- Firms in competitive markets. (Lecture 14)

Содержание

- 2. WHAT IS A COMPETITIVE MARKET? A perfectly competitive market has the following characteristics: There are many

- 3. WHAT IS A COMPETITIVE MARKET? As a result of its characteristics, the perfectly competitive market has

- 4. WHAT IS A COMPETITIVE MARKET? A competitive market has many buyers and sellers trading identical products

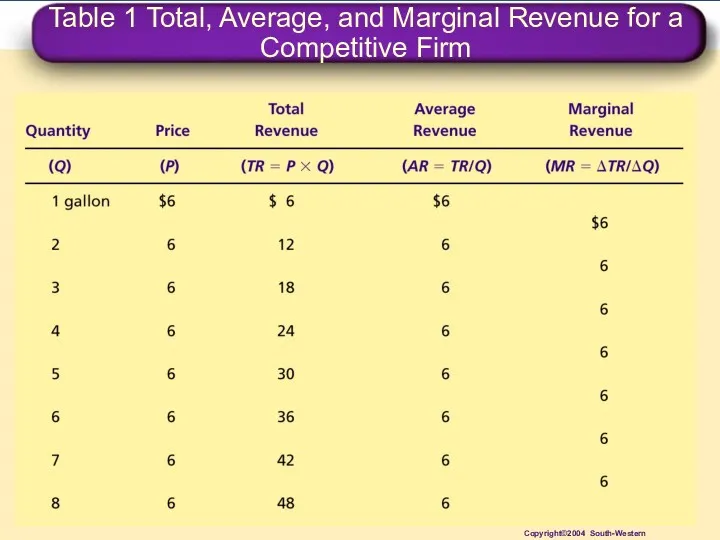

- 5. The Revenue of a Competitive Firm Total revenue for a firm is the selling price times

- 6. The Revenue of a Competitive Firm Total revenue is proportional to the amount of output.

- 7. The Revenue of a Competitive Firm Average revenue tells us how much revenue a firm receives

- 8. The Revenue of a Competitive Firm In perfect competition, average revenue equals the price of the

- 9. The Revenue of a Competitive Firm Marginal revenue is the change in total revenue from an

- 10. The Revenue of a Competitive Firm For competitive firms, marginal revenue equals the price of the

- 11. Table 1 Total, Average, and Marginal Revenue for a Competitive Firm Copyright©2004 South-Western

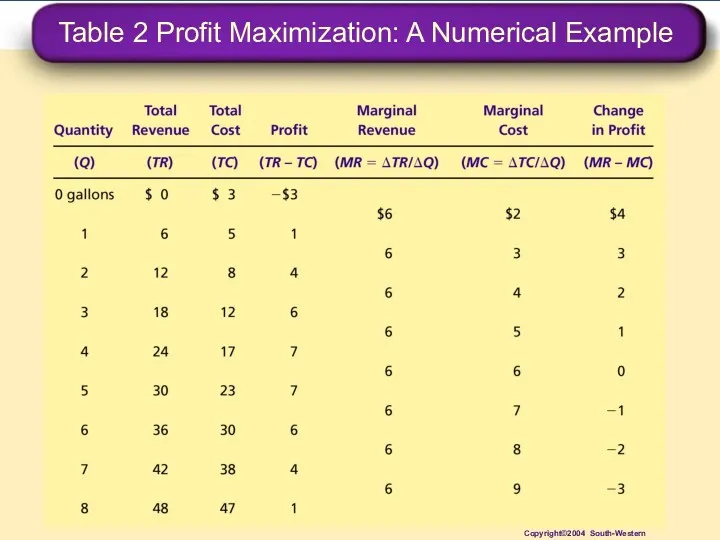

- 12. PROFIT MAXIMIZATION AND THE COMPETITIVE FIRM’S SUPPLY CURVE The goal of a competitive firm is to

- 13. Table 2 Profit Maximization: A Numerical Example Copyright©2004 South-Western

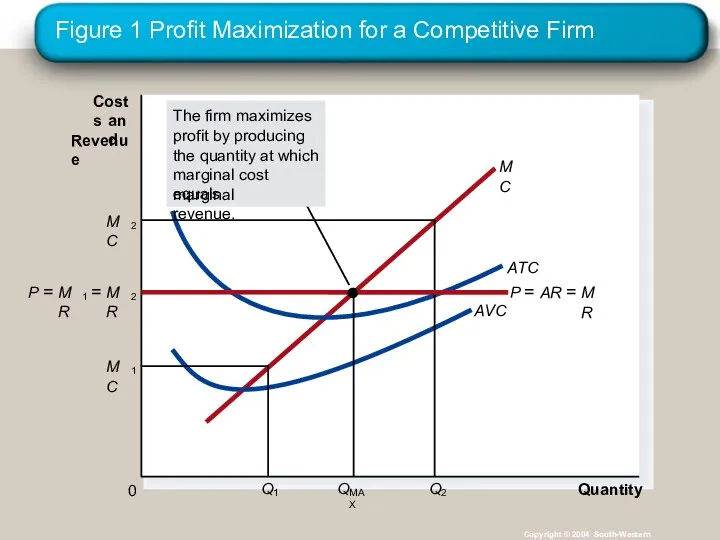

- 14. Figure 1 Profit Maximization for a Competitive Firm Copyright © 2004 South-Western Quantity 0 Costs and

- 15. PROFIT MAXIMIZATION AND THE COMPETITIVE FIRM’S SUPPLY CURVE Profit maximization occurs at the quantity where marginal

- 16. PROFIT MAXIMIZATION AND THE COMPETITIVE FIRM’S SUPPLY CURVE When MR > MC - increase Q When

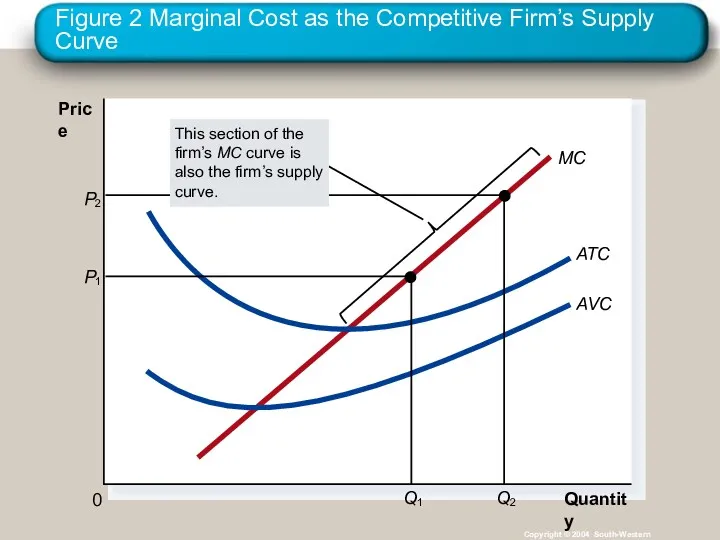

- 17. Figure 2 Marginal Cost as the Competitive Firm’s Supply Curve Copyright © 2004 South-Western Quantity 0

- 18. The Firm’s Short-Run Decision to Shut Down A shutdown refers to a short-run decision not to

- 19. The Firm’s Short-Run Decision to Shut Down The firm considers its sunk costs when deciding to

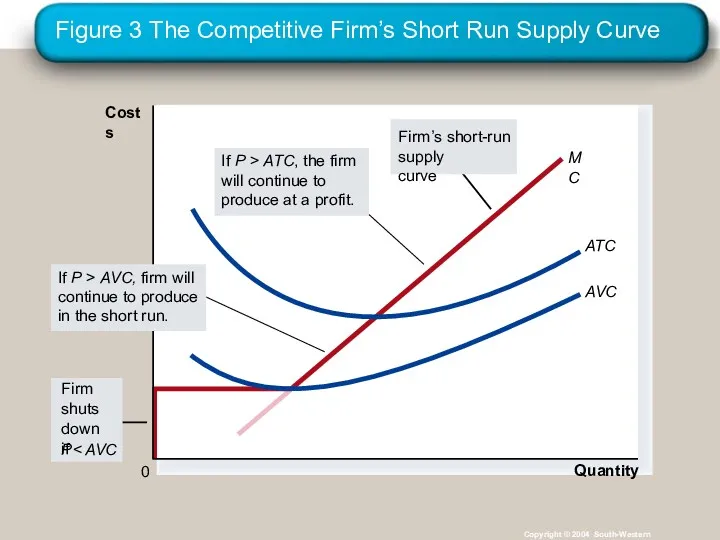

- 20. The Firm’s Short-Run Decision to Shut Down The firm shuts down if the revenue it gets

- 21. Figure 3 The Competitive Firm’s Short Run Supply Curve Copyright © 2004 South-Western Quantity 0 Costs

- 22. The Firm’s Short-Run Decision to Shut Down The portion of the marginal-cost curve that lies above

- 23. The Firm’s Long-Run Decision to Exit or Enter a Market In the long run, the firm

- 24. The Firm’s Long-Run Decision to Exit or Enter a Market A firm will enter the industry

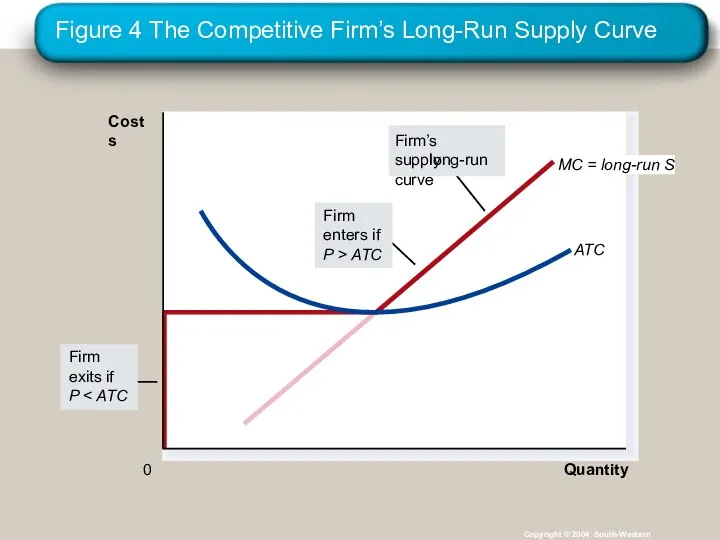

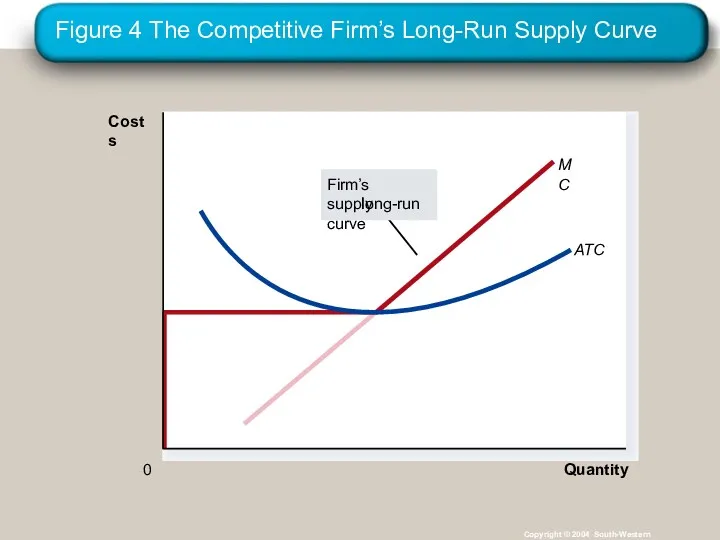

- 25. Figure 4 The Competitive Firm’s Long-Run Supply Curve Copyright © 2004 South-Western Quantity 0 Costs

- 26. THE SUPPLY CURVE IN A COMPETITIVE MARKET The competitive firm’s long-run supply curve is the portion

- 27. Figure 4 The Competitive Firm’s Long-Run Supply Curve Copyright © 2004 South-Western Quantity 0 Costs

- 28. THE SUPPLY CURVE IN A COMPETITIVE MARKET Short-Run Supply Curve The portion of its marginal cost

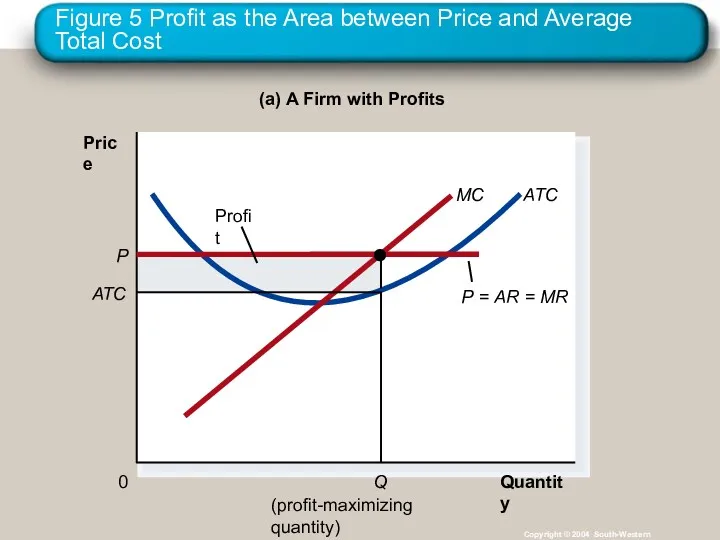

- 29. Figure 5 Profit as the Area between Price and Average Total Cost Copyright © 2004 South-Western

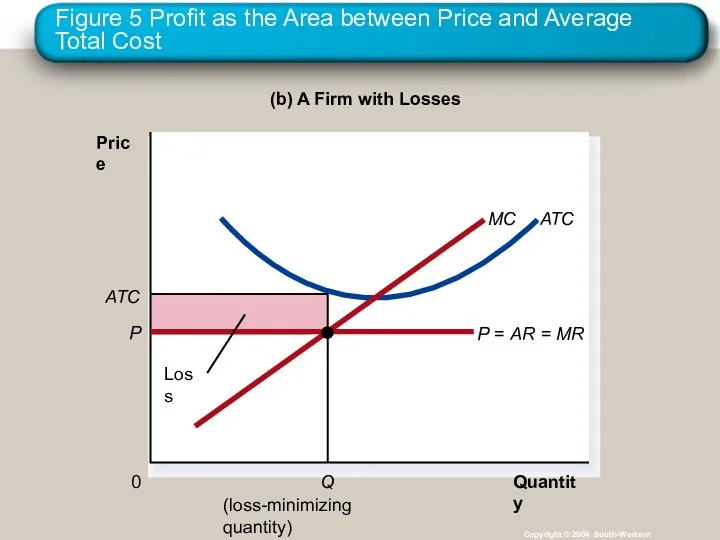

- 30. Figure 5 Profit as the Area between Price and Average Total Cost Copyright © 2004 South-Western

- 31. THE SUPPLY CURVE IN A COMPETITIVE MARKET Market supply equals the sum of the quantities supplied

- 32. The Short Run: Market Supply with a Fixed Number of Firms For any given price, each

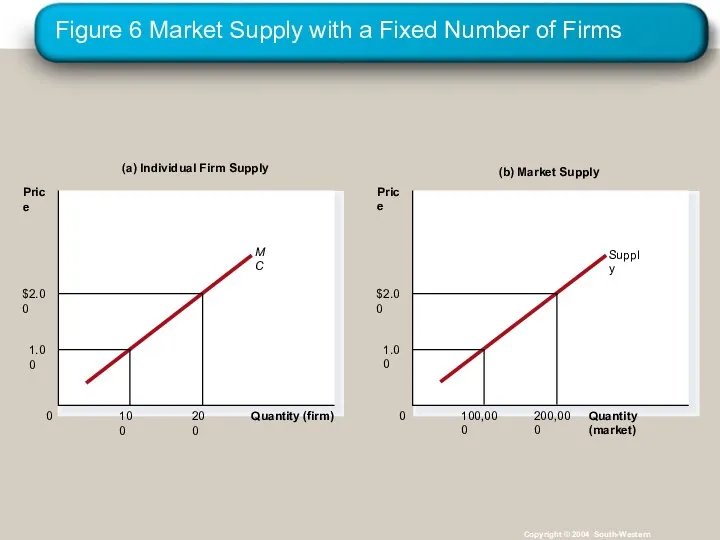

- 33. Figure 6 Market Supply with a Fixed Number of Firms Copyright © 2004 South-Western (a) Individual

- 34. The Long Run: Market Supply with Entry and Exit Firms will enter or exit the market

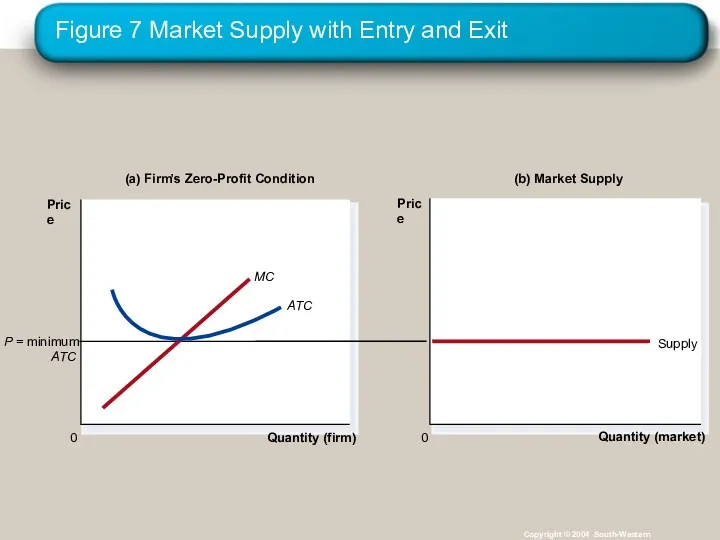

- 35. Figure 7 Market Supply with Entry and Exit Copyright © 2004 South-Western (a) Firm ’ s

- 36. The Long Run: Market Supply with Entry and Exit At the end of the process of

- 37. Why Do Competitive Firms Stay in Business If They Make Zero Profit? Profit equals total revenue

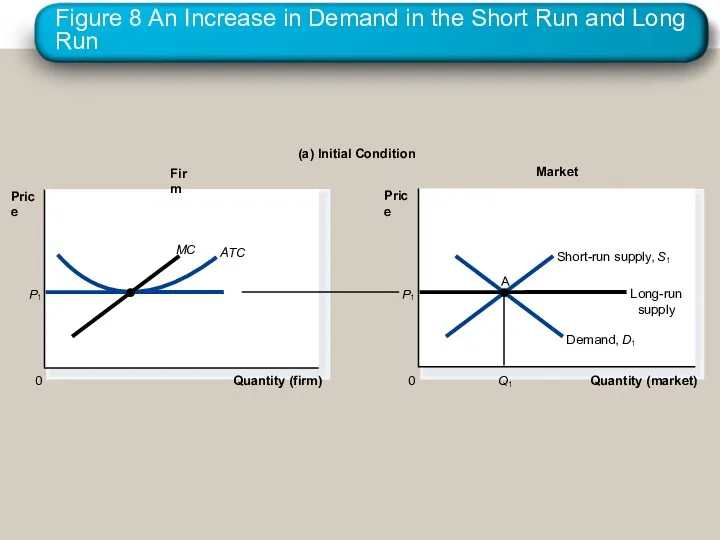

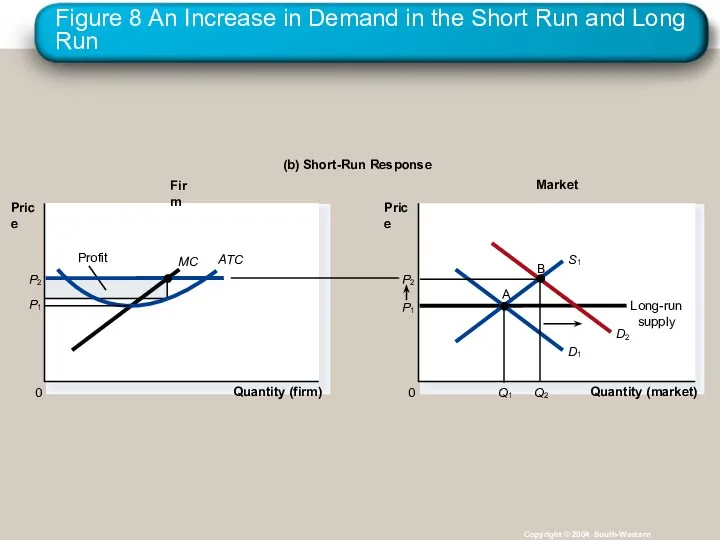

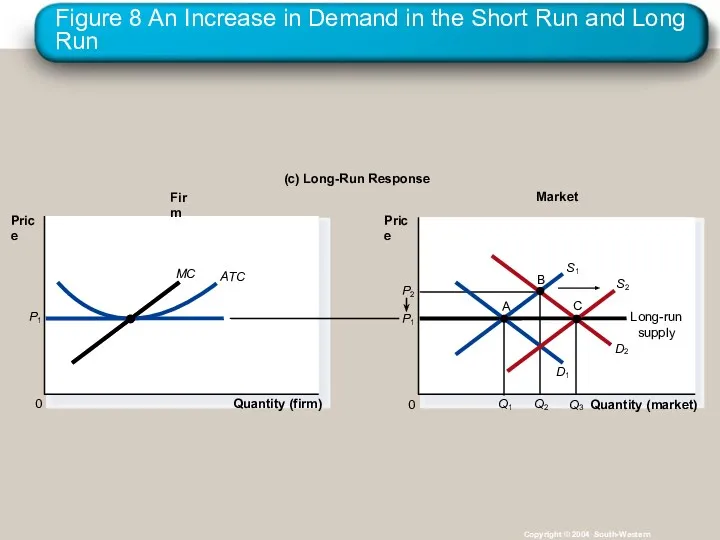

- 38. A Shift in Demand in the Short Run and Long Run An increase in demand raises

- 39. Figure 8 An Increase in Demand in the Short Run and Long Run Firm (a) Initial

- 40. Figure 8 An Increase in Demand in the Short Run and Long Run Copyright © 2004

- 41. Figure 8 An Increase in Demand in the Short Run and Long Run Copyright © 2004

- 42. Why the Long-Run Supply Curve Might Slope Upward Some resources used in production may be available

- 43. Why the Long-Run Supply Curve Might Slope Upward Marginal Firm The marginal firm is the firm

- 44. Summary Because a competitive firm is a price taker, its revenue is proportional to the amount

- 45. Summary To maximize profit, a firm chooses the quantity of output such that marginal revenue equals

- 46. Summary In the short run, when a firm cannot recover its fixed costs, the firm will

- 48. Скачать презентацию

WHAT IS A COMPETITIVE MARKET?

A perfectly competitive market has the following

WHAT IS A COMPETITIVE MARKET?

A perfectly competitive market has the following

WHAT IS A COMPETITIVE MARKET?

As a result of its characteristics, the

WHAT IS A COMPETITIVE MARKET?

As a result of its characteristics, the

WHAT IS A COMPETITIVE MARKET?

A competitive market has many buyers and

WHAT IS A COMPETITIVE MARKET?

A competitive market has many buyers and

The Revenue of a Competitive Firm

Total revenue for a firm is

The Revenue of a Competitive Firm

Total revenue for a firm is

The Revenue of a Competitive Firm

Total revenue is proportional to the

The Revenue of a Competitive Firm

Total revenue is proportional to the

The Revenue of a Competitive Firm

Average revenue tells us how much

The Revenue of a Competitive Firm

Average revenue tells us how much

The Revenue of a Competitive Firm

In perfect competition, average revenue equals

The Revenue of a Competitive Firm

In perfect competition, average revenue equals

The Revenue of a Competitive Firm

Marginal revenue is the change in

The Revenue of a Competitive Firm

Marginal revenue is the change in

The Revenue of a Competitive Firm

For competitive firms, marginal revenue equals

The Revenue of a Competitive Firm

For competitive firms, marginal revenue equals

Table 1 Total, Average, and Marginal Revenue for a Competitive Firm

Copyright©2004

Table 1 Total, Average, and Marginal Revenue for a Competitive Firm

Copyright©2004

PROFIT MAXIMIZATION AND THE COMPETITIVE FIRM’S SUPPLY CURVE

The goal of a

PROFIT MAXIMIZATION AND THE COMPETITIVE FIRM’S SUPPLY CURVE

The goal of a

Table 2 Profit Maximization: A Numerical Example

Copyright©2004 South-Western

Table 2 Profit Maximization: A Numerical Example

Copyright©2004 South-Western

Figure 1 Profit Maximization for a Competitive Firm

Copyright © 2004 South-Western

Quantity

0

Costs

and

Revenue

Figure 1 Profit Maximization for a Competitive Firm

Copyright © 2004 South-Western

Quantity

0

Costs

and

Revenue

PROFIT MAXIMIZATION AND THE COMPETITIVE FIRM’S SUPPLY CURVE

Profit maximization occurs at

PROFIT MAXIMIZATION AND THE COMPETITIVE FIRM’S SUPPLY CURVE

Profit maximization occurs at

PROFIT MAXIMIZATION AND THE COMPETITIVE FIRM’S SUPPLY CURVE

When MR > MC

PROFIT MAXIMIZATION AND THE COMPETITIVE FIRM’S SUPPLY CURVE

When MR > MC

Figure 2 Marginal Cost as the Competitive Firm’s Supply Curve

Copyright ©

Figure 2 Marginal Cost as the Competitive Firm’s Supply Curve

Copyright ©

The Firm’s Short-Run Decision to Shut Down

A shutdown refers to a

The Firm’s Short-Run Decision to Shut Down

A shutdown refers to a

The Firm’s Short-Run Decision to Shut Down

The firm considers its sunk

The Firm’s Short-Run Decision to Shut Down

The firm considers its sunk

The Firm’s Short-Run Decision to Shut Down

The firm shuts down if

The Firm’s Short-Run Decision to Shut Down

The firm shuts down if

Figure 3 The Competitive Firm’s Short Run Supply Curve

Copyright © 2004

Figure 3 The Competitive Firm’s Short Run Supply Curve

Copyright © 2004

The Firm’s Short-Run Decision to Shut Down

The portion of the marginal-cost

The Firm’s Short-Run Decision to Shut Down

The portion of the marginal-cost

The Firm’s Long-Run Decision to Exit or Enter a Market

In the

The Firm’s Long-Run Decision to Exit or Enter a Market

In the

The Firm’s Long-Run Decision to Exit or Enter a Market

A firm

The Firm’s Long-Run Decision to Exit or Enter a Market

A firm

Figure 4 The Competitive Firm’s Long-Run Supply Curve

Copyright © 2004 South-Western

Quantity

0

Costs

Figure 4 The Competitive Firm’s Long-Run Supply Curve

Copyright © 2004 South-Western

Quantity

0

Costs

THE SUPPLY CURVE IN A COMPETITIVE MARKET

The competitive firm’s long-run supply

THE SUPPLY CURVE IN A COMPETITIVE MARKET

The competitive firm’s long-run supply

Figure 4 The Competitive Firm’s Long-Run Supply Curve

Copyright © 2004 South-Western

Quantity

0

Costs

Figure 4 The Competitive Firm’s Long-Run Supply Curve

Copyright © 2004 South-Western

Quantity

0

Costs

THE SUPPLY CURVE IN A COMPETITIVE MARKET

Short-Run Supply Curve

The portion of

THE SUPPLY CURVE IN A COMPETITIVE MARKET

Short-Run Supply Curve

The portion of

Figure 5 Profit as the Area between Price and Average Total

Figure 5 Profit as the Area between Price and Average Total

Figure 5 Profit as the Area between Price and Average Total

Figure 5 Profit as the Area between Price and Average Total

THE SUPPLY CURVE IN A COMPETITIVE MARKET

Market supply equals the sum

THE SUPPLY CURVE IN A COMPETITIVE MARKET

Market supply equals the sum

The Short Run: Market Supply with a Fixed Number of Firms

For

The Short Run: Market Supply with a Fixed Number of Firms

For

Figure 6 Market Supply with a Fixed Number of Firms

Copyright ©

Figure 6 Market Supply with a Fixed Number of Firms

Copyright ©

The Long Run: Market Supply with Entry and Exit

Firms will enter

The Long Run: Market Supply with Entry and Exit

Firms will enter

Figure 7 Market Supply with Entry and Exit

Copyright © 2004 South-Western

(a)

Figure 7 Market Supply with Entry and Exit

Copyright © 2004 South-Western

(a)

The Long Run: Market Supply with Entry and Exit

At the end

The Long Run: Market Supply with Entry and Exit

At the end

Why Do Competitive Firms Stay in Business If They Make Zero

Why Do Competitive Firms Stay in Business If They Make Zero

A Shift in Demand in the Short Run and

Long Run

An

A Shift in Demand in the Short Run and

Long Run

An

Figure 8 An Increase in Demand in the Short Run and

Figure 8 An Increase in Demand in the Short Run and

Figure 8 An Increase in Demand in the Short Run and

Figure 8 An Increase in Demand in the Short Run and

Figure 8 An Increase in Demand in the Short Run and

Figure 8 An Increase in Demand in the Short Run and

Why the Long-Run Supply Curve Might Slope Upward

Some resources used in

Why the Long-Run Supply Curve Might Slope Upward

Some resources used in

Why the Long-Run Supply Curve Might Slope Upward

Marginal Firm

The marginal

Why the Long-Run Supply Curve Might Slope Upward

Marginal Firm

The marginal

Summary

Because a competitive firm is a price taker, its revenue is

Summary

Because a competitive firm is a price taker, its revenue is

Summary

To maximize profit, a firm chooses the quantity of output such

Summary

To maximize profit, a firm chooses the quantity of output such

Summary

In the short run, when a firm cannot recover its fixed

Summary

In the short run, when a firm cannot recover its fixed

Теория общественного выбора. Общественный выбор, предмет и метод анализа

Теория общественного выбора. Общественный выбор, предмет и метод анализа Международная торговля услугами

Международная торговля услугами Природные богатства и труд людей - основа экономики

Природные богатства и труд людей - основа экономики Фирмы в экономике

Фирмы в экономике Рынок. Рыночный механизм

Рынок. Рыночный механизм Эффект дохода

Эффект дохода Инфляция (виды, причины и последствия)

Инфляция (виды, причины и последствия) Виды торговли

Виды торговли Реформы А.Н.Косыгина

Реформы А.Н.Косыгина Оценка конкурентоспособности коммерческого предприятия и пути её повышения

Оценка конкурентоспособности коммерческого предприятия и пути её повышения Экономика фирмы. Фирма на рынке. Рыночные структуры

Экономика фирмы. Фирма на рынке. Рыночные структуры Экономика для юриспруденции. Схемы, таблицы, графики

Экономика для юриспруденции. Схемы, таблицы, графики Интераактивная игра. Семейный бюджет

Интераактивная игра. Семейный бюджет Введение в экономику. Рынок. Рыночный механизм

Введение в экономику. Рынок. Рыночный механизм Содержание, предмет, задачи и методика экономического анализа. (Тема 1)

Содержание, предмет, задачи и методика экономического анализа. (Тема 1) Миграция рабочей силы Японии

Миграция рабочей силы Японии Саны экономикалық белсенді халық

Саны экономикалық белсенді халық Развитие торгово - экономических связей между Китаем и Россией

Развитие торгово - экономических связей между Китаем и Россией Понятие и виды цен. (Лекция 1)

Понятие и виды цен. (Лекция 1) Инфляция (виды, причины и последствия)

Инфляция (виды, причины и последствия) Международные экономические отношения. (Тема 15)

Международные экономические отношения. (Тема 15) Девелопмент в инвестиционно-строительной деятельности

Девелопмент в инвестиционно-строительной деятельности Сущность и содержание государственного регулирования рыночной экономики

Сущность и содержание государственного регулирования рыночной экономики Аналіз наявності та ефективності використання основних засобів і нематеріальних активів підприємства

Аналіз наявності та ефективності використання основних засобів і нематеріальних активів підприємства Россия в системе международного бизнеса

Россия в системе международного бизнеса Организация оплаты труда на предприятии. Вопрос 4

Организация оплаты труда на предприятии. Вопрос 4 Теория рыночного равновесия под воздействием закона спроса и предложения

Теория рыночного равновесия под воздействием закона спроса и предложения Модель экономического роста Р.Нельсона – С.Уинтера

Модель экономического роста Р.Нельсона – С.Уинтера