- Dynamic models and the Kalman filter

Содержание

- 2. Introduction and Motivation The dynamics of a time series can be influenced by “unobservable” (sometimes called

- 3. Introduction and Motivation (continued) State space representation is a way to describe the law of motion

- 4. Common Usage of These Techniques Macroeconomics, finance, time series models Autopilot, radar tracking Orbit tracking, satellite

- 5. Another example Use nightlight data and the Kalman filter to adjust official GDP growth statistics. The

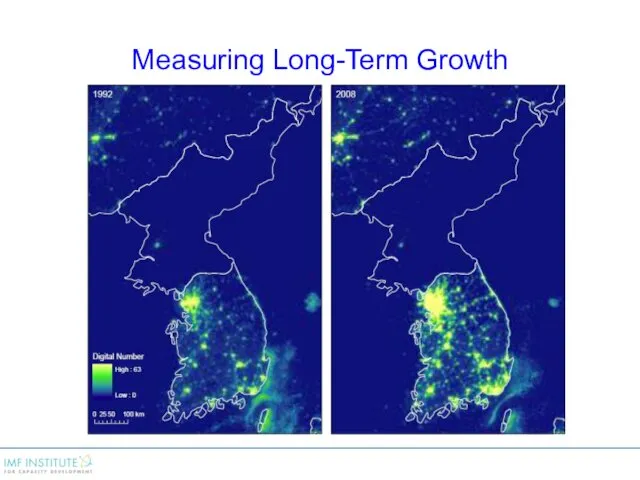

- 6. Measuring Long-Term Growth

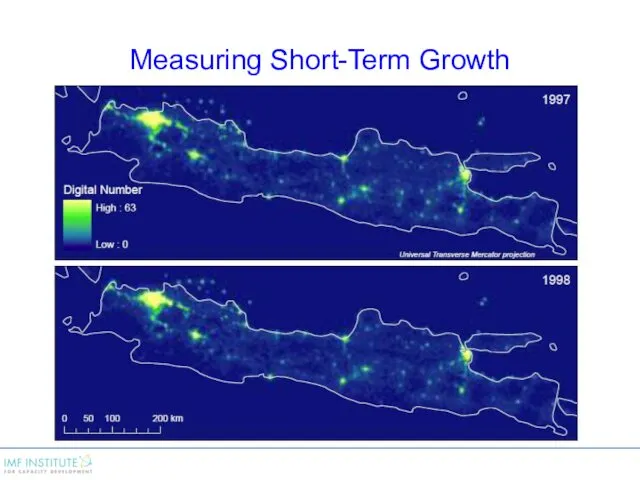

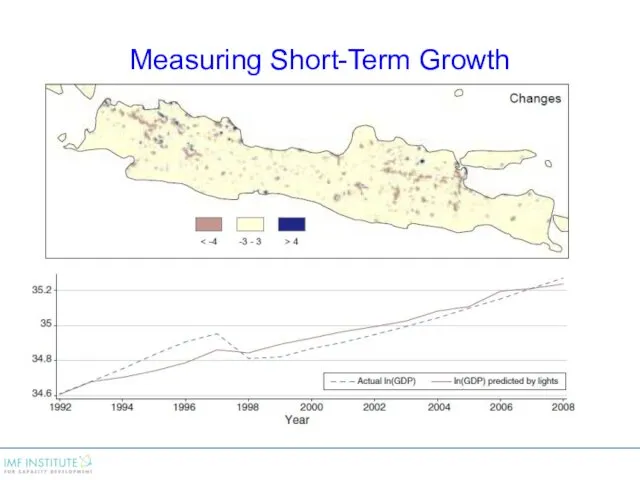

- 7. Measuring Short-Term Growth

- 8. Measuring Short-Term Growth

- 9. Content Outline: Lecture Segments State Space Representation The Kalman Filter Maximum Likelihood Estimation and Kalman Smoothing

- 10. Content Outline: Workshops Workshops Estimation of equilibrium real interest rate, trend growth rate, and potential output

- 11. State Space Representation

- 12. Basic Setup Let yt be an (or a vector) observable variable(s) at time t. E.g., return

- 13. Basic Setup The state-space representation of the dynamics of yt is given by : We assume

- 14. Basic Setup The state-space representation of the dynamics of yt is given by : with The

- 15. Basic Setup The error terms in the two equations are such that: State equation Observation equation

- 16. What if you know that are serially correlated: and , Then so one of the assumptions

- 17. The State Space Representation: Examples Example #1: simple version of the CAPM st one variable, return

- 18. Example #2: growth and real business cycle (small open economy with a large export sector) st

- 19. Example #3: interest rates on zero-coupon bonds of different maturity st one variable, latent variable yt

- 20. Example #4: an AR(2) process Can we still apply the state space representation? Yes! Consider the

- 21. Example #4: an AR(2) process The state equation: And the observation equation: What are matrices Ω

- 22. Consider the same AR(2) process Another possible state equation: And the corresponding observation equation: These two

- 23. Example #5: an MA(2) process Consider the following state equation: And the observation equation: What are

- 24. Example #5: an MA(2) process Consider the following state equation: And the observation equation: What are

- 25. Example #6: A random walk plus drift process State equation? Observation equation? What are the loadings

- 26. In this course we will deal only with stable systems: Such systems that for any initial

- 27. The Kalman Filter

- 28. State Space Representation [univariate case]: Notation: is the best linear predictor of st conditional on the

- 29. Kalman Filter: Main Idea Moving from t-1 to t Suppose we know and at time t-1.

- 30. Kalman Filter: Main Idea How to update st|t ? Idea: use the observed prediction error to

- 31. Kalman Filter: More Notations is the prediction error variance of given the history of observed variables

- 32. Kalman Gain: Intuition Kalman gain is chosen so that is minimized. It can be shown that

- 33. Kalman Filter: Example Kalman gain is Consider State equation Observation equation Additionally , where is a

- 34. Kalman Filter: The last step How do we get from to using ? Recall that for

- 35. Kalman Filter: Finally From the previous slide st|t = st|t-1+βPt|t-1(Ft|t-1)-1(yt - yt|t-1) Pt|t = Pt|t-1 –

- 36. Kalman Filter: Review We start from and . yt|t-1 = αxt + βst|t-1 Calculate Kalman gain

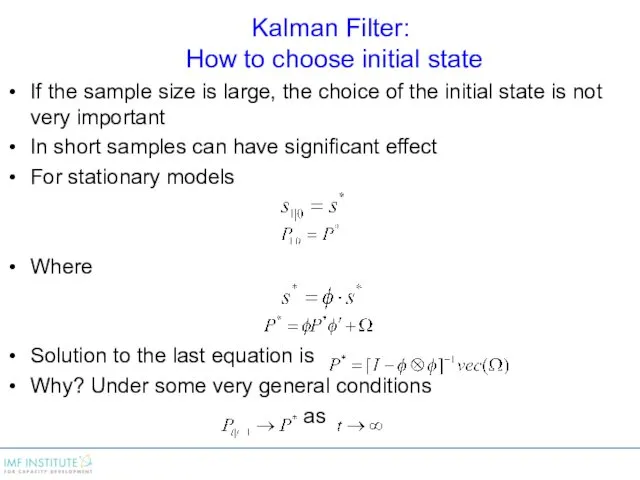

- 37. Kalman Filter: How to choose initial state If the sample size is large, the choice of

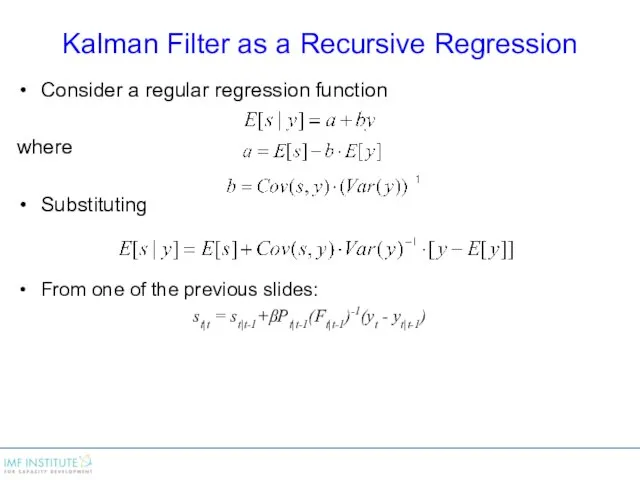

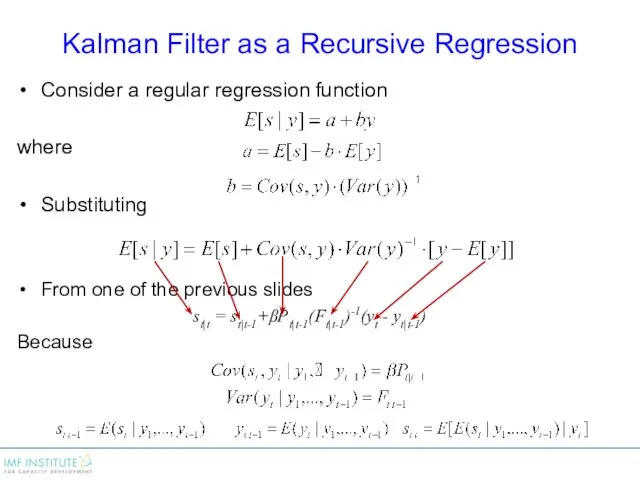

- 38. Kalman Filter as a Recursive Regression Consider a regular regression function where Substituting From one of

- 39. Kalman Filter as a Recursive Regression Consider a regular regression function where Substituting From one of

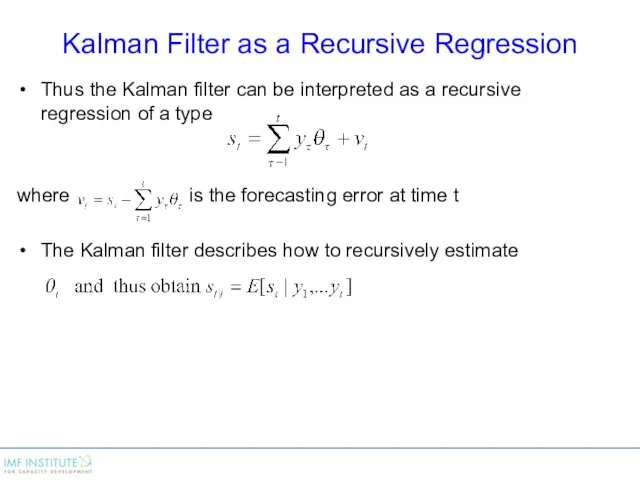

- 40. Kalman Filter as a Recursive Regression Thus the Kalman filter can be interpreted as a recursive

- 41. Optimality of the Kalman Filter Using the property of OLS estimates that constructed residuals are uncorrelated

- 42. Kalman Filter Some comments Within the class of linear (in observables) predictors the Kalman filter algorithm

- 43. Kalman Filter - Multivariate Case The Kalman Filter algorithm can be easily generalized to the generic

- 44. Kalman Filter Algorithm – Multivariate Case

- 45. Kalman Filter Algorithm – Multivariate Case (cont.)

- 46. Kalman Filter Algorithm – Multivariate Case (cont.)

- 47. ML Estimation and Kalman Smoothing

- 48. Maximum Likelihood Estimation The algorithm in the previous section assumes knowledge of the parameters. If these

- 49. To estimate model parameters through maximizing log-likelihood: Step 1: For every set of the underlying parameters,

- 50. Kalman Smoothing For each period t, the Kalman filter uses only information available up to time

- 51. Kalman Smoothing Using the same principles for normal conditional distribution, it is possible to show that

- 53. Скачать презентацию

Introduction and Motivation

The dynamics of a time series can be influenced

Introduction and Motivation

The dynamics of a time series can be influenced

Introduction and Motivation (continued)

State space representation is a way to describe

Introduction and Motivation (continued)

State space representation is a way to describe

Common Usage of These Techniques

Macroeconomics, finance, time series models

Autopilot, radar tracking

Orbit

Common Usage of These Techniques

Macroeconomics, finance, time series models

Autopilot, radar tracking

Orbit

Another example

Use nightlight data and the Kalman filter to adjust official

Another example

Use nightlight data and the Kalman filter to adjust official

Measuring Long-Term Growth

Measuring Long-Term Growth

Measuring Short-Term Growth

Measuring Short-Term Growth

Measuring Short-Term Growth

Measuring Short-Term Growth

Content Outline: Lecture Segments

State Space Representation

The Kalman Filter

Maximum Likelihood Estimation and

Content Outline: Lecture Segments

State Space Representation

The Kalman Filter

Maximum Likelihood Estimation and

Content Outline: Workshops

Workshops

Estimation of equilibrium real interest rate, trend growth rate,

Content Outline: Workshops

Workshops

Estimation of equilibrium real interest rate, trend growth rate,

State Space Representation

State Space Representation

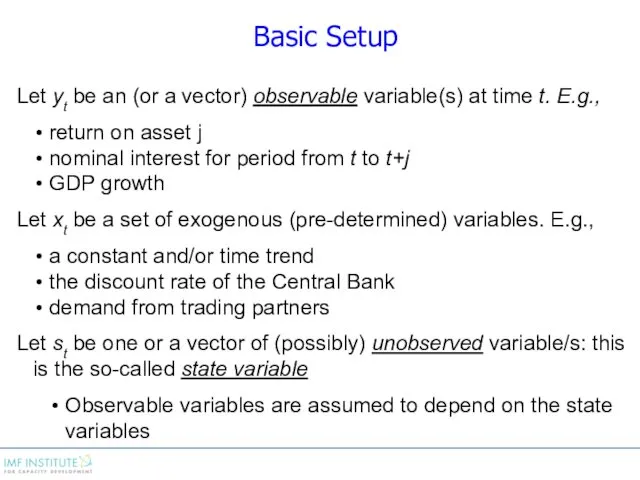

Basic Setup

Let yt be an (or a vector) observable variable(s) at

Basic Setup

Let yt be an (or a vector) observable variable(s) at

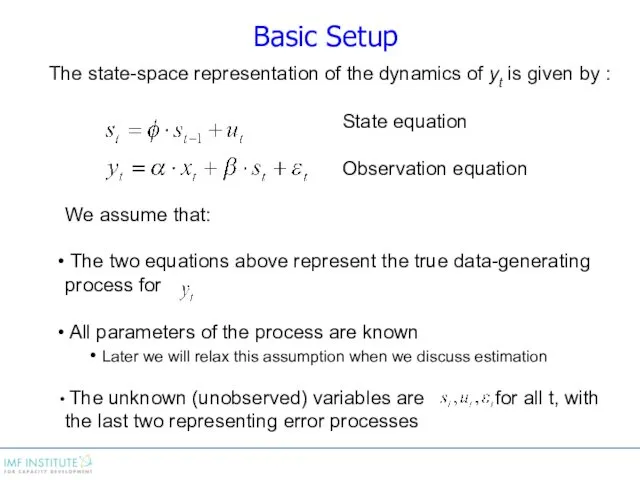

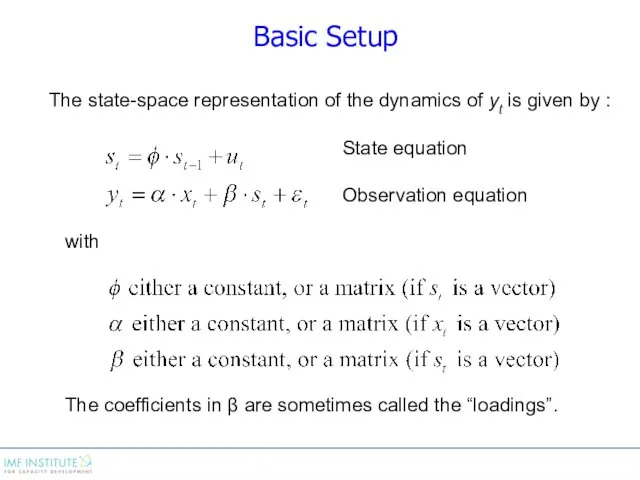

Basic Setup

The state-space representation of the dynamics of yt is given

Basic Setup

The state-space representation of the dynamics of yt is given

Basic Setup

The state-space representation of the dynamics of yt is given

Basic Setup

The state-space representation of the dynamics of yt is given

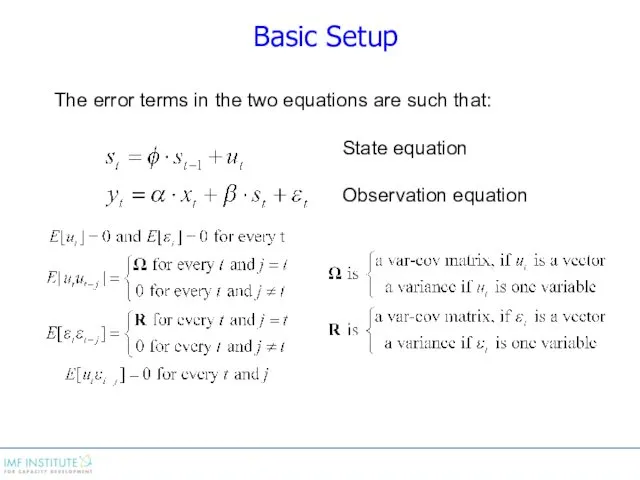

Basic Setup

The error terms in the two equations are such that:

State

Basic Setup

The error terms in the two equations are such that:

State

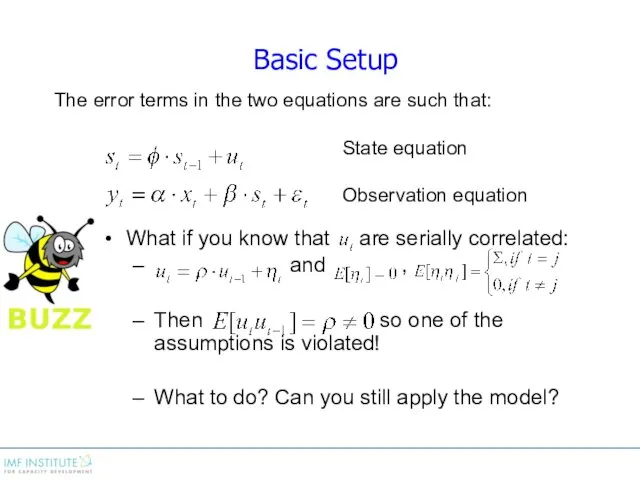

What if you know that are serially correlated:

and ,

What if you know that are serially correlated:

and ,

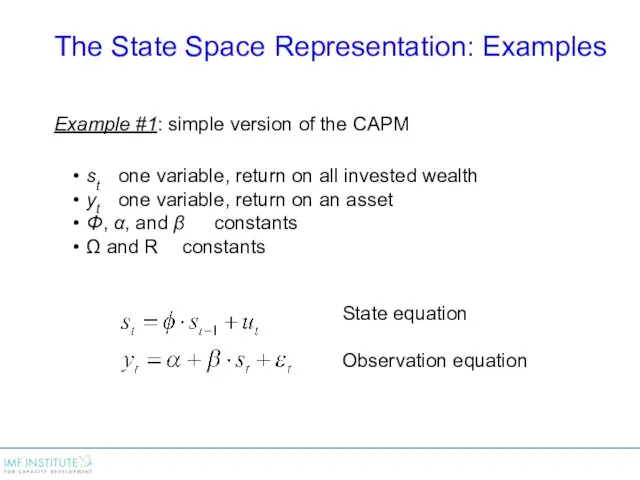

The State Space Representation: Examples

Example #1: simple version of the CAPM

st one

The State Space Representation: Examples

Example #1: simple version of the CAPM

st one

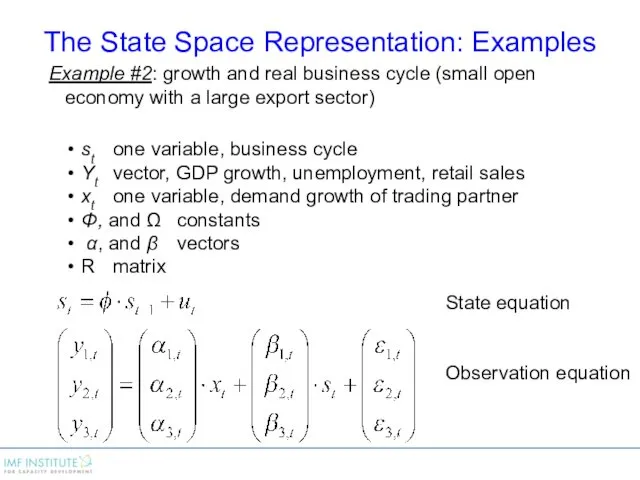

Example #2: growth and real business cycle (small open economy with

Example #2: growth and real business cycle (small open economy with

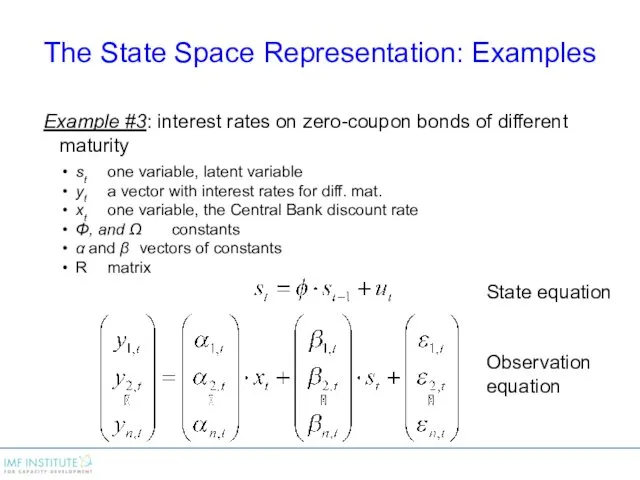

Example #3: interest rates on zero-coupon bonds of different maturity

st one variable,

Example #3: interest rates on zero-coupon bonds of different maturity

st one variable,

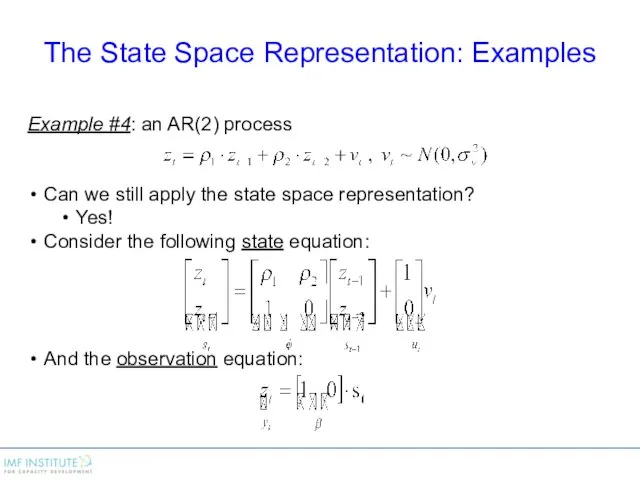

Example #4: an AR(2) process

Can we still apply the state space

Example #4: an AR(2) process

Can we still apply the state space

Example #4: an AR(2) process

The state equation:

And the observation equation:

What are

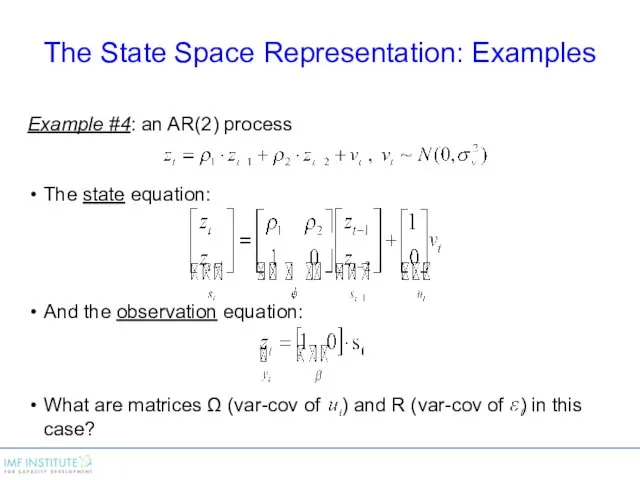

Example #4: an AR(2) process

The state equation:

And the observation equation:

What are

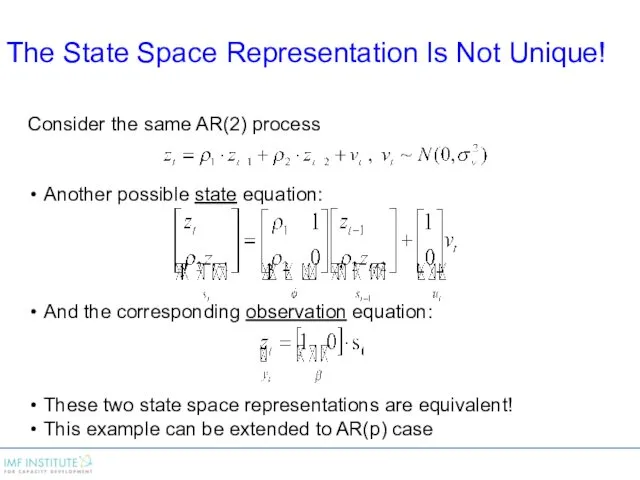

Consider the same AR(2) process

Another possible state equation:

And the corresponding observation

Consider the same AR(2) process

Another possible state equation:

And the corresponding observation

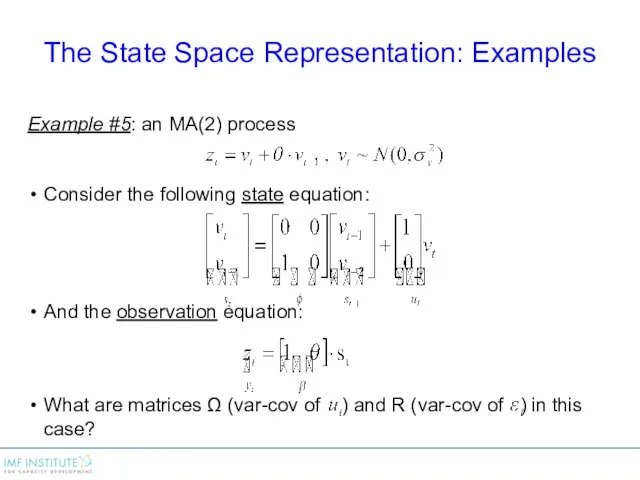

Example #5: an MA(2) process

Consider the following state equation:

And the observation

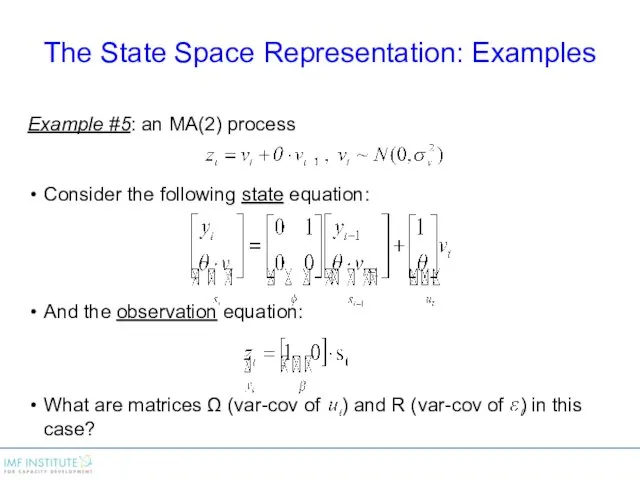

Example #5: an MA(2) process

Consider the following state equation:

And the observation

Example #5: an MA(2) process

Consider the following state equation:

And the observation

Example #5: an MA(2) process

Consider the following state equation:

And the observation

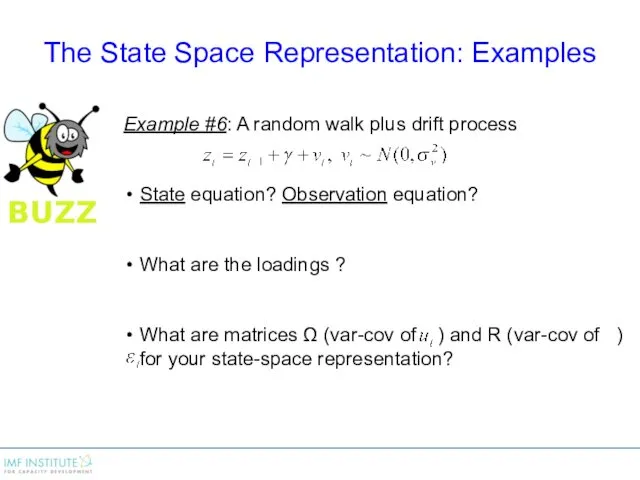

Example #6: A random walk plus drift process

State equation? Observation equation?

What

Example #6: A random walk plus drift process

State equation? Observation equation?

What

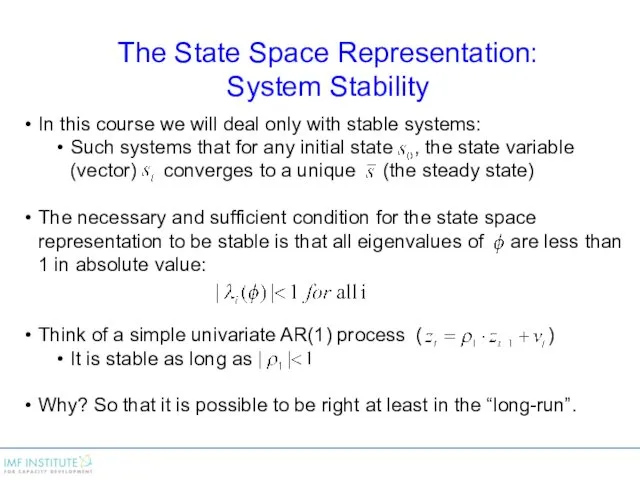

In this course we will deal only with stable systems:

Such systems

In this course we will deal only with stable systems:

Such systems

The Kalman Filter

The Kalman Filter

![State Space Representation [univariate case]: Notation: is the best linear](/_ipx/f_webp&q_80&fit_contain&s_1440x1080/imagesDir/jpg/96593/slide-27.jpg)

State Space Representation [univariate case]:

Notation:

is the best linear predictor

State Space Representation [univariate case]:

Notation:

is the best linear predictor

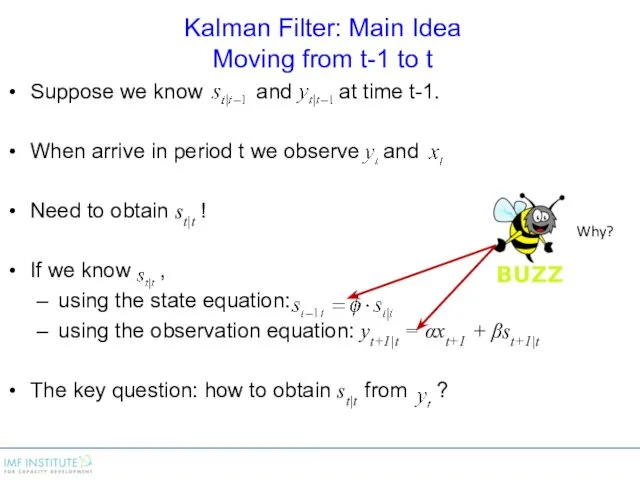

Kalman Filter: Main Idea

Moving from t-1 to t

Suppose we know

Kalman Filter: Main Idea

Moving from t-1 to t

Suppose we know

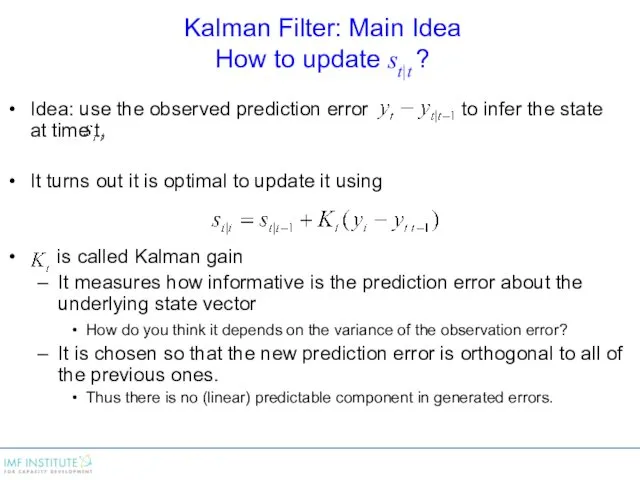

Kalman Filter: Main Idea

How to update st|t ?

Idea: use the observed

Kalman Filter: Main Idea

How to update st|t ?

Idea: use the observed

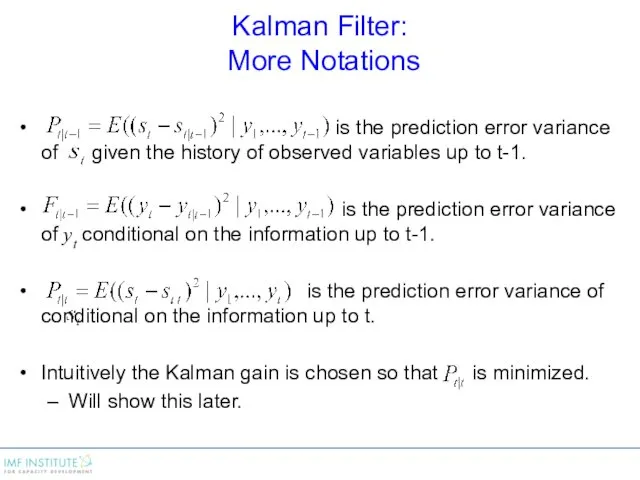

Kalman Filter:

More Notations

is the prediction error variance of given

Kalman Filter:

More Notations

is the prediction error variance of given

Kalman Gain:

Intuition

Kalman gain is chosen so that is minimized.

It can be

Kalman Gain:

Intuition

Kalman gain is chosen so that is minimized.

It can be

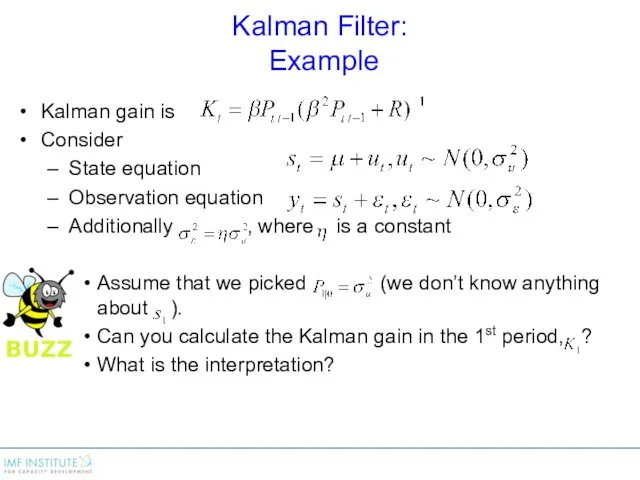

Kalman Filter:

Example

Kalman gain is

Consider

State equation

Observation equation

Additionally

Kalman Filter:

Example

Kalman gain is

Consider

State equation

Observation equation

Additionally

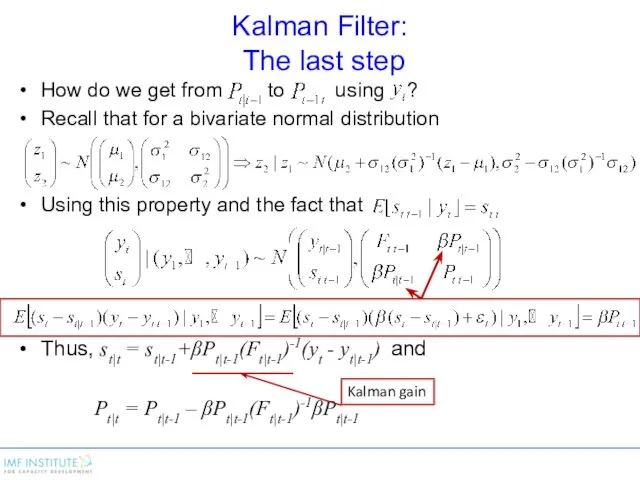

Kalman Filter:

The last step

How do we get from to using

Kalman Filter:

The last step

How do we get from to using

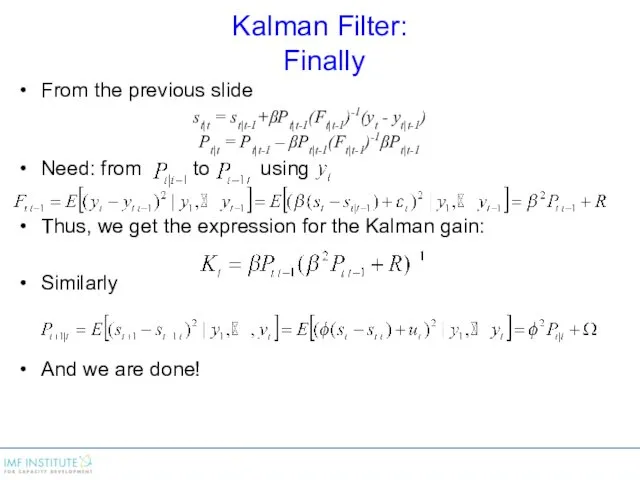

Kalman Filter:

Finally

From the previous slide

st|t = st|t-1+βPt|t-1(Ft|t-1)-1(yt - yt|t-1)

Pt|t

Kalman Filter:

Finally

From the previous slide

st|t = st|t-1+βPt|t-1(Ft|t-1)-1(yt - yt|t-1)

Pt|t

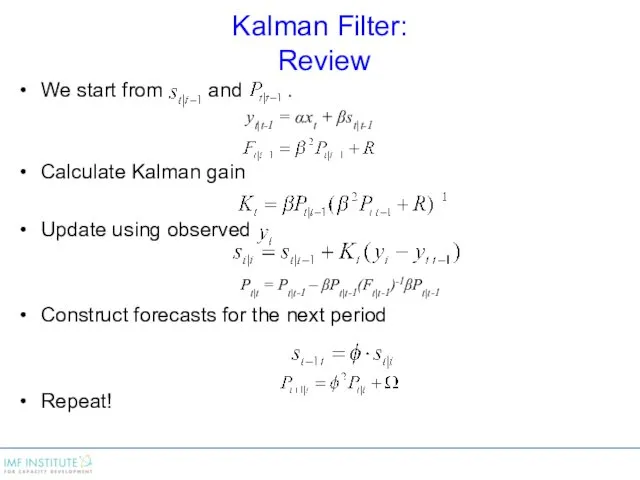

Kalman Filter:

Review

We start from and .

yt|t-1 = αxt +

Kalman Filter:

Review

We start from and .

yt|t-1 = αxt +

Kalman Filter:

How to choose initial state

If the sample size is

Kalman Filter:

How to choose initial state

If the sample size is

Kalman Filter as a Recursive Regression

Consider a regular regression function

where

Substituting

From

Kalman Filter as a Recursive Regression

Consider a regular regression function

where

Substituting

From

Kalman Filter as a Recursive Regression

Consider a regular regression function

where

Substituting

From

Kalman Filter as a Recursive Regression

Consider a regular regression function

where

Substituting

From

Kalman Filter as a Recursive Regression

Thus the Kalman filter can be

Kalman Filter as a Recursive Regression

Thus the Kalman filter can be

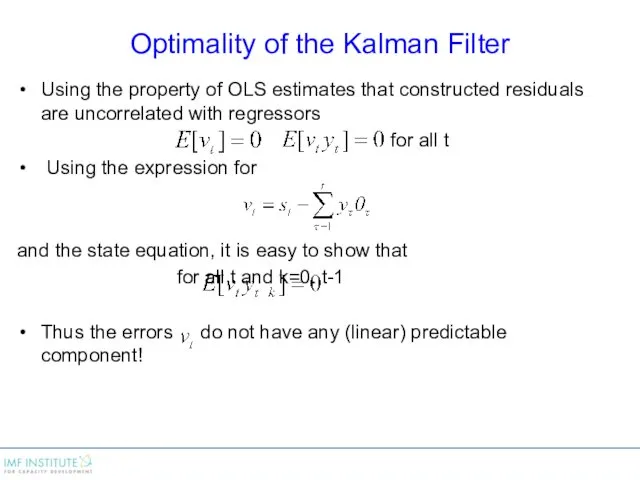

Optimality of the Kalman Filter

Using the property of OLS estimates that

Optimality of the Kalman Filter

Using the property of OLS estimates that

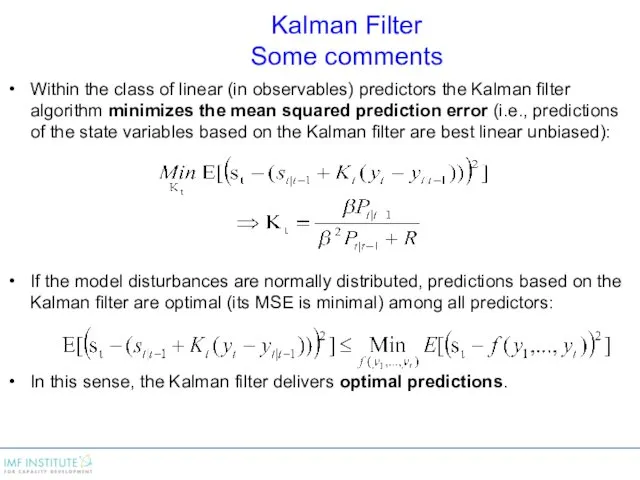

Kalman Filter

Some comments

Within the class of linear (in observables) predictors the

Kalman Filter

Some comments

Within the class of linear (in observables) predictors the

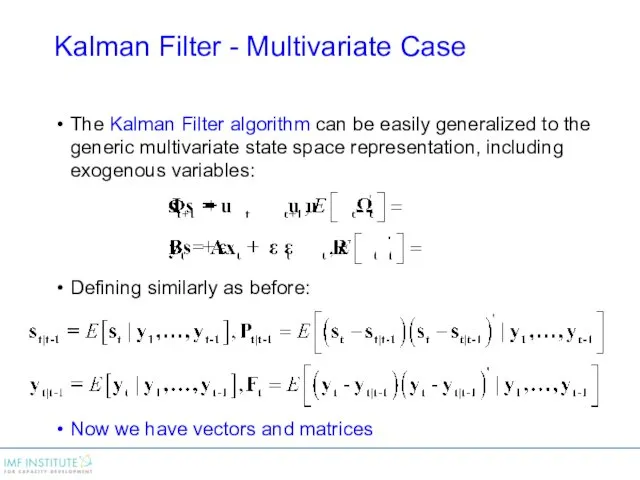

Kalman Filter - Multivariate Case

The Kalman Filter algorithm can be easily

Kalman Filter - Multivariate Case

The Kalman Filter algorithm can be easily

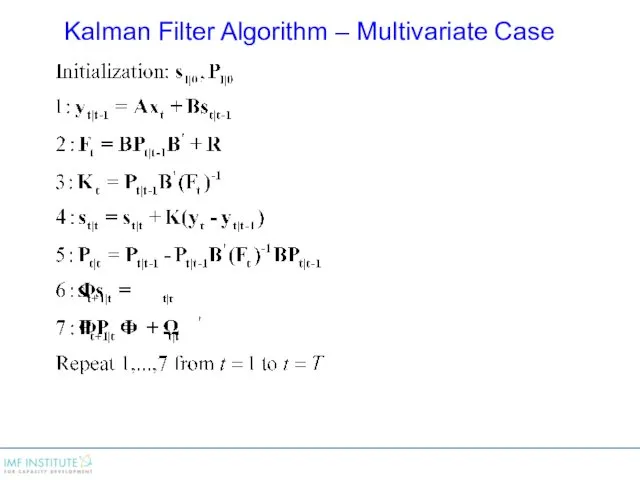

Kalman Filter Algorithm – Multivariate Case

Kalman Filter Algorithm – Multivariate Case

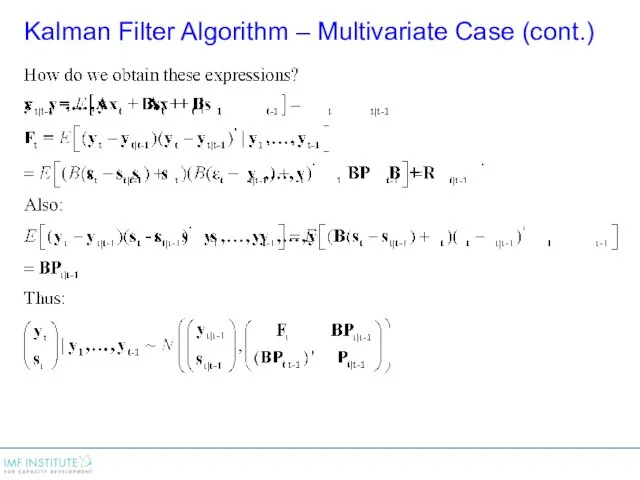

Kalman Filter Algorithm – Multivariate Case (cont.)

Kalman Filter Algorithm – Multivariate Case (cont.)

Kalman Filter Algorithm – Multivariate Case (cont.)

Kalman Filter Algorithm – Multivariate Case (cont.)

ML Estimation and Kalman Smoothing

ML Estimation and Kalman Smoothing

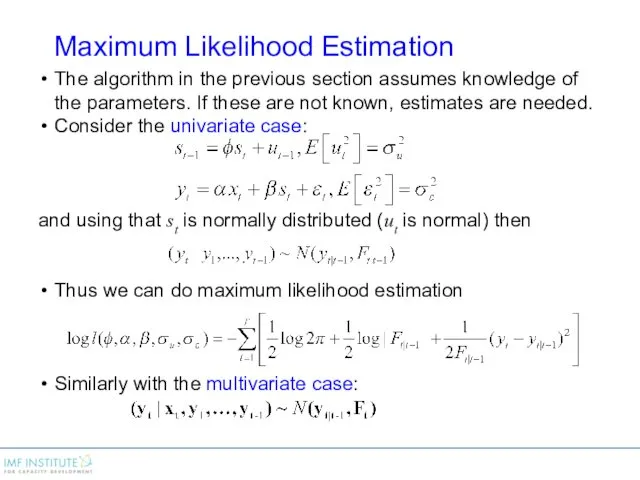

Maximum Likelihood Estimation

The algorithm in the previous section assumes knowledge of

Maximum Likelihood Estimation

The algorithm in the previous section assumes knowledge of

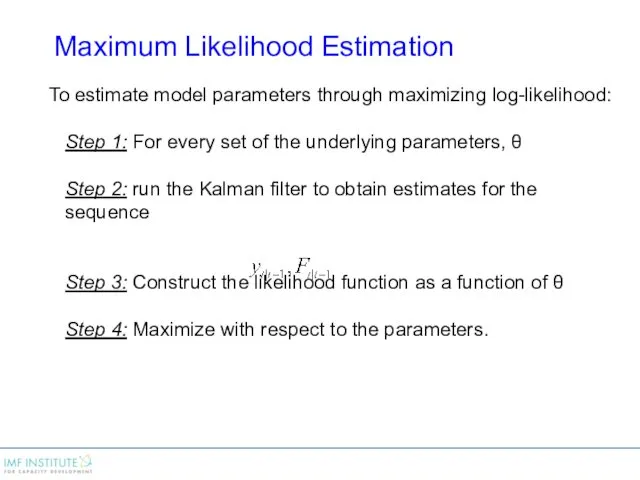

To estimate model parameters through maximizing log-likelihood:

Step 1: For every set

To estimate model parameters through maximizing log-likelihood:

Step 1: For every set

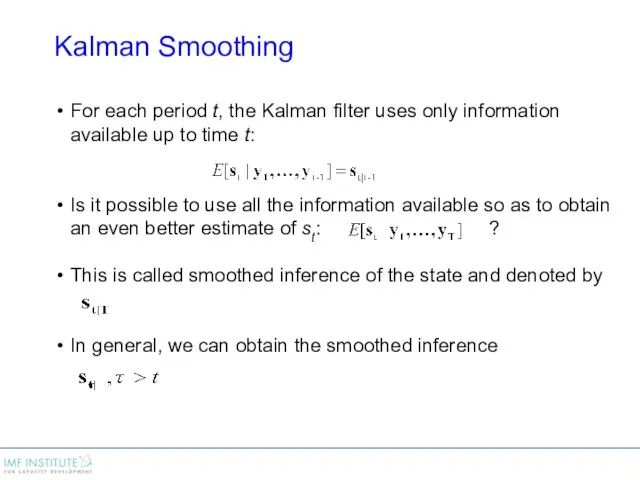

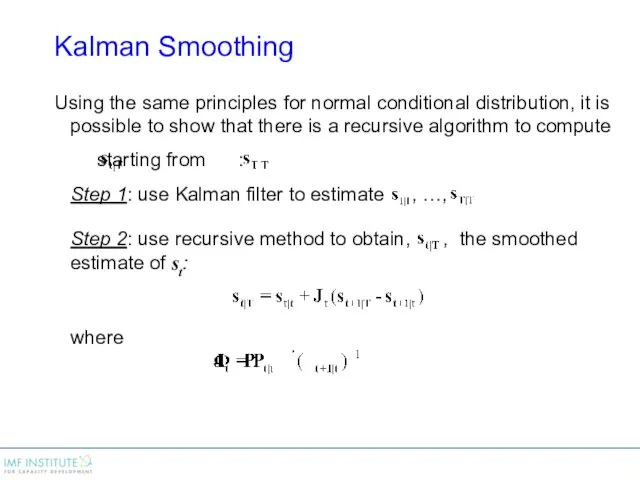

Kalman Smoothing

For each period t, the Kalman filter uses only information

Kalman Smoothing

For each period t, the Kalman filter uses only information

Kalman Smoothing

Using the same principles for normal conditional distribution, it is

Kalman Smoothing

Using the same principles for normal conditional distribution, it is

Равнодействующая сил

Равнодействующая сил Protein structure: prediction engineering design

Protein structure: prediction engineering design Механика жидкостей и газов. (Лекция 9)

Механика жидкостей и газов. (Лекция 9) Масса тела

Масса тела Ремонт автомобилей. Ремонт коленчатых валов и шатунов. (Тема 4.5)

Ремонт автомобилей. Ремонт коленчатых валов и шатунов. (Тема 4.5) Техническое обслуживание рулевого управления автомобиля Toyota Mark II

Техническое обслуживание рулевого управления автомобиля Toyota Mark II Простые механизмы в технике и в быту

Простые механизмы в технике и в быту Машиноведение. История создания швейной машины

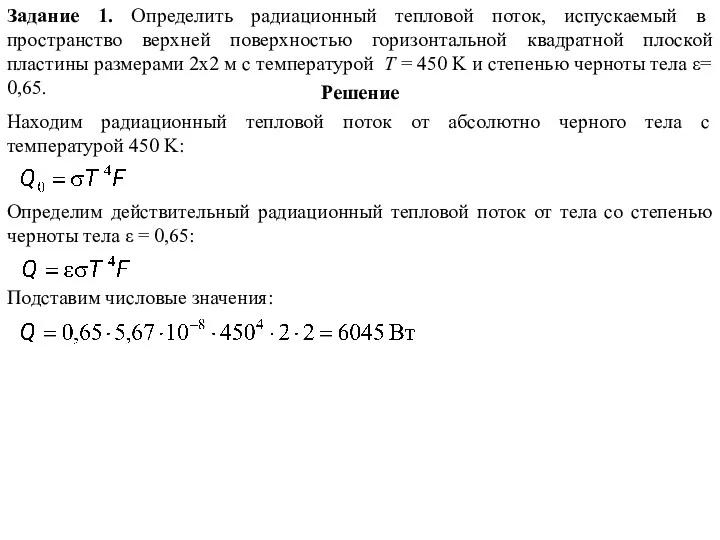

Машиноведение. История создания швейной машины Тепловое излучение. Задачи

Тепловое излучение. Задачи Что изучает физика? Некоторые физические термины

Что изучает физика? Некоторые физические термины Прості механізми побутових пристроїв

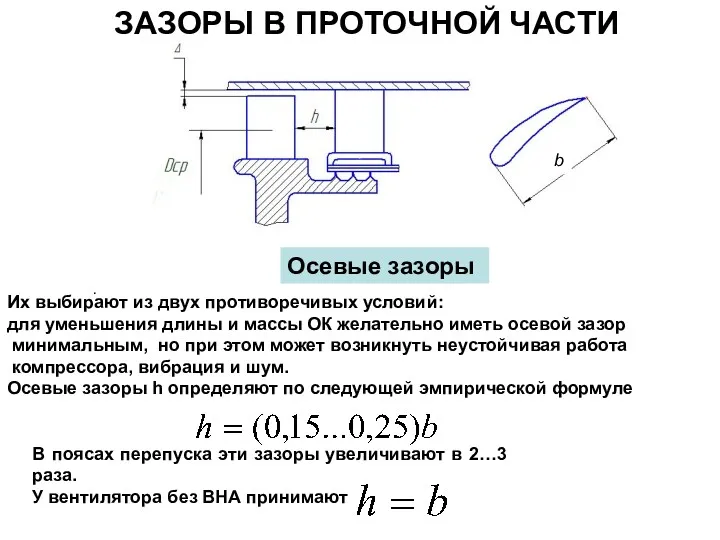

Прості механізми побутових пристроїв Зазоры в проточной части

Зазоры в проточной части Магнитное поле. Взаимодействие токов

Магнитное поле. Взаимодействие токов Механізація подрібнення стеблових кормів

Механізація подрібнення стеблових кормів Сила трения. Трение в природе и технике

Сила трения. Трение в природе и технике Ремонт авиационного оборудования с боевыми и эксплуатационными повреждениями

Ремонт авиационного оборудования с боевыми и эксплуатационными повреждениями Коробки перемены передач

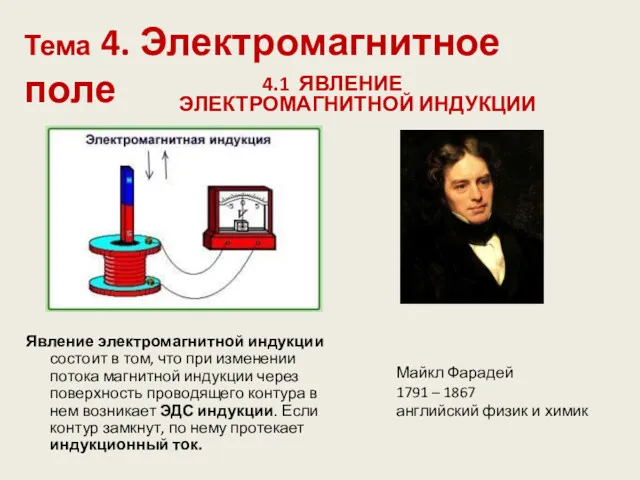

Коробки перемены передач Электромагнитное поле

Электромагнитное поле Физика в нашей жизни

Физика в нашей жизни Влияние на работу дороги природных факторов

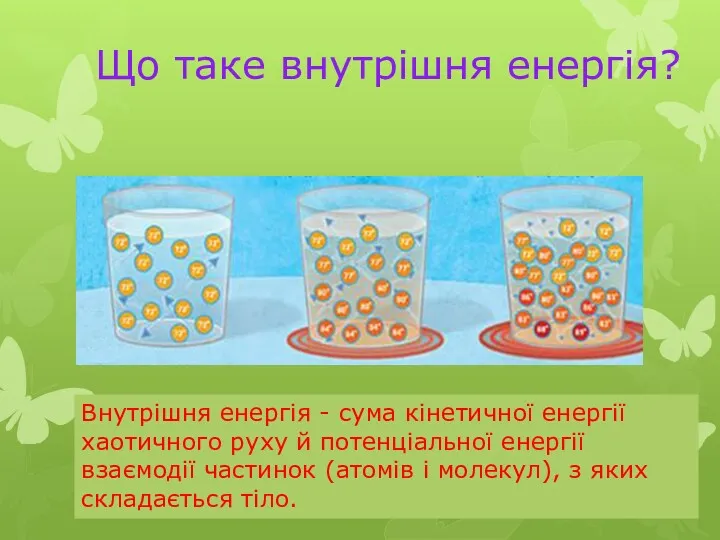

Влияние на работу дороги природных факторов Внутрішня енергія

Внутрішня енергія Основы поверхностной обработки полупроводниковых материалов

Основы поверхностной обработки полупроводниковых материалов Урок презентация Реактивное движение

Урок презентация Реактивное движение Закон Ома на участке цепи. Диаграмма связи величин: U, I, R

Закон Ома на участке цепи. Диаграмма связи величин: U, I, R Разработка установки для замены масла в двигателе

Разработка установки для замены масла в двигателе Закон всемирного тяготения

Закон всемирного тяготения Магнитное поле

Магнитное поле Ионизирующие излучения

Ионизирующие излучения