- Advanced. Topics in risk management

Содержание

- 2. Agenda The Changing Scope of Risk Management Enterprise Risk Management Insurance Market Dynamics Loss Forecasting Financial

- 3. The Changing Scope of Risk Management Today, the risk manager’s job: Involves more than simply purchasing

- 4. The Changing Scope of Risk Management Financial Risk Management refers to the identification, analysis, and treatment

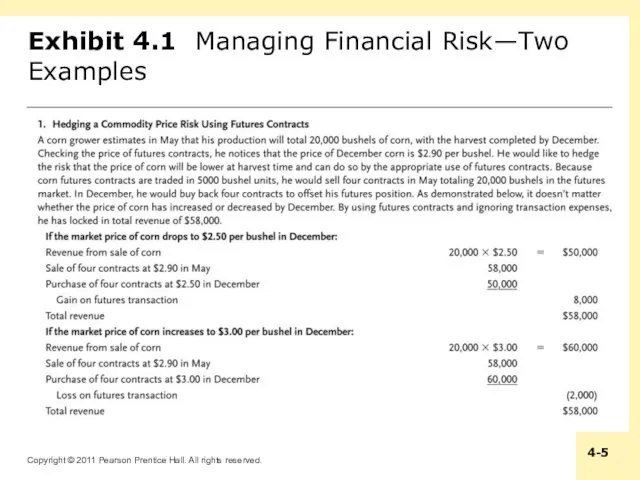

- 5. Exhibit 4.1 Managing Financial Risk—Two Examples

- 6. Exhibit 4.1 Managing Financial Risk—Two Examples

- 7. The Changing Scope of Risk Management An integrated risk management program is a risk treatment technique

- 8. Enterprise Risk Management Enterprise Risk Management (ERM) is a comprehensive risk management program that addresses the

- 9. The Financial Crisis and Enterprise Risk Management The US stock market dropped by more than fifty

- 10. Exhibit 4.2 Timeline of Events Related to the Financial Crisis

- 11. The Financial Crisis and Enterprise Risk Management AIG mentions an active ERM program in its 2007

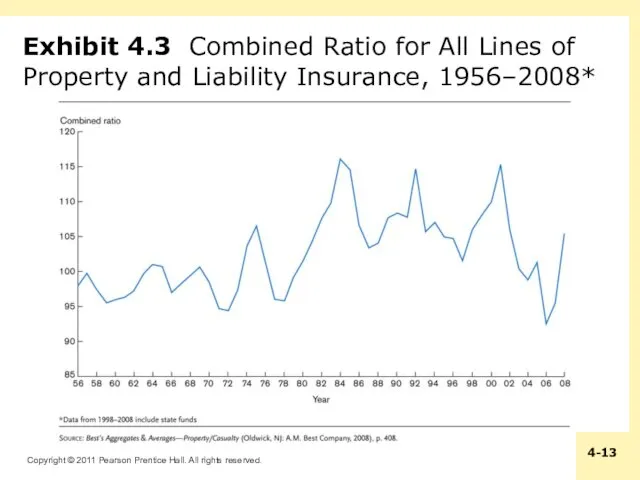

- 12. Insurance Market Dynamics Decisions about whether to retain or transfer risks are influenced by conditions in

- 13. Exhibit 4.3 Combined Ratio for All Lines of Property and Liability Insurance, 1956–2008*

- 14. Insurance Market Dynamics Many factors affect property and liability insurance pricing and underwriting decisions: Insurance industry

- 15. Insurance Market Dynamics The trend toward consolidation in the financial services industry is continuing Consolidation refers

- 16. Capital Market Risk Financing Alternatives Insurers are making increasing use of capital markets to assist in

- 17. Exhibit 4.4 Catastrophe Bonds: Annual Number of Transactions and Issue Size

- 18. Loss Forecasting The risk manager can predict losses using several different techniques: Probability analysis Regression analysis

- 19. Loss Forecasting Probability analysis: the risk manager can assign probabilities to individual and joint events The

- 20. Loss Forecasting Regression analysis characterizes the relationship between two or more variables and then uses this

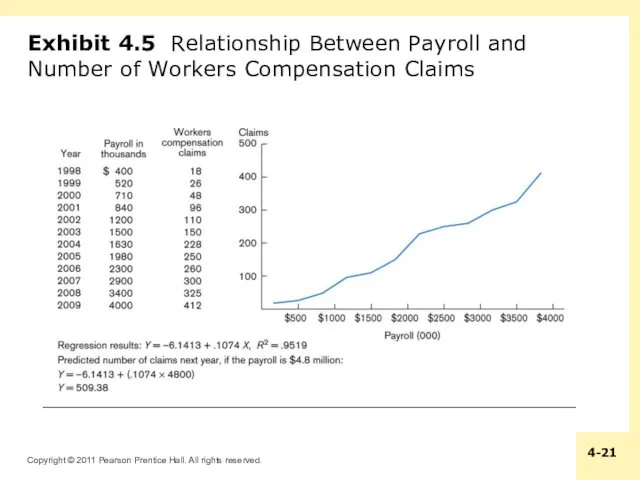

- 21. Exhibit 4.5 Relationship Between Payroll and Number of Workers Compensation Claims

- 22. Loss Forecasting A loss distribution is a probability distribution of losses that could occur Useful for

- 23. Financial Analysis in Risk Management Decision Making The time value of money must be considered when

- 24. Other Risk Management Tools A risk management information system (RMIS) is a computerized database that permits

- 26. Скачать презентацию

Agenda

The Changing Scope of Risk Management

Enterprise Risk Management

Insurance Market Dynamics

Loss Forecasting

Financial

Agenda

The Changing Scope of Risk Management

Enterprise Risk Management

Insurance Market Dynamics

Loss Forecasting

Financial

The Changing Scope of Risk Management

Today, the risk manager’s job:

Involves more

The Changing Scope of Risk Management

Today, the risk manager’s job:

Involves more

The Changing Scope of Risk Management

Financial Risk Management refers to

The Changing Scope of Risk Management

Financial Risk Management refers to

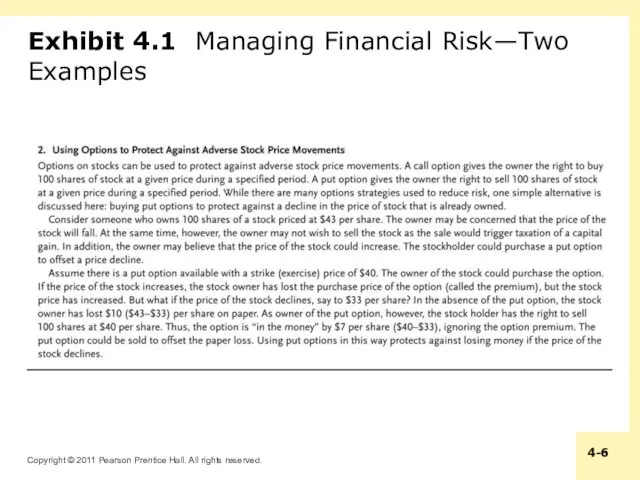

Exhibit 4.1 Managing Financial Risk—Two Examples

Exhibit 4.1 Managing Financial Risk—Two Examples

Exhibit 4.1 Managing Financial Risk—Two Examples

Exhibit 4.1 Managing Financial Risk—Two Examples

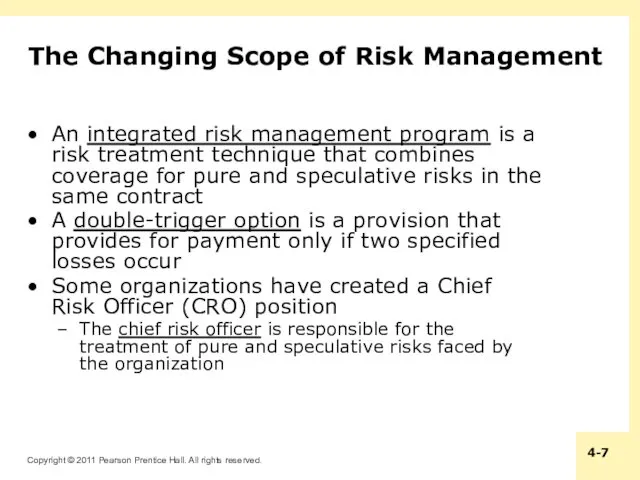

The Changing Scope of Risk Management

An integrated risk management program is

The Changing Scope of Risk Management

An integrated risk management program is

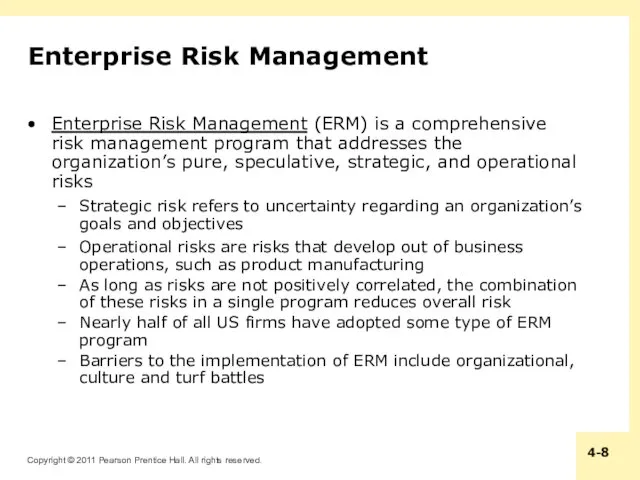

Enterprise Risk Management

Enterprise Risk Management (ERM) is a comprehensive risk management

Enterprise Risk Management

Enterprise Risk Management (ERM) is a comprehensive risk management

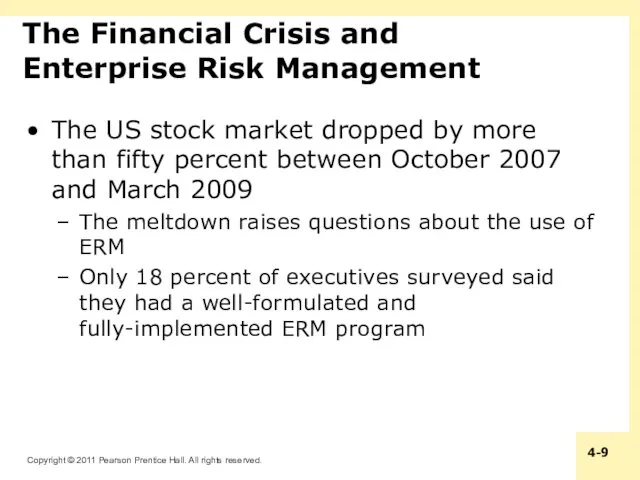

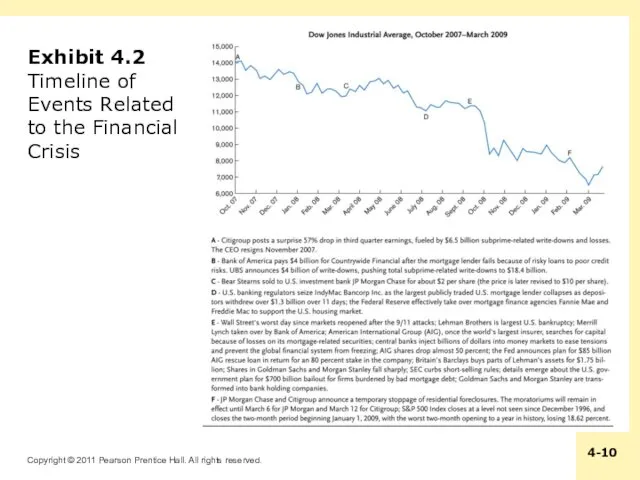

The Financial Crisis and Enterprise Risk Management

The US stock market dropped

The Financial Crisis and Enterprise Risk Management

The US stock market dropped

Exhibit 4.2 Timeline of Events Related to the Financial Crisis

Exhibit 4.2 Timeline of Events Related to the Financial Crisis

The Financial Crisis and Enterprise Risk Management

AIG mentions an active ERM

The Financial Crisis and Enterprise Risk Management

AIG mentions an active ERM

Insurance Market Dynamics

Decisions about whether to retain or transfer risks

Insurance Market Dynamics

Decisions about whether to retain or transfer risks

Exhibit 4.3 Combined Ratio for All Lines of Property and Liability

Exhibit 4.3 Combined Ratio for All Lines of Property and Liability

Insurance Market Dynamics

Many factors affect property and liability insurance pricing and

Insurance Market Dynamics

Many factors affect property and liability insurance pricing and

Insurance Market Dynamics

The trend toward consolidation in the financial services industry

Insurance Market Dynamics

The trend toward consolidation in the financial services industry

Capital Market Risk Financing Alternatives

Insurers are making increasing use of capital

Capital Market Risk Financing Alternatives

Insurers are making increasing use of capital

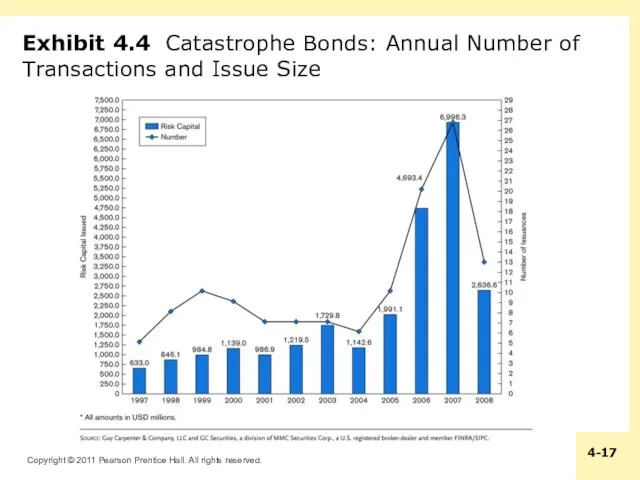

Exhibit 4.4 Catastrophe Bonds: Annual Number of Transactions and Issue Size

Exhibit 4.4 Catastrophe Bonds: Annual Number of Transactions and Issue Size

Loss Forecasting

The risk manager can predict losses using several different techniques:

Probability

Loss Forecasting

The risk manager can predict losses using several different techniques:

Probability

Loss Forecasting

Probability analysis: the risk manager can assign probabilities to individual

Loss Forecasting

Probability analysis: the risk manager can assign probabilities to individual

Loss Forecasting

Regression analysis characterizes the relationship between two or more variables

Loss Forecasting

Regression analysis characterizes the relationship between two or more variables

Exhibit 4.5 Relationship Between Payroll and Number of Workers Compensation Claims

Exhibit 4.5 Relationship Between Payroll and Number of Workers Compensation Claims

Loss Forecasting

A loss distribution is a probability distribution of losses that

Loss Forecasting

A loss distribution is a probability distribution of losses that

Financial Analysis in Risk Management Decision Making

The time value of money

Financial Analysis in Risk Management Decision Making

The time value of money

Other Risk Management Tools

A risk management information system (RMIS) is a

Other Risk Management Tools

A risk management information system (RMIS) is a

Управление проектами. Основы профессиональных знаний (ICB IPMA)

Управление проектами. Основы профессиональных знаний (ICB IPMA) Źródła innowacji w organizacji

Źródła innowacji w organizacji The Britannia Steam Ship Insurance

The Britannia Steam Ship Insurance Понятие, цели и этапы деловой оценки персонала

Понятие, цели и этапы деловой оценки персонала Основы организации пассажирских перевозок. Оценка качества пассажирских перевозок

Основы организации пассажирских перевозок. Оценка качества пассажирских перевозок Управление персоналом

Управление персоналом Управление IT-отделом

Управление IT-отделом Стандарты качества. Лекция 3

Стандарты качества. Лекция 3 Бизнес-планирование в системе стратегического менеджмента

Бизнес-планирование в системе стратегического менеджмента Стандарты обслуживания КЦ

Стандарты обслуживания КЦ Управление развитием персонала в современном МОАУ

Управление развитием персонала в современном МОАУ Менеджмент інформаційних систем. Лекція №1

Менеджмент інформаційних систем. Лекція №1 Создание организаций. (Тема 10)

Создание организаций. (Тема 10) Оценка управленческих компетенций методом Ассесмента

Оценка управленческих компетенций методом Ассесмента Ситуационные центры органов государственной власти РФ. (Тема 8)

Ситуационные центры органов государственной власти РФ. (Тема 8) Сутність та види в менеджменте

Сутність та види в менеджменте Сыртқы орта және корпоративтік мәдениет

Сыртқы орта және корпоративтік мәдениет Разработка управленческих решений в условиях определенности

Разработка управленческих решений в условиях определенности Multicultural assessment, expatriates selection & testing cultural intelligent

Multicultural assessment, expatriates selection & testing cultural intelligent Разработка и принятие управленческих решений

Разработка и принятие управленческих решений Мотивация персонала. Обучение и аттестация. Роль руководителя в служебной иерархии

Мотивация персонала. Обучение и аттестация. Роль руководителя в служебной иерархии Проект От профессиональной культуры к профессиональной карьере

Проект От профессиональной культуры к профессиональной карьере Статистика оплаты труда

Статистика оплаты труда История создания и развития бережливого производства

История создания и развития бережливого производства Основы управления качеством в сфере образования

Основы управления качеством в сфере образования Шаблоны матриц курсовой работы

Шаблоны матриц курсовой работы Гриль-бары ШашлыкоFF

Гриль-бары ШашлыкоFF Кадровые интервью на должность автослесаря автомастерской Автодиас

Кадровые интервью на должность автослесаря автомастерской Автодиас