- Auctions. (Lecture 10)

Содержание

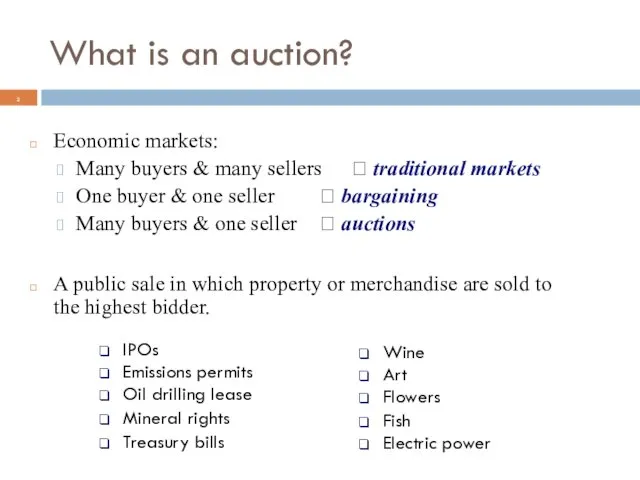

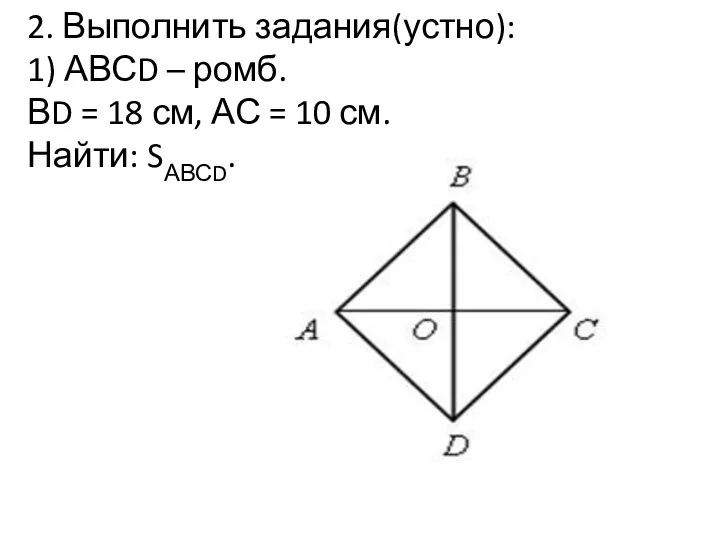

- 2. What is an auction? Economic markets: Many buyers & many sellers ? traditional markets One buyer

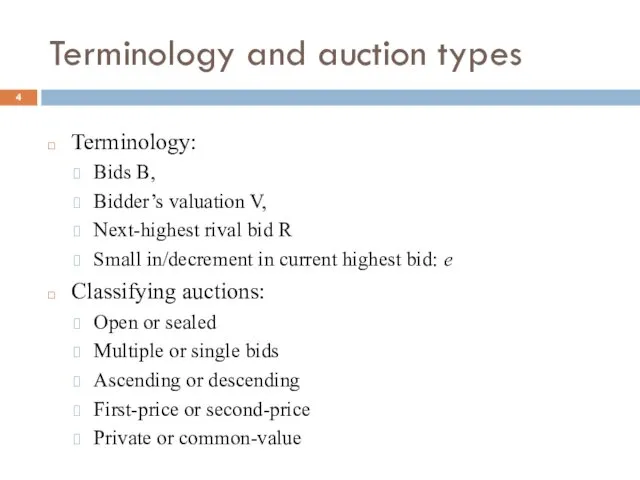

- 4. Terminology and auction types Terminology: Bids B, Bidder’s valuation V, Next-highest rival bid R Small in/decrement

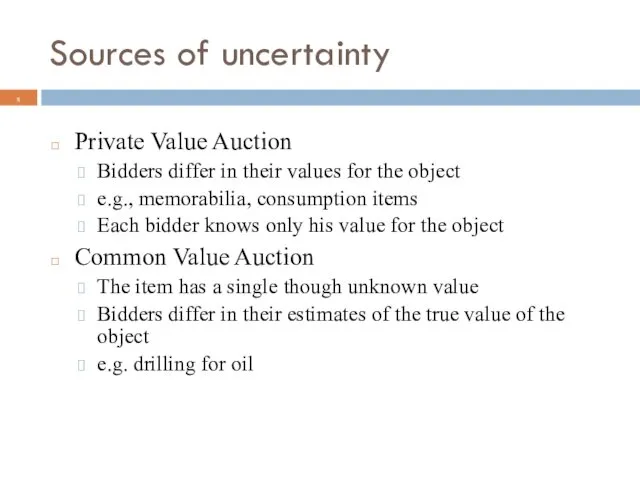

- 5. Sources of uncertainty Private Value Auction Bidders differ in their values for the object e.g., memorabilia,

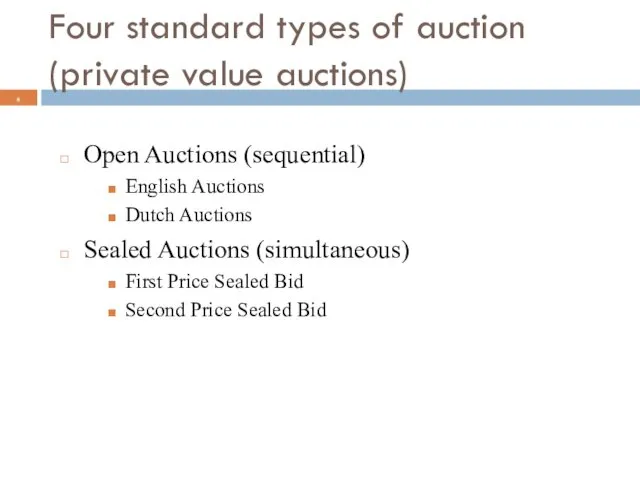

- 6. Four standard types of auction (private value auctions) Open Auctions (sequential) English Auctions Dutch Auctions Sealed

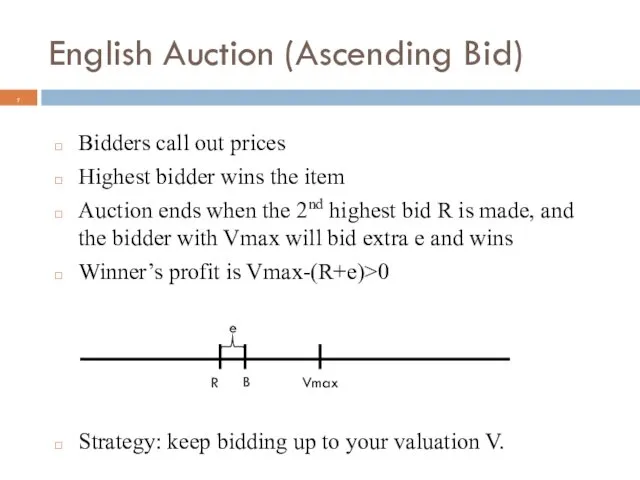

- 7. English Auction (Ascending Bid) Bidders call out prices Highest bidder wins the item Auction ends when

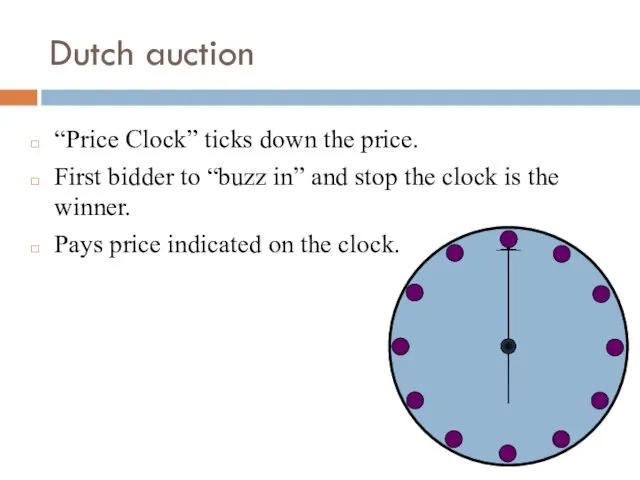

- 8. Dutch auction “Price Clock” ticks down the price. First bidder to “buzz in” and stop the

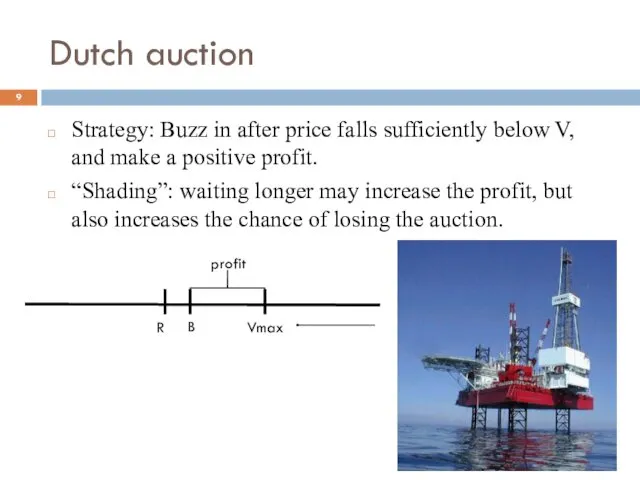

- 9. Dutch auction Strategy: Buzz in after price falls sufficiently below V, and make a positive profit.

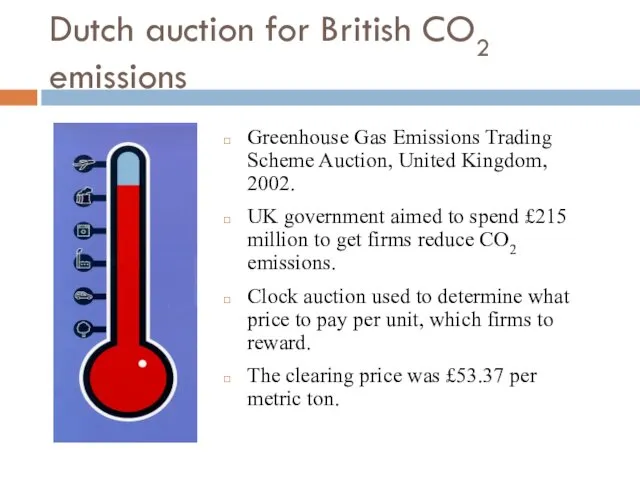

- 10. Dutch auction for British CO2 emissions Greenhouse Gas Emissions Trading Scheme Auction, United Kingdom, 2002. UK

- 11. First Price Auctions All buyers submit bids simultaneously. The bidder who submits the highest bid wins,

- 12. First Price Auctions Profit is Vmax - B Shading: B must be below V to generate

- 13. Second Price Auctions All bidders submit bids simultaneously. The bidder who submits the highest bid wins,

- 14. Second Price Auctions It is strategically equivalent to an English auction

- 15. Second Price Auctions Possible bids: B>V or B=V or B Bidding V is a dominant strategy

- 16. Second Price Auctions Bidding higher than my valuation B wins, pays R, profit is V-R, same

- 17. Second Price Auctions Bidding lower than my valuation B wins, pays R, profit is V-R, same

- 18. Second Price Auction In a second price auction, always bid your true valuation (Vickrey’s truth serum).

- 19. Which auction is better for the seller? In a second price auction Bidders bid their true

- 20. Revenue Equivalence All 4 standard auction formats yield the same expected revenue Any auctions in which:

- 21. Revenue Equivalence On average, Vmax-shading = 2nd highest V. The optimal shading strategy is such that

- 22. Are all auctions truly equivalent? For sellers, all 4 standard auctions are theoretically equivalent. However, this

- 23. Are all auctions truly equivalent? Inexperienced bidders In second-price auctions, it is optimal to bid V.

- 24. Collusion in auctions In second-price auctions, bidders may agree not to bid against a designated winner.

- 25. Collusion in auctions Collusion is also possible in English auctions. Bidders may be able to signal

- 26. Number of Bidders Having more bidders leads to higher prices. Example: Second price auction Two bidders

- 27. Number of Bidders Three bidders Each has a V of either 20 or 40 There are

- 28. Number of Bidders Assume more generally that valuations are drawn uniformly from [20,40]:

- 29. The European 3G telecom auctions The 2000-2001 European auctions of 3G mobile telecommunication licenses were some

- 30. The European 3G telecom auctions Netherlands 4 licences; 4 incumbents. Potential entrants could not realistically compete

- 31. Common Value Auctions Common Value Auction The item has a single though unknown value, and bidders

- 32. Hypothetical Oil Field Auction Each bidder knows the amount of oil in his or her quadrant

- 33. The winner’s curse The estimates are correct, on average $80 $70 $50 $40 $60 $60

- 34. The winner’s curse Winner’s curse = In common value auctions, winners are likely to overpay, and

- 35. Dealing with the winner’s curse Given that I win an auction …All others bid less than

- 36. Avoiding the winner’s curse Bidding with no regrets: Since winning means you have the most optimistic

- 37. All-pay auctions Common value first-price auction in which bidders pays the amount of their bid, even

- 38. All-pay auctions Example 3: Research and development, patent race. Competing pharmaceutical firms search for a new

- 39. All-pay auctions Optimal strategy If everyone else bids aggressively, your best response is to bid 0

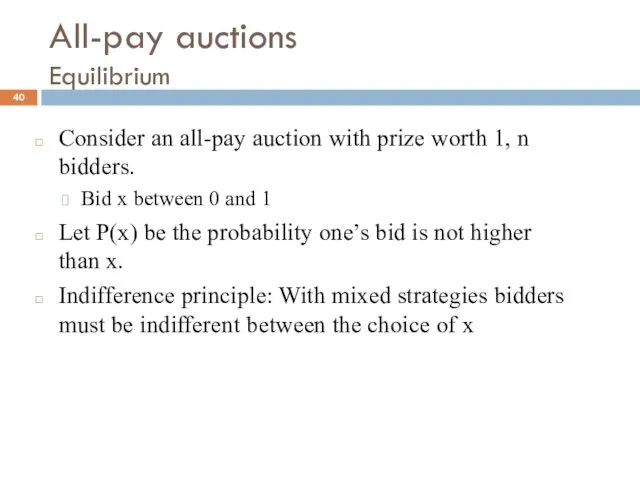

- 40. All-pay auctions Equilibrium Consider an all-pay auction with prize worth 1, n bidders. Bid x between

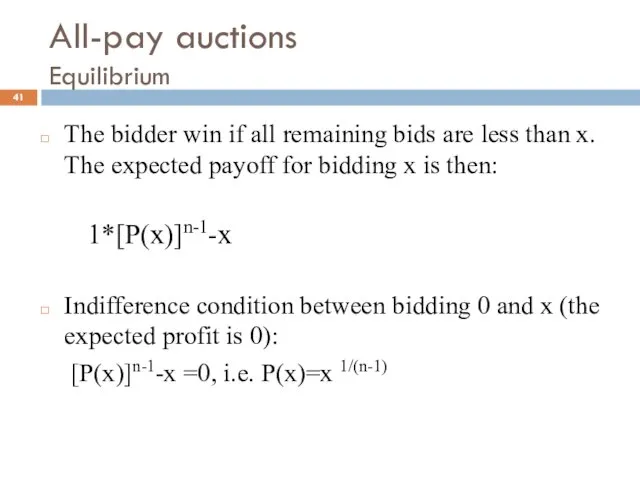

- 41. All-pay auctions Equilibrium The bidder win if all remaining bids are less than x. The expected

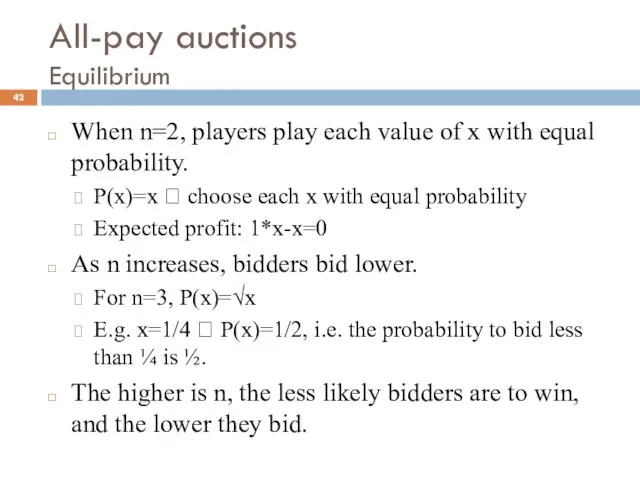

- 42. All-pay auctions Equilibrium When n=2, players play each value of x with equal probability. P(x)=x ?

- 43. All-pay auctions Overbidding Class experiments: Auction of a $20 bill Students start bidding $3, $4… When

- 45. Скачать презентацию

What is an auction?

Economic markets:

Many buyers & many sellers ? traditional markets

One

What is an auction?

Economic markets:

Many buyers & many sellers ? traditional markets

One

Terminology and auction types

Terminology:

Bids B,

Bidder’s valuation V,

Next-highest rival bid

Terminology and auction types

Terminology:

Bids B,

Bidder’s valuation V,

Next-highest rival bid

Sources of uncertainty

Private Value Auction

Bidders differ in their values for the

Sources of uncertainty

Private Value Auction

Bidders differ in their values for the

Four standard types of auction (private value auctions)

Open Auctions (sequential)

English Auctions

Dutch

Four standard types of auction (private value auctions)

Open Auctions (sequential)

English Auctions

Dutch

English Auction (Ascending Bid)

Bidders call out prices

Highest bidder wins the

English Auction (Ascending Bid)

Bidders call out prices

Highest bidder wins the

Dutch auction

“Price Clock” ticks down the price.

First bidder to “buzz in”

Dutch auction

“Price Clock” ticks down the price.

First bidder to “buzz in”

Dutch auction

Strategy: Buzz in after price falls sufficiently below V, and

Dutch auction

Strategy: Buzz in after price falls sufficiently below V, and

Dutch auction for British CO2 emissions

Greenhouse Gas Emissions Trading Scheme Auction,

Dutch auction for British CO2 emissions

Greenhouse Gas Emissions Trading Scheme Auction,

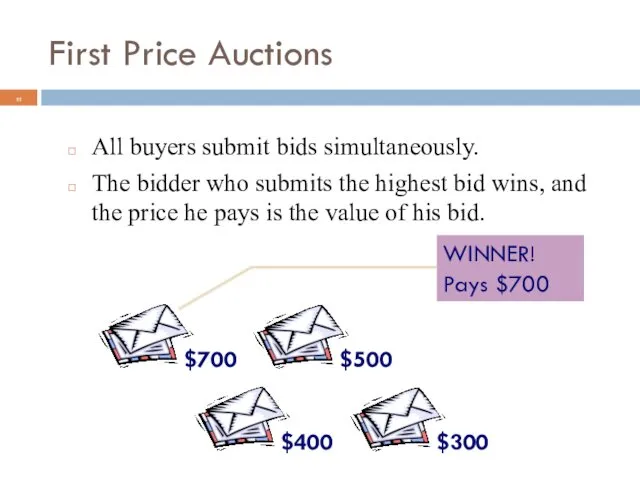

First Price Auctions

All buyers submit bids simultaneously.

The bidder who submits the

First Price Auctions

All buyers submit bids simultaneously.

The bidder who submits the

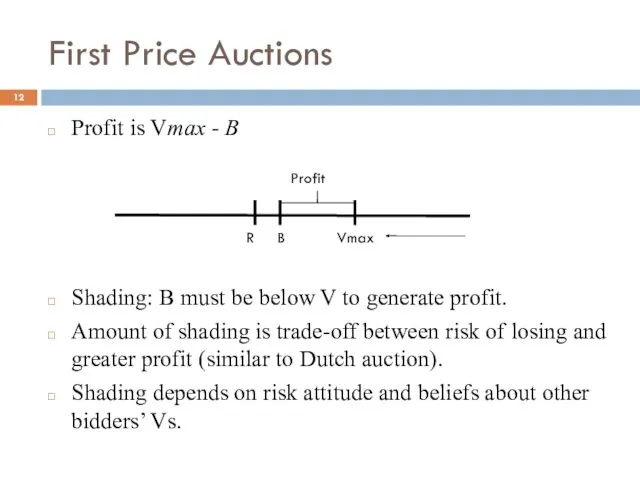

First Price Auctions

Profit is Vmax - B

Shading: B must be below

First Price Auctions

Profit is Vmax - B

Shading: B must be below

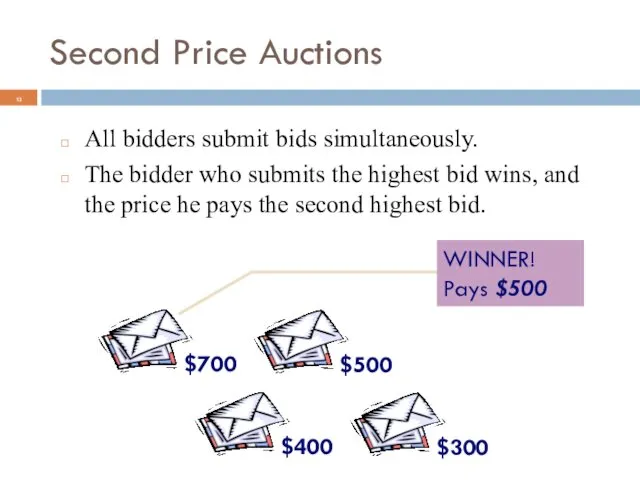

Second Price Auctions

All bidders submit bids simultaneously.

The bidder who submits the

Second Price Auctions

All bidders submit bids simultaneously.

The bidder who submits the

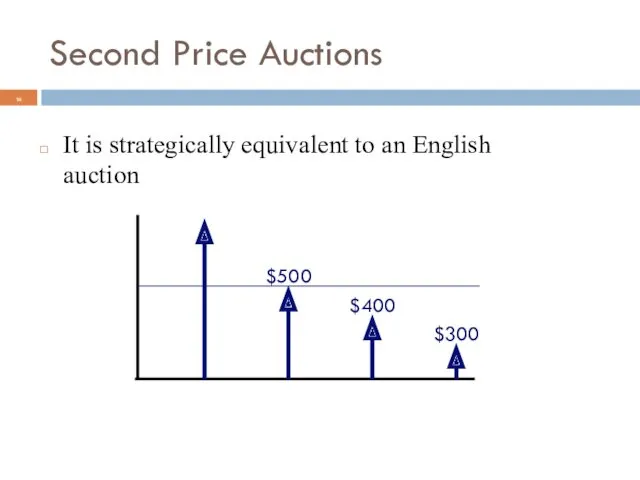

Second Price Auctions

It is strategically equivalent to an English auction

Second Price Auctions

It is strategically equivalent to an English auction

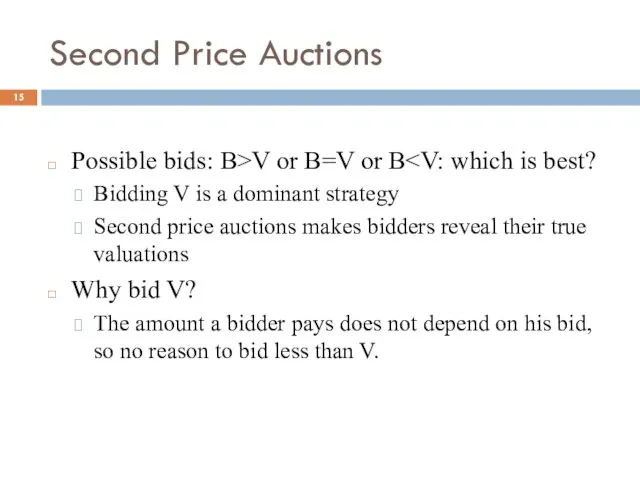

Second Price Auctions

Possible bids: B>V or B=V or B

Second Price Auctions

Possible bids: B>V or B=V or B

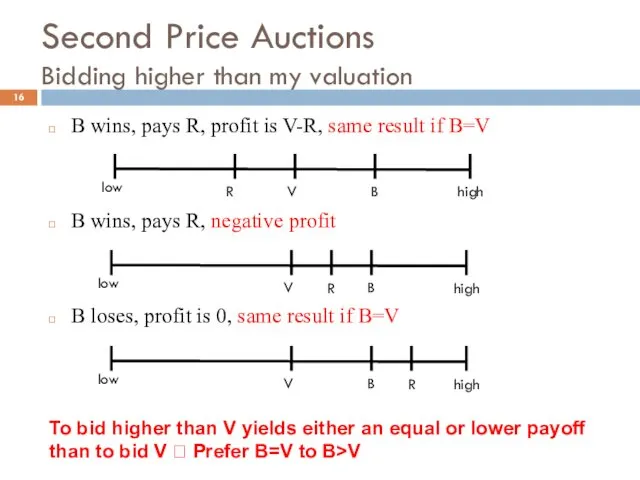

Second Price Auctions

Bidding higher than my valuation

B wins, pays R, profit

Second Price Auctions

Bidding higher than my valuation

B wins, pays R, profit

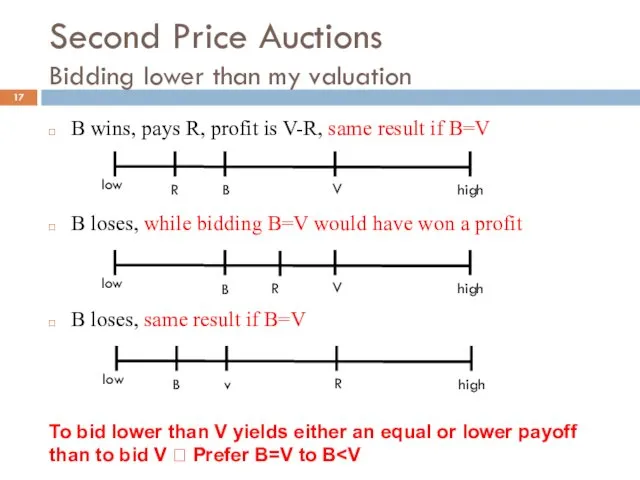

Second Price Auctions

Bidding lower than my valuation

B wins, pays R, profit

Second Price Auctions

Bidding lower than my valuation

B wins, pays R, profit

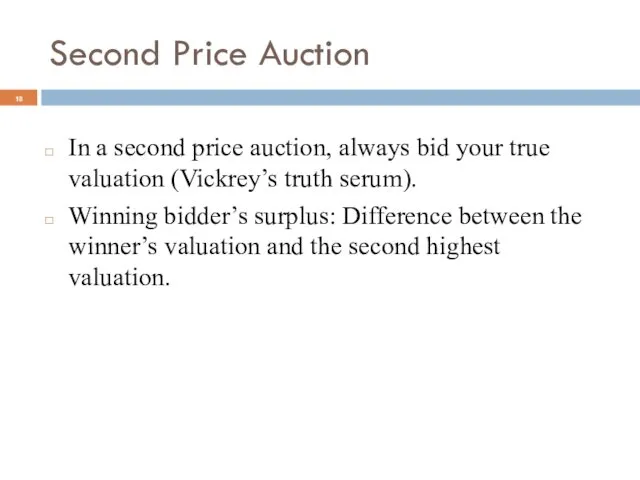

Second Price Auction

In a second price auction, always bid your true

Second Price Auction

In a second price auction, always bid your true

Which auction is better for the seller?

In a second price auction

Bidders

Which auction is better for the seller?

In a second price auction

Bidders

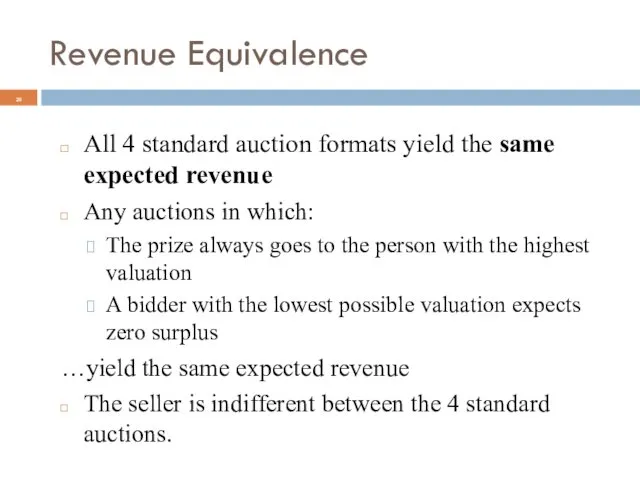

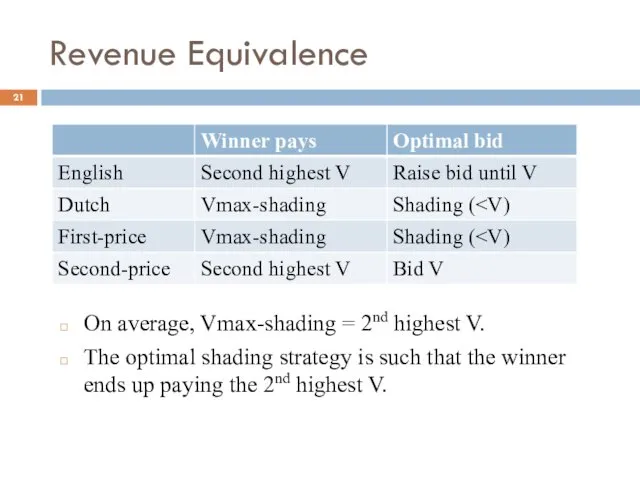

Revenue Equivalence

All 4 standard auction formats yield the same expected revenue

Any

Revenue Equivalence

All 4 standard auction formats yield the same expected revenue

Any

Revenue Equivalence

On average, Vmax-shading = 2nd highest V.

The optimal shading strategy

Revenue Equivalence

On average, Vmax-shading = 2nd highest V.

The optimal shading strategy

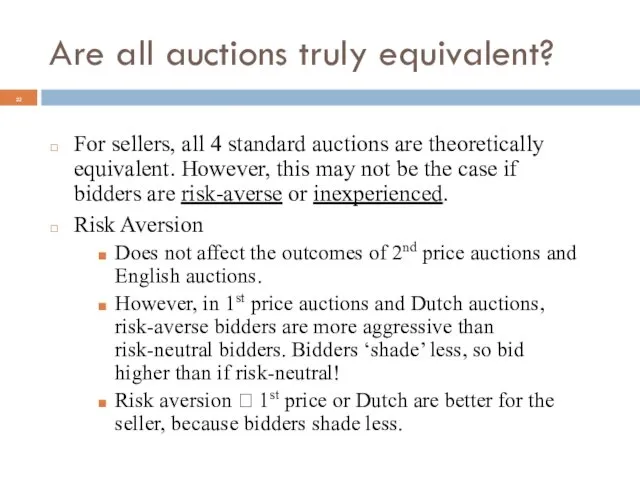

Are all auctions truly equivalent?

For sellers, all 4 standard auctions are

Are all auctions truly equivalent?

For sellers, all 4 standard auctions are

Are all auctions truly equivalent?

Inexperienced bidders

In second-price auctions, it is optimal

Are all auctions truly equivalent?

Inexperienced bidders

In second-price auctions, it is optimal

Collusion in auctions

In second-price auctions, bidders may agree not to bid

Collusion in auctions

In second-price auctions, bidders may agree not to bid

Collusion in auctions

Collusion is also possible in English auctions. Bidders may

Collusion in auctions

Collusion is also possible in English auctions. Bidders may

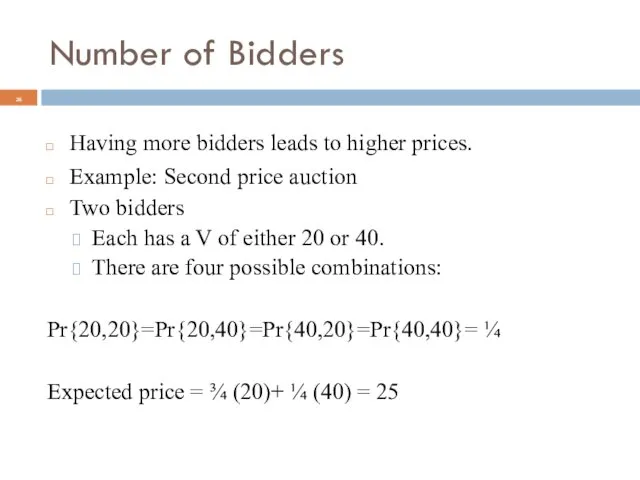

Number of Bidders

Having more bidders leads to higher prices.

Example: Second price

Number of Bidders

Having more bidders leads to higher prices.

Example: Second price

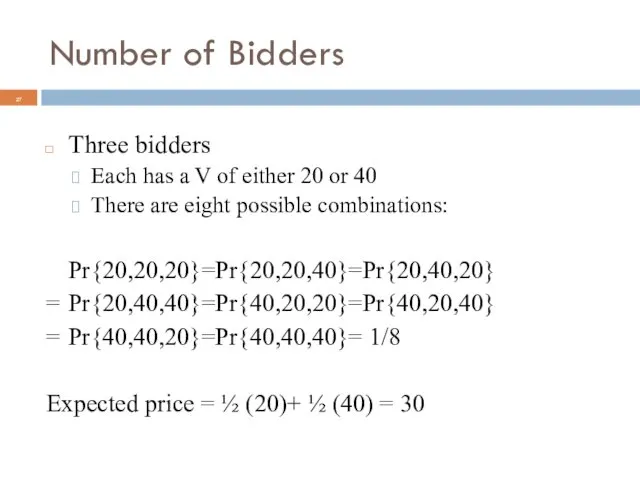

Number of Bidders

Three bidders

Each has a V of either 20 or

Number of Bidders

Three bidders

Each has a V of either 20 or

![Number of Bidders Assume more generally that valuations are drawn uniformly from [20,40]:](/_ipx/f_webp&q_80&fit_contain&s_1440x1080/imagesDir/jpg/15706/slide-27.jpg)

Number of Bidders

Assume more generally that valuations are drawn uniformly from

Number of Bidders

Assume more generally that valuations are drawn uniformly from

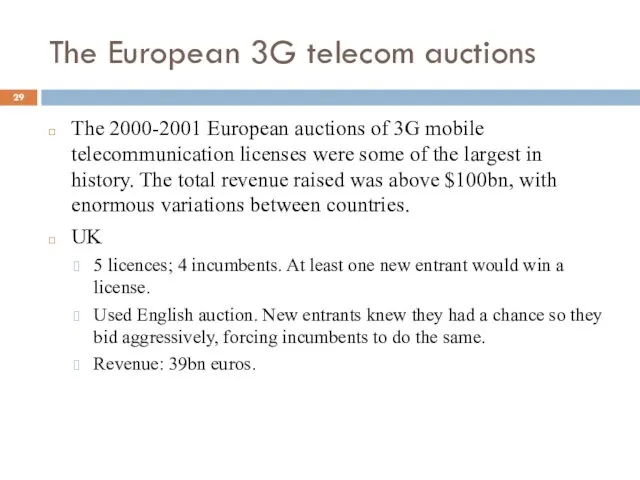

The European 3G telecom auctions

The 2000-2001 European auctions of 3G mobile

The European 3G telecom auctions

The 2000-2001 European auctions of 3G mobile

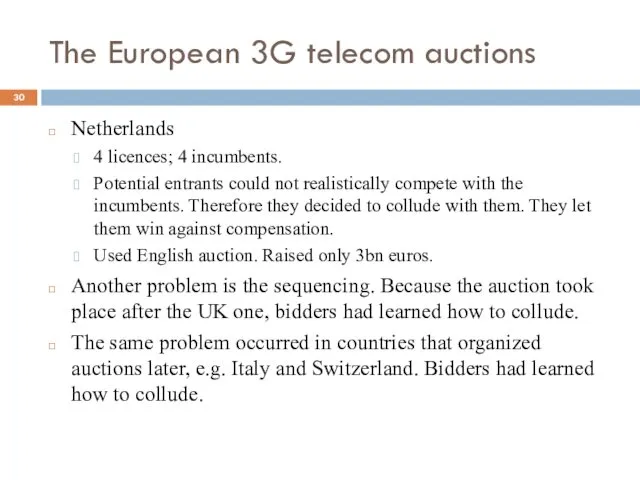

The European 3G telecom auctions

Netherlands

4 licences; 4 incumbents.

Potential entrants could

The European 3G telecom auctions

Netherlands

4 licences; 4 incumbents.

Potential entrants could

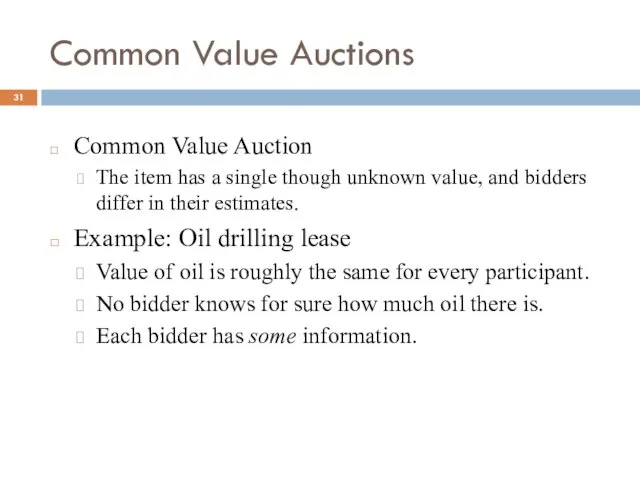

Common Value Auctions

Common Value Auction

The item has a single though unknown

Common Value Auctions

Common Value Auction

The item has a single though unknown

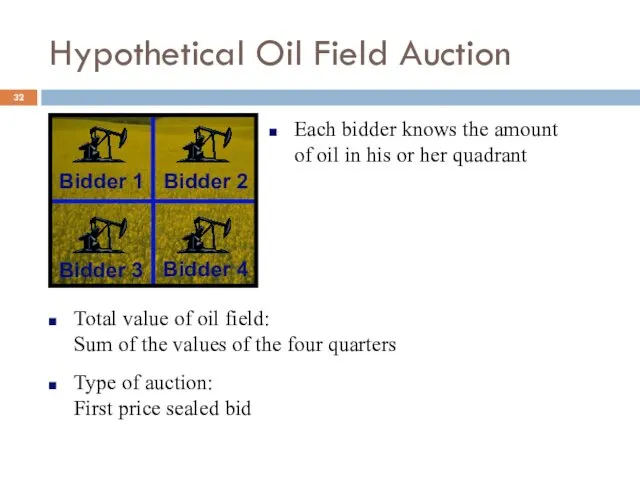

Hypothetical Oil Field Auction

Each bidder knows the amount of oil in

Hypothetical Oil Field Auction

Each bidder knows the amount of oil in

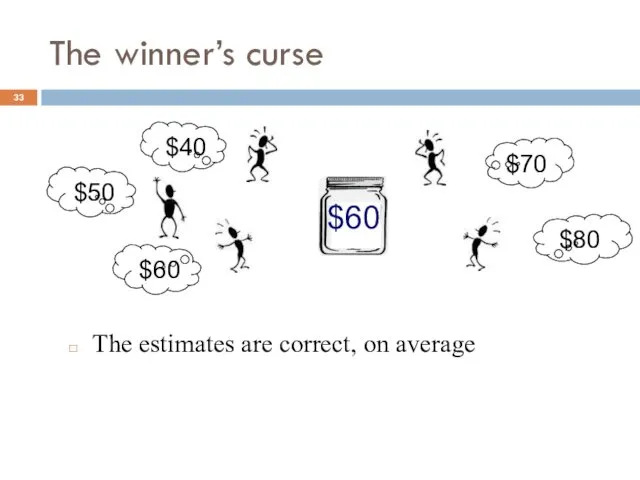

The winner’s curse

The estimates are correct, on average

$80

$70

$50

$40

$60

$60

The winner’s curse

The estimates are correct, on average

$80

$70

$50

$40

$60

$60

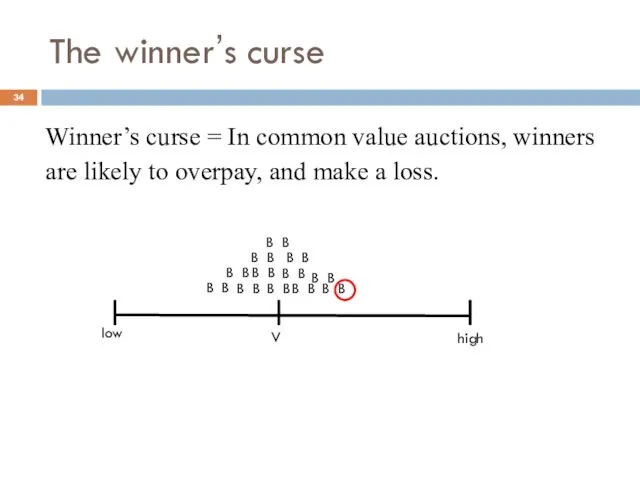

The winner’s curse

Winner’s curse = In common value auctions, winners

are

The winner’s curse

Winner’s curse = In common value auctions, winners

are

Dealing with the winner’s curse

Given that I win an auction …All

Dealing with the winner’s curse

Given that I win an auction …All

Avoiding the winner’s curse

Bidding with no regrets:

Since winning means you have

Avoiding the winner’s curse

Bidding with no regrets:

Since winning means you have

All-pay auctions

Common value first-price auction in which bidders pays the amount

All-pay auctions

Common value first-price auction in which bidders pays the amount

All-pay auctions

Example 3: Research and development, patent race.

Competing pharmaceutical firms search

All-pay auctions

Example 3: Research and development, patent race.

Competing pharmaceutical firms search

All-pay auctions

Optimal strategy

If everyone else bids aggressively, your best response is

All-pay auctions

Optimal strategy

If everyone else bids aggressively, your best response is

All-pay auctions

Equilibrium

Consider an all-pay auction with prize worth 1, n bidders.

Bid

All-pay auctions

Equilibrium

Consider an all-pay auction with prize worth 1, n bidders.

Bid

All-pay auctions

Equilibrium

The bidder win if all remaining bids are less than

All-pay auctions

Equilibrium

The bidder win if all remaining bids are less than

All-pay auctions

Equilibrium

When n=2, players play each value of x with equal

All-pay auctions

Equilibrium

When n=2, players play each value of x with equal

All-pay auctions

Overbidding

Class experiments: Auction of a $20 bill

Students start bidding $3,

All-pay auctions

Overbidding

Class experiments: Auction of a $20 bill

Students start bidding $3,

Применение производной и интегралов в различных областях биологии и химии

Применение производной и интегралов в различных областях биологии и химии Теорема Пифагора

Теорема Пифагора Самостоятельная работа

Самостоятельная работа Түзусызықты теңайнымалы қозғалыс, үдеу

Түзусызықты теңайнымалы қозғалыс, үдеу Из истории геометрических терминов

Из истории геометрических терминов Презентация Сочетательное свойство сложения

Презентация Сочетательное свойство сложения Решение задач на смеси и сплавы

Решение задач на смеси и сплавы Интеллектуальные информационные системы. Лекция 6. Нечеткая логика. Математические основы

Интеллектуальные информационные системы. Лекция 6. Нечеткая логика. Математические основы Решение задач по теме Параллельность плоскостей. Тетраэдр и параллелепипед

Решение задач по теме Параллельность плоскостей. Тетраэдр и параллелепипед Повторення вивченого. Додаткові вправи. Урок №136

Повторення вивченого. Додаткові вправи. Урок №136 Игра – самый умный математик. 6 класс

Игра – самый умный математик. 6 класс Расстояние между двумя точками. Масштаб

Расстояние между двумя точками. Масштаб Таблица истинности для импликации

Таблица истинности для импликации Нестандартные способы решения тригонометрических уравнений

Нестандартные способы решения тригонометрических уравнений Площади параллелограмма, треугольника и трапеции. Урок 21-22

Площади параллелограмма, треугольника и трапеции. Урок 21-22 Графоаналитические методы оценки параметров распределения (лекция 5)

Графоаналитические методы оценки параметров распределения (лекция 5) Додавання і віднімання раціональних чисел

Додавання і віднімання раціональних чисел П’єр де Ферма (1601-1665)

П’єр де Ферма (1601-1665) Презентация к уроку Задача 1 класс

Презентация к уроку Задача 1 класс Рішення рівнянь

Рішення рівнянь Делители и кратные (часть 3)

Делители и кратные (часть 3) Тест по теме: четырехугольники

Тест по теме: четырехугольники Решение систем линейных уравнений методом Крамера, методом Гаусса и матричным методом (вопросы)

Решение систем линейных уравнений методом Крамера, методом Гаусса и матричным методом (вопросы) Дроби. Нахождение части числа. Нахождение целого по его части.

Дроби. Нахождение части числа. Нахождение целого по его части. Умножение и деление положительных и отрицательных чисел

Умножение и деление положительных и отрицательных чисел Меньше или больше. Демонстрационный материал. 5 класс

Меньше или больше. Демонстрационный материал. 5 класс ПРЕЗЕНТАЦИЯ Умножение многозначного числа на однозначное (закрепление)

ПРЕЗЕНТАЦИЯ Умножение многозначного числа на однозначное (закрепление) Презентация ТАНГРАМ Животные

Презентация ТАНГРАМ Животные