- National Income: Where It Comes From and Where It Goes

Содержание

- 2. IN THIS CHAPTER, YOU WILL LEARN: What determines the economy’s total output/ income How the prices

- 3. Outline of model CHAPTER 3 National Income 2 A closed economy, market-clearing model Supply side factor

- 4. Factors of production CHAPTER 3 National Income 3 K = capital: tools, machines, and structures used

- 5. The production function: Y = F (K , L) CHAPTER 3 National Income 4 Shows how

- 6. Returns to scale: a review CHAPTER 3 National Income 5 Initially Y1 = F (K1 ,

- 7. Returns to scale: Example 1 CHAPTER 3 National Income 6 KL (zK)(zL) F(K,L) = F(zK,zL) =

- 8. Returns to scale: Example 2 CHAPTER 3 National Income 7 F(K,L) = K 2 + L2

- 9. NOW YOU TRY 8 Determine whether each of these production functions has constant, decreasing, or increasing

- 10. NOW YOU TRY 9 L F (K,L) = K 2 zL F (zK, zL) = (zK

- 11. NOW YOU TRY F (K,L) = K + L F (zK, zL) = zK + zL

- 12. Assumptions CHAPTER 3 National Income 11 Technology is fixed. The economy’s supplies of capital and labor

- 13. Determining GDP CHAPTER 3 National Income 12 Output is determined by the fixed factor supplies and

- 14. The distribution of national income CHAPTER 3 National Income 13 determined by factor prices, the prices

- 15. Notation CHAPTER 3 National Income 14 W = nominal wage R = nominal rental rate P

- 16. How factor prices are determined CHAPTER 3 National Income 15 Factor prices are determined by supply

- 17. Demand for labor CHAPTER 3 National Income 16 Assume markets are competitive: each firm takes W,

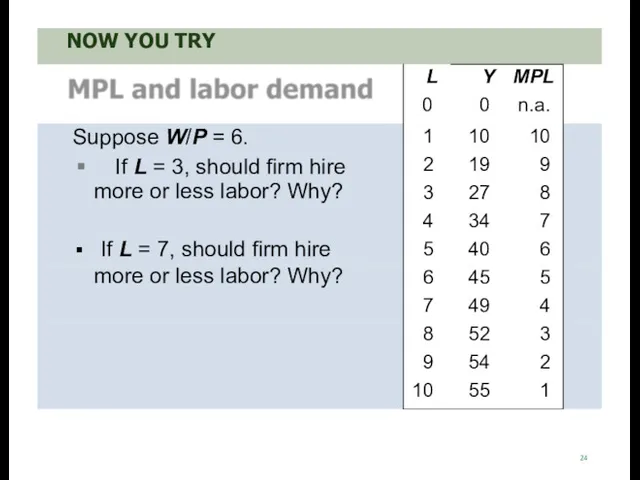

- 18. Marginal product of labor (MPL ) CHAPTER 3 National Income 17 Definition: The extra output the

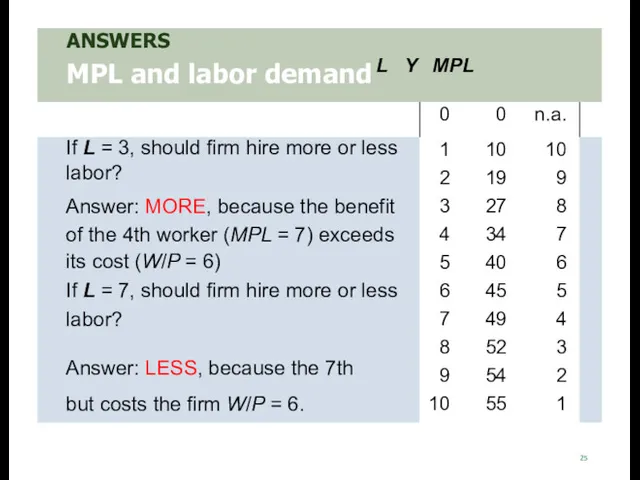

- 19. NOW YOU TRY Compute & graph MPL 18 Determine MPL at each value of L. Graph

- 20. ANSWERS Compute & graph MPL 19 MPL (units of output) Marginal Product of Labor 12 10

- 21. Y output MPL and the production function CHAPTER 3 National Income 20 L labor F (K

- 22. Diminishing marginal returns CHAPTER 3 National Income 21 As one input is increased (holding other inputs

- 23. NOW YOU TRY Identifying diminishing returns 22 Which of these production functions have diminishing marginal returns

- 24. ANSWERS Identifying diminishing returns 23 a) F (K,L) = 2K + 15L No, MPL = 15

- 25. 24

- 26. worker adds MPL = 4 units of output 25

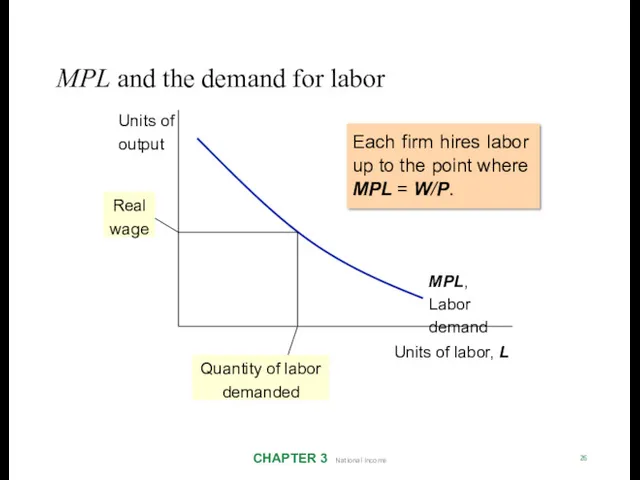

- 27. MPL and the demand for labor CHAPTER 3 National Income 26 Each firm hires labor up

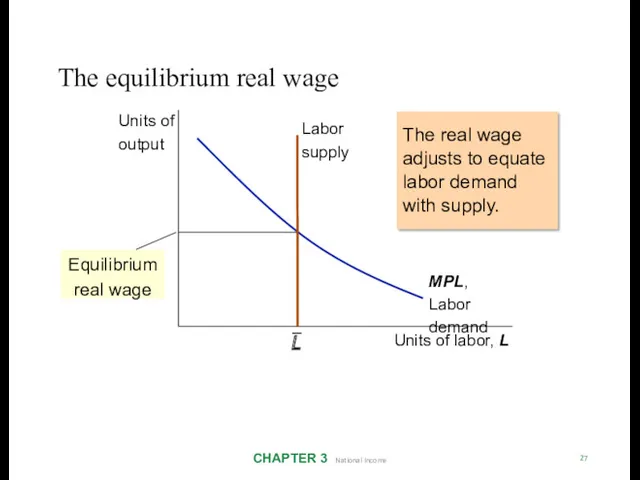

- 28. The equilibrium real wage CHAPTER 3 National Income 27 The real wage adjusts to equate labor

- 29. Determining the rental rate CHAPTER 3 National Income 28 We have just seen that MPL =

- 30. The equilibrium real rental rate CHAPTER 3 National Income 29 The real rental rate adjusts to

- 31. The neoclassical theory of distribution CHAPTER 3 National Income 30 States that each factor input is

- 32. How income is distributed to L and K CHAPTER 3 National Income 31 Total labor income

- 33. How income is distributed to L and K CHAPTER 3 National Income 32

- 34. How income is distributed to L and K CHAPTER 3 National Income 33

- 35. How income is distributed to L and K CHAPTER 3 National Income 34

- 36. 0.1 0 0.2 0.3 0.4 0.7 0.6 0.5 0.8 0.9 1 1960 1965 1970 1975 1980

- 37. The Cobb-Douglas production function has constant factor shares: CHAPTER 3 National Income 36 The Cobb-Douglas production

- 38. The Cobb-Douglas production function CHAPTER 3 National Income 37 Each factor’s marginal product is proportional to

- 39. Labor productivity and wages CHAPTER 3 National Income 38 Theory: wages depend on labor productivity U.S.

- 40. The growing gap between rich & poor 0.30 0.45 0.50 0.40 Gini coefficient 0.35 Inequality has

- 41. Explanations for rising inequality CHAPTER 3 National Income 40 Rise in capital’s share of income, since

- 42. Outline of model CHAPTER 3 National Income 41 A closed economy, market-clearing model Supply side DONE

- 43. Demand for goods and services CHAPTER 3 National Income 42 Components of aggregate demand: C =

- 44. Consumption, C CHAPTER 3 National Income 43 Disposable income is total income minus total taxes: Y

- 45. The consumption function CHAPTER 3 National Income 44 C Y – T C (Y –T )

- 46. Investment, I CHAPTER 3 National Income 45 The investment function is I = I (r )

- 47. The investment function CHAPTER 3 National Income 46 r I (r ) I Spending on investment

- 48. Government spending, G CHAPTER 3 National Income 47 G = govt spending on goods and services

- 49. The market for goods & services CHAPTER 3 National Income 48 Aggregate demand: Aggregate supply: Equilibrium:

- 50. The loanable funds market CHAPTER 3 National Income 49 A simple supply–demand model of the financial

- 51. Demand for funds: investment CHAPTER 3 National Income 50 The demand for loanable funds . .

- 52. Loanable funds demand curve CHAPTER 3 National Income 51 r I (r ) I The investment

- 53. Supply of funds: saving CHAPTER 3 National Income 52 The supply of loanable funds comes from

- 54. Types of saving CHAPTER 3 National Income 53 Private saving Public saving = (Y – T

- 55. Notation: Δ = change in a variable CHAPTER 3 National Income 54 For any variable X,

- 56. NOW YOU TRY Calculate the change in saving 55 Suppose MPC = 0.8 and MPL =

- 57. ANSWERS Calculate the change in saving 56 ΔS = ΔY− ΔC−Δ G = Δ Y −

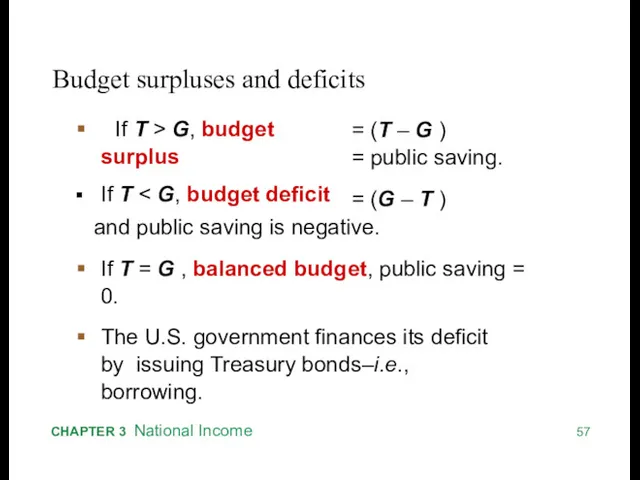

- 58. 57 CHAPTER 3 National Income Budget surpluses and deficits If T > G, budget surplus If

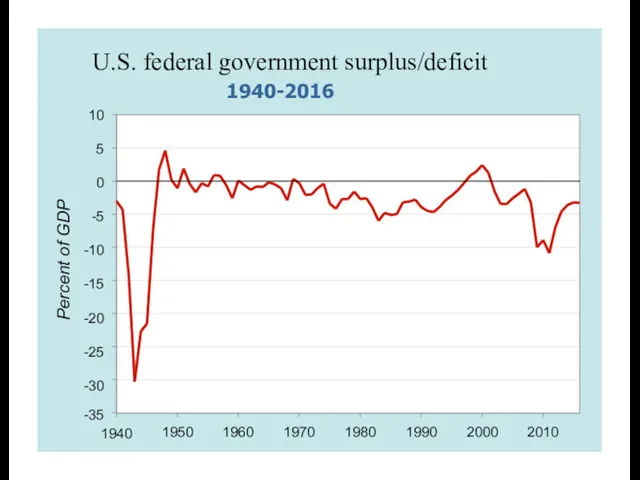

- 59. 1940-2016 Percent of GDP 10 5 0 -5 -10 -15 -20 -25 -30 -35 1940 1950

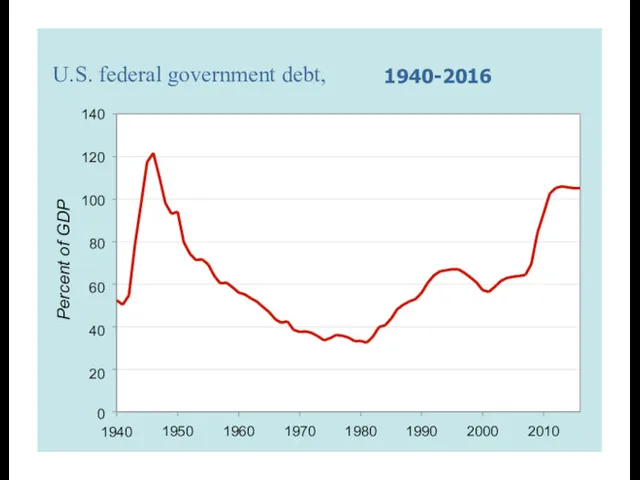

- 60. U.S. federal government debt, 1940-2016 Percent of GDP 140 120 100 80 60 40 20 0

- 61. Loanable funds supply curve CHAPTER 3 National Income 60 r S, I S =Y − C

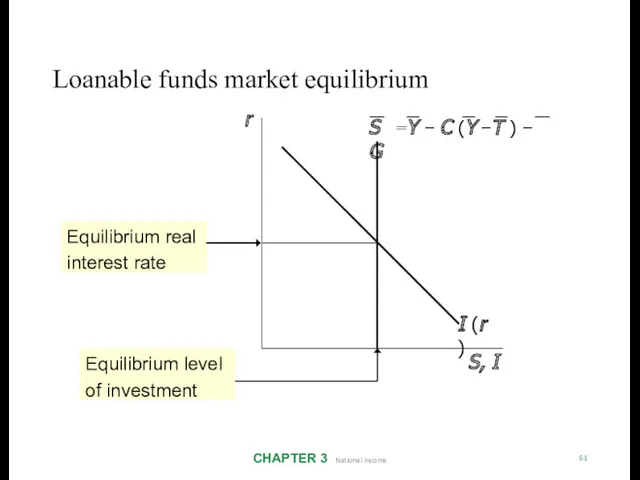

- 62. Loanable funds market equilibrium CHAPTER 3 National Income 61 r S, I I (r ) S

- 63. The special role of r CHAPTER 3 National Income 62 r adjusts to equilibrate the goods

- 64. Digression: mastering models CHAPTER 3 National Income 63 To master a model, be sure to know:

- 65. Mastering the loanable funds model CHAPTER 3 National Income 64 Things that shift the saving curve:

- 66. CASE STUDY: The Reagan Deficits CHAPTER 3 National Income 65 Reagan policies during early 1980s: increases

- 67. CASE STUDY: The Reagan Deficits CHAPTER 3 National Income 66 r S, I S 1 I

- 68. Are the data consistent with these results? CHAPTER 3 National Income 67 T–G, S, and I

- 69. NOW YOU TRY 68 Draw the diagram for the loanable funds model. Suppose the tax laws

- 70. Mastering the loanable funds model CHAPTER 3 National Income 69 (continued) Things that shift the investment

- 71. An increase in investment demand CHAPTER 3 National Income 79 An increase in desired investment… r

- 72. Saving and the interest rate CHAPTER 3 National Income 71 Why might saving depend on r

- 73. An increase in investment demand when saving depends on r CHAPTER 3 National Income 72 r

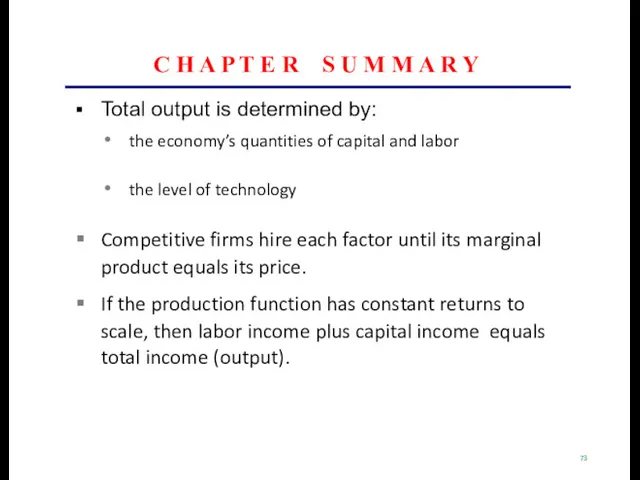

- 74. C H A P T E R S U M M A R Y Total output

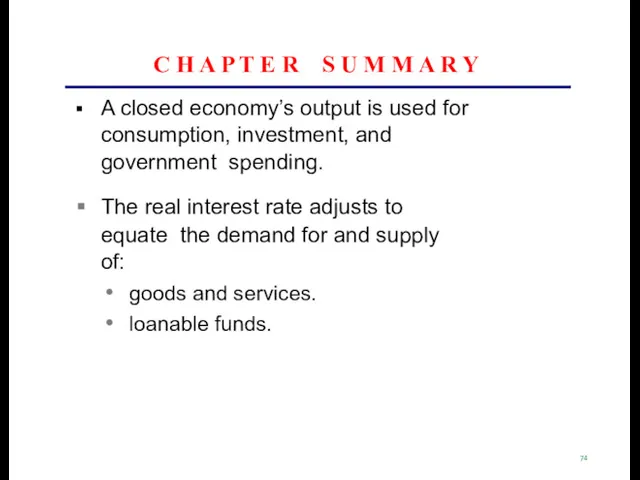

- 75. C H A P T E R S U M M A R Y A closed

- 77. Скачать презентацию

IN THIS CHAPTER, YOU WILL LEARN:

What determines the economy’s total output/

IN THIS CHAPTER, YOU WILL LEARN:

What determines the economy’s total output/

Outline of model

CHAPTER 3 National Income

2

A closed economy, market-clearing model

Supply side

factor

Outline of model

CHAPTER 3 National Income

2

A closed economy, market-clearing model

Supply side

factor

Factors of production

CHAPTER 3 National Income

3

K = capital:

tools, machines, and structures used

Factors of production

CHAPTER 3 National Income

3

K = capital:

tools, machines, and structures used

The production function: Y = F (K , L)

CHAPTER 3 National

The production function: Y = F (K , L)

CHAPTER 3 National

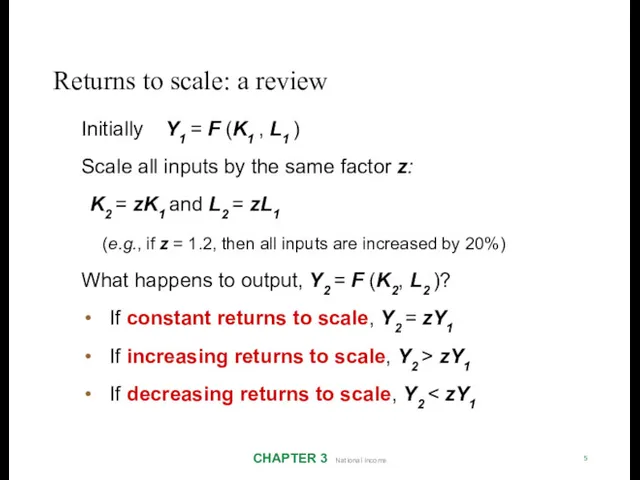

Returns to scale: a review

CHAPTER 3 National Income

5

Initially Y1 = F (K1

Returns to scale: a review

CHAPTER 3 National Income

5

Initially Y1 = F (K1

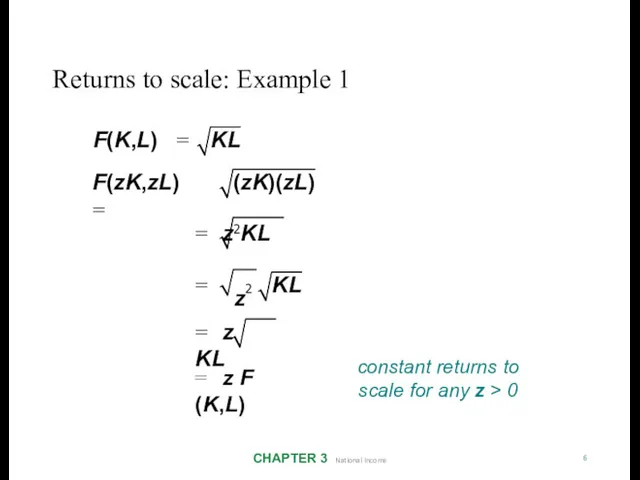

Returns to scale: Example 1

CHAPTER 3 National Income

6

KL

(zK)(zL)

F(K,L) =

F(zK,zL) =

= z2KL

KL

=

z2

= z KL

= z F (K,L)

constant returns

Returns to scale: Example 1

CHAPTER 3 National Income

6

KL

(zK)(zL)

F(K,L) =

F(zK,zL) =

= z2KL

KL

=

z2

= z KL

= z F (K,L)

constant returns

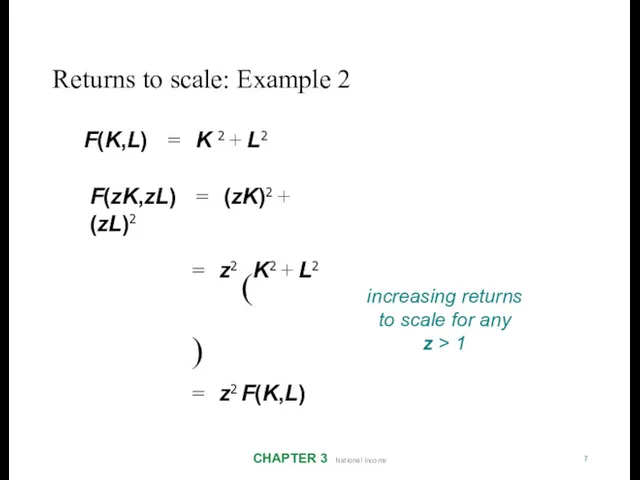

Returns to scale: Example 2

CHAPTER 3 National Income

7

F(K,L) = K 2 + L2

F(zK,zL) = (zK)2

Returns to scale: Example 2

CHAPTER 3 National Income

7

F(K,L) = K 2 + L2

F(zK,zL) = (zK)2

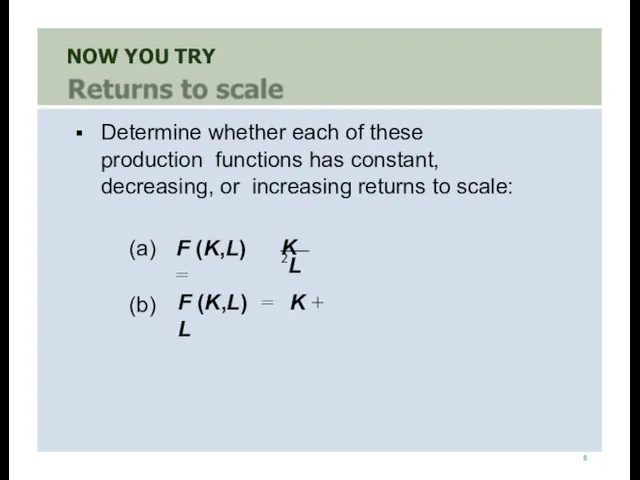

NOW YOU TRY

8

Determine whether each of these production functions has constant,

NOW YOU TRY

8

Determine whether each of these production functions has constant,

NOW YOU TRY

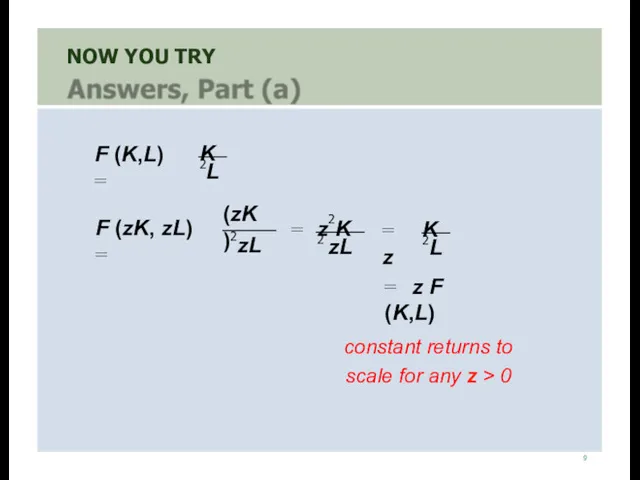

9

L

F (K,L) =

K 2

zL

F (zK, zL) =

(zK )2

zL

=

z2K 2

L

= z

K 2

= z F

NOW YOU TRY

9

L

F (K,L) =

K 2

zL

F (zK, zL) =

(zK )2

zL

=

z2K 2

L

= z

K 2

= z F

NOW YOU TRY

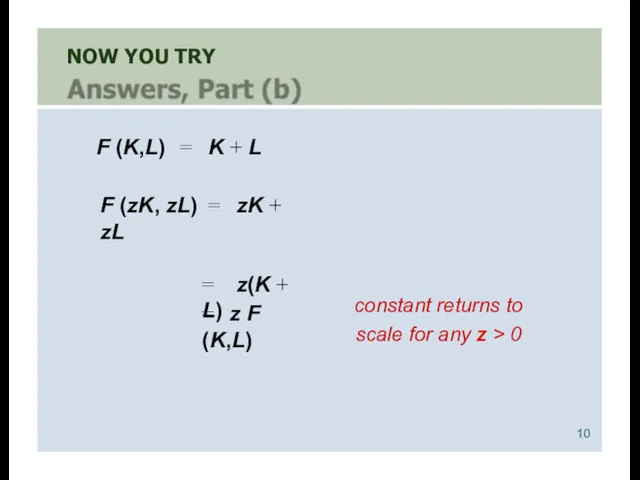

F (K,L) = K + L

F (zK, zL) = zK + zL

= z(K +

NOW YOU TRY

F (K,L) = K + L

F (zK, zL) = zK + zL

= z(K +

Assumptions

CHAPTER 3 National Income

11

Technology is fixed.

The economy’s supplies of capital and

Assumptions

CHAPTER 3 National Income

11

Technology is fixed.

The economy’s supplies of capital and

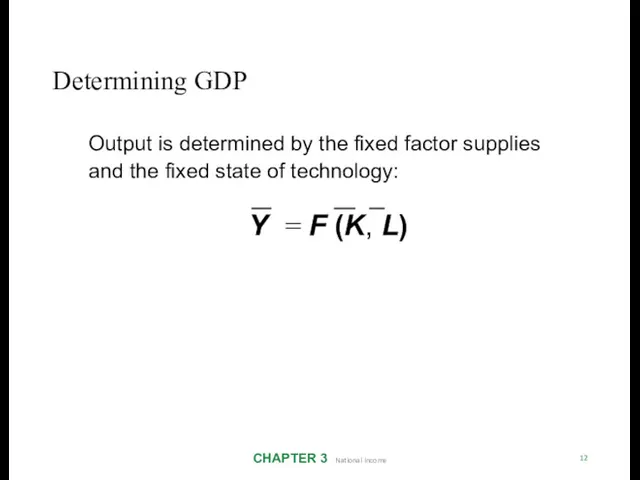

Determining GDP

CHAPTER 3 National Income

12

Output is determined by the fixed factor

Determining GDP

CHAPTER 3 National Income

12

Output is determined by the fixed factor

The distribution of national income

CHAPTER 3 National Income

13

determined by factor prices,

the

The distribution of national income

CHAPTER 3 National Income

13

determined by factor prices,

the

Notation

CHAPTER 3 National Income

14

W = nominal wage

R = nominal rental rate

P = price of

Notation

CHAPTER 3 National Income

14

W = nominal wage

R = nominal rental rate

P = price of

How factor prices are determined

CHAPTER 3 National Income

15

Factor prices are determined

How factor prices are determined

CHAPTER 3 National Income

15

Factor prices are determined

Demand for labor

CHAPTER 3 National Income

16

Assume markets are competitive: each firm

Demand for labor

CHAPTER 3 National Income

16

Assume markets are competitive: each firm

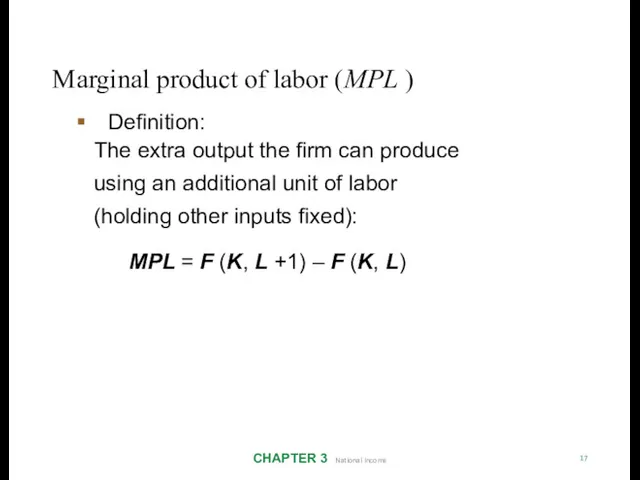

Marginal product of labor (MPL )

CHAPTER 3 National Income

17

Definition:

The extra

Marginal product of labor (MPL )

CHAPTER 3 National Income

17

Definition:

The extra

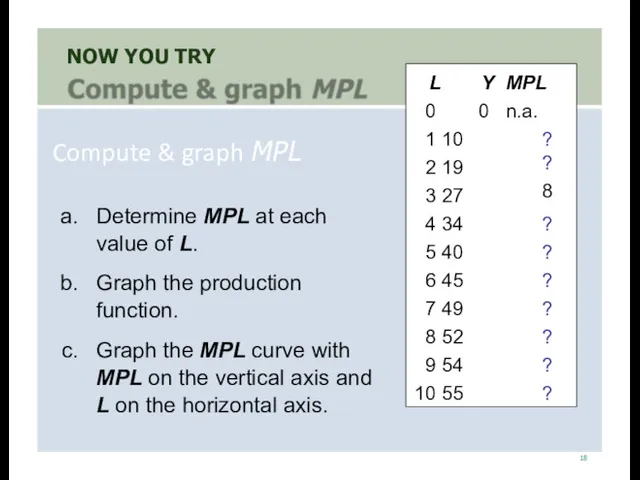

NOW YOU TRY

Compute & graph MPL

18

Determine MPL at each value of

NOW YOU TRY

Compute & graph MPL

18

Determine MPL at each value of

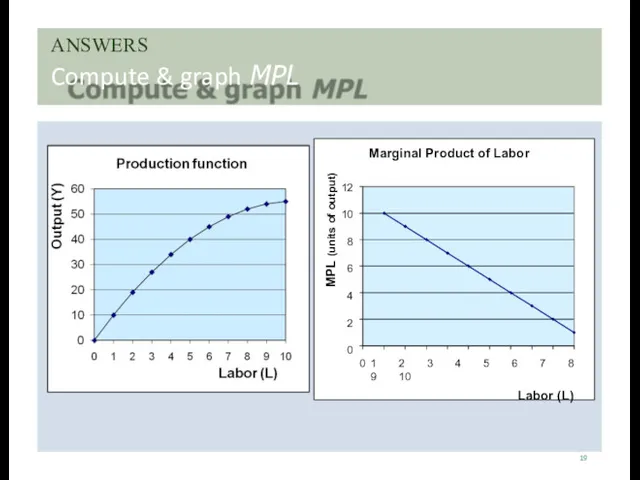

ANSWERS

Compute & graph MPL

19

MPL (units of output)

Marginal Product of Labor

12

10

8

6

4

2

0

0 1 2 3 4 5 6 7 8 9 10

Labor (L)

ANSWERS

Compute & graph MPL

19

MPL (units of output)

Marginal Product of Labor

12

10

8

6

4

2

0

0 1 2 3 4 5 6 7 8 9 10

Labor (L)

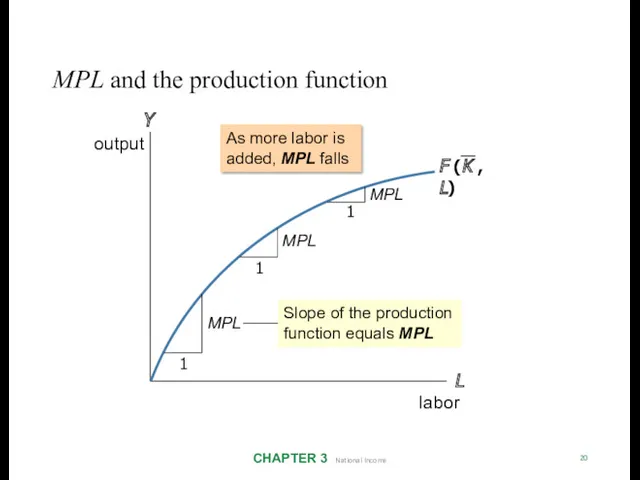

Y

output

MPL and the production function

CHAPTER 3 National Income

20

L

labor

F (K , L)

1

MPL

1

MPL

1

MPL

As

Y

output

MPL and the production function

CHAPTER 3 National Income

20

L

labor

F (K , L)

1

MPL

1

MPL

1

MPL

As

Diminishing marginal returns

CHAPTER 3 National Income

21

As one input is increased (holding

Diminishing marginal returns

CHAPTER 3 National Income

21

As one input is increased (holding

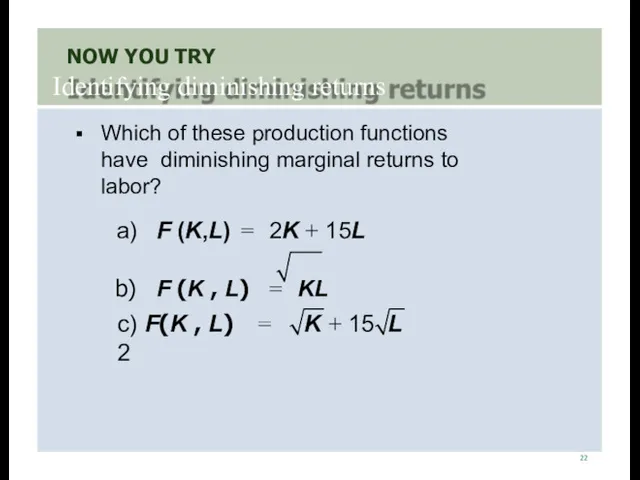

NOW YOU TRY

Identifying diminishing returns

22

Which of these production functions have diminishing

NOW YOU TRY

Identifying diminishing returns

22

Which of these production functions have diminishing

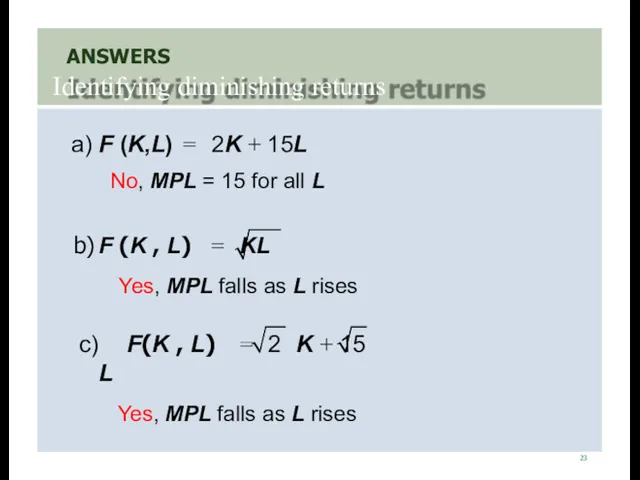

ANSWERS

Identifying diminishing returns

23

a) F (K,L) = 2K + 15L

No, MPL = 15 for all

ANSWERS

Identifying diminishing returns

23

a) F (K,L) = 2K + 15L

No, MPL = 15 for all

24

24

worker adds MPL = 4 units of output

25

worker adds MPL = 4 units of output

25

MPL and the demand for labor

CHAPTER 3 National Income

26

Each firm hires

MPL and the demand for labor

CHAPTER 3 National Income

26

Each firm hires

The equilibrium real wage

CHAPTER 3 National Income

27

The real wage adjusts to

The equilibrium real wage

CHAPTER 3 National Income

27

The real wage adjusts to

Determining the rental rate

CHAPTER 3 National Income

28

We have just seen that

Determining the rental rate

CHAPTER 3 National Income

28

We have just seen that

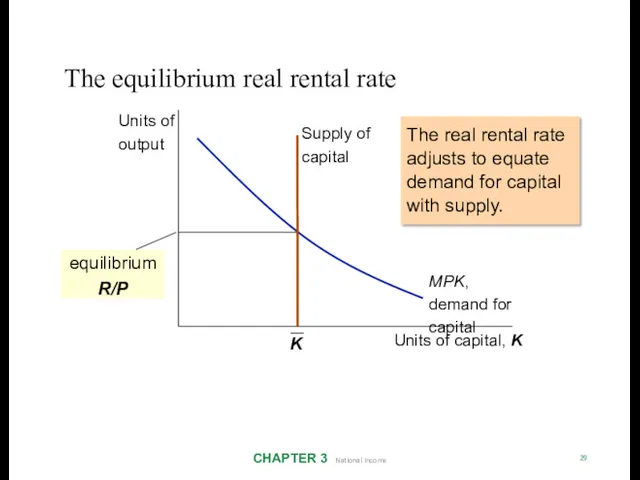

The equilibrium real rental rate

CHAPTER 3 National Income

29

The real rental rate

The equilibrium real rental rate

CHAPTER 3 National Income

29

The real rental rate

The neoclassical theory of distribution

CHAPTER 3 National Income

30

States that each factor

The neoclassical theory of distribution

CHAPTER 3 National Income

30

States that each factor

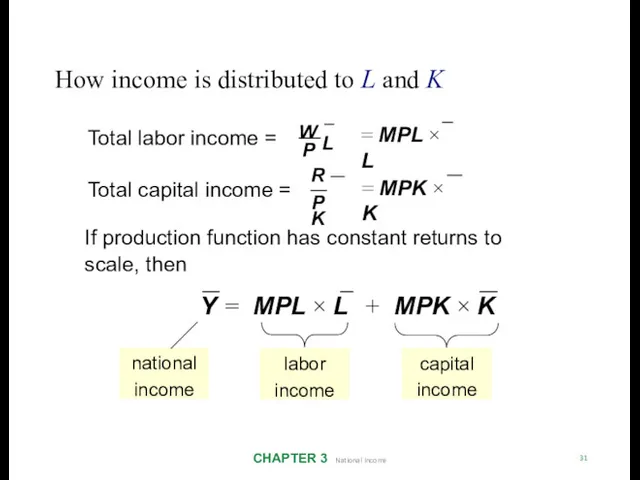

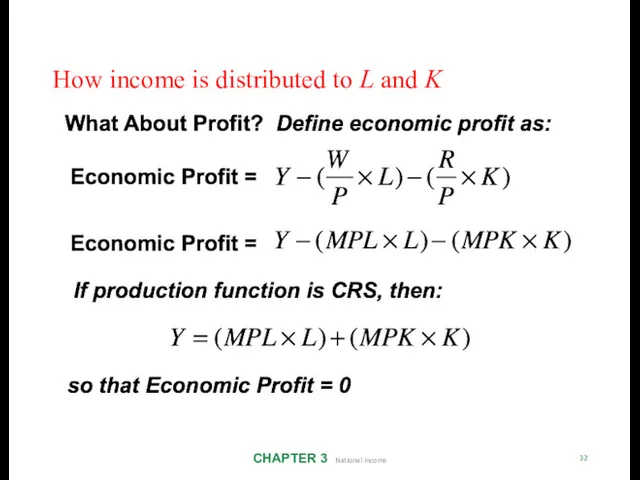

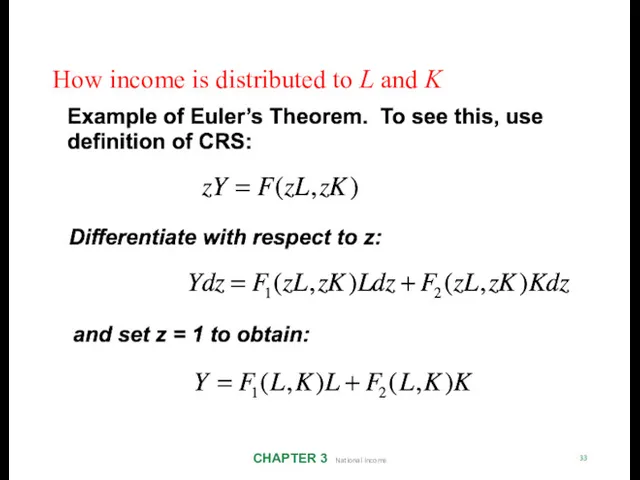

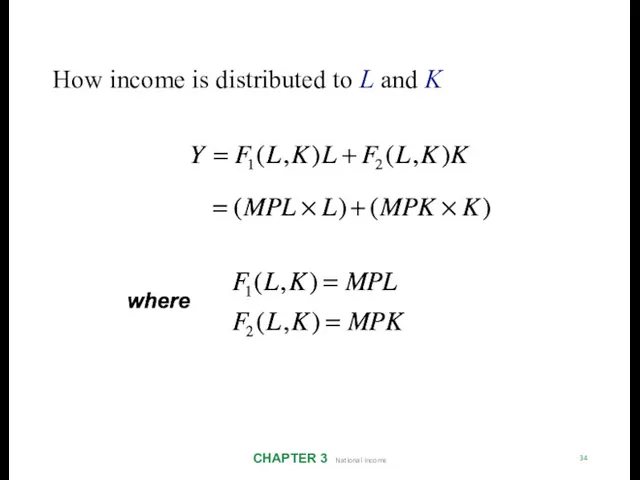

How income is distributed to L and K

CHAPTER 3 National Income

31

Total

How income is distributed to L and K

CHAPTER 3 National Income

31

Total

How income is distributed to L and K

CHAPTER 3 National Income

32

How income is distributed to L and K

CHAPTER 3 National Income

32

How income is distributed to L and K

CHAPTER 3 National Income

33

How income is distributed to L and K

CHAPTER 3 National Income

33

How income is distributed to L and K

CHAPTER 3 National Income

34

How income is distributed to L and K

CHAPTER 3 National Income

34

0.1

0

0.2

0.3

0.4

0.7

0.6

0.5

0.8

0.9

1

1960

1965 1970 1975 1980

1985 1990 1995 2000 2005 2010

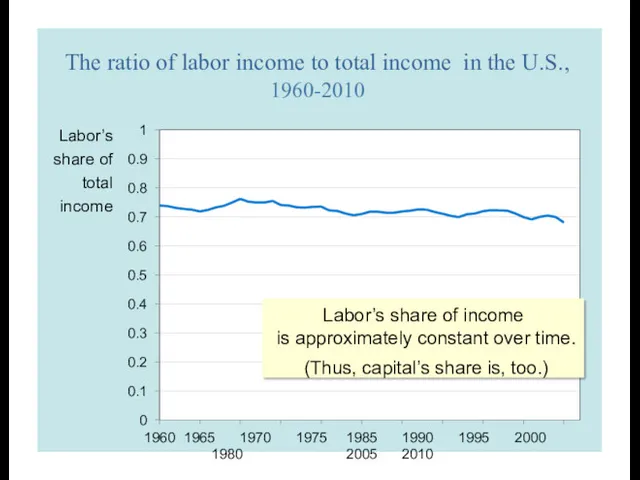

The ratio of labor income to total income in the U.S.,

0.1

0

0.2

0.3

0.4

0.7

0.6

0.5

0.8

0.9

1

1960

1965 1970 1975 1980

1985 1990 1995 2000 2005 2010

The ratio of labor income to total income in the U.S.,

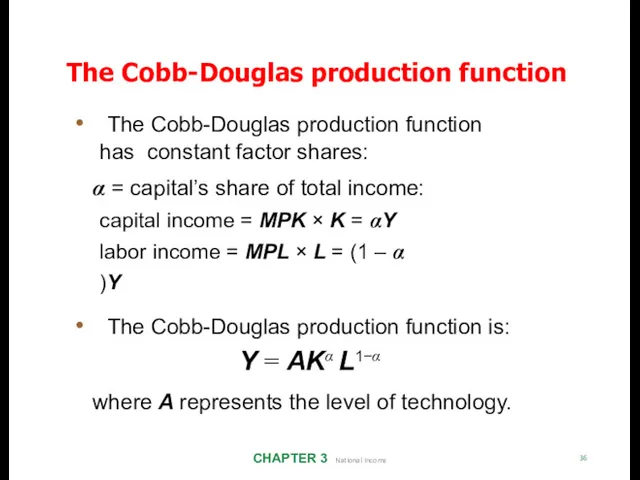

The Cobb-Douglas production function has constant factor shares:

CHAPTER 3 National

The Cobb-Douglas production function has constant factor shares:

CHAPTER 3 National

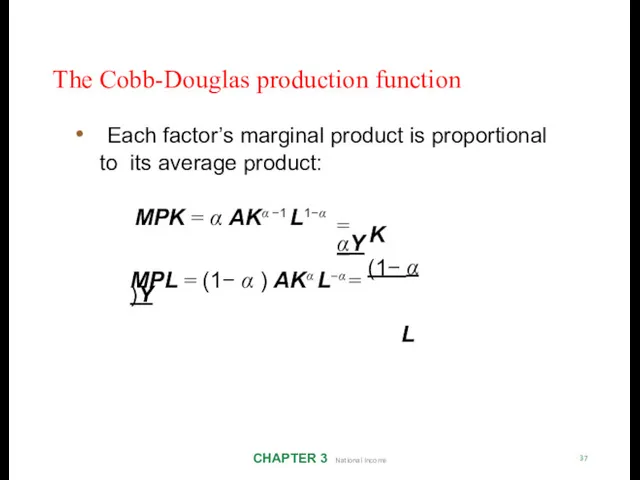

The Cobb-Douglas production function

CHAPTER 3 National Income

37

Each factor’s marginal product

The Cobb-Douglas production function

CHAPTER 3 National Income

37

Each factor’s marginal product

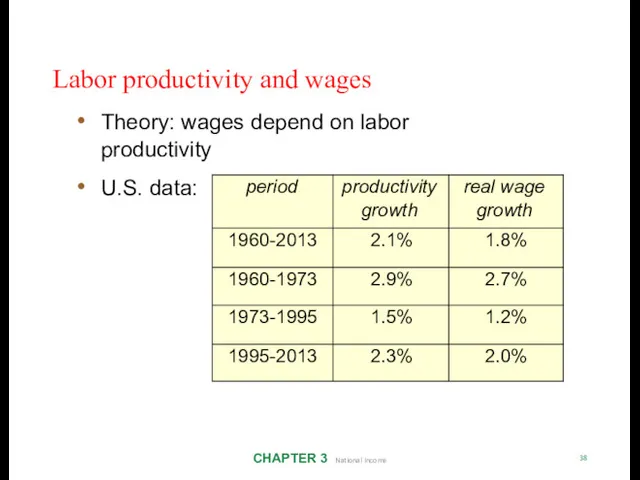

Labor productivity and wages

CHAPTER 3 National Income

38

Theory: wages depend on labor

Labor productivity and wages

CHAPTER 3 National Income

38

Theory: wages depend on labor

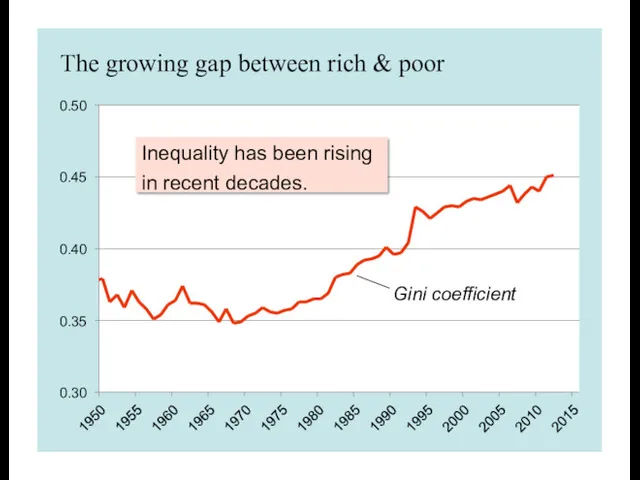

The growing gap between rich & poor

0.30

0.45

0.50

0.40

Gini coefficient

0.35

Inequality has been rising

The growing gap between rich & poor

0.30

0.45

0.50

0.40

Gini coefficient

0.35

Inequality has been rising

Explanations for rising inequality

CHAPTER 3 National Income

40

Rise in capital’s share of

Explanations for rising inequality

CHAPTER 3 National Income

40

Rise in capital’s share of

Outline of model

CHAPTER 3 National Income

41

A closed economy, market-clearing model

Supply side

DONE

Outline of model

CHAPTER 3 National Income

41

A closed economy, market-clearing model

Supply side

DONE

Demand for goods and services

CHAPTER 3 National Income

42

Components of aggregate demand:

C

Demand for goods and services

CHAPTER 3 National Income

42

Components of aggregate demand:

C

Consumption, C

CHAPTER 3 National Income

43

Disposable income is total income minus total

Consumption, C

CHAPTER 3 National Income

43

Disposable income is total income minus total

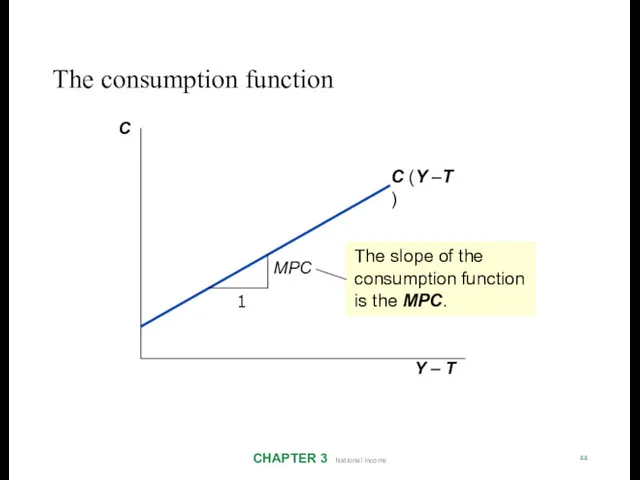

The consumption function

CHAPTER 3 National Income

44

C

Y – T

C (Y –T )

1

MPC

The

The consumption function

CHAPTER 3 National Income

44

C

Y – T

C (Y –T )

1

MPC

The

Investment, I

CHAPTER 3 National Income

45

The investment function is I = I

Investment, I

CHAPTER 3 National Income

45

The investment function is I = I

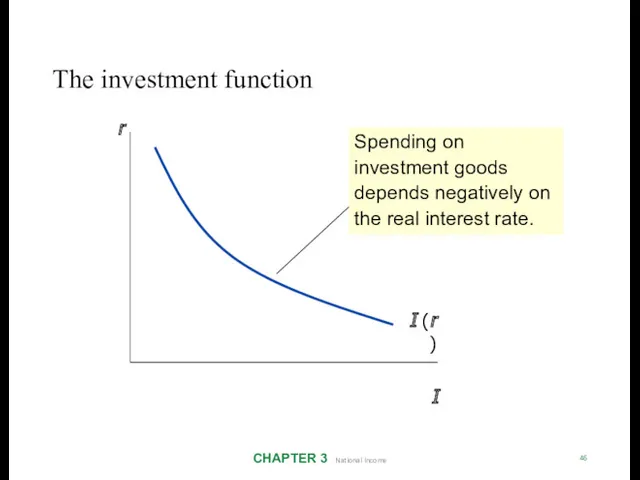

The investment function

CHAPTER 3 National Income

46

r

I (r )

I

Spending on investment goods

The investment function

CHAPTER 3 National Income

46

r

I (r )

I

Spending on investment goods

Government spending, G

CHAPTER 3 National Income

47

G = govt spending on goods

Government spending, G

CHAPTER 3 National Income

47

G = govt spending on goods

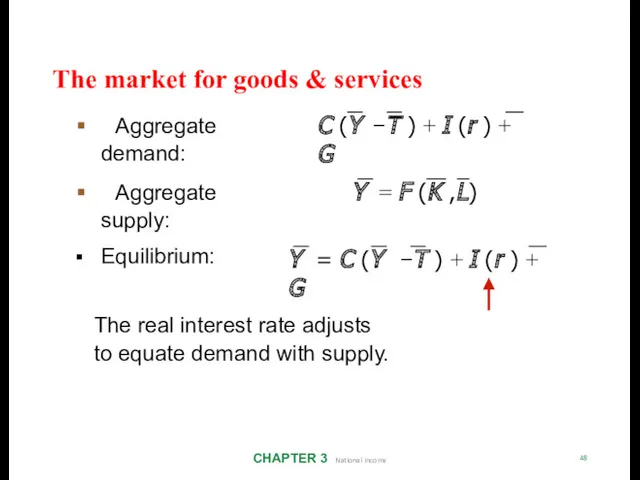

The market for goods & services

CHAPTER 3 National Income

48

Aggregate demand:

The market for goods & services

CHAPTER 3 National Income

48

Aggregate demand:

The loanable funds market

CHAPTER 3 National Income

49

A simple supply–demand model of

The loanable funds market

CHAPTER 3 National Income

49

A simple supply–demand model of

Demand for funds: investment

CHAPTER 3 National Income

50

The demand for loanable funds

Demand for funds: investment

CHAPTER 3 National Income

50

The demand for loanable funds

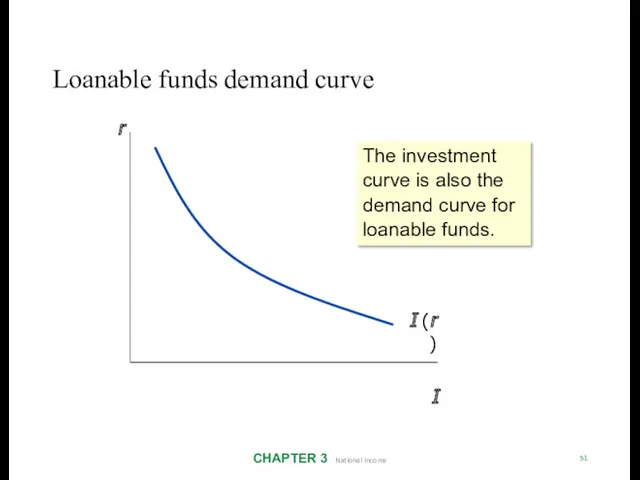

Loanable funds demand curve

CHAPTER 3 National Income

51

r

I (r )

I

The investment curve

Loanable funds demand curve

CHAPTER 3 National Income

51

r

I (r )

I

The investment curve

Supply of funds: saving

CHAPTER 3 National Income

52

The supply of loanable funds

Supply of funds: saving

CHAPTER 3 National Income

52

The supply of loanable funds

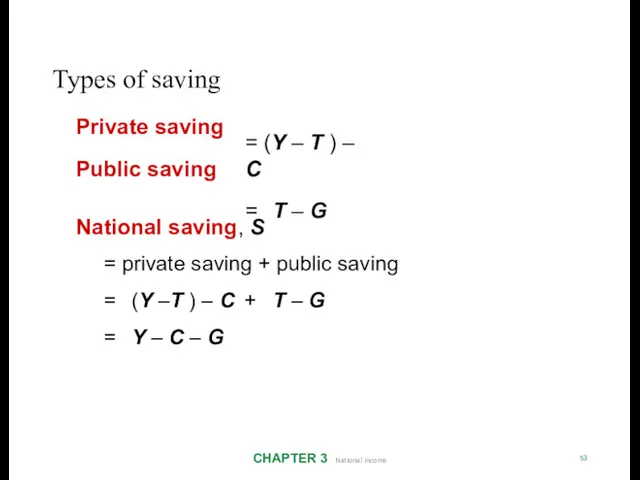

Types of saving

CHAPTER 3 National Income

53

Private saving Public saving

= (Y –

Types of saving

CHAPTER 3 National Income

53

Private saving Public saving

= (Y –

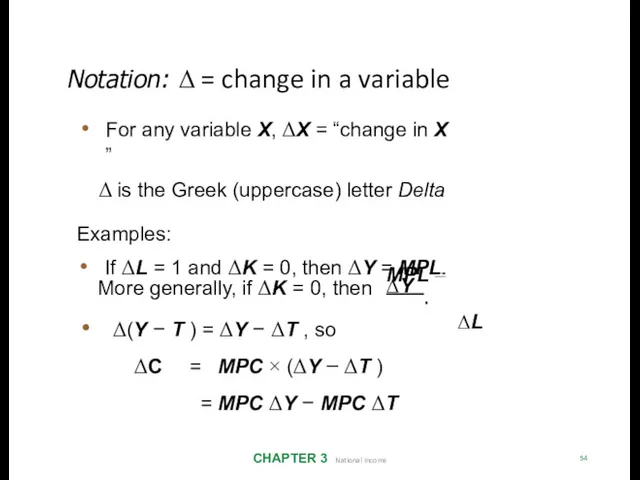

Notation: Δ = change in a variable

CHAPTER 3 National Income

54

For any variable

Notation: Δ = change in a variable

CHAPTER 3 National Income

54

For any variable

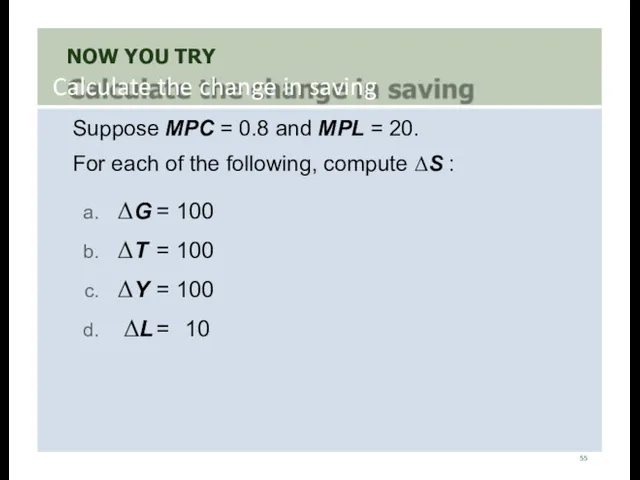

NOW YOU TRY

Calculate the change in saving

55

Suppose MPC = 0.8 and

NOW YOU TRY

Calculate the change in saving

55

Suppose MPC = 0.8 and

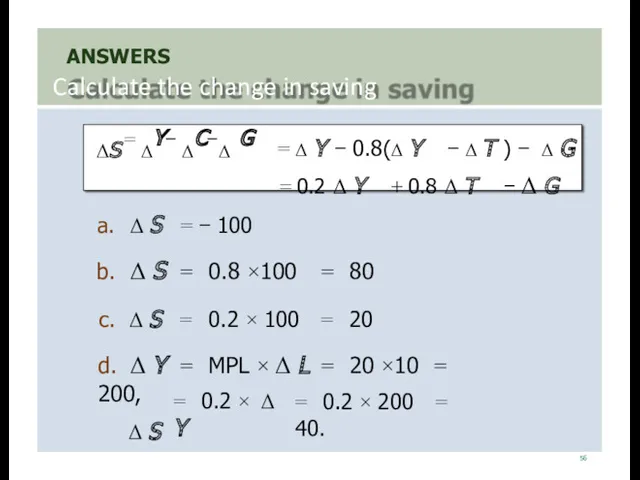

ANSWERS

Calculate the change in saving

56

ΔS = ΔY− ΔC−Δ G

= Δ Y − 0.8(Δ

ANSWERS

Calculate the change in saving

56

ΔS = ΔY− ΔC−Δ G

= Δ Y − 0.8(Δ

57

CHAPTER 3 National Income

Budget surpluses and deficits

If T > G,

57

CHAPTER 3 National Income

Budget surpluses and deficits

If T > G,

1940-2016

Percent of GDP

10

5

0

-5

-10

-15

-20

-25

-30

-35

1940

1950

1960

1970

1980

1990

2000

2010

U.S. federal government surplus/deficit

1940-2016

Percent of GDP

10

5

0

-5

-10

-15

-20

-25

-30

-35

1940

1950

1960

1970

1980

1990

2000

2010

U.S. federal government surplus/deficit

U.S. federal government debt,

1940-2016

Percent of GDP

140

120

100

80

60

40

20

0

1940

1950

1960

1970

1980

1990

2000

2010

U.S. federal government debt,

1940-2016

Percent of GDP

140

120

100

80

60

40

20

0

1940

1950

1960

1970

1980

1990

2000

2010

Loanable funds supply curve

CHAPTER 3 National Income

60

r

S, I

S =Y − C (Y −T )

Loanable funds supply curve

CHAPTER 3 National Income

60

r

S, I

S =Y − C (Y −T )

Loanable funds market equilibrium

CHAPTER 3 National Income

61

r

S, I

I (r )

S =Y − C

Loanable funds market equilibrium

CHAPTER 3 National Income

61

r

S, I

I (r )

S =Y − C

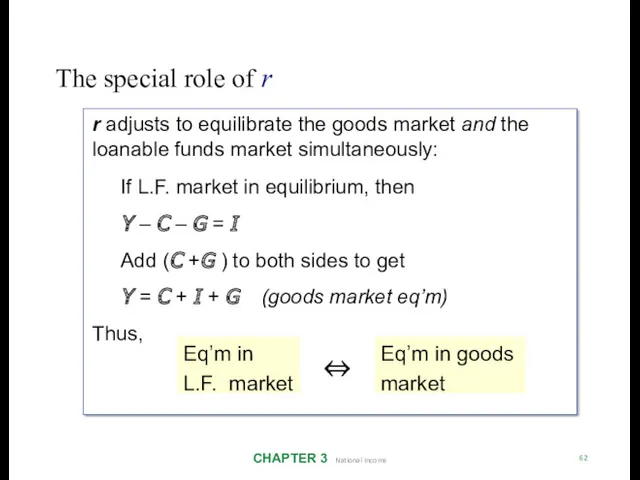

The special role of r

CHAPTER 3 National Income

62

r adjusts to equilibrate

The special role of r

CHAPTER 3 National Income

62

r adjusts to equilibrate

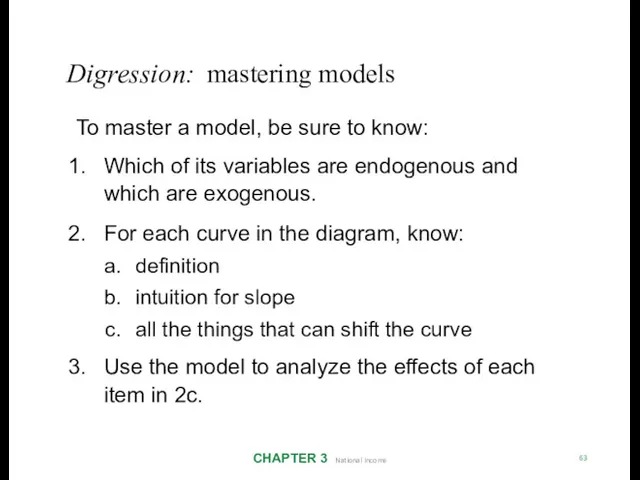

Digression: mastering models

CHAPTER 3 National Income

63

To master a model, be sure to

Digression: mastering models

CHAPTER 3 National Income

63

To master a model, be sure to

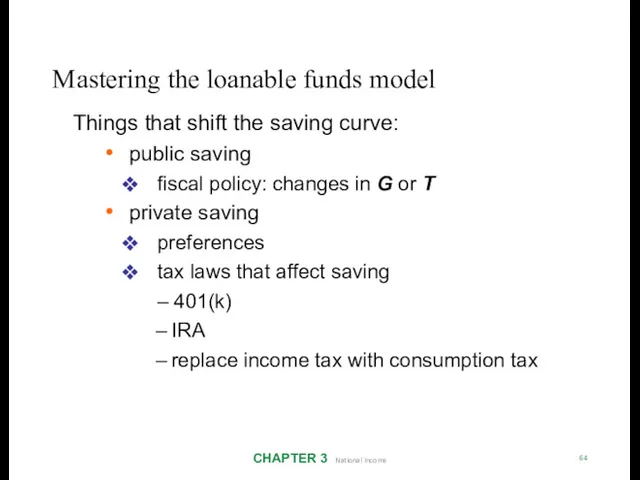

Mastering the loanable funds model

CHAPTER 3 National Income

64

Things that shift the

Mastering the loanable funds model

CHAPTER 3 National Income

64

Things that shift the

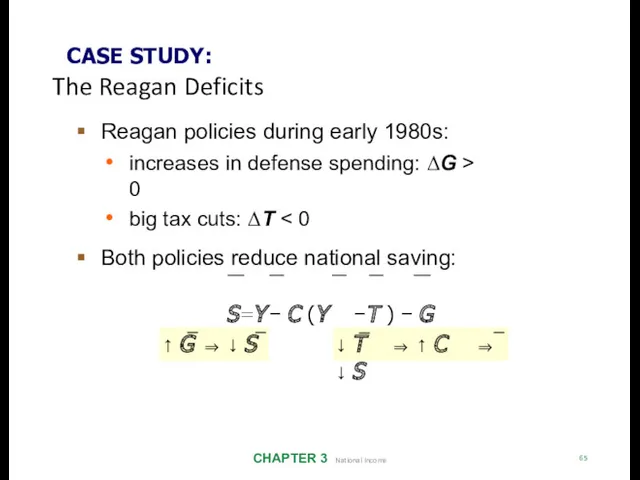

CASE STUDY:

The Reagan Deficits

CHAPTER 3 National Income

65

Reagan policies during early 1980s:

increases

CASE STUDY:

The Reagan Deficits

CHAPTER 3 National Income

65

Reagan policies during early 1980s:

increases

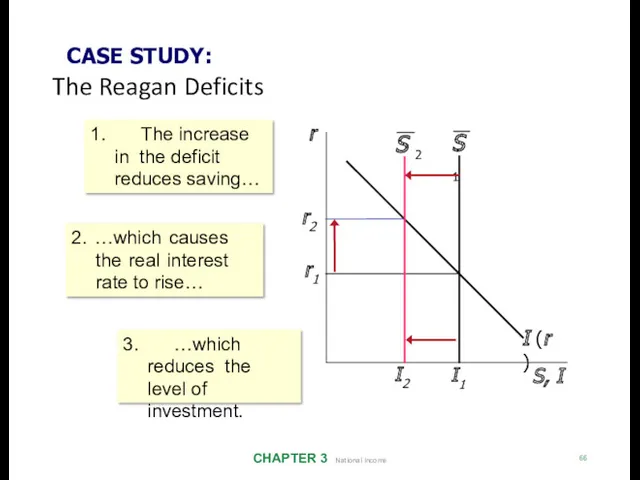

CASE STUDY:

The Reagan Deficits

CHAPTER 3 National Income

66

r

S, I

S 1

I (r )

r1

I1

r2

2.

CASE STUDY:

The Reagan Deficits

CHAPTER 3 National Income

66

r

S, I

S 1

I (r )

r1

I1

r2

2.

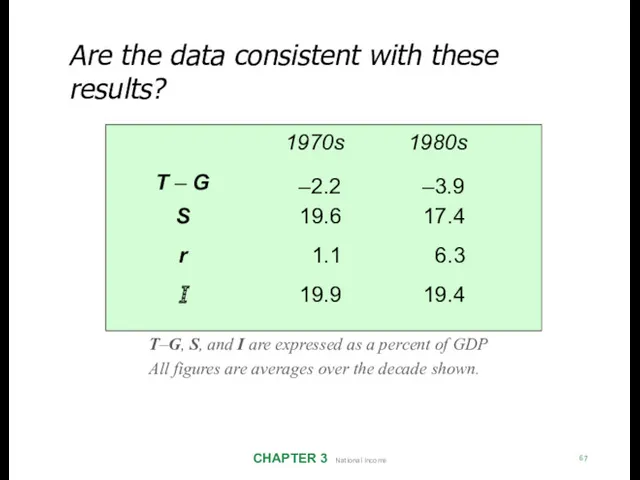

Are the data consistent with these results?

CHAPTER 3 National Income

67

T–G, S,

Are the data consistent with these results?

CHAPTER 3 National Income

67

T–G, S,

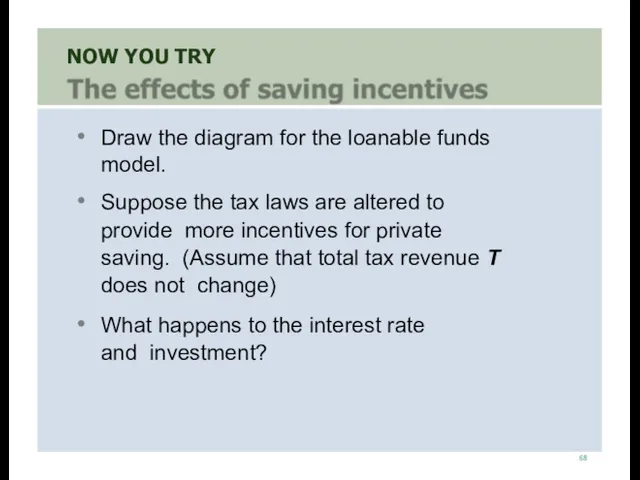

NOW YOU TRY

68

Draw the diagram for the loanable funds model.

Suppose the

NOW YOU TRY

68

Draw the diagram for the loanable funds model.

Suppose the

Mastering the loanable funds model

CHAPTER 3 National Income

69

(continued)

Things that shift the

Mastering the loanable funds model

CHAPTER 3 National Income

69

(continued)

Things that shift the

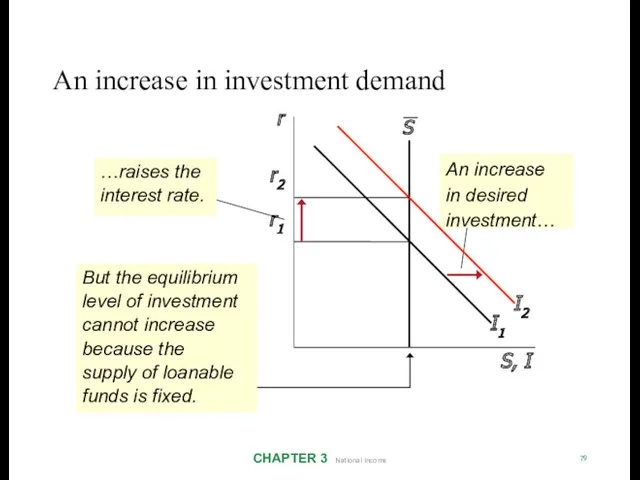

An increase in investment demand

CHAPTER 3 National Income

79

An increase in desired

An increase in investment demand

CHAPTER 3 National Income

79

An increase in desired

Saving and the interest rate

CHAPTER 3 National Income

71

Why might saving depend

Saving and the interest rate

CHAPTER 3 National Income

71

Why might saving depend

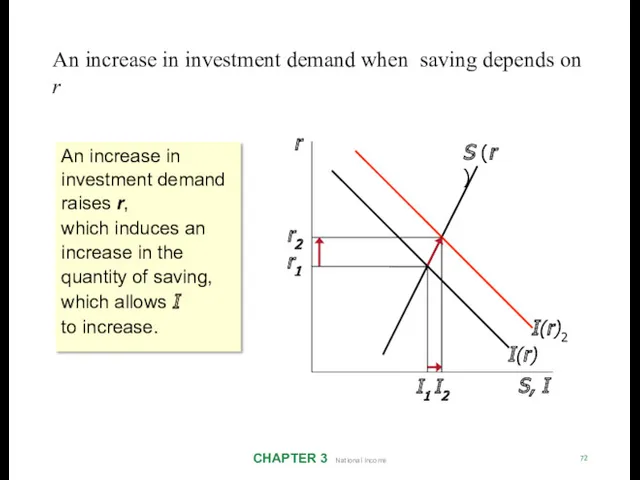

An increase in investment demand when saving depends on r

CHAPTER 3

An increase in investment demand when saving depends on r

CHAPTER 3

C H A P T E R S U M M A

C H A P T E R S U M M A

C H A P T E R S U M M A

C H A P T E R S U M M A

Формализация задач мониторинга и оценки новаций в проектировании регионального устойчивого инновационного развития

Формализация задач мониторинга и оценки новаций в проектировании регионального устойчивого инновационного развития Международное разделение труда в мировом хозяйстве

Международное разделение труда в мировом хозяйстве Типы экономических систем

Типы экономических систем Платежный баланс

Платежный баланс Цена. Основные функции цены

Цена. Основные функции цены Економічний аналіз та методи економічної оцінки в сфері охорони здоров’я

Економічний аналіз та методи економічної оцінки в сфері охорони здоров’я Искусство и экономика. Художественный аукцион

Искусство и экономика. Художественный аукцион Итоги производственной и финансово-экономической деятельности эксплуатационного локомотивного депо Уссурийск

Итоги производственной и финансово-экономической деятельности эксплуатационного локомотивного депо Уссурийск Особенности методики школьного экономического образования. (Лекция 2)

Особенности методики школьного экономического образования. (Лекция 2) Аралас экономика және қазіргі қоғамдық өндіріс қызмет етуінің объективті нысаны

Аралас экономика және қазіргі қоғамдық өндіріс қызмет етуінің объективті нысаны Безработица как социально-экономическая проблема

Безработица как социально-экономическая проблема Общая характеристика рыночной экономики

Общая характеристика рыночной экономики Анализ экономических показателей на основе применения метода динамических рядов

Анализ экономических показателей на основе применения метода динамических рядов Организация труда и трудовые отношения

Организация труда и трудовые отношения Экономическая свобода и социальная ответственность

Экономическая свобода и социальная ответственность Prezentatsia_kursovoy_raboty

Prezentatsia_kursovoy_raboty Финансы как экономическая категория

Финансы как экономическая категория Экономика. Экономические блага и ресурсы

Экономика. Экономические блага и ресурсы Forecast combinations

Forecast combinations Definition capacity

Definition capacity Правовые и экономические особенности закупки ТРУ отдельными юридическими лицами

Правовые и экономические особенности закупки ТРУ отдельными юридическими лицами Мектеп кеме-білім теңіз

Мектеп кеме-білім теңіз Народосбережение. Демографическая ситуация, основные причины сложившегося положения дел, задачи народосбережения

Народосбережение. Демографическая ситуация, основные причины сложившегося положения дел, задачи народосбережения Сельское хозяйство Великобритании

Сельское хозяйство Великобритании Система национальных счетов. Основные макроэкономические показатели

Система национальных счетов. Основные макроэкономические показатели Собственность, как экономическая категория

Собственность, как экономическая категория Планирование материально-технического обеспечения и механизации. Планирование труда и прибыли

Планирование материально-технического обеспечения и механизации. Планирование труда и прибыли Современная система ценообразования в энергетике. Оптовый рынок электроэнергии (мощности)

Современная система ценообразования в энергетике. Оптовый рынок электроэнергии (мощности)