- Modeling of nonstationary time series using nonparametric methods

Содержание

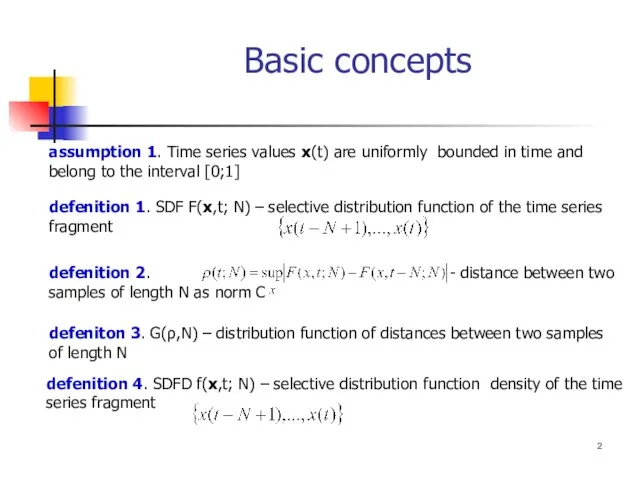

- 2. Basic concepts assumption 1. Time series values x(t) are uniformly bounded in time and belong to

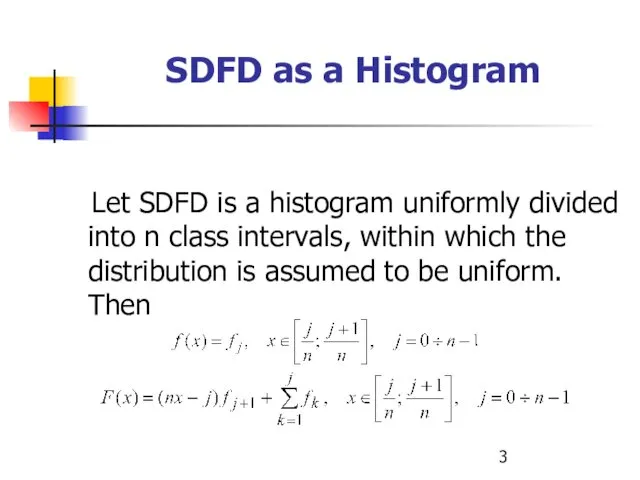

- 3. Let SDFD is a histogram uniformly divided into n class intervals, within which the distribution is

- 4. Solved problems Developing of a nonparametric indicator of a breakdown for a selective distribution function in

- 5. Practical use Earthquake research Medicine Text analysis Telecommunications Stocks market

- 6. Why is it important to take in account the non stationary nature of the series All

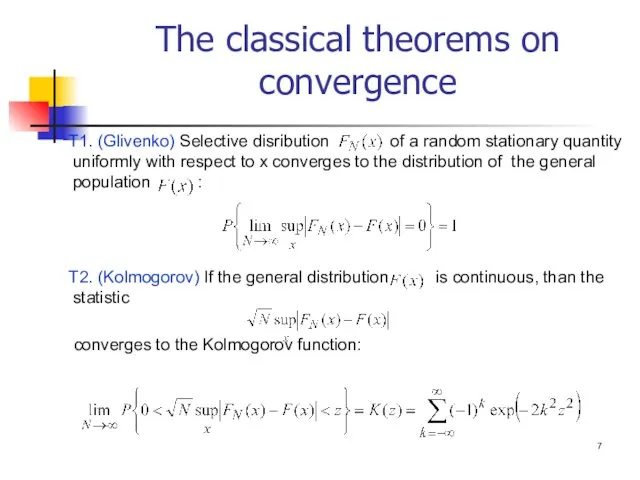

- 7. The classical theorems on convergence Т1. (Glivenko) Selective disribution of a random stationary quantity uniformly with

- 8. Methods of the nonstationary time series analysis Ordinary least squares. Time series cointegriation, i. e. the

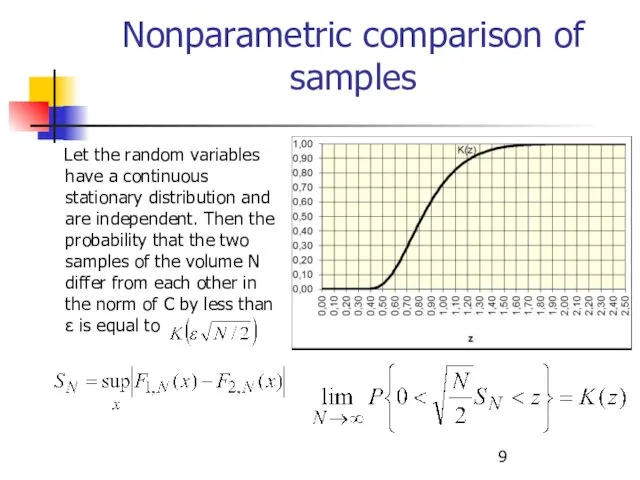

- 9. Nonparametric comparison of samples Let the random variables have a continuous stationary distribution and are independent.

- 10. Distribution function as random value If random value has distribution function F(x), than the distribution function

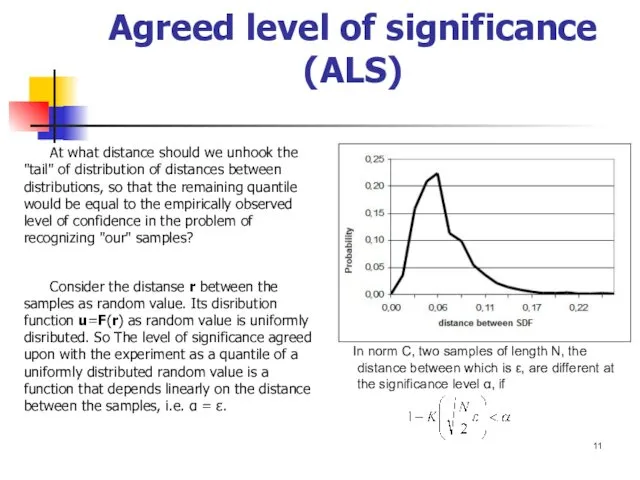

- 11. Agreed level of significance (ALS) At what distance should we unhook the "tail" of distribution of

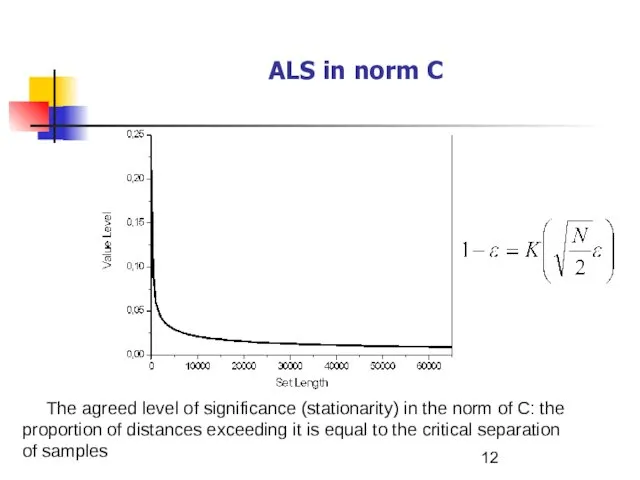

- 12. The agreed level of significance (stationarity) in the norm of C: the proportion of distances exceeding

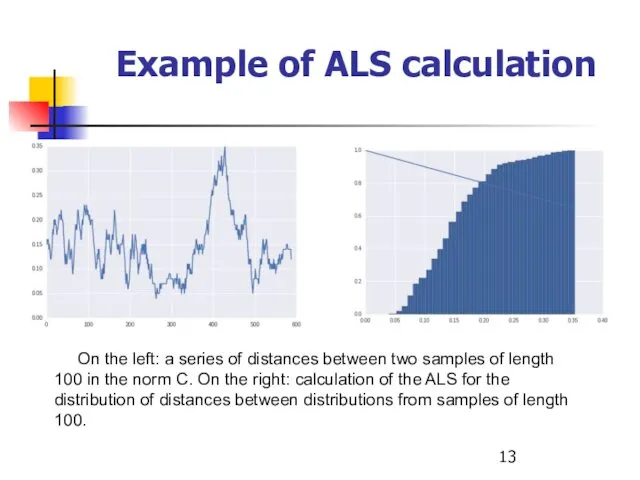

- 13. On the left: a series of distances between two samples of length 100 in the norm

- 14. The ALS in the norm of C for stationary disributions does not depend on the type

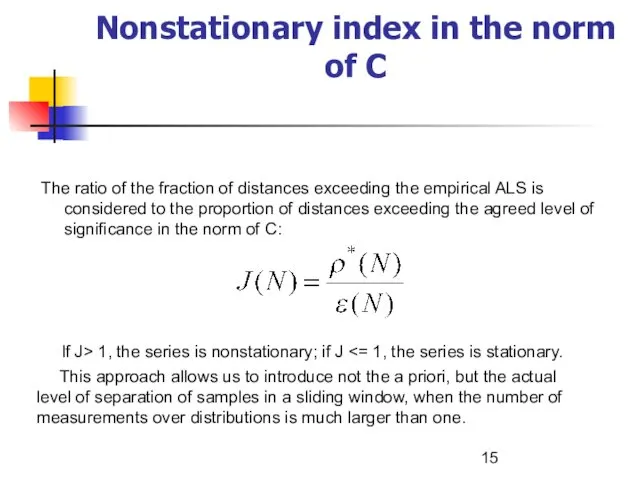

- 15. If J> 1, the series is nonstationary; if J This approach allows us to introduce not

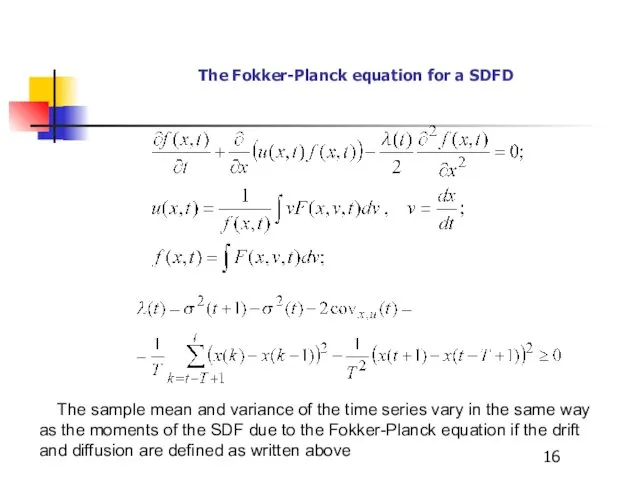

- 16. The Fokker-Planck equation for a SDFD The sample mean and variance of the time series vary

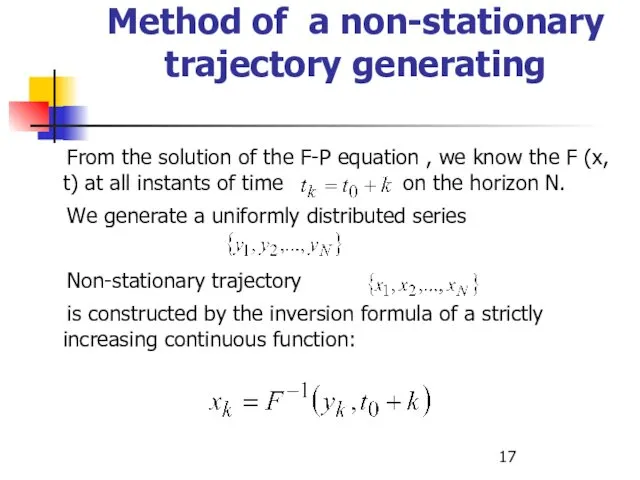

- 17. From the solution of the F-P equation , we know the F (x, t) at all

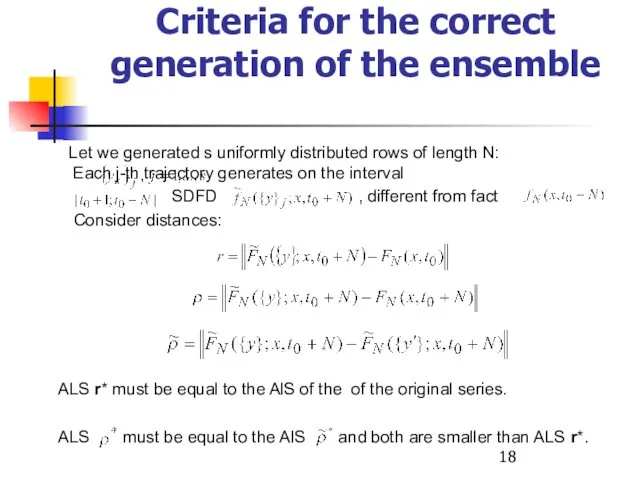

- 18. Criteria for the correct generation of the ensemble Let we generated s uniformly distributed rows of

- 19. Practical examples Example 1 - earthquake statistics In problems of earthquake prediction the main objects of

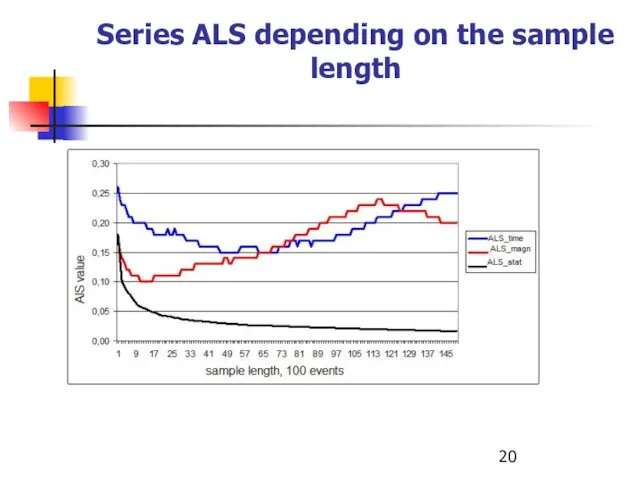

- 20. Series ALS depending on the sample length

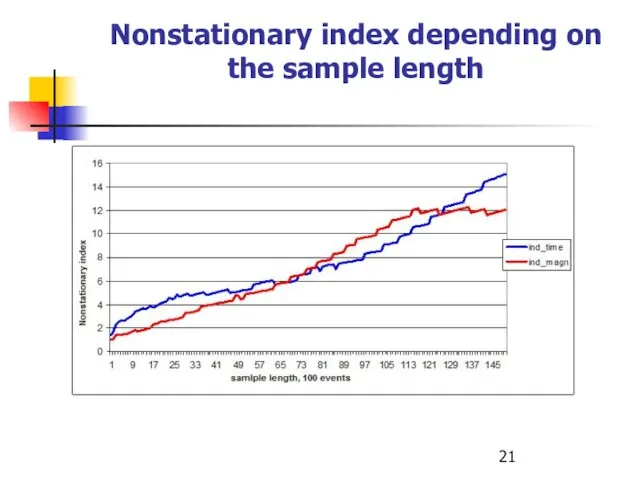

- 21. Nonstationary index depending on the sample length

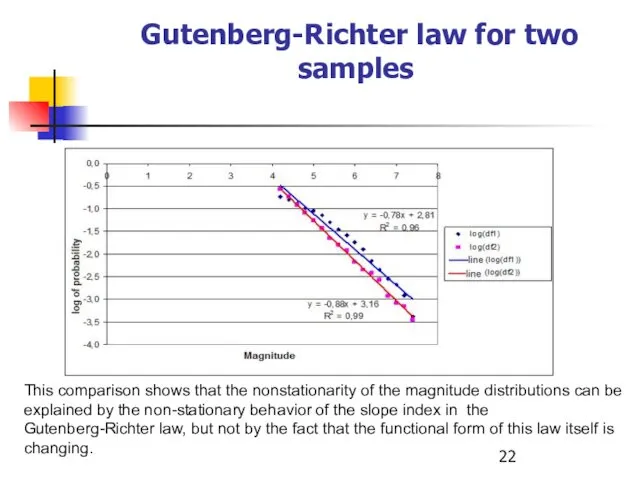

- 22. Gutenberg-Richter law for two samples This comparison shows that the nonstationarity of the magnitude distributions can

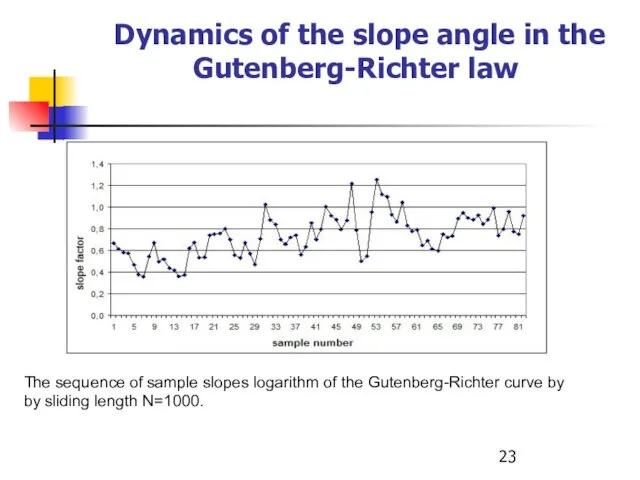

- 23. Dynamics of the slope angle in the Gutenberg-Richter law The sequence of sample slopes logarithm of

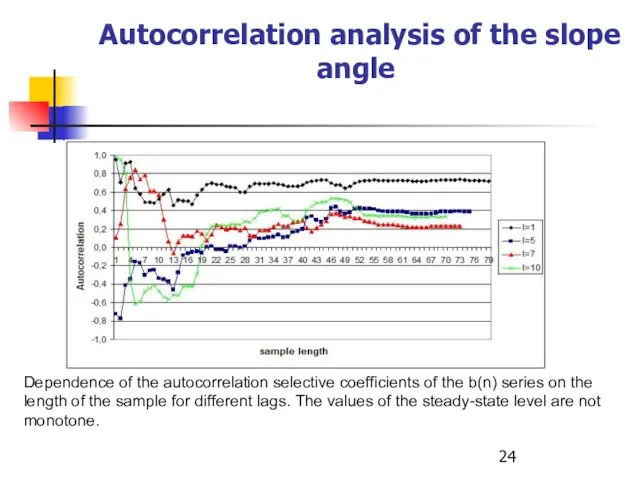

- 24. Autocorrelation analysis of the slope angle Dependence of the autocorrelation selective coefficients of the b(n) series

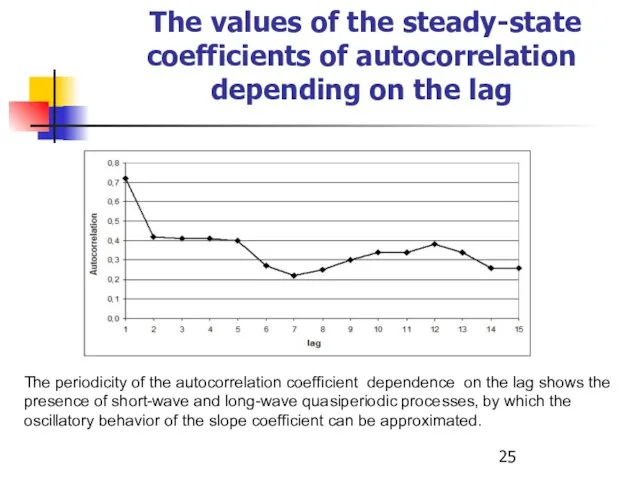

- 25. The values of the steady-state coefficients of autocorrelation depending on the lag The periodicity of the

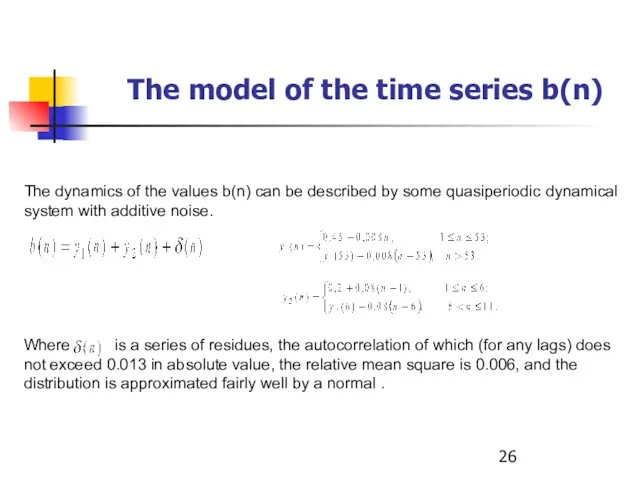

- 26. The model of the time series b(n) The dynamics of the values b(n) can be described

- 27. Nonstationary distributions of magnitudes it was found that the nonstationarity of the distributions magnitude is due

- 28. Earthquake statistics results We analyzed the stationary level of JMA catalog of magnitude and time intervals

- 29. Example 2 - SIR statistics for analysis of 5G networks The reliability of mobile communication is

- 30. From the known distribution function f (x, t), a three-dimensional set of trajectories x (t) is

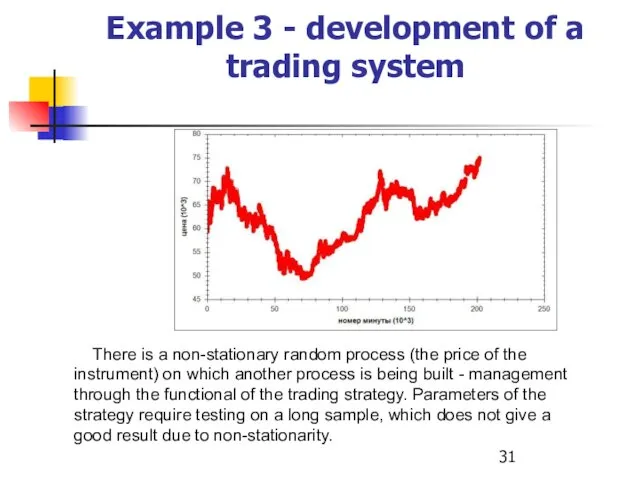

- 31. Example 3 - development of a trading system There is a non-stationary random process (the price

- 32. Problems types Selection of system parameters by historical data Risk-management of a trading System

- 33. Selection of system parameters by historical data A small amount of historical data does not give

- 34. Two types of trajectiories beam generation Generation by historical change of selective distribution. Generation by forecast

- 35. Trajectories beam example

- 36. Strategy equities

- 37. Conclusion Modeling of nonstationary time series has a wide practical application.

- 39. Скачать презентацию

Basic concepts

assumption 1. Time series values x(t) are uniformly bounded

Basic concepts

assumption 1. Time series values x(t) are uniformly bounded

Let SDFD is a histogram uniformly divided into n

Let SDFD is a histogram uniformly divided into n

Solved problems

Developing of a nonparametric indicator of a breakdown for a

Solved problems

Developing of a nonparametric indicator of a breakdown for a

Practical use

Earthquake research

Medicine

Text analysis

Telecommunications

Stocks market

Practical use

Earthquake research

Medicine

Text analysis

Telecommunications

Stocks market

Why is it important to take in account the non stationary

Why is it important to take in account the non stationary

The classical theorems on convergence

Т1. (Glivenko) Selective disribution of a

The classical theorems on convergence

Т1. (Glivenko) Selective disribution of a

Methods of the nonstationary time series analysis

Ordinary least squares.

Time series cointegriation,

Methods of the nonstationary time series analysis

Ordinary least squares.

Time series cointegriation,

Nonparametric comparison of samples

Let the random variables have a continuous

Let the random variables have a continuous

Distribution function as random value

If random value has distribution function F(x),

Distribution function as random value

If random value has distribution function F(x),

Agreed level of significance (ALS)

At what distance should we unhook

Agreed level of significance (ALS)

At what distance should we unhook

The agreed level of significance (stationarity) in the norm of

The agreed level of significance (stationarity) in the norm of

On the left: a series of distances between two samples

On the left: a series of distances between two samples

The ALS in the norm of C for stationary disributions

The ALS in the norm of C for stationary disributions

If J> 1, the series is nonstationary; if J <=

If J> 1, the series is nonstationary; if J <=

The Fokker-Planck equation for a SDFD

The sample mean and variance

The sample mean and variance

From the solution of the F-P equation , we know

From the solution of the F-P equation , we know

Criteria for the correct generation of the ensemble

Let we generated

Criteria for the correct generation of the ensemble

Let we generated

Practical examples

Example 1 - earthquake statistics

In problems of earthquake prediction the

Practical examples

Example 1 - earthquake statistics

In problems of earthquake prediction the

Series ALS depending on the sample length

Nonstationary index depending on the sample length

Gutenberg-Richter law for two samples

This comparison shows that the

Gutenberg-Richter law for two samples

This comparison shows that the

Dynamics of the slope angle in the Gutenberg-Richter law

The

Dynamics of the slope angle in the Gutenberg-Richter law

The

Autocorrelation analysis of the slope angle

Dependence of the

Autocorrelation analysis of the slope angle

Dependence of the

The values of the steady-state coefficients of autocorrelation depending on

The values of the steady-state coefficients of autocorrelation depending on

The model of the time series b(n)

The dynamics of

The model of the time series b(n)

The dynamics of

Nonstationary distributions of magnitudes

it was found that the nonstationarity of

it was found that the nonstationarity of

Earthquake statistics

results

We analyzed the stationary level of JMA catalog of

results

We analyzed the stationary level of JMA catalog of

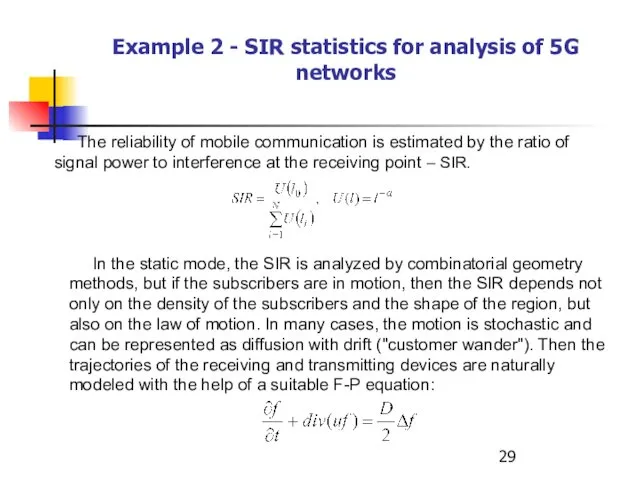

Example 2 - SIR statistics for analysis of 5G networks

Example 2 - SIR statistics for analysis of 5G networks

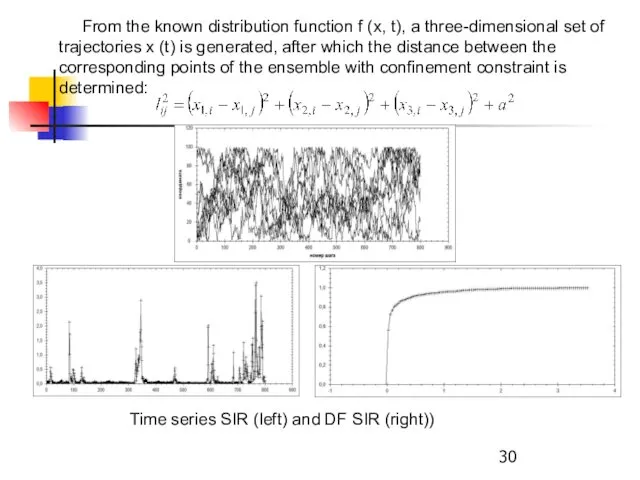

From the known distribution function f (x, t), a three-dimensional

From the known distribution function f (x, t), a three-dimensional

Example 3 - development of a trading system

There is a

There is a

Problems types

Selection of system parameters by historical data

Risk-management of a

Problems types

Selection of system parameters by historical data

Risk-management of a

Selection of system parameters by historical data

A small amount

Selection of system parameters by historical data

A small amount

Two types of trajectiories beam generation

Generation by historical change of

Two types of trajectiories beam generation

Generation by historical change of

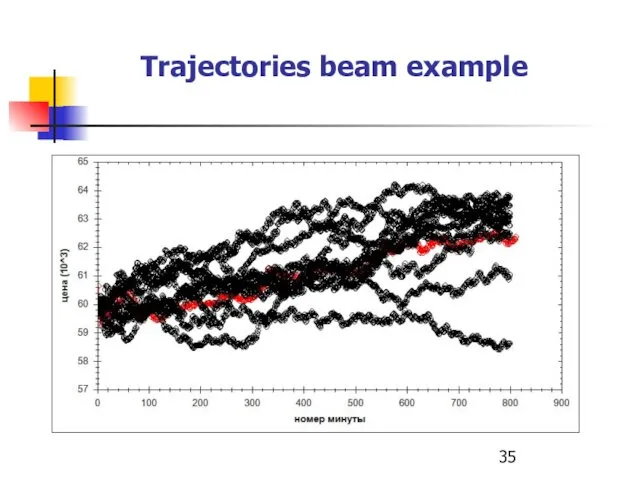

Trajectories beam example

Trajectories beam example

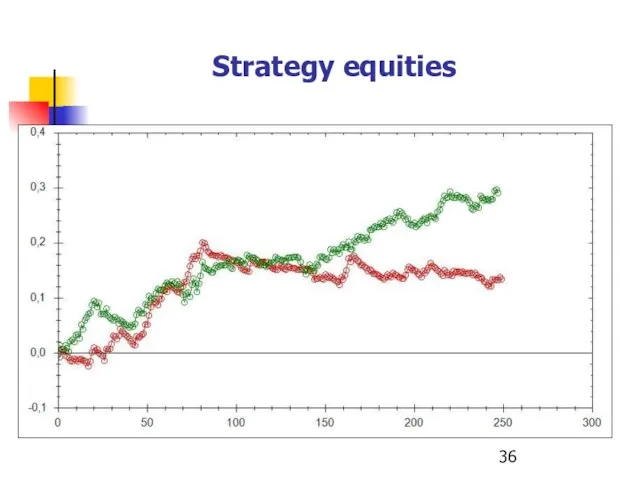

Strategy equities

Strategy equities

Conclusion

Modeling of nonstationary time series has a wide practical application.

Conclusion

Modeling of nonstationary time series has a wide practical application.

Інформаційно-комунікаційні технології професійної діяльності педагога

Інформаційно-комунікаційні технології професійної діяльності педагога Информационные технологии управления

Информационные технологии управления Введение в специальность. Развитие информационного общества: перспективные направления исследования

Введение в специальность. Развитие информационного общества: перспективные направления исследования Системы счисления

Системы счисления The method of software upgrade for tablet PC B902

The method of software upgrade for tablet PC B902 WEB GRAPHS/ Modeling the Internet and the Web School of Information and Computer Science

WEB GRAPHS/ Modeling the Internet and the Web School of Information and Computer Science ГОСТ Р 7.0.100-2018 Одноуровневое библиографическое описание

ГОСТ Р 7.0.100-2018 Одноуровневое библиографическое описание Современный образовательный портал MegaCampus

Современный образовательный портал MegaCampus Цикл с параметром (цикл с заданным числом повторений, цикл-ДЛЯ)

Цикл с параметром (цикл с заданным числом повторений, цикл-ДЛЯ) Створення, відкривання і збереження текстового документа

Створення, відкривання і збереження текстового документа Анализ систем управления

Анализ систем управления Что делать с неповоротливым JQuery

Что делать с неповоротливым JQuery Презентация Понятие алгоритма. Исполнители алгоритма. Свойства алгоритма.

Презентация Понятие алгоритма. Исполнители алгоритма. Свойства алгоритма. Обработка текстовой и изобразительной информации

Обработка текстовой и изобразительной информации SQL. Манипулирование данными

SQL. Манипулирование данными Introduction to algorithms and data structures & recursion. Lecture 1. Part I

Introduction to algorithms and data structures & recursion. Lecture 1. Part I Шрифтовый дизайн

Шрифтовый дизайн Программа MS Access

Программа MS Access Управление промышленными мехатронными системами

Управление промышленными мехатронными системами ВКР: Разработка игрового приложения жанра “Shooter” в среде разработки Unity

ВКР: Разработка игрового приложения жанра “Shooter” в среде разработки Unity Отечественный опыт развития электронной торговли

Отечественный опыт развития электронной торговли Системы счисления. ОГЭ

Системы счисления. ОГЭ Условные операторы

Условные операторы Кодирование и обработка звуковой информации

Кодирование и обработка звуковой информации Что такое массив? Алгоритмизация и программирование, язык Python. 10 класс

Что такое массив? Алгоритмизация и программирование, язык Python. 10 класс Измерение информации. 10 класс

Измерение информации. 10 класс Установочная лекция по дисциплине Информатика

Установочная лекция по дисциплине Информатика Все пути дерева (3 кл)

Все пути дерева (3 кл)