- Decision time frames

Содержание

- 2. Decision Time Frames The Short Run The short run is a time frame in which the

- 3. Decision Time Frames The Long Run The long run is a time frame in which the

- 4. Example With regard to economic decision making for firms, the short run is A) a definite

- 5. Example With regard to economic decision making for firms, the long run is a period in

- 6. Example Sandra has plans to go to an opera and already has a $100 non-refundable, non-exchangeable,

- 7. Short-Run Technology Constraint To increase output in the short run, a firm must increase the amount

- 8. Short-Run Technology Constraint Total product is the total output produced in a given period. The marginal

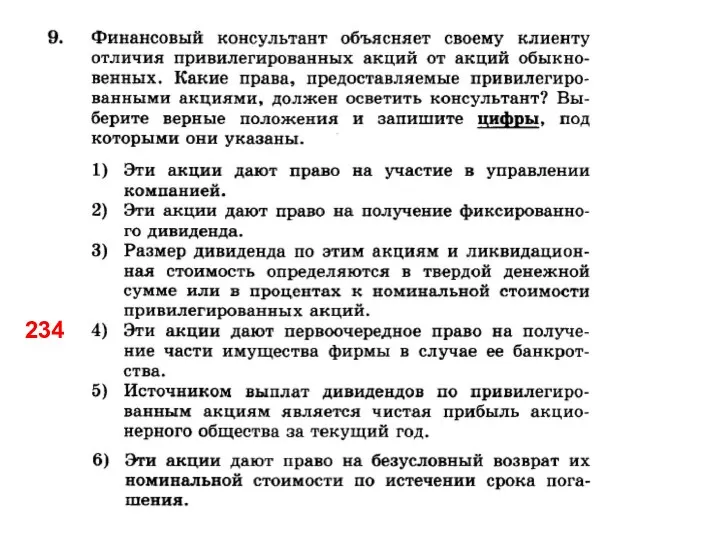

- 9. Total Product, Marginal Product, Average Product

- 10. Total Product It separates attainable output levels from unattainable output levels in the short run.

- 11. Figure 4: Total and Marginal Product 30 90 130 161 184 196 Total Product ΔQ from

- 12. Short-Run Technology Constraint Initially increasing marginal returns When the marginal product of a worker exceeds the

- 13. Short-Run Technology Constraint Increasing marginal returns arise from increased specialization and division of labor. Diminishing marginal

- 14. Example The following data show the total output for a firm when different amounts of labor

- 15. Short-Run Technology Constraint When marginal product exceeds average product, average product increases. When marginal product is

- 16. Example Consider a basket-producing firm with fixed capital. If the firm can produce 36 baskets per

- 17. Short-Run Cost To produce more output in the short run, the firm must employ more labor,

- 18. Short-Run Cost Total Cost A firm’s total cost (TC) is the cost of all resources used.

- 19. Total Costs of Production

- 20. Example Larry’s Performance Pizza is a small restaurant that sells low-carbohydrate pizzas in a health -

- 21. Total Costs of Production Total fixed cost is the same at each output level. Total variable

- 22. Short-Run Cost Marginal Cost Marginal cost (MC) is the increase in total cost that results from

- 23. Short-Run Cost Average Cost Average cost measures can be derived from each of the total cost

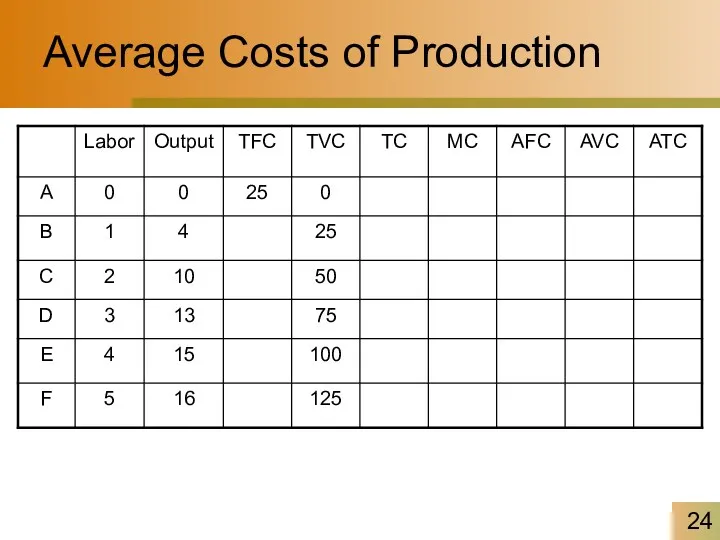

- 24. Average Costs of Production

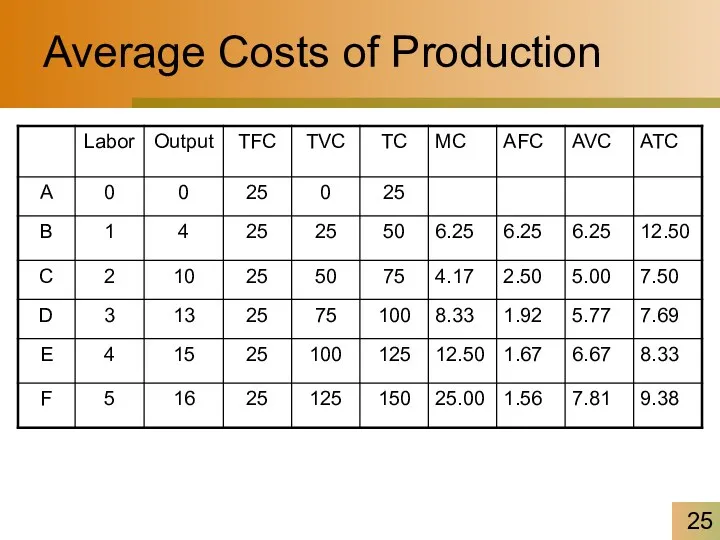

- 25. Average Costs of Production

- 26. Example

- 27. Example The following data show the total output for a firm when specified amounts of labor

- 28. Average And Marginal Costs MC AVC ATC AFC

- 29. The Relationship Between Average And Marginal Costs At low levels of output, the MC curve lies

- 30. Example Suppose a firm producing digital cameras is operating such that marginal costs are higher than

- 31. Short-Run Cost Shifts in Cost Curves The position of a firm’s cost curves depend on two

- 32. Short-Run Cost Technological change influences both the productivity curves and the cost curves. An increase in

- 33. Short-Run Cost Changes in the prices of resources shift the cost curves. An increase in a

- 34. Example In the short run, when capital is a fixed factor, a rise in the cost

- 35. Production And Cost in the Long Run In the long run, costs behave differently Firm can

- 36. Production And Cost in the Long Run Long-run total cost The cost of producing each quantity

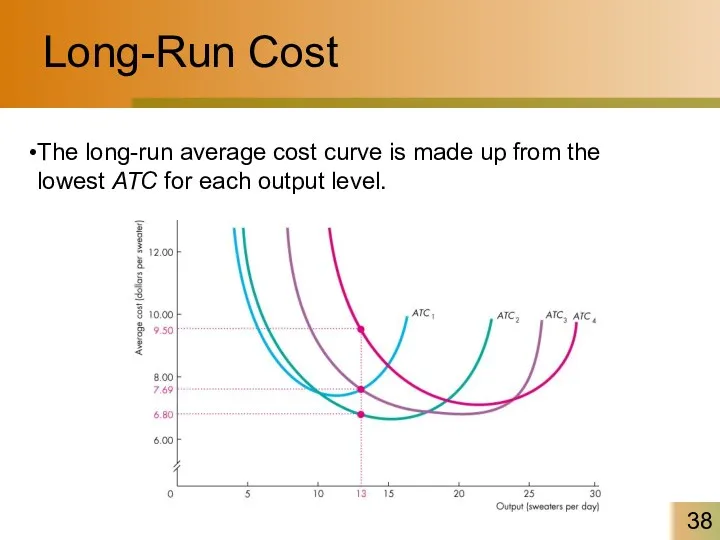

- 37. Long-Run Cost The average cost of producing a given output varies and depends on the firm’s

- 38. Long-Run Cost

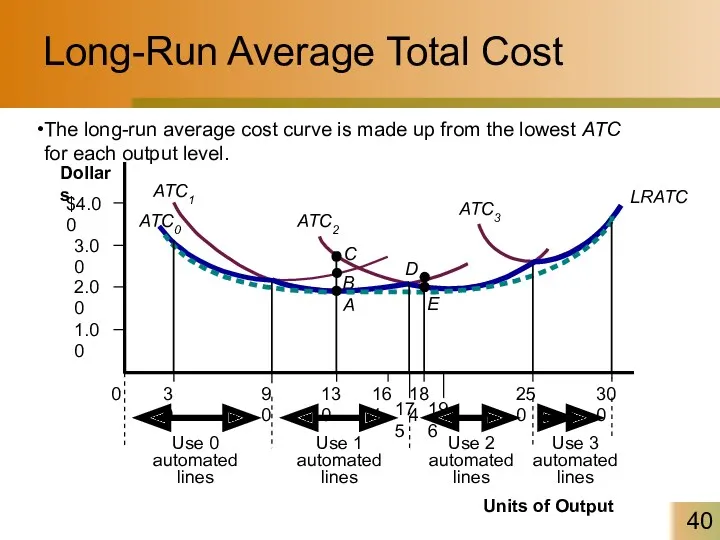

- 39. Long-Run Cost Long-Run Average Cost Curve The long-run average cost curve is the relationship between the

- 40. Long-Run Average Total Cost LRATC ATC1 Use 0 automated lines ATC3 ATC0 C B A ATC2

- 41. Example The table below shows 4 alternative production techniques for producing 1,000 widgets per month. Technique

- 42. Example Ike’s bikes is a major manufacturer of bicycles. Currently, the company produces bikes in one

- 43. Example 1. Suppose Ike’s Bikes is currently producing 500 bikes per month in its (only) factory.

- 44. Long-Run Cost Economies and Diseconomies of Scale Economies of scale are features of a firm’s technology

- 45. The Shape Of LRATC Units of Output LRATC Economies of Scale Constant Returns to Scale Diseconomies

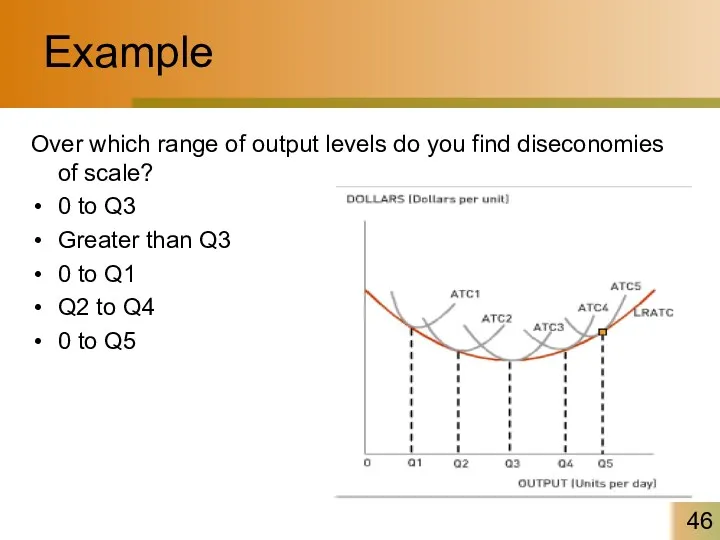

- 46. Example Over which range of output levels do you find diseconomies of scale? 0 to Q3

- 47. Long-Run Cost A firm experiences economies of scale up to some output level. Beyond that output

- 48. Returns to Scale In production, returns to scale refers to changes in output subsequent to a

- 49. Example Assume a firm is using 10 units of labor and 10 units of capital and

- 51. Скачать презентацию

Decision Time Frames

The Short Run

The short run is a time frame

Decision Time Frames

The Short Run

The short run is a time frame

Decision Time Frames

The Long Run

The long run is a time frame

Decision Time Frames

The Long Run

The long run is a time frame

Example

With regard to economic decision making for firms, the short run

Example

With regard to economic decision making for firms, the short run

Example

With regard to economic decision making for firms, the long run

Example

With regard to economic decision making for firms, the long run

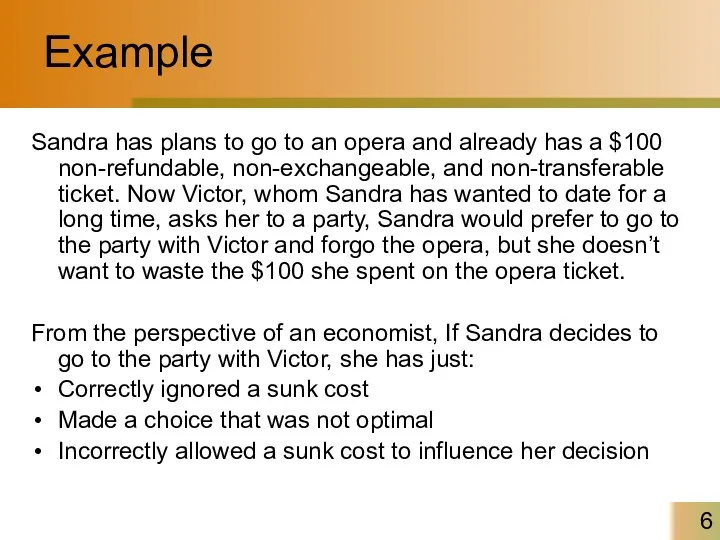

Example

Sandra has plans to go to an opera and already has

Example

Sandra has plans to go to an opera and already has

Short-Run Technology Constraint

To increase output in the short run, a firm

Short-Run Technology Constraint

To increase output in the short run, a firm

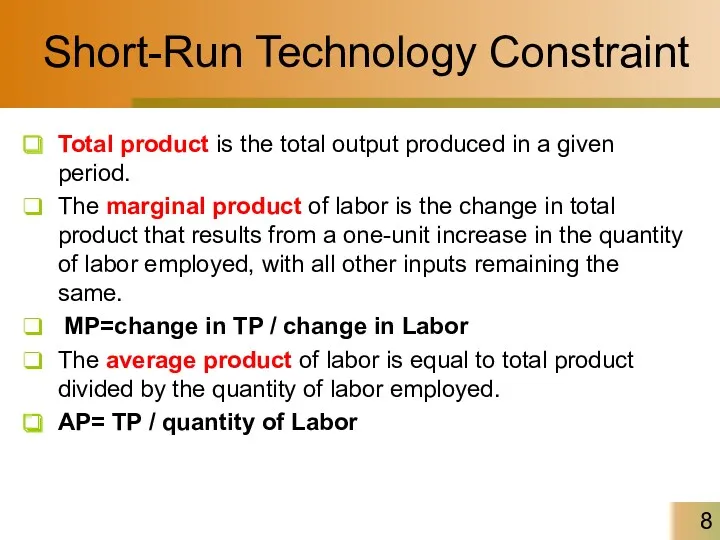

Short-Run Technology Constraint

Total product is the total output produced in a

Short-Run Technology Constraint

Total product is the total output produced in a

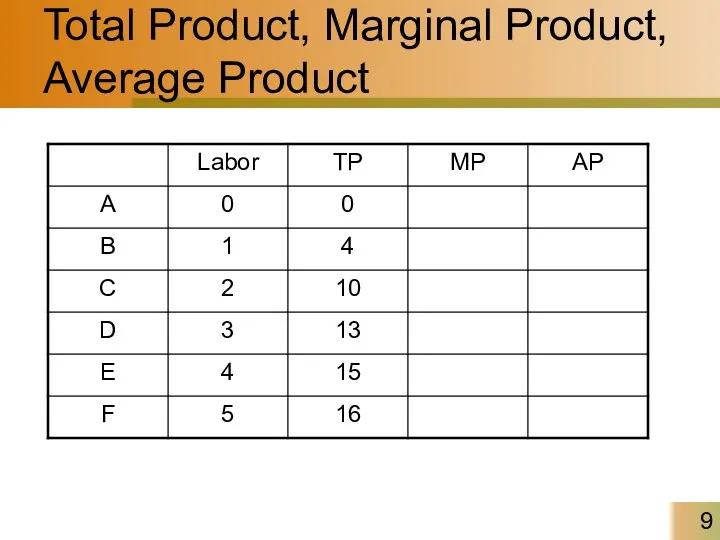

Total Product, Marginal Product, Average Product

Total Product, Marginal Product, Average Product

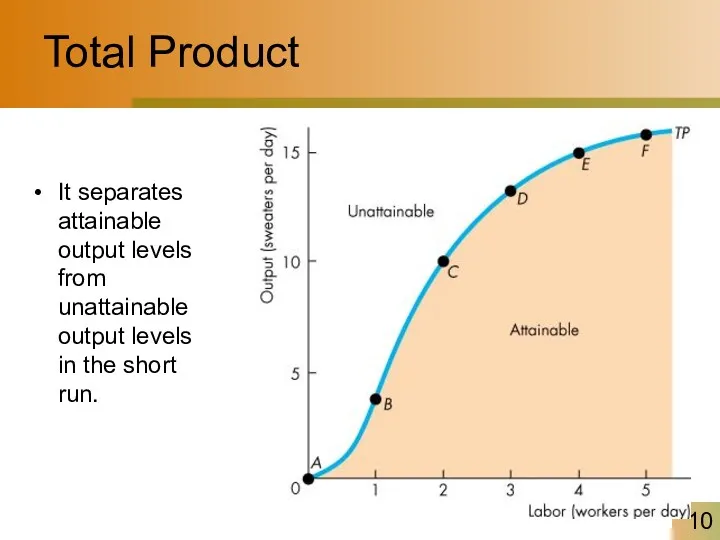

Total Product

It separates attainable output levels from unattainable output levels in

Total Product

It separates attainable output levels from unattainable output levels in

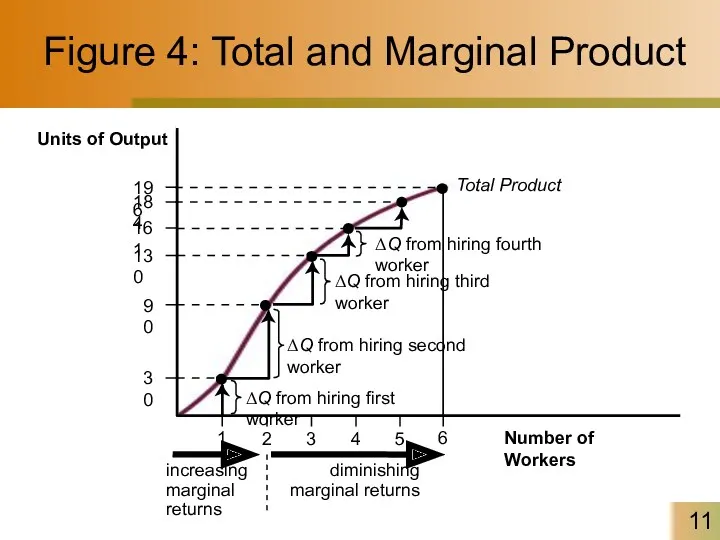

Figure 4: Total and Marginal Product

30

90

130

161

184

196

Total Product

ΔQ from hiring fourth worker

ΔQ

Figure 4: Total and Marginal Product

30

90

130

161

184

196

Total Product

ΔQ from hiring fourth worker

ΔQ

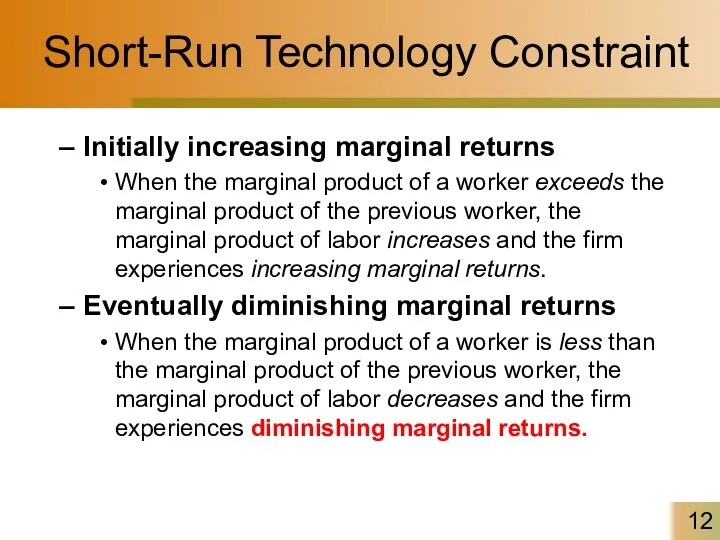

Short-Run Technology Constraint

Initially increasing marginal returns

When the marginal product of a

Short-Run Technology Constraint

Initially increasing marginal returns

When the marginal product of a

Short-Run Technology Constraint

Increasing marginal returns arise from increased specialization and division

Short-Run Technology Constraint

Increasing marginal returns arise from increased specialization and division

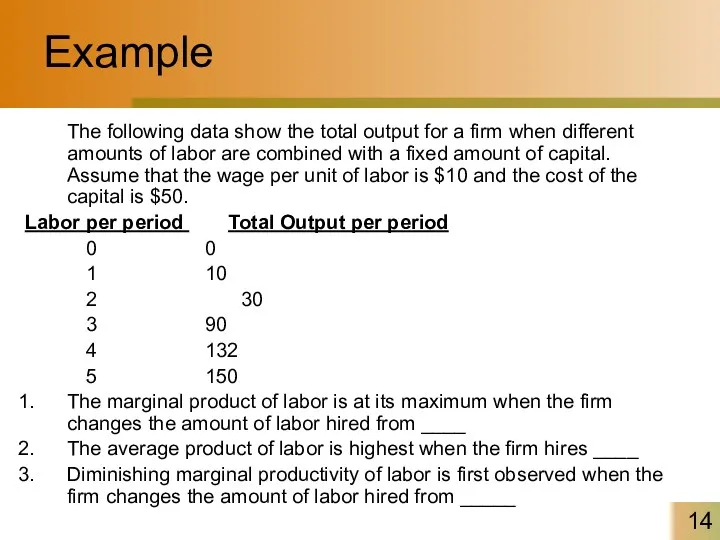

Example

The following data show the total output for a firm when

Example

The following data show the total output for a firm when

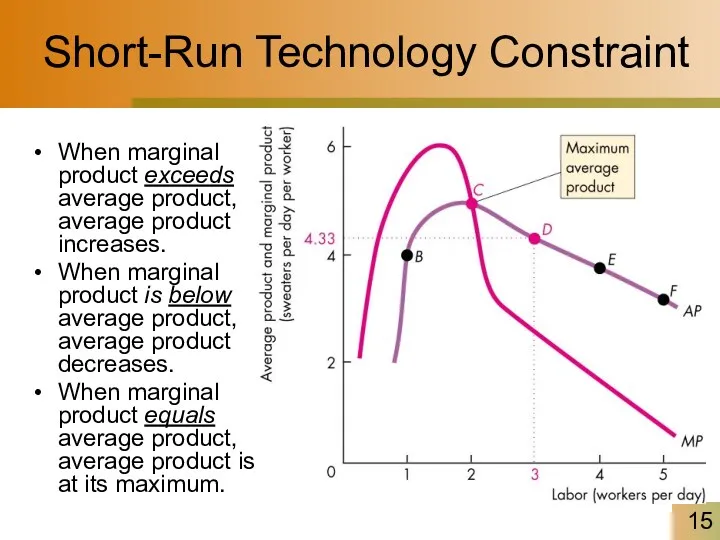

Short-Run Technology Constraint

When marginal product exceeds average product, average product increases.

When

Short-Run Technology Constraint

When marginal product exceeds average product, average product increases.

When

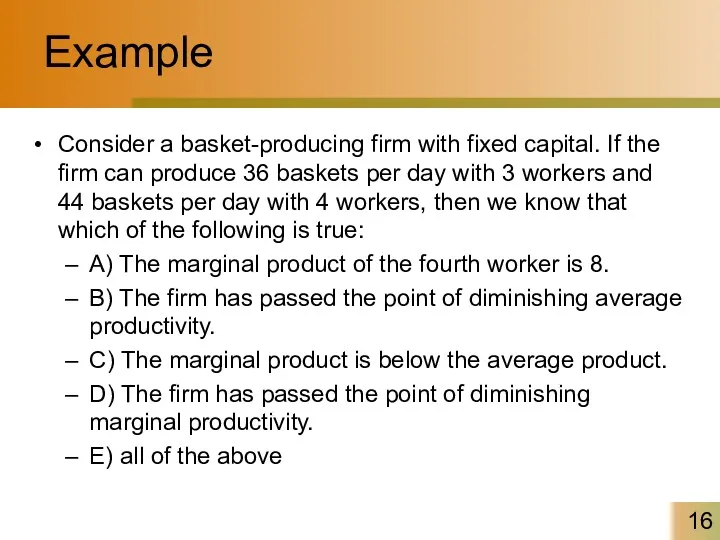

Example

Consider a basket-producing firm with fixed capital. If the firm can

Example

Consider a basket-producing firm with fixed capital. If the firm can

Short-Run Cost

To produce more output in the short run, the firm

Short-Run Cost

To produce more output in the short run, the firm

Short-Run Cost

Total Cost

A firm’s total cost (TC) is the cost of

Short-Run Cost

Total Cost

A firm’s total cost (TC) is the cost of

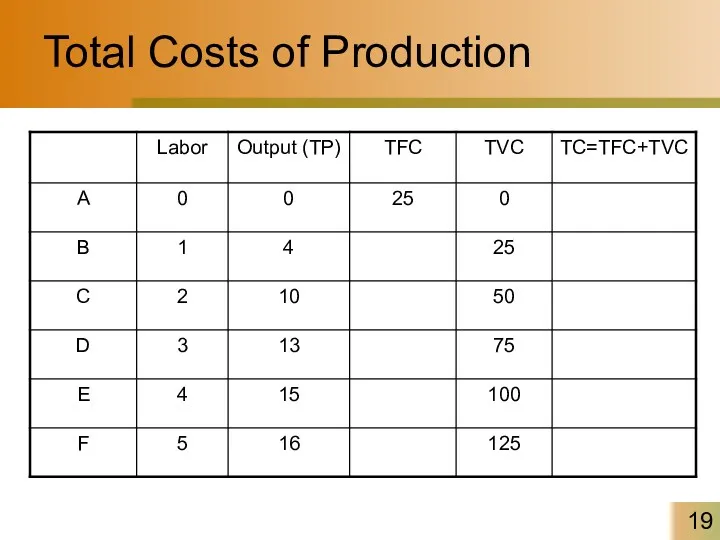

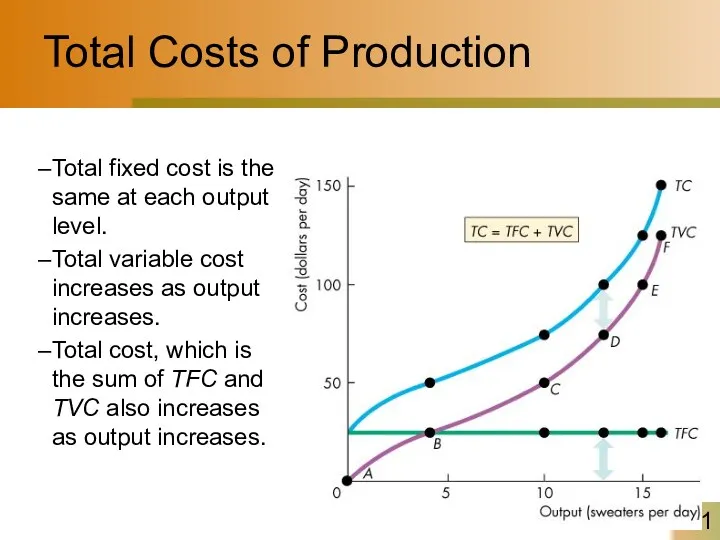

Total Costs of Production

Total Costs of Production

Example

Larry’s Performance Pizza is a small restaurant that sells low-carbohydrate pizzas

Example

Larry’s Performance Pizza is a small restaurant that sells low-carbohydrate pizzas

Total Costs of Production

Total fixed cost is the same at each

Total Costs of Production

Total fixed cost is the same at each

Short-Run Cost

Marginal Cost

Marginal cost (MC) is the increase in total cost

Short-Run Cost

Marginal Cost

Marginal cost (MC) is the increase in total cost

Short-Run Cost

Average Cost

Average cost measures can be derived from each of

Short-Run Cost

Average Cost

Average cost measures can be derived from each of

Average Costs of Production

Average Costs of Production

Average Costs of Production

Average Costs of Production

Example

Example

Example

The following data show the total output for a firm when

Example

The following data show the total output for a firm when

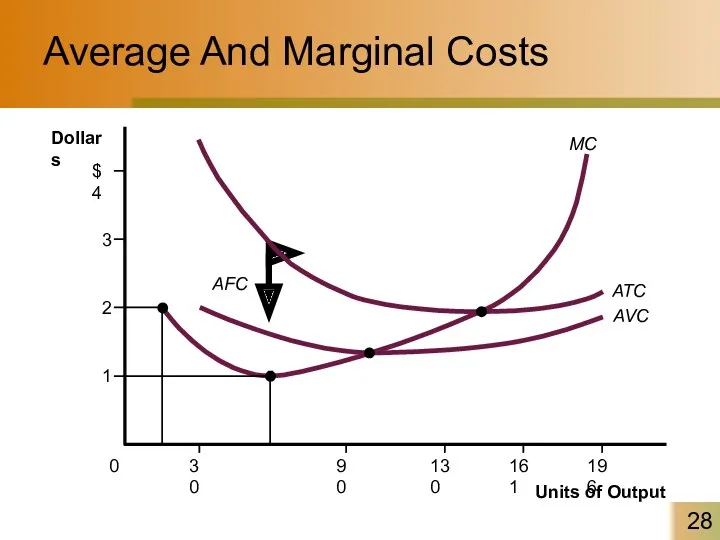

Average And Marginal Costs

MC

AVC

ATC

AFC

Average And Marginal Costs

MC

AVC

ATC

AFC

The Relationship Between Average And Marginal Costs

At low levels of output,

The Relationship Between Average And Marginal Costs

At low levels of output,

Example

Suppose a firm producing digital cameras is operating such that marginal

Example

Suppose a firm producing digital cameras is operating such that marginal

Short-Run Cost

Shifts in Cost Curves

The position of a firm’s cost curves

Short-Run Cost

Shifts in Cost Curves

The position of a firm’s cost curves

Short-Run Cost

Technological change influences both the productivity curves and the cost

Short-Run Cost

Technological change influences both the productivity curves and the cost

Short-Run Cost

Changes in the prices of resources shift the cost curves.

An

Short-Run Cost

Changes in the prices of resources shift the cost curves.

An

Example

In the short run, when capital is a fixed factor, a

Example

In the short run, when capital is a fixed factor, a

Production And Cost in the Long Run

In the long run, costs

Production And Cost in the Long Run

In the long run, costs

Production And Cost in the Long Run

Long-run total cost

The cost of

Production And Cost in the Long Run

Long-run total cost

The cost of

Long-Run Cost

The average cost of producing a given output varies and

Long-Run Cost

The average cost of producing a given output varies and

Long-Run Cost

Long-Run Cost

Long-Run Cost

Long-Run Average Cost Curve

The long-run average cost curve is the

Long-Run Cost

Long-Run Average Cost Curve

The long-run average cost curve is the

Long-Run Average Total Cost

LRATC

ATC1

Use 0 automated lines

ATC3

ATC0

C

B

A

ATC2

D

E

175

Use 1 automated lines

Use 2

Long-Run Average Total Cost

LRATC

ATC1

Use 0 automated lines

ATC3

ATC0

C

B

A

ATC2

D

E

175

Use 1 automated lines

Use 2

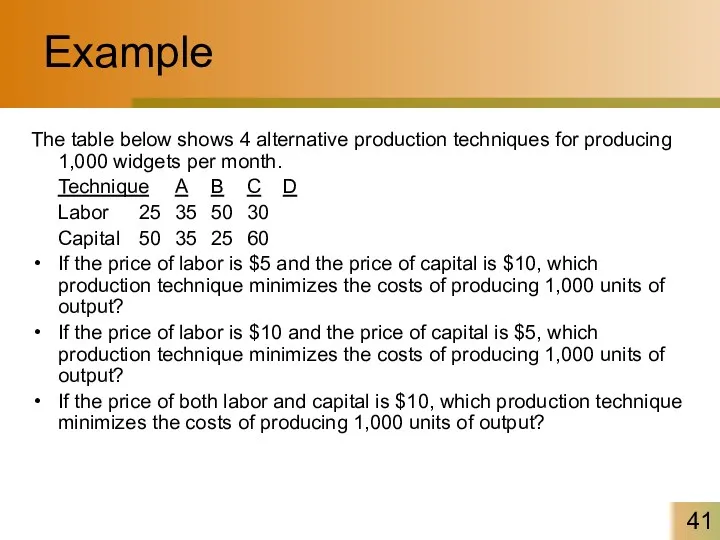

Example

The table below shows 4 alternative production techniques for producing 1,000

Example

The table below shows 4 alternative production techniques for producing 1,000

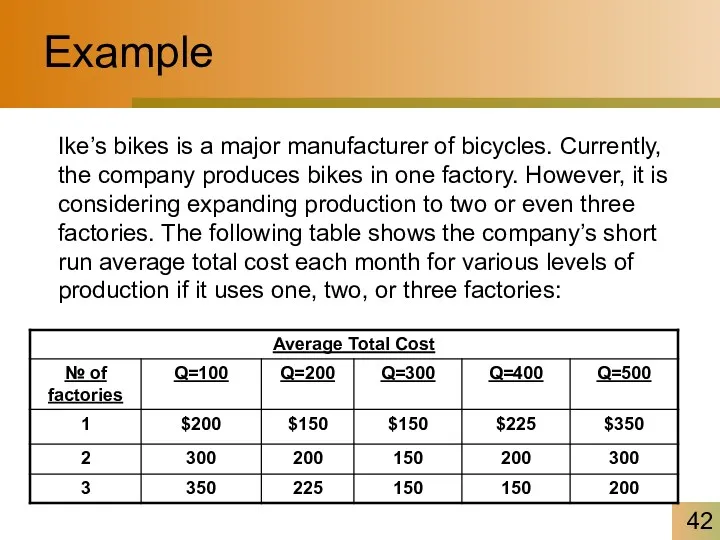

Example

Ike’s bikes is a major manufacturer of bicycles. Currently, the company

Example

Ike’s bikes is a major manufacturer of bicycles. Currently, the company

Example

1. Suppose Ike’s Bikes is currently producing 500 bikes per month in

Example

1. Suppose Ike’s Bikes is currently producing 500 bikes per month in

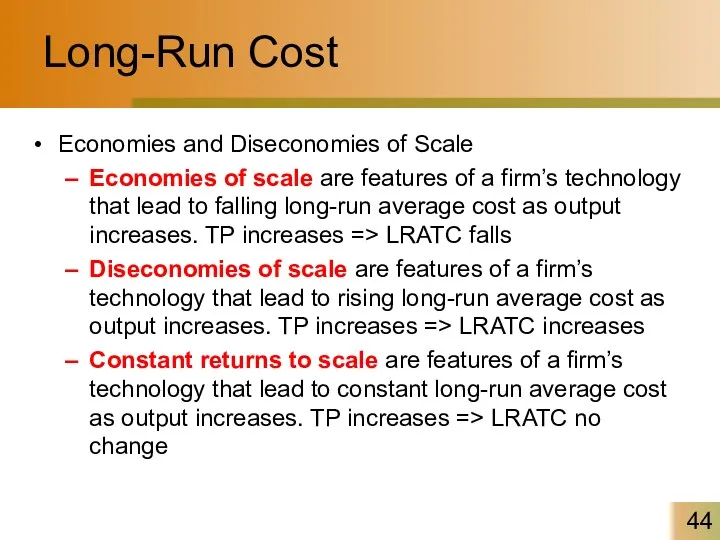

Long-Run Cost

Economies and Diseconomies of Scale

Economies of scale are features of

Long-Run Cost

Economies and Diseconomies of Scale

Economies of scale are features of

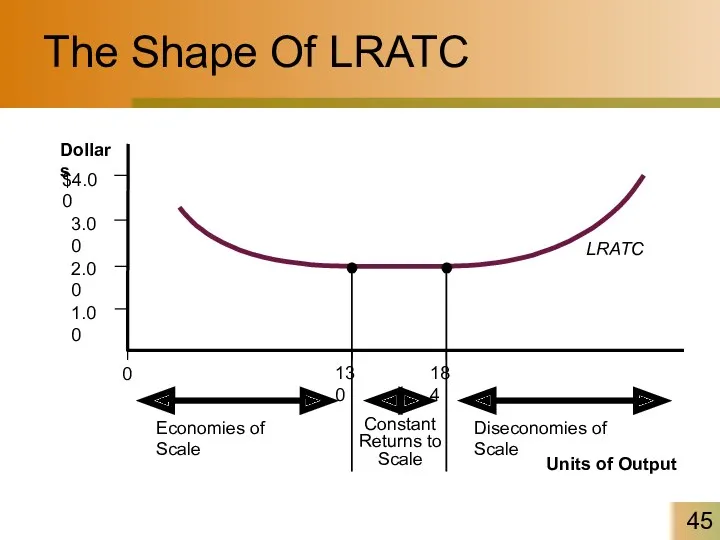

The Shape Of LRATC

Units of Output

LRATC

Economies of Scale

Constant Returns to Scale

Diseconomies

The Shape Of LRATC

Units of Output

LRATC

Economies of Scale

Constant Returns to Scale

Diseconomies

Example

Over which range of output levels do you find diseconomies of

Example

Over which range of output levels do you find diseconomies of

Long-Run Cost

A firm experiences economies of scale up to some output

Long-Run Cost

A firm experiences economies of scale up to some output

Returns to Scale

In production, returns to scale refers to changes in

Returns to Scale

In production, returns to scale refers to changes in

Example

Assume a firm is using 10 units of labor and 10

Example

Assume a firm is using 10 units of labor and 10

Impact of globalization on local culture

Impact of globalization on local culture Спрос и предложение на рынке труда

Спрос и предложение на рынке труда Развитие экспортного потенциала культурных и креативных индустрий в Европейском союзе

Развитие экспортного потенциала культурных и креативных индустрий в Европейском союзе Индикаторы устойчивого развития-2

Индикаторы устойчивого развития-2 Человек в мире экономических отношений

Человек в мире экономических отношений Международные валютные отношения и валютный рынок. (Темы 1-2) Валюта как ключевая категория международных валютных отношений

Международные валютные отношения и валютный рынок. (Темы 1-2) Валюта как ключевая категория международных валютных отношений Теории эластичности спроса и предложения

Теории эластичности спроса и предложения Макроэкономическая нестабильность. Безработица и занятость (макроэкономические показатели)

Макроэкономическая нестабильность. Безработица и занятость (макроэкономические показатели) Організація та технологія надання пасажирських послуг

Організація та технологія надання пасажирських послуг Өндіріс факторларының нарығы

Өндіріс факторларының нарығы Альтерглобалізм та його форми

Альтерглобалізм та його форми Экономика и государство

Экономика и государство Кейнсианство. Джон Мейнард Кейнс

Кейнсианство. Джон Мейнард Кейнс Производственная программа и производственные мощности. Экономика организации. (Лекция 7)

Производственная программа и производственные мощности. Экономика организации. (Лекция 7) Цели, организация и методы антимонопольного регулирования

Цели, организация и методы антимонопольного регулирования Анализ возможностей выхода ПАО Газпром на Азиатско-тихоокеанские рынки

Анализ возможностей выхода ПАО Газпром на Азиатско-тихоокеанские рынки Спрос. Закон спроса. Эластичность спроса

Спрос. Закон спроса. Эластичность спроса Підприємницька ідея: механізм генерування та впровадження

Підприємницька ідея: механізм генерування та впровадження Место Китая в мировом хозяйстве

Место Китая в мировом хозяйстве Экономика организации. Трудовые ресурсы организации. Основы организации труда и его оплаты

Экономика организации. Трудовые ресурсы организации. Основы организации труда и его оплаты Анализ рынка СЭД в РФ

Анализ рынка СЭД в РФ Әлеуметтік – экономикалық дамудағы дағдарыс түсінігі және оның пайда болу себептері

Әлеуметтік – экономикалық дамудағы дағдарыс түсінігі және оның пайда болу себептері Рыночная экономика. Тема 14. Обществознание. 8 класс

Рыночная экономика. Тема 14. Обществознание. 8 класс Фінансові ресурси торговельного підприємства. (Лекція 11)

Фінансові ресурси торговельного підприємства. (Лекція 11) Тема 10. Экономическая роль государства

Тема 10. Экономическая роль государства Рынки факторов производства

Рынки факторов производства Риск в экономике

Риск в экономике История создания ГАТТ/ВТО. Организационная структура ВТО

История создания ГАТТ/ВТО. Организационная структура ВТО