- An introduction to risk management in real estate development

Содержание

- 2. DEFINITION OF REAL ESTATE DEVELOPMENT The views expressed in specialist literature regarding the precise definition of

- 3. DEFINITION OF REAL ESTATE DEVELOPMENT Real estate is a triangle of space, money and time. In

- 4. DEFINITION OF REAL ESTATE DEVELOPMENT Development is an idea that comes to fruition when consumers –

- 5. THE PURPOSE OF REAL ESTATE DEVELOPMENT The purpose of real estate development is therefore to recognise

- 6. THE PURPOSE OF REAL ESTATE DEVELOPMENT Generally, the priority goal of a developer is the optimal

- 7. THE PURPOSE OF REAL ESTATE DEVELOPMENT To meet its objectives, a developer has to focus on

- 8. THE PURPOSE OF REAL ESTATE DEVELOPMENT Development is a complex process which entails the orchestration of

- 9. THE PURPOSE OF REAL ESTATE DEVELOPMENT Real estate development is required to combine the aspects of

- 10. THE PURPOSE OF REAL ESTATE DEVELOPMENT This conceptual understanding makes stronger reference to the production factors

- 11. RISKY NATURE OF REAL ESTATE DEVELOPMENT Real estate development is considered to be one of the

- 12. Wiegelmann T. W. Risk Management in the Real Estate Development Industry: Ph. D. Thesis, 2012 //

- 13. REGULATORY PRESSURE Regulatory and corporate governance provisions are increasingly requiring greater awareness of risk and risk

- 14. CAPITAL MARKETS PRESSURE The capital market now also requires adequate corporate risk management. Organisations, which are

- 15. STAKEHOLDERS' PRESSURE Other stakeholders of real estate development organisations expect an effective allocation and use of

- 16. REAL ESTATE AS A UNIQUE ASSET CLASS The most prominent characteristics of real estate are that

- 17. REAL ESTATE AS A UNIQUE ASSET CLASS Land cannot be reproduced, any structures built or developed

- 18. REAL ESTATE AS A UNIQUE ASSET CLASS Real estate development is a highly complex, dynamic and

- 19. REAL ESTATE AS A UNIQUE ASSET CLASS Finally, real estate is also characterised by its long

- 20. SPECIFIC CHARACTERISTICS OF THE REAL ESTATE MARKET The real estate market is fundamentally an open, generally

- 21. SPECIFIC CHARACTERISTICS OF THE REAL ESTATE MARKET The most prominent characteristic in this context is the

- 22. SPECIFIC CHARACTERISTICS OF THE REAL ESTATE MARKET Generally, the market participants only have access to limited

- 23. SPECIFIC CHARACTERISTICS OF THE REAL ESTATE MARKET The cyclical nature of real estate markets requires strategic

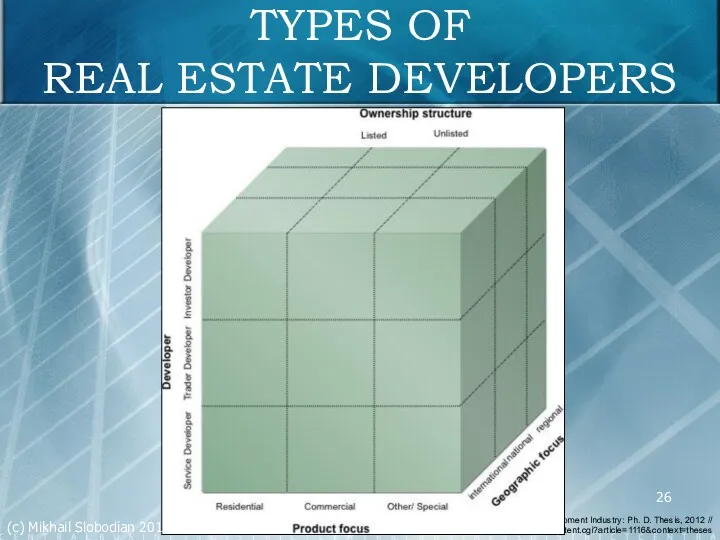

- 24. TYPES OF REAL ESTATE DEVELOPERS There are many types of developers and an all-encompassing definition is

- 25. TYPES OF REAL ESTATE DEVELOPERS Essentially, real estate developers operate as either trader or investor developers.

- 26. TYPES OF REAL ESTATE DEVELOPERS Wiegelmann T. W. Risk Management in the Real Estate Development Industry:

- 27. TYPES OF REAL ESTATE DEVELOPERS Trader-developers typically assume the entire risk until completion of the relevant

- 28. TYPES OF REAL ESTATE DEVELOPERS Investor-developers carry out projects to establish a portfolio or for use

- 29. TYPES OF REAL ESTATE DEVELOPERS Investor-developers and trader-developers share many characteristics. However, as the time of

- 30. TYPES OF REAL ESTATE DEVELOPERS Service developers render specific real estate development services as a service

- 31. (c) Mikhail Slobodian 2015 TYPES OF REAL ESTATE DEVELOPERS Financially, service developers commit themselves to the

- 32. TYPES OF REAL ESTATE DEVELOPERS With regards to the geographical focus of developer's activities, a differentiation

- 33. TYPES OF REAL ESTATE DEVELOPERS In order to distinguish between different development projects, it would be

- 34. TYPES OF REAL ESTATE DEVELOPERS Organisational size could potentially act as a further classification aspect for

- 35. Wiegelmann T. W. Risk Management in the Real Estate Development Industry: Ph. D. Thesis, 2012 //

- 36. STATE OF AFFAIRS IN REAL ESTATE INDUSTRY most real estate developers do not conduct their risk

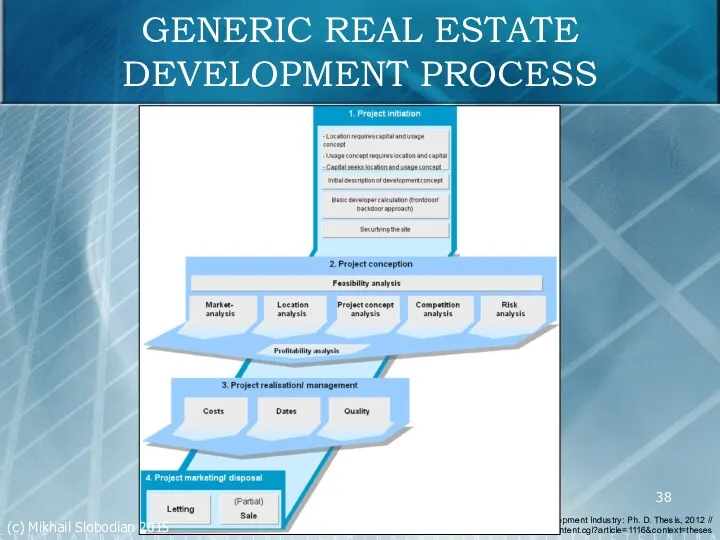

- 37. OVERVIEW TO THE GENERIC REAL ESTATE DEVELOPMENT PROCESS The real estate development process is based on

- 38. GENERIC REAL ESTATE DEVELOPMENT PROCESS Wiegelmann T. W. Risk Management in the Real Estate Development Industry:

- 39. GENERIC REAL ESTATE DEVELOPMENT PROJECT (c) Mikhail Slobodian 2015

- 40. PROJECT INITIATION The initiation phase commences the development process. A main expertise of a development organisation

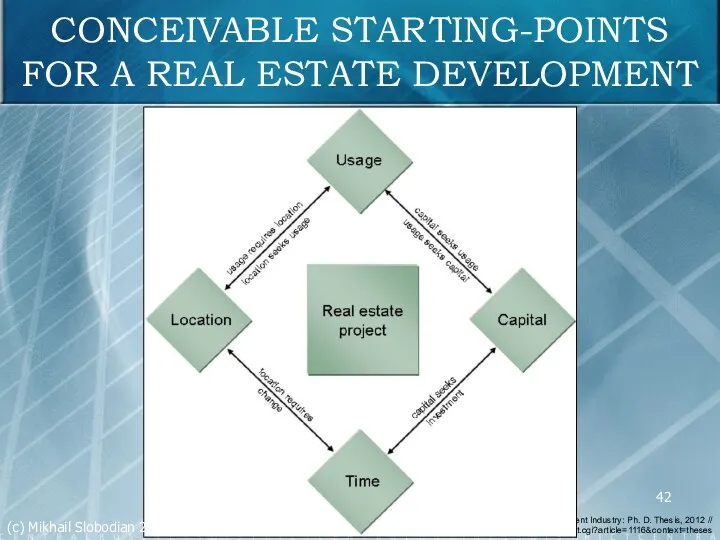

- 41. PROJECT INITIATION Accordingly, the starting situation for a development may either be: an existing plot of

- 42. CONCEIVABLE STARTING-POINTS FOR A REAL ESTATE DEVELOPMENT Wiegelmann T. W. Risk Management in the Real Estate

- 43. PROJECT INITIATION Accurate and pre-planned “timing” is a critical success factor in this context. This depends

- 44. PROJECT INITIATION Based on a positive evaluation, the next major step is to typically obtain approval

- 45. PROJECT INITIATION Option agreements or a purchase subject to conditions precedent are possible routes to achieve

- 46. PROJECT CONCEPTION The conception phase starts with the project feasibility analysis and ends in the implementation

- 47. PROJECT CONCEPTION This is ultimately intended to answer the question whether and in which manner the

- 48. PROJECT CONCEPTION The term “feasibility analysis” has become accepted as a general term for the many

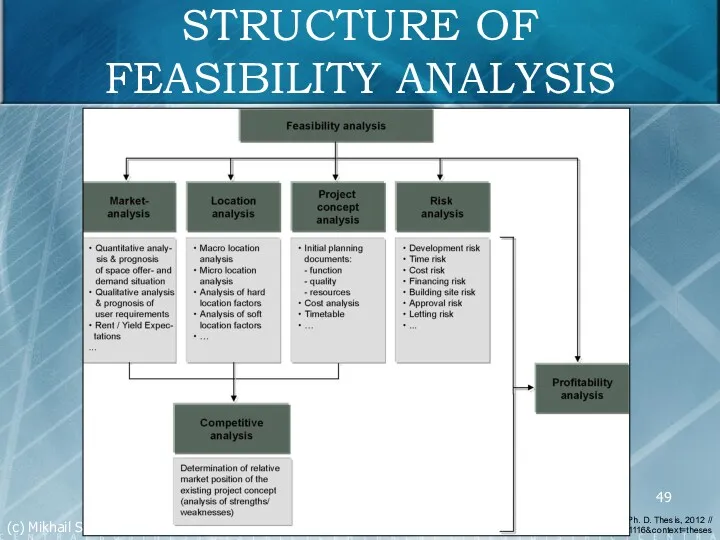

- 49. STRUCTURE OF FEASIBILITY ANALYSIS Wiegelmann T. W. Risk Management in the Real Estate Development Industry: Ph.

- 50. MARKET ANALYSIS The market analysis concerns itself with the supply and demand situation in the short

- 51. LOCATION ANALYSIS The analysis of the location should critically verify the findings of the inception phase

- 52. PROJECT CONCEPT ANALYSIS The building or usage concept for the use of the property must be

- 53. COMPETITION ANALYSIS The three above aspects of market, location and usage concept typically run parallel and

- 54. RISK ANALYSIS While risks are present at all stages of property development, the feasibility analysis offers

- 55. RISK ANALYSIS The project-specific manoeuvrability, i. e. the scope for structuring architectural, technical, economic and legal

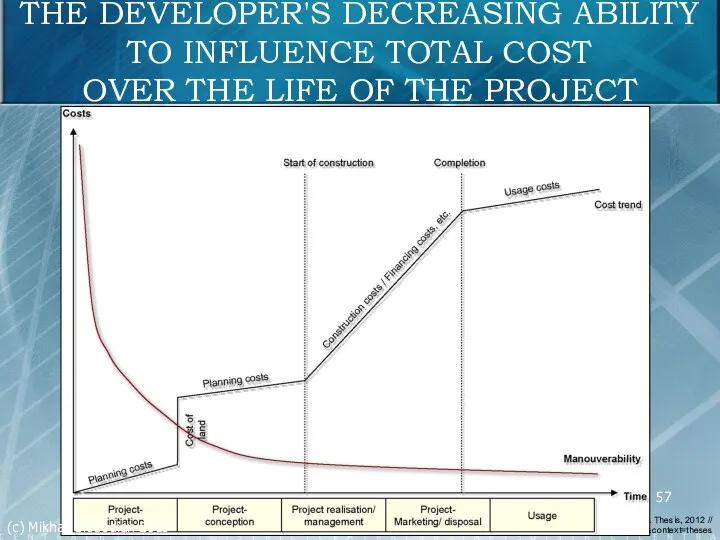

- 56. RISK ANALYSIS Furthermore, although the overall complexity of the project decreases during the stages of the

- 57. THE DEVELOPER'S DECREASING ABILITY TO INFLUENCE TOTAL COST OVER THE LIFE OF THE PROJECT Wiegelmann T.

- 58. Wiegelmann T. W. Risk Management in the Real Estate Development Industry: Ph. D. Thesis, 2012 //

- 59. METHODS OF RISK IDENTIFICATION Wiegelmann T. W. Risk Management in the Real Estate Development Industry: Ph.

- 60. DEVELOPMENT RISK Development risk is defined as the risk that the leasing or sale of the

- 61. (c) Mikhail Slobodian 2015 DEVELOPMENT RISK Forecasting and planning risk are also part of risk management.

- 62. TIME RISK In general, exceeding the planned project time line leads to two main risks: cost

- 63. COST RISK The cost risk is closely related to time risk, as the time needed for

- 64. (c) Mikhail Slobodian 2015 FINANCIAL RISK Typically, developers have to obtain appropriate financing schemes at favourable

- 65. FINANCIAL RISK Also, time and finance risk are driven by related factors, so delays in the

- 66. FINANCIAL RISK It should also be considered that there are significant differences between a development financing

- 67. BUILDING SITE RISK This is the risk that the selected site is unsuitable, or needs to

- 68. APPROVAL RISK All development is subject to planning, and while developers in general apply for permissions

- 69. PROFITABILITY ANALYSIS Combining the results of the five analyses above (market, location, project concept, risk and

- 70. PROFITABILITY ANALYSIS The profitability analysis should use clearly defined quantitative measures of a project's robustness and

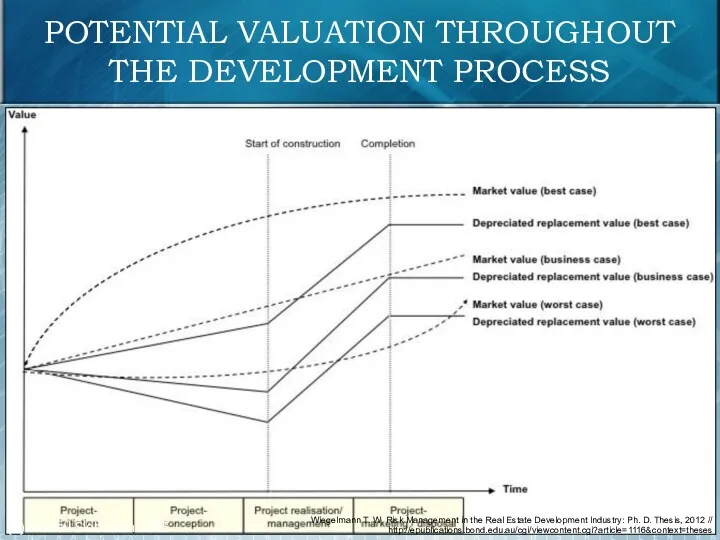

- 71. POTENTIAL VALUATION THROUGHOUT THE DEVELOPMENT PROCESS Wiegelmann T. W. Risk Management in the Real Estate Development

- 72. CONCLUDING THE FEASIBILITY ANALYSIS Having assembled the above data and analysed it based on appropriate assumptions,

- 73. CONCLUDING THE FEASIBILITY ANALYSIS In the framework of the project initiation, it is the objective to

- 74. PROJECT REALISATION / MANAGEMENT The confirmation of the project's potential for success by the feasibility analysis

- 75. PROJECT REALISATION / MANAGEMENT While the decision to realize the project was only provisional until that

- 76. PROJECT REALISATION / MANAGEMENT The acquisition is made in the project realisation phase by means of

- 77. PROJECT REALISATION / MANAGEMENT General risks that can occur during this phase include title issues which

- 78. PROJECT REALISATION / MANAGEMENT Questions of building functionality, flexibility of use, building efficiency and architectural design

- 79. PROJECT REALISATION / MANAGEMENT Alternatively, the developer may wish to hold the completed asset as investment

- 80. PROJECT DESIGN The objectives of the project design should be to balance the requirements of the

- 81. PROJECT DESIGN Detailed plans for land, structural and capital improvements have to be prepared and necessary

- 82. PROJECT DESIGN A significant risk is that the project design does not meet market needs and

- 83. PROCUREMENT One of the main procurement tasks of the real estate developer is to obtain a

- 84. CONSTRUCTION The construction phase starts with the granting of the building permit and the aim is

- 85. CONSTRUCTION The high portion of outside financing makes real estate developers very susceptible to variations in

- 86. CONSTRUCTION The availability of financing depends on credit market conditions, economic conditions and industry trends, which

- 87. CONSTRUCTION The marketing of the project via leasing or sale can begin at any time in

- 88. PROJECT MARKETING / DISPOSAL In real estate industry practice, distribution policy is often characterized by specific

- 89. PROJECT MARKETING / DISPOSAL The focus is therefore on developing and safeguarding a “unique selling proposition”,

- 90. PROJECT MARKETING / DISPOSAL As part of this task it is necessary to plan and budget

- 91. PROJECT MARKETING / DISPOSAL Lease negotiation and execution involves the screening of prospective tenants, and negotiating,

- 92. PROJECT MARKETING / DISPOSAL Significant risks of the leasing process are that not sufficient tenants are

- 93. PROJECT MARKETING / DISPOSAL There is a significant risk that a tenant can terminate a legally

- 94. PROJECT MARKETING / DISPOSAL The development process ends with the completion, handover for use and /

- 96. Скачать презентацию

DEFINITION OF

REAL ESTATE DEVELOPMENT

The views expressed in specialist literature regarding the

DEFINITION OF

REAL ESTATE DEVELOPMENT

The views expressed in specialist literature regarding the

DEFINITION OF

REAL ESTATE DEVELOPMENT

Real estate is a triangle of space, money

DEFINITION OF

REAL ESTATE DEVELOPMENT

Real estate is a triangle of space, money

DEFINITION OF

REAL ESTATE DEVELOPMENT

Development is an idea that comes to fruition

DEFINITION OF

REAL ESTATE DEVELOPMENT

Development is an idea that comes to fruition

THE PURPOSE OF

REAL ESTATE DEVELOPMENT

The purpose of real estate development is

THE PURPOSE OF

REAL ESTATE DEVELOPMENT

The purpose of real estate development is

THE PURPOSE OF

REAL ESTATE DEVELOPMENT

Generally, the priority goal of a developer

THE PURPOSE OF

REAL ESTATE DEVELOPMENT

Generally, the priority goal of a developer

THE PURPOSE OF

REAL ESTATE DEVELOPMENT

To meet its objectives, a developer has

THE PURPOSE OF

REAL ESTATE DEVELOPMENT

To meet its objectives, a developer has

THE PURPOSE OF

REAL ESTATE DEVELOPMENT

Development is a complex process which entails

THE PURPOSE OF

REAL ESTATE DEVELOPMENT

Development is a complex process which entails

THE PURPOSE OF

REAL ESTATE DEVELOPMENT

Real estate development is required to combine

THE PURPOSE OF

REAL ESTATE DEVELOPMENT

Real estate development is required to combine

THE PURPOSE OF

REAL ESTATE DEVELOPMENT

This conceptual understanding makes stronger reference to

THE PURPOSE OF

REAL ESTATE DEVELOPMENT

This conceptual understanding makes stronger reference to

RISKY NATURE OF

REAL ESTATE DEVELOPMENT

Real estate development is considered to be

RISKY NATURE OF

REAL ESTATE DEVELOPMENT

Real estate development is considered to be

Wiegelmann T. W. Risk Management in the Real Estate Development Industry:

Wiegelmann T. W. Risk Management in the Real Estate Development Industry:

REGULATORY PRESSURE

Regulatory and corporate governance provisions are increasingly requiring greater awareness

REGULATORY PRESSURE

Regulatory and corporate governance provisions are increasingly requiring greater awareness

CAPITAL MARKETS PRESSURE

The capital market now also requires adequate corporate risk

CAPITAL MARKETS PRESSURE

The capital market now also requires adequate corporate risk

STAKEHOLDERS' PRESSURE

Other stakeholders of real estate development organisations expect an effective

STAKEHOLDERS' PRESSURE

Other stakeholders of real estate development organisations expect an effective

REAL ESTATE AS

A UNIQUE ASSET CLASS

The most prominent characteristics of real

REAL ESTATE AS

A UNIQUE ASSET CLASS

The most prominent characteristics of real

REAL ESTATE AS

A UNIQUE ASSET CLASS

Land cannot be reproduced, any structures

REAL ESTATE AS

A UNIQUE ASSET CLASS

Land cannot be reproduced, any structures

REAL ESTATE AS

A UNIQUE ASSET CLASS

Real estate development is a highly

REAL ESTATE AS

A UNIQUE ASSET CLASS

Real estate development is a highly

REAL ESTATE AS

A UNIQUE ASSET CLASS

Finally, real estate is also characterised

REAL ESTATE AS

A UNIQUE ASSET CLASS

Finally, real estate is also characterised

SPECIFIC CHARACTERISTICS OF THE REAL ESTATE MARKET

The real estate market is

SPECIFIC CHARACTERISTICS OF THE REAL ESTATE MARKET

The real estate market is

SPECIFIC CHARACTERISTICS OF THE REAL ESTATE MARKET

The most prominent characteristic in

SPECIFIC CHARACTERISTICS OF THE REAL ESTATE MARKET

The most prominent characteristic in

SPECIFIC CHARACTERISTICS OF THE REAL ESTATE MARKET

Generally, the market participants only

SPECIFIC CHARACTERISTICS OF THE REAL ESTATE MARKET

Generally, the market participants only

SPECIFIC CHARACTERISTICS OF THE REAL ESTATE MARKET

The cyclical nature of real

SPECIFIC CHARACTERISTICS OF THE REAL ESTATE MARKET

The cyclical nature of real

TYPES OF

REAL ESTATE DEVELOPERS

There are many types of developers and an

TYPES OF

REAL ESTATE DEVELOPERS

There are many types of developers and an

TYPES OF

REAL ESTATE DEVELOPERS

Essentially, real estate developers operate as either trader

TYPES OF

REAL ESTATE DEVELOPERS

Essentially, real estate developers operate as either trader

TYPES OF

REAL ESTATE DEVELOPERS

Wiegelmann T. W. Risk Management in the Real

TYPES OF

REAL ESTATE DEVELOPERS

Wiegelmann T. W. Risk Management in the Real

TYPES OF

REAL ESTATE DEVELOPERS

Trader-developers typically assume the entire risk until completion

TYPES OF

REAL ESTATE DEVELOPERS

Trader-developers typically assume the entire risk until completion

TYPES OF

REAL ESTATE DEVELOPERS

Investor-developers carry out projects to establish a portfolio

TYPES OF

REAL ESTATE DEVELOPERS

Investor-developers carry out projects to establish a portfolio

TYPES OF

REAL ESTATE DEVELOPERS

Investor-developers and trader-developers share many characteristics. However, as

TYPES OF

REAL ESTATE DEVELOPERS

Investor-developers and trader-developers share many characteristics. However, as

TYPES OF

REAL ESTATE DEVELOPERS

Service developers render specific real estate development services

TYPES OF

REAL ESTATE DEVELOPERS

Service developers render specific real estate development services

(c) Mikhail Slobodian 2015

TYPES OF

REAL ESTATE DEVELOPERS

Financially, service developers commit themselves

(c) Mikhail Slobodian 2015

TYPES OF

REAL ESTATE DEVELOPERS

Financially, service developers commit themselves

TYPES OF

REAL ESTATE DEVELOPERS

With regards to the geographical focus of developer's

TYPES OF

REAL ESTATE DEVELOPERS

With regards to the geographical focus of developer's

TYPES OF

REAL ESTATE DEVELOPERS

In order to distinguish between different development projects,

TYPES OF

REAL ESTATE DEVELOPERS

In order to distinguish between different development projects,

TYPES OF

REAL ESTATE DEVELOPERS

Organisational size could potentially act as a further

TYPES OF

REAL ESTATE DEVELOPERS

Organisational size could potentially act as a further

Wiegelmann T. W. Risk Management in the Real Estate Development Industry:

Wiegelmann T. W. Risk Management in the Real Estate Development Industry:

STATE OF AFFAIRS IN

REAL ESTATE INDUSTRY

most real estate developers do not

STATE OF AFFAIRS IN

REAL ESTATE INDUSTRY

most real estate developers do not

OVERVIEW TO THE GENERIC REAL ESTATE DEVELOPMENT PROCESS

The real estate development

OVERVIEW TO THE GENERIC REAL ESTATE DEVELOPMENT PROCESS

The real estate development

GENERIC REAL ESTATE DEVELOPMENT PROCESS

Wiegelmann T. W. Risk Management in the

GENERIC REAL ESTATE DEVELOPMENT PROCESS

Wiegelmann T. W. Risk Management in the

GENERIC REAL ESTATE DEVELOPMENT PROJECT

(c) Mikhail Slobodian 2015

GENERIC REAL ESTATE DEVELOPMENT PROJECT

(c) Mikhail Slobodian 2015

PROJECT INITIATION

The initiation phase commences the development process.

A main expertise of

PROJECT INITIATION

The initiation phase commences the development process.

A main expertise of

PROJECT INITIATION

Accordingly, the starting situation for a development may either be:

an

PROJECT INITIATION

Accordingly, the starting situation for a development may either be:

an

CONCEIVABLE STARTING-POINTS FOR A REAL ESTATE DEVELOPMENT

Wiegelmann T. W. Risk Management

CONCEIVABLE STARTING-POINTS FOR A REAL ESTATE DEVELOPMENT

Wiegelmann T. W. Risk Management

PROJECT INITIATION

Accurate and pre-planned “timing” is a critical success factor in

PROJECT INITIATION

Accurate and pre-planned “timing” is a critical success factor in

PROJECT INITIATION

Based on a positive evaluation, the next major step is

PROJECT INITIATION

Based on a positive evaluation, the next major step is

PROJECT INITIATION

Option agreements or a purchase subject to conditions precedent are

PROJECT INITIATION

Option agreements or a purchase subject to conditions precedent are

PROJECT CONCEPTION

The conception phase starts with the project feasibility analysis and

PROJECT CONCEPTION

The conception phase starts with the project feasibility analysis and

PROJECT CONCEPTION

This is ultimately intended to answer the question whether and

PROJECT CONCEPTION

This is ultimately intended to answer the question whether and

PROJECT CONCEPTION

The term “feasibility analysis” has become accepted as a general

PROJECT CONCEPTION

The term “feasibility analysis” has become accepted as a general

STRUCTURE OF

FEASIBILITY ANALYSIS

Wiegelmann T. W. Risk Management in the Real Estate

STRUCTURE OF

FEASIBILITY ANALYSIS

Wiegelmann T. W. Risk Management in the Real Estate

MARKET ANALYSIS

The market analysis concerns itself with the supply and demand

MARKET ANALYSIS

The market analysis concerns itself with the supply and demand

LOCATION ANALYSIS

The analysis of the location should critically verify the findings

LOCATION ANALYSIS

The analysis of the location should critically verify the findings

PROJECT CONCEPT ANALYSIS

The building or usage concept for the use of

PROJECT CONCEPT ANALYSIS

The building or usage concept for the use of

COMPETITION ANALYSIS

The three above aspects of market, location and usage concept

COMPETITION ANALYSIS

The three above aspects of market, location and usage concept

RISK ANALYSIS

While risks are present at all stages of property development,

RISK ANALYSIS

While risks are present at all stages of property development,

RISK ANALYSIS

The project-specific manoeuvrability, i. e. the scope for structuring architectural,

RISK ANALYSIS

The project-specific manoeuvrability, i. e. the scope for structuring architectural,

RISK ANALYSIS

Furthermore, although the overall complexity of the project decreases during

RISK ANALYSIS

Furthermore, although the overall complexity of the project decreases during

THE DEVELOPER'S DECREASING ABILITY TO INFLUENCE TOTAL COST

OVER THE LIFE OF

THE DEVELOPER'S DECREASING ABILITY TO INFLUENCE TOTAL COST OVER THE LIFE OF

Wiegelmann T. W. Risk Management in the Real Estate Development Industry:

Wiegelmann T. W. Risk Management in the Real Estate Development Industry:

METHODS OF

RISK IDENTIFICATION

Wiegelmann T. W. Risk Management in the Real Estate

METHODS OF

RISK IDENTIFICATION

Wiegelmann T. W. Risk Management in the Real Estate

DEVELOPMENT RISK

Development risk is defined as the risk that the leasing

DEVELOPMENT RISK

Development risk is defined as the risk that the leasing

(c) Mikhail Slobodian 2015

DEVELOPMENT RISK

Forecasting and planning risk are also part

(c) Mikhail Slobodian 2015

DEVELOPMENT RISK

Forecasting and planning risk are also part

TIME RISK

In general, exceeding the planned project time line leads to

TIME RISK

In general, exceeding the planned project time line leads to

COST RISK

The cost risk is closely related to time risk, as

COST RISK

The cost risk is closely related to time risk, as

(c) Mikhail Slobodian 2015

FINANCIAL RISK

Typically, developers have to obtain appropriate financing

(c) Mikhail Slobodian 2015

FINANCIAL RISK

Typically, developers have to obtain appropriate financing

FINANCIAL RISK

Also, time and finance risk are driven by related factors,

FINANCIAL RISK

Also, time and finance risk are driven by related factors,

FINANCIAL RISK

It should also be considered that there are significant differences

FINANCIAL RISK

It should also be considered that there are significant differences

BUILDING SITE RISK

This is the risk that the selected site is

BUILDING SITE RISK

This is the risk that the selected site is

APPROVAL RISK

All development is subject to planning, and while developers in

APPROVAL RISK

All development is subject to planning, and while developers in

PROFITABILITY ANALYSIS

Combining the results of the five analyses above (market, location,

PROFITABILITY ANALYSIS

Combining the results of the five analyses above (market, location,

PROFITABILITY ANALYSIS

The profitability analysis should use clearly defined quantitative measures of

PROFITABILITY ANALYSIS

The profitability analysis should use clearly defined quantitative measures of

POTENTIAL VALUATION THROUGHOUT THE DEVELOPMENT PROCESS

Wiegelmann T. W. Risk Management in

POTENTIAL VALUATION THROUGHOUT THE DEVELOPMENT PROCESS

Wiegelmann T. W. Risk Management in

CONCLUDING

THE FEASIBILITY ANALYSIS

Having assembled the above data and analysed it based

CONCLUDING

THE FEASIBILITY ANALYSIS

Having assembled the above data and analysed it based

CONCLUDING

THE FEASIBILITY ANALYSIS

In the framework of the project initiation, it is

CONCLUDING

THE FEASIBILITY ANALYSIS

In the framework of the project initiation, it is

PROJECT

REALISATION / MANAGEMENT

The confirmation of the project's potential for success by

PROJECT

REALISATION / MANAGEMENT

The confirmation of the project's potential for success by

PROJECT

REALISATION / MANAGEMENT

While the decision to realize the project was only

PROJECT

REALISATION / MANAGEMENT

While the decision to realize the project was only

PROJECT

REALISATION / MANAGEMENT

The acquisition is made in the project realisation phase

PROJECT

REALISATION / MANAGEMENT

The acquisition is made in the project realisation phase

PROJECT

REALISATION / MANAGEMENT

General risks that can occur during this phase include

PROJECT

REALISATION / MANAGEMENT

General risks that can occur during this phase include

PROJECT

REALISATION / MANAGEMENT

Questions of building functionality, flexibility of use, building efficiency

PROJECT

REALISATION / MANAGEMENT

Questions of building functionality, flexibility of use, building efficiency

PROJECT

REALISATION / MANAGEMENT

Alternatively, the developer may wish to hold the completed

PROJECT

REALISATION / MANAGEMENT

Alternatively, the developer may wish to hold the completed

PROJECT DESIGN

The objectives of the project design should be to balance

PROJECT DESIGN

The objectives of the project design should be to balance

PROJECT DESIGN

Detailed plans for land, structural and capital improvements have to

PROJECT DESIGN

Detailed plans for land, structural and capital improvements have to

PROJECT DESIGN

A significant risk is that the project design does not

PROJECT DESIGN

A significant risk is that the project design does not

PROCUREMENT

One of the main procurement tasks of the real estate developer

PROCUREMENT

One of the main procurement tasks of the real estate developer

CONSTRUCTION

The construction phase starts with the granting of the building permit

CONSTRUCTION

The construction phase starts with the granting of the building permit

CONSTRUCTION

The high portion of outside financing makes real estate developers very

CONSTRUCTION

The high portion of outside financing makes real estate developers very

CONSTRUCTION

The availability of financing depends on credit market conditions, economic conditions

CONSTRUCTION

The availability of financing depends on credit market conditions, economic conditions

CONSTRUCTION

The marketing of the project via leasing or sale can begin

CONSTRUCTION

The marketing of the project via leasing or sale can begin

PROJECT

MARKETING / DISPOSAL

In real estate industry practice, distribution policy is often

PROJECT

MARKETING / DISPOSAL

In real estate industry practice, distribution policy is often

PROJECT

MARKETING / DISPOSAL

The focus is therefore on developing and safeguarding

a “unique

PROJECT

MARKETING / DISPOSAL

The focus is therefore on developing and safeguarding a “unique

PROJECT

MARKETING / DISPOSAL

As part of this task it is necessary to

PROJECT

MARKETING / DISPOSAL

As part of this task it is necessary to

PROJECT

MARKETING / DISPOSAL

Lease negotiation and execution involves the screening of prospective

PROJECT

MARKETING / DISPOSAL

Lease negotiation and execution involves the screening of prospective

PROJECT

MARKETING / DISPOSAL

Significant risks of the leasing process are that not

PROJECT

MARKETING / DISPOSAL

Significant risks of the leasing process are that not

PROJECT

MARKETING / DISPOSAL

There is a significant risk that a tenant can

PROJECT

MARKETING / DISPOSAL

There is a significant risk that a tenant can

PROJECT

MARKETING / DISPOSAL

The development process ends with the completion, handover for

PROJECT

MARKETING / DISPOSAL

The development process ends with the completion, handover for

Система Business Studio

Система Business Studio Ғылыми кадрларды даярлау және пайдалану жүйесі

Ғылыми кадрларды даярлау және пайдалану жүйесі Глава 5. Как мы доносим информацию о спринте до всех в компании

Глава 5. Как мы доносим информацию о спринте до всех в компании Тренинг для менеджеров по процессам в магазине компании adidas GROUP. Предотвращение внутреннего воровства

Тренинг для менеджеров по процессам в магазине компании adidas GROUP. Предотвращение внутреннего воровства Zahtjevi za implementaciju lean i agilnog opskrbnog lanca

Zahtjevi za implementaciju lean i agilnog opskrbnog lanca Motivation. Ideal working place

Motivation. Ideal working place Введение в сбалансированную систему показателей. Стратегическое управление. Управление по показателям

Введение в сбалансированную систему показателей. Стратегическое управление. Управление по показателям Планирование и прогнозирование деятельности предприятия. Методологические основы планирования

Планирование и прогнозирование деятельности предприятия. Методологические основы планирования Opportunities for alumni of the program From Idea to аction

Opportunities for alumni of the program From Idea to аction Системный подход к управлению проектами

Системный подход к управлению проектами Страхование экологических рисков

Страхование экологических рисков Организация как система управления

Организация как система управления Правила корпорации Ritz – Carlton Hotel Company

Правила корпорации Ritz – Carlton Hotel Company Музыкальный менеджмент. Понятие, цели и задачи. Лекция 1

Музыкальный менеджмент. Понятие, цели и задачи. Лекция 1 Массовый подбор

Массовый подбор Стратегический менеджмент

Стратегический менеджмент Бөлінген мұрағаттарды жүргізу технологиясы

Бөлінген мұрағаттарды жүргізу технологиясы Организационно-методические основы создания системы контроллинга в организации. (Тема 3.1)

Организационно-методические основы создания системы контроллинга в организации. (Тема 3.1) Управление IT-отделом

Управление IT-отделом Исследование вовлеченности сотрудников

Исследование вовлеченности сотрудников Sinif yönetiminin temel kavramlari ve özellikleri

Sinif yönetiminin temel kavramlari ve özellikleri Теоретический анализ концепций лидерства

Теоретический анализ концепций лидерства Методы стандартизации

Методы стандартизации Стандартизация и сертификация в туризме

Стандартизация и сертификация в туризме Организация обслуживания производства. Производственная инфраструктура предприятия

Организация обслуживания производства. Производственная инфраструктура предприятия Національні концепції управління якістю

Національні концепції управління якістю Оценка профессиональных рисков

Оценка профессиональных рисков Экспертные области в управлении проектами

Экспертные области в управлении проектами