- ARCH and GARCH. Modeling Volatility Dynamics

Содержание

- 2. Modeling Unequal Variability Equal Variability: Homoscedasticity Unequal Variability: Heteroscedasticity Means any variability (around the mean) that

- 3. What These Acronym Mean? ARCH Autoregressive Conditional Heteroscedasticity GARCH Generalized ARCH

- 4. Information in e2 Let εt have the mean 0 and the variance σt. Let et be

- 5. ARCH Modeling of σt2. ARCH(1) ARCH as AR(1) on

- 6. GARCH GARCH(1) GARCH (1) as ARMA(1,1) on

- 7. Asymmetry in GARCH - TARCH TARCH(1,1) d = 1 if εt 0

- 8. Asymmetry in GARCH - EGARCH EGARCH(1,1)

- 10. Скачать презентацию

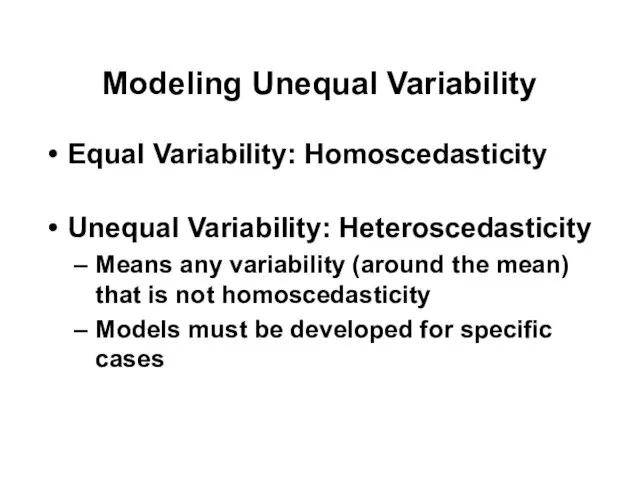

Modeling Unequal Variability

Equal Variability: Homoscedasticity

Unequal Variability: Heteroscedasticity

Means any variability (around the

Modeling Unequal Variability

Equal Variability: Homoscedasticity

Unequal Variability: Heteroscedasticity

Means any variability (around the

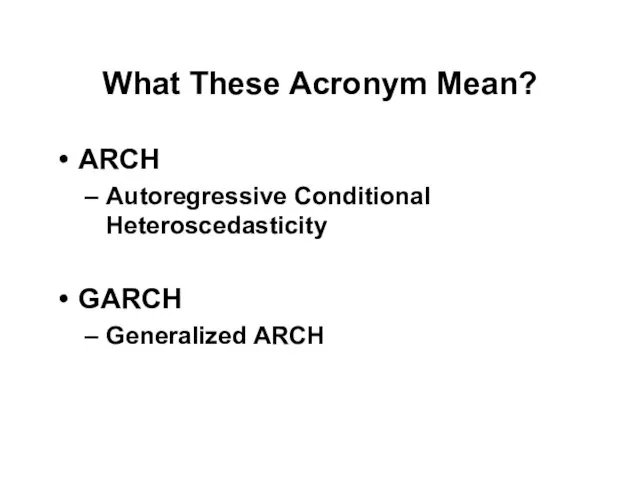

What These Acronym Mean?

ARCH

Autoregressive Conditional Heteroscedasticity

GARCH

Generalized ARCH

What These Acronym Mean?

ARCH

Autoregressive Conditional Heteroscedasticity

GARCH

Generalized ARCH

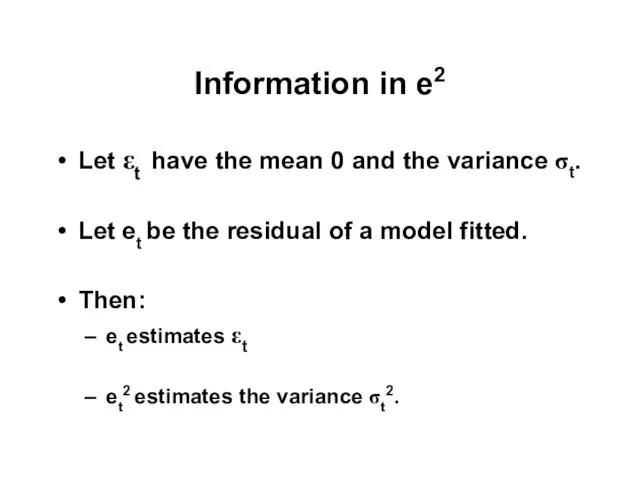

Information in e2

Let εt have the mean 0 and the variance

Information in e2

Let εt have the mean 0 and the variance

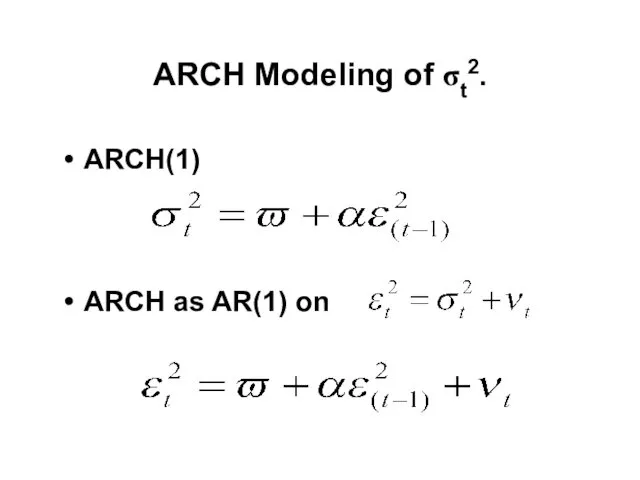

ARCH Modeling of σt2.

ARCH(1)

ARCH as AR(1) on

ARCH Modeling of σt2.

ARCH(1)

ARCH as AR(1) on

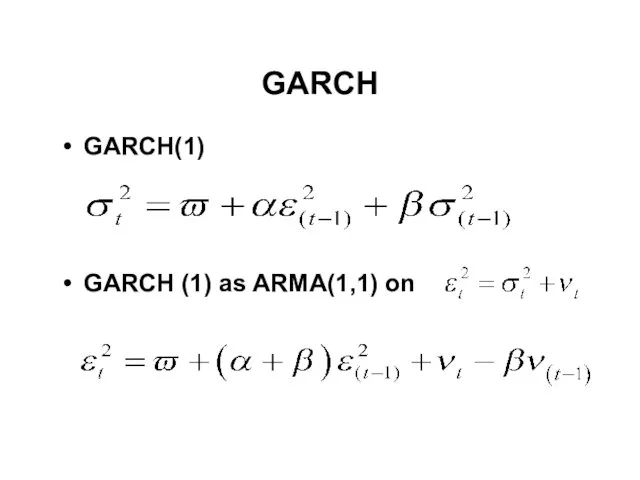

GARCH

GARCH(1)

GARCH (1) as ARMA(1,1) on

GARCH

GARCH(1)

GARCH (1) as ARMA(1,1) on

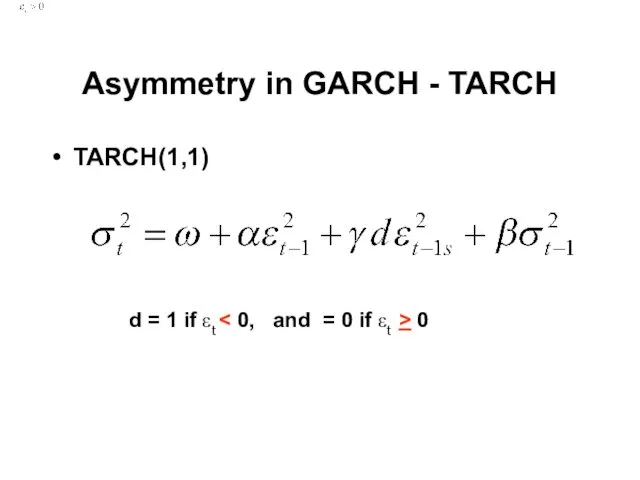

Asymmetry in GARCH - TARCH

TARCH(1,1)

d = 1 if εt < 0,

Asymmetry in GARCH - TARCH

TARCH(1,1)

d = 1 if εt < 0,

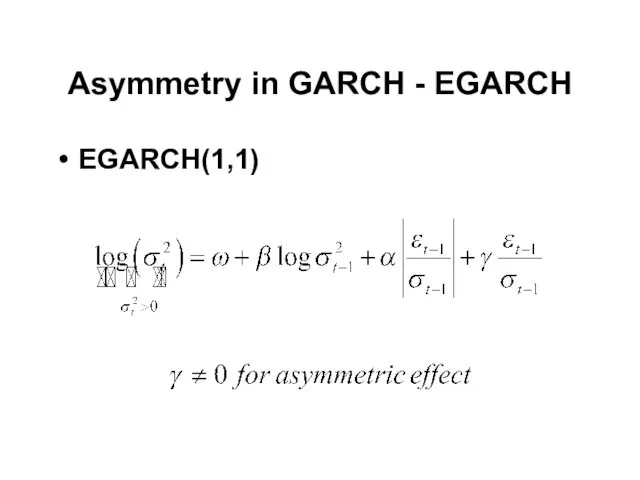

Asymmetry in GARCH - EGARCH

EGARCH(1,1)

Asymmetry in GARCH - EGARCH

EGARCH(1,1)

Презентация Учим цифры

Презентация Учим цифры Сложение и вычитание натуральных чисел

Сложение и вычитание натуральных чисел Презентация Арифметические задачи, 2 класс

Презентация Арифметические задачи, 2 класс Взаимное положение прямой и плоскости, двух плоскостей. Позиционные задачи. (Лекция 4)

Взаимное положение прямой и плоскости, двух плоскостей. Позиционные задачи. (Лекция 4) Простейшие вероятностные задачи (11 класс)

Простейшие вероятностные задачи (11 класс) Координатная плоскость. 6 класс

Координатная плоскость. 6 класс Своя игра. Степень с натуральным показателем

Своя игра. Степень с натуральным показателем Формула площади прямоугольника

Формула площади прямоугольника Вычисление объемов и площадей поверхности геометрических тел

Вычисление объемов и площадей поверхности геометрических тел Похідна. Геометричний зміст похідної

Похідна. Геометричний зміст похідної Теорема о трех перпендикулярах

Теорема о трех перпендикулярах Комбинация призмы и цилиндра

Комбинация призмы и цилиндра Автокорреляция

Автокорреляция Презентация Играем и учимся со счетными палочками

Презентация Играем и учимся со счетными палочками Противоположные числа

Противоположные числа Арифметические действия с положительными и отрицательными числами

Арифметические действия с положительными и отрицательными числами Метод проекций. Задание прямой линии на чертеже. Взаимное положение двух прямых. Теорема о проекциях прямого угла. (Лекция 1)

Метод проекций. Задание прямой линии на чертеже. Взаимное положение двух прямых. Теорема о проекциях прямого угла. (Лекция 1) Сложение и вычитание десятичных дробей. Зачёт

Сложение и вычитание десятичных дробей. Зачёт Урок математики в 1 классе. Перестановка слагаемых

Урок математики в 1 классе. Перестановка слагаемых Пирамида. Правильная пирамида

Пирамида. Правильная пирамида Производная функции в точке

Производная функции в точке Числа от 1-8. УМК Школа 2100

Числа от 1-8. УМК Школа 2100 Тренажёр по математике

Тренажёр по математике Графический метод решения системы уравнений с двумя переменными. 7 класс

Графический метод решения системы уравнений с двумя переменными. 7 класс Решение уравнений. Урок математики

Решение уравнений. Урок математики Линейные пространства. Тема 7

Линейные пространства. Тема 7 Экономико-математические методы и модели. Теоремы двойственности

Экономико-математические методы и модели. Теоремы двойственности Обыкновенные дроби. Дробь как результат деления натуральных чисел

Обыкновенные дроби. Дробь как результат деления натуральных чисел