

- 85. In the study of external energy policy of Europe it is possible to classify it under

- 86. Pan-European Energy Community is “common regulatory space” in other words “common trade, transit and environment rules”

- 87. European Neighbourhood Policy In the European Neighbourhood Policy Strategy Paper, the Commission indicates that “Enhancing our

- 88. EU energy goals require efficient usage of financial instruments through European Investment Bank (EIB), European Bank

- 89. The Kyoto Protocol (1997) The Kyoto Protocol is an international agreement which is intended to lower

- 90. NORWAY Norway is the second major natural gas and oil supplier to the European Union. June

- 91. Norway Norway differs from other energy suppliers to the Union because it is a member of

- 92. Norway Not only the EU needs Norway as a reliable oil and gas supplier but also

- 93. Norway Norway and the EU act together to further develop their partnership. The Commission as well

- 94. Africa Concerning EU’s dialogue with Africa, energy is incorporated within the development and governance issues. Poverty

- 95. Africa In the region, the EU policy makers associate the Union’s energy interests with broader political

- 96. Africa Nevertheless, Africa, more specifically North Africa has a significant potential not only in hydrocarbons but

- 97. Middle East Middle East is the world’s important energy producing region and world’s richest proven oil

- 98. Middle East Despite the Union’s intense energy dialogues with Russia or Caspian region, Middle East remains

- 99. Middle East Concerning the region, EU’s effort to achieve international cooperation in energy is not limited

- 100. Caspian Region Caspian region refers to five Caspian littoral states namely, Azerbaijan, Iran, Kazakhstan, Turkmenistan and

- 101. Caspian Region This identification is necessary because, if the Caspian is a sea, in line with

- 102. Caspian Region Apart from the legal status of the potential reserves, the fact that Azerbaijan, Kazakhstan

- 103. Caspian Region The institutionalization of relations with the Caspian Region countries: the INOGATE, Interstate Oil and

- 104. Caspian Region Energy outstands as the main item among the imports from the region. Nevertheless, mineral

- 105. Southern Gas Corridor The Southern Gas Corridor is an initiative of the European Commission for the

- 106. Topic 4. The EU-Russia energy dialog

- 107. Russia is the main exporter of energy resources to the European Union. This distinguishes Russia from

- 108. When Russia’s internal energy sector is examined the most outstanding feature is state’s control over resources.

- 109. Concerning the natural gas sector, again a state run monopoly, Gazprom accounts for almost 90% of

- 110. 2. NORTHERN LIGHTS AND YAMAL EUROPE Capacity: 84 bilion cubic meters per year. Partners: Gazprom, Beltrangaz,

- 111. 4. BLUE STREAM Capacity: 16 bilion cubic meters per year (expanding to 19 bcm). Partners: Gazprom,

- 112. 6. NORD STREAM 2 Capacity: 55 billion cubic meters per year. Partners: Gazprom, Shell, OMV, E.ON.

- 113. 8. EASTRING PIPELINE Capacity: 20 billion to 40 billion cubic meters per year. Partners: Eustream, Transgaz,

- 114. The institutionalization of EU-Russia relationship concerning energy can be identified by three main legal grounds: European

- 115. Due to Russia’s non-ratification of Energy Charter Treaty, the relationship between EU and Russia has to

- 117. Скачать презентацию

European Union Energy Policy:

Topic 1. Main and additional priorities of

Topic 1. Main and additional priorities of

Topic 1. Main and additional priorities of the European Union energy

Topic 1. Main and additional priorities of the European Union energy

Energy is the irreplaceable part of almost every aspect of modern

Energy is a fundamental factor in the construction of European Union

Energy is a fundamental factor in the construction of European Union

Nevertheless, despite energy’s importance in our daily lives, despite the fact

Nevertheless, despite energy’s importance in our daily lives, despite the fact

The EU’s energy dependence (import dependence) ? ? ?

Energy is

The EU’s energy dependence (import dependence) ? ? ?

Energy is

The issue gets further complicated with the inclusion of worries about

The issue gets further complicated with the inclusion of worries about

With these challenges on the background, until recently, climate change and

With these challenges on the background, until recently, climate change and

Although some of the policies are still up to the individual

Although some of the policies are still up to the individual

The milestones of EU energy policy:

SUSTAINABILITY

COMPETITIVENESS

SECURITY

The milestones of EU energy policy:

SUSTAINABILITY

COMPETITIVENESS

SECURITY

Major European documents constituting these milestones of European energy policy:

Major European documents constituting these milestones of European energy policy:

SUSTAINABILITY

linked to climate change

80% of greenhouse gas (GHG) emission in the

linked to climate change

80% of greenhouse gas (GHG) emission in the

COMPETITIVENESS

aims at liberalization of energy market ?

at the

COMPETITIVENESS

aims at liberalization of energy market ?

at the

SECURITY OF SUPPLY

Concerns for energy security and continuity of oil and

Concerns for energy security and continuity of oil and

SECURITY OF SUPPLY

In 2030, it is expected that reliance on

SECURITY OF SUPPLY

In 2030, it is expected that reliance on

SECURITY OF SUPPLY

When such a level of dependency is combined with

When such a level of dependency is combined with

DEVELOPMENT OF EU ENERGY POLICIES OVER TIME

DEVELOPMENT OF EU ENERGY POLICIES OVER TIME

EVOLUTION OF EUROPEAN ENERGY UNION

In the evolution of the EU itself,

In the evolution of the EU itself,

European energy policy initiated as a need to be capable of

European energy policy initiated as a need to be capable of

International Energy Supply Crises ? two major concerns:

1). political instability in

International Energy Supply Crises ? two major concerns:

1). political instability in

THE RESPONSE TO SUCH CRISES:

Oil Stock Directive, 1968

An amendment

THE RESPONSE TO SUCH CRISES:

Oil Stock Directive, 1968

An amendment

The end of Cold War ?

the end of ideological, political

the end of ideological, political

EUROPEAN ENERGY CHARTER, 1991:

competition

free transit

taxation

transparency

conditions on

EUROPEAN ENERGY CHARTER, 1991:

competition

free transit

taxation

transparency

conditions on

Between 1990 and 2000 – THREE Green Papers on ENERGY =

BASELINES

Between 1990 and 2000 – THREE Green Papers on ENERGY =

BASELINES

1994 – the Green Paper “For A European Union Energy Policy”

1994 – the Green Paper “For A European Union Energy Policy”

1996 – the Green Paper “Energy for the Future: Renewable

1996 – the Green Paper “Energy for the Future: Renewable

!!! 2000 – the Green Paper “Towards a European Strategy for

!!! 2000 – the Green Paper “Towards a European Strategy for

2005 – the Green Paper “Green Paper on Energy Efficiency or

2005 – the Green Paper “Green Paper on Energy Efficiency or

Russia – Ukraine crises (2006) ?

Member States understood the importance

Russia – Ukraine crises (2006) ?

Member States understood the importance

2006 – the Green Paper “A European Strategy for Sustainable, Competitive

“An Energy Policy for Europe” introduced

“20/20 Package” (2007):

reducing GHG

“An Energy Policy for Europe” introduced

“20/20 Package” (2007):

reducing GHG

2008 - An EU Energy Security and Solidarity Action Plan

infrastructure needs

2008 - An EU Energy Security and Solidarity Action Plan

infrastructure needs

The Kyoto Protocol

The Kyoto Protocol (1997) is an international agreement which

The Kyoto Protocol

The Kyoto Protocol (1997) is an international agreement which

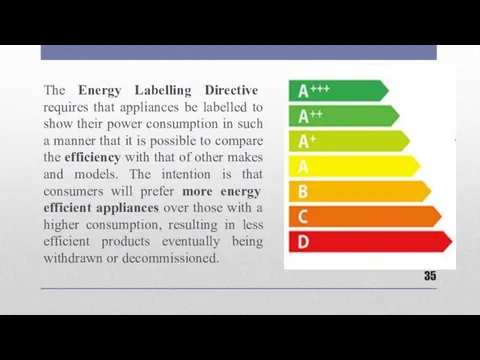

The Energy Labelling Directive requires that appliances be labelled to show

The Energy Labelling Directive requires that appliances be labelled to show

EUROPEAN EMISSIONS STANDARDS

Each of the standards Euro 1 to Euro 6

EUROPEAN EMISSIONS STANDARDS

Each of the standards Euro 1 to Euro 6

INTELLIGENT ENERGY EUROPE

Intelligent Energy – Europe (IEE) offered a helping hand

INTELLIGENT ENERGY EUROPE

Intelligent Energy – Europe (IEE) offered a helping hand

2011 - A Roadmap for Moving to a Competitive, Low-Carbon Economy

2011 - A Roadmap for Moving to a Competitive, Low-Carbon Economy

The latest decisions in this matter have come from the European

Today the main goal is to establish ENERGY UNION!

In 2015, the

Today the main goal is to establish ENERGY UNION!

In 2015, the

Topic 2. Fuel and energy balance of the EU

Topic 2. Fuel and energy balance of the EU

The energy balance remains subject to the national level, not common

Oil:

Malta, Cyprus,

Nuclear energy:

France, Sweden, Belgium

Coal:

Poland, the Czech Republic, Bulgaria

Gas:

the

Malta, Cyprus,

Nuclear energy:

France, Sweden, Belgium

Coal:

Poland, the Czech Republic, Bulgaria

Gas:

the

The energy available in the European Union comes from energy produced

In 2015, the energy mix in the EU, meaning the range

In 2015, the energy mix in the EU, meaning the range

WHAT DOES THE EU PRODUCE?

Nuclear energy (29 % of total EU

Nuclear energy (29 % of total EU

However, the production of energy is very different from one Member

What does the EU import? Oil.

What does the EU import? Oil.

What does the EU import? Coal.

What does the EU import? Coal.

What does the EU import? Gas.

What does the EU import? Gas.

How dependent is the EU from energy produced outside the EU?

In

How dependent is the EU from energy produced outside the EU?

In

GAS. ADVANTAGES:

much lower emissions

there is no need to maintain

GAS. ADVANTAGES:

much lower emissions

there is no need to maintain

The drawback of gas is the difficulty in transporting, high cost

The drawback of gas is the difficulty in transporting, high cost

The largest importers of Russian gas in the European Union are

The largest importers of Russian gas in the European Union are

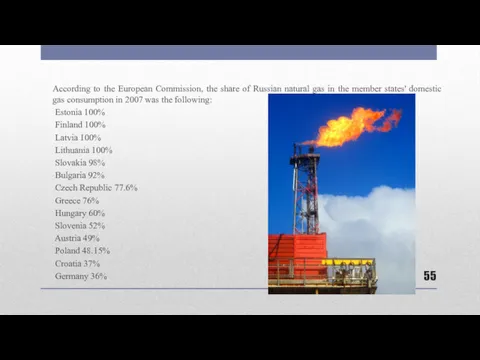

According to the European Commission, the share of Russian natural gas

According to the European Commission, the share of Russian natural gas

Oil. Advantages.

Oil is a mix of hydrocarbons that are liquid

Oil. Advantages.

Oil is a mix of hydrocarbons that are liquid

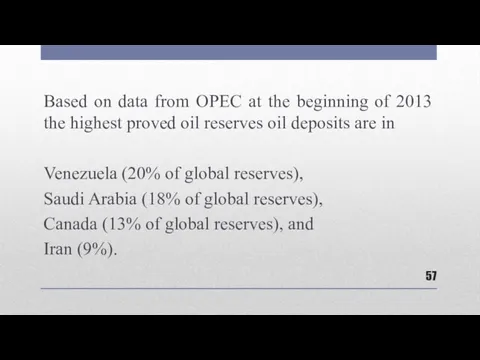

Based on data from OPEC at the beginning of 2013 the

Based on data from OPEC at the beginning of 2013 the

European dependence on oil imports has grown from 76% in 2000

European dependence on oil imports has grown from 76% in 2000

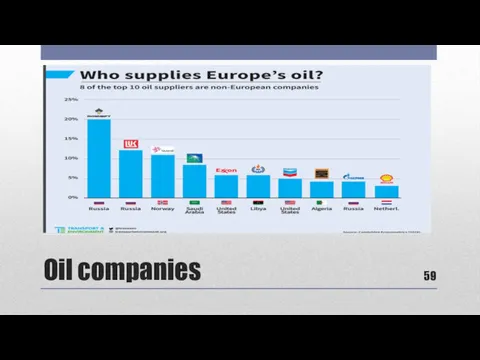

Oil companies

Oil companies

More than 40% of the oil was exported from Middle Eastern

More than 40% of the oil was exported from Middle Eastern

Coal

Countries exporting coal to EU are Russia, Colombia and Australia

Coal

Countries exporting coal to EU are Russia, Colombia and Australia

Coal

Coal, as the largest artificial contributor to carbon dioxide emissions,

Coal

Coal, as the largest artificial contributor to carbon dioxide emissions,

Nuclear energy

potentially very cheap

the lowest carbon emissions

Nuclear

Nuclear energy

potentially very cheap

the lowest carbon emissions

Nuclear

Nuclear safety

The EU promotes the highest safety standards for all types

Nuclear safety

The EU promotes the highest safety standards for all types

Radioactive waste and decommissioning

Radioactive waste results from nuclear activities such as

Radioactive waste and decommissioning

Radioactive waste results from nuclear activities such as

Nuclear energy

France is the one country that has the most

Nuclear energy

France is the one country that has the most

Nuclear energy

Russian nuclear reactors in the EU are in Bulgaria

Nuclear energy

Russian nuclear reactors in the EU are in Bulgaria

Renewable energy

The use of renewable energy has many potential benefits,

Renewable energy

The use of renewable energy has many potential benefits,

Renewable energy

The share of renewable energy in energy consumption increased

Renewable energy

The share of renewable energy in energy consumption increased

Renewable energy

The share of renewable energy in the Member States

Renewable energy

The share of renewable energy in the Member States

Renewable energy

This positive development has been prompted by the legally

Renewable energy

This positive development has been prompted by the legally

Renewable energy in the EU

Renewable energy in the EU

Topic 3. Liberalization of EU gas and energy markets

Topic 3. Liberalization of EU gas and energy markets

Liberalization Process: Legislation

The liberalization process of the natural gas market is

Liberalization Process: Legislation

The liberalization process of the natural gas market is

Liberalization Process

In all of the Directives, there are several components that

Liberalization Process

In all of the Directives, there are several components that

Liberalization Process

The first portion of the liberalization process requires states to

Liberalization Process

The first portion of the liberalization process requires states to

Liberalization Process

The 2003 Directive extended third-party access to gas storage facilities

Liberalization Process

The 2003 Directive extended third-party access to gas storage facilities

Liberalization . Unbundling.

The next aspect of the Directives is the concept

Liberalization . Unbundling.

The next aspect of the Directives is the concept

Liberalization. Interruptible contracts

The EU Directives is encouraging shorter and interruptible contracts,

Liberalization. Interruptible contracts

The EU Directives is encouraging shorter and interruptible contracts,

Liberalization. Regulatory authority

The last major area of focus in liberalization reform

Liberalization. Regulatory authority

The last major area of focus in liberalization reform

Liberalization of EU gas market

The Third Energy Package consists of two

Liberalization of EU gas market

The Third Energy Package consists of two

Topic 4. EU energy diplomacy and external actions

Internal and external energy policies cannot be separated from each other

Internal and external energy policies cannot be separated from each other

Concerning its ambitious goals about sustainability, renewable resources and fight against

Concerning its ambitious goals about sustainability, renewable resources and fight against

In the study of external energy policy of Europe it is

In the study of external energy policy of Europe it is

Pan-European Energy Community is “common regulatory space” in other words “common

Pan-European Energy Community is “common regulatory space” in other words “common

European Neighbourhood Policy

In the European Neighbourhood Policy Strategy Paper, the

European Neighbourhood Policy

In the European Neighbourhood Policy Strategy Paper, the

EU energy goals require efficient usage of financial instruments through European

EU energy goals require efficient usage of financial instruments through European

The Kyoto Protocol (1997)

The Kyoto Protocol is an international agreement which

The Kyoto Protocol (1997)

The Kyoto Protocol is an international agreement which

NORWAY

Norway is the second major natural gas and oil supplier

NORWAY

Norway is the second major natural gas and oil supplier

Norway

Norway differs from other energy suppliers to the Union because

Norway

Norway differs from other energy suppliers to the Union because

Norway

Not only the EU needs Norway as a reliable oil

Norway

Not only the EU needs Norway as a reliable oil

Norway

Norway and the EU act together to further develop their

Norway

Norway and the EU act together to further develop their

Africa

Concerning EU’s dialogue with Africa, energy is incorporated within the

Africa

Concerning EU’s dialogue with Africa, energy is incorporated within the

Africa

In the region, the EU policy makers associate the Union’s

Africa

In the region, the EU policy makers associate the Union’s

Africa

Nevertheless, Africa, more specifically North Africa has a significant potential

Africa

Nevertheless, Africa, more specifically North Africa has a significant potential

Middle East

Middle East is the world’s important energy producing region and

Middle East

Middle East is the world’s important energy producing region and

Middle East

Despite the Union’s intense energy dialogues with Russia or Caspian

Middle East

Despite the Union’s intense energy dialogues with Russia or Caspian

Middle East

Concerning the region, EU’s effort to achieve international cooperation in

Middle East

Concerning the region, EU’s effort to achieve international cooperation in

Caspian Region

Caspian region refers to five Caspian littoral states namely,

Caspian Region

Caspian region refers to five Caspian littoral states namely,

Caspian Region

This identification is necessary because, if the Caspian is

Caspian Region

This identification is necessary because, if the Caspian is

Caspian Region

Apart from the legal status of the potential reserves,

Caspian Region

Apart from the legal status of the potential reserves,

Caspian Region

The institutionalization of relations with the Caspian Region countries:

the

Caspian Region

The institutionalization of relations with the Caspian Region countries:

the

Caspian Region

Energy outstands as the main item among the imports

Caspian Region

Energy outstands as the main item among the imports

Southern Gas Corridor

The Southern Gas Corridor is an initiative of the

Southern Gas Corridor

The Southern Gas Corridor is an initiative of the

Topic 4. The EU-Russia energy dialog

Russia is the main exporter of energy resources to the European

Russia is the main exporter of energy resources to the European

When Russia’s internal energy sector is examined the most outstanding feature

When Russia’s internal energy sector is examined the most outstanding feature

Concerning the natural gas sector, again a state run monopoly, Gazprom

Concerning the natural gas sector, again a state run monopoly, Gazprom

2. NORTHERN LIGHTS AND YAMAL EUROPE

Capacity: 84 bilion cubic meters per

2. NORTHERN LIGHTS AND YAMAL EUROPE

Capacity: 84 bilion cubic meters per

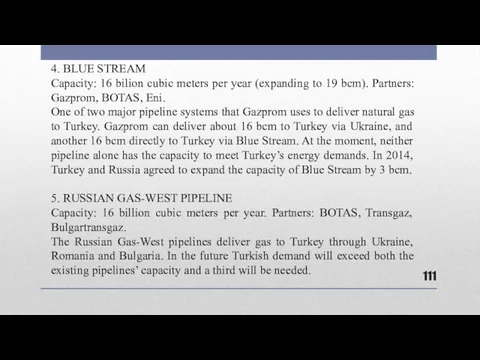

4. BLUE STREAM

Capacity: 16 bilion cubic meters per year (expanding to

4. BLUE STREAM

Capacity: 16 bilion cubic meters per year (expanding to

6. NORD STREAM 2

Capacity: 55 billion cubic meters per year. Partners:

6. NORD STREAM 2

Capacity: 55 billion cubic meters per year. Partners:

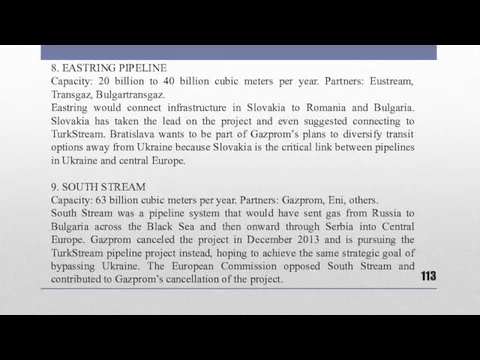

8. EASTRING PIPELINE

Capacity: 20 billion to 40 billion cubic meters per

8. EASTRING PIPELINE

Capacity: 20 billion to 40 billion cubic meters per

The institutionalization of EU-Russia relationship concerning energy can be identified by

The institutionalization of EU-Russia relationship concerning energy can be identified by

Due to Russia’s non-ratification of Energy Charter Treaty, the relationship between

Due to Russia’s non-ratification of Energy Charter Treaty, the relationship between

Загрязнение пластиком океанов России

Загрязнение пластиком океанов России Экологические общественные организации

Экологические общественные организации Человек- ты за все в ответе

Человек- ты за все в ответе Государственное регулирование природоохранной деятельности

Государственное регулирование природоохранной деятельности Изучение факторов формирования склоновых ландшафтов города Уфа

Изучение факторов формирования склоновых ландшафтов города Уфа Экологические проблемы химической промышленности. Производство неорганических веществ

Экологические проблемы химической промышленности. Производство неорганических веществ История экологического образования в России

История экологического образования в России Альтернативные источники энергии

Альтернативные источники энергии Демографическая информация в исследованиях по экологии человека

Демографическая информация в исследованиях по экологии человека Собирайка. Социально-экологический проект для школ и детских садов города Санкт-Петербурга

Собирайка. Социально-экологический проект для школ и детских садов города Санкт-Петербурга Презентация Табигатьне саклыйк!!!

Презентация Табигатьне саклыйк!!! Учение о биосфере В.И. Вернадского

Учение о биосфере В.И. Вернадского Оценка рекреационного потенциала городских лесов г. Ижевска и мероприятия по его улучшению

Оценка рекреационного потенциала городских лесов г. Ижевска и мероприятия по его улучшению Техногенные ландшафты

Техногенные ландшафты Забруднення навколишнього середовища

Забруднення навколишнього середовища Рациональное природопользование в профессии дизайнера среды

Рациональное природопользование в профессии дизайнера среды Обеспечение пожарной и экологической безопасности при функционировании АЗС в г.Уфе(на примере АЗС № 02-101 ООО АНК Башнефть)

Обеспечение пожарной и экологической безопасности при функционировании АЗС в г.Уфе(на примере АЗС № 02-101 ООО АНК Башнефть) Влияние загрязнения атмосферы на человека и окружающую среду

Влияние загрязнения атмосферы на человека и окружающую среду Принципы гигиенической регламентации факторов окружающей среды

Принципы гигиенической регламентации факторов окружающей среды взаимоотношения с природой в исламе

взаимоотношения с природой в исламе Ліси. День без паперу

Ліси. День без паперу День заповедников и парков 2022

День заповедников и парков 2022 Птицы на кормушках

Птицы на кормушках Ecological problems

Ecological problems У природі все взаємопов'язано

У природі все взаємопов'язано Право природопользования

Право природопользования Тимуровский отряд Прометей

Тимуровский отряд Прометей Мы выбираем здоровье

Мы выбираем здоровье