- Capital Market History and Risk & Return

Содержание

- 2. A2. Capital Market History and Risk & Return (continued) Expected Returns and Variances Portfolios Announcements, Surprises,

- 3. A3. Risk, Return, and Financial Markets “. . . Wall Street shapes Main Street. Financial markets

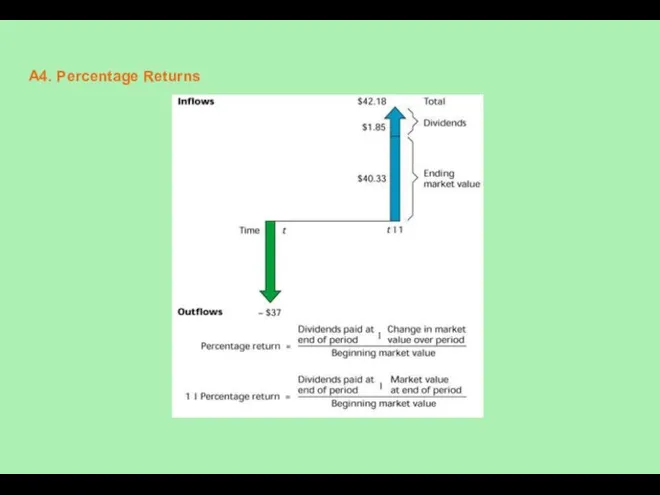

- 4. A4. Percentage Returns

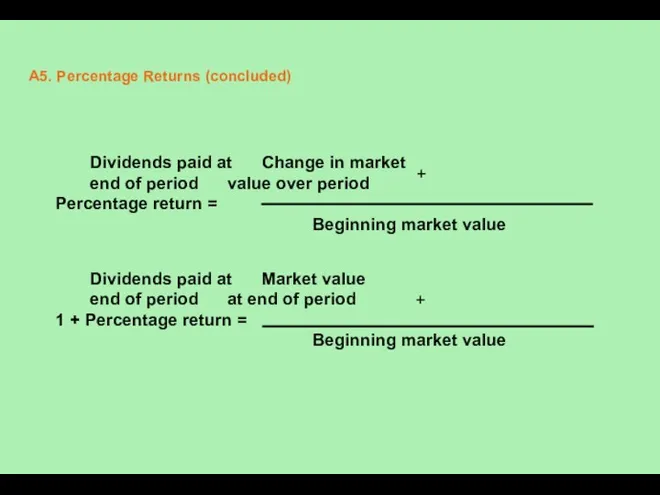

- 5. A5. Percentage Returns (concluded) Dividends paid at Change in market end of period value over period

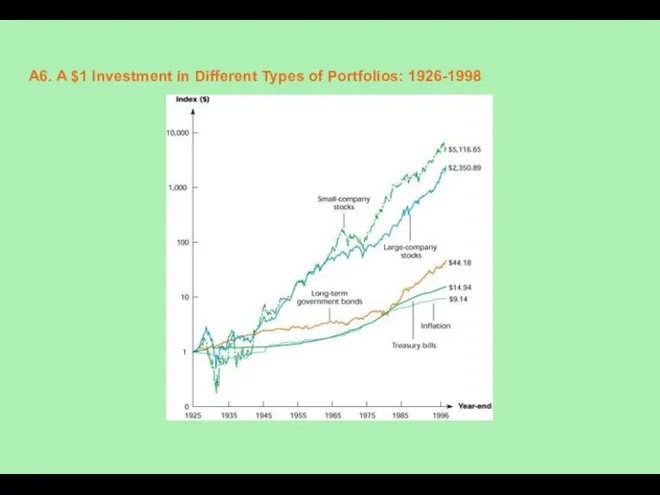

- 6. A6. A $1 Investment in Different Types of Portfolios: 1926-1998

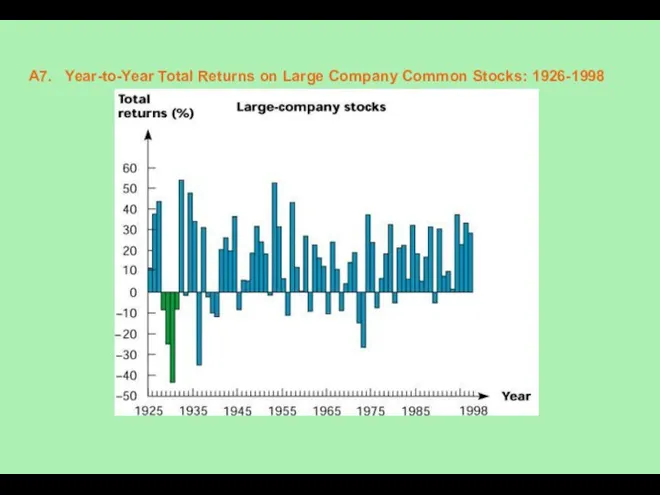

- 7. A7. Year-to-Year Total Returns on Large Company Common Stocks: 1926-1998

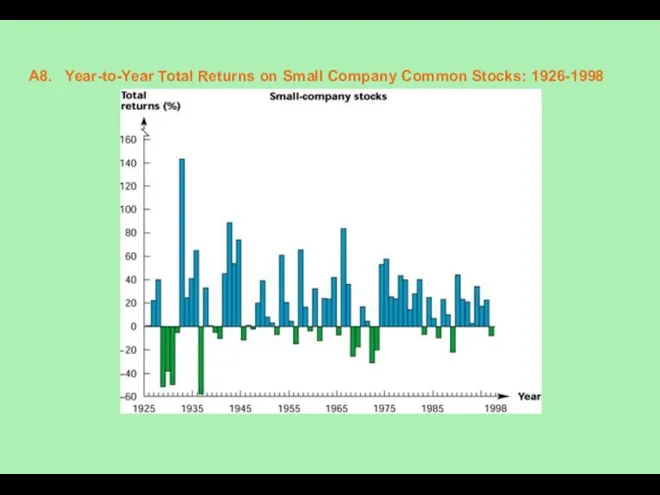

- 8. A8. Year-to-Year Total Returns on Small Company Common Stocks: 1926-1998

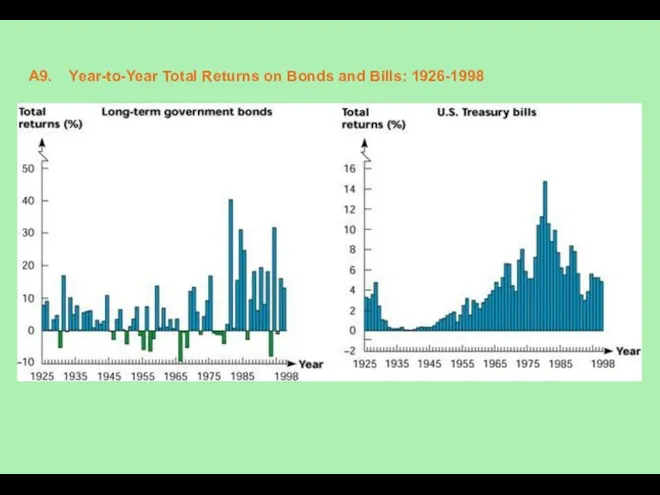

- 9. A9. Year-to-Year Total Returns on Bonds and Bills: 1926-1998

- 10. A10. Year-to-Year Total Returns on Bonds and Bills: 1926-1998 (concluded) Total Returns (%) 16 14 12

- 11. A11. Year-to-Year Inflation: 1926-1998

- 12. A12. Historical Dividend Yield on Common Stocks 10% 9 8 7 6 5 4 3 2

- 13. A13. S&P 500 Risk Premiums: 1926-1998

- 14. A14. Small Stock Risk Premiums: 1926-1998

- 15. A15. Using Capital Market History Now let’s use our knowledge of capital market history to make

- 16. A16. Using Capital Market History (continued) Risk premiums: First, we calculate risk premiums. The risk premium

- 17. A17. Using Capital Market History (continued) Risk premiums: First, we calculate risk premiums. The risk premium

- 18. A18. Using Capital Market History (concluded) Let’s return to our earlier questions. Suppose the current T-bill

- 19. A19. Average Annual Returns and Risk Premiums: 1926-1998 Investment Average Return Risk Premium Large-company stocks 13.2%

- 20. A20. Frequency Distribution of Returns on Common Stocks, 1926-1998

- 21. A21. Historical Returns, Standard Deviations, and Frequency Distributions: 1926-1998

- 22. A22. The Normal Distribution

- 23. A23. Two Views on Market Efficiency “ . . . in price movements . . .

- 24. A24. Stock Price Reaction to New Information in Efficient and Inefficient Markets Efficient market reaction: The

- 25. A25. A Quick Quiz Here are three questions that should be easy to answer (if you’ve

- 26. A26. Chapter 12 Quick Quiz (continued) 1. How are average annual returns measured? Annual returns are

- 27. A27. Chapter 12 Quick Quiz (continued) 2. How is volatility measured? Given a normal distribution, volatility

- 28. A28. Chapter 12 Quick Quiz (concluded) 3. Assume your portfolio has had returns of 11%, -8%,

- 29. A29. A Few Examples Suppose a stock had an initial price of $58 per share, paid

- 30. A30. A Few Examples (continued) Suppose a stock had an initial price of $58 per share,

- 31. A31. A Few Examples (continued) Using the following returns, calculate the average returns, the variances, and

- 32. A32. A Few Examples (continued) Mean return on X = (.18 + .11 - .09 +

- 33. A33. A Few Examples (concluded) Mean return on X = (.18 + .11 - .09 +

- 34. A34. Expected Return and Variance: Basic Ideas The quantification of risk and return is a crucial

- 35. A35. Example: Calculating the Expected Return pi Ri Probability Return in State of Economy of state

- 36. A36. Example: Calculating the Expected Return (concluded) i (pi × Ri) i = 1 -1.25% i

- 37. A37. Calculation of Expected Return Stock L Stock U (3) (5) (2) Rate of Rate of

- 38. A38. Example: Calculating the Variance pi ri Probability Return in State of Economy of state i

- 39. A39. Calculating the Variance (concluded) i (Ri - R)2 pi × (Ri - R)2 i=1 .04

- 40. A40. Example: Expected Returns and Variances State of the Probability Return on Return on economy of

- 41. A41. Example: Expected Returns and Variances (concluded) B. Variances Var(RA) = 0.40 × (.30 - .06)2

- 42. A42. Example: Portfolio Expected Returns and Variances Portfolio weights: put 50% in Asset A and 50%

- 43. A43. Example: Portfolio Expected Returns and Variances (continued) A. E(RP) = 0.40 × (.125) + 0.60

- 44. A44. Example: Portfolio Expected Returns and Variances (concluded) New portfolio weights: put 3/7 in A and

- 45. A45. The Effect of Diversification on Portfolio Variance Stock A returns 0.05 0.04 0.03 0.02 0.01

- 46. A46. Announcements, Surprises, and Expected Returns Key issues: What are the components of the total return?

- 47. A47. Risk: Systematic and Unsystematic Systematic and Unsystematic Risk Types of surprises 1. Systematic or “market”

- 48. A48. Peter Bernstein on Risk and Diversification “Big risks are scary when you cannot diversify them,

- 49. A49. Standard Deviations of Annual Portfolio Returns ( 3) (2) Ratio of Portfolio (1) Average Standard

- 50. A50. Portfolio Diversification

- 51. A51. Beta Coefficients for Selected Companies Beta Company Coefficient American Electric Power .65 Exxon .80 IBM

- 52. A52. Example: Portfolio Beta Calculations Amount Portfolio Stock Invested Weights Beta (1) (2) (3) (4) (3)

- 53. A53. Example: Portfolio Expected Returns and Betas Assume you wish to hold a portfolio consisting of

- 54. A54. Example: Portfolio Expected Returns and Betas (concluded) Proportion Proportion Portfolio Invested in Invested in Expected

- 55. A55. Return, Risk, and Equilibrium Key issues: What is the relationship between risk and return? What

- 56. A56. Return, Risk, and Equilibrium (concluded) Example: Asset A has an expected return of 12% and

- 57. A57. Return, Risk, and Equilibrium (concluded) Example: Asset A has an expected return of 12% and

- 58. A58. The Capital Asset Pricing Model The Capital Asset Pricing Model (CAPM) - an equilibrium model

- 59. A59. The Security Market Line (SML)

- 60. A60. Summary of Risk and Return I. Total risk - the variance (or the standard deviation)

- 61. A61. Another Quick Quiz 1. Assume: the historic market risk premium has been about 8.5%. The

- 62. A62. Another Quick Quiz (continued) 1. Assume: the historic market risk premium has been about 8.5%.

- 63. A63. An Example Consider the following information: State of Prob. of State Stock A Stock B

- 64. A64. Solution to the Example Expected returns on an equal-weighted portfolio a. Boom E[Rp] = (.14

- 65. A65. Solution to the Example (continued) b. Boom: E[Rp] = __ (.14) + .15(.15) + .70(.33)

- 66. A66. Solution to the Example (concluded) b. Boom: E[Rp] = .15(.14) + .15(.15) + .70(.33) =

- 67. A67. Another Example Using information from capital market history, determine the return on a portfolio that

- 69. Скачать презентацию

A2. Capital Market History and Risk & Return (continued)

Expected Returns

A2. Capital Market History and Risk & Return (continued)

Expected Returns

A3. Risk, Return, and Financial Markets

“. . . Wall Street

A3. Risk, Return, and Financial Markets

“. . . Wall Street

A4. Percentage Returns

A4. Percentage Returns

A5. Percentage Returns (concluded)

Dividends paid at Change in market

end of

A5. Percentage Returns (concluded)

Dividends paid at Change in market end of

A6. A $1 Investment in Different Types of Portfolios: 1926-1998

A6. A $1 Investment in Different Types of Portfolios: 1926-1998

A7. Year-to-Year Total Returns on Large Company Common Stocks: 1926-1998

A7. Year-to-Year Total Returns on Large Company Common Stocks: 1926-1998

A8. Year-to-Year Total Returns on Small Company Common Stocks: 1926-1998

A8. Year-to-Year Total Returns on Small Company Common Stocks: 1926-1998

A9. Year-to-Year Total Returns on Bonds and Bills: 1926-1998

A9. Year-to-Year Total Returns on Bonds and Bills: 1926-1998

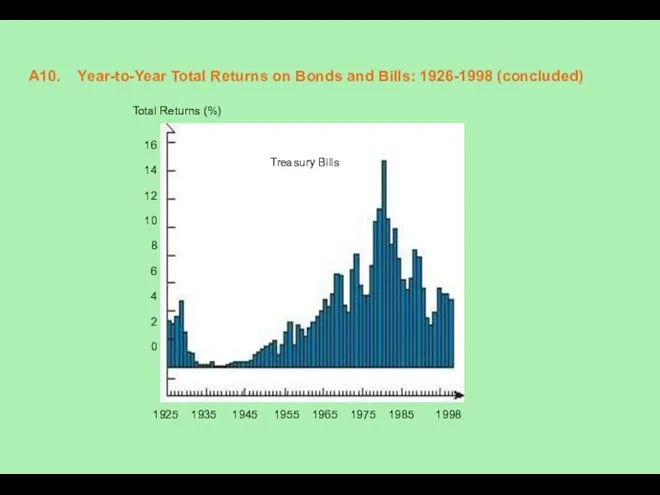

A10. Year-to-Year Total Returns on Bonds and Bills: 1926-1998 (concluded)

Total Returns

A10. Year-to-Year Total Returns on Bonds and Bills: 1926-1998 (concluded)

Total Returns

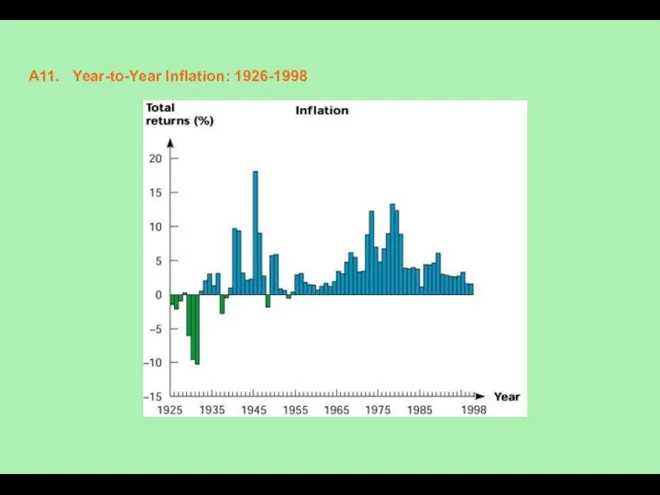

A11. Year-to-Year Inflation: 1926-1998

A11. Year-to-Year Inflation: 1926-1998

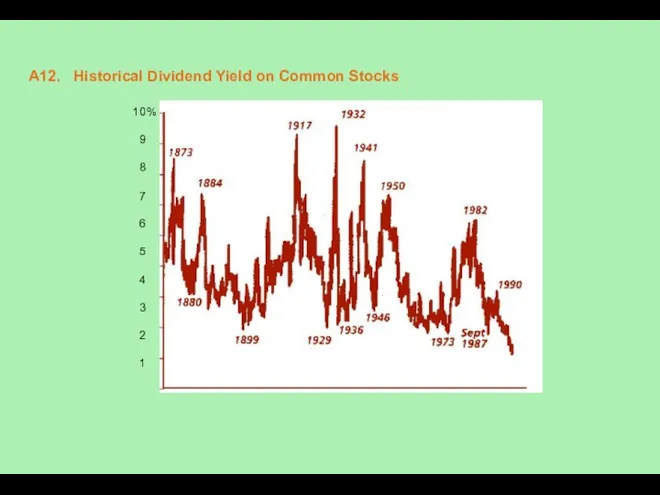

A12. Historical Dividend Yield on Common Stocks

10%

9

8

7

6

5

4

3

A12. Historical Dividend Yield on Common Stocks

10%

9

8

7

6

5

4

3

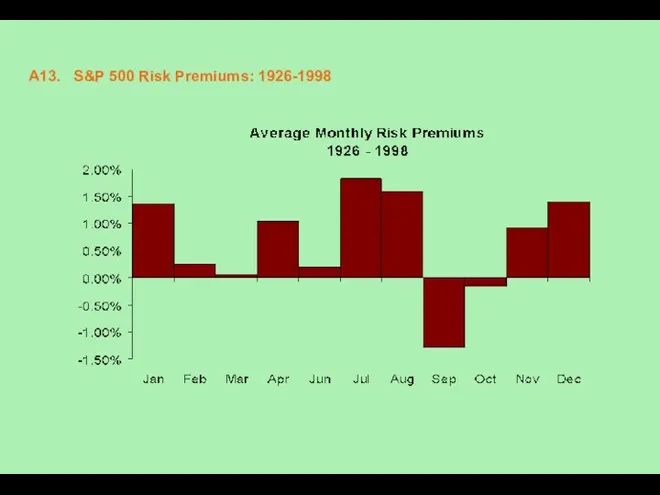

A13. S&P 500 Risk Premiums: 1926-1998

A13. S&P 500 Risk Premiums: 1926-1998

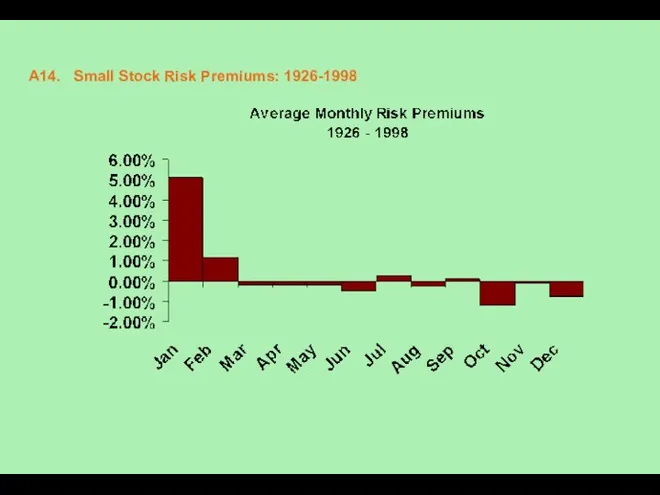

A14. Small Stock Risk Premiums: 1926-1998

A14. Small Stock Risk Premiums: 1926-1998

A15. Using Capital Market History

Now let’s use our knowledge of capital

A15. Using Capital Market History

Now let’s use our knowledge of capital

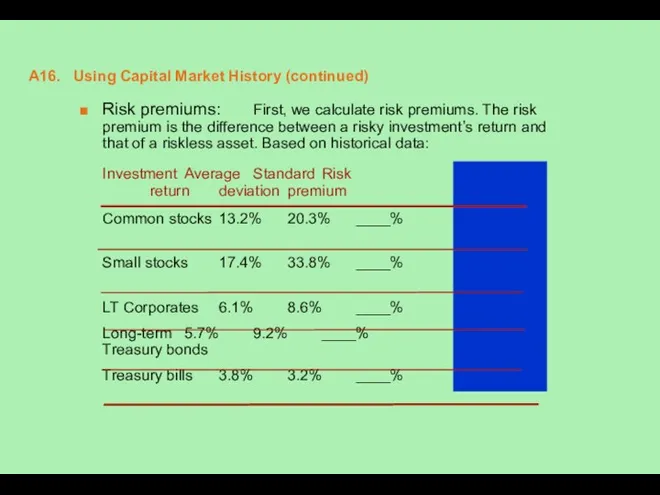

A16. Using Capital Market History (continued)

Risk premiums: First, we calculate risk

A16. Using Capital Market History (continued)

Risk premiums: First, we calculate risk

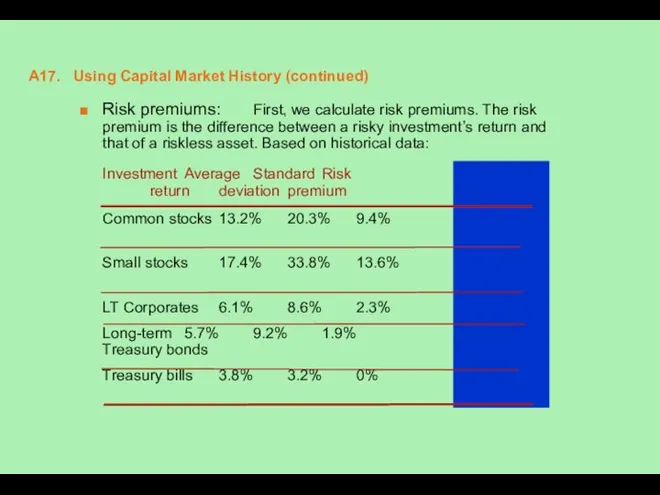

A17. Using Capital Market History (continued)

Risk premiums: First, we calculate risk

A17. Using Capital Market History (continued)

Risk premiums: First, we calculate risk

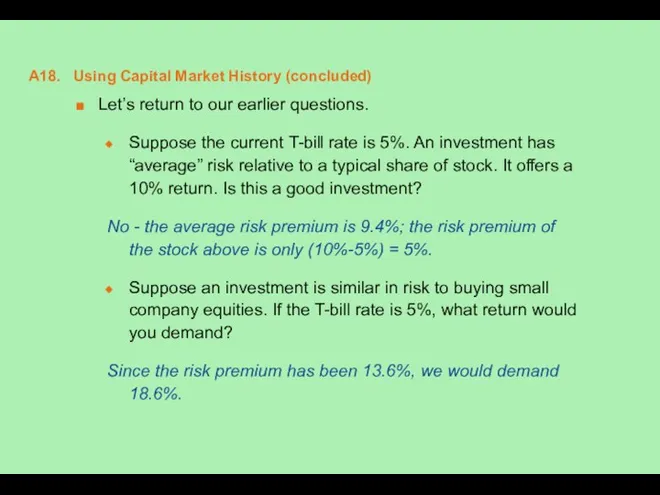

A18. Using Capital Market History (concluded)

Let’s return to our earlier questions.

Suppose

A18. Using Capital Market History (concluded)

Let’s return to our earlier questions.

Suppose

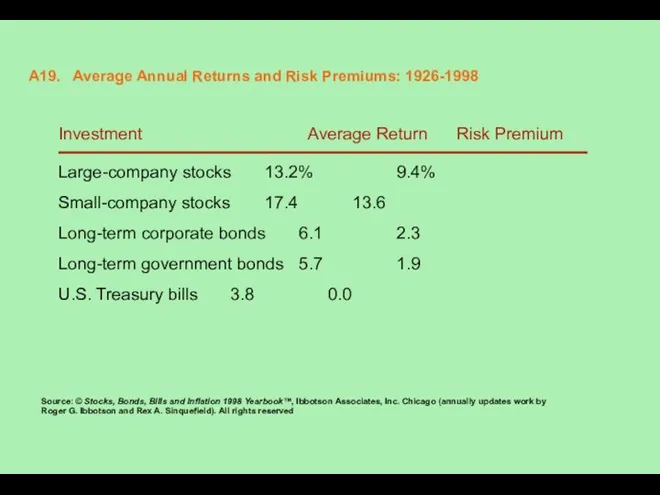

A19. Average Annual Returns and Risk Premiums: 1926-1998

Investment Average Return Risk

A19. Average Annual Returns and Risk Premiums: 1926-1998

Investment Average Return Risk

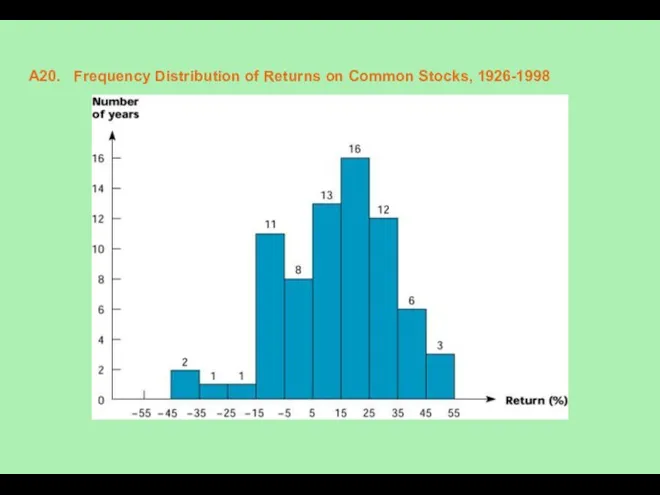

A20. Frequency Distribution of Returns on Common Stocks, 1926-1998

A20. Frequency Distribution of Returns on Common Stocks, 1926-1998

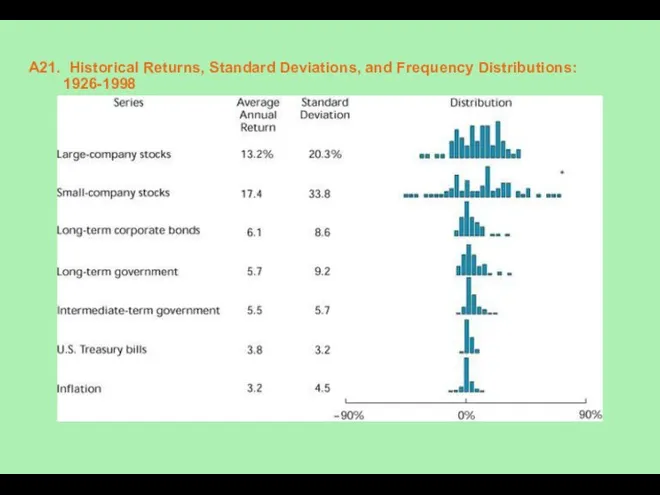

A21. Historical Returns, Standard Deviations, and Frequency Distributions:

1926-1998

A21. Historical Returns, Standard Deviations, and Frequency Distributions:

1926-1998

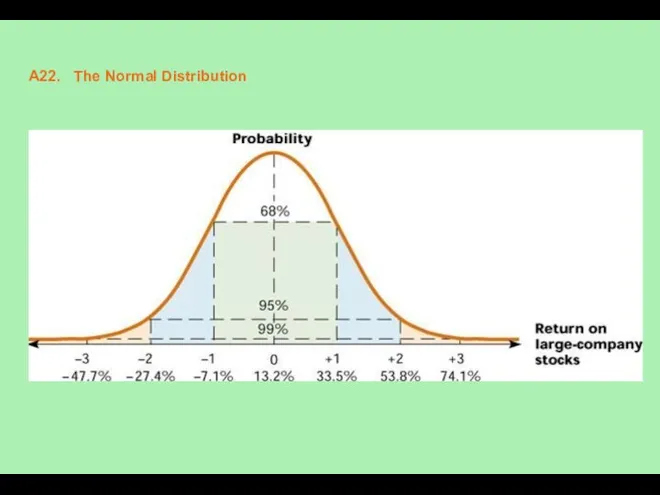

A22. The Normal Distribution

A22. The Normal Distribution

A23. Two Views on Market Efficiency

“ . . . in price

A23. Two Views on Market Efficiency

“ . . . in price

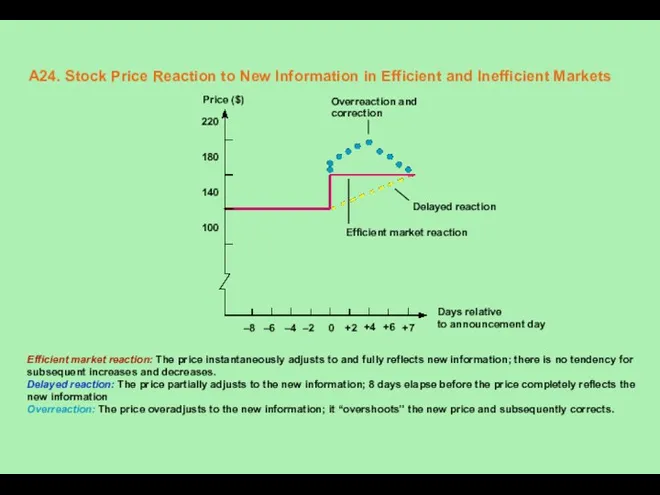

A24. Stock Price Reaction to New Information in Efficient and Inefficient

A24. Stock Price Reaction to New Information in Efficient and Inefficient

A25. A Quick Quiz

Here are three questions that should be easy

A25. A Quick Quiz

Here are three questions that should be easy

A26. Chapter 12 Quick Quiz (continued)

1. How are average annual returns

A26. Chapter 12 Quick Quiz (continued)

1. How are average annual returns

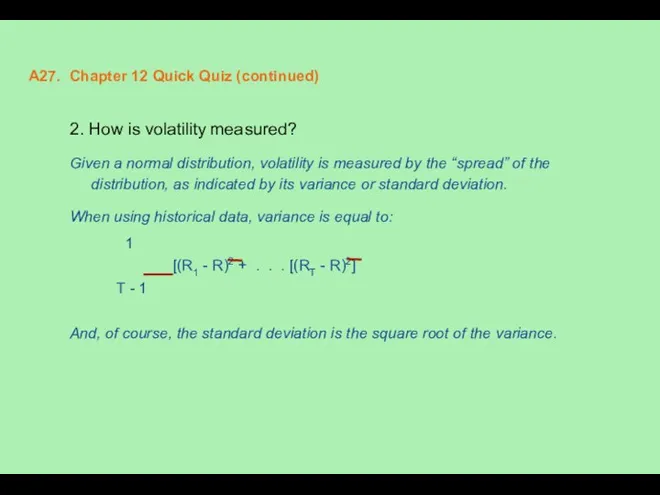

A27. Chapter 12 Quick Quiz (continued)

2. How is volatility measured?

Given a

A27. Chapter 12 Quick Quiz (continued)

2. How is volatility measured?

Given a

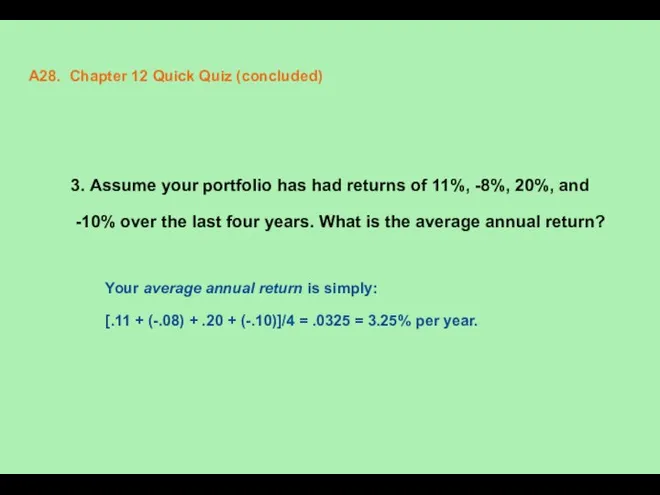

A28. Chapter 12 Quick Quiz (concluded)

3. Assume your portfolio has had

A28. Chapter 12 Quick Quiz (concluded)

3. Assume your portfolio has had

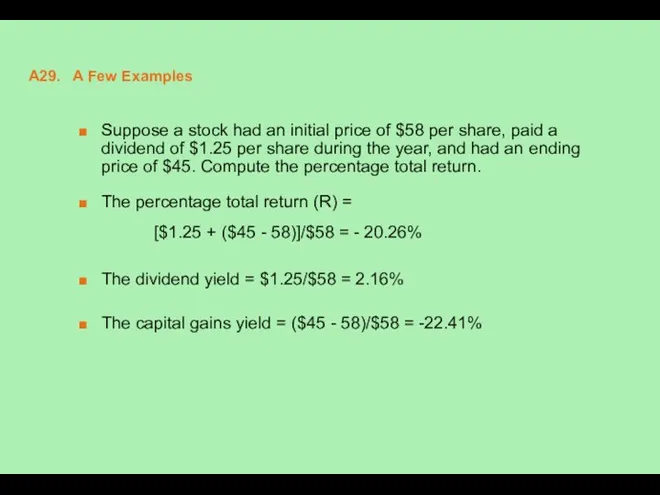

A29. A Few Examples

Suppose a stock had an initial price of

A29. A Few Examples

Suppose a stock had an initial price of

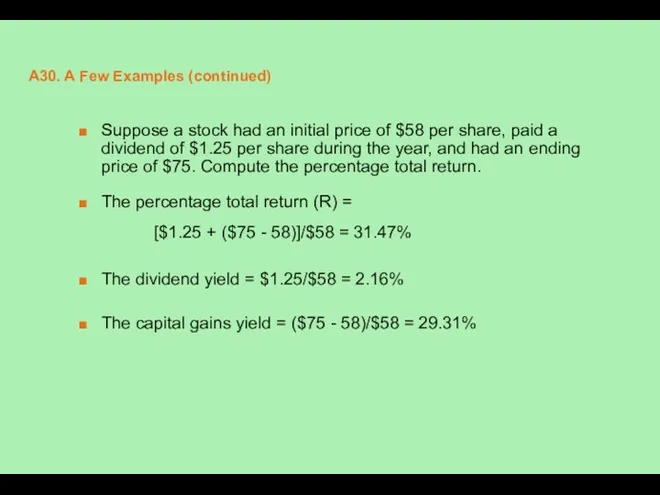

A30. A Few Examples (continued)

Suppose a stock had an initial price

A30. A Few Examples (continued)

Suppose a stock had an initial price

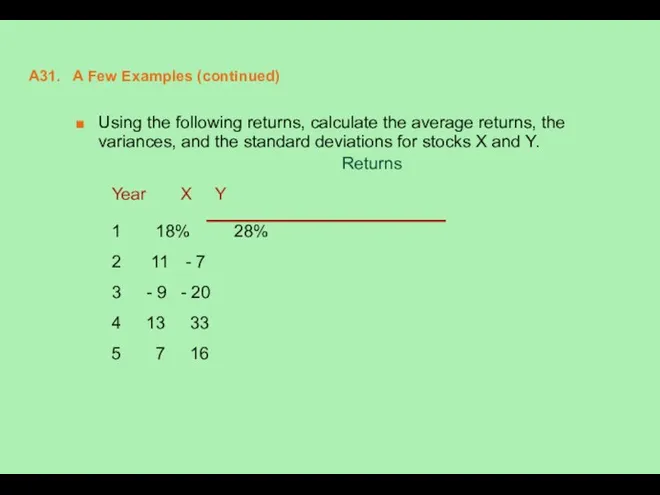

A31. A Few Examples (continued)

Using the following returns, calculate the average

A31. A Few Examples (continued)

Using the following returns, calculate the average

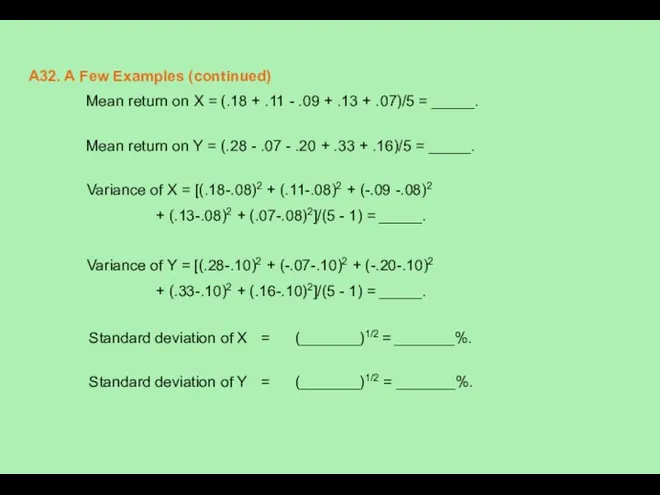

A32. A Few Examples (continued)

Mean return on X = (.18 +

A32. A Few Examples (continued)

Mean return on X = (.18 +

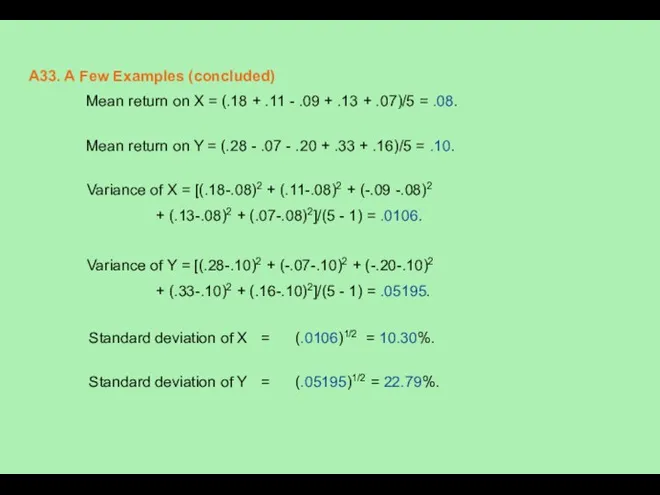

A33. A Few Examples (concluded)

Mean return on X = (.18 +

A33. A Few Examples (concluded)

Mean return on X = (.18 +

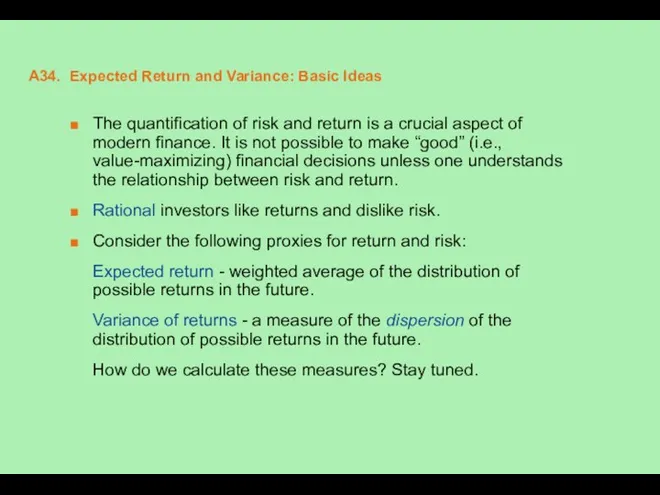

A34. Expected Return and Variance: Basic Ideas

The quantification of risk and

A34. Expected Return and Variance: Basic Ideas

The quantification of risk and

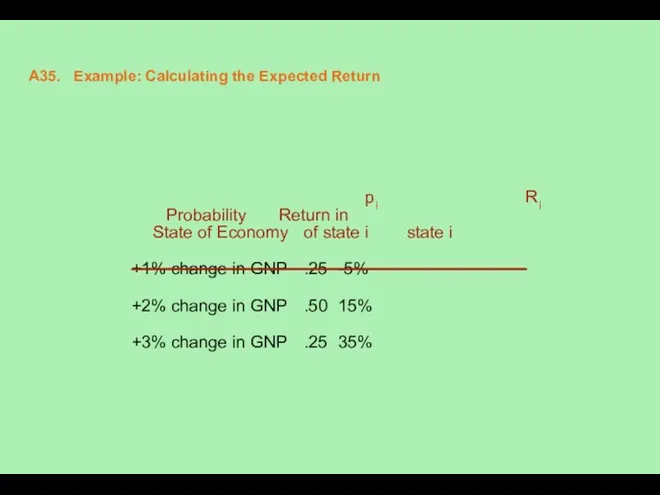

A35. Example: Calculating the Expected Return

pi Ri

Probability Return in

State of Economy of

A35. Example: Calculating the Expected Return

pi Ri

Probability Return in

State of Economy of

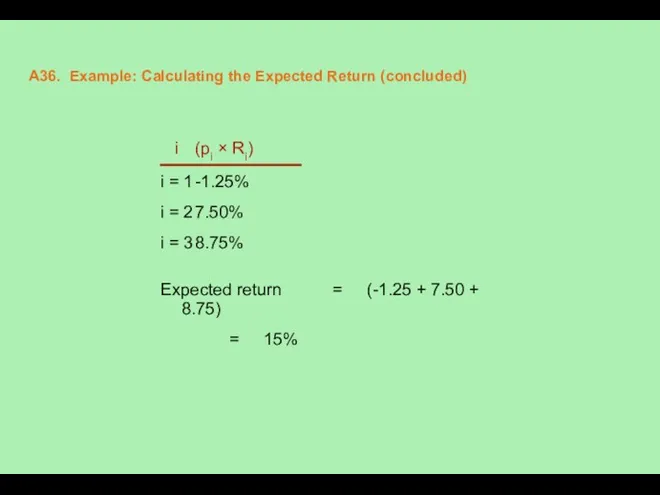

A36. Example: Calculating the Expected Return (concluded)

i (pi × Ri)

i =

A36. Example: Calculating the Expected Return (concluded)

i (pi × Ri)

i =

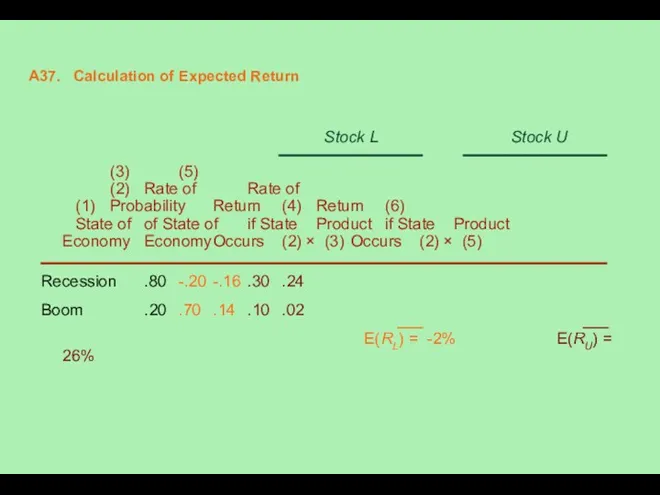

A37. Calculation of Expected Return

Stock L Stock U

(3) (5)

(2) Rate

A37. Calculation of Expected Return

Stock L Stock U

(3) (5)

(2) Rate

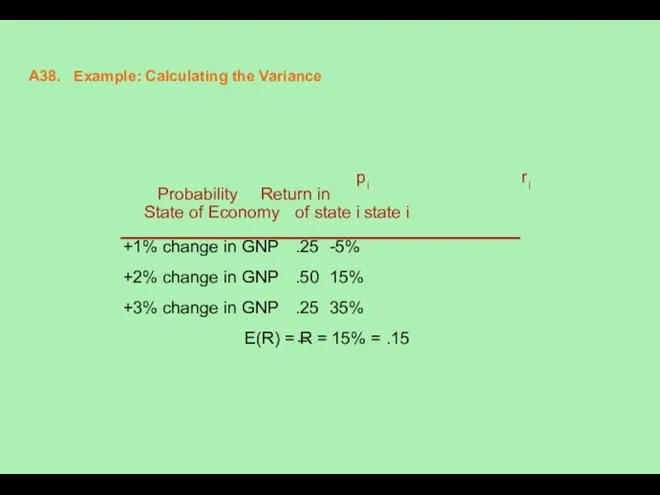

A38. Example: Calculating the Variance

pi ri

Probability Return in

State of Economy of

A38. Example: Calculating the Variance

pi ri

Probability Return in

State of Economy of

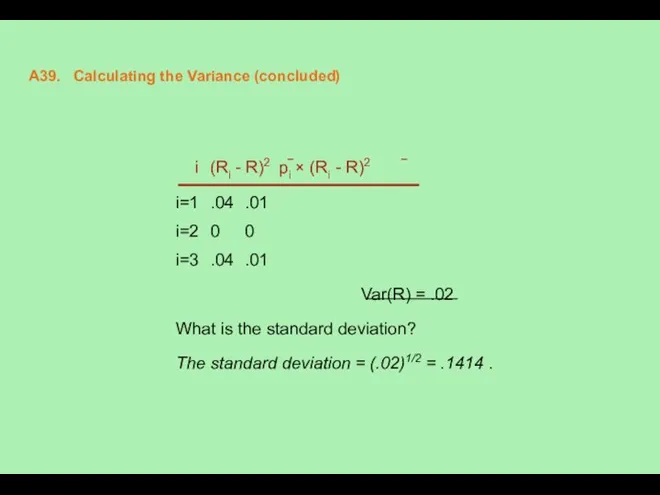

A39. Calculating the Variance (concluded)

i (Ri - R)2 pi × (Ri

A39. Calculating the Variance (concluded)

i (Ri - R)2 pi × (Ri

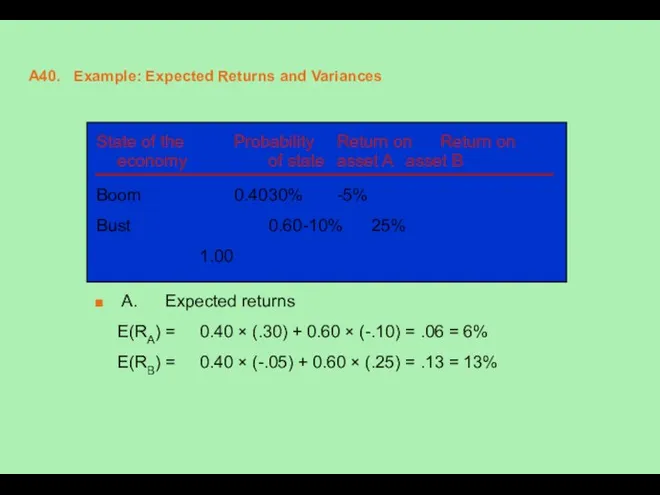

A40. Example: Expected Returns and Variances

State of the Probability Return on Return on

economy of state asset

A40. Example: Expected Returns and Variances

State of the Probability Return on Return on economy of state asset

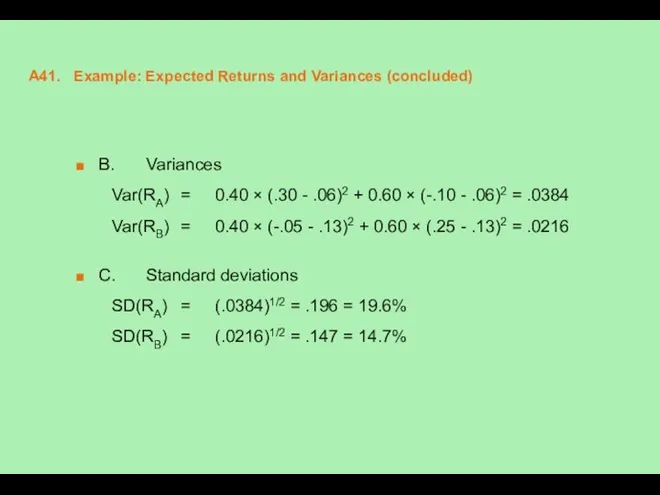

A41. Example: Expected Returns and Variances (concluded)

B. Variances

Var(RA) = 0.40 ×

A41. Example: Expected Returns and Variances (concluded)

B. Variances

Var(RA) = 0.40 ×

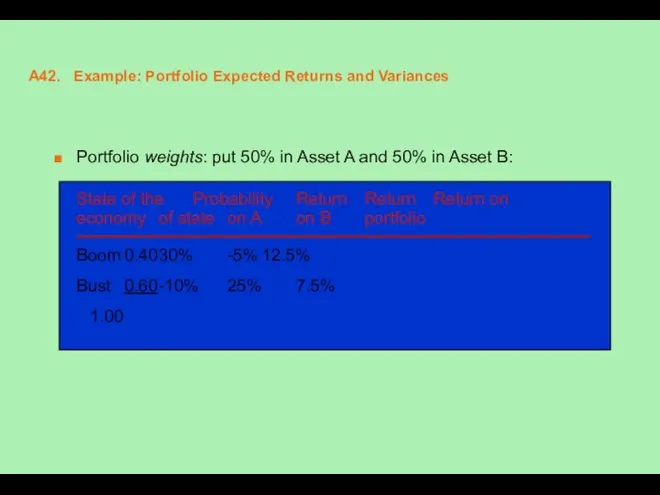

A42. Example: Portfolio Expected Returns and Variances

Portfolio weights: put 50% in

A42. Example: Portfolio Expected Returns and Variances

Portfolio weights: put 50% in

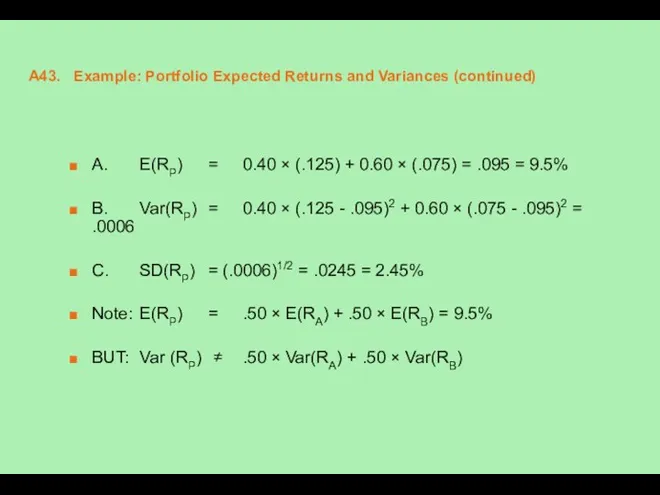

A43. Example: Portfolio Expected Returns and Variances (continued)

A. E(RP) = 0.40 ×

A43. Example: Portfolio Expected Returns and Variances (continued)

A. E(RP) = 0.40 ×

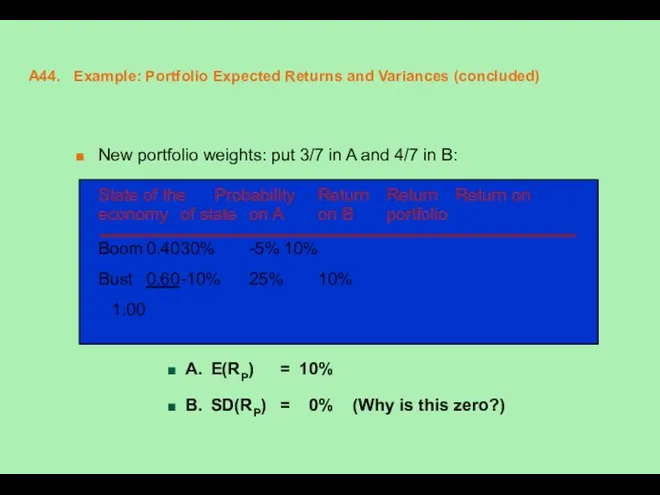

A44. Example: Portfolio Expected Returns and Variances (concluded)

New portfolio weights: put

A44. Example: Portfolio Expected Returns and Variances (concluded)

New portfolio weights: put

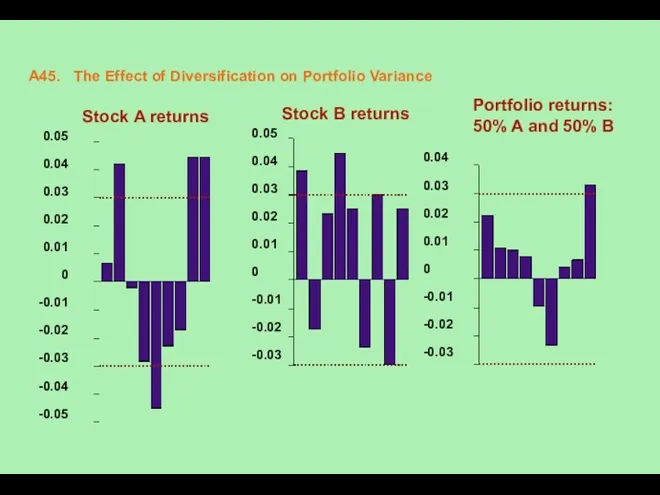

A45. The Effect of Diversification on Portfolio Variance

Stock A returns

0.05

0.04

0.03

0.02

0.01

0

-0.01

-0.02

-0.03

-0.04

-0.05

0.05

0.04

0.03

0.02

0.01

0

-0.01

-0.02

-0.03

Stock B

A45. The Effect of Diversification on Portfolio Variance

Stock A returns

0.05

0.04

0.03

0.02

0.01

0

-0.01

-0.02

-0.03

-0.04

-0.05

0.05

0.04

0.03

0.02

0.01

0

-0.01

-0.02

-0.03

Stock B

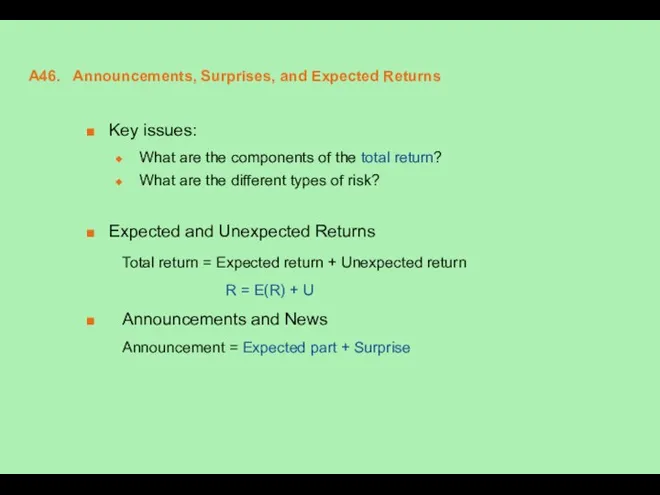

A46. Announcements, Surprises, and Expected Returns

Key issues:

What are the components of

A46. Announcements, Surprises, and Expected Returns

Key issues:

What are the components of

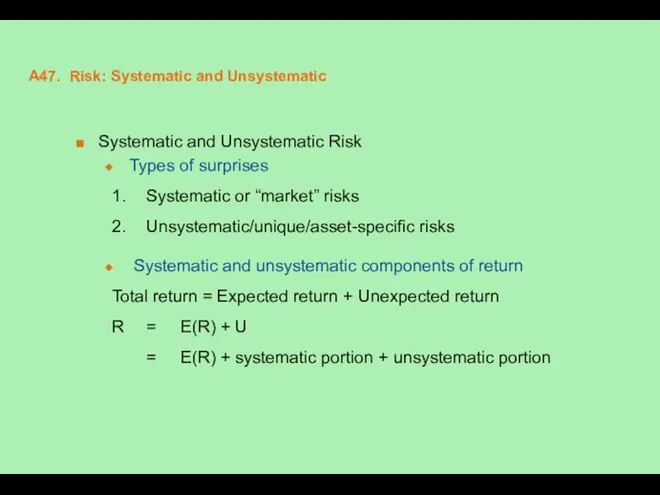

A47. Risk: Systematic and Unsystematic

Systematic and Unsystematic Risk

Types of surprises

1. Systematic

A47. Risk: Systematic and Unsystematic

Systematic and Unsystematic Risk

Types of surprises

1. Systematic

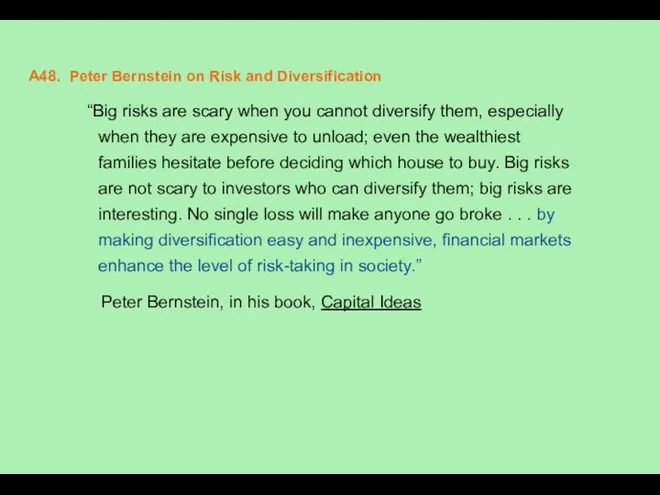

A48. Peter Bernstein on Risk and Diversification

“Big risks are scary

A48. Peter Bernstein on Risk and Diversification

“Big risks are scary

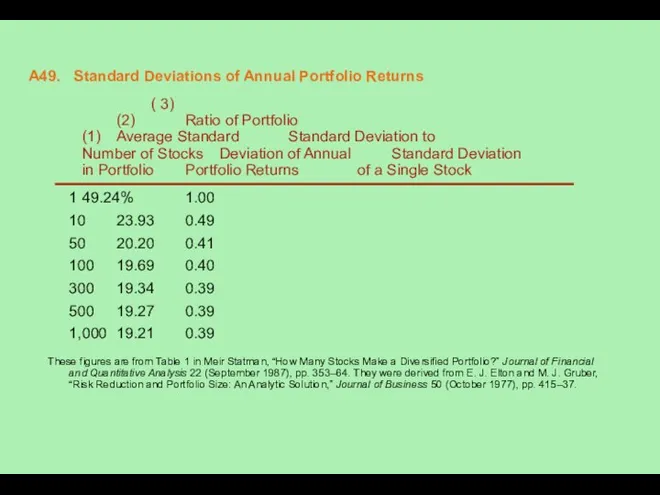

A49. Standard Deviations of Annual Portfolio Returns

( 3)

(2) Ratio of

A49. Standard Deviations of Annual Portfolio Returns

( 3) (2) Ratio of

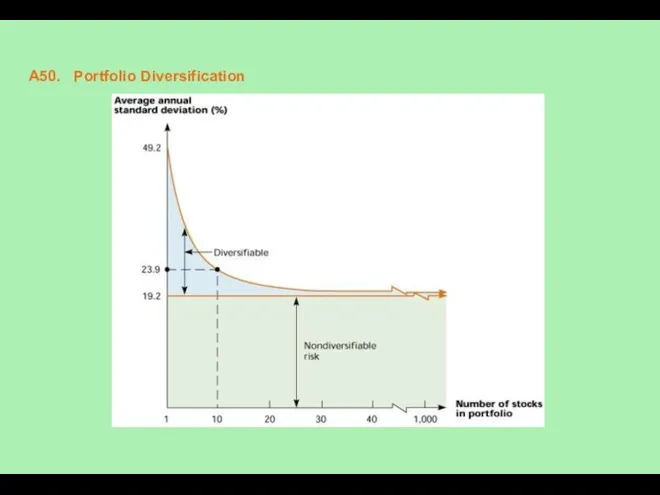

A50. Portfolio Diversification

A50. Portfolio Diversification

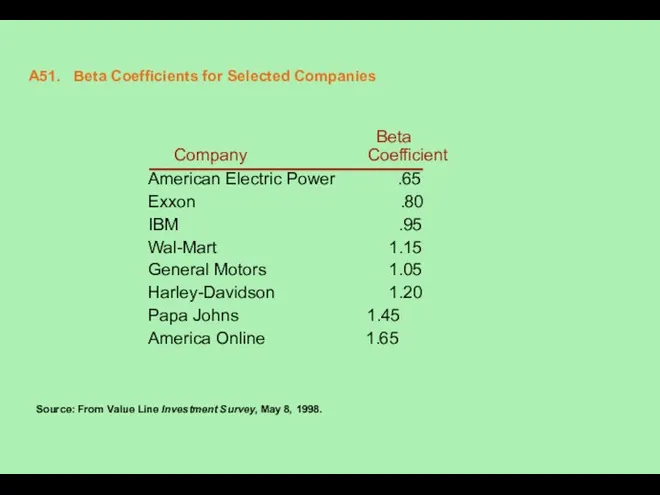

A51. Beta Coefficients for Selected Companies

Beta Company Coefficient

American Electric Power

A51. Beta Coefficients for Selected Companies

Beta Company Coefficient

American Electric Power

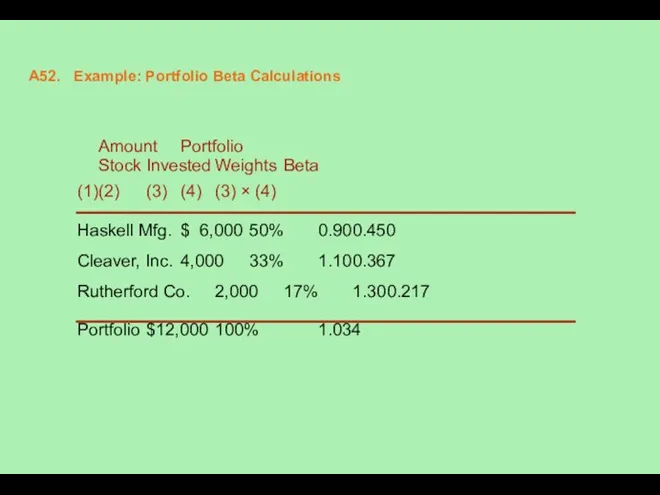

A52. Example: Portfolio Beta Calculations

Amount Portfolio

Stock Invested Weights Beta

(1) (2) (3) (4) (3) × (4)

Haskell Mfg. $ 6,000 50% 0.90 0.450

Cleaver,

A52. Example: Portfolio Beta Calculations

Amount Portfolio

Stock Invested Weights Beta

(1) (2) (3) (4) (3) × (4)

Haskell Mfg. $ 6,000 50% 0.90 0.450

Cleaver,

A53. Example: Portfolio Expected Returns and Betas

Assume you wish to hold

A53. Example: Portfolio Expected Returns and Betas

Assume you wish to hold

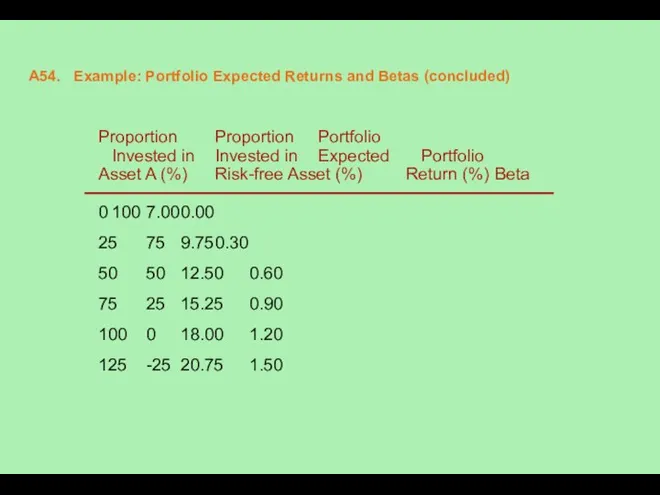

A54. Example: Portfolio Expected Returns and Betas (concluded)

Proportion Proportion Portfolio

Invested

A54. Example: Portfolio Expected Returns and Betas (concluded)

Proportion Proportion Portfolio Invested

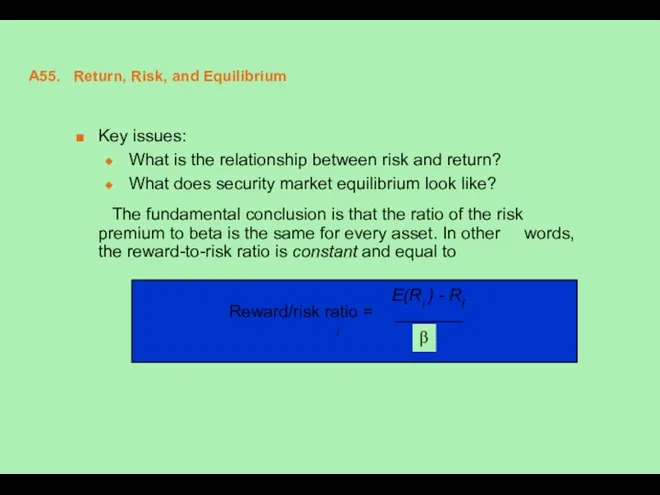

A55. Return, Risk, and Equilibrium

Key issues:

What is the relationship between risk

A55. Return, Risk, and Equilibrium

Key issues:

What is the relationship between risk

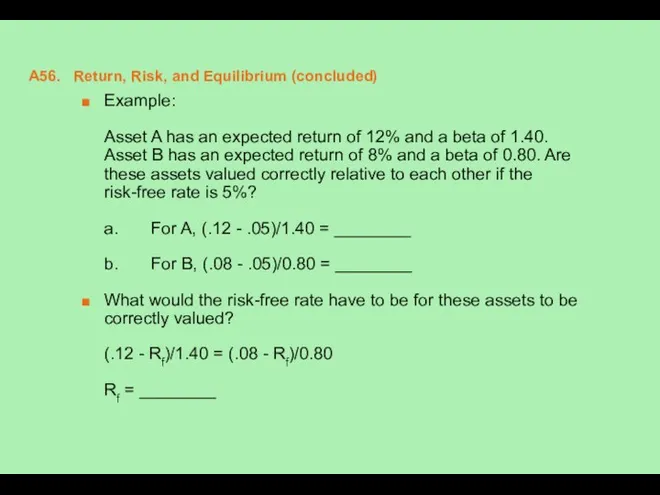

A56. Return, Risk, and Equilibrium (concluded)

Example:

Asset A has an expected

A56. Return, Risk, and Equilibrium (concluded)

Example:

Asset A has an expected

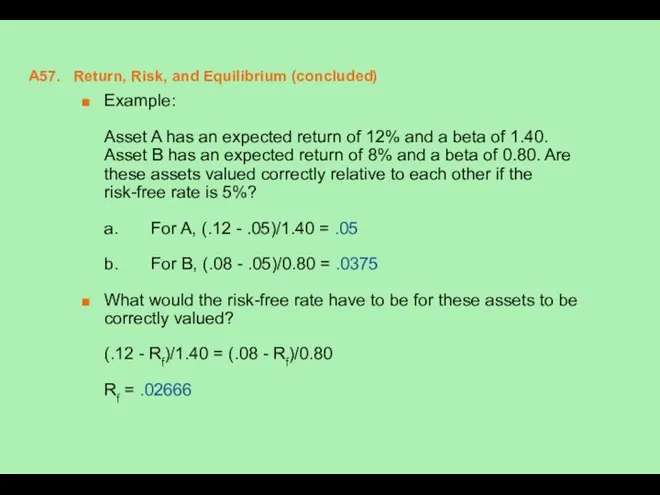

A57. Return, Risk, and Equilibrium (concluded)

Example:

Asset A has an expected

A57. Return, Risk, and Equilibrium (concluded)

Example:

Asset A has an expected

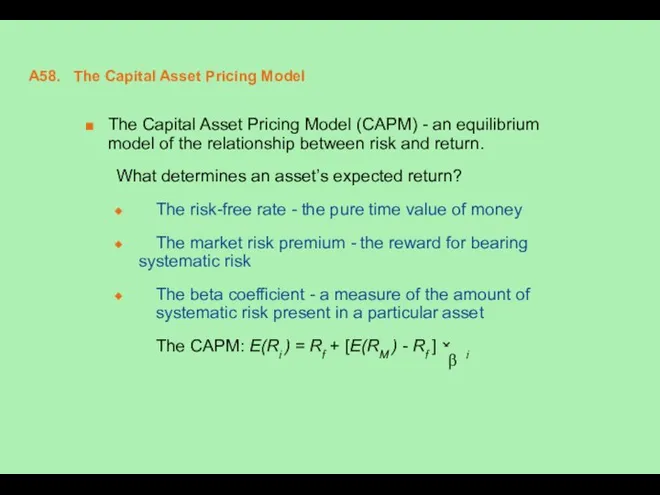

A58. The Capital Asset Pricing Model

The Capital Asset Pricing Model (CAPM)

A58. The Capital Asset Pricing Model

The Capital Asset Pricing Model (CAPM)

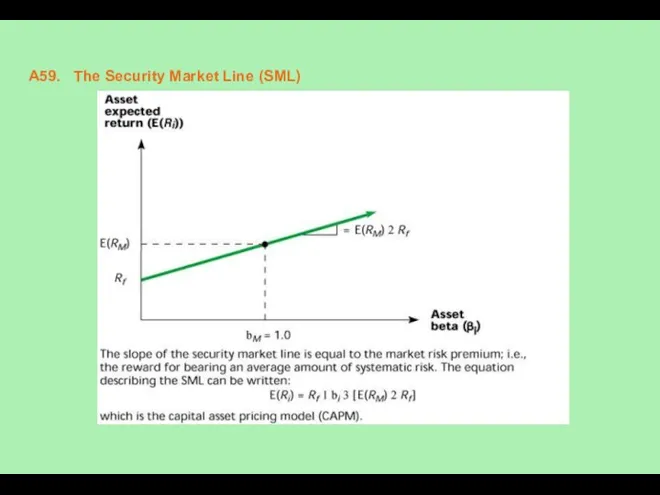

A59. The Security Market Line (SML)

A59. The Security Market Line (SML)

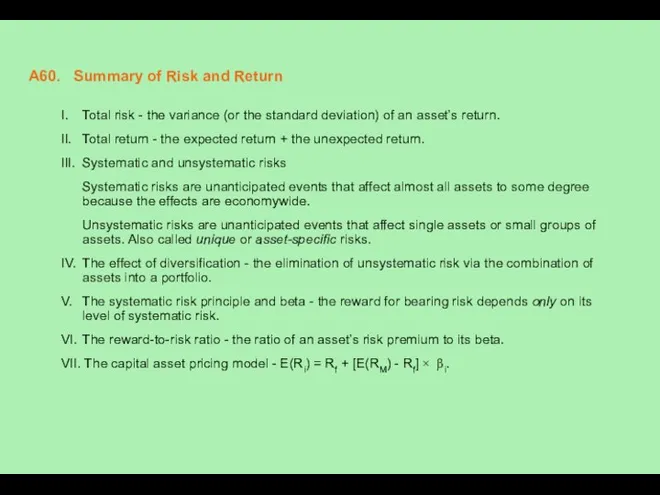

A60. Summary of Risk and Return

I. Total risk - the variance (or

A60. Summary of Risk and Return

I. Total risk - the variance (or

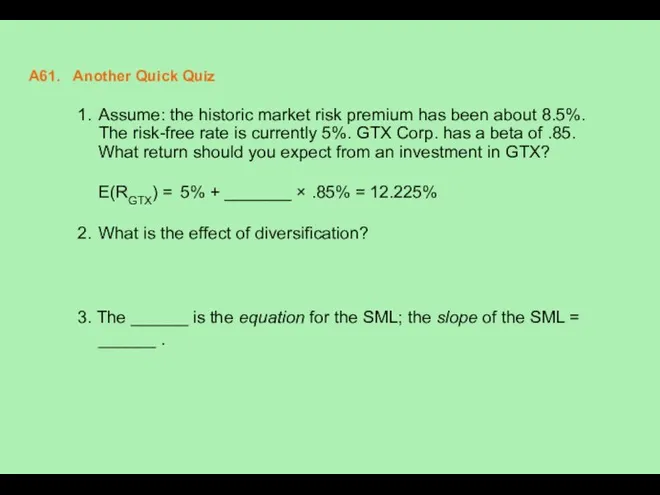

A61. Another Quick Quiz

1. Assume: the historic market risk premium has been

A61. Another Quick Quiz

1. Assume: the historic market risk premium has been

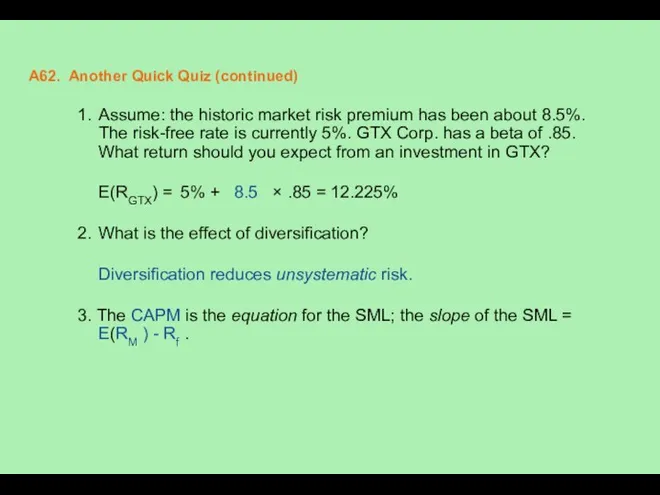

A62. Another Quick Quiz (continued)

1. Assume: the historic market risk premium has

A62. Another Quick Quiz (continued)

1. Assume: the historic market risk premium has

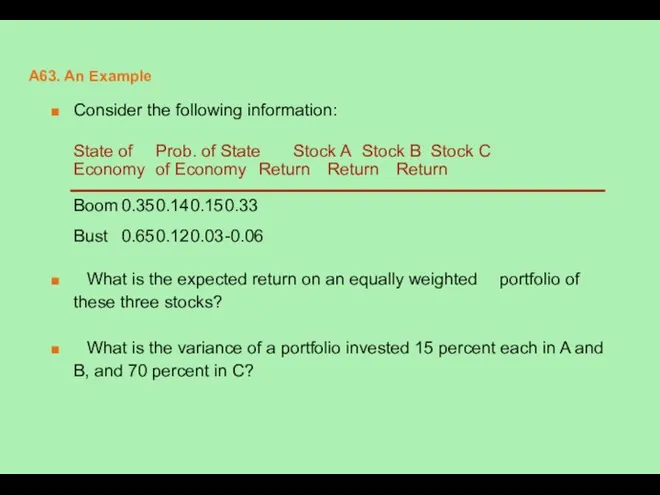

A63. An Example

Consider the following information:

State of Prob. of State Stock A Stock

A63. An Example

Consider the following information:

State of Prob. of State Stock A Stock

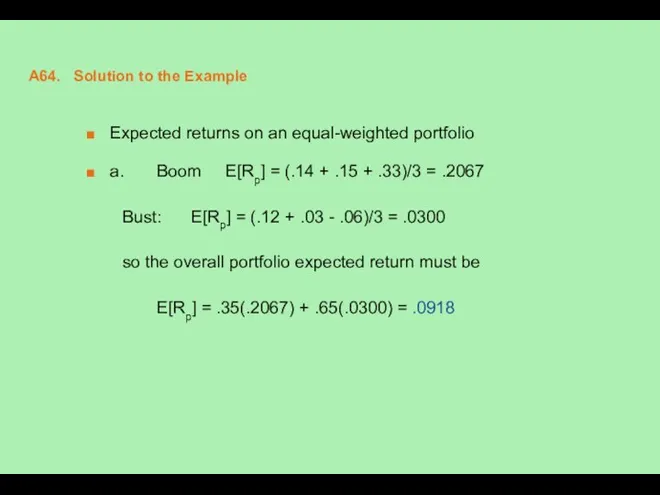

A64. Solution to the Example

Expected returns on an equal-weighted portfolio

a. Boom E[Rp] =

A64. Solution to the Example

Expected returns on an equal-weighted portfolio

a. Boom E[Rp] =

![A65. Solution to the Example (continued) b. Boom: E[Rp] =](/_ipx/f_webp&q_80&fit_contain&s_1440x1080/imagesDir/jpg/359583/slide-64.jpg)

A65. Solution to the Example (continued)

b. Boom: E[Rp] = __ (.14) + .15(.15)

A65. Solution to the Example (continued)

b. Boom: E[Rp] = __ (.14) + .15(.15)

![A66. Solution to the Example (concluded) b. Boom: E[Rp] =](/_ipx/f_webp&q_80&fit_contain&s_1440x1080/imagesDir/jpg/359583/slide-65.jpg)

A66. Solution to the Example (concluded)

b. Boom: E[Rp] = .15(.14) + .15(.15) +

A66. Solution to the Example (concluded)

b. Boom: E[Rp] = .15(.14) + .15(.15) +

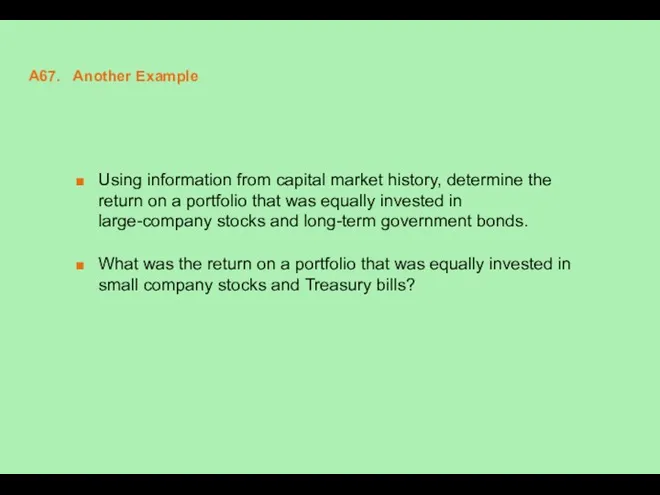

A67. Another Example

Using information from capital market history, determine the return

A67. Another Example

Using information from capital market history, determine the return

Выпускная работа. Обоснование перспектив развития предприятия Фортуна Крым Трейд

Выпускная работа. Обоснование перспектив развития предприятия Фортуна Крым Трейд Ценообразование на монополизированном рынке

Ценообразование на монополизированном рынке Безработица. Трудоспособное и нетрудоспособное население

Безработица. Трудоспособное и нетрудоспособное население Методы ABC, XYZ. Задача на знание метода ABC

Методы ABC, XYZ. Задача на знание метода ABC Макроэкономика. Сущность макроэкономики, ее основные цели

Макроэкономика. Сущность макроэкономики, ее основные цели Економічна теорія як наука

Економічна теорія як наука Государственные финансы

Государственные финансы Märkte für Produktionsfaktoren

Märkte für Produktionsfaktoren Общая характеристика направления менеджмент и ее профилей. (Раздел 1)

Общая характеристика направления менеджмент и ее профилей. (Раздел 1) Денежно-кредитная политика государства

Денежно-кредитная политика государства Трудовые ресурсы предприятия: основные понятия, структура, показатели

Трудовые ресурсы предприятия: основные понятия, структура, показатели Организация и проведение массовой оценки объектов недвижимости

Организация и проведение массовой оценки объектов недвижимости Interaction of logical and nominal meanings

Interaction of logical and nominal meanings Научно-техническая безопасность и экономический рост

Научно-техническая безопасность и экономический рост Теоретичні засади податків

Теоретичні засади податків Собственность. Предпринимательство. Издержки производства. Прибыль

Собственность. Предпринимательство. Издержки производства. Прибыль Контроль за соблюдением норм и правил охраны труда. (Лекция 2)

Контроль за соблюдением норм и правил охраны труда. (Лекция 2) Задачи по экономике

Задачи по экономике Экономическая природа фирмы: основные формы деловых предприятий

Экономическая природа фирмы: основные формы деловых предприятий Нематериальные активы (НМА) организации

Нематериальные активы (НМА) организации Экономика. Главные вопросы экономики

Экономика. Главные вопросы экономики Нобелевские премии по экономике

Нобелевские премии по экономике Введение в логистику

Введение в логистику Основные производственные фонды. Понятие и классификация основных фондов

Основные производственные фонды. Понятие и классификация основных фондов Өндіріс факторларының арақатынасы теориясын эмпирикалық тексеру және олардың шектеулілігі мәселесі

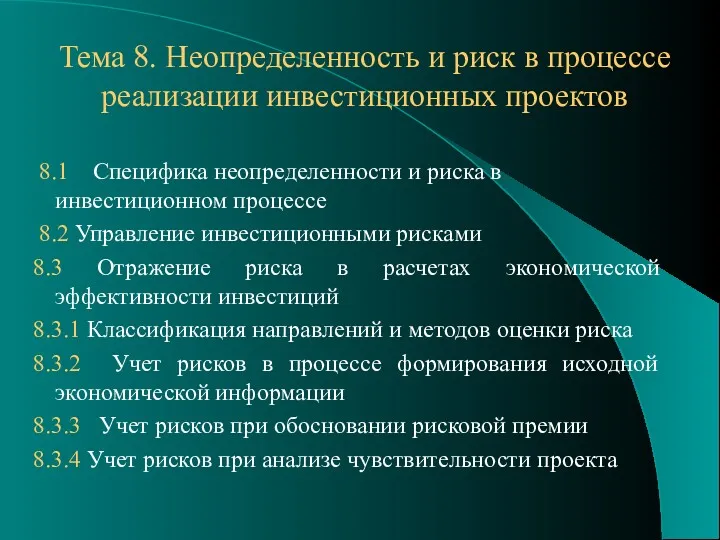

Өндіріс факторларының арақатынасы теориясын эмпирикалық тексеру және олардың шектеулілігі мәселесі Неопределенность и риск в процессе реализации инвестиционных проектов

Неопределенность и риск в процессе реализации инвестиционных проектов Неолиберализм. Сущность и особенности неолиберализма

Неолиберализм. Сущность и особенности неолиберализма Комплексный план развития Куединского муниципального округа Пермского края

Комплексный план развития Куединского муниципального округа Пермского края