- Top 10 Audit & Program Review Findings

Содержание

- 2. Top Audit Findings Repeat finding – failure to take corrective action R2T4 funds made late Return

- 3. Top Audit Findings (cont’d) Qualified auditor’s opinion cited in audit Pell overpayment/underpayment Entrance/Exit counseling deficiencies Student

- 4. Top Program Review Findings Verification violations Student credit balance deficiencies Return to Title IV (R2T4) Calculation

- 5. Top Program Review Findings (cont’d) Inaccurate recordkeeping Pell Grant overpayments/underpayments Account records inadequate/not reconciled R2T4 funds

- 6. Findings on Both Top Ten Lists R2T4 calculation errors R2T4 funds made late Pell Grant overpayment/underpayment

- 7. Audit Findings

- 8. Repeat Finding – Failure To Take Corrective Action Failure to implement Corrective Action Plan (CAP) CAP

- 9. Repeat Finding- Failure to Take Corrective Action Example: Repeat findings for Untimely Return of Funds Solution:

- 10. Additional Compliance Solutions Review results of Corrective Action Plan (CAP) - Is it working? - Are

- 11. Return of Title IV Funds Made Late School’s policy and procedures not followed Returns not made

- 12. Return To Title IV Funds Made Late Example: Returns not made within the required timeframe (45

- 13. Additional Compliance Solutions Audit Findings Periodically review processes and procedures to ensure compliance - Tracking/monitoring deadlines

- 14. R2T4 Calculation Errors Incorrect number of days Ineligible funds used as aid that ‘could have been

- 15. R2T4 Calculation Errors Example: Incorrect calculation due to using the wrong number of days for the

- 16. Additional Compliance Solutions Pay attention to new regulations; revise procedures as needed Perform self-assessment by reviewing

- 17. Student Status – Inaccurate/Untimely Reporting Failure to provide notification of last date of attendance/changes in student

- 18. Student Status- Inaccurate/Untimely Reporting Example: Failure to report change in student enrollment status when student is

- 19. Additional Compliance Solutions Maintain accurate enrollment records Automate enrollment reporting - Batch uploads or individual online

- 20. Verification Violations Verification worksheet missing/incomplete Income tax transcripts missing Conflicting data not resolved Untaxed income not

- 21. Verification Violations Example: Conflicting information reported on the verification worksheet and on the Institutional Student Information

- 22. Additional Compliance Solutions Develop appropriate verification procedures to ensure timely submission of all required documents Monitor

- 23. Auditor’s Opinion Cited in Audit (Qualified or Adverse) Anything other than an unqualified opinion Serious deficiencies/areas

- 24. Auditor’s Opinion Cited in Audit (Qualified or Adverse) Example: School did not reconcile Title IV program

- 25. Additional Compliance Solutions Assessment of entire financial aid/fiscal process - Design an institution-wide plan of action

- 26. Pell Grant Overpayment/Underpayment Incorrect Pell Grant formula Inaccurate calculations - Proration - Incorrect EFC - Adjustments

- 27. Pell Grant Overpayment/Underpayment Example: Student changed enrollment status between terms, from full-time to half-time, resulting in

- 28. Additional Compliance Solutions Prorate when needed Use correct enrollment status Use correct Pell Grant formula/schedule Assign

- 29. Entrance/Exit Counseling Deficiencies Entrance counseling not conducted/ documented for first-time borrowers Exit counseling not conducted/documented for

- 30. Entrance/Exit Counseling Deficiencies Example: Exit counseling not completed for unofficial or mid-year withdrawals Solution: Develop and

- 31. Additional Compliance Solutions Assign responsibility for monitoring the entrance/exit interview process Develop and implement procedures to

- 32. Student Credit Balance Deficiencies Credit balance not released to student within 14 days No process in

- 33. Student Credit Balance Deficiencies Example: Credit balances were not paid timely; credit balance authorization incorrect or

- 34. Additional Compliance Solutions Establish internal controls to track dates associated with credit balances payment Conduct a

- 35. Student Confirmation Report Filed Late/Inaccurate Roster file (formerly called Student Status Confirmation Report [SSCR]) not submitted

- 36. Student Confirmation Report Filed Late/Inaccurate Example: Failure to submit Roster File timely; no policies and procedures

- 37. Additional Compliance Solutions Review, update, and verify student enrollment statuses, effective dates of enrollment, and completion

- 38. Program Review Findings

- 39. Program Review Findings Verification violations Student credit balance deficiencies Return to Title IV (R2T4) Calculation Errors

- 40. Program Review Findings Inaccurate recordkeeping Pell Grant overpayments/underpayments Account records inadequate/not reconciled R2T4 funds made late

- 41. Crime Awareness Requirements Not Met Campus security policies and procedures not adequately developed Annual report not

- 42. Crime Awareness Requirements Not Met Example: Failure to include all reportable offenses in crime statistics report

- 43. Additional Compliance Solutions Post a link for security reports to school’s webpage Review The Handbook for

- 44. SAP Policy Not Adequately Developed/Monitored Disbursement of aid to students not meeting the SAP standards Failure

- 45. SAP Policy Not Adequately Developed/Monitored Example: Failure to disclose the quantitative measure required to maintain Title

- 46. Additional Compliance Solutions FSA Assessments: Students - Satisfactory Academic Progress (SAP) Module FSA Handbook, Volume 1,

- 47. Account Records Inadequate/Not Reconciled Failure to use an accounting system that adequately tracks all transactions involving

- 48. Account Records Inadequate/Not Reconciled Example: Student ledger reflected a Federal Pell Grant in the amount of

- 49. Additional Compliance Solutions Perform routine reconciliation of all program accounts with COD and G5 Establish internal

- 50. Inaccurate Recordkeeping Inadequate or mismatched attendance records for schools that are required to take attendance Failure

- 51. Inaccurate Recordkeeping Example: School failed to properly record attendance, allowed students to clock in and out

- 52. Additional Compliance Solutions Communicate the importance of accuracy of all FSA records with all staff members

- 53. Lack of Administrative Capability Significant findings that indicate a failure to administer aid programs in accordance

- 54. Lack of Administrative Capability Example: General ledgers not reconciled with Common Origination Disbursement (COD) report and/or

- 55. Additional Compliance Solutions Training - Fundamentals of Title IV Administration - FSA Coach - Attend FSA

- 56. Information in Student Files Missing/Inconsistent No system in place to coordinate information collected in different offices

- 57. Information In Student Files Missing/Inconsistent Example: Institutional aid application and ISIR showed student as married, tax

- 58. Additional Compliance Solutions Establish communication with other offices to identify and address inconsistent information Perform periodic

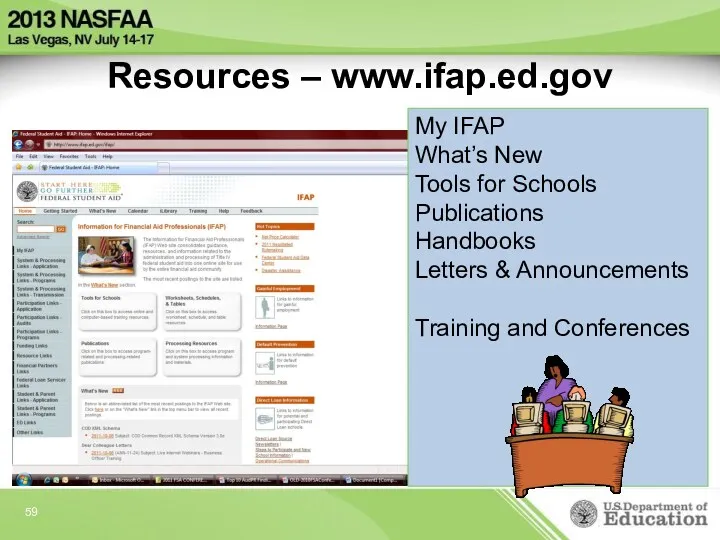

- 59. Resources – www.ifap.ed.gov My IFAP What’s New Tools for Schools Publications Handbooks Letters & Announcements Training

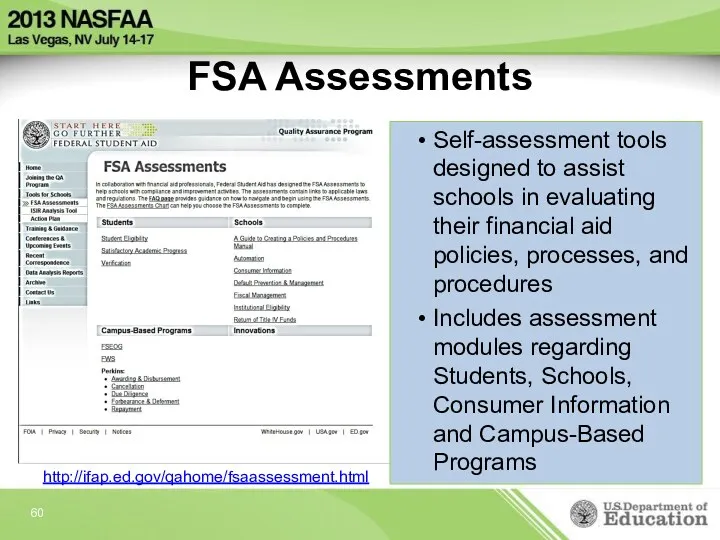

- 60. FSA Assessments Self-assessment tools designed to assist schools in evaluating their financial aid policies, processes, and

- 61. QUESTIONS?

- 62. Contact Information We appreciate your feedback and comments. I can be reached at: Renée Gullotto Institutional

- 64. Скачать презентацию

Top Audit Findings

Repeat finding – failure to take corrective action

R2T4 funds

Top Audit Findings

Repeat finding – failure to take corrective action

R2T4 funds

Top Audit Findings (cont’d)

Qualified auditor’s opinion cited in audit

Pell overpayment/underpayment

Entrance/Exit counseling

Top Audit Findings (cont’d)

Qualified auditor’s opinion cited in audit

Pell overpayment/underpayment

Entrance/Exit counseling

Top Program Review Findings

Verification violations

Student credit balance deficiencies

Return to Title IV

Top Program Review Findings

Verification violations

Student credit balance deficiencies

Return to Title IV

Top Program Review Findings (cont’d)

Inaccurate recordkeeping

Pell Grant overpayments/underpayments

Account records

Top Program Review Findings (cont’d)

Inaccurate recordkeeping

Pell Grant overpayments/underpayments

Account records

Findings on Both Top Ten Lists

R2T4 calculation errors

R2T4 funds made late

Pell

Findings on Both Top Ten Lists

R2T4 calculation errors

R2T4 funds made late

Pell

Audit Findings

Audit Findings

Repeat Finding –

Failure To Take Corrective Action

Failure to implement Corrective Action

Repeat Finding –

Failure To Take Corrective Action

Failure to implement Corrective Action

Repeat Finding-

Failure to Take Corrective Action

Example: Repeat findings for Untimely

Repeat Finding-

Failure to Take Corrective Action

Example: Repeat findings for Untimely

Additional Compliance Solutions

Review results of Corrective Action Plan (CAP)

- Is it

Additional Compliance Solutions

Review results of Corrective Action Plan (CAP)

- Is it

Return of Title IV Funds Made Late

School’s policy and procedures not

Return of Title IV Funds Made Late

School’s policy and procedures not

Return To Title IV Funds Made Late

Example: Returns not made within

Return To Title IV Funds Made Late

Example: Returns not made within

Additional Compliance Solutions

Audit Findings

Periodically review processes and procedures to ensure

Additional Compliance Solutions

Audit Findings

Periodically review processes and procedures to ensure

R2T4 Calculation Errors

Incorrect number of days

Ineligible funds used as aid that

R2T4 Calculation Errors

Incorrect number of days

Ineligible funds used as aid that

R2T4 Calculation Errors

Example: Incorrect calculation due to using the wrong number

R2T4 Calculation Errors

Example: Incorrect calculation due to using the wrong number

Additional Compliance Solutions

Pay attention to new regulations; revise procedures as needed

Perform

Additional Compliance Solutions

Pay attention to new regulations; revise procedures as needed

Perform

Student Status –

Inaccurate/Untimely Reporting

Failure to provide notification of last date of

Student Status –

Inaccurate/Untimely Reporting

Failure to provide notification of last date of

Student Status-

Inaccurate/Untimely Reporting

Example: Failure to report change in student enrollment

Student Status-

Inaccurate/Untimely Reporting

Example: Failure to report change in student enrollment

Additional Compliance Solutions

Maintain accurate enrollment records

Automate enrollment reporting

- Batch uploads or

Additional Compliance Solutions

Maintain accurate enrollment records

Automate enrollment reporting

- Batch uploads or

Verification Violations

Verification worksheet missing/incomplete

Income tax transcripts missing

Conflicting data not resolved

Untaxed

Verification Violations

Verification worksheet missing/incomplete

Income tax transcripts missing

Conflicting data not resolved

Untaxed

Verification Violations

Example: Conflicting information reported on the verification worksheet and on

Verification Violations

Example: Conflicting information reported on the verification worksheet and on

Additional Compliance Solutions

Develop appropriate verification procedures to ensure timely submission of

Additional Compliance Solutions

Develop appropriate verification procedures to ensure timely submission of

Auditor’s Opinion Cited in Audit

(Qualified or Adverse)

Anything other than an unqualified

Auditor’s Opinion Cited in Audit

(Qualified or Adverse)

Anything other than an unqualified

Auditor’s Opinion Cited in Audit

(Qualified or Adverse)

Example: School did not reconcile

Auditor’s Opinion Cited in Audit

(Qualified or Adverse)

Example: School did not reconcile

Additional Compliance Solutions

Assessment of entire financial aid/fiscal process

- Design an institution-wide

Additional Compliance Solutions

Assessment of entire financial aid/fiscal process

- Design an institution-wide

Pell Grant

Overpayment/Underpayment

Incorrect Pell Grant formula

Inaccurate calculations

- Proration

- Incorrect

Pell Grant

Overpayment/Underpayment

Incorrect Pell Grant formula

Inaccurate calculations

- Proration

- Incorrect

Pell Grant

Overpayment/Underpayment

Example: Student changed enrollment status between terms, from full-time to

Pell Grant

Overpayment/Underpayment

Example: Student changed enrollment status between terms, from full-time to

Additional Compliance Solutions

Prorate when needed

Use correct enrollment status

Use correct Pell Grant

Additional Compliance Solutions

Prorate when needed

Use correct enrollment status

Use correct Pell Grant

Entrance/Exit Counseling

Deficiencies

Entrance counseling not conducted/

documented for first-time borrowers

Exit

Entrance/Exit Counseling

Deficiencies

Entrance counseling not conducted/

documented for first-time borrowers

Exit

Entrance/Exit Counseling Deficiencies

Example: Exit counseling not completed for unofficial or

Entrance/Exit Counseling Deficiencies

Example: Exit counseling not completed for unofficial or

Additional Compliance Solutions

Assign responsibility for monitoring the entrance/exit interview process

Develop and

Additional Compliance Solutions

Assign responsibility for monitoring the entrance/exit interview process

Develop and

Student Credit Balance

Deficiencies

Credit balance not released to student within 14

Student Credit Balance

Deficiencies

Credit balance not released to student within 14

Student Credit Balance Deficiencies

Example: Credit balances were not paid timely; credit

Student Credit Balance Deficiencies

Example: Credit balances were not paid timely; credit

Additional Compliance Solutions

Establish internal controls to track dates associated with credit

Additional Compliance Solutions

Establish internal controls to track dates associated with credit

Student Confirmation Report Filed Late/Inaccurate

Roster file (formerly called Student Status Confirmation

Student Confirmation Report Filed Late/Inaccurate

Roster file (formerly called Student Status Confirmation

Student Confirmation Report Filed Late/Inaccurate

Example: Failure to submit Roster File timely;

Student Confirmation Report Filed Late/Inaccurate

Example: Failure to submit Roster File timely;

Additional Compliance Solutions

Review, update, and verify student enrollment statuses, effective dates

Additional Compliance Solutions

Review, update, and verify student enrollment statuses, effective dates

Program Review Findings

Program Review Findings

Program Review Findings

Verification violations

Student credit balance deficiencies

Return to Title IV (R2T4)

Program Review Findings

Verification violations

Student credit balance deficiencies

Return to Title IV (R2T4)

Program Review Findings

Inaccurate recordkeeping

Pell Grant overpayments/underpayments

Account records inadequate/not reconciled

R2T4 funds

Program Review Findings

Inaccurate recordkeeping

Pell Grant overpayments/underpayments

Account records inadequate/not reconciled

R2T4 funds

Crime Awareness Requirements Not Met

Campus security policies and procedures not adequately

Crime Awareness Requirements Not Met

Campus security policies and procedures not adequately

Crime Awareness Requirements Not Met

Example: Failure to include all reportable offenses

Crime Awareness Requirements Not Met

Example: Failure to include all reportable offenses

Additional Compliance Solutions

Post a link for security reports to school’s webpage

Additional Compliance Solutions

Post a link for security reports to school’s webpage

SAP Policy

Not Adequately Developed/Monitored

Disbursement of aid to students not meeting the

SAP Policy

Not Adequately Developed/Monitored

Disbursement of aid to students not meeting the

SAP Policy

Not Adequately Developed/Monitored

Example: Failure to disclose the quantitative measure required

SAP Policy

Not Adequately Developed/Monitored

Example: Failure to disclose the quantitative measure required

Additional Compliance Solutions

FSA Assessments: Students - Satisfactory Academic Progress (SAP) Module

FSA

Additional Compliance Solutions

FSA Assessments: Students - Satisfactory Academic Progress (SAP) Module

FSA

Account Records

Inadequate/Not Reconciled

Failure to use an accounting system that adequately tracks

Account Records

Inadequate/Not Reconciled

Failure to use an accounting system that adequately tracks

Account Records

Inadequate/Not Reconciled

Example: Student ledger reflected a Federal Pell Grant in

Account Records

Inadequate/Not Reconciled

Example: Student ledger reflected a Federal Pell Grant in

Additional Compliance Solutions

Perform routine reconciliation of all program accounts with COD

Additional Compliance Solutions

Perform routine reconciliation of all program accounts with COD

Inaccurate Recordkeeping

Inadequate or mismatched attendance records for schools that are required

Inaccurate Recordkeeping

Inadequate or mismatched attendance records for schools that are required

Inaccurate Recordkeeping

Example: School failed to properly record attendance, allowed students to

Inaccurate Recordkeeping

Example: School failed to properly record attendance, allowed students to

Additional Compliance Solutions

Communicate the importance of accuracy of all FSA records

Additional Compliance Solutions

Communicate the importance of accuracy of all FSA records

Lack of Administrative Capability

Significant findings that indicate a failure to administer

Lack of Administrative Capability

Significant findings that indicate a failure to administer

Lack of Administrative Capability

Example: General ledgers not reconciled with Common Origination

Lack of Administrative Capability

Example: General ledgers not reconciled with Common Origination

Additional Compliance Solutions

Training

- Fundamentals of Title IV Administration

- FSA Coach

- Attend

Additional Compliance Solutions

Training

- Fundamentals of Title IV Administration

- FSA Coach

- Attend

Information in Student Files

Missing/Inconsistent

No system in place to coordinate information

Information in Student Files

Missing/Inconsistent

No system in place to coordinate information

Information In Student Files

Missing/Inconsistent

Example: Institutional aid application and ISIR showed student

Information In Student Files

Missing/Inconsistent

Example: Institutional aid application and ISIR showed student

Additional Compliance Solutions

Establish communication with other offices to identify and address

Additional Compliance Solutions

Establish communication with other offices to identify and address

Resources – www.ifap.ed.gov

My IFAP

What’s New

Tools for Schools

Publications

Handbooks

Letters & Announcements

Training and Conferences

Resources – www.ifap.ed.gov

My IFAP

What’s New

Tools for Schools

Publications

Handbooks

Letters & Announcements

Training and Conferences

FSA Assessments

Self-assessment tools designed to assist schools in evaluating their financial

FSA Assessments

Self-assessment tools designed to assist schools in evaluating their financial

QUESTIONS?

QUESTIONS?

Contact Information

We appreciate your feedback and comments. I can be reached

Contact Information

We appreciate your feedback and comments. I can be reached

Instructions for use. Open this document in Google Slides

Instructions for use. Open this document in Google Slides Способы кодировки информации

Способы кодировки информации Software Architecture and Software Architect T-Systems RUS. JavaSchool

Software Architecture and Software Architect T-Systems RUS. JavaSchool Концепция портала культуры Ярославской области

Концепция портала культуры Ярославской области Дослідження методів та засобів захисту інформації в корпоративних мережах

Дослідження методів та засобів захисту інформації в корпоративних мережах Мой Арбитр

Мой Арбитр Улучшения в функционале подключения и изменения настроек 1С-Отчетности

Улучшения в функционале подключения и изменения настроек 1С-Отчетности Методы сортировки

Методы сортировки Кодирование текстовой информации

Кодирование текстовой информации Facebook для інструкторів з груднічкового плавання

Facebook для інструкторів з груднічкового плавання Дерева. Основні поняття та властивості дерев

Дерева. Основні поняття та властивості дерев Учебный проект

Учебный проект Операционные системы 1

Операционные системы 1 Технологии создания и преобразования информационных объектов

Технологии создания и преобразования информационных объектов Программное обеспечение. Прикладные и системные программы

Программное обеспечение. Прикладные и системные программы ТЗ. Настроить работу фильтра

ТЗ. Настроить работу фильтра НБИКС - Сервис для организации корпоративного обучения

НБИКС - Сервис для организации корпоративного обучения Отчет по учебной практике ПМ08. Разработка дизайна веб-приложений

Отчет по учебной практике ПМ08. Разработка дизайна веб-приложений Процедурные расширения SQL. Хранимые процедуры и триггеры

Процедурные расширения SQL. Хранимые процедуры и триггеры Компьютерные справочно-правовые системы

Компьютерные справочно-правовые системы Программное обеспечение для финансовых организаций

Программное обеспечение для финансовых организаций Электронный дневник на сайте школы

Электронный дневник на сайте школы Классы. Свойства классов. Методы классов. Перегрузка методов. Лекция 39

Классы. Свойства классов. Методы классов. Перегрузка методов. Лекция 39 Пример построения ER-модели

Пример построения ER-модели Компетентностно-ориентированное задание.

Компетентностно-ориентированное задание. Рост эффективности, инвестиционной привлекательности и капитализации бизнеса при использовании ERP-решений фирмы 1С

Рост эффективности, инвестиционной привлекательности и капитализации бизнеса при использовании ERP-решений фирмы 1С Программирование циклических алгоритмов. Начала программирования

Программирование циклических алгоритмов. Начала программирования Основы технологии ASP.Net Web Forms. Обзор платформы Microsoft .Net

Основы технологии ASP.Net Web Forms. Обзор платформы Microsoft .Net