- 05 II. Inflation. Its causes, effects, and social costs

Содержание

- 2. Lenin is said to have declared that the best way to destroy the Capitalist System was

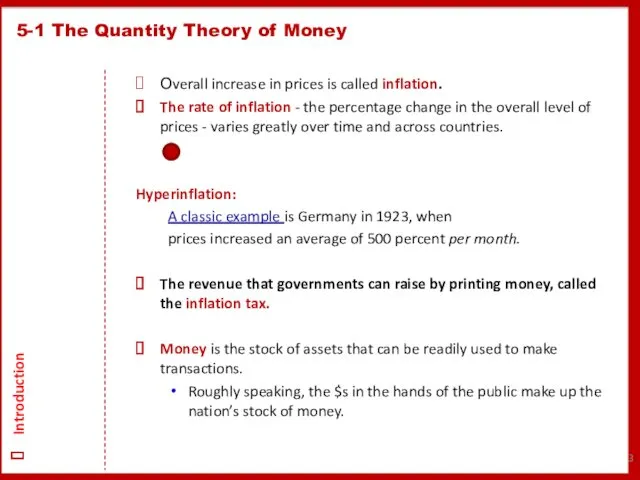

- 3. Оverall increase in prices is called inflation. The rate of inflation - the percentage change in

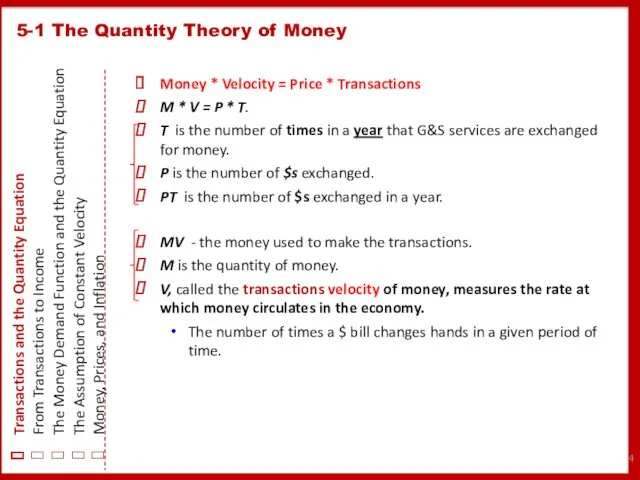

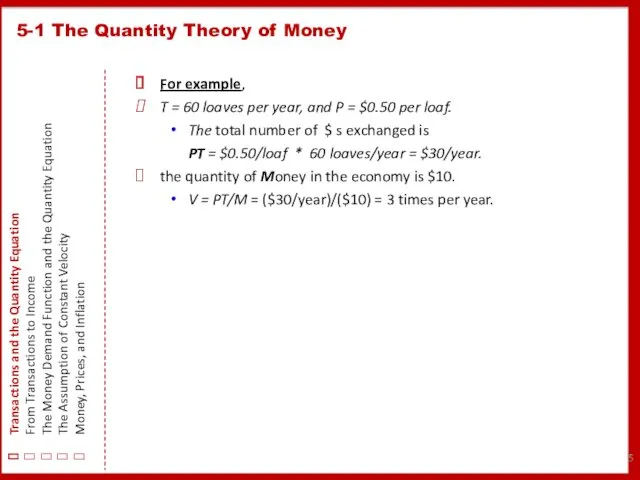

- 4. Money * Velocity = Price * Transactions M * V = P * T. T is

- 5. 5-1 The Quantity Theory of Money Transactions and the Quantity Equation From Transactions to Income The

- 6. 5-1 The Quantity Theory of Money Transactions and the Quantity Equation From Transactions to Income The

- 7. 5-1 The Quantity Theory of Money Transactions and the Quantity Equation From Transactions to Income The

- 8. 5-1 The Quantity Theory of Money Transactions and the Quantity Equation From Transactions to Income The

- 9. 5-1 The Quantity Theory of Money Transactions and the Quantity Equation From Transactions to Income The

- 10. Inflation and Money Growth

- 11. Inflation and Money Growth

- 12. 5-2 Seigniorage: The Revenue From Printing Money The revenue raised by the printing of money is

- 13. Although seigniorage has not been a major source of revenue for the U.S. Government in recent

- 14. The interest rate that the bank pays is called the nominal interest rate, and the increase

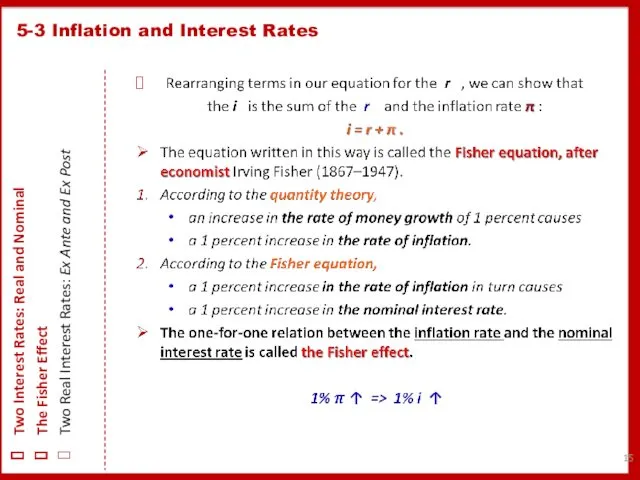

- 15. 5-3 Inflation and Interest Rates Two Interest Rates: Real and Nominal The Fisher Effect Two Real

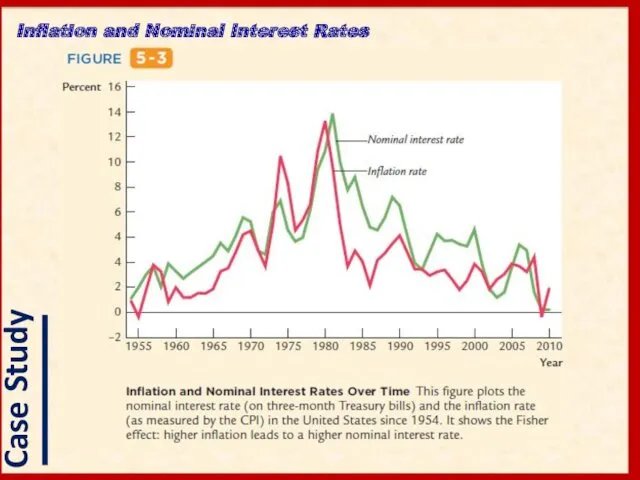

- 16. Inflation and Nominal Interest Rates

- 17. Inflation and Nominal Interest Rates

- 18. 5-3 Inflation and Interest Rates Two Interest Rates: Real and Nominal The Fisher Effect Two Real

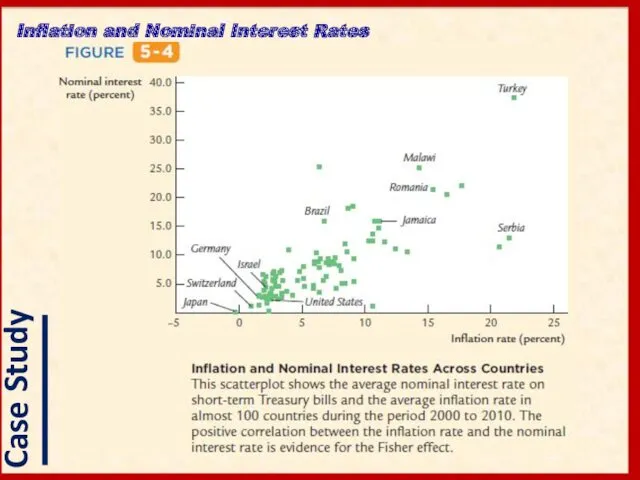

- 19. Although recent data show a positive relationship between nominal interest rates and inflation rates, this finding

- 20. The money you hold in your wallet does not earn interest. If you deposited it in

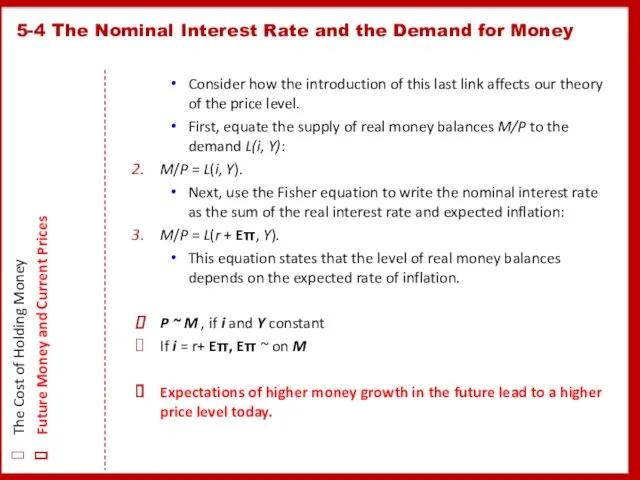

- 21. 5-4 The Nominal Interest Rate and the Demand for Money The Cost of Holding Money Future

- 22. 5-4 The Nominal Interest Rate and the Demand for Money The Cost of Holding Money Future

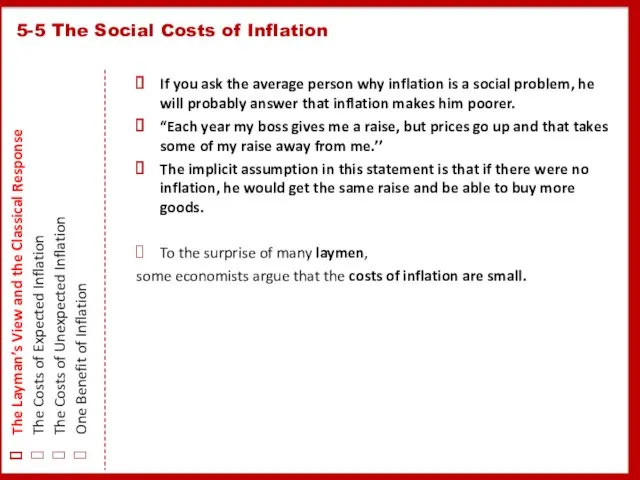

- 23. If you ask the average person why inflation is a social problem, he will probably answer

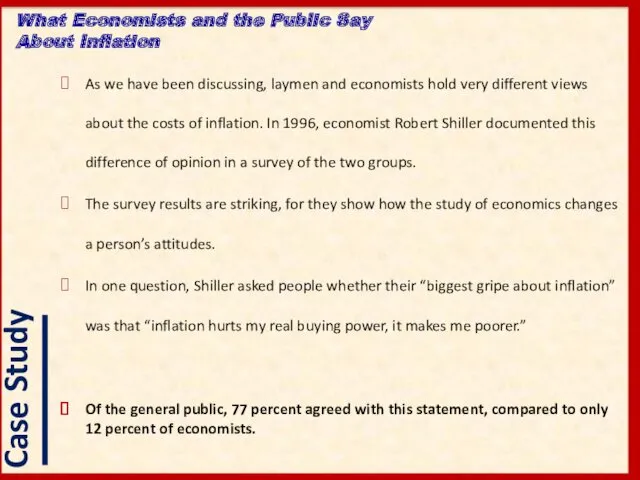

- 24. As we have been discussing, laymen and economists hold very different views about the costs of

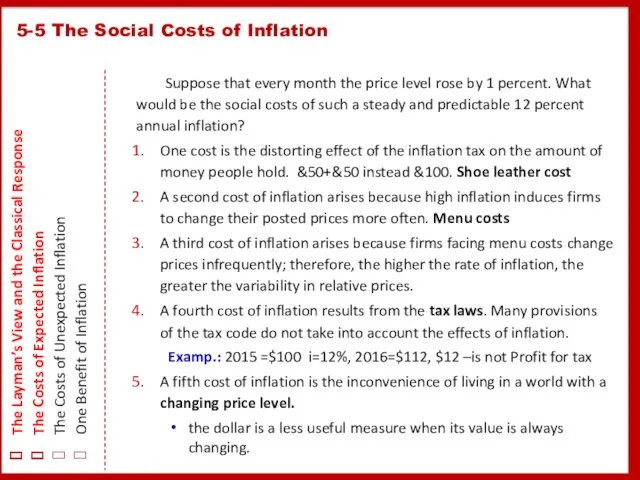

- 25. Suppose that every month the price level rose by 1 percent. What would be the social

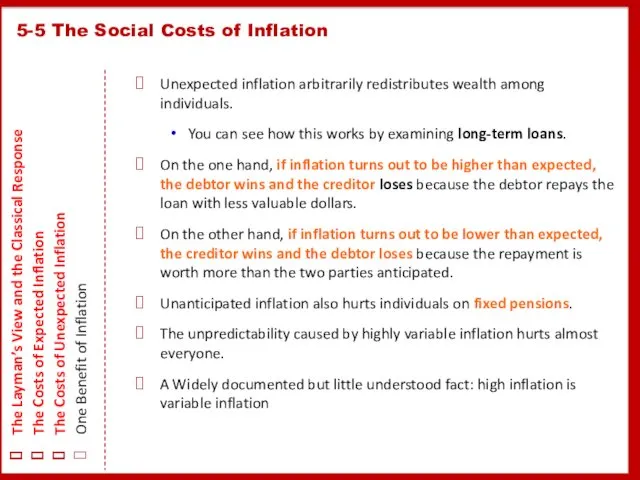

- 26. Unexpected inflation arbitrarily redistributes wealth among individuals. You can see how this works by examining long-term

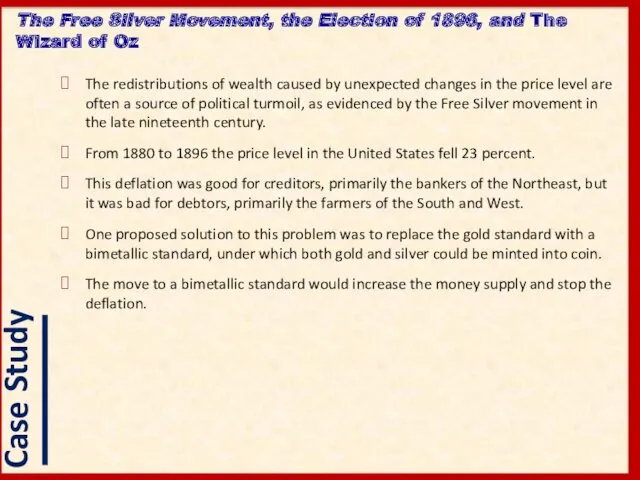

- 27. The redistributions of wealth caused by unexpected changes in the price level are often a source

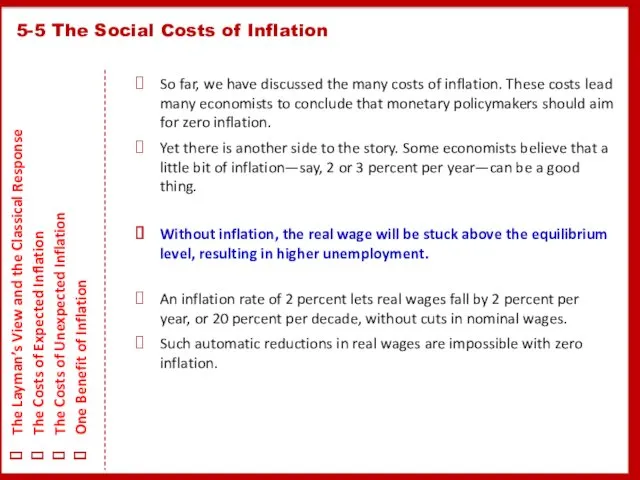

- 28. So far, we have discussed the many costs of inflation. These costs lead many economists to

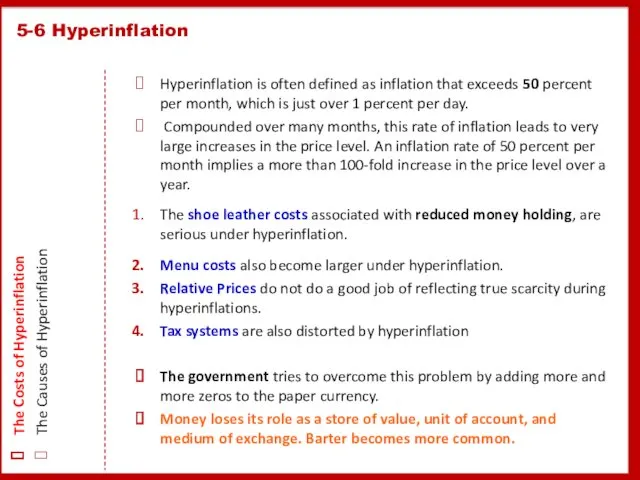

- 29. Hyperinflation is often defined as inflation that exceeds 50 percent per month, which is just over

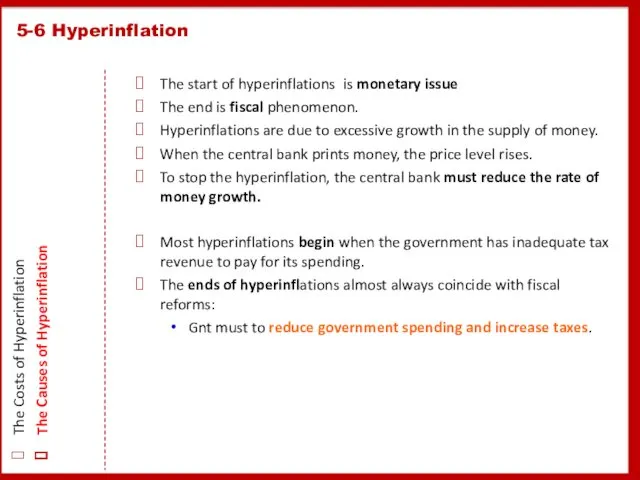

- 30. The start of hyperinflations is monetary issue The end is fiscal phenomenon. Hyperinflations are due to

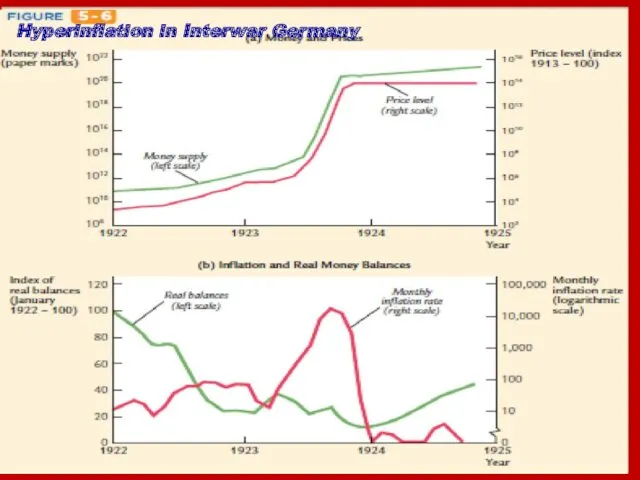

- 31. Hyperinflation in Interwar Germany

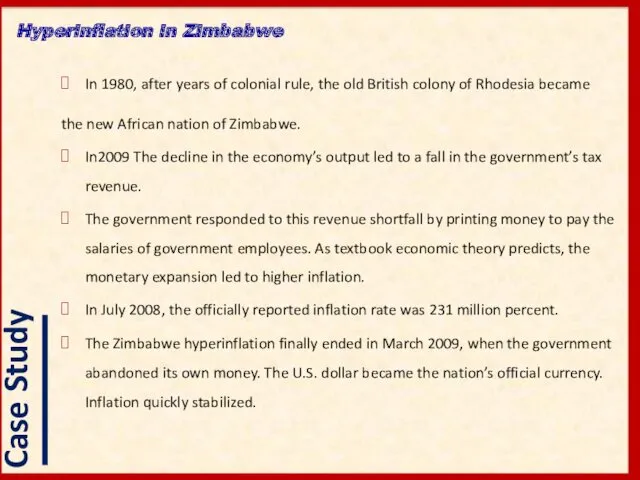

- 32. In 1980, after years of colonial rule, the old British colony of Rhodesia became the new

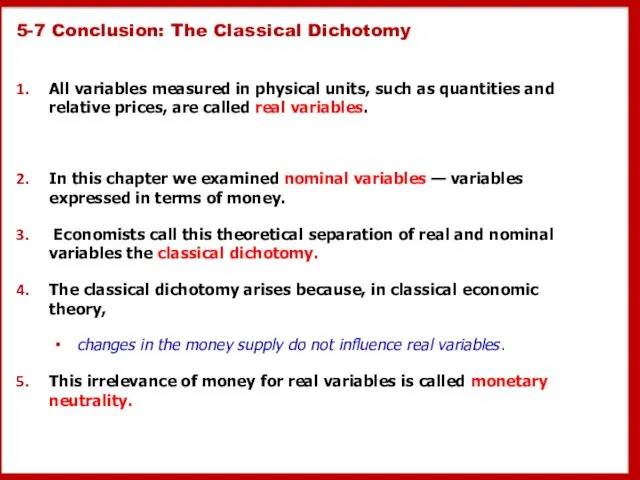

- 33. 5-7 Conclusion: The Classical Dichotomy All variables measured in physical units, such as quantities and relative

- 35. Скачать презентацию

Lenin is said to have declared that the best way to

Lenin is said to have declared that the best way to

Оverall increase in prices is called inflation.

The rate of inflation -

Оverall increase in prices is called inflation.

The rate of inflation -

Money * Velocity = Price * Transactions

M * V = P

Money * Velocity = Price * Transactions

M * V = P

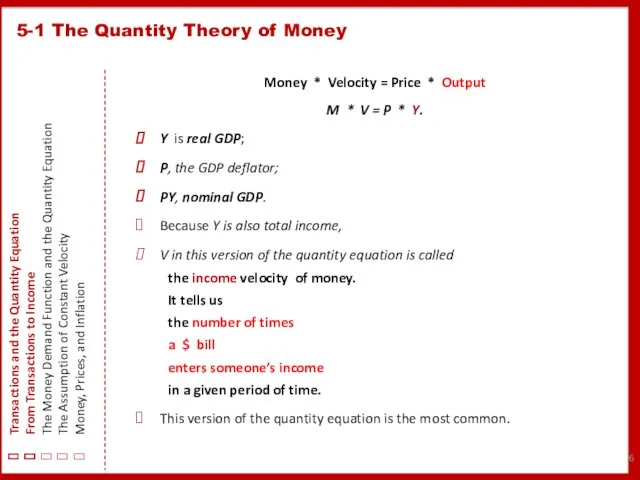

5-1 The Quantity Theory of Money

Transactions and the Quantity Equation

5-1 The Quantity Theory of Money

Transactions and the Quantity Equation

5-1 The Quantity Theory of Money

Transactions and the Quantity Equation

5-1 The Quantity Theory of Money

Transactions and the Quantity Equation

5-1 The Quantity Theory of Money

Transactions and the Quantity Equation

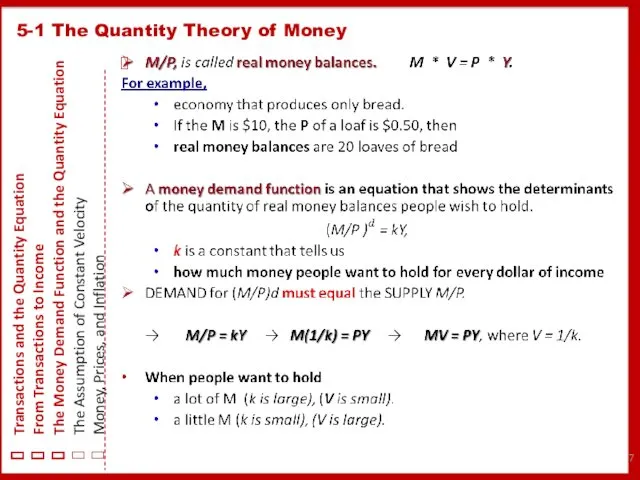

5-1 The Quantity Theory of Money

Transactions and the Quantity Equation

5-1 The Quantity Theory of Money

Transactions and the Quantity Equation

5-1 The Quantity Theory of Money

Transactions and the Quantity Equation

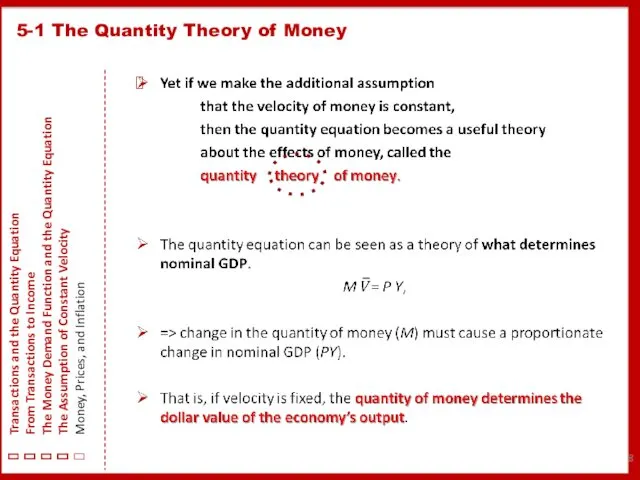

5-1 The Quantity Theory of Money

Transactions and the Quantity Equation

5-1 The Quantity Theory of Money

Transactions and the Quantity Equation

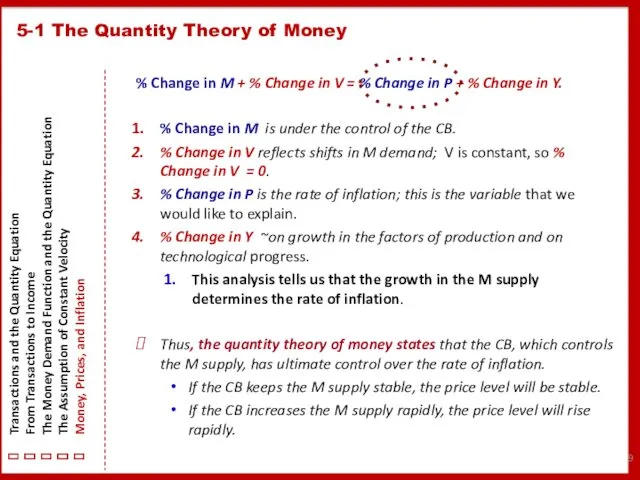

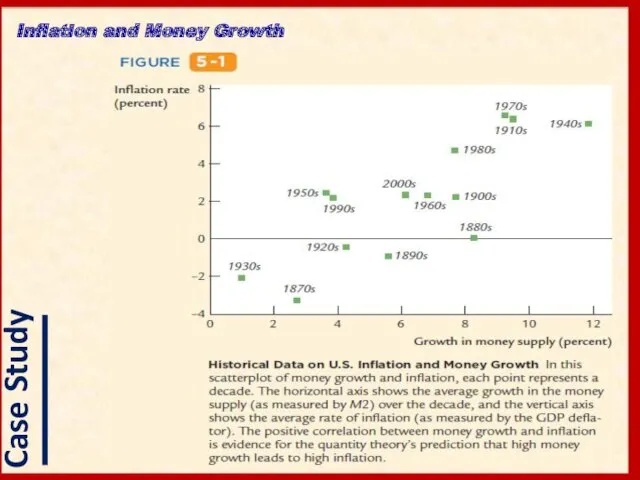

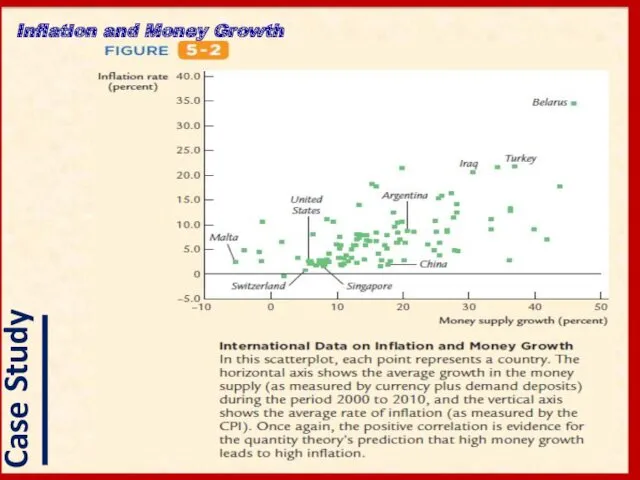

Inflation and Money Growth

Inflation and Money Growth

Inflation and Money Growth

Inflation and Money Growth

5-2 Seigniorage: The Revenue From Printing Money

The revenue raised by the

5-2 Seigniorage: The Revenue From Printing Money

The revenue raised by the

Although seigniorage has not been a major source of revenue for

Although seigniorage has not been a major source of revenue for

The interest rate that the bank pays is called the nominal

The interest rate that the bank pays is called the nominal

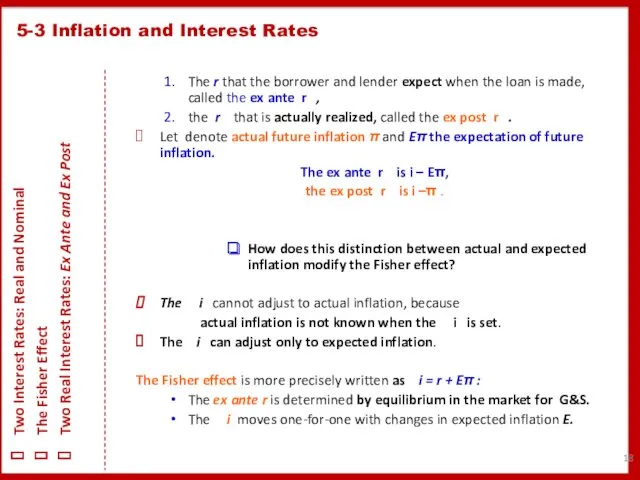

5-3 Inflation and Interest Rates

Two Interest Rates: Real and Nominal

The Fisher

5-3 Inflation and Interest Rates

Two Interest Rates: Real and Nominal

The Fisher

Inflation and Nominal Interest Rates

Inflation and Nominal Interest Rates

Inflation and Nominal Interest Rates

Inflation and Nominal Interest Rates

5-3 Inflation and Interest Rates

Two Interest Rates: Real and Nominal

The Fisher

5-3 Inflation and Interest Rates

Two Interest Rates: Real and Nominal

The Fisher

Although recent data show a positive relationship between nominal interest rates

Although recent data show a positive relationship between nominal interest rates

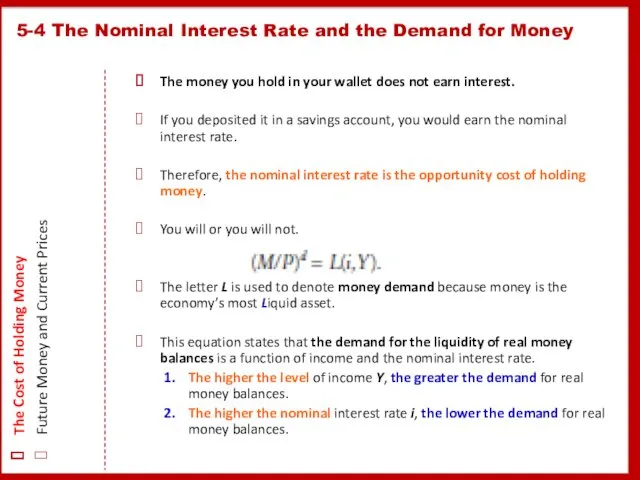

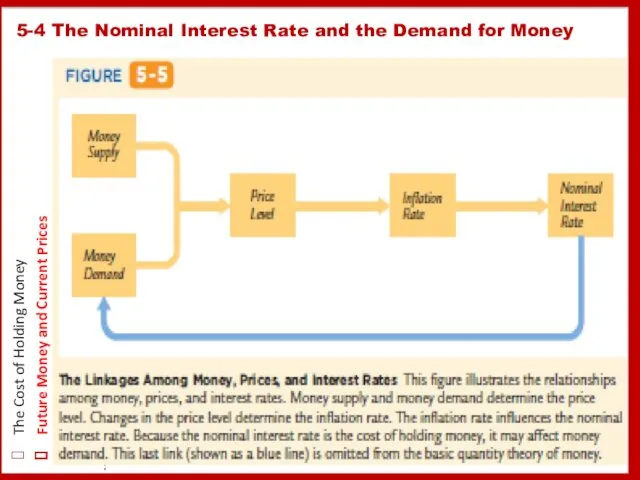

The money you hold in your wallet does not earn interest.

The money you hold in your wallet does not earn interest.

5-4 The Nominal Interest Rate and the Demand for Money

The

5-4 The Nominal Interest Rate and the Demand for Money

The

5-4 The Nominal Interest Rate and the Demand for Money

The

5-4 The Nominal Interest Rate and the Demand for Money

The

If you ask the average person why inflation is a social

If you ask the average person why inflation is a social

As we have been discussing, laymen and economists hold very different

As we have been discussing, laymen and economists hold very different

Suppose that every month the price level rose by 1

Suppose that every month the price level rose by 1

Unexpected inflation arbitrarily redistributes wealth among individuals.

You can see how this

Unexpected inflation arbitrarily redistributes wealth among individuals.

You can see how this

The redistributions of wealth caused by unexpected changes in the price

The redistributions of wealth caused by unexpected changes in the price

So far, we have discussed the many costs of inflation. These

So far, we have discussed the many costs of inflation. These

Hyperinflation is often defined as inflation that exceeds 50 percent per

Hyperinflation is often defined as inflation that exceeds 50 percent per

The start of hyperinflations is monetary issue

The end is fiscal phenomenon.

Hyperinflations

The start of hyperinflations is monetary issue

The end is fiscal phenomenon.

Hyperinflations

Hyperinflation in Interwar Germany

Hyperinflation in Interwar Germany

In 1980, after years of colonial rule, the old British colony

In 1980, after years of colonial rule, the old British colony

5-7 Conclusion: The Classical Dichotomy

All variables measured in physical units, such

5-7 Conclusion: The Classical Dichotomy

All variables measured in physical units, such

Споруди та пристрої сигналізації, зв'язку і обчислювальної техніки. Сигнали. (Розділ 6)

Споруди та пристрої сигналізації, зв'язку і обчислювальної техніки. Сигнали. (Розділ 6) Pavel_Blyume_prezentatsia

Pavel_Blyume_prezentatsia Противофазное включение двигателей СН в момент восстановления питания. ЭЧСЭСП, часть 4, лекции 35-45

Противофазное включение двигателей СН в момент восстановления питания. ЭЧСЭСП, часть 4, лекции 35-45 Техническое обследование жилых зданий. (Тема 1)

Техническое обследование жилых зданий. (Тема 1) Инфекционные болезни

Инфекционные болезни Связьтранснефть I квартал 2021, свод замечаний СКК

Связьтранснефть I квартал 2021, свод замечаний СКК Master class de português

Master class de português Водные обитатели. Рыбы

Водные обитатели. Рыбы Посвящение в члены Отряда юных пожарных

Посвящение в члены Отряда юных пожарных Петербургские повести Н.В. Гоголя. Образ маленького человека в литературе

Петербургские повести Н.В. Гоголя. Образ маленького человека в литературе Основні поняття хімічної термодинаміки

Основні поняття хімічної термодинаміки Презентация Программа Система диагностики и коррекции психического развития детей дошкольного возраста

Презентация Программа Система диагностики и коррекции психического развития детей дошкольного возраста Системные платы

Системные платы Культурная жизнь Кубани в период оттепели.

Культурная жизнь Кубани в период оттепели. Внешняя политика в XVII веке

Внешняя политика в XVII веке Презентация Река и ее части

Презентация Река и ее части Домашние животные

Домашние животные Биполярные транзисторы

Биполярные транзисторы Этапы процесса транскрипции в генетике. (Лекция 16)

Этапы процесса транскрипции в генетике. (Лекция 16) Арифметические операции в системах счисления

Арифметические операции в системах счисления Жердің ғаламшар ретіндегі жалпы сипаттамасы

Жердің ғаламшар ретіндегі жалпы сипаттамасы Расписание автобусов с 30 04 2020

Расписание автобусов с 30 04 2020 Точение. Правильный выбор геометрии

Точение. Правильный выбор геометрии Ливонская война

Ливонская война Студенческая олимпиада: Я-профессионал

Студенческая олимпиада: Я-профессионал Улучшение окружающей среды.

Улучшение окружающей среды. Создания в классе развивающей среды как условия повышения образовательного потенциала обучающихся

Создания в классе развивающей среды как условия повышения образовательного потенциала обучающихся Профилактика табакокурения у подростков

Профилактика табакокурения у подростков